Abstract

In recent decades, the craft beer sector has grown rapidly, and it has been studied across the world through various lenses. In Norway and Sweden, the sector is a well-established complement to large-scale beer producers, but it has yet to be thoroughly studied. Previous studies show that the location of a brewery is important in terms of marketing and branding approaches, but also that craft brewers contribute to place development. The aim of this study is to explore how context affects the possibilities of craft breweries to contribute to local place development. The study results are built on a web-survey, answered by 201 craft beer brewers in Norway and Sweden. The findings show that brewers, especially those located in rural areas, struggle under tough conditions regarding profit margins, as well as troublesome and limiting legislation. Place is considered very important, but breweries in rural areas use place-connection to a higher extent. Tourism is important, especially for breweries located in rural areas, and changes in regulation could increase the importance even more. The results of this study show that there exist contextual differences which also have an impact on the extent to which the brewers can contribute to their local community.

Introduction

In the pre-industrial period, a brewery was something that existed locally and on a small scale (Liu et al., 2018). However, aspects such as technological advances in production, more efficient transportation and mass marketing led to the industrialisation of beer brewing in the 19th century (Cabras and Higgins, 2016). The tendency towards large-scale production and internationalisation of the brewing industry continued into the 1990s when the number of larger breweries fell dramatically all over the world, and microbreweries became more and more common (Garavaglia and Swinnen, 2018). Some date the turning point of these changes in the beer sector to the 1980s or even the 1970s, with the craft beer revolution starting to change the production and consumption of beer (Fastigi et al., 2018; Garavaglia and Swinnen, 2018). This development has since taken place in countries like the U.S., the U.K., Italy (Fastigi et al., 2015) and other parts of Europe (Garavaglia and Swinnen, 2018), South America (Toro-Gonzalez, 2018) and China (Li et al., 2018). Scholars have studied the growth of the sector through various perspectives since the early stages of this transformation (Nave et al., 2022; Shears, 2014). One of the topics that has gathered the attention of scholars is the relevance of place. A distinguishable example of this is Gatrell et al. (2018), pointing out the importance of the sector’s entrepreneurship and its connection to local place development: (Gatrell et al., 2018: 363). Argent (2018) highlight the positive role of craft breweries in place development not only through its contribution to social, symbolic and financial capital, but also by its strengthening of local tourism; Argent also points to the value and use of place in terms of marketing and branding approaches. This means that craft breweries and place are knit together, as breweries use place specifics and attributes to distinguish themselves in various ways (Argent, 2018; Sjölander-Lindqvist et al., 2019), and places benefit from effects such as marketing, craft brewery tourism and real estate development (Alonso et al., 2017; Argent, 2018; Cabras and Bosworth, 2014).

For many people, Norway and Sweden may not be considered to have a well-known beer tradition and culture. However, the two countries contain a rich and lively brewing tradition, which, like many other countries, has followed this rapidly transformed craft brewing sector (Halkier et al., 2017). This transformation has come to change the brewing sector and in the last 30 years the number of breweries has increased sharply in Norway as well as in Sweden (Brønnøysundregistrene, 2020; Statistics Sweden, 2021a). Previous research argue that the craft beer movement opens up new platforms for local economic development, especially, in highly rural contexts (Sjölander-Lindqvist et al., 2019; Skoglund, 2019). However, different alcohol policies in the Nordic countries, where Norway and Sweden in particular are disadvantaged due to strict rules regarding distribution and high alcohol taxes, give an indication that opportunities for creating economically sustainable breweries are more limited for brewers in Norway and Sweden (c.f. Williams, 2017). Furthermore, since previous research show that rural areas often are exposed to greater challenges (Korsgaard et al., 2015) spatial aspects should be taken into account, concerning where in the country the breweries are located, that is, in urban or in sparsely populated areas.

The overall aim of this study is to explore how context affects the possibilities of craft breweries to contribute to local place development through their entrepreneurial endeavours. The study investigates whether brewers in rural areas face different challenges compared to those in more urban settings and whether or not this affects the tendency to use place as a measure in the business idea. The study attempts to sort out possible differing characteristics and features of craft breweries depending on contextual conditions, and in terms of performance and objectives for contributing to local place development. This implies comparison of breweries that are located in sparsely populated regions, (i.e. rural areas) with those that operate in larger and more populated places. More precisely, this study is guided by two research questions: (1) What kind of differences in character are identifiable between rural craft brewers and brewers operating in more populated areas in terms of performance, growth ambitions and perceived obstacles? and (2) In what way do the contextual prerequisites effect the breweries’ contributions to local place development?

This study intends to strengthen the knowledge of the craft beer sector by attempting to identify if and how contextual differences influence the capacity of brewers to contribute to local place development in their regions. With Norway and Sweden having experienced a rather simultaneous and recent craft beer sector development, there is also a need for more contributions to the research agenda on craft beer on the Scandinavian peninsula. Hence, this study of the Norwegian and Swedish craft beer sector builds upon the earlier country accounts (see, for example, Garavaglia and Swinnen, 2018; Patterson and Hoalst-Pullen, 2014), and can be seen as a continuation of these.

Craft beer – Definitions and research frontiers

What is craft beer?

‘Microbrewery’, ‘brewpub’, ‘artisanal brewery’ and henceforth ‘craft brewery’ are terms referring to a new kind of production in the brewing industry contraposed to the mass production of beer, which has started and been spreading through almost all industrialised countries in recent decades (Garavaglia and Swinnen, 2017: 4; Nave et al., 2022). The background to the craft beer revolution, which many claim to have started in the U.S., can be found in aspects such as reduced government regulations (Elzinga et al., 2015), interest in less homogenous and more locally distinct flavours (Flack, 1997; Gatrell et al., 2018), interest in pairing food together with beer (Bamforth and Cabras, 2016) and increased income levels (Barajas et al., 2017). Even though the terms above are similar and often refer to the same thing, there is an ongoing discussion about what it is that characterises the craft beer sector (Fillis, 2004). For example, a microbrewery is often defined entirely by size, but can, if it meets other criteria, be considered as a craft brewery. These criteria are, however, hard to unify in a commonly accepted definition, and Morgan et al. (2020) therefore argue that it may even be easier to define what craft beer is not, than to define what it is. Still, there are a number of common criteria often used in definitions of craft beer, such as size (Fillis, 2004), the balance between automation and ‘hands on process’ (Dahm and Mathur, 1990; Rice, 2016), high gravity dilution (Watt and Dickie, 2013) independent ownership (Brewers Association, 2021), ingredients (Bogdan and Kordialik-Bogacka, 2017) and creativity and innovation (Gatrell et al., 2018). Recent research confirms that there still is no universally accepted definition of what craft beer is (Baiano, 2021; Nave et al., 2022), and Morgan et al. (2020: 925) summarise the craft beer sector as follows: ‘Craft beer is certainly not mass produced, and it is difficult to associate craft beer with multinational brewing and the organisations who produce mainstream beer. Craft beer is perceived as “honest” and uncompromising in terms of flavour but may be either traditional or modern. Craft beer is made using traditional brewing processes and uses the best quality raw ingredients with adjuncts included to enhance the flavour and experience not to reduce cost’.

Continuing on this topic, Jahrn et al. (2017) claim that there exists a consensus between producers that highlights the fact that central to becoming a microbrewery is a specific mentality and approach to the brewery process: experimentation, flexibility, focus on quality, passion for craft and customer focus. This means that the borderline in the industry is continually negotiated, and the concept of craft beer rather underlines the kind of production, rather than the firm’s size.

In this study, we use the definition of craft brewery focussing on volume of production, independent ownership and the kind of production. This is based on the Norwegian Brewery and Beverage association which in 2017 defined ‘small-scale producers’ as firms with a total volume of production below 3 million litres (Bryggeri- og Drikkevareforeningen, 2023). This is the same as the Swedish organisation for ‘independent breweries’ (Föreningen Sveriges Oberoende Småbryggerier, 2020). We also include the American Brewers Association’s definition that states that craft breweries are small, independent (less than 25% owned by a brewing industry actor), and use traditional yet innovative brewing methods (Brewers Association, 2021).

Previous research in the craft beer sector

While craft beer is becoming increasingly popular in many countries (Garavaglia and Swinnen, 2017) the research interest in the area has increased dramatically as well and there is a vast and varied literature on craft beer (Baiano, 2021; Nave et al., 2022). A recent overview divides articles on craft beer into seven general themes, including definitions, fiscal policy, innovation, safety, health, consumer knowledge and sustainability (Baiano, 2021). Another article identified four main themes: industry and market, marketing and branding, consumer behaviour and sustainability (Nave et al., 2022). Dodd et al. (2021) elevate how various types of capital, such as economic, spatial, cultural, social and symbolic, contribute to the potential success and growth of the sector. Esposti et al. (2017) studying the importance of agglomeration economics for the sector in an Italian context, claiming an overemphasis on such spatial factors for craft brewery development. Recent studies highlight the use of traditional methods in the production of commercial beer (Bråtå, 2017). Other studies point out logistics and transports as important for craft brewers (Sjölander-Lindqvist et al., 2019; Skoglund, 2019), alongside factors as producers working in networks, using alternative funding sources and having jobs on the side in order to keep their breweries in business. Jahrn et al. (2017) have undertaken a qualitative study on cooperation and competition among young and small-scale breweries. In an attempt to establish research needs in the social science dimensions of the craft beer sector, Withers (2017) divide previous research into three categories; (1) space, place and identity; (2) production, markets and consumer culture; (3) tourism perspectives and sustainability. At the same time, Withers point out a need for more research on the status, authenticity and cultural capital within craft beer culture; sustainability perspectives of production; as well as race, class, gender and sexuality dimensions surrounding the same culture. Smith et al. (2017) claim that the dimensions of consumer behaviour, tourism, local impact and commercial development of craft breweries are relevant for further studies in the sector. Previous research demonstrates how entrepreneurial activities are strongly influenced by the context where they occur and that entrepreneurs in rural areas ‘leverage their placial embeddedness and non-local strategic networks to create opportunities’ (Korsgaard et al., 2015: 594) (Korsgaard et al., 2015: p. 594).

Craft breweries and the importance of place

The impact of craft brewing on local, regional and place development has been studied by scholars from various perspectives. These studies tend to elevate how craft breweries often collaborate locally with other craft breweries and food producers in order to resist large industry domination and to stay independent, thereby often deviating from the traditional and more aggressive growth strategies, applied in a lesser degree among craft breweries than in other business sectors (Cabras and Bamforth, 2016; Cunningham and Barclay, 2020; Nave et al., 2022). The place orientation in earlier craft beer studies is often connected to neo-localism; exemplified by customers’ interest and desire for the local and authentic, in elevating local place names by using them in branding and marketing (Eberts, 2014; Flack, 1997), or in spatial branding as a measure for competitiveness (Gatrell et al., 2018; Lane et al., 2016). Argent (2018) pinpoints the large focus craft brewers have on contributing to local place development, and Cappellano et al. (2023) even labels some breweries ‘local development agents’ due to their intense local community engagement. Argent (2018) also stresses how place is important in terms of marketing and branding, as well as how craft brewers aim to contribute to local tourism. The tourism perspective is rather widely studied, from stakeholder theory analysis (Alonso et al., 2017), to craft beer routes (Csapó and Wetzl, 2016). Other studies, such as Fletchall (2016) and Nelson (2021), connect how the experience of authenticity is often increased by brewery visits among tourists, thereby also highlighting the relation between neo-localism and tourism.

Previous studies also suggest that craft breweries and pubs sometimes take the lead in reviving run-down neighbourhoods by attracting tourists, providing community meeting places and also adding value to real estate (Cabras and Bosworth, 2014; Florida 2017; Reid, 2018). Regarding the value of the craft beer sector for place development, Miller et al. (2019) found that value chains in the craft beer sector generated nearly 500 million USD to Michigan’s economy, and several studies highlight that a reduction in taxes and fewer regulations could be used as measures to further increase the economic impact of the craft beer sector (Elzinga et al., 2015; Malone and Lusk, 2016; Williams, 2017). Similar studies on craft beer have been undertaken in Scandinavia, although research efforts have been scarce.

The growth of the craft beer sector in Norway and Sweden

Sweden and Norway have a long tradition of beer brewing, and in the past, many local farms have had their own breweries (Faxälv and Olofsson, 2007; Maehle, 2021). Furthermore, the two nations’ craft brewing industry has, over the last decade, experienced an expansion, similar to the rest of the world. Box (2017), and Halkier et al. (2017) argue that there is a renewed interest in local beer and local products in Scandinavia. Maehle (2021) points out how rapidly the Norwegian craft beer sector has grown since the beginning of 2000, identifying shifting consumer demand towards unique, local flavours as the main underlying factor for this shift. The first craft brewery in Norway was established in 1989 (Maehle, 2021), and since then, the sector has grown rapidly to about 300 in 2020 (Brønnøysundregistrene, 2020). Historically, the industrialisation of the brewing sector in Norway have been centred around a few large breweries, with Ringnes and Hansa Borg accounting for 86% of the entire beer market in the country. From the 1990s, a distinctive growth in the number of Swedish breweries begun and the number of Swedish breweries was about 500 in 2020. Of these, only two were larger companies with more than 100 employees in 2020, while about 73% run their businesses without any employees (Statistics Sweden, 2021a). Most of the breweries are located within Sweden’s three biggest cities, Stockholm, Gothenburg and Malmö. However, two of the country’s very sparsely populated regions, Gotland and Jämtland, have the highest number of breweries per 100,000 inhabitants (Beernews, 2018).

Among the Nordic countries, Sweden, Norway and Iceland have the most stringent legislation relating to the distribution of alcoholic beverages (Maehle, 2021). The milder regulations in Denmark and Finland allow people above a given age to buy alcoholic beverages, such as beer, wine and spirits, in grocery shops (Hallencreutz, 2018). Different rules for producers within EU countries are problematic, not least from a competition perspective, and previous research shows that policies on economy, such as taxation and legislation ‘may have a marked influence on the processes and outcomes of new and established businesses’. (Ribeiro-Soriano and Galindo-Martín, 2012: 861). The purpose of business regulations is primarily to promote entrepreneurship; however, it has long been known that there is a need ‘for innovation as a rationale for government involvement in entrepreneurship’. (Michael and Pearce, 2009: 285). In ‘managed economies’ (see Audretsch and Thurik, 2001), growth policies are designed at a national level, which creates policies regardless of local needs. The trend towards more entrepreneurial economies, however, calls for policies to be developed locally according to Murdock (2012). Despite the fact that Sweden is considered a representative of the ‘new entrepreneurial economy’ (Murdock, 2012: 887), it seems that the regulation of the brewing industry in Sweden, as well as in Norway, still follows the older, national policy, that is, a lack of policies adapted to regional conditions.

There are several reasons making the Scandinavian context particularly interesting to study as many factors (climate, alcohol legislation and policy, culture, funding options etc.) are similar, and distinguish the countries from other context. In addition, there are some internal nuances (e.g. regional policy, access to market), which allows for an even more detailed assessment of motivation, drivers and barriers to growth. Our study thus compliments previous research which highlights the importance of place in understanding the development within the craft beer industry (Argent, 2018; Gatrell et al., 2018).

Method

Survey design and data sampling

This study is based on a web survey, aiming to address the research opportunities identified by the literature analysis (Argent, 2018; Korsgaard et al., 2015; Williams, 2017). The survey was distributed in 2020 to 579 craft beer breweries in Norway and Sweden. Questions in the survey were a combination of straight quantitative questions, qualitative open-ended questions and statements where respondents could answer on a 5-point Likert scale to extract their views. The questions in the survey were inspired by previous research, se below, and were developed jointly by the author group in December 2019, that is, before the Covid-19 pandemic.

Through the use of statistical and public industry coding (SNI 11.050 ‘Production of beverages: production of beer’), 512 breweries in Sweden were identified as matching the industry code. Eventually, the survey reached 374 Swedish breweries, since some of them were no longer active or did not provide contact information. In total, 146 Swedish firms responded to the survey, resulting in an overall response rate of 39%. In Norway all craft beer breweries (code 11.050 Production of beer) were approached using the Norwegian official list of 301 breweries (Brønnøysundregistrene, 2020). After excluding businesses that no longer existed or lacked contact information, the survey was sent out to 205 Norwegian breweries. On the Norwegian side of the border 55 breweries responded, corresponding to a response rate of 27%. On aggregate, the data thus consists of 201 Swedish and Norwegian breweries and a total response rate of 35%.

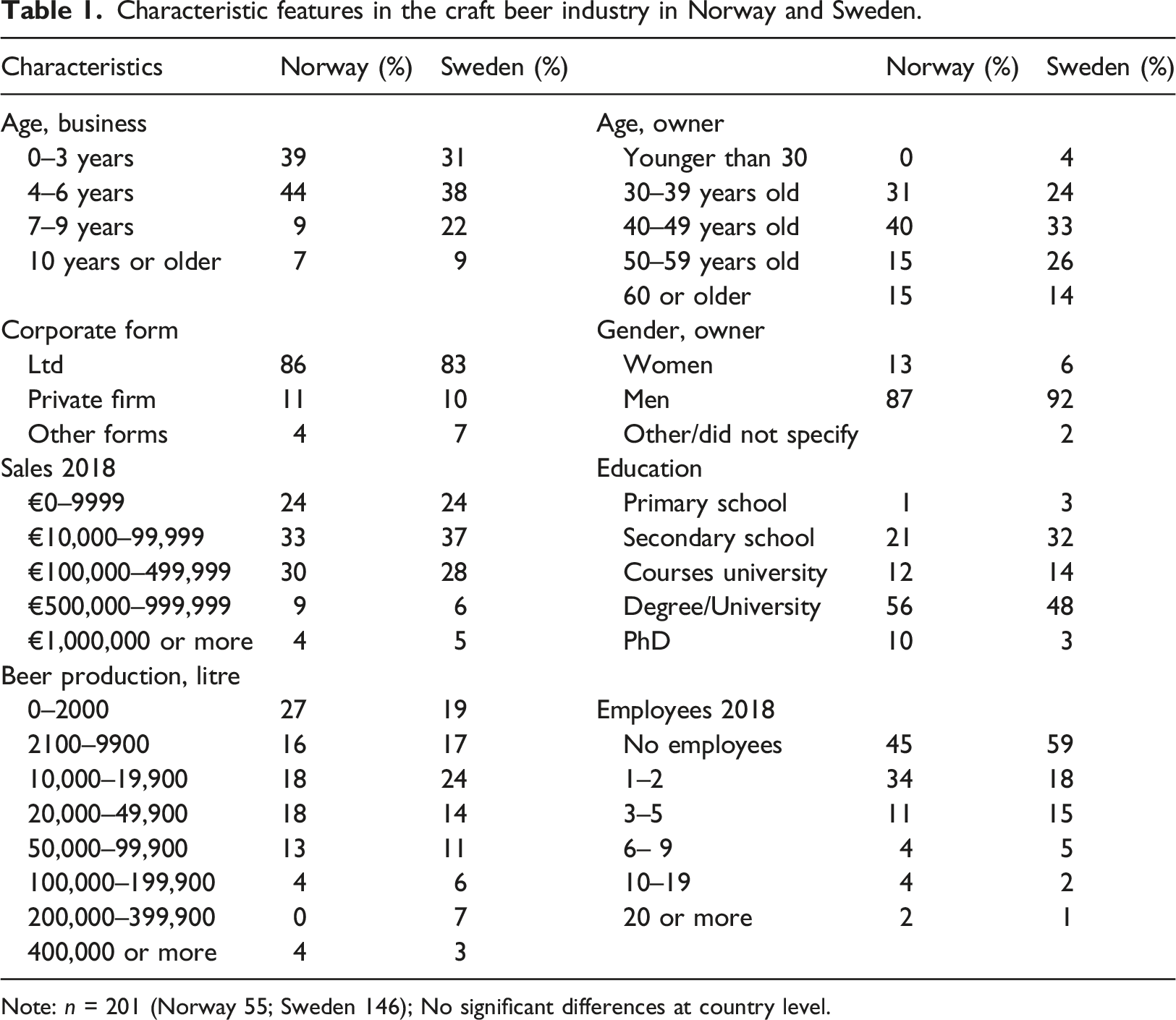

Characteristic features in the craft beer industry in Norway and Sweden.

Note: n = 201 (Norway 55; Sweden 146); No significant differences at country level.

Operationalisation and data analysis

The survey had five themes: (1) Information about the brewery (Garavaglia and Swinnen, 2018) (2) Motivation (drivers) to start/run a craft beer brewery (Olson et al., 2014), (3) Administrative and financial enablers in the process of starting a craft beer brewery (Cardoni et al., 2018), (4) Ownership and partners (Garavaglia and Swinnen, 2017) and (5) Marketing and place attachment (Eberts, 2014).

In order to investigate whether there are differences between rurally located breweries and others, we divide the data depending on where the breweries were located. This was done using the question: Where is the brewery located?

The nature of the term rural varies from place to place, and in a simplistic way, rural is any area that is not urban. Woods and McDonagh (2011) criticises the dichotomisation and underlines the different kinds, or degrees, of rurality, from fairly populated areas with extensive cropland to less-densely settled areas. Rural areas change over time due to economic factors (tourism income, farming profitability, primary sector jobs), environmental factors (land use, pollution, conservation) and social factors (population change and migration, leisure time, retirement population) (FAO, 2018). In this study, the access to or distance from a market is a crucial factor. Ideally, all breweries should be located close to towns or densely populated areas, but in spite of this, a large number of craft beer companies are located in the countryside (Beernews, 2018). The way that contextual factors constitute both obstacles and possibilities are at the core of this study.

In this study we define rural areas as settlements with fewer than 3000 residents. This categorisation is in accordance with the Swedish Agency for Growth Policy Analysis (Glesbygdsverket, 2007), and hereafter used to analyse the empirical findings of the study.

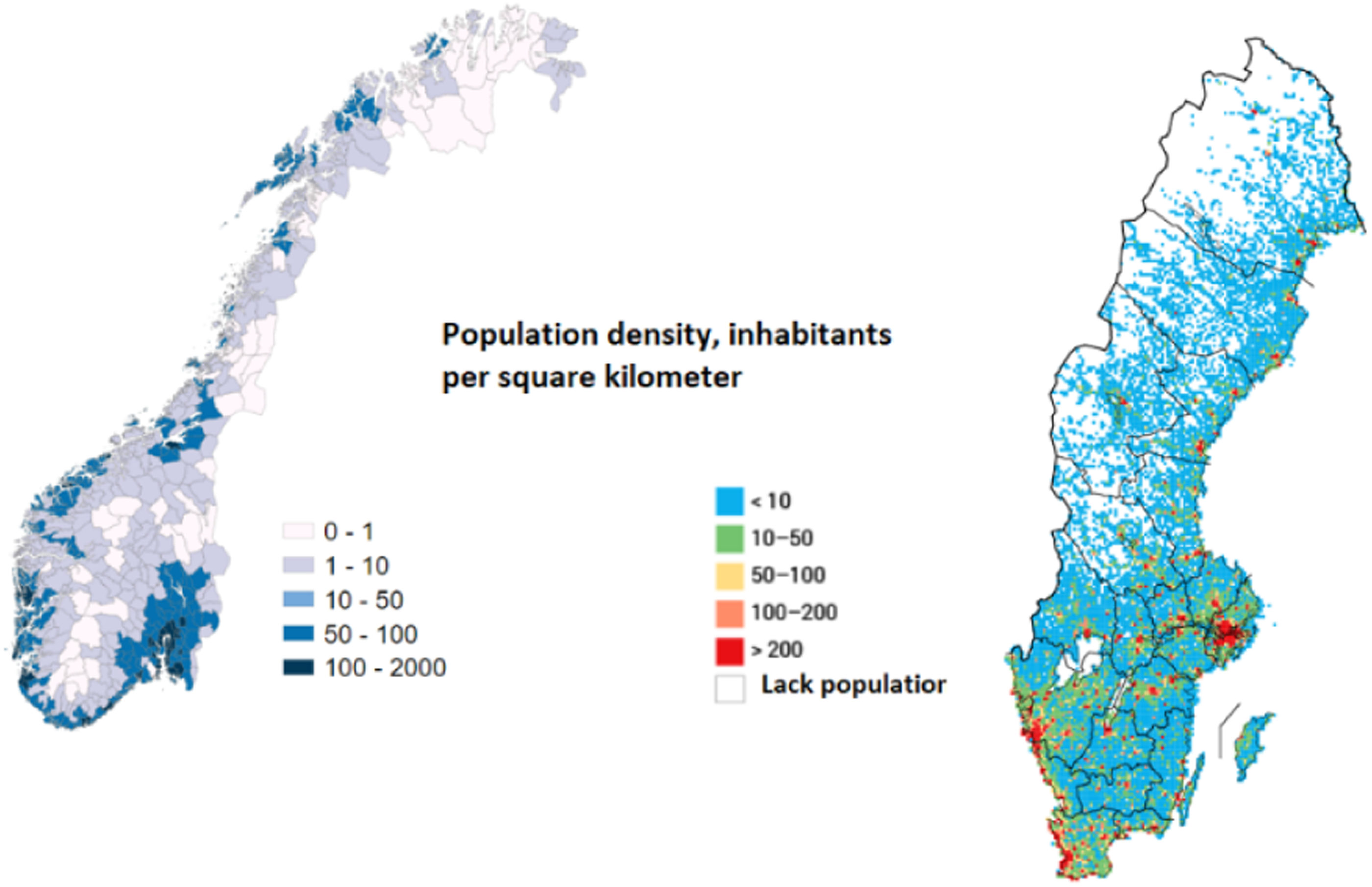

Sweden, like Norway, mostly consists of sparsely populated regions. There are approximately 10.5 million inhabitants in Sweden and 5.3 million in Norway, and both countries have few cities with more than 50,000 inhabitants. On average, the population density in Sweden amounts to 25.2 inhabitants per square kilometre, and in Norway there are 17 inhabitants per square kilometre (Figure 1).

In order to explore the breweries’ attitude and contribution to local place development various issues were investigated. One question was: To what extent did the following statement influence you to start the brewery? I wanted to contribute to the local community. A five-point Likert scale was used where 1 = Very low impact, to 5 = Very high impact.

Another, open-ended question, was: What motivated you to start selling your beer on the market? This question was analysed through thematization, and different areas were identified related to economy, market supply, demand, self-appreciation as well as a desire to contribute to the place where the brewery was located.

The breweries’ contribution to place development, or place attachment was investigated through the following question:

To what extent is local anchoring used in the following processes in the brewery?

A five-point Likert scale was used where 1 = Never used, to 5 = Often used

The survey data was processed in SPSS, in which descriptive frequency analysis techniques and correlation analysis techniques were used to analyse the data. In order to identify significant differences between the Rural breweries, compared with the Others, the Mann–Whitney U-test was employed. Mann–Whitney U-test is a non-parametric test that is used instead of t-test when the variables are on an ordinal scale level (1–5).

In the findings section, quotes from the brewers have been included in order to underpin and clarify some of the quantitative results. The quotes are taken from the open-ended questions in the survey. Appendix 1 shows characteristics of the cited brewers (B1, B2, etc.).

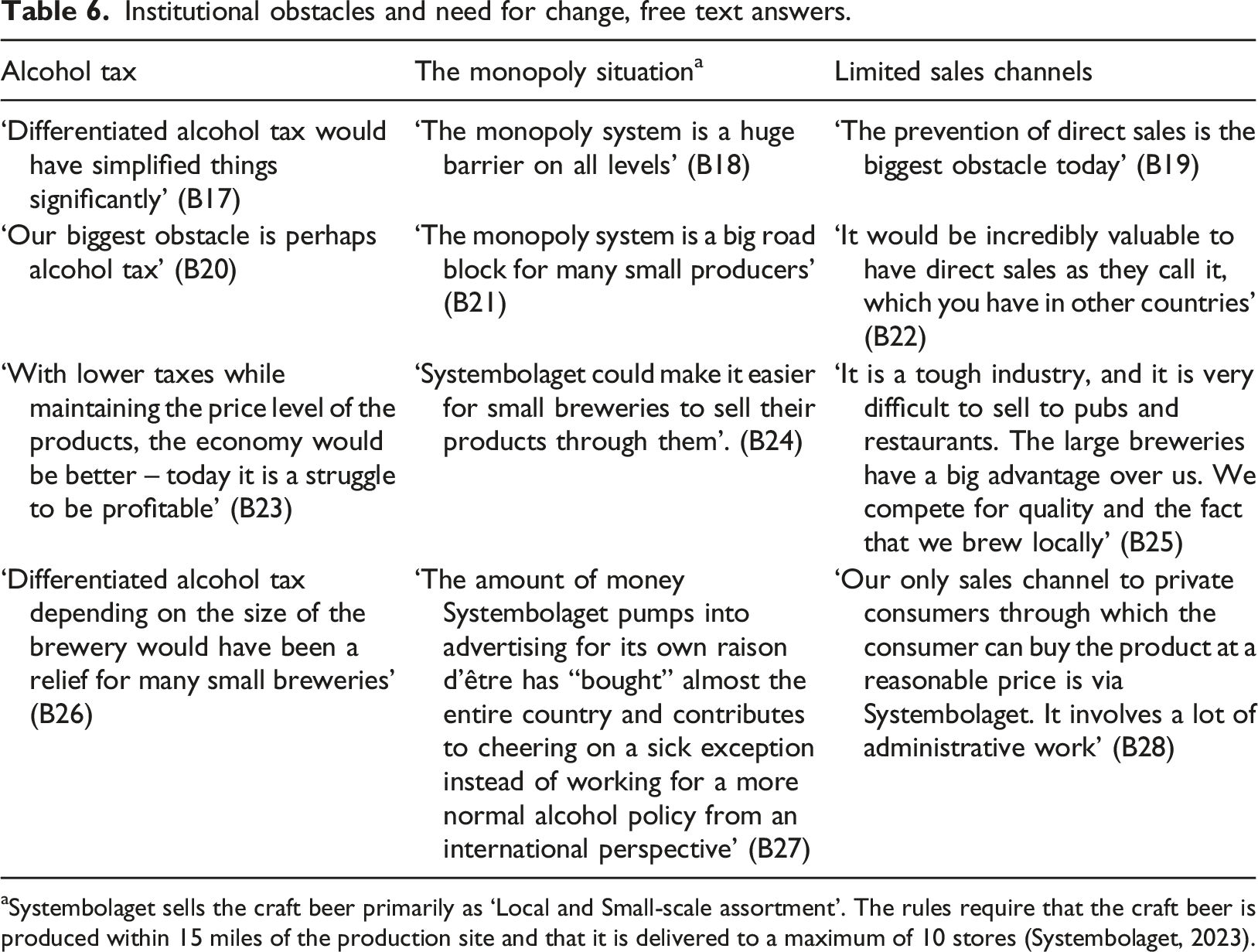

The final question in the survey concerned the brewers' everyday life: ‘What knowledge about obstacles and opportunities in the craft brewing industry do you think needs to be brought forward?’ The thematizing of the question, highlight the strictly regulated market that the brewers in Norway and Sweden operate within, including the monopoly situation, high taxes and the limited sales channels (Table 6).

Craft breweries in Norway and Sweden – Study results

Location of the breweries

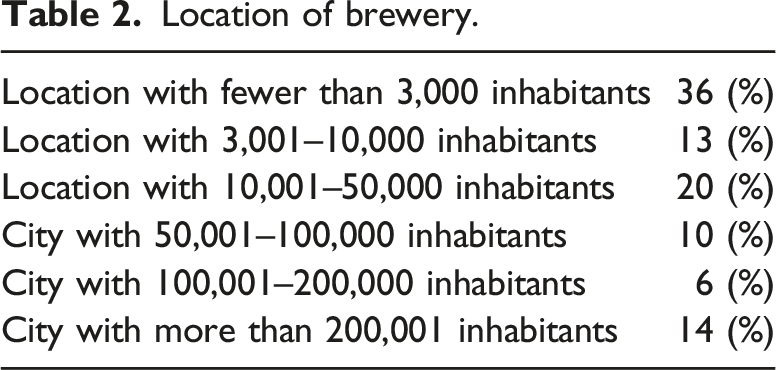

Location of brewery.

Henceforth, the focus in the study is on comparing the characteristics of the rural microbrewery entrepreneurs with those who run businesses in communities with more than 3000 inhabitants.

Differences between locations

Age of brewery and location.

Note: Significant at: ** p < .01.

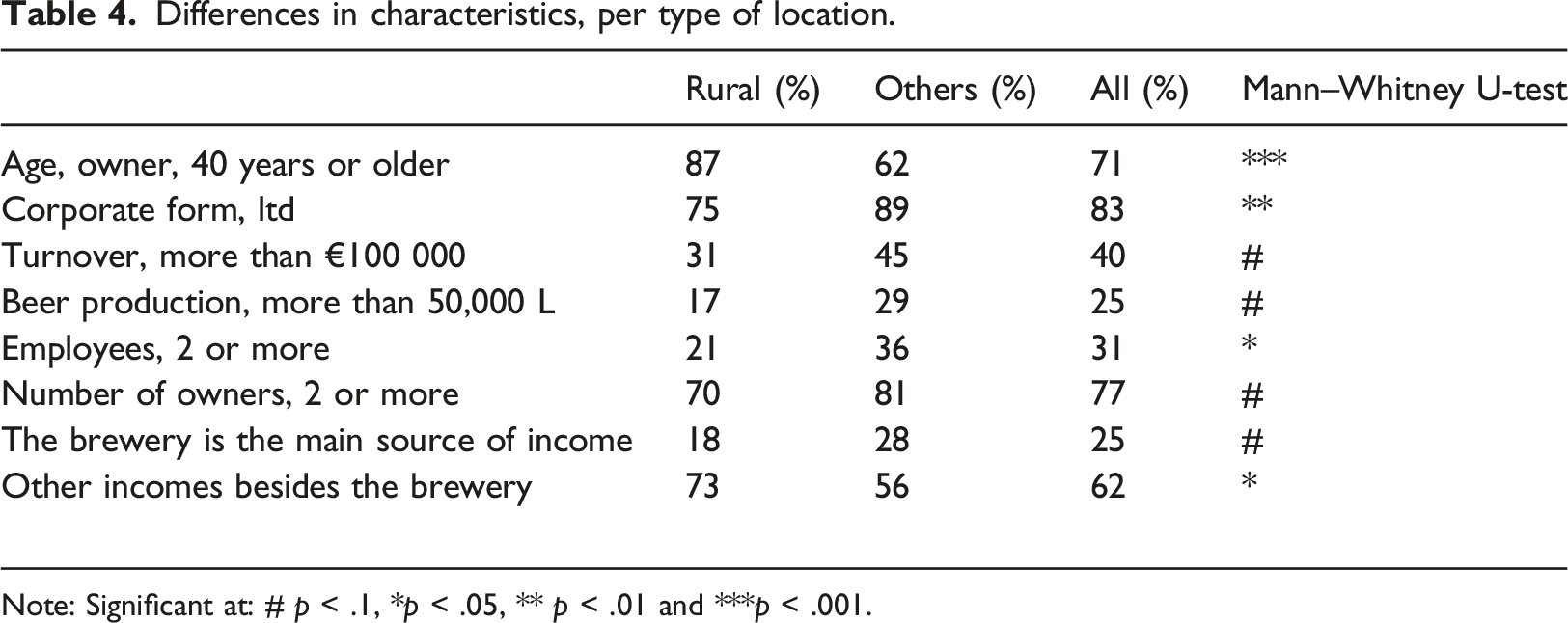

Differences in characteristics, per type of location.

Note: Significant at: # p < .1, *p < .05, ** p < .01 and ***p < .001.

Firstly, the rural brewers are slightly older with an average age of 51 years compared to 47 years. This difference can however mainly be explained by the difference in newly started breweries (0–3 years). If a comparison instead is made between breweries that are older than 3 years, rural brewers are still somewhat older, but the differences are not significant. Secondly, the breweries are mainly (83%) operated as limited companies, but as shown in Table 4, there are significant differences between the rural breweries and the more urban ones. Rural breweries are operated as private firms to a higher degree (18% compared with 6%). Thirdly, most breweries are very small, in terms of both turnover and the number of employees. This also means that the majority (62%) have additional sources of income other than the brewery. Regarding the number of owners, 77% of the respondents state that they own the brewery together with someone else, that is, only 23% own the brewery themselves. This is quite remarkable, since solo-entrepreneurship otherwise is the most common ownership form in other industries. Population density in Norway and Sweden. Source: Statistics Norway (2021); Statistics Sweden (2021b).

As shown above, and in Table 1, the vast majority of the breweries are small. For example, only a quarter of the breweries produce more than 50,000 L per year and about half of all the breweries have no employees, whether rural or ‘others’. Furthermore, the majority of the brewers’ state that they cannot support themselves on the income from the brewery.

Figure 2 shows significant differences between rural brewers and those in more urban areas in terms of whether the brewery is the main source of income (p < .1). 75% of the brewers in rural areas state that the brewery is not their main source of income – they instead need to have additional sources of income. 28% of brewers who operate in more urban locations state that the brewery is their main source of income, compared with just under a fifth (19%) of brewers in rural areas. The brewery is the main source of income*.

Entrepreneurial motives – Perspectives on economic growth and location

The majority (92%) of the breweries have launched their products on an open market. Those who do not retail their beer specify in the open responses that they only produce and sell the beer in their own pub, or that they are in the process of launching the beer commercially but that it takes time due to rules and bureaucracy. ‘I brew beer and sell it in my own pub. The sale of bottled beer requires a separate permit and a separate room with a separate entrance’ (B1); ‘It has taken a lot of time and money to refurbish and rebuild the brewery because we did not get the loans we needed, so we can only complete it at the rate we earn our own money, which means that it takes a lot of time’ (B2).

The majority of the breweries, regardless of location, (82%) were established on the basis of the owners' passion for beer brewing and were initially run on a hobby basis (75%). ‘We had been a hobby brewer since the beginning of the 21st century and simply wanted to start a brewery so that more people could taste our products’. (B3). ‘The hobby grew, and the beer thus needed to be sold’ (B4).

The following word-cloud (Figure 3) represents scaled phrases (according to sampled responses) to the question ‘Why was the brewery commercialised?’, Reason why the brewery was commercialised (Survey January, 2020).

The qualitative free text answers to this question show that the most common theme is about financial issues (economy, money, survival etc.). ‘Of course, you need to sell your beer on the market, otherwise it is hardly a brewery you have …’ (B5), or; ‘In order to create a sustainable brewery/company, this was absolutely necessary’ (B6). As many respondents point out, commercialisation of the company’s products is necessary to survival. However, many of the respondents also highlight other reasons why they introduced themselves to the market, and one of these is about their own product: ‘We quickly got a high quality of beer and felt confident in investing’ (B7); ‘We wanted to delight others with the good beer!’ (B8). A lot of brewers highlight the product from a customer perspective: ‘People wanted to buy our beers!’ (B9), and ‘We did home brewing for many years and were asked by those who tasted our beer why we did not start a brewery’ (B10). Some breweries, especially those located in rural areas, highlighted a local perspective as a reason for commercialising the brewery. ‘I wanted to develop the countryside’ (B11) or ‘I want to offer locally produced quality beer to customers in the region’ (B12). Finally, there were brewers’ that, pointing to the passion, expectations and excitement about how the market will accept and perceive the artisanal product, that is, about

The rural brewers highlight to a greater extent the local community as a reason why the brewery was commercialised. The desire to contribute to the local community seems, however, to be high regardless of location. 61% of the breweries argue that one reason why they also started their brewery is an ambition to contribute to the local community. In summary, the respondents highlight both extrinsic (financial and demand) as intrinsic (the product, the place and self-esteem) motivations for commercialising the brewery (Olson et al., 2014).

Local anchoring and place branding

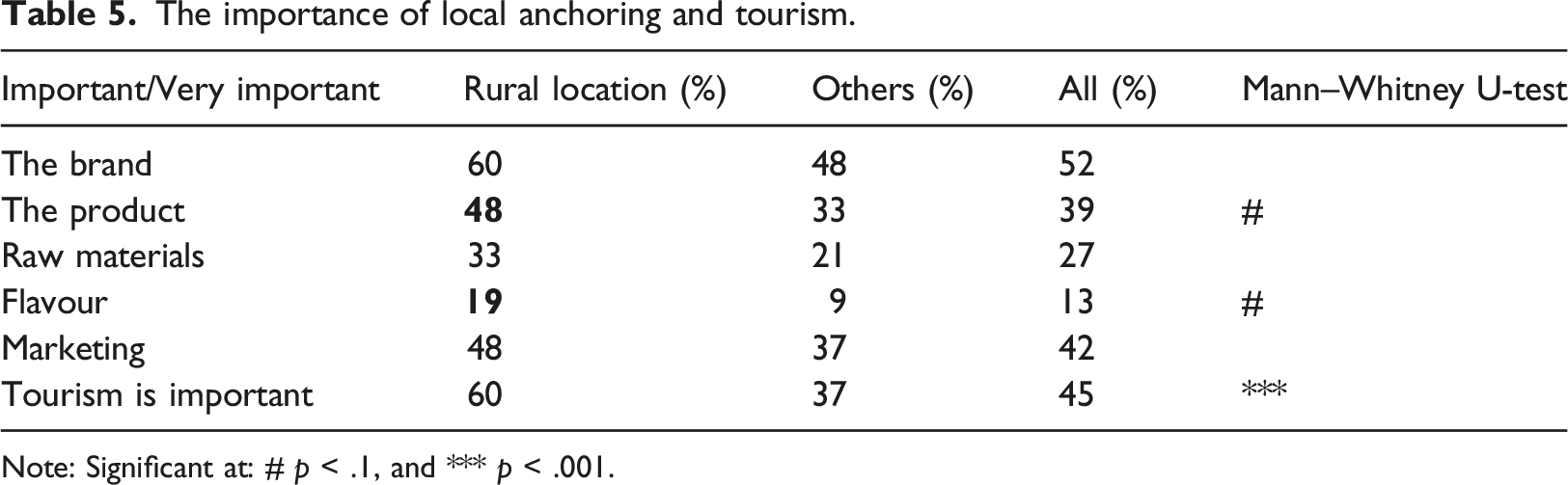

The importance of local anchoring and tourism.

Note: Significant at: # p < .1, and *** p < .001.

Almost half of the breweries (45%) argue that tourism is important or very important. However, the results show significant differences between breweries in rural regions compared to the others. The breweries that are rurally located state to a much higher extent that tourism is important or very important for the brewery (p < .001). ‘As we can sell low-alcohol beer directly to consumers, tourism is very important for marketing, to showcase both the brewery and the place’ B15). However, many breweries do not produce beer with low alcohol content leading to the opinion that tourism not is important for them: ‘Tourism could be important if we had the opportunity for farm sales and tastings. Not many people are interested in visiting a brewery without even being able to taste the beer, or to buy something. With farm sales and the possibility of tasting, tourism could have been extremely more important than it is today. It must become a reality’ (B16). The limited distribution channels are one of the regulations that make up the everyday life of craft brewers, alongside the monopoly situation and the high taxes, see below.

Institutions and ‘regulatory space’

Institutional obstacles and need for change, free text answers.

aSystembolaget sells the craft beer primarily as ‘Local and Small-scale assortment’. The rules require that the craft beer is produced within 15 miles of the production site and that it is delivered to a maximum of 10 stores (Systembolaget, 2023).

In summary – differences between the rural and urban entrepreneurs

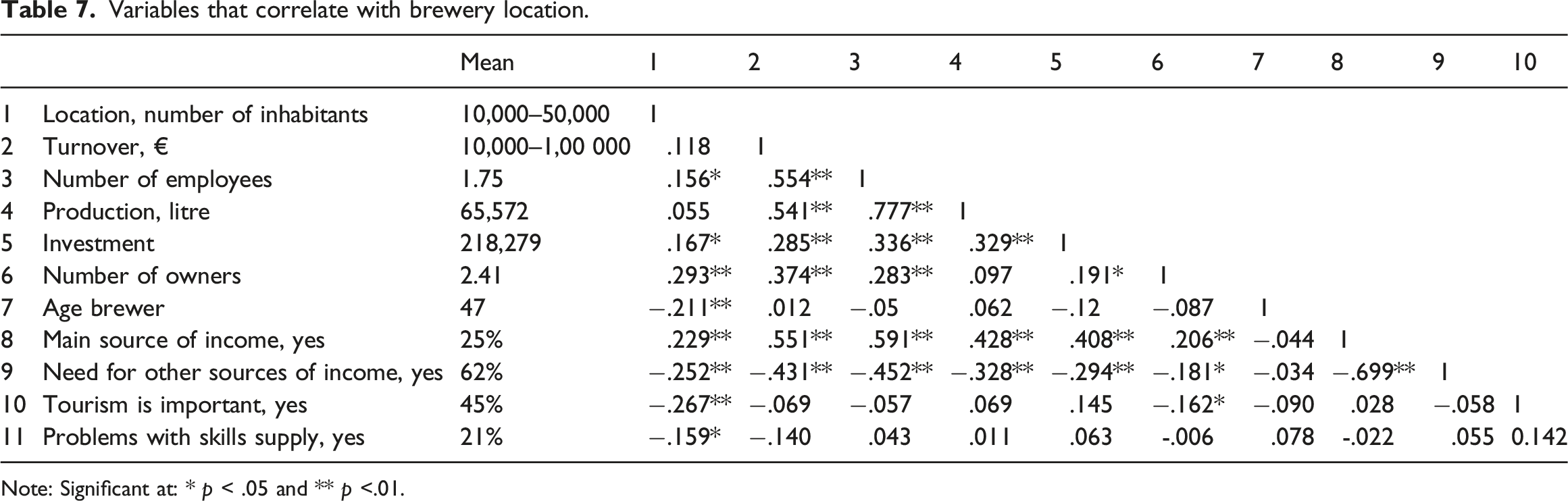

Variables that correlate with brewery location.

Note: Significant at: * p < .05 and ** p <.01.

Discussion

Performance, growth ambitions and perceived obstacles in craft breweries

This study underlines the recent and extensive growth in the number of craft beer breweries in the US, Australia and Europe (Garavaglia and Swinnen, 2018; Gatrell et al., 2018). The increasing consumer interest in quality and craftsmanship opens new market spaces for small firms focussing on the quality of their output (Lane et al., 2016), as well as new forms of entrepreneurship, such as those that transform a passion (i.e. home brewing, see Olson et al., 2014) into remunerative and job-creating economic activity (Fastigi et al., 2015). This study of the Swedish and Norwegian craft beer producers shows the importance of contextual factors, not least those related to policy and tax regulations, as also could be seen in earlier studies by Malone and Lusk (2016) and Elzinga et al. (2015). This study also reveals a high degree of rural location among the breweries, and some general characteristics among these two sparsely populated countries are discussed. Additionally, we highlight the breweries’ characteristics, and identify interesting and significant differences, based on the contextual conditions, and finally we show how contextual prerequisites effect the breweries' contributions to local place development.

Of the total number of craft beer breweries, 36% are in rural areas where there are fewer than 3000 inhabitants, and 49% are in areas with fewer than 10,000. The overall picture, of both characteristics and locations of craft beer breweries, seems to be quite similar between these countries. This can be explained by contextual factors, such as a high proportion of sparsely populated area (also defined as countryside), restrictive alcohol policies and high taxes, common history, and a generally high standard of living. The two Nordic countries have the most regulated laws relating to the distribution of alcoholic beverages (Penttilä and Österberg, 2017). Despite the large number of breweries, half have no employees, and 62% of the brewers have other sources of income. The result from the study shows that the establishment of new breweries, in recent years, mainly has taken place in denser areas. If this is due to the strict legislation, the result, in line with Williams (2017), shows how regulations can inhibit the growth in the craft beer industry.

Craft beer breweries and local place development

Previous research by Flack (1997) and Holtkamp et al. (2016), suggested that neo-localism represents a conscious effort by businesses to develop a connection to place-based attributes of the community, which can, for example, be identified by the use of local names and images, in labelling and marketing, in environmental sustainability and in social and community engagement. In this study the results show that breweries located in rural areas use local connection in the product's name and flavouring to a higher degree. The rural breweries are often smaller businesses, and paradoxically in close proximity to the market, mainly because the market is primarily local. In less-densely populated areas, a common characteristic is that these brewers know each other. They are connected as a community, and many choose to support local activities and businesses. Holtkamp et al. (2016) noted that the highlighting of name and marketing is key to both businesses and customers for developing a sense of place and further engaging with the local community. ‘What makes neo-localism different from local ties in the past is its self-conscious aspect. It is the result of people cultivating local ties by choice, not necessity’ (Schnell and Reese, 2003: 56).

Table 5 underlines the fact that breweries, independent of location, use local naming to a high degree in the branding as well as in the naming of the beers. Reintroducing local heritage to communities through labelling is just one of the ways in which local businesses are trying to reinvent their local identity (Eberts, 2014; Murray and Kline, 2015; Schnell and Reese, 2003). Brand loyalty is important because loyal customers buy more products, are less price sensitive, pay less attention to competitors’ advertising and they help recruit other customers by word-of-mouth (Argent, 2018; Reichheld and Sasser, 1990). The connection to neo-localism and the use of local markers in business operations and marketing also shows a tight relationship with the symbolic capital as highlighted by Fletchall (2016) and Dodd et al. (2021).

Argent (2018) also pinpoints the way that craft brewers aim to contribute to place development by, for example, strengthening local and rural tourism. In this context, or in the case of breweries being used for culinary tourism, a fast-growing niche tourism product – destination loyalty – has been explored to a greater extent than brand loyalty (Argent, 2018; Murray and Kline, 2015). It is partly by focussing on these local themes, connections to local communities, and the overall ties to place that craft breweries have been able to experience their remarkable growth (Cunningham and Barclay, 2020; Schnell and Reese, 2014). The results show significant results in terms of their dependence on tourism. 60% of the brewers in rural areas highlight the fact that tourism is important or very important for their operations. For smaller regions in rural settings, breweries can be a main attraction for visitors and not at least for local residents, and as such contribute to a revitalisation of the neighbourhood through the creation of meeting places (Florida, 2017; Murray and Kline, 2015; Reid, 2018). ‘Tourism is very important for marketing, to showcase both the brewery and the place’ and ‘it could be even more important if the rule were to change’, and ‘Tourism could be important if we had the opportunity for direct sales’.

Conclusions and implications

The aim of this paper was to explore how context affects the possibilities of craft breweries to contribute to local place development through their entrepreneurial endeavours. The results highlight significant differences in character between breweries that are located in very sparsely populated regions (i.e. rural breweries) and those breweries that operate in slightly larger locations. Breweries located in sparsely populated areas are more likely to use local anchoring in branding their products, and they further emphasise the fact that tourism is important. However, running a brewery in a rural area turns out to be challenging. The results show that these breweries have more difficulty compared to those located in more populated places with regard to earning a living, which means that, to a greater extent, brewers need to have other sources of income. Furthermore, breweries located in rural areas correlate negatively with the number of employees and owners, and the size of investments, which means that they are smaller than breweries located in other places. Additionally, the results show that breweries located in rural areas experience greater challenges in terms of skills supply. The results from the study also show significant differences with regards to conditions and outcomes. This finding is consistent with previous results from Korsgaard et al. (2015: 594), who argue that ‘context does indeed impact on entrepreneurial activities’.

More than one third of breweries in Sweden and Norway are located in rural areas. They struggle with low profitability and long distances. Previous research by Williams (2017) shows the negative impact that regulations, such as those that restrict how brewers can distribute and retail their beer, have on the development of the craft beer industry. In recent years, many more breweries have started outside the rural areas, which might be a result of the regulation. Most breweries, regardless of location, highlight direct sales as an opportunity and an important change needed in the strictly regulated brewery market. Breweries located in rural areas would especially be assisted by this change, as they also highlight the importance of tourism. By opening up the market, rural breweries could become more sustainable and thus further contribute to local place development. Reduced alcohol tax, for the very smallest breweries, is another solution suggested by many brewers. However, some also point out the importance of the regulations and the sales through the national alcohol monopoly, wanting to keep some variation of this in any future modifications to the legislation. In line with Murdock (2012: 889), we want to ‘emphasize the difficulty in isolating and measuring the impact of policy’ and we therefore call for more research into the effects of alcohol policies in different countries.

One limitation of the study is that it was conducted when the pandemic was in its infancy, that is, early spring 2020. Recently, research show that the Covid-19 pandemic has influenced the craft brewing sector and that the significant contextual differences between breweries located in rural and urban areas, identified before the pandemic, are continued and have even worsened which further highlights the need for new research in the craft beer area (Cabras et al., 2023). This study has also shown significant differences between rural and urban craft breweries that affect their ability to contribute to local place development in different ways. Hence, this calls for an overview of national support structures for different contexts.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study has partly been funded by the INTERREG Sweden-Norway programme.