Abstract

Unfunded liabilities of pension plans sponsored by state and local governments have drastically increased in the past few years. This article examines the potential challenges faced by states and municipalities in meeting their pension obligations and explores the cost and benefits of a switch from traditional defined benefit (DB) plans to defined contribution (DC) plans. The authors draw on the experience of the private sector to depict the potential cost savings for governments and the likely impacts on employees. The authors also identify several issues that are unique to governments if a shift in pension coverage plans is to occur. One of the attractions of public sector employment has been the generous benefits offered; the authors examine whether it will be harder to recruit people in the public sector if the government does not offer DB pensions. The authors explore equity issues and the effects of eroding political support for public sector DB systems in light of their demise in the private sector. The authors also address the issue of financial illiteracy in the work place and its impact on the human resource function in the context of DC plan implementation. Finally, the authors pose critical questions regarding DC plan rollout and its inherent difficulties.

Introduction

Although no state or local government has defaulted on its pension obligations to date, many are seriously underfunded and are searching for alternative courses of action. The underfunding of state-defined benefit (DB) systems was recently estimated at 1 trillion dollars (Pew Center for the States, 2010). The cities of San Diego, Miami, and Philadelphia are among the many local governments facing budget shortfalls caused in part by their need to play “catch-up” with projected pension funding shortfalls, and their plights have been featured in the popular press. A recent New York Times article on the “hidden debt” of state and local governments reported that if the pension obligations of the 50 states are recalculated in the same way bond markets value debt, the unfunded liability is US$3.23 trillion (Walsh, 2010, p. A3).

Overly generous benefits and poor stock market performance are the reasons commonly cited for these shortfalls. The market values of pension fund assets and liabilities are actually off the balance sheets (Statement of Net Assets) of state and local governments. Nonetheless, these liabilities are like bonds, in terms of obligation to pay: If a government entity failed to fulfill its promises to retirees when they become due, it would have to either raise taxes or cut back on the programs it currently provides to its constituents (Cho, 2009; Novy-Marx & Rauh, 2009). Given the amount of underfunding of DB pension plans and their current high exposure to market risks, the problems with public retirement systems should be a major concern to taxpayers, both current and future. The idea that the federal government would step in and make up any shortfalls may be driving the observed “morally hazardous” behavior in regard to pension funding, but this may be a slim reed to lean on in light of projected Social Security shortfalls.

To cope with increasing unfunded liabilities, several state legislatures have voted bills cutting back on public pensions. Local governments have also been trying to reduce benefit generosity by incrementally raising the retirement age or lowering benefit multipliers for each year of service (Pew Center on the States, 2010). Although some have enacted bolder changes in their pension policies, the majority of state and local governments have chosen to preserve the status quo with only minor alterations. Such stop-gap steps are unlikely to solve what we observe to be the looming pension crisis by compensating for the substantial shortfalls faced public employee pension funds. Well-intentioned efforts to bolster actuarial soundness of the traditional public retirement system make legal and ethical sense, but history suggests they are palliatives for what appears to be a terminal patient.

In fact, the current financial crisis has only exacerbated the long-standing issue regarding the solvency of DB systems in the public sector. Plans sponsored by state and local governments have been chronically underfunded for a variety of reasons. The institutional and management structure of DB systems (Eaton & Nofsinger, 2001) combined with the short-time horizons of elected officials (Giertz & Papke, 2007) create strong incentives for governments to underfund their pension plans. In addition, most state and many local governments are fueled by procyclical revenue sources, meaning that elected officials have been loath to increase pension fund contributions during economic upturns and have manifested a tendency to cut taxes—and, hence, pension contributions—during downturns (Benner, 2009; Mahoney, 2002; Peng, 2008).

Some 20 years ago the issue of DB plans underfunding confronted the private sector and led to their virtual demise and the subsequent proliferation of individual-defined contribution (DC) plans, in which employees save for their retirements and manage the allocation of their pension assets. At first, only financially distressed companies pursued the DC alternative, but eventually even financially stable corporations abandoned their DB plans (Munnell, Golub-Sass, Soto, & Vitagliano, 2006; Rauh & Stefanescu, 2009). The conditions that brought corporate DB plans to closure are currently faced by state and local governments. From the standpoint of the employers, the cost of sustaining those plans has increased substantially due to both demographic (i.e., aging workforce with higher life expectancy) and economic factors (i.e., volatile financial markets). From the standpoint of employees, the lack of benefit portability and the long vesting periods under DB plans have been considered a burden in times of increasing labor mobility.

The DB-to-DC metamorphosis that has taken place in the private sector has not, as yet, taken hold in the public sector; the experimentation that has occurred has been limited and inconclusive. We argue that the political and economic landscape has evolved in ways that make the move from DB plans to DC plans inevitable. We expect a major reshaping of pension plans in the public sector, one that will mirror the changes that took place in private sector over the past 30 years. As the DB framework effectively dissolves in the private sector, the public sector will follow suit. Other factors, such as changes in attitudes toward retirement, the funding difficulties faced by the Social Security system, and demographics, are also likely to play roles in the eventual shift from DB to DC plans in the public sector.

This article reviews the current standing of DB plans in the public sector, specifically their affordability and sustainability. Our central thesis is that substantial change is likely to take place and that the conversion will increase in speed and scope for four reasons:

Political realities

Given the increasingly large proportions of the American workforce deemed “temporary” with no pension, health care, or sick leave, political support for public DB plans (as well as other public sector postemployments benefits, or OPEBs) is likely to decline (Coy, Conlin, & Herbst, 2010), particularly when jurisdictional contributions begin to cut into expenditures for salient services.

Legislative realities

The Pension Protection Act (PPA) of 2006 (PL 109-280) signed into law on August 17, 2006, is widely considered “the most sweeping pension legislation in over 30 years” (Internal Revenue Service, 2009, p. 1). The act embraces principles of behavioral economics that allow for considerable employer latitude in DC plans, effectively recognizing them, rather than DB plans, as typical in the workplace. Furthermore, certain provisions of this act designed to bolster the solvency of surviving DB plans have effectively backfired as a result of the economic downtown of 2008-2009 (Goldstein, 2008; McTague, 2010). This possibility was foreseen prior to the crisis (Collins, 2007). In essence, the PPA’s efforts at mandating more solvent DBs exacerbated rather than ameliorated their chronic underfunding.

The pension benefit guaranty corporation’s unfunded liabilities

Another factor contributing to the downfall of DB plans in the private sector are the unfunded liabilities faced by The Pension Benefit Guaranty Corporation (PBGC; 2009a-b). The PBGC was formed in 1974 as part of the Employment Retirement Income Security Act (ERISA). The PBGC insures private sector DB plan payouts as a “safety net” in the event of corporate bankruptcy, up to a maximum of US$54,000 annually for a 65-year-old (PBGC, 2009a). Companies with DB plans pay experience-based premiums for coverage. As a result of the past decade’s bankruptcies in the steel and airline industries as well as the more recent assumption of liabilities from auto suppliers such as Delphi, the PBGC has an unfunded liability of US$35 billion (PBGC, 2009b) and the stock market declines experienced in recent years are likely increase this significantly (Taylor, 2008). This augurs for significant premium hikes in coming years.

History has shown, however, that PBGC premium increases accelerate the freezing or termination of DB plans (Government Accountability Office [GAO], 2004). This acceleration makes the high proportion of DB coverage in government all the more glaring. Moreover, the PBGC’s financial duress underscores the actuarial problems inherent to DB solvency in the current economic landscape (GAO, 2004).

The GASB’s transparency initiatives

The Governmental Accounting Standards Board sets desirable accounting and financial reporting standards for governmental entities, the violation of which can result in higher interest rates on debt issues. State and local governments are required to report the difference between their annual required contributions to each benefit plan (ARC), including pension plans, and their actual contribution; if the former exceeds the latter they report a liability (an unfunded actuarial accrued liability, or UAAL, which can accumulate). The ARC is the sum of the normal cost allocated to the reporting period and the annualized actuarial liability (AAL) or the normal cost allocated to all periods prior to the current period (i.e., the funds that should have been contributed in the past but were not). The normal cost is the portion of the actuarial present value of total pension plan benefits allocated to the current year (determined through one of six available methods). Total plan benefits are calculated by an actuary employing actuarial standards and defensible assumptions (from Voorhees, 2005). The UAAL represents a funding liability rather than the difference between the current market value of the benefits promised to date and the current market value of the assets held by the plan. The former is employed for legitimate ends, but the latter is a better indicator of the financial position of the pension plan (e.g., it is reported in the financial statements of the plan, which may represent several jurisdictions). The GASB would seem to be moving towards greater transparency regarding the financial position of individual plans in order to meet the information needs of citizens, the financial establishment, and potential investors.

The rest of the article is organized as follows. We first review the essential funding dilemma that has historically threatened DB solvency in the public sector, namely, the tendency of politics and short-term expedience to outweigh long-term solvency in funding decisions. We next address the assumption that DB plans are needed to offset ostensibly lower wages received by public sector workers. Following this discussion, we examine the impact that behavioral economics has had on DC plan operations in the private sector via critical components of the Pension Protection Act of 2006, with the recognition that a financially illiterate population needs employer guidance in savings and investment decisions if it is to accumulate sufficient wealth for retirement. In the next section we discuss selected strategies to implement DC plans and possible difficulties inherent to this transformation; we also briefly review the international experience with public sector DC transitions. We conclude by tying this transformation to a larger mosaic of the impending retirement crisis and America’s “fit” within a competitive global economy, with an eye to further research in the public budgeting and financial management realm.

Public DB Plans: Affordability and Sustainability

Ubiquity of DB Plans in Government

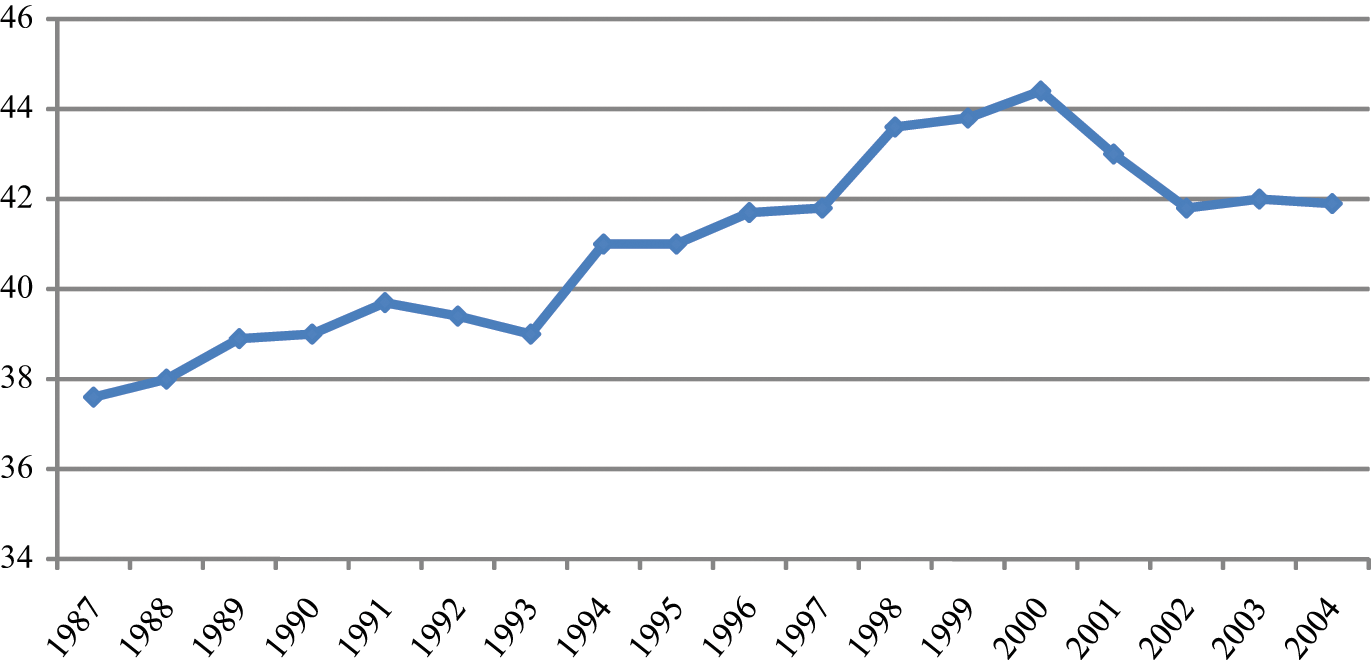

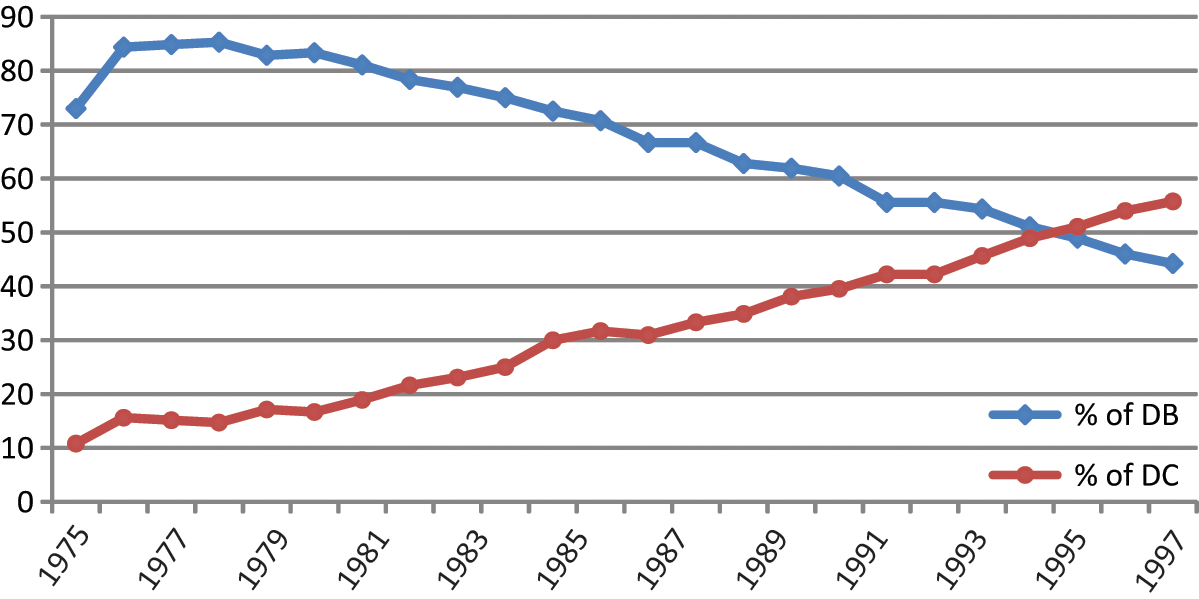

Defined-benefit pension plans have become one of the distinguishing staples of public sector employment. Eighty-four percent of government employees have such pension plans, but only 21% of private sector employees enjoy this benefit (“Promises to Keep,” p. 24). In 2006, more than 7 million public sector retirees were receiving defined benefit pensions, and 2,600 state and local public pension systems represented more than 11 million more active government employees (Chapman, 2008). In contrast, less than half the workforce in the United States enjoys any kind of pension coverage (Figure 1), and this percentage has been steadily shrinking since 2000 (Coy et al., 2010; Feldman, 2009; Gandel, 2009).

The ubiquity of DB plans in the public sector has been variously attributed to three general factors: a workforce that is more tolerant of vesting requirements and limited portability of earned benefits; the relative insulation of public sector enterprises that shields them from the competitive market forces that are forcing many private sector employers to eliminate pensions altogether; and their status as “on-going” entities that theoretically allow for any pension underfunding to be remedied over a longer period of time than private entities (Giertz & Papke, 2007; Munnell, Haverstick, & Soto, 2007).

Percentage of participation in any pension plan for all workers

DB pension plans became popular in the late 19th century as railroad companies began to adopt them as a way of mitigating labor unrest. It made some sense for an expanding industry to push its labor costs into the future. Some would say that DBs serve the same purpose in the public sector, as employees and their representatives are encouraged to accept lower current wages in return for generous future pensions (the future costs of which were chronically underfunded). In turn, policy makers meet their own needs for political support, lower present costs, and create a trough of funds to feed capital projects or sundry perceived needs (Giertz & Papke, 2007). Much the same often occurred in private sector DB systems until the passage of the Employee Retirement Income Security Act (ERISA) in 1974; its regulations for the operation of these plans and the requirement to report their actuarial soundness to the Department of Labor encouraged many private enterprises to drop DB plans and switch to quickly developed variants of DC pension plans. The absence of ERISA-type provisions in the public sector is a factor cited for the chronic underfunding of DB plans (Coggburn & Kearney, 2010; Leonard, 1986).

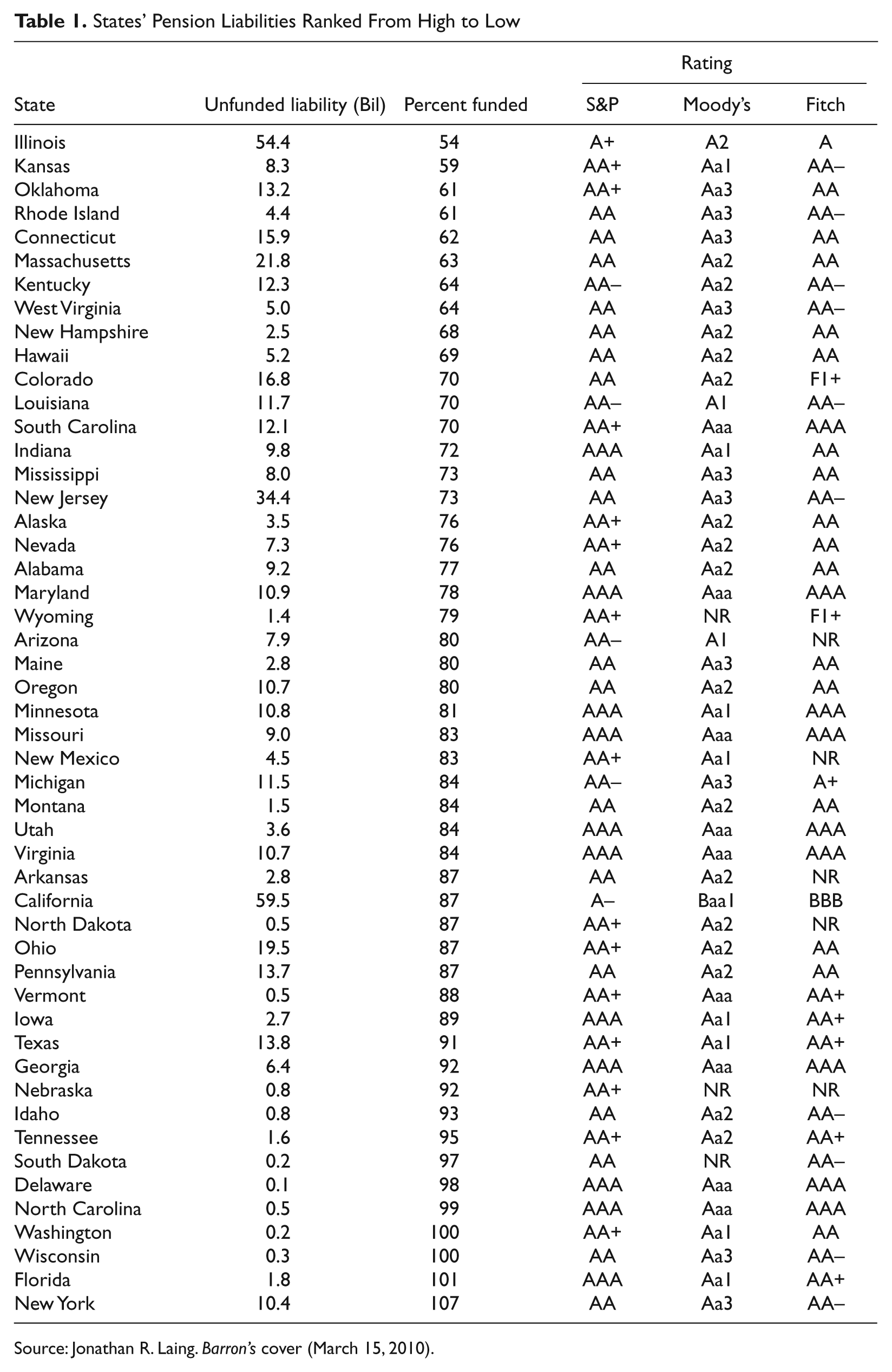

The market collapse of 2008 has led to an explosive growth of current plan obligations making them headline news in many cities and states (Gollan, 2008). Table 1 presents the current amounts of unfunded liabilities and funded status of state pension plans and how a particular state fares compared to others. Because of the high equity exposure of state and local DB plans, the stock market decline has led to substantial losses. Clark and Sabelhaus (2009) show that the wealth loss is equal to more than 8 years worth of combined employers and employee contributions. This growth and its concomitant displacement of funding for other current services effectively calls into question the long-term viability of public DB plans. States like Illinois are already having their public pension funds nearest to insolvency. According to the recent report of the governor’s pension task force, half of the US$11.4-billion state budget deficit projected for 2011 is due to pension-related spending pressures. However, in the case of Illinois, the state has been failing to properly fund the five state employee plans for more than 35 years. Munnell, Aubry, and Haverstick (2008) find that only 54% of the states and 69% of the local governments sampled “made their ARC” in 2006 (though 67% of the former and 58% of the latter were constrained by legal limits). “Making their ARC” will only get more difficult as their UAALs increase due to these shortfalls (and their difficulties are compounded by legal limits). A more recent study by Munnell et al. (Munnell, Aubry, and Quinby (2010) on the funding status of state and local public plans finds that the reported levels for 2009 are the lowest in 15 years and are likely to decline further. The study also documents that the percent of ARC paid by public employers in 2009 has been significantly lower than in prior years. As the authors note, “This decline is only the beginning of the bad news that will emerge as the losses are spread over the next several years” (p. 7).

States’ Pension Liabilities Ranked From High to Low

Without a major change in the pension provision paradigm, the only option to restore DB plans’ financial health is an increase in the funding levels (Clark & Sabelhaus, 2009; Munnell, Aubry et al., 2010). The money for this increase would have to come from taxpayers rather than from increased contributions from plan participants since the constitutional and court-imposed restriction in many states prohibit governments from changing the benefit formulas for current employees. 1 As Clark and Sabelhaus (p. 494) pit it, “The debate over increased funding is likely to trigger a significant battle for resources between plan participants and taxpayers.” Similarly, Reilly, Schoener, and Bolin (2007) warn that eventually the wage and benefit levels of public employees and the disparity with private sector counterparts will become more visible and could lead to direct democracy referenda to cap revenues or even reduce pensions.

Actuarial Solvency and Politics

In assessing ongoing DB pension shortfalls, one could envision drivers at two sides of a continuum. On one side would be the incompetent management of these plans with poor investment decision making, and on the other side of the continuum would be heavy-handed political influence that attenuates the fiscal discipline needed to operate sound pension plans.

DB fund managers face conflicting fiduciary responsibilities that tend to intensify in times of financial hardship. Management has a fiduciary responsibility to the citizens of the sponsoring jurisdictions to minimize fund contributions and, hence, tax burdens as well as a fiduciary responsibility to maintain adequate funding levels. Coggburn and Reddick (2006) and Albrecht and Lynch (2006) find that public sector fiduciaries are aware of investment benchmarks, weigh the pros and cons of passive versus active management, understand the import of overseas investment in today’s environment, and view equities as necessary for greater-than-inflation investment returns. Weller and Wenger (2009) investigate the determinants of asset allocations in DB public pension plans and find no evidence that public sector plans systematically engaged in what could be considered imprudent investment behavior. 2 Fund managers rebalanced their assets in response to stock price changes and held more risky assets only when funding levels were high. Plan managers tended to reduce the percentage of their shares in equities when the workforce age and demands on contribution increase. This is a dramatic change from 10 years ago, when a “buy-and-hold” strategy dominated pension fund thinking (Miller, 2010).

The empirical evidence suggests that political drivers are the ones that continue to erode long-term solvency. This assertion is embodied in Eaton’s and Nofsinger’s (2001) examination of 364 public pension plans from 1990 to 1996, which indicated little correlation between actuarially determined Expected Rate of Return (ERR) and actual future public pension returns. Why would actuarially set rates of return differ from those realized? The answer lies in the political drivers of solvency. We know that funding of public DB plans is procyclical. This means that elected officials tend to cut pension funding at the top of business cycles at the very time they should be maintaining them (Mahoney, 2002; Peng, 2008). Conversely, cuts in pension funding are a traditional modus operandi for balancing budgets in bad times (Benner, 2009; Coggburn & Kearney, 2010).

We also know that short-term budget balancing is frequently facilitated by accepting short-term and mid-term wage restraint in exchange for higher pension benefits or earlier retirement (Leonard, 1986; Lowenstein, 2008). From the vantage point of the political actor, this trade-off allows for the appearance of “being tough” on employees or their unions in the short term while dumping greater financial burdens on future generations long after they have left office. And in a similar vein, union leadership can “sell” wage concessions to the rank and file in exchange for higher pensions and shorter careers. These trade-offs can be made with “paper and pencil” via acceptance of unrealistic actuarial assumptions (San Diego’s recent near brush with bankruptcy manifested this practice) regarding investment returns or life expectancies. But the ultimate result is an unsustainable pension structure that has promised to many “thirty-and-out” or similar overgenerous provisions amid increasing evidence that such promises cannot be kept.

In theory, changes in governmental accounting might have led to greater discipline on the part of public sector labor and management. In 1994, the Governmental Accounting Standards Board (GASB) brought ERISA-like controls to public sector DB systems. As above, GASB Statement 27 requires that annual DB pension contributions be actuarially calculated to reflect annual pension costs incurred each year and that any liability for unpaid contributions be recognized. Statement 25 requires that each DB plan submit two reports: current financial information on plan assets, and actuarially determined information reflecting a long-term perspective on plan funding. Other postemployment benefits (OPEBs) were similarly treated by GASB in Statements 24 and 45 (Voorhees, 2005). Some have held that making shortfalls more transparent would result in a reduction of benefits and a movement to DC plans that would parallel the response of the private sector to ERISA regulations. However, unlike private sector enterprises, governments face no direct penalties for noncompliance. Notwithstanding the absence of penalties, the GASB recognized OPEBs and pensions as deferred compensation that should be expensed over the life of the worker’s employment instead of when the actual cash outlays occurred (Voorhees, 2005). Although it appears that the recent accounting changes have only increased the visibility of chronic underfunding and have done little to change the underlying dynamics that perpetuate it, the full force of the recent downtown in shares has yet to find its way into the ARCs.

These long-term underfunding patterns underscore our assertion that incremental changes in plan benefits can do little to “save” DB’s future. These measures include, but are not limited to, raising the retirement age, lowering benefit multipliers for each year of service, averaging a greater number of years as the salary base for benefit computation, and limiting overtime pay in benefit contributions (Pew Center on the States, 2010). We submit that these actions are palliatives that may buy time and help the transition to DC plans, but political realities will gut the likely impact of these actions and simply delay the day of reckoning.

Switching to DC Regime and Its Consequences

Lessons From Abroad

Strong pressures for reform of public pension systems have been felt throughout the industrialized world during the last two decades (Holzmann & Palmer, 2006). Restructuring of old pension systems has been pursued by high-income countries such as the members of the Organization for Economic Cooperation and Development (OECD), by countries in a process of transition from planned to market economies in Central and Eastern Europe, as well as by middle- and lower-middle-income countries in Latin America. Although the extent and dynamics of policy change has varied across the countries, the reform movement has been ubiquitous.

The literature identifies the affordability issue as the main driver of pension reforms around the world (Holzmann & Palmer, 2006; Weaver, 2003). During the last decades of the previous century, most OECD countries experienced demographic shocks much greater than the one faced by the United States. Increased life expectancy and low fertility rates led to a shrinking of the workers-to-pensioners ratio. Since most of the traditional public pensions system operated on a pay-as-you-go basis (often with a dedicated payroll tax to fund pensions), any increased pension costs had to be borne by a decreasing number of workers. The demographic changes combined with fiscal pressures that resulted from slower economic growth led to what Weaver calls “a shift from enrichment to austerity politics.” Weaver distinguishes between three major responses to austerity in pension policymaking that occurred in the OECD countries: (1) cuts in the generosity of pension programs manifested as various types of “retrenchment in benefits and/or eligibility,” such as changes in the benefit formulas, gradual increases in the retirement age, and cuts in postretirement indexation; (2) refinancing the pension plans through a number of mechanisms such as increasing contribution rates, as well as adding taxes to finance pensions; and (3) fundamental restructuring of pension systems, such as a gradual replacement of public DB systems with a DC-type social insurance based on individual accounts.

Brooks (2007) closely analyzes the third category of Weaver’s typology of government responses, that is, when countries implement structural pension reform and a DC pension provision supplants the traditional DB system. Generally, two major models of DC systems have been adopted by governments attempting to reduce, long-term pension costs: funded defined contribution (FDC) and notional defined contribution (NDC; also known as nonfinancial defined contribution scheme) model. In both models, the reform entails a switch from a DB system to a system of individual accounts, where workers’ pensions depend on the amounts accumulated in their retirement accounts. The models differ in the ways they are financed and managed, 3 but both are much more transparent compared to traditional DB plans and workers can monitor the assets accumulated in their accounts. Brooks contends that a total of 23 countries had adopted some form of the FDC pension reform by 2005: ranging from the United Kingdom to Estonia, and Lithuania. Although it emerged more recently, the NDC model became increasingly popular in the 1990s.The model originated from Sweden (Palmer, 2002) and has also been adopted in Italy, Poland, and Latvia.

The international experience shows that the pension issues are not unique to the United States. Many advanced industrial countries have already undergone pension restructuring, and the new DC systems established by some of them have proven to be politically and financially viable, albeit their effectiveness vary across political and institutional contexts.

Lessons From the Private Sector Transition

Active participants in DB versus DC in Private Sector

Beginning in the 1980s, corporations have been increasingly closing their DB plans and replacing them with less costly DC plans of 401(k) type. Pursued at first by only financially distressed firms, the shift away from DB plans has become commonplace (Figure 2). A study by Munnell, Golub-Sass et al. (2006) reports that even healthy firms have abandoned their DB plans. This has taken a variety of forms: Some have closed their DB plans to new hires, others have closed them to both new entrants and some existing employees, and others have eliminated them for all workers. Under ERISA, a DB plan can be terminated only if the plan is fully funded, so the employer can either purchase a group annuity from an insurance company or pay workers their accrued benefits as lump-sum amounts (Rauh & Stefanescu, 2009).

Corporations have also pioneered in establishing a “hybrid” type of cash balance (CB) plan. In this case the firm retains its DB plan, but instead of paying lifelong benefits, it distributes one lump sum upon retirement based on the account balance of each participant. According to Rauh and Stefanescu (2009), most DB plan shifts that occurred in the airline and telecommunication industries between 1999 and 2007 were of the CB type: There were 577 instances of CB conversions versus 482 instances of DB plan freezes and 211 cases of terminations. The CB plans, however, become increasingly unpopular after a court ruling in 2003 in a case against IBM that the plans discriminate against older workers. Some of the most problematic aspects of the plans have been addressed under the 2006 Pension Protection Act (Hansen, 2010), yet the controversies associated with these plans have remained.

Although the shift away from DB plans has been taking place in the private sector for quite some time, researchers are still determining the cost savings generated for employers by plan conversions. Assuming an average required contribution of 7% to 8% of payrolls for sponsoring a DB plan, Munnell, Golub-Sass et al. (2006) calculate that the switch reduces this amount to 3% or even less depending on the employer’s match to (401)k plan. Rauh and Stefanescu (2009) examine the impact of pension freezes by tracking the changes to the projected benefit obligation (PBO) around plan changes. They find that pension freezes dramatically reduce the PBO faced by employers: 1 year after the freeze plan changes, employers realize an 8% reduction in PBO liabilities compared to similar firms that have not pursued plan transformations. Similarly, a study by Ghilarducci and Sun (2006) examines the pension choices of a large number of individual firms and finds that employers choose DC plans to lower their overall pension costs. Drawing on a sample of 727 firms that sponsored pension plans between 1981 and 1998, the authors report that a 10% increase in the use of DC plans reduces the employers pension cost per worker by 1.7% to 3.5%. In addition, the study finds that 401(k)s significantly reduce administrative expenses for firms whereas DB plans administration has increased in complexity. The possibility of high and hidden management fees paid by workers in 401(k) plans has also been recognized.

The research analyzing the impact of plan changes on employees reports that the shift affects workers unevenly depending on the stage of their careers. Munnell, Golub-Sass et al. (2006) show that midcareer employees have more to lose from the conversion to DC plans than their younger colleagues. Those that are close to retirement are virtually unaffected by the change. Although the investment risk in DC plans is shifted from the employer to workers and pension assets accumulation depends on the employee’s investment history, these plans do not necessary produce lower wealth outcomes. Poterba, Rauh, Venti, and Wise, (2007) use simulation to compare the distribution of retirement wealth under private DB and DC plans for several possible allocation strategies. The study finds that individual DC plans that invest substantially in equities produce greater retirement wealth accruals compared to private DB plans. Yet, the authors warn that DC plans are also more likely to generate lower wealth outcomes than projected.

In sum, though switching from DB to DC might have immediate adverse effects for midcareer workers, it might be superior for young and mobile workers. Given the portability of 401(k) assets, Munnell, Golub-Sass et al. (2006) contend that freezing DB pension has little adverse impact on the ability of companies to recruit and retain workers, especially younger ones. An important question is whether the findings from private sector transition would hold true for governments. In theory, one of the attractions of the public sector has been associated with the generous benefits that it offers, particularly in the pension realm, the topic we turn to in the next section.

Would Government Become a Less Attractive Employer?

Reilly et al. (2007) contend that “local governments are more likely to reduce their workforce, reduce or eliminate services, and/or raise taxes or user fees rather than scale back wages and benefits” (p. 39). Why? Union pressure is clearly part of this dynamic, since many pension plans are subjects to collective bargaining agreements. Another is the seemingly accepted wisdom that public sector employees accept lower wages than they could realize for similar jobs in the private sector in exchange for future benefits. However, this assumption may not square with empirical reality and maintenance of the DB system may have nonmonetary costs on workforce composition and flexibility that are downplayed in the discussion of DBs future in the public sector.

The blanket contention that DB plans are needed to compensate for lower wages in the public sector is considered dubious by many in today’s job market (Fletcher, 2010, “The Government Pay Boom,” p. A18). According to the latest data released by the Bureau of Labor Statistics, in 2009 public employees earn salaries that are about one-third higher on average than what private workers are paid for an hour. If the benefits are included in the calculation, the statistics show that the average state or local public employee receives US$39.66 in total compensation per hour versus US$27.42 for private workers (“The Government Pay Boom,” p. A18). The academic research has also reached similar findings: public sector workers at all levels have experienced significant wage gains in the last quarter century (Bender, 2003; Krueger, 1988). Borjas (2003) shows that state workers experienced decreasing wage penalties between 1980 and 2000. Smith (1977) finds that public sector wages, excluding benefits, tended to be higher than private sector wages at all levels of government, but when controlling for education, experience, and occupation, men experienced a wage penalty and women a premium at the state level. Belman and Haywood (2004) found the largest public sector wage premium at the federal level and the smallest at the local level (controlling for the same variables except gender).

Llorens (2008) concludes that a majority of the states pay above-average rates when controlling for human capital characteristics. He does, however, acknowledge that premiums differ widely among states and “that estimates of public-private wage gaps are largely dependent on one’s choice of methodology as well as on the decision to aggregate or disaggregate data across employment sectors” (p. 324). Nonetheless, further evidence suggests that when benefits are added to wages, total compensation creates a substantial premium for the public sector (Quinn, 1982; Roberts, 2004). Petersen (2004) estimates that the average cost of pension benefits to employers in the private sector is 24% of wages; the cost to governments is 31%, yet it is not clear whether the former included Social Security payments that some governments avoid. 4

We acknowledge that uncompetitive pay may be an impediment to attracting managerial talent in government (Elling & Thompson, 2006), but this difficulty may be exacerbated by collective bargaining that leads to salary compression that benefits lower-ranking employees at the expense of their superiors, potentially driving the latter from government (Nigro et. al., 2007). We further admit that benefits are becoming “an increasing proportion of the total compensation in the public sector” (Kearney, 2003, p. 307) and that DB plans may enhance the likelihood of longer employee tenure (Nyce, 2007). On the other hand, DB plan features provide disincentives for older, experienced workers to stay employed in a shrinking labor force at a time when Social Security’s funding has become a critical issue (James, 1996; Penner, Perun, & Steuerle, 2003). Furthermore, younger workers are increasingly disinclined to meet the length of service required for vesting in DB systems (Dolan, 2007). This later point is amplified by Bowman and West (2006) who note that the successors to the baby boomers “are not expected to have a career, much less a calling, in the public sector” (p. 155).

In sum, the axiom regarding the need for generous pensions (typically, DB) in the public sector as compensation for lower-than-market wages does not necessarily hold up to empirical scrutiny. It may be that DB plans’ vesting and service requirements “turn off” at least some younger workers while encouraging a “brain drain” of older workers. It appears that adoption of DC plans per se do not affect long-term human resources planning in government. If, however, generous DB plans are indeed designed to compensate public employees for accepting lower wages than they could command in comparable private sector positions, they are clearly a form of deferred compensation owned by the employees. DC plans are conceptually more compatible with such schemes than are DB plans, which can render employees captives of their organizations. Equally generous DC plans may result in higher present costs and less generous DC plans may call for higher wages, but either may make government a more attractive employer.

DC Plans in Public Sector

Although still rare in the public sector, some state and local governments have already experimented with defined contribution retirement regimes (Clark & Sabelhaus, 2009; Holland, et al., 2008; Munnell, Golub-Sass, Haverstick, Soto, & Wiles, 2008; Snell, 2010). There are at least a dozen states offering some form of DC plans. The options range from DC being mandatory primary plan for new hires, to a combination of both DC and DB, to having DC only as an option that new employees can elect. Michigan has been the first state to adopt a mandatory DC plan for new state employees 5 since March 31, 1997. Alaska followed suit: State’s legislature voted in 2005 to close its DB plans for public employees and teachers to new employees and replace it with DC plan. The switch came into effect in July 1, 2006. 6 Two states—Oregon and Indiana—have mandatory combined plans, according to which the employees are required to participate in both DB and DC plans. Utah’s legislature enacted in 2010 a bill that gave the state employees a choice between a DC plan and hybrid plan with DB and DC components. Several states, including Colorado, Florida, Montana, North Dakota, Vermont, and South Carolina, have offered DC plan as an optional primary plans and public employees have the choice to join either a DB or DC plan. Washington offers a choice between DC and hybrid plan, and Ohio allows its employees to choose between all three options: DB, DC, or hybrid plan. The variation is even greater at the local level.

Since most of these changes occurred just recently and only two states have switched completely to DC plans after closing their DB plans, the effects of the transformation are yet to be estimated. A recent study by Thom (2010) examines whether Michigan’s decision to switch to DC has led to cost abatement. The study draws on financial data from 1998 to 2010 and finds that Michigan’s decision to enroll new state employees in a 401(k) has had two major effects. First, the closure of the DB plan to new participants has reduced the growth in the state’s long-term liabilities. Second, it has been on average less costly for the state budget. Specifically, the comparison between state contribution pension rates for both plans—the DC plan for new employees and the DB plan for previous hires and retirees—shows that the 401(k) is the less expensive alternative, often by double digits, except for the first few years after its introduction. The estimates for 2009 and 2010 look at a 12- to 15-percentage-points cost advantage for the DC plan. In addition, annual contribution cost associated with the DC plan has been stable compared to the much less consistent annual contribution rates to the DB plan. Finally, in terms of administrative expenses, the 401(k) plan turned out to be less extensive for the state of Michigan, because the fees were borne by the individual participants.

DC plans in the state and local sector are clearly limited as the default option, and it may be unfair to judge their long-term success or failure in terms of replacement income for retirees. Moreover, DB plan administrators may have an inherent fear of establishing DC plans from the perspective of adverse selection. Simply put, it is likely that higher income, better-educated plan participants will choose DC plan options, leaving a lower-income base of enrollees with shorter life expectancies in the DB option (Bodie, Marcus, & Merton, 1988; Clark & Pitts, 1999).

The 25 years of experience with the Federal Thrift Plan may provide a better assessment for the potential success of the DC plans in the local (state) sector. This plan’s common stock portfolio averaged 9.29% returns from 1993 to 2002; its fixed income account averaged 6.24% during that timeframe (Moore, 2003). The plan’s low costs and solid returns have been cited as a possible model for Social Security reform (Moore, 2003) And though the plan’s size and economies of scale may not be possible in other governments (Investment Company Institute, 2008), the Thrift Plan’s success suggests that over time and with appropriate investment training, DC plans can work in the public sector.

We further note that many professors in state university systems are covered by DC plans such as TIAA-CREF, ING, and other large investment firms. This suggests that state human resource administrators acknowledge that, as a class, professors prefer the portability and investment flexibility accorded by participation in these plans and reinforces Clark and Pitts’ (1999) contention that when given a choice between DB and DC plans, over time, workers will choose the latter.

Governments have experimented with cash benefit plans, yet their application has been very limited in the public sector. As mentioned above, cash balance retirement plans are a hybrid that allow plan participants to obtain a “shadow balance” of their accrued retirement benefit, frequently on an annual basis, with this balance being portable upon separation. These plans are frequently part of guaranteed investment contracts or similar vehicles in which the employer or designated fund manager makes investment decisions. These attributes are viewed by some as making the cash balance plan a desirable alternative to DC plans in that they have DC plan portability but relieve financially illiterate employees of the burdens associated with asset allocation over a lifetime (Costrell & Podgursky, 2010; Hansen, 2010).

Our difficulty in supporting this option is twofold. First, these plans are technically DB plans. This suggests that the balance sheet burden of their appropriate funding remains on state-local books. Recent funding history suggests that cash balance plans are unlikely to be appropriately funded; their establishment will not relieve state and local governments of the unfunded pension liabilities they currently face. Consistent with this problem is the fact that cash balance plans in the private sector are guaranteed by the Pension Benefit Guarantee Corporation. As noted earlier, this guarantor is facing its own unfunded liabilities. More important, without similar ERISA coverage, one can ask how cash balance plans would be guaranteed in terms of solvency. In sum, the cash balance option’s defined-benefit roots are unlikely to provide a solution to the unfunded liabilities currently facing state and local governments.

Transitioning to the DC Paradigm: Some Critical Questions

In this section we raise four critical issues regarding the implementation of DC plans in government within the context of the Pension Protection Act. We believe that effective implementation will require a simultaneous search for answers to the following questions.

How to Begin the Transition?

Perhaps the biggest question to address is how to effect the transition. We hypothesize that as the funding shortfalls in public DB plans increase in size and scope, labor, management, and elected officials will come to realize the inherent instability of the system. At this juncture, introduction of DC plans for new hires and those with less experience (perhaps 10 years of experience and under age 45) will appear not only be plausible but also legally and morally desirable as a means of preserving benefits of current pensioners and employees within a decade of retirement. This latter group has done its “life planning” under a set of expectations that may make new adjustments painful during or close to retirement. This three-bracket approach was used in the unsuccessful Social Security reform proposal undertaken by President George Bush in 2005. Notwithstanding this failure, the three-group approach makes sense in terms of rollout given the concern for benefit preservation of older members in the system.

We acknowledge that the “middle group” is perhaps the most difficult to consider analytically. As Coggburn and Kearney (2010) note, the public sector has little experience with “hybrid” pension systems that combine DB and DC elements. Conceptually, this might be the most appropriate pension for this group. In practice this might overload human resources personnel who would have to maintain two systems. Moreover, its actuarial implications add uncertainty to long-range financial planning. Thus, switching the “middle group” to DC plans via lump-sum payout may be the most attractive option, despite its higher “up-front” costs.

The 1983 reforms to Social Security provide further guidance for pension reform in the present context. Actions recommended by the Greenspan Commission (gradual raising of the retirement age to 67; taxation of benefits, delays in cost of living increases) took place because of bipartisan recognition that the system was heading for insolvency on its current path and that future recipients should have as long a lead time as possible to adjust their financial planning. The authors believe that the current state of DB plans in the public sector will require—and induce—Greenspan Commission–type statesmanship to thwart insolvency and preserve benefits for those in or near retirement.

Another vital component of ameliorating the DB crisis would be to mimic the private sector’s solution for its unfunded OPEB liabilities and create Pension Benefit Associations (PBAs) directly analogous to the Voluntary Employee Benefits Associations (VEBA’s created by General Motors, Chrysler, and Ford (in cooperation with the United Auto Workers) to fund reserves needed for current and future health care. These PBAs could conceivably mirror New York’s Municipal Assistance Corporation (MAC) created in 1975; they would have debt-raising capacity that might be needed to fund future pension obligations and, like the MAC, end their existence once current and future beneficiaries pass from the scene (Lisberg, 2008).

Our reasoning behind the PBAs is simple. From a management perspective, the unfunded liabilities on state and municipal balance sheets may, like their unfunded pensions and OPEBs at other legacy employers (i.e., steel companies, pre-deregulation air carriers), become crippling in terms of bond rating or debt capacity. Management could in theory take this debt off its books and transfer it to a third party and remove obligations that might ultimately threaten ability to borrow. Similarly, government employees, like their counterparts at “The Big Three” and elsewhere, might feel more secure about their future benefits knowing their pension assets were effectively “corralled” from political raids of elected officials or procyclical funding patterns. In essence, we envision these PBAs as independent authorities with the sole purpose of funding and managing the pension obligations they incur. The contemporaneous switch of new employees to DC plans and the creation of PBAs would, in theory, establish clear financial and temporal bounds on future pension obligations while facilitating the transition to DC plans.

Some would also argue that legal constraints imposed by state constitutions and court rulings would restrict the widespread reduction of DB plan benefits, much less the adoption of DC plans. Many state constitutions limit the ability of states to make changes that would lead to reducing the monetary value of pension benefit for those already in the plan (Monahan, 2010; Munnell, Aubry et al., 2010). In addition, state courts have ruled that pension plans are in effect contracts between the state and employee and a unilateral alteration on the part of the state is a violation of the contract. In a detailed review of the legal framework, Monahan points out that such protection is not provided to the other aspects of employment: The employer can unilaterally alter the salary, fringe benefits, and even employment status. The author calls for states to adopt the approach taken by the federal government and protect only the retirement benefits that employees have earned to date but not the future benefit for which services have not been rendered. Schneider (2005) also acknowledges the “idiosyncratic legal environments of public plans” (p. 122), subject to legislative approval and union contracts. Yet current realities demonstrate that legal restrictions are not as concrete as many believe. In recent years, the cities of Miami and Philadelphia, as well as the states of New Jersey and California, have invoked “fiscal emergency” status to reduce pension benefits of current and future recipients (Mendel, 2010; Rabin, 2009; Rabin & Mazzei, 2010). This underscores our belief that a paradigm shift in public pension plans is likely, given the unsustainable levels of benefits promised to plan recipients. In essence, it appears quite likely that many state and local governments will be following in the footsteps of legacy airlines postderegulation in mandating significant reductions of retirement benefits in order to balance their budget and to preclude the erosion of current services. The depth of the “Great Recession” is effectively removing the accepted wisdom that accrued pension benefits and the formulae used in their calculation are an untouchable property right garnered through prior political decisions or collective bargaining.

Can Agencies Implement Effective Workplace-Based Financial Literacy Training?

Americans suffer from widespread financial illiteracy. Most Americans have difficulties computing their net worth, balancing their checkbooks, comparing insurance quotations, budgeting monthly expenses, or procuring financial services (Frank, 1997). This illiteracy has been noted by current Federal Reserve Board Chairman Ben Bernanke as potentially damaging to our economy in that it may negate effective competition among financial services providers and lead to serious misallocation of capital (Bernanke, 2008).

The consequences of this illiteracy have been documented in the context of 401(k) and 403(b) asset allocations (Frank, Condon, Dunlop, & Rothman, 2000; Turner, 2006). Many Americans have no idea where to begin to allocate stocks, bond, cash, or “other” throughout their life cycles. Many show what is termed “reckless conservatism” by investing in cash or low-yielding investments that fail to keep pace with inflation. Large proportions of DC participants—upwards of 50%—fail to change investment allocations over their tenure. In a recent study of large employer 401(k) participants, DeGroote and Deaves termed 26% “needy” and another 15% “disengaged,” suggesting that approximately 40% had neither the time nor desire to seek investment advice (2004, p. 6). Not surprisingly, participants in these categories were typically those with lowest income and wealth, in effect, those with the greatest need.

Dovetailed against this backdrop of financial illiteracy is another sociocultural issue—Americans’ unwillingness to save. Left to their repose, most Americans—even those earning US$100,000 or more—inflict a tremendous “savings shortfall” upon themselves (Singletary, 2008, p. 3E). The lack of savings shows in 401(k) balances, where, for example, the 11 million workers across 17,100 companies covered by Fidelity Investments averaged a paltry US$50,200 at the close of 2008 (Petruno, 2009). Workers in the 55 to 64 age bracket nearing retirement showed a median value of US$100,000 in their accounts according to Census data in a 2007 Congressional Research Service report, showing some improvement over their younger peers, but far less than the US$500,000 in assets needed to assure replacement of preretirement earnings. 7

A significant body of literature confirms that though overall financial literacy is low, it is particularly lacking in women and minorities (Chen & Volpe, 2002; Frank et al., 2000; Lusardi & Mitchell, 2005). Yet these groups have shown a historic preference for government employment (Blank, 1985; Burbridge, 1994; Lewis & Frank, 2002). This investment knowledge gap raises a possibility that adoption of DC plans could make the public sector less attractive to these groups to the extent that retirement plan type is an inducement to hire. Such an eventuality would compromise public management’s long standing commitment to affirmative action.

The antidote to these issues is to recognize the importance of financial literacy training in the workplace, specifically; the fact that investment and financial counseling have become valued benefits in many private firms (Armone, 2006; Knapp, 1991) and the advent of DC plans in government would make the introduction of this training an imperative. It also suggests that public employers are no different from their private counterparts and that they must recognize that vendors of financial products are unlikely to offer the unbiased advice that workers need (Frank et al., 2000). Hence, the HR function in many governments will need to augment financial literacy counseling and may even consider the provision of low- or no-cost annual financial “checkups” for employees.

Thus, a question arises as to how well the Public HR function can provide enhanced employee financial literacy in an era of DC plan implementation. Unfortunately, the public personnel function is often associated with rigidity and rule-bound behavior rather than meeting strategic needs, particularly in governments with high degree of unionization (Kellough & Selden, 2003). Implementing enhanced employee training in financial literacy will be a significant challenge for many HR functions in the public sector, and it remains to be seen how well personnel staff will adapt to their potential roles as educators in personal finance.

Which Default Savings and Investment Alternatives Work Best in the Public Setting?

Critical components of the PPA address the financial illiteracy and undersavings issues and are based on the contributions of the field of behavioral economics to health care and retirement. The intellectual cornerstone of this approach is that default options are critical means for overcoming individual inertia and establishing improved behavioral norms (Orszag, 2008). The PPA embeds the following in 401(k) plans that could be extended to 403(b) and 457 plans in the public sector.

Autoenrollment

The PPA preempts state laws that prohibit implementation of automatic enrollment in DC plans. This does not mandate autoenrollment but facilitates “opting-out” of employer enrollment, rather than the “opting-in” called for prior to PPA passage.

Autoescalation

The PPA allows for initial enrollment at 3% of salary with automatic annual increases to 4% in the second year, 5% in the third year, and 6% in subsequent years, with automatic election capped at 10%.

Qualified default investment alternatives (QDIAs)

So-called safe-harbor provisions of the PPA allow employers to place salary deductions into three QDIAs: (1) Life-cycle or targeted retirement-date funds, (2) balanced funds, or (3) professionally managed accounts.

Employers’ provision of specific investment advice on plans

Other “safe-harbor” provisions build upon prior ERISA legislation that encourages employer investment counseling by minimizing potential lawsuits resulting from investment allocations. “This creates significant opportunities for participants to get the advice they are begging for without leaving the employer exposed to the outcome” (Hepburn, 2006, p. 25).

These provisions of the PPA establish a legislative paradigm that empowers public employers to overcome their workers’ investment ignorance and spendthrift behavior within the context of a DC retirement system. Although this system is still in its infancy, it provides a model for implementation of DC plans that acknowledge critical social-cultural shortcoming that negatively affect retirement savings at a time when DB plan participation is diminishing.

To date, the target or life-cycle fund is the preferred QDIA under the PPA (Capital Guardian Trust, 2007). These funds, comprised of stocks, bonds, and cash, are assets allocated in various proportions according to anticipated retirement date (e.g., “2020, “2025,” “2040”). Over time, allocation in these funds switches from growth-oriented stocks to income-oriented bonds and cash. They are envisioned as a “one-stop shop” for investors in that fund managers automatically rebalance these accounts, theoretically easing the investing “glide path” to retirement.

All target funds are not created equal. Funds for given target differ dramatically in their composition between and within asset classes. Conservatively managed funds avoid foreign investments, whereas other funds go overseas. Some have higher proportion of equities over time. In short, like any investment, life-cycle funds require vigilance with respect to cost and performance (National Association of Government Defined Contribution Administrators, 2007).

The performance of these funds was not immune to the economic downturn of 2008 (Antolin & Stewart, 2009). This underscored another issue related to life-cycle funds, namely, their significant equity component in funds for those at or near retirement age. From a capital preservation perspective this is understandable, given the need to “inflation proof” a portfolio via equity participation. But this also adds volatility to portfolio to those later in life. This heightened volatility underscores the need for supplanting life-cycle funds with other investments such as traditional bond funds or guaranteed investments such as fixed annuities.

Given the nascent status of the PPA and the fact that this short span has witnessed one severe market downturn, the question of which QDIA works best throughout two or more business cycles remains unanswered. An important corollary is that the QDIAs that provide best returns on investment in one sector’s employees may not carry over to another. Public employees may have different risk tolerance levels or investment horizons than their private or nonprofit counterparts. Stated differently, a one-size-fits-all approach to QDIAs may not apply and implementation of DC plans in government may need emphasis on different default options. Only time and empirical study can answer if that really is the case.

Will Federal Laws “Cure” the “Leakage” Problem and Establish Autoannuitization?

Although federal legislation allows for autoenrollment and autoescalation, it does not mandate autorollover of 401(k) plans or their siblings into IRA or other retirement savings accounts (Gale, Iwry, & Orszag, 2005; Poterba, Venti, & Wise, 1999) upon employment separation. Nor does it preclude borrowing against plan assets (Beshears, Choi, Laibson, & Madrian, 2008). These two options foster “leakage” from retirement savings assets that can be significant, particularly for lower-income workers. Given Americans’ spending habits and the increased reliance DC plans will play in American retirement income, these policies may need careful reexamination.

A related issue is the belief that DC plans should require mandatory annuitization upon retirement (Horneff, Maurer, Mitchell, & Dus, 2006; Lowenstein, 2008; Ortiz, 2004). This approach, used in the United Kingdom, Israel, Chile, and elsewhere, requires all or part of assets accumulated under DC plans to be rolled over into an annuity that provides an income stream that overcomes “longevity risk” or outliving one’s savings. Many Americans do not understand the mechanics of annuitization or its attendant cost; hence, implementation would require considerable consumer education. But the absence of this requirement reduces the value of DC plans in the context of the traditional “three-legged” stool of Social Security, personal savings, and pensions.

As this is written, the Departments of Labor and Treasury are jointly considering the adoption of mandatory annuitization for the major defined-contribution plans (U.S. Department of Labor/U.S. Department of the Treasury Joint Hearing, 2010). This line of reasoning has been mentioned in retirement policy in the context of both Social Security reforms that would “privatize” all or part of benefit streams as well as traditional defined contribution plans. Three factors contribute to this belief:

Longevity risk: There is a better than 50/50 chance that an individual who reaches age 50 will live to age 60. Increased life expectancy augurs for retirement plans that assure a stream of income for life. Annuititization, which pools one individual’s retirement assets with others, is viewed as an antidote to longevity risk. Although recent evidence suggests that many Americans dislike the prospect of mandatory annuitization, it is likely that forthcoming federal legislation may encourage annuitization as an option at retirement (Powell, 2010).

The possibility of retiring during a “lost decade” for financial assets: Even the most prudent of retirees faces the chance retiring at or near the onset of a “lost decade” for financial assets. Wachovia Securities notes, for example, that an individual with US$500,000 of assets who retired in 1975 and drew down 5% of assets annually—a typical amount used for retirement planning—would have no assets in 1985. By way of comparison, an individual who retired in 1985 with the same US$500,000 and the same 5% drawdown would have US$1,000,000 in 1995. And lastly, using the same lump-sum and draw-down parameters, a 1995 retiree would have US$1.5 million in 2005 (Wachovia Securities, 2008). Simply put, expected annual returns to given asset classes do not account for “lost decades” for financial assets such as the 1970s or the 2000s. This theme is further illustrated in Prudential’s (2010) notion of the retirement “Red Zone” that emphasizes the import of financial planning in the 5 years prior and subsequent to retirement; one or two downward price shocks during those years can have devastating impact on incomes streams during retirement. Here again, pooling of assets among a group of retirees can effectively smooth these shocks.

Americans’ spending habits may divert retirement assets for current consumption: The sad reality is that absent mandatory annuitization that effectively sequesters retirement savings, Americans may spend down accrued retirement savings for other consumptions. This rationale also plays a role in some advocating the mandatory rollover of defined-contribution assets into IRAs or similar vehicles upon separation from employment.

To our knowledge, these interrelated policy questions have been off public administration’s radar screen and may be seen by some as arcane or perhaps even trivial (Frank, 1997). We submit that in an era increasingly characterized by DC plans, the autorollover and autoannuitization issues are absolutely critical and deserve attention in the public sector.

Conclusion

Thirty years ago, the notion that public employees might lose defined benefit pensions would be characterized as a symptom of “deprivileging” (Hays, 1996; Peters & Savoie, 1994; Ridley, 1983). This term was coined to describe the belief held by Great Britain’s Prime Minister Margaret Thatcher and her supporters that DB plans were, along with inflation-adjusted wages and lifetime employment, characteristic of a civil service that was immune from market forces and a competitive world economy. Thirty years later, it appears that a number of forces, both economic and political, are leading to this outcome. Unfortunately, public administration has tended to overlook the shrinking real income and the relatively poor performance of the American economy over the past several decades (Carroll, 1992; Frank, 1997). The current public pension crisis reflects a basic affordability issue that has been exacerbated by chronic underfunding largely attributable to political unwillingness to forego current services at the expense of long-term pension solvency. Changes in accounting rules have only made this long-term solvency issue more transparent. Against this backdrop, a DB-to-DC transition should not be viewed as “deprivileging,” but rather, acknowledgment of the political and economic realities facing organizations across all sectors.

From a standpoint of public policy, DB plans that encourage retirement before age 65 must be viewed with deep concern during a time of increased life expectancy. Notions of “Thirty-and-Out” may have made sense in an industrial era, but today’s retirees are likely to find working in their 60s and early 70s to be psychologically and financially necessary. The public sector should tailor its retirement systems with an eye to this emerging reality. Another issue to consider is that of intergenerational equity. Nearly two decades ago, George Frederickson (1994) asserted that public administrators have obligations to future generations, a position recently reaffirmed by Carol Lewis (2006). The operation of pension plans that are currently unaffordable and ultimately add to future generations’ accrued debt burdens compromises that obligation. Transitioning to DC plans in the public sector is unlikely to come easily, but the long-term transition costs for all stakeholders—taxpayers, governments, and employees— 8 are likely to be less severe than current incremental changes such as increasing the retirement age, changing benefit multipliers, or changing the portfolio mix of retirement plans (Stalebrink, Kriz, & Guo, 2010). Maintaining the DB paradigm has been difficult in less challenging economic environments; its sustainability is questionable in the low-to slow-growth economy frequently typified as “The New Normal” (El-Erian, 2008).

We further submit that the study of public sector pensions must be holistic and integrative. The current public administration retirement literature is largely segmented between financial management and human resources. Solving the current retirement crisis in the public sector will require careful examination of solvency, compensation, financial literacy, and related issues. This calls for research that melds traditional financial management with strategic human resources planning while acknowledging changing political and economic realities.

The state and local sectors employ approximately 19.5 million workers (Baumol & Blinder, 2008, p. 29). Public sector managers and elected officials should view the current public sector pension crisis as an opportunity to develop sustainable retirement plans for work forces that, like their private counterparts, have limited financial literacy and retirement savings. This is a difficult task. But the first step in designing these systems will be the recognition that the current DB-based structure is no longer functional. New systems, utilizing the default-based Pension Protection Act paradigm are the apparent successor. Time and future research will tell if the state and local sector transition experience provides lessons for practice elsewhere.

Footnotes

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The author(s) received no financial support for the research, authorship, and/or publication of this article.