Abstract

This paper presents the results of a survey-based study, which involved 120 small and medium sized enterprises in the East Midlands region of the UK, and aims to explore small and medium sized enterprises environmental practices, environmental capabilities and awareness of the regional support for green growth. Environmental capabilities of small and medium sized enterprises are found to be bound to energy efficiency projects, with very few small and medium sized enterprises having a strategic outlook toward developing these capabilities. The majority of small and medium sized enterprises did not access governmental grants to improve energy efficiency, and those who did accessed governmental rather than NGO or private sources. Around a third of small and medium sized enterprises did not invest in any form of Environmental Management System or Environmental Management Accreditation over the last two years. Environmental capabilities, which are considered to have a direct positive impact on cost reduction, are found to be attracting the highest demand from small and medium sized enterprises. The study offers a typology of small and medium sized enterprises environmental capabilities providing a valuable conceptual development in understanding the links between various environmental capabilities and their significance for the strategic success of an enterprise.

Keywords

Introduction

The low-carbon economy (LCE), defined as the activities that generate products or services which themselves deliver low carbon outputs (Department for Business Innovation and Skills (DBIS), 2015), is seen as one of the significant developments in the current policy and socio-economic landscape worldwide (Department for Energy and Climate Change (DECC), 2013; Department for Environment, Food and Rural Affairs (DEFRA), 2013; DEFRA, 2014; European Commission, 2010a, 2010b, 2014, 2016; United Nations Environment Programme (UNEP), 2011; World Bank Group, 2016). Some scholars argue that the fundamental aims of a LCE are to achieve high energy efficiency, to use clean and renewable energy, and to pursue green GDP via technological innovation, while maintaining the same levels of energy security, electricity supply and economic growth (Muro et al., 2011). Muro et al. (2011) contend that such a wide-ranging transformation will involve a comprehensive policy response from regions that will require radical changes in behaviour and consumption patterns. The study presented in this paper is empirical research into the environmental capabilities (Baranova and Meadows, 2017) of small and medium sized enterprises (SMEs) in the East Midlands region of England in support of a three year ERDF (European Regional Development Fund) funded project to support SME business growth through opportunities presented by the emerging low carbon economy.

Review of the literature

Much of the research and business literature addressing the shift towards a LCE is focused on large companies and large scale change initiatives in cities, regions and whole countries (Rifkin, 2011; Uyarra et al., 2016; Whiteman et al., 2011). Much less is published on the practices, challenges and benefits for small and medium size businesses (Altham, 2007; Confederation of British Industries (CBI), 2015; Gadenne et al., 2009; Hillary, 2004). This is surprising given that SMEs represent the dominant form of business organisation globally. In Europe, there were 21.2 million SMEs in the non-financial business sector in 2013, accounting for 99% of all enterprises in this sector, 67% of total employment and 58% of total value added generated (European Commission, 2014). 1

SMEs and green growth

In the UK, SMEs account for more than 90% of the low carbon sector (Carbon Trust, 2013), with 11,550 businesses directly engaged in the LCE across the UK in 2013. Nationally employment in the low carbon sector grew 12 per cent from 2010 to 2013, with a total of 460,600 people working in the LCE supply chains. This represents approximately 1.5% of all UK jobs (Department for Business Innovation and Skills, 2015). SMEs are, therefore, significant contributors to the LCE by virtue of their prevalence and importance to local communities, through the employees they engage, their business practices and SMEs role in supply chains (Lee and Klassen, 2008; Powell, 2000; Williamson et al., 2006).

Cost saving through more efficient use of materials and energy efficiency are seen as compelling enablers for SMEs to engage in sustainability initiatives (Klewitz et al., 2012; Triguero et al., 2013). However, SMEs are reported to be lagging behind larger companies in adopting sustainability related improvements. According to a survey of over 1000 SMEs by Lloyds Banking Group (Lloyds Commercial Banking, 2013), a quarter of SMEs cite sustainable practices as one of their top priorities in the coming years. However, a study by the Association of Certified Chartered Accountants (ACCA, 2012) showed that only 29% of SMEs had introduced any measures to save energy or raw materials compared with 46% of large enterprises and only 4% had comprehensive energy efficiency systems in place compared with 19% of large enterprises. Whilst SMEs represent a significant share of the low carbon economy and are key players in the sustainability transition, they also represent a potentially significant level of inertia given the challenges they face in prioritising de-carbonisation efforts.

Scholarly literature consistently reports that lack of resources such as time, money, technical skills and organisational capacity hold back SME ‘eco-innovation’ (European Commission, 2010b; Perry and Towers, 2009; Triguero et al., 2013). Gibb (2000) and Jenkins (2004) argue that attempts to engage SMEs in the low carbon agenda or corporate sustainability have failed due to a lack of understanding of smaller business needs and weak policy setting and implementation. On the other hand, regulators such as the UK Environment Agency complain that SMEs are unresponsive to environmental regulations and concede that the sheer number of SMEs means that compliance inspection rates are very low (Environmental Agency, 2009). The regulator observes that as SMEs are exempt from many of the mandatory legal requirements that drive larger businesses, they are often loathed to go beyond regulatory compliance to make substantial investment in efficiency measures, for fear that their bottom line and competitiveness will be affected.

Currently, the research about SMEs’ sustainability practices can be broadly grouped into four main streams: eco-innovation, environmental practices, leverage of sustainability practices to gain competitive advantage and positioning of SMEs within green supply chains (GSC). Research into all four streams is growing and providing valuable empirical insights into the organisational practices that support sustainability and low carbon orientation of SMEs. There is growing evidence that SMEs, who go beyond minimum responses, also perform better financially or are more successful in product or process innovation (Figge and Hahn, 2012; Torugsa et al., 2012; Uhlaner et al., 2012).

Whilst cost saving through more efficient use of materials or energy efficiency are seen as compelling enablers for SMEs (Klewitz et al., 2012; Triguero et al., 2013), there is also an increasing awareness that a competitive advantage can be gained from the enhanced reputation developed through demonstrating ‘green credentials’ to ethically driven customers. In reality, as Bansal and Roth (2000) show, low carbon or environmental business practices are likely to be driven by a combination of influences that include regulations, business case, stakeholder pressure and the ethical preferences of the business owner. Whilst the values of the business owner and commitment to their locality are influential, a number of studies demonstrate that the main pressure for SMEs to adopt ‘environmental measures’, improve energy or resource efficiency comes from the supply chain in which they operate (Perry and Towers, 2009; Rutherford et al., 2000; Seuring and Muller, 2008).

‘Lack of relevance’ is seen as one of the barrier to SMEs engagement with low carbon agenda (Van Hemel and Cramer, 2002). It is argued that the specifics of the SMEs, such as management and leadership, work and organisation practices, financial pressures and aspirations towards sustainability, need to be taken into account when designing the support mechanisms at national and regional levels. Policy makers are urged to recognise the various ‘subcultures’ in order to tailor initiatives that will support SMEs shift to lower carbon alternatives.

Environmental capability

Considerable research has been undertaken to explore the role of firm-specific capabilities in the pursuit of competitive advantage. The vast majority of existing research considers internal sources such as skills and routines (Nelson and Winter, 1982) as the main sources for capability building in organisations. External sources have also been explored to an extent, including consideration of the role of formal and informal relationships with other firms (Gulati et al., 2000); the degree of network density that affects the capability building of the firm (Ahuja, 2000; Burt, 1992; Coleman, 1990; McEvily and Zaheer, 1999); and the effects of different types of network ties on capability acquisition by individual members and through interactions with each other (Mahmood et al., 2011; McEvily and Marcus, 2005).

A firm’s environmental capabilities are those capabilities that allow a firm to reduce its ecological footprint (Baranova and Meadows, 2017). As a part of a firm’s strategic capabilities, they are significant for the success of the firm’s environmental strategies (Aragon-Correa and Sharma, 2003; Buysse and Verbeke, 2003; Klassen and Whybark, 1999; Rugman and Verbeke, 1998). These capabilities include, for instance, environmental management skills and routines, product/service design with a focus on sustainability, waste management, resource efficiency skills and practices and others that focus on the reduction of the ecological footprint of the firm. It is noted that the concept of ecological footprint (Hart, 1995) is defined sufficiently broadly to include the impact of the firm’s activities in supporting a reduction in the ecological footprint of the firm’s key stakeholders such as its suppliers and customers.

The existing literature on capability building is dominated by studies, which emphasise capabilities that are internally generated, with heterogeneity primarily arising from imperfections in factor markets (Barney, 1986), distinct organisational skills and routines (Nelson and Winter, 1982), causal ambiguity and uncertain imitability (Dierickx and Cool, 1989) and deliberate investment in learning and making improvements (Zollo and Winter, 2002). In this study, it is argued that, while an internal focus on capability-building is critical, it has to be inclusive of the external perspective on capability building (Gulati et al., 2000). This includes capability development through becoming a part of the GSC, as well as broader networks, which support decarbonisation efforts and broader sustainability initiatives.

In SMEs, various environmental capabilities have been found to positively impact proactive environmental strategies or ‘pattern of environmental practices that goes beyond compliance with environmental regulations’ (Aragon-Correa and Sharma, 2003: 71). Environmental management and associated training are seen to be important pre-requisites to successful environmental strategies of SMEs (Cassells and Lewis, 2017; Hillary, 2004). Organisational capabilities of SMEs, in particular: team learning, stakeholder management and shared vison, were found of significance to successful implementing environmental strategies (Tibon, 2015). The influence of firm’s stakeholder and positive effects of proactive stakeholder management practices on environmental strategies in SME context have been considered in studies by Williamson et al. (2006) and Darnall et al. (2010). A link between eco-innovation and proactive environmental strategies of SMEs has also attracted scholarly interests in recent years (Marin et al., 2015; Triguero et al., 2016). A positive relationship between firm’s marketing and R&D competences and environmental strategy, which contributes to the superior financial performance, is recently reported in the study of UK SMEs operating in technology sector (Ko and Liu, 2017).

Support for development of SMEs’ environmental capabilities

SMEs that focus on the production and marketing of low carbon and environmental goods and services (LCEGS) designed to reduce carbon and other greenhouse gas (GHG) emissions are found across the length and breadth of the UK. Low carbon hubs have emerged in London, Oxford, Cambridge, Leeds and Southampton. Relative to their population, Derbyshire and Nottinghamshire also have a high proportion of low carbon SMEs. There is an increasing variety of initiatives that support the transition to a LCE in Derby, Derbyshire, Nottingham Nottinghamshire (D2N2) region from central and regional governments; with UK and European funding creating a climate of growth for low carbon SMEs (D2N2, 2014; D2N2 Growth Hub, 2015).

However, Uyarra et al. (2016) argue that a lack of coherence and consistency in UK low-carbon innovation policy is creating uncertainty and hampering private sector investment. They also contend that the loss of anchor institutions and significantly depleted regional capacity (that lacks a clear mandate from government) has resulted in a fragmented intermediary support landscape. Within this context in the UK, Local Enterprise Partnerships (LEPs) now provide the key structural support for low carbon business development across the regions (Britton and Woodman, 2014).

D2N2 LEP has an excellent reputation for supporting low carbon business across the region. In a review of all 36 UK LEPs, Britton and Woodman (2014) found that D2N2 was one of 11 areas in which low-carbon growth was well embedded in strategic planning, with the broader concept of ‘greening growth’ seen as a cross-cutting principle across the whole local economy. These findings were amplified by a more recent study of the sustainability landscape in the West Midlands (SWM, 2016), where the D2N2 region was ranked fourth most committed to climate change, adaptation, mitigation and the LCE overall; and third most committed to the LCE. The D2N2 LEP was commended for its attention to mapping opportunities to grow low carbon business across the region – most notably in key sectors, such as power generation, low carbon buildings construction, carbon capture and storage, environmental services and low carbon vehicles and fuels. The SWM study also noted that in some regions, a lack of awareness of local factors that currently hold back growth of the LCEGS sector may be a barrier to future interventions being targeted appropriately.

Whilst the picture for the D2N2 region is positive, there should be no complacency. DECC figures show that after seven years of declining gas and electric consumption for non-domestic consumers, similar to other regions across the UK, the East Midlands saw a small rise in energy consumption in 2014 (DECC, 2016). These figures do not differentiate between larger and smaller businesses – although research suggests that smaller businesses are less inclined to undertake substantial energy efficiency measures than larger ones (ACCA, 2012).

As Uyarra et al. (2016) note, the mix of policy incentives and regional support initiatives for SMEs can seem rather opaque and inaccessible to small business leaders. They are not always well matched with individual business or local market needs (2016: 246). However, there is a growing body of both theoretical and empirical research that indicates the significance, nature and benefits of business networks, clusters and collective systems that work towards common purposes such as environmental sustainability or social value (Geels and Kemp, 2007; Planko et al., 2016; Roscoe et al., 2016; Ryan et al., 2012; Steward, 2012). Such networks can be led from a variety of sources; regional agencies, universities, local government, business networks or individual businesses. In the D2N2 region, low carbon sector is one of the eight ‘strategic-priority’ sectors for growth identified in the D2N2 Strategic Economic Plan (D2N2 LEP, 2014). Planko et al. (2016) identify 22 activities that contribute to building local business networks or collective systems that are collected under four headings; technology development, market creation, socio-cultural changes and cluster coordination. Such a range of activity clearly requires a degree of orchestration, clarity of purpose, platform building and commitment over time (Ryan et al., 2012): we return to these aspects in the discussion section of this paper. According to the literature reviewed by Planko et al. (2016) one clear benefit for individual business managers is that these networks (or collective systems in their terms) create supportive environments in which innovations can flourish. What is less clear from the emerging literature is how such networks connect the contemporary and emerging needs of local SMEs with the interests of the local, national and international markets.

Research approach and method

The current study was part of the preliminary data gathering in support of a collaborative bid with Derby City and County Councils for ERDF for a region-wide programme to help SMEs become more energy efficient and to support business growth through exploring opportunities presented by the transition to a low carbon economy. The initial data gathering set out to explore local SMEs energy efficiency initiatives, their environmental capabilities and awareness of regional support for green growth and carbon reduction. As part of the study, a survey was launched at the beginning of September 2015 using Survey Monkey functionality. The survey was opened for four weeks.

A reminder message was sent out one week before the survey closed. More than 3200 emails were sent to named contacts via the university. The survey was also promoted via the social media channels of Derby Business School, Derby City and Derbyshire County Council business services, the regional Chamber of Commerce and several cleantech and green business networks linked to the D2N2 LEP Low Carbon Hub. Collectively, these regional environmental stakeholders have access to a network with more than 5000 business contacts or subscribers. Although the degree of overlap or cross-posting that this entailed was not analysed (and the exact sample size uncertain), cross posting was deemed likely to be more beneficial than detrimental (as businesses may be more likely to complete the survey if they realised it was being promoted by more than one reputable local organisation). We estimate the survey was sent to between 5000 and 8000 businesses in the D2N2 LEP region. One hundred and twenty questionnaires were returned; giving a response rate of between 1.5 and 2%. This level of response is not uncommon for web-based surveys of this nature (Archer, 2008).

The survey was designed to gather responses from SMEs around the following themes:

Energy savings and energy efficiency initiatives; Environmental management systems (EMS) and accreditation (EMA); Availability of support towards energy efficiency and sustainability; Barriers in accessing support and adaptation of ‘green’ initiatives; Requirements for capability building to succeed in the LCE.

The above research process generated over 250 survey-monkey entries of the response data. Survey Monkey functionality and Excel functionality was deployed to analyse the data. The survey data were analysed per question and in relation to the type of the SMEs surveyed, for instance per sector/industry where SME operates in and/or per SME size.

Analysis and findings

The sample characteristics of the 120 SMEs that responded to the survey are as follows: 51% of the SMEs in the sample were micro businesses employing less than 10 employees, 36% were small firms (10–50 employees), 9% were medium sized enterprises with 4 (of the 120) respondents representing large enterprises. The largest proportion of the firms surveyed (25%) operate in the high-tech manufacturing and engineering sector. Other industries had the following representation: 20% of the firms work in construction and housing; 13% in IT and creative industries; 12% in retail; 10 % in hospitality and tourism; 7% in health and wellbeing and management services and consultancy; with transport and logistics, food and drink and low carbon goods and services each reflecting 6% of the respondents to the survey. The analysis of the survey data provides insights into the following areas.

Energy savings and energy efficiency projects

The vast majority of SMEs surveyed, 78%, said they had already invested in some form of energy efficiency projects over the previous two years; although the majority of investments were described as small (25%) with only 14% of SMEs making ‘substantial’ investment in energy (or resources) efficiencies. 36% of the firms surveyed stated that there was ‘some’ potential for further energy cost savings in the business, 23% of SMEs indicated that such potential is ‘significant’, with 8% considering the potential as ‘substantial’.

Around 30% of the SMEs surveyed had not invested at all in any form of EMS or accreditation (EMA) over the previous two years; with some 26% of the SMEs making ‘some’ investment; and 20% defining their investment in these areas as ‘small’.

Support towards energy efficiency and sustainability

Given D2N2 LEP’s excellent reputation for supporting the transition to LCE in the region (DBIS, 2015), it was surprising that the vast majority of our respondents, 93 out of 120 SMEs surveyed, were not aware of any support available to SMEs to improve their energy efficiency and to reduce their impact on the environment. 19% of our respondents confirmed that they were aware of governmental support, with only six firms saying they were aware of non-governmental sources for such support.

Eighty-two percent of the SMEs’ that responded to the survey had not been able to access any support for energy efficiency. Of those firms that had accessed support, the vast majority (18/21) had accessed government schemes (with only three firms accessing non-government support).

Barriers to reducing environmental impact

The major barriers to reducing the firm’s impact on the natural environment were identified as: lack of funding and finance; the initial costs of efficiency measures being too high; lack of clear advice from the government and other bodies; lack of specialist expertise/capacity to undertake the measures and finally the perception that return on investment in energy efficiency and other measures were not strong enough an incentive.

The data confirms that for many SMEs, efforts to reduce carbon emissions seem expensive in terms of time, staff allocation and the necessary accreditations. Environmental/carbon accreditations are often seen as time consuming to obtain, maintain and renew. It appears that many SMEs and micro businesses still consider low carbon initiatives and accreditations as ‘nice to have, but not critical’ to business success or survival.

The data also suggests that many SMEs still require support in developing the ‘business case’ for low-carbon interventions, including help with investment options, return on investment and value added options. Assistance in attracting external funding as well as project management expertise could, therefore, have a significant impact on SMEs’ confidence towards low carbon, eco-innovation and energy-efficiency projects.

Environmental capability: Developmental areas

A firm’s environmental capabilities are capabilities that allow a firm to reduce its ecological footprint (Baranova and Meadows, 2017). As a part of a firm’s strategic capabilities, they are significant for the success of the firm’s environmental strategies (Aragon-Correa and Sharma, 2003; Buysse and Verbeke, 2003). These capabilities can include, for instance, environmental management skills and routines, product/service design with a focus on sustainability, waste management, resource efficiency skills and other practices that focus on the reduction of the ecological footprint of the firm. As part of the survey, the SMEs were asked to indicate the type of capability they require to take advantage of the opportunities presented by the transition to a low carbon economy.

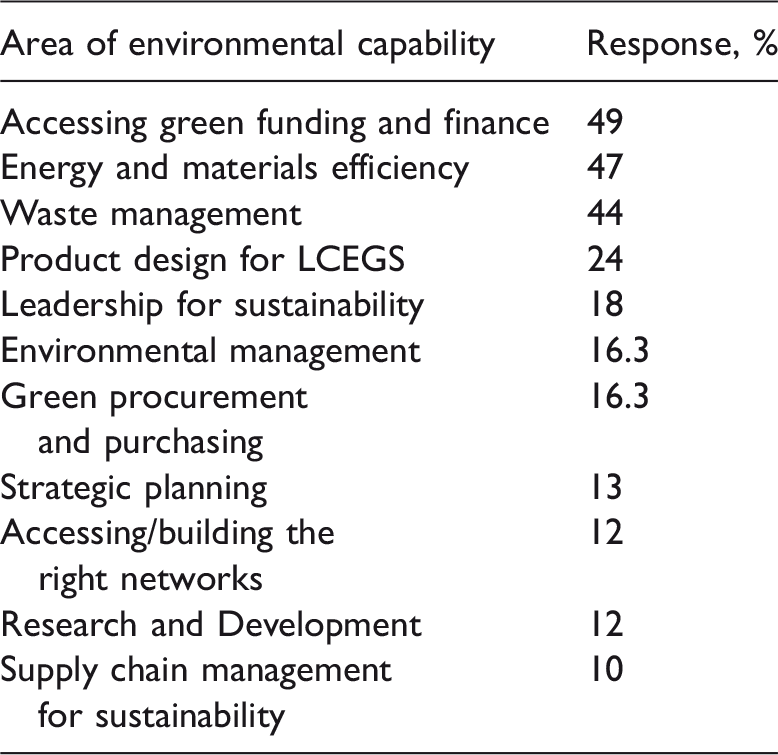

SMEs’ demand for environmental capabilities.

SMEs: small and medium sized enterprises; LCEGS: low carbon and environmental goods and services.

Source: D2EE ERDF project survey, September 2015.

The capability associated with ‘accessing funding and finance’ attracted the highest interest (49%), closely followed by ‘energy and materials efficiency’ (47%) and ‘waste management’ (44%). ‘Design for low carbon product and services’ category attracted substantial attention (24%); ‘leadership for sustainability’ (18%) with ‘environmental management’ and procurement and purchasing both attracting the same interest with 16%, with ‘strategic planning’ (13%) and ‘accessing and building the right networks’ (12%) not far behind.

When considering these responses by sector, the ‘accessing funding and finance’ category attracted attention from the majority of sectors attracting 29% of responses. SMEs from construction and housing, and retail sectors had the highest representation in this category, indicating that access to funding and finance was the most important category of capabilities to support their sustainability initiatives. The second largest capability category, attracting 27% of the responses across the sectors studied, was ‘energy and materials efficiency’. Half of all SMEs surveyed operating in high-tech manufacture and engineering in the region indicated that such capability was critical to them; at the same time only 18% of SMEs from the same sector stated that the ‘access to finance’ was important to them. Forty-two percent of SMEs operating in IT and Creative industries and 34% of SMEs in construction and housing indicated that ‘energy and materials efficiency’ was the key environmental capability for them to develop.

‘Waste management’ was another category of environmental capability that attracted significant attention from the regional SMEs surveyed, which is consistent with earlier studies (Ilomaki and Melanen, 2001). Twenty-eight percent of SME responses indicated that skills and competences in waste management were significant to their sustainability efforts. Seventy-five percent of SMEs operating in food and drink, 64% in retail and 60% in low carbon goods and services sectors indicated that this capability was of interest for development in these sectorial contexts.

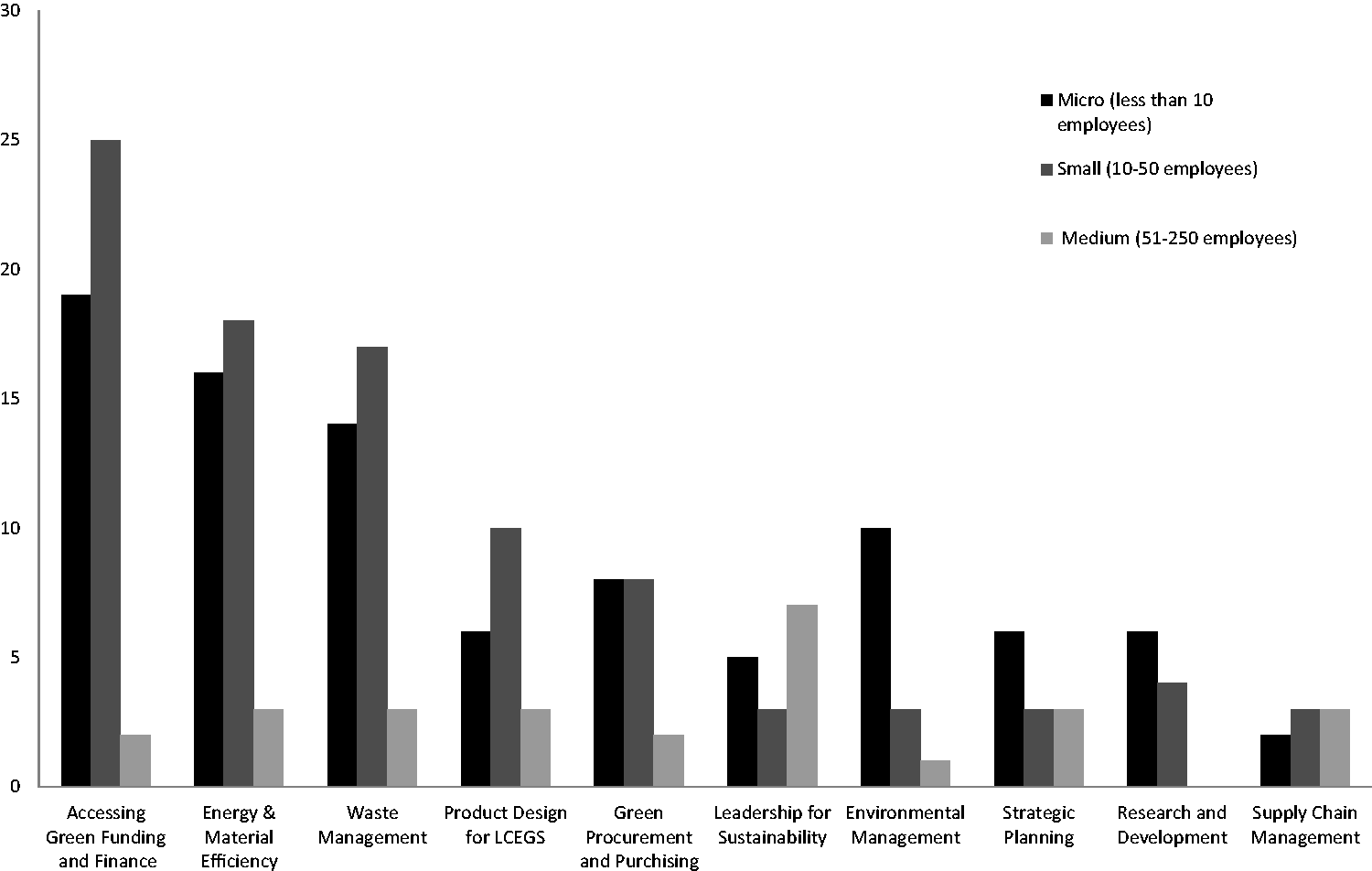

Another interesting aspect of the survey data analysis considered the demand for environmental capabilities in relation to the size of the regional SMEs. This relationship has been explored earlier in studies of firm’s size and attitudes towards Corporate Social Responsibility (Lepoutre and Heene, 2006). Figure 1 illustrates the analysis of the demand for various environmental capabilities depending on firm’s size.

Our analysis indicated that for micro (less than 10 employees) and small (10–50 employees) enterprises, the capabilities that attracted the most attention are: ‘access to funding and finance’ (45% of micro and small enterprise responses), ‘energy and material efficiency’ (37%) and ‘waste management’ (35%). But for the medium sized enterprises (51–250 employees), the picture is different. Seventy-three percent of medium sized enterprises that took part in the survey considered ‘leadership of sustainability’ as an important area for development. The following capabilities: ‘design for new low carbon products and services’, ‘energy and materials efficiency’, ‘strategic planning’ and ‘waste management’ attracted the same number of responses, at 36%, of medium-sized enterprises that took part in the survey. This picture is indicative of the shifting priorities as businesses grow. The priorities of micro and small businesses lie in achieving short term priorities, often measured in financial terms, i.e. positive cash flow, payback on investments, reinvestments in growths. However, as businesses become more established, as in case of medium enterprises, these priorities shift towards longer term horizons. Thus, capabilities in leadership, strategic planning and design for products and services attract more attention as the business confidence grows.

Discussion

As a result of the analysis of the survey data and the literature reviewed about the role of SMEs in the transition to a LCE, the following areas are of interest in relation to the development of SMEs’ environmental capabilities.

Access to funding and finance

Our data reveal that access to finance and funding is seen by the SMEs as a major area where they require capability development. This is not surprising, as the lack of finance and the ability to attract funds from external sources is seen as one of the major limiting factors preventing SMEs to engage in sustainability initiatives (Lewis and Cassells, 2010; Perry and Towers, 2009; Torugsa et al., 2012). The ability to attract external funds is high on the agenda of the regional SMEs, which indicates that SMEs often struggle to develop a business case for sustainability (Moor and Manring, 2009). Thus, developing a strategic rationale of suitability initiatives, which considers not only cost cutting as a main short-term gain of the green investment, but longer-term benefits contributing to sustainable business growth and development are important prerequisites in SMEs’ pursuit of funding and finance to support sustainability and energy efficiency efforts.

Greening of regional supply chains

Many SMEs are part of vast supply chains and networks at regional, national and supranational levels. Development of sustainable sourcing approaches and effective carbon management across supply chains is vital. Recent studies confirm (Foerstl et al., 2010; Gimenez and Sierra, 2013; Lee and Klassen, 2008) that being a part of a supply chain that encourages sustainable sourcing and conduct has a positive impact on sustainability orientation of the supply chain participants. Lee and Klassen (2008) found that, in a case study of SMEs, a combination of evaluation and collaboration provides synergies that help suppliers building their organisational capabilities in order to enable them to improve their environmental performance and that of their customers (i.e. the buying firms). In a similar vein, Reuter et al. (2010) confirmed that a combination of assessment and collaboration strategies generates the greatest effect for the greening of supply chains.

Eco-innovation

In the D2N2 region, the LEP and Chamber of Commerce are becoming increasingly attuned to the sustainability agenda, which forms a major part of their strategies for the region. Support for ‘green’ innovation is heavily featured on the agenda of these key regional players, as well as at the national level through organisations like the Low Carbon Innovation Co-ordination Group (LCICG) and the network of Energy Research Partnerships (ERPs). Capability building for low carbon innovation is an emergent area of business activity, where both public and private sectors are supporting investment in low carbon technologies, such as bioenergy, carbon capture and storage, electricity networks, hydrogen for transport, offshore wind, electricity storage and marine energy (LCICG, 2014).

For SMEs to succeed in this arena, they need to be supported with finance and leadership for eco-innovation, which require a long term perspective, tolerance of failure and consistency. Furthermore, companies need to keep abreast of developments in technology, design, and infrastructure, which are creating the space for new solutions to emerge. They need to engage proactively in creating platforms for collaboration and open innovation with suppliers, customers and other partners. The dynamic nature of the sector requires more open collaboration and sharing of technical knowledge which, in turn, depends upon a good understanding of intellectual property issues – expertise not always held by smaller businesses. Such a collaborative activity inevitably requires leadership ambition, strategic foresight and capability building to encourage innovation, market development and growth through collaborative strategies.

Sustainable business models

In the context of transition to a low carbon economy SMEs also need to be open to the creation and redesign of existing business models, which encompass sustainability. This proposition requires a deep understanding of value chain dynamics as well as customer needs and customer behaviour.

Many big companies have started to use technology in the development of sustainable business models: for instance, BT, a telecommunications services company, is working with suppliers to develop products and services designed for ‘circularity’, while also aligning its revenue model with a ‘net positive’ enablement of carbon reduction (Carbon Trust, 2013). A nationwide retailer, Kingfisher, is developing closed-loop hardware products, as well as service-focused propositions for customers undertaking big ‘do-it-yourself' (DIY) projects (Kingfisher, 2016). These examples show that, if done correctly, more value can be delivered while cutting waste and material resource requirements.

The trend of combining product-service propositions to deliver more sustainable solutions represent a strategic shift for SMEs as they develop their competences to match demands for sustainable product and service solutions. As these models develop they will create opportunities for a number of ‘enabling’ industries where SMEs have a significant presence. These include ICT (telematics, tracking and ‘smart’ infrastructure), logistics (for reverse logistics of used products, collection/distribution of asset-sharing models), and financial services (insuring and financing leased assets) (Smith-Gillespie, 2013). Sustainable business models present opportunities for new solutions in organisational design and infrastructure. Indeed, SMEs could take a lead in developing such bespoke solutions and in crafting new and unexplored ‘niches’ for competitive success by taking advantage of their flexibility and close proximity to the customer base.

Leadership and leadership development for sustainable business

There is a growing body of literature exploring the nature and role of sustainability leadership (Boiral et al., 2008; Egri and Herman, 2000; Metcalf and Benn, 2013; Wolfgramm et al., 2015). In the context of SMEs, leadership agendas are often focused around familiar business priorities, with sustainability leadership often seen as secondary; although in our view these are increasingly becoming interchangeable terms, which are strongly associated with the success of sustainable business strategies.

Our data confirm the criticality of the senior management commitment and a hands-on approach to working with employees across the organisation and beyond to provide support and stewardship for the success of sustainability initiatives. Support and active engagement of staff in sustainability initiatives are critical to ensuring the success of any company’s green growth strategy. Sustainability needs to be positioned at the heart of the organisational strategy and viewed as critical to behavioural change at individual and organisational level. Encouraging employees to ‘do one more task on the list’ in addition to their contractual roles and responsibilities is a real challenge for SMEs as they struggle for resources. Their staff often work to full capacity with little time for ‘other’ tasks and duties, such as becoming environmental champions (Taylor et al., 2012) in initiating and supporting green practices.

Greater university-business co-operation

As Uyarra et al. (2016) have shown, business growth is influenced by SMEs’ ability to connect with universities, technology centres, government resources and private funding. However, our research has shown that even in a highly regarded LEP, such as D2N2, the exchange of knowledge and information between SMEs and the local support agencies about funding opportunities, technical support and business-to-business insights into carbon reduction and sustainability practices is perceived as weak. This is where universities might bolster their role to strengthen leadership capacity for sustainability at a regional level. HEFCE’s Sustainable Development Framework (HEFCE, 2014) outlines the important role that universities can play in supporting sustainable development principles. Part of this role is to enable researchers and stakeholders in business, policy and civil society to develop and share new methodologies, data, conceptual frameworks, skills and practices to support acceleration of a LCE. For SMEs, such an orientation presents opportunities to develop collaborative projects with universities in order to support eco-innovation and business growth, as well as to create partnerships to encourage and advance debates about the role of SMEs and their contribution towards a low carbon economy.

Next steps

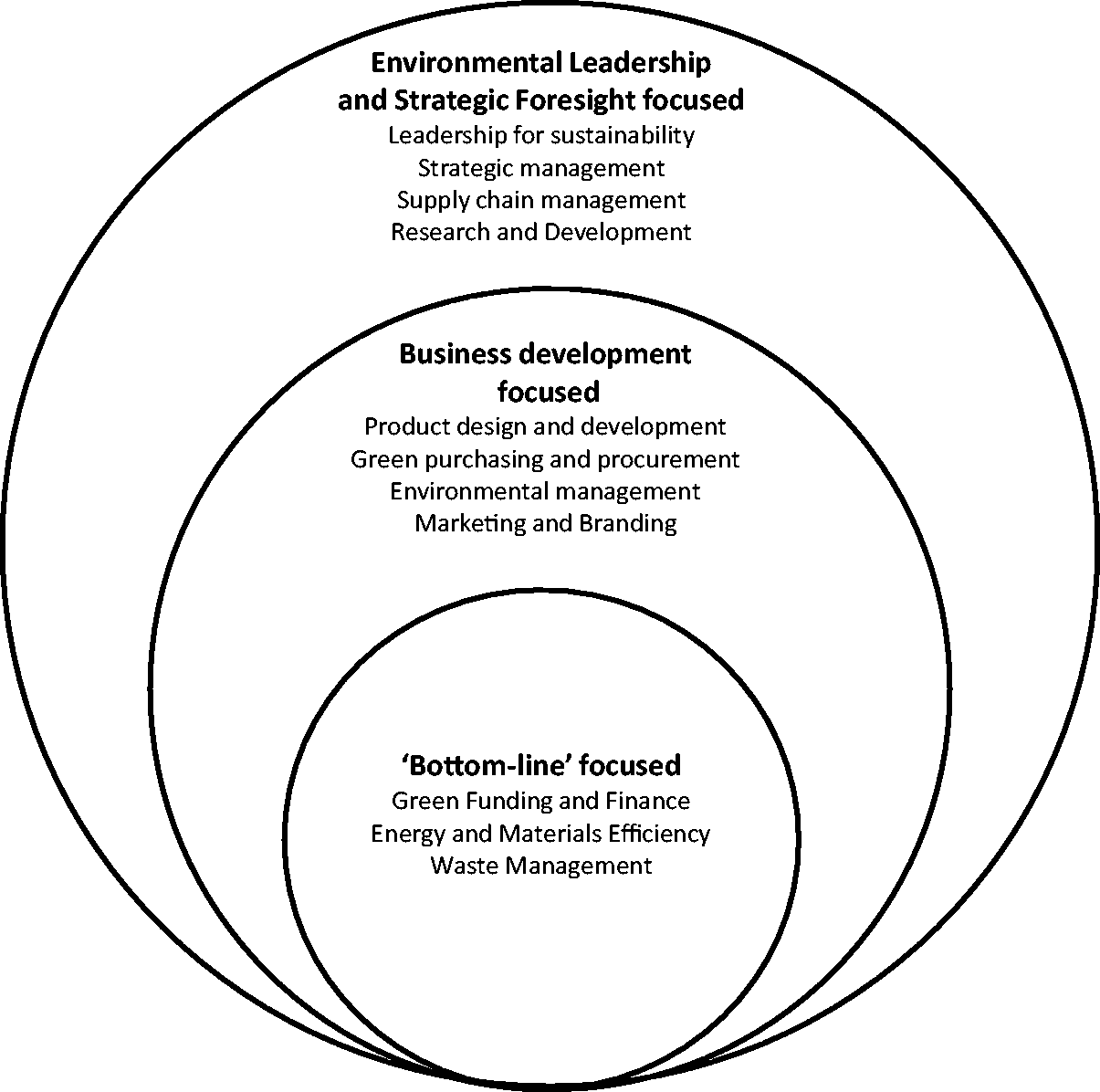

The ERDF Low Carbon Business Network project is well into its first year of running. The study presented in the paper provides useful insights into the environmental practices of the regional SMEs as well as their needs in relation to environmental capabilities at the beginning of the project. As the project work with SMEs continues, we are beginning to discern the following pattern (Figure 2) in how SMEs recognise the need for environmental capabilities that support the firm’s ability to take advantage of opportunities presented by the transition to a low carbon economy.

Demand for development of environmental capabilities by SME size. Typology of environmental capabilities of SMEs.

The majority of SMEs recognise the need for what we refer to as ‘bottom-line’ focused environmental capabilities. These capabilities are perceived to have positive impact on the financial bottom line of an SME either though opportunities to cut costs or attracted additional financial resources to the business. It is viewed that these capabilities will be able to generate the return on investment short term and may not require sustained efforts either in attaining or developing these capabilities ‘in house’. The examples of these capabilities, which are often requested by SMEs we work with in the first instance, include: access to green finding and finance, energy and materials efficiency (opportunities to reduce costs through energy usage and materials usage) and waste management. These areas seem to attract the most attention, as they are perceived to have the biggest benefit to an enterprise, where resources are scarce (Chen and Hambrick, 1995; Dean et al., 1998; Welsh and White, 1981).

The second category of environmental capabilities is focused on business development. These are often associated with opportunities for consolidation and a gradual expansion of an enterprise. They require either the introduction of new ways of working, often accompanied by new process and systems, or changes from the established practices in the following areas: purchasing and procurement, product design, environmental management, intellectual property management, marketing and branding. A short-to-medium term perspective is necessary in relation to acquisition and/or development of these capabilities in order to gain positive returns. They require sustained efforts in maintaining the expertise in these areas, which is often not readily available in micro and small sized enterprises.

The third category of environmental capability is linked to SMEs demonstrating aptitudes for environmental leadership and strategic foresight. These SMEs actively engage in sustainability practices. C are for the natural environment forms an important part of the firm’s business strategy. They often have the necessary environmental management accreditations, and brand and reputation associated with sustainability. They readily engage with various networks and demonstrate the confidence in developing relationships with various stakeholders, including much larger organisations. And where they exist as part of a supply chain, they generally consider themselves as proactive partners. Thus, their environmental practices often span outside the organisational boundaries and involve capability building with external partners (Gulati et al., 2000). To achieve success in developing these capabilities, a long-term perspective is exercised alongside the continuous and tenacious efforts to reduce carbon footprint.

Conclusion and recommendations

Our study has shown that SMEs are substantial contributors to the shift to a LCE; that many are optimistic about the new opportunities afforded by the emerging markets for low carbon goods and services; and that many are engaged in becoming more resource and energy efficient as well as more broadly sustainable. However, a high proportion of SMEs remain unaware of the support, guidance and funding that will facilitate their sustainable business development.

The survey results indicate that whilst many SMEs have adopted quite rudimentary steps to reduce their carbon footprint, a significant minority have developed more sophisticated or innovative approaches to their own carbon management, including alternative power generation. Like various other studies, the main impediments to engagement were seen as lack of time and money, lack of relevance to the business (due to the micro-size of some of the respondents) and lack of knowledge of sustainable alternatives. A very few respondents actively measured or set targets for their carbon output, which are commonly viewed as an initial step to making organisational change and establishing environmental reputation in order to support business growth and development (Benn et al., 2014; Haigh and Griffiths, 2012; Hoffman, 2005). This is clearly an area where firms could be better supported.

The majority of the SMEs surveyed indicated that they engage in various energy efficiency projects. These types of initiatives can be seen as the first steps towards carbon reduction ambitions, which are often linked to cost cutting. In our view, SMEs should go beyond ‘energy efficiency’ rationale when answering the questions ‘Are we fit to take advantage of the green growth? and ‘How can we support a shift to a low carbon economy?’. To succeed in a low carbon economy, they need to apply a more strategic approach to building capabilities (Baranova and Meadows, 2017). Some of these considerations could be about an SME’s responses to the emerging niches for LCEGS in their current markets. Some of them could be about developing competitive advantage derived from sustainability-centred business models and some are about disruptive innovation offering carbon neutral product and service substitutes.

Although the majority of SMEs surveyed indicated that their main needs were access to funding and finance, followed by capabilities in energy and materials efficiency, and waste management, we argue that attracting finance to support sustainability efforts requires strong leadership and a strategic perspective on how these investments can, not only reduce costs in the short term, but aid long-term growth aspirations. We also found variations in the demand for environmental capabilities across the sectors we studied, as well as variations that relates to the size of an enterprise. Thus, the development of a business case for green investment needs to consider how SMEs can take advantage of the opportunity presented by green growth more strategically and include development of environmental capabilities, which goes beyond the aspirations to cut energy bills. This is so that regional SMEs are fit to grow and compete successfully whilst supporting transition to a LCE. In pursuit of these aims, we offer a typology of SMEs environmental capabilities and anticipate further research to explore the utility of this conceptual development.

As for the regional support to ensure SMEs engage and take advantage of the opportunities presented by green growth, a much more integrated and collaborative approach is required that recognises the specific requirements of smaller businesses. We argue that local government, corporate businesses, a range of national and regional NGOs, as well as higher education institutions (HEIs) should all play a much more active role in contributing to SMEs’ support networks, partnerships and supply chain collaboration to accelerate the shift to a more sustainable economy.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.