Abstract

There has been academic and policy concern about the financial capacity of administratively fragmented metropolitan areas to implement inclusive development measures and provide public services. Metropolitan public financing is problematic because there is a geographical mismatch between extended functional urban regions and administrative units. While local governments are responsible for implementing policies, spending, and raising revenues, financial capacity tends to differ across jurisdictions in response to economic, social and political factors, resulting in manifold disparities. Such variations can be particularly acute depending on the complexity and size of the metropolitan area, and can lead to major spatial disparities in the life standards of residents. This paper focuses on the local financial condition in Mexico City Metropolitan Area, which is often used to exemplify a fragmented metropolitan area. Official statistics from 1989 to 2018 are used to identify major intra-metropolitan variations in the financial condition of local governments. A novel methodology is used to classify municipalities according to their financial health, and discriminant analysis is used to explore the factors shaping the geography of financial performance. The economic and demographic size of municipalities appear to play a significant role.

Introduction

The predominance of metropolitan areas, especially in less-developed countries, is a growing phenomenon accompanying recent global urbanization. Metropolitan areas face daunting economic and financial challenges which are increasing in both scale and scope. Many of these challenges require efficient ways of governing, managing and financing such urban centers which are often poorly managed. Tax and transfer systems are not adapted to the shape and function of cities and regions’ modern economies, and policies rarely recognize or address the particular characteristics of metropolitan areas (OECD, 2001). The management and financing of metropolitan areas is particularly problematic: the political boundaries of governments rarely coincide with the boundaries of the metropolitan area where multiple local governments provide services, raise revenues and spend; problems arise in coordinating service delivery and sharing costs appropriately; and governmental economic, technical, and financial condition tend to differ across jurisdictions resulting in manifold disparities. Public finance, in particular, is among the most critical threats to the performance of metropolitan regions because the governmental institutions whose taxing, spending, and borrowing are recorded almost never map into the economically relevant metropolitan area (Bird and Slack, 2007). The existence of financial and fiscal disparities in a large metropolitan area is a major problem because it shapes the geography of economic opportunity and development. For metropolitan areas to take a wider role in competitiveness and development, they need to first recognize and then effectively tackle their governance and financial challenges.

Bird and Slack (2007) claim that despite the obvious importance of this problem, attempts to systematically analyze the public finances of metropolitan regions remain scarce. Initially what appears to be needed most is a more comprehensive appraisal and understanding of the financial performance and fiscal condition of local governments in such metropolitan contexts. Studies of fiscal decentralization, intergovernmental relations and public finances generally continue to center on the formal tiers of government, failing to consider the particular settings of metropolitan areas (Raich, 2006). For instance, how metropolitan areas are situated in the national fiscal, institutional and political framework is an important but neglected issue, especially in the study of urban public finances (Smoke, 2015).

In the analysis of intra-metropolitan financial health, it has been assumed that compared to suburban jurisdictions, many central cities face above-average service costs and below-average financial capacity; that is, suburbs enjoy some fiscal advantages (Chernick and Reschovsky, 2013). Analysis of these differences across jurisdictions grouped in metropolitan areas has not been addressed in the literature on local or urban finances in Mexico. There is a particular need to distinguish and explain the fiscal, economic, and political differences within the metropolitan area of Mexico City to be able to problematize the implications for territorial and social justice in one of the largest metropolises in the world. Although Mexico City has more responsibilities and an excessive financial burden due to the services provided to its large floating population, as a city-state it also has acquired more financial and fiscal powers than local governments within its metropolitan area have. This paper contributes to the literature by analyzing the geography of the performance of public finances in Mexico City Metropolitan Area (MCMA). MCMA is one of the largest urban agglomerations in the world, with national economic, political, and demographic pre-eminence. It is also the most complex metropolitan area in Mexico in terms of its political and administrative fragmentation.

The paper addresses the following group of questions: (1) What is the financial condition of local governments, and what is the extent of the spatial disparities in MCMA? and (2) What are the factors behind the spatial variation in the financial condition of the MCMA’s jurisdictions? The objective is to identify major intra-metropolitan variations in the financial condition of local governments using a novel methodology to classify municipalities according to their financial health, and to explore what shapes MCMA’s financial geography. This is an issue to investigate when jurisdictions in a metropolitan area are of different economic, administrative, and fiscal natures, as in the case of MCMA. Such study is needed to inform metropolitan initiatives aiming to promote good governance and inclusive sustainable development.

Based on a data set of the public budgets of constituent local governments in MCMA, I estimate customized indexes of financial conditions to create a categorization of local governments. I propose some criteria for the classification of municipalities and employ discriminant analysis to explore the influence of a number of socioeconomic factors on the geography of local financial performance. By presenting a synthetic literature review, I first discuss issues of the financial condition of local governments and their disparities. I then describe the case study and explain the methodology. The results of the empirical analysis of MCMA are discussed, and the paper closes with some conclusions.

Public financing in metropolitan areas and the geography of financial condition

A metropolitan area is a complex urban setting with a larger population and higher concentration of production than is found in other cities, often with a problematic jurisdictional and intergovernmental structure. Metropolitan areas face an adverse environment of political fragmentation, a lack of strong governance and weak local autonomy (OECD, 2001). The complexity of metropolitan areas lies mostly in the superposition of functions across multiple jurisdictions and levels of government (Meza, 2004). Such particularities create increasing pressure on the use of public resources, usually requiring financial reforms that promote efficiency and equity (Bird and Slack, 2005).

Decentralization and intergovernmental relations are powerful forces influencing the management of metropolitan areas and their fiscal and financial performance. In a decentralized environment, jurisdictional fragmentation disconnects the territorial scope of urban needs from the public resources required to meet them. This mismatch increasingly occurs in a context where public budgets are being reduced and local authorities have to do more with less. Overall, metropolitan governments and institutions have a limited range of responsibilities and functions and are ruled at the same level as lower tiers of government (Bahl, 2010). But attempts at territorial reorganization to serve urban realities better tend to be hindered by the status quo, especially in less-developed countries, and the task of fiscal and financial reform has been severely restricted by political factors including local authorities’ poor capacity, and the lack of local political will and national political support (Trejo Nieto, 2020).

According to Chernick and Reschovsky (2006), in the absence of an adequate metropolitan or fiscal institution, fragmentation negatively affects the behavior of public finances, economic performance and the inclusive provision of public services. With limited resources this often leads to a poor quality of life, loss of competitiveness and multifarious disparities. Asymmetries in financial performance tend to emerge across metropolitan areas that are highly fragmented and have no metropolitan fiscal structure. Fiscal and financial disparities are a hot policy issue because widely varying intra-metropolitan fiscal performance is commonly linked to other urban inequalities.

Local financial condition

Intense concern about the fiscal conditions and disparities of local governments emerged in the 1970s and 1980s in the United States (Yilmaz, et al., 2006). Studies have also looked at vertical disparities and the role of intergovernmental transfers in the elimination of fiscal gaps (Heng, 2008). Much of this literature has been motivated by attempts to develop objective measures of local government’s fiscal conditions for use in equalization policies designed to reduce financial disparities and policies assuring that each successive lower-level government has sufficient fiscal resources to guarantee that its residents have access to a specified set of public services (Chernick and Reschovsky, 2013). Interest in fiscal health and disparities in metropolitan areas arises from concern about fiscal stress and the inadequate provision of urban services and infrastructure in extended urban areas.

Fiscal health is a complex normative concept that tends to be audience-specific (Justice and Scorsone, 2013). Broadly speaking, it refers to governments’ ability to meet their obligations and provide services adequately, or their capacity to finance base-level programs and services as required by law. A local government is considered fiscally healthy if its revenue meets its obligations. Financial condition is a similar concept: “Simply stated, financial condition is understood as the ability of a government to balance its financial obligations with its available revenue streams” (McDonald, 2017: p. 2). Because it involves several financial and administrative issues (Jacob and Hendrick, 2013), there is no uniquely correct concept of the financial condition of local governments, nor only one measure of fiscal health (Bird, 2014). Thus, in addition to the lack of data availability, a key issue in assessing fiscal condition is deciding suitable definitions and indicators (Gordon, 2018).

Local governments are often said to be in budgetary crisis because their fiscal needs exceed their revenue. According to Bird (2014), the fundamental fiscal health of a city has less to do with balancing its budget than with the quantity and quality of the services provided and the state of its infrastructure. Even the most basic public services are threatened if a local government is not fiscally healthy (Levine, et al., 2013). The problem with fiscally unhealthy local governments is not only that they may experience fiscal stress but also that the financial constraints to providing services and infrastructure create hardships in the daily management of social and economic problems (McDonald III, 2017).

The representative tax system approach, which attempts to capture the fiscal gap (defined as the difference between spending needs and fiscal capacity) 1 , has been used to quantify differences in fiscal health and compare revenue capacity (fiscal effort) and spending needs across jurisdictions. But there is usually insufficient data available to allow the estimation of fiscal gaps with this approach. Other approaches have been used to evaluate horizontal fiscal disparities. Heng (2008), for instance, uses inequality indexes such as the Gini coefficient, the coefficient of variation, and generalized entropy indexes to measure disparities in per-capita revenue and expenditure in Chinese provinces. The standard deviation in per capita revenue and spending also measures the extent of variation across local governments’ fiscal capacities and expenditure needs.

Some evaluations of local financial conditions borrow analytical instruments from the private sector using financial condition ratios from city balance sheets and activity statements. Ratios are used because they are easily obtained from financial reports, although the choice of indicators, critical values and benchmarks is highly subjective (Gordon, 2018; McDonald III, 2017). Despite these drawbacks, useful indicators can readily be constructed from available financial data to assess the simpler but interrelated concepts of sustainability, flexibility, and vulnerability, which are linked to the levels of taxation, indebtedness, and transfers that provide an approximation of governments’ fiscal condition. Financial performance is usually evaluated via a broader benchmarking exercise (Bird, 2014).

Fiscal sustainability is a growing perspective from which to analyze the current state of urban finances and a city’s long-term prospects. Sustainability approaches to fiscal health attempt to capture the extent to which local governments face fiscal stress in terms of their ability or resiliency in the management of public finances (Bird, 2014). Justice and Scorsone (2013) identify three areas of financial condition: (1) sustainability, or the ability of a government to meet its financial and service commitments; (2) flexibility, or the degree to which governments can change their debt; and (3) vulnerability, or the degree to which a government is dependent on sources of funding outside its influence. Bird (2014) proposes similar criteria.

Attempts to assess the performance of local public finances using ratios have included aspects of local government such as their self-financing ability, degree of dependence on national transfers, saving capacity, and dependence on debt, among others. Others emphasize administrative capacity for managing local finances, and the execution of programs and projects. Available data usually allow exploration of the three aspects mentioned above: sustainability, flexibility and vulnerability. Sustainability focuses on the degree to which a government can maintain its existing programs and services and meet its current financial obligations without increasing its debt or raising taxes. Flexibility represents revenue capacity and measures the degree to which a government can increase its taxes or own income, often in response to changing environmental conditions. Vulnerability is a function either of transfer dependency or of the risks created by exogenous shocks that affect the local tax base (Bird, 2014). In this paper, we used this approach to look at local financial condition.

Fiscal disparities in metropolitan areas

Disparities appear in local financial condition for different reasons. On the one hand, local public revenues depend on local governments’ fiscal capacity, which is contingent on the level of economic activity and development in the jurisdiction and on the various tax and revenue instruments applied. On the other hand, expenditure needs vary across local governments because bigger jurisdictions are required to provide a broader range of public services, even if they all have the same public-service responsibilities (Chernick and Reschovsky, 2013). Moreover, the cost of providing public services and other spending needs vary across local governments due to aspects of a jurisdiction that they cannot control such as population size, density, sociodemographic characteristics, physical characteristics of neighborhoods, the prevalence of low-income households, overcrowding, local preference for public services, and local inefficiencies. Costs may be higher in the central city than on the periphery because the infrastructure tends to be older and maintenance and repair costs are therefore generally higher. Similarly, per capita costs in central cities may be greater because governments must provide public safety, sanitation and cultural and recreational services for a significant number of non-residents, whether suburban commuters or tourists.

The implication of widely varying intra-metropolitan fiscal performance is that, depending on their location, the residents receive different levels of public services even though they face identical tax burdens. Unequal fiscal conditions create an incentive for households and companies to move to locations in the metropolitan area with better fiscal health, in turn stimulating greater imbalances. Independent local jurisdictions’ uncoordinated policies create frictions that limit the growth potential of the entire metropolis. This tends to be most pronounced in highly jurisdictionally-fragmented metropolitan areas (Bahl, 2013).

A vast body of literature on metropolitan fiscal health and disparities has developed, most of which analyzes the US case. But there is also interest in a more extensive treatment of local fiscal health (e.g., Levine et al. 2013). Chernick and Reschovsky (2013), on their part, find substantial fiscal differences between the central city and the suburbs in the Milwaukee metropolitan area in terms of the spending levels, property tax base, intergovernmental aid, and tax rates, as well as substantial variation among the suburban jurisdictions. They suggest that inner areas face fiscal disadvantages. However other case studies might involve dissimilar patterns of fiscal performance.

Mexico City Metropolitan Area as a case study

Mexico City Metropolitan Area is the biggest metropolitan area in Mexico and one of the largest in the world. As an example of jurisdictional fragmentation (Bahl, 2013) it consists of Mexico City proper (the administrative jurisdiction that includes the main urban center and is divided into 16 boroughs), 59 municipalities in the State of Mexico and 1 municipality in the state of Hidalgo. The 2015 inter-census survey recorded a population of 20.9 million, 57% of whom were living in the municipalities outside Mexico City proper (INEGI, 2015).

Mexico has three levels of government—federal, state, and municipal—each of which is autonomous in both its capacity to collect revenues and its spending practices. But metropolitan areas are not recognized as formal political entities that can handle decentralized resources and responsibilities. Historically, the ability to deal with metropolitan issues and problems has been restricted by fiscal federalism and decentralization. In MCMA, home rule prevails to the detriment of coordination and efficiency. Services are delivered by the capital district and 76 local governments in two different states (Bahl et al., 2013). Coordination is complicated by the number of layers of government involved, the number of local governments, the involvement of two states and a national capital district, and the coexistence of political parties with different orientations (Bahl, 2013). Although there have been instances of metropolitan coordination bringing together the authorities at the state level on specific issues and problems involving the environment, water and drainage, public safety and justice, human settlements, and transportation and roads, there are no formal designated metropolitan institutions, and such instances have proved ineffective due to a lack of financial, regulatory and decision-making authority (Cenizal, 2015).

The fiscal organization of Mexico City Metropolitan Area

The fiscal system that operates in this metropolitan area is as complex and heterogeneous as the political-administrative system. Mexico City proper has a special political and administrative status as the country’s capital city, creating fiscal complexities that differentiate MCMA from other metropolitan areas. A multilevel fiscal structure and different fiscal regimes operate simultaneously due to the presence of governments at the federal, state, Mexico City proper, municipal and borough levels. The nature of the spending responsibilities, the types of revenue tools used, and the extent of local fiscal autonomy vary across jurisdictions. Mexico City proper has a different fiscal regime from that of ordinary states, and its boroughs also differ from municipalities. Moreover, the pressures on and demand for services and social programs vary compared to commuter and suburban municipalities. As a national capital, every day Mexico City proper receives an influx of commuters and floating population who use public transport and put excessive pressure on other public services (OECD, 2004).

Due to a political reform that culminated in 2016, the former Federal District became a sort of city-state whose government acquired all the fiscal powers of intermediate government (i.e., state government). As a result, the now officially named Mexico City (Mexico City proper) centralizes boroughs’ fiscal functions and budget processes, leaving them without either the power of taxation or the fiscal autonomy of municipalities in the rest of the country. Thus Mexico City proper collects state taxes (i.e., payroll, car tenure, hotel room among others) and local taxes, with the result that as a level of government it collects more than any state or municipal government. While Mexico City proper is excluded from receiving certain federal transfers (the funds earmarked to state education—FAEB and FAETA—and to the municipal infrastructure fund—FAIS), it is the target of larger direct federal spending. According to Article 122 of the Constitution, Mexico City proper has to provide local services which are mostly delivered by the city government in coordination with local mayors (Bird and Slack, 2005).

In contrast, the metropolitan municipalities in the States of Mexico and Hidalgo have the same revenue sources and manage the same areas of expenditure as municipalities in the rest of the country. The decentralization that began in the 1980s has included several constitutional reforms granting municipalities increasing powers (Jalomo, 2011). The 1983, 1987, 1999, and 2009 reforms to Article 115 of the Constitution placed the municipality at the center of the administrative and political organization of the federation. The Article stipulates municipalities’ autonomy, sources of revenue (property tax, tariffs and fees), and their main tasks (the provision of local public services including drinking water and sewerage, public lighting, cleaning, markets and supply centers, cemeteries, streets, parks and gardens, public safety, and transportation) (Meza, 2004).

The 1980 National System of Fiscal Coordination (NSFC) gave the federal government wide taxation powers (Courchene and Diaz-Cayeros, 2000; Meza, 2004) and left municipalities with few sources of own income (Díaz, 2015). In addition to very small portions coming from fees and tariffs from services, property tax (predial) is the main potential source of municipalities’ own revenue. The autonomy that the State confers on the municipalities can create significant divergences in the management of property tax. Municipalities across the country can propose their own tax rates to state congresses, adjust them, and implement organizational changes and collection strategies (Marín Origel, 2012). Although the changes brought about by fiscal decentralization have impacted local governments differently, in general Mexican municipalities have not been able to increase their financial autonomy, and the potential for revenue collection has been wasted. They have not been sufficiently proactive in improving tax enforcement or achieving substantial progress in tax collection (Espinosa et al., 2018; Unda Gutiérrez, 2018). Revenues from property tax in Mexico are among the lowest in Latin America (Espinosa et al., 2018): only 21% of local revenue comes from own income, with property tax contributing only 8.8% (Unda Gutiérrez, 2018). Among the federal-country members of the OECD, local governments in Mexico have the lowest revenue and spending capacity at about 2% of GDP (OECD, 2016).

Some evidence shows that greater economic development has positive dynamic effects on municipal fiscal effort (Mendoza, 2019). Greater institutional and technical capacity (Unda Gutiérrez, 2018, 2021), concrete efforts to update the cadastre, and efficient municipal tax administration systems contribute to explain the apparent success of municipalities’ collection performance (Espinosa et al., 2018). On the other hand, weak tax bases, lack of comprehensive cadastral modernization strategies, and insufficient development of tax administration mechanisms seem to determine municipalities’ fiscal weakness (Espinosa et al., 2018). A prevalent reality is that mayors, treasurers and directors of land registers do not increase rates or update land registries and cadastral values because they are unwilling to pay the political costs for so doing. This belief comes from the idea that taxes are a political problem, unpopular by nature, and require the construction of a consensus with society (Mendoza, 2019; Unda Gutiérrez, 2018).

The fiscal decentralization model has revealed the lack of incentives, infrastructure for cadastral modernization, and human resources trained to effectively operationalize the tax powers granted to municipalities (Flores, 2002; Mustre and Urzúa, 2017). Under the National System of Fiscal Coordination, federal transfers make up around 70% of total revenue in the vast majority of municipal governments (Unda Gutiérrez, 2018). The most important items in the tax-sharing system financing municipalities are compensatory unconditional transfers and compensatory conditional transfers. The latter include funding for basic local infrastructure. There is a widespread notion that the Mexican transfer system created disincentives to collecting own revenues and reduced local fiscal effort (Castro et al., 2019; Flores, 2002; Mendoza, 2019), but Unda Gutiérrez and Moreno-Jaimes (2015) and Unda Gutiérrez (2021) find that intergovernmental fiscal transfers have not necessarily discouraged the collection of property tax. The local political environment has an impact on the differences in municipalities’ financial dependence (Ibarra Salazar et al., 2013)

Further problems with local finances in Mexico include inadequate finance policies; recurring operational deficits (Meza, 2004); a boom in borrowing (Kinto, 2009); and limited human, technical and operational resources (Rosales, 2012). The municipalities’ poor financial capacity has significantly affected their efficiency at providing local public services. They face financial constraints and challenging spending responsibilities.

Methods and data sources

Only a few studies of local public finances in Mexico analyze metropolitan areas; for instance Aguilar (2010) examines the determining factors of tax capacity in the three largest metropolitan areas, and Moya (2014) analyzes the Metropolitan Fund designed to finance metropolitan projects in the country. Based on available data of yearly local revenue and expenditure budgets, I produced a database of MCMA’s public finances. Annual series of the National Institute of Statistics and Geography (INEGI)’s State and Municipal Public Finances for the years 1989–2018 were used. Data in current prices are deflated based on the national consumer price index (INPC), using 2012 as the base year. One shortcoming of this data is that some municipalities tend not to report their acquired debt to INEGI. The advantage is that INEGI’s information provides a comprehensive and comparable dataset from 1989 onwards that includes most municipalities in the country. Boroughs in Mexico City only have an expenditure budget.

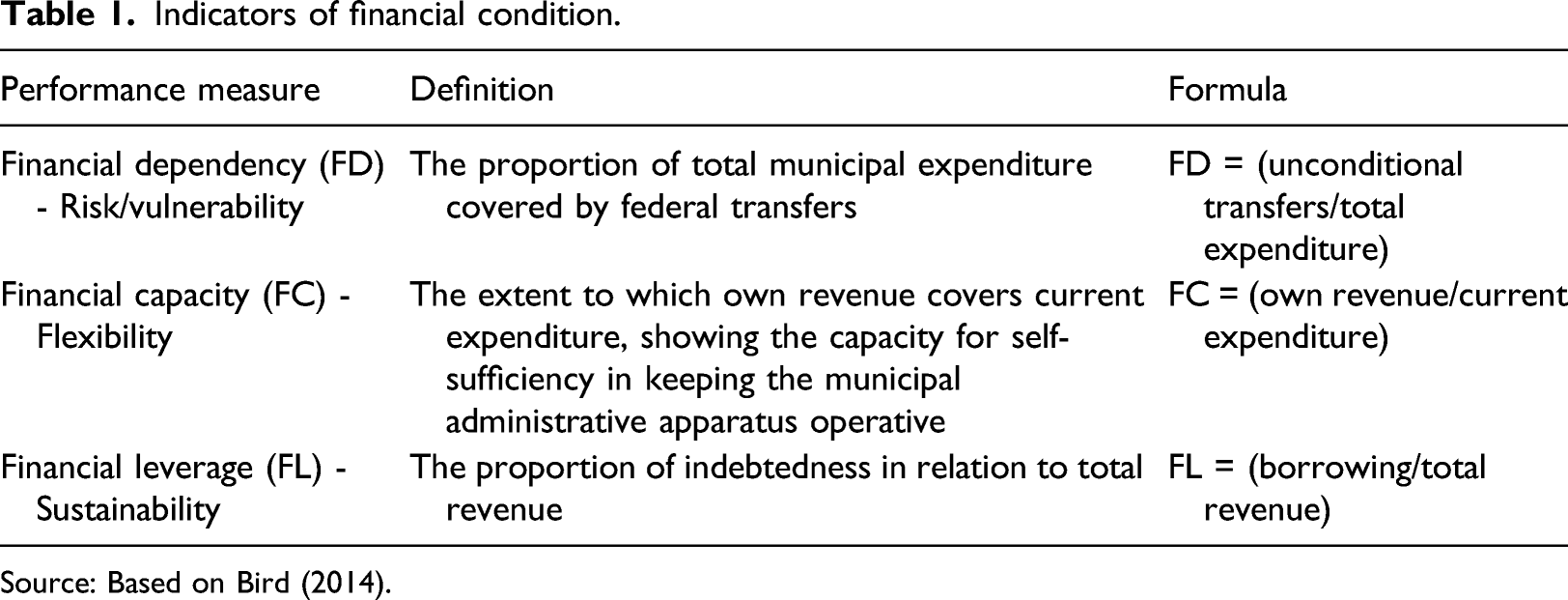

Indicators of financial condition.

Source: Based on Bird (2014).

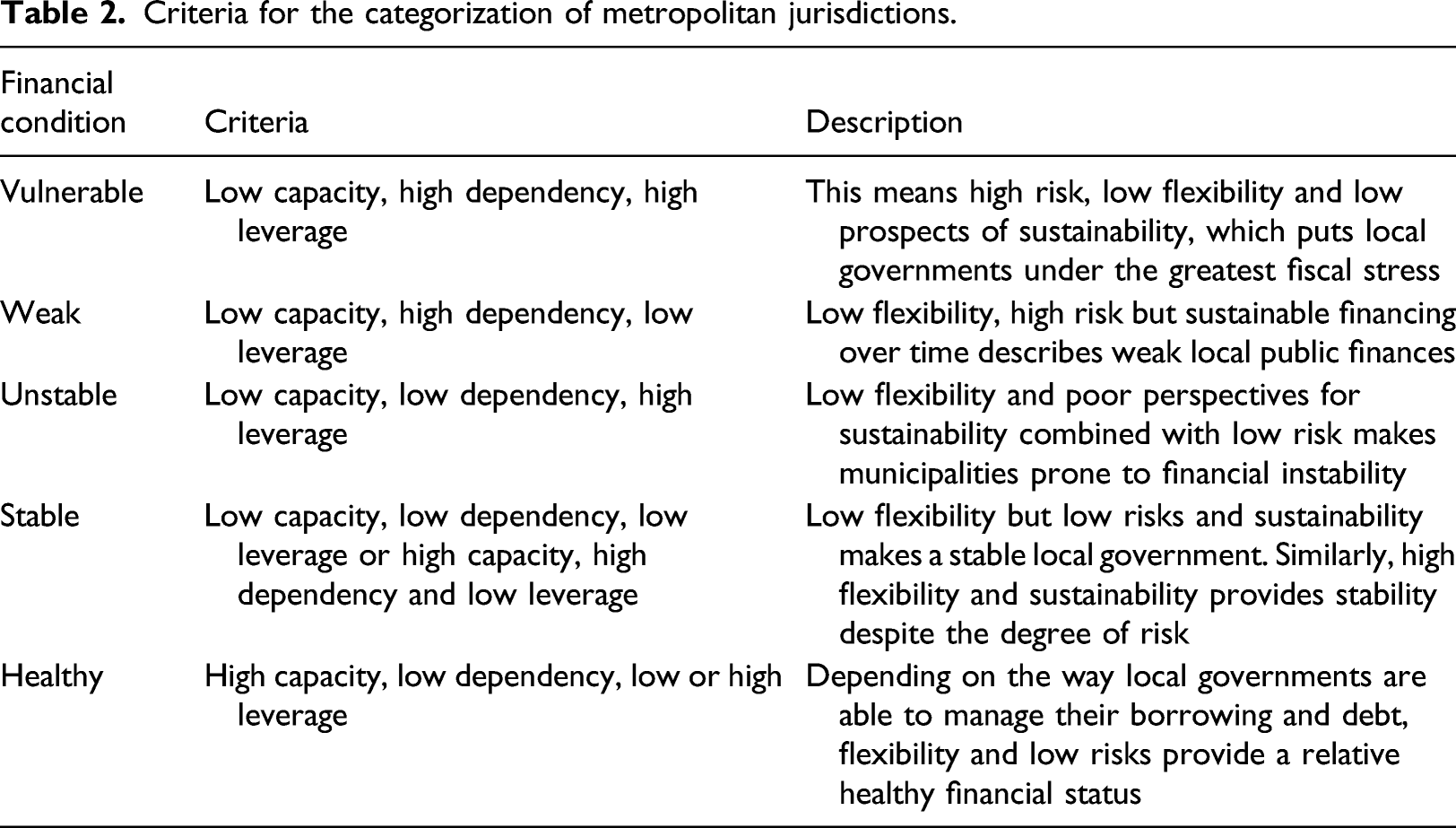

Criteria for the categorization of metropolitan jurisdictions.

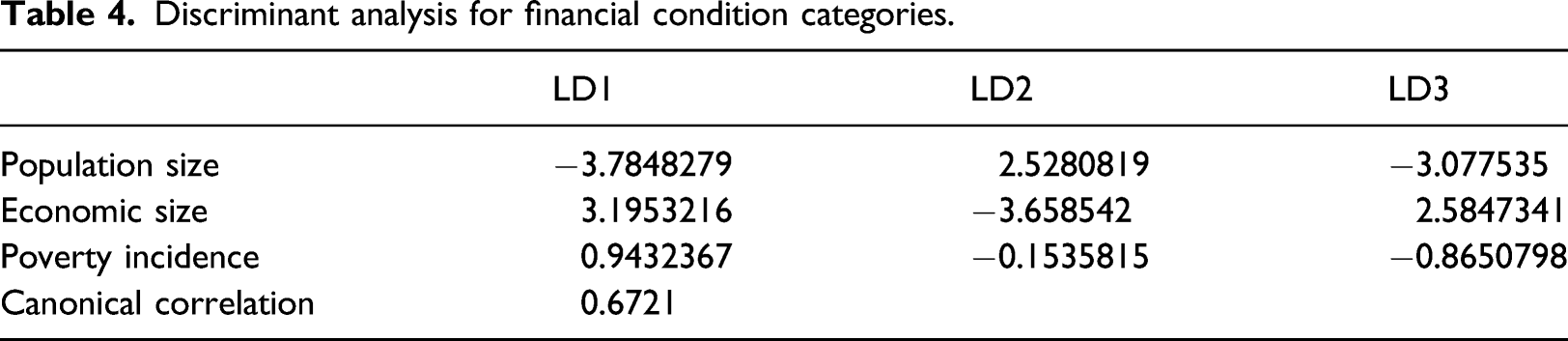

Lastly, I use discriminant analysis to explore the economic factors related to the differing financial condition of local governments. This multivariate technique determines whether some characteristics of local jurisdictions can be systematically linked to categories of financial condition. 2 The canonical correlation R is computed to measure the association between the groups formed by the dependent variables (here, financial condition) and the given discriminant function based on the X-variables representing fiscal capacities and population needs (i.e., the extent to which units are correctly classified into groups). When R is zero there is no relationship between the groups and the function. A large R means there is a high correlation between the discriminant functions and that the groups and the discriminant variables can be considered good predictors of the performance of the local governments under consideration.

Given that there is still a generalized problem with Mexico’s technical and institutional capacities and political refusal to increase tax rates, I focus on the socio-economic aspects of financial condition. Marín Origel (2012) finds that despite a gradual and slow growth in tax revenues, one of the greatest problems in the financial capacity of local municipalities in the State of Mexico is their weak collection capacity. Their tax collection is insufficient to meet their public services provision obligations. The situation is consistent across most local governments.

Following one strand of the literature, the discriminating criteria used here are socioeconomic variables gauging financial capacity, measured as the economic bases (municipal gross production according to economic censuses), and population needs (population size according to population censuses and poverty incidence according to Mexico’s National Council for the Evaluation of Social Development Policy).

Metropolitan public finances and the geography of financial condition

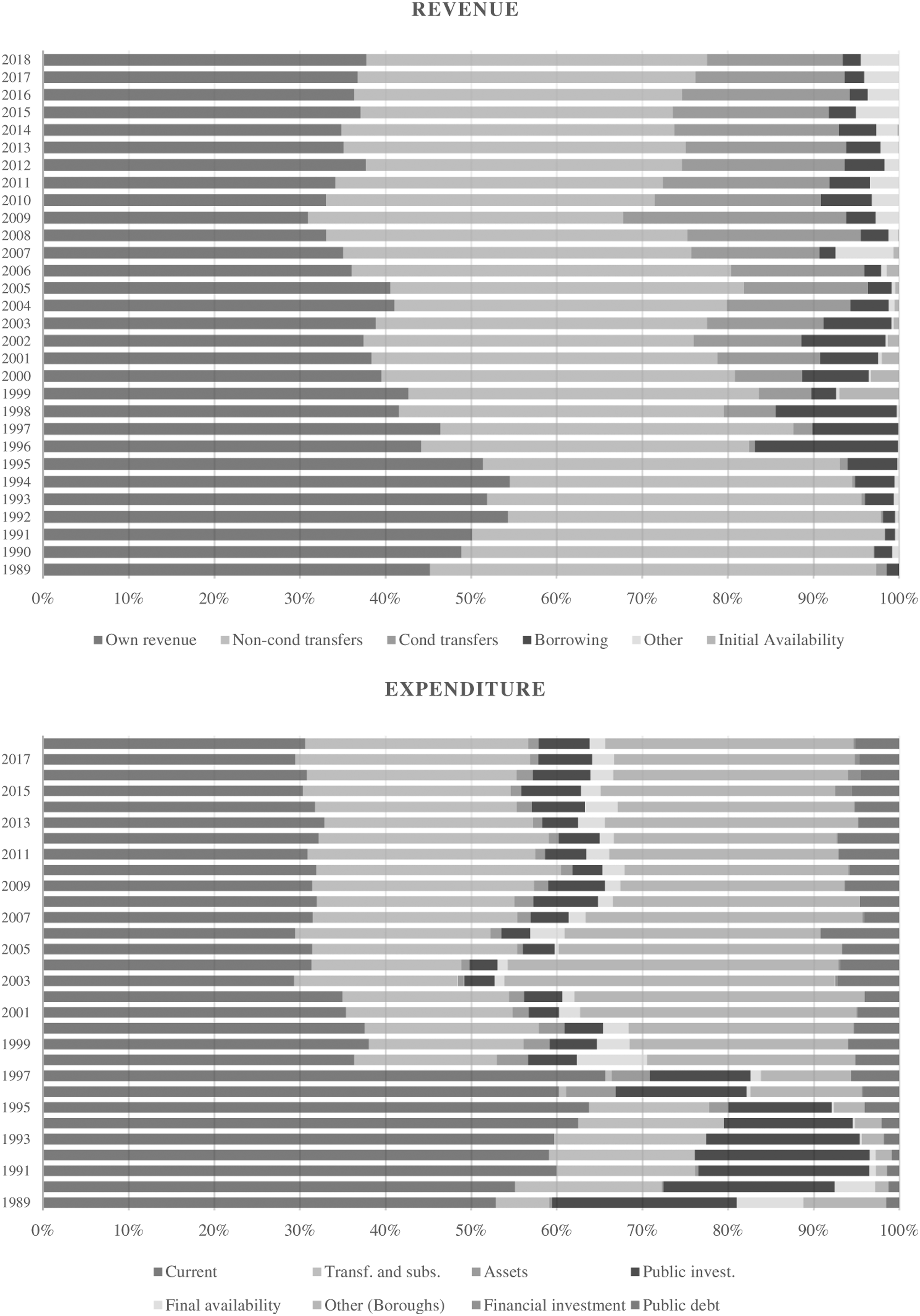

The aggregate budget in MCMA has been steadily increasing since 1989, apart from important drops in 1995 and 2009 following the two severe economic crises. Revenue and expenditure items have grown at different rates. Between 1989 and 2018 total budgets grew by an annual average of 4.4%, Federal transfers at 4.7% and Borrowing at 22%. Own revenue increased at the lowest rate (4%) for the whole period, but grew at a rate of 6.2% between 2010 and 2018, faster than all other revenue items. In expenditure, Public investment increased at an annual rate of 3.8%, similar to Current spending (3.1%). Public debt was a fast-growing item with an average of 13.3% increase per year.

As shown in Figure 1, total Federal transfers (i.e., conditional and unconditional transfers) are the main revenue item with more than 50% of the total. The flow of own revenue has improved since 2009 but remains a secondary source of financing. Since 1998 Social transfers and subsidies (which area part of economic and social policies) represent an important and increasing portion of total spending. In contrast, the shares of Current spending and Public investment have decreased. This restructuring reflects the effects of the administrative and fiscal decentralization in favor of Mexico City. Before 1996, the administrative department in charge of managing the city’s public resources depended on a federal executive office setting the orientation and implementation of public expenditure, which was driven mainly by national objectives rather than local needs, but this arrangement was modified in a reform to Article 122 (Rodríguez, 2009). Composition of public revenue and expenditure in MCMA, 1989–2018 (%). Source: Based on INEGI (2020).

Fiscal disparities

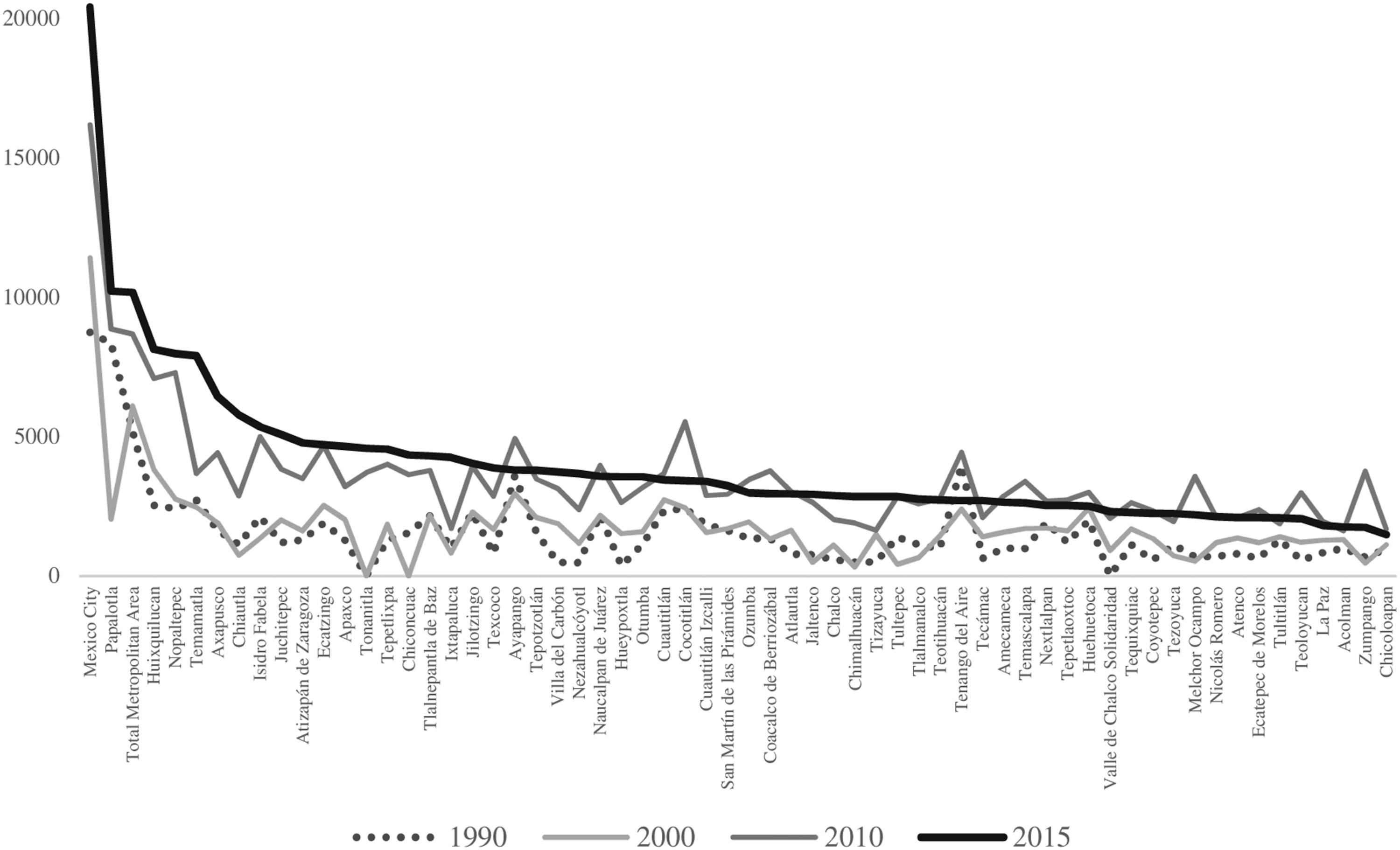

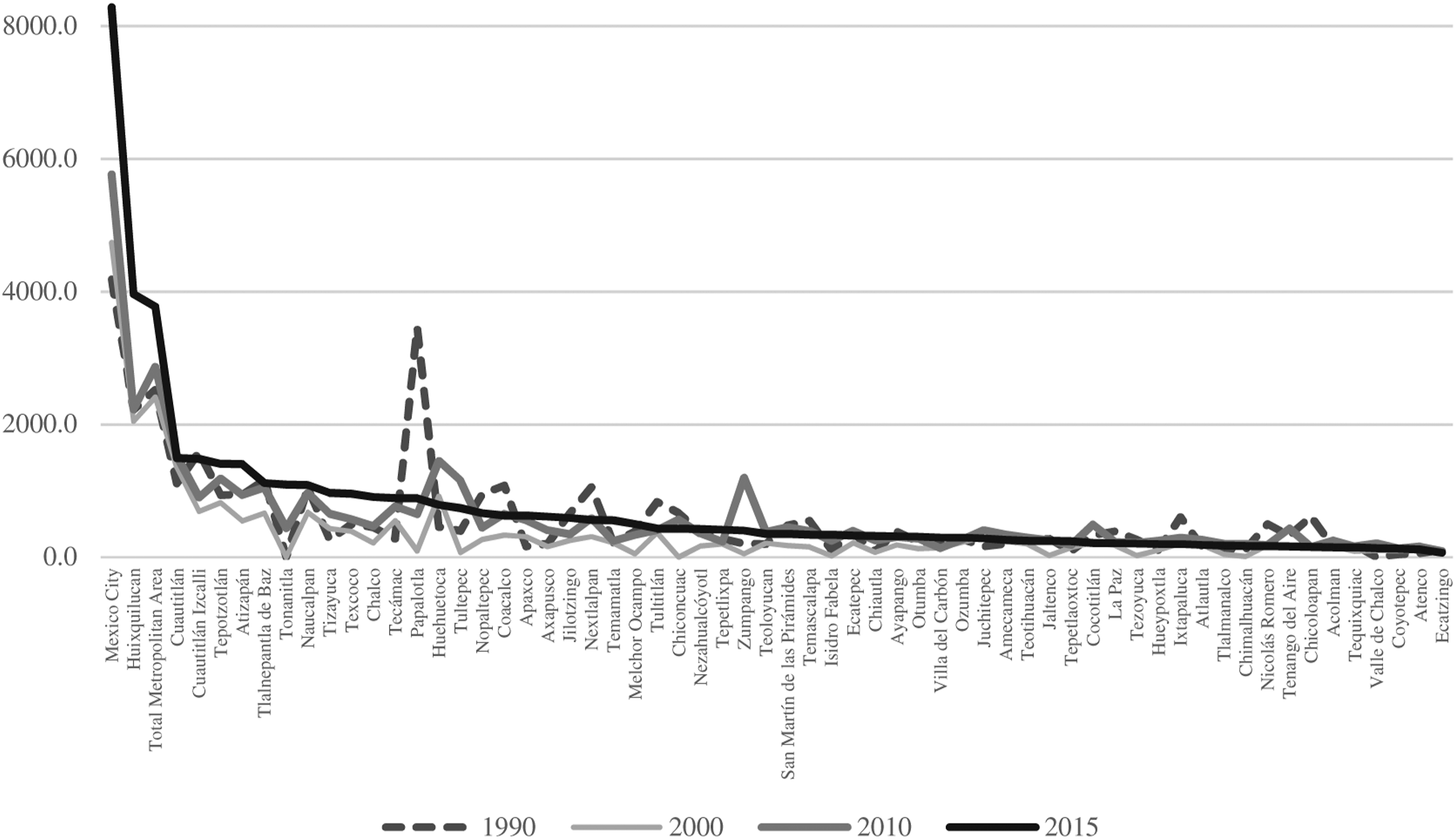

Geographically speaking, 80–90% of public resources are concentrated in Mexico City proper in clear contrast to the distribution of the population, implying important disparities in relation to the other metropolitan municipalities. Previous research has shown that while many of the problems and challenges are common to all of Mexico’s municipalities, their financial performance is unequal (Cabrero and Martinez-Vazquez, 2000; Díaz, 2015). There are disparities in spending and especially in public investment (Cabrero and Martinez-Vazquez, 2000). The municipal governments’ financial autonomy also varies considerably (Rosales, 2012), with differences even between municipalities of the same size (Cabrero, 2004). Such horizontal disparities are observed within MCMA. The OECD (2004) attributes the significant fiscal disparities between Mexico City and the municipalities in its metropolitan area to the former’s more advanced economic development and significantly greater fiscal powers. This concentration has also been attributed to Mexico City proper’s above-average collection efficiency and stronger fiscal base. My data confirms substantial per capita gaps between Mexico City proper and the metropolitan municipalities. For instance, in 2015 per capita revenue in Mexico City proper was about 14 times that of Chicoloapan, the municipality with the lowest per capita revenue (Figure 2). Municipal per capita revenues tend to increase over time, with the exception of a number of cases. Larger differences emerge in per capita own revenues since Mexico City proper’s per capita own revenue is 124 times that of Ecatzingo and double that of Huixquiluca, the municipality with the highest per capita own revenue (Figure 3). Local public budgets per capita, 1990, 2000, 2010, and 2015 (Mexican pesos, 2012=100). Source: Based on INEGI (2015, 2020). Own revenue per capita, 1990, 2000, 2010, and 2015 (Mexican pesos, 2012=100). Source: Based on INEGI (2015, 2020).

Fiscal disparities 1990, 2000, 2010 and 2015 (Mexican pesos, 2012 = 100).

Source: Based on INEGI (2020).

A geography and explanation of local financial condition in Mexico City Metropolitan Area

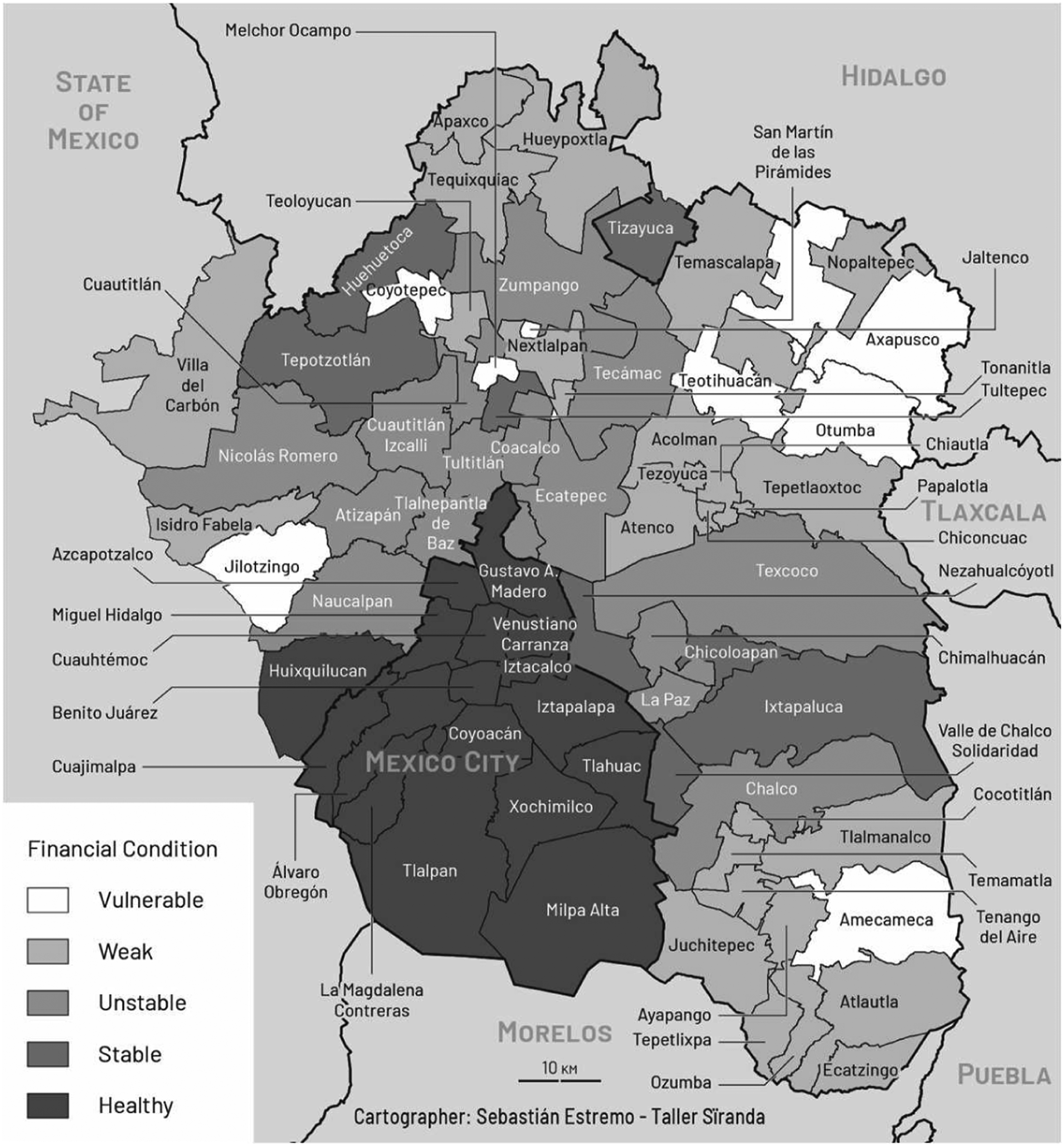

The three measures and the five proposed categories of financial condition provide us with a perspective on the geography of financial condition in MCMA (see averages in Supplemental Table). The largest proportion of local governments (46%) has weak finances, followed by 25% with unstable finances. Around 13% of municipalities’ finances are vulnerable, the worst condition, and 13% are financially stable. Lastly, Mexico City and the municipality of Huixquilucan have relatively healthy finances, with low dependence on transfers and high fiscal capacity (Figure 4). Municipal financial condition, MCMA (Average, 1989–2018).

Some patterns are identifiable: smaller municipalities tend to be highly vulnerable or financially weak; vulnerable municipalities are located in the most peripheral areas; several highly industrialized municipalities with large populations and neighboring Mexico City proper are in the unstable category (they are probably under strong fiscal pressure to provide services and renovate their infrastructure); and the two jurisdictions with the best financial health have a broad fiscal base and the economic potential for levying taxes.

Hence despite the greater pressure on expenditure for service provision, the central city financially outperforms almost all of the municipalities. This is a contrasting geography to that which describes the fiscal and financial disadvantages of central cities compared to suburban municipalities in metropolitan areas. The depicted geography of financial condition confirms the clear financial disparities across the metropolitan area, especially between Mexico City proper and the municipalities.

Discriminant analysis for financial condition categories.

Three discriminant functions are obtained (the three columns). The figures reported in the rows are the canonical loadings representing the weights of each variable used to categorize municipalities into groups. The absolute value of the coefficient has a similar interpretation of the significance of a variable in a regression estimate. The discriminant variables are acceptable predictors of the performance of the local governments. Economic and population size play a significant role in discriminating between groups. The signs of those two variables in the first function, which is the most accurate, correspond to the expectations: a negative effect of population size and a positive effect of economic base. Even though the model fails to identify any municipality in the Vulnerable category, and does a poor identification of the Stable group, almost all municipalities are correctly classified in the Unstable, Weak and Healthy categories (63% of municipalities). Despite the financial burden implied by the prevalence of low-income households, surprisingly, poverty incidence is not a highly significant discriminant factor. Arguably political, technical and operative aspects of local governments are necessary to explain the financial condition in the most financially vulnerable municipalities in MCMA. Systematic research on the issue of the determinants of financial condition will be needed to expand this first exploration.

Conclusions

Like many metropolitan areas in the world, MCMA is fragmented in multiple ways. Local governments exercise their functions, provide services, and manage their public finances autonomously. Allocated sources of revenue and spending responsibilities are the same across municipalities, regardless of their size or administrative capacity. But there is a special case: Mexico City proper, the capital city, has more taxing powers than any other state or municipality in the country. Revenue needs vary with urban dynamics, sociodemographic structure, geographic location, and other factors. This paper depicts a geography of financial condition in MCMA. The diagnosis of its aggregated budgets confirms substantial dependence on federal transfers and poor financial autonomy. Public investment has fallen, while debt has increased. There are clear fiscal disparities among jurisdictions, especially between the urban core and the periphery.

The categorization proposed in this paper shows that the financial condition of most metropolitan municipalities is fragile or unstable, while Mexico City proper is better positioned. The map of financial condition reveals that the central city has been able to financially outperform its suburban municipalities. Small municipalities, especially those on the periphery, are classified as highly vulnerable or financially weak. Several highly industrialized municipalities with large populations in the vicinity of Mexico City proper have unstable finances. With such disparities, significant differences in the level and quality of the public services provided are also expected.

Discriminant analysis provides some early answers regarding the socioeconomic factors influencing spatial differences in local financial condition. Economy and population size account for the classification of most municipalities, with the exception of the most vulnerable. These results are conditioned by variations in other factors, and further research is needed to study these. A deeper look at the different fiscal regimes of Mexico City proper and its municipalities (i.e., variations in their taxing powers) might be important in this regard. However, as the fiscal regime is the same across all of the metropolitan municipalities, this would not change the suburban geography of financial performance much. Similarly, municipalities have comparable institutional and political limitations with respect to collecting own revenue. In addition to their own particular expenditure needs, financial sustainability (leverage) is a variable worth investigation, as borrowing has been increasing and municipalities manage their debt differently. The evolution over time of the depicted geography is also worth looking at.

The geography of MCMA’s financial condition and its generalized poor financial health shows how the absence of metropolitan fiscal arrangements make a metropolitan-wide scheme necessary if the metropolis wishes to improve its overall performance. Huge resources are needed to maintain a competitive metropolis with adequate public services. It is good sign that the central city has a financial regime close to the desirable fiscal model for metropolitan areas, concentrating the fiscal powers of municipalities and states. The large tax base in MCMA could make a significant contribution to its financial performance if the revenue potential were adequately tapped by local governments. However, most municipalities struggle to adjust to existing fiscal structures and face financial pressure to provide services and fulfill their duties. Peripheral municipalities and those with above-average spending needs require special attention from researches and policy makers.

The institutional, administrative, and fiscal conditions prevailing in MCMA have revealed their limitations regarding the effective management of fiscal imbalances and other financial issues. Fragmentation and poor coordination are the main obstacles to adequate governance. While voluntary intermunicipal cooperation and other mechanisms do exist, metropolitan governance and financing have made uncertain progress. Managing metropolitan fiscal relations and disparities without a unifying structure is not simple, and extensive fiscal reforms would be required to substantially improve financial efficiency and equity. Improved capacities and incentives, and a metropolitan governance model that establishes fiscal institutions promoting the equitable provision of services at reasonable financial cost are also necessary. Metropolitan arrangements that include adequate principles of financial efficiency, fiscal decentralization, and equalization will continue to be challenging because reform ultimately requires multilevel governmental effort, political compromise, and the agreement of taxpayers and citizens.

Supplemental Material

sj-pdf-1-lec-10.1177_02690942211060478 – Supplemental Material for The geography of financial condition in the Mexico City metropolitan area

Supplemental Material, sj-pdf-1-lec-10.1177_02690942211060478 for The geography of financial condition in the Mexico City metropolitan area by Alejandra Trejo-Nieto in Local Economy: The Journal of the Local Economy Policy Unit

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.