Abstract

This article attempts to evaluate the role the legislative budgetary oversight plays in enhancing budget transparency. This relationship has not been empirically tested so far. For a sample of 93 countries surveyed by International Budget Partnership in 2010, we show that, as expected, legislative budgetary oversight has a positive influence on budget transparency. Besides, the legal system, political competition, and economic level are also found to affect budget transparency. As an additional analysis, we investigate the determinants of legislative budgetary oversight along the budgetary process. In this vein, the type of legislature, legal system, Supreme Audit Institution’s budgetary oversight, economic level, and democratic level determine legislative budgetary oversight.

“The pattern of conflicts reflected the struggle over economic and political institutions. Parliament wanted an end to absolutist political institutions; the king wanted them strengthened. These conflicts were rooted in economics.”

Introduction

Governments have a moral obligation to their citizens to be transparent about their handling of tax-payers’ money (Fölscher, Krafchik, & Shapiro, 2000). Government budgets represent financial plans which specify how public resources are going to be used to meet policy goals (Organisation for Economic Cooperation and Development [OECD], 2006). The budget plays a central role in the lives of every citizen. Citizens, especially poor and low-income ones, are the primary beneficiaries of government programs financed through the budget. It is therefore essential that citizens understand government budgets, and have access to information that will allow them to hold the government accountable for the use of public funds. Unfortunately, citizens, legislatures, and the media have been traditionally excluded from budget decision-making and monitoring. In most developing countries, public budgeting is still considered as a state secret, and the process is controlled exclusively by the executive (de Renzio & Krafchik, 2007). Moreover, modern economies’ budgets are very complex, allowing practices that aim to hide the real budget balance. Politicians have little incentives to disclose simple, clear, and transparent budgets (Alesina & Perotti, 1996). Accordingly, accountability mechanisms are required to verify that governments meet their duties.

Budget transparency can be one of these mechanisms. Fiscal transparency has been recently defined by the International Monetary Fund (IMF) as the clarity, reliability, frequency, timeliness, and relevance of public fiscal reporting and the openness to the public of the government’s fiscal policy-making process (IMF, 2012).

The importance of government fiscal transparency was highlighted during the Asian financial crisis of the late 1990s, which showed the risks of opaque and unaccountable management of finances (Santiso, 2005a). Investors and rating agencies failed to detect creeping fiscal disequilibria, large public contingent liabilities, vulnerable asset-liability structures, and time inconsistencies of fiscal policy (Marcel & Tokman, 2002). Nowadays, history is almost repeating itself with the financial crisis involving Greece, which threatens to splinter the Eurozone (Manessiotis, 2011). Thus, it is clear the key role budget transparency plays in the credibility of governments’ policies. Higher budget transparency enhances the performance of all economic agents in the country. Besides, budget transparency may be a tool to fight against poverty. In fact, budget transparency is often weakest in countries where poverty is highest. The result is a huge misuse of public resources into unnecessary projects, corruption, and ineffective service delivery, which undermines efforts to reduce poverty, improve governance, and consolidate democracy (de Renzio & Krafchik, 2007).

Accordingly, the role of budget transparency has increasingly attracted attention from governments and international organizations as a way to prevent such failures in the future and give credibility to economic policies. This concern has triggered the development of budget transparency international standards such as the “Code of Good Practices on Fiscal Transparency” (published by IMF in 1998 and updated in 2007) or the “Best Practices for Budget Transparency” (published by the OECD in 2001). Furthermore, in 2006, the International Budget Partnership (IBP), a civil society organization sponsored by the Centre for Budget and Policy Priorities, published the Open Budget Index (OBI) for the first time to provide central governments with a systematic measure of their budget transparency level. This questionnaire-based index fits the budget transparency international standards established by IMF, OECD, and International Organization of Supreme Audit Institutions (INTOSAI; IBP, 2010). The average 2010 OBI score for the surveyed countries is only 42 out of 100, which indicates that central governments should take further steps to enhance budget transparency.

Despite the growing interest that budget transparency has received in the last decade, empirical studies on its determinants are quite limited (Andreula, Chong, & Guillén, 2009; Rodríguez, Alcaide, & López, 2013; Wehner & de Renzio, 2013). Specifically, there is a renewed interest in the contribution of parliaments to the governance of the budget and the oversight of public finances, prompted, in part, by calls for greater transparency and accountability in government financial managements (Santiso, 2005a). According to Wehner (2006), legislative oversight over budgets is defined as the power to scrutinize and influence budget policy and to ensure its implementation. International organizations assume that legislative budgetary oversight ensures government accountability and promotes greater public finances’ transparency (IMF, 1998; OECD, 2001). Legislative budgetary oversight should improve the transparency of public accounts by providing independent checks on government budget execution (Dye & Stapenhurst, 1998; Santiso, 2005b). However, the impact of legislative budgetary oversight on budget transparency has never been empirically tested (Pelizzo, 2011).

In this regard, this article attempts to analyze what institutional, political, and socio-economic factors promote central governments’ budget transparency, focusing primarily on how the budgetary oversight of the legislature over the executive affects budget transparency. We use data on 93 countries. To measure budget transparency in each country, we use the 2010 OBI. We also build some indicators based on 2010 IBP questionnaire items to measure legislative oversight along all phases of budgetary process.

This article specifically seeks to contribute to the literature in three ways. First, as stated above, the relationship between legislative budgetary oversight and budget transparency has never been empirically tested. Moreover, little is known about budget transparency determinants in an international comparative approach (Andreula et al., 2009; Rodríguez et al., 2013; Wehner & de Renzio, 2013). Second, we use the 2010 OBI to measure budget transparency, which overcomes some of the limitations of fiscal transparency indexes proposed in previous studies (Alt & Lassen, 2006; Benito & Bastida, 2009). On the one hand, IBP surveys are filled by independent experts not associated with the government. Thus, the independence of the OBI research process makes it far less susceptible to government manipulation. On the other hand, the countries covered by the OBI are located in different geographical areas and have different income levels, political regimes, and administrative cultures. Besides, data are collected simultaneously, providing a comparative snapshot of fiscal transparency at one point in time (Wehner & de Renzio, 2013). Third, legislative budgeting remains also a neglected area in comparative research (Wehner, 2005). In fact, apart from recent works of Stapenhurst, Pelizzo, Olson, and von Trapp (2008) and Wehner (2010), literature on international legislative budgetary oversight is rather scarce.

Literature Review

Budget Transparency and Legislative Budgetary Oversight

Both rule-of-law principle and agency theory shape the way governments are transparent (Hood, 2001). On the one hand, rule-of-law deems compulsory publicity and transparent management as cornerstones of public management. On the other hand, agency theory posits that principal (citizen) and agent (politician) may not pursue identical preferences, as incumbents have their own interest, which do not always maximize citizens’ welfare. Thereby, citizens press incumbents to disclose information as a way to weaken information asymmetry and to allow the former to monitor incumbents’ activities (Zimmerman, 1977).

Premchand (1993) defines budget transparency as the public availability of information regarding governments’ decision procedures and transactions. Kopits and Craig (1998) add that this information must be reliable, comprehensive, timely, understandable, and internationally comparable. Furthermore, Blöndal (2003) argues that budget transparency has three essential elements: (a) the release of budget data (systematic and timely release of all relevant fiscal information); (b) an effective role for the legislature (scrutinizing and independently reviewing budget reports, discussing and influencing budget policy, and holding government accountable); and (c) an effective role for civil society through the media and non-governmental organizations (influencing budget policy, holding government accountable).

Regarding the role of the legislature and its impact on civil society, legislators have wide discretion to use their resources, benefiting in some cases their own constituency and/or campaign contributors. However, the oversight role is a public good within the legislature, thus benefiting the entire population (Benito & Bastida, 2009). In fact, budget transparency depends on the role the legislature plays regarding budgetary oversight (Santiso, 2005a).

The agency theory in general states that the principal (citizens) should be able to hold the agent (government) accountable. In the context of our research, the legislature represents the citizens’ interests. According to Alesina and Perotti (1996), governments have little incentive to disclose clear and transparent budgets. These authors state that the problem of lack of budget transparency can be addressed either by setting standards (e.g., procedural fiscal rules and hard budget constraints) or having independent agencies which provide a check on the accuracy of the budget (e.g., general audit offices and legislative budget institutions). Therefore, budgetary oversight by critical legislatures and external auditing of public accounts by credible general audit offices are key mechanisms of financial accountability (Santiso, 2005a).

Ambition theory suggests that legislators will use their powers to expand their authority over policy making through legislative oversight (Desposato, 2008). Effective and responsible legislatures can help mitigate the risks of excessive executive budgetary discretion by reinforcing the compensatory mechanisms of government accountability and legislative scrutiny (Santiso, 2005a). By providing independent checks and balances on executive discretion, legislative budgetary oversight should improve the transparency of public accounts. Therefore, legislatures help ensure that governments are held accountable for public finances management (Dye & Stapenhurst, 1998; Santiso, 2005b). In other words, enhancing legislative budgetary scrutiny leads to a strengthening of government accountability and promotes greater transparency in the management of public finances (IMF, 1998; OECD, 2001). In addition, information asymmetries between government and society that stem from agency theory may be diminished by legislative oversight. The legislature, by opening up the budget to public debate on governments’ policies and public funds management, it helps create the conditions for greater governments’ accountability (Santiso, 2005a). Hence, an effective financial scrutiny may enhance executive accountability, facilitate public debate and broaden participation in the budgetary process. By creating demand for financial information disclosure, the legislative oversight can improve budgetary process transparency where it was previously secret (Wehner, 2007).

Legislatures around the world have the constitutional power to consider national budgets and authorize governments to raise revenues and carry out expenditures. Currently, there is a trend to enhance legislative involvement in the budget process. Some OECD-country legislatures are seeking to regain a more active role in the budget process (Stapenhurst, 2008). France, for example, introduced reforms to support parliamentary oversight and to expand the powers to amend expenditures. In developing countries, there is also a trend toward legislative budget activism, as a way to increase the transparency of previously closed budgetary systems. For instance, in Brazil, constitutional changes have given the Congress powers to modify the budget. In this country, the Congress had historically played no significant role in the budget process. In Africa changes are occurring too: South Africa and Uganda have passed financial administration acts or budget acts that give more influence to the legislature during the budget formulation and approval processes.

All the aforementioned reforms are aimed to strengthen the traditional legislative control over executive financial indicators. Recently, performance management literature claims a shift from finance-focused accountability to performance-based in financial reporting. Performance management is defined as a reform that focuses on the use of performance measures in budget decisions, as well as a philosophical shift to focus on results rather than inputs or processes (Bourdeaux & Chikoto, 2008; Hatry, 1999). In this vein, recent reforms are shaping new legislative roles in setting overall fiscal policy targets and checking government performance (Posner & Park, 2007). Executives and legislatures in many countries now require agencies to report on the performance and financial costs of government. Thus, for example, France, Korea, the United Kingdom, and the United States require agencies to develop performance plans and reports that for the first time disclose on a systematic and often public basis how government programs are working to achieve outputs and outcomes (Posner & Park, 2007). These examples show that the actual exercise of the legislative oversight over the budget varies widely (Stapenhurst, 2008).

The annual budgetary process can be divided into four stages: drafting, approval, execution, and audit and evaluation (Lee & Johnson, 1998). The role of the legislature in every stage differs from one country to another. For instance, the U.S. Congress focuses on the ex-ante process, in which various financial committees decide fiscal parameters, tax policy, and the allocation of available funds. However, the Congress has no dedicated committee for the consideration of audit findings. In the German Bundestag, for example, the Budget Committee both approves the annual budget and later considers audit results (Wehner, 2004). The contribution of legislatures in public budgeting can be best assessed along the main stages of the budgetary cycle (Lienert, 2005; Wehner, 2007). Traditionally, using game theory models, the literature about legislative budgeting has evaluated the role of parliaments in the initial phases of the budgetary process (Saporiti & Streb, 2008). However, parliaments not only oversee ex-ante, in the drafting and approval stages. They also do it concurrently, during the execution stage, as well as ex-post, in the audit and evaluation stage. In fact, ex-ante scrutiny of the draft budget supports accountability for policy; in-year scrutiny provides an opportunity to perceive deviations between the approved budget and actual spending; and ex-post scrutiny of audit findings supports accountability for policy implementation (Wehner, 2007). Therefore, we should consider the role of the legislature in budget planning and expenditure allocations (ex-ante), budget execution (during), and evaluation (ex-post) phases of the budget process (Stapenhurst et al., 2008; Wehner, 2007).

The potential role of legislature at each stage of the budgetary process is displayed in Figure 1.

The potential role of the legislature along all stages of the budgetary process.

The annual budget process is embedded within a broader socio-economic and political environment that affects the potential for legislative scrutiny (Hudson & Wren, 2007). In fact, there may be reverse causality, such that budget transparency may affect the degree of legislative budgetary oversight. According to Barraclough and Dorotinsky (2008), both IBP’s and OECD’s recommended good practices defend that legislatures should scrutinize the budget to hold governments accountable and that the executive should report transparent budget to enable meaningful engagement in the budget process by the legislature. This acknowledgment by both IBP and OECD indicates the reverse causality between budget transparency and legislative budgetary oversight.

So far, we have studied the impact of legislative budgetary oversight on budget transparency and we have also showed that we expect a reverse causality. Now we turn our focus on the reverse influence, that is, how budget transparency affects legislative budgetary oversight. As von Hagen (1992) and Bernoth and Wolff (2008) state, parliamentary oversight can be reduced by fiscal misreporting. Therefore, transparency is considered as a cross-cutting issue that has an influence on the legislative potential to be involved in each stage of the budgetary cycle. For instance, regarding the first step of legislature’s involvement in the budgetary process, legislatures require transparent information to be able to prepare the budget (Anderson, 2008). But not only in the first step, but also through the whole budgetary process. Thus, legislative oversight throughout the budgetary cycle requires comprehensive, accurate, appropriate, and timely information to be disclosed by the executive (Wehner, 2004, 2007). If the budget transparency is undermined by the executive, for example, by manipulating budget figures, the oversight role of the legislature is clearly hindered (Wildavsky & Caiden, 2001).

Apart from budget transparency, the literature identifies institutional/political and socio-economic factors that also impact the degree of legislative budgetary oversight.

Institutional and political determinants of legislative budgetary oversight

Type of government

The choice between presidential and parliamentary systems of government has several implications, for example, on budgetary oversight (Lijphart, 1992). Indeed, in presidential systems, where legislature and executive powers are strongly separated, the legislature is a powerful agenda-setter and decision-maker and it is able to reinforce its budgetary oversight over the executive (Dubrow, 2002; Lienert, 2005). However, in parliamentary systems, where there is no a clear separation of powers between the legislature and the executive, the former generally has fewer opportunities for oversight (Dubrow, 2002). In fact, although Parliament votes on the annual budget, if the government has a majority in Parliament, the government alone determines the shape and size of the budget (Lienert, 2005).

However, Wehner (2005) does not find a significant relationship between the government system and the legislative budgetary oversight.

Type of legislature

If members of a second legislative chamber are independently elected, both chambers may have different points of view over draft budget law proposals. The second chamber, depending on its constitutional and legal powers, can veto budget legislation that has already been adopted by both the government and the first chamber. Consequently, whether a second chamber of the legislature is provided with budgetary powers, it strengthens the legislative budgetary powers relative to those of the executive (Lienert, 2005).

Legal system

Legal culture helps explain why some legislatures have more budget authority than others. In continental countries, high-level courts ensure that budget-related laws are consistent with written constitutions. In these countries, the Constitution specifies key elements of the annual budget and requires that the budget system be established by law. However, in Westminster countries, the legal formalities are lighter and the options for legal instruments other than formal statute are greater. Therefore, the latter group is unrestrained by extensive written constitutions and even written constitutional provisions for budgeting are interpreted in a liberal way. Moreover, in Westminster countries, the delegation of budget authority to the executive appears to be higher than that in the legally formalistic ones (Lienert & Jung, 2004). In fact, Wehner (2005) finds that Westminster-heritage countries’ legislatures have fewer budgetary powers.

Supreme Audit Institution’s (SAI) budgetary oversight

The audit and evaluation stage follows the end of the fiscal year (Wehner, 2007). A SAI, such as an auditor general or audit court, is tasked with assessing government accounts and financial statements (Stapenhurst & Titsworth, 2001). Strengthening SAIs’ capacity and improving their relationship with public accounts committees may help improve legislative budgetary oversight (Santiso, 2005a).

In this respect, Santiso (2006) finds that external auditing does not appear to be related to the strength of legislative budgetary powers, while there is a higher correlation between the auditing and the centralization of budgetary powers in the executive. According to this author, these results suggest that there is a significant gap between external auditing and legislative oversight and that SAIs are required to counteract weaknesses in legislative oversight and check executive’s discretion.

Party discipline

Party discipline involves voting along party lines although the outcome does not fully match individual legislators’ preferences (von Hagen, 1992). An overly strict party discipline may constrain legislators’ actions (Hudson & Wren, 2007). Party majorities only ensure the predictability of legislative behavior when matched with tight party discipline, which is not always the case (Wehner, 2004). Legislators may cultivate a “personal vote” and distinguish themselves from their party affiliation, diminishing the ability of government parties to enforce party discipline (Wehner, 2005).

This separation of purpose can be attributed to the effects of different electoral systems. Carey and Shugart (1995) investigate how electoral formulas induce legislators to cultivate a “personal vote.” In this regard, candidate-centered electoral systems are usually associated with low levels of party cohesion (Wehner, 2004). This contrasts with party-centered systems, where the alignment of ideologies leads to more cohesive governments (Lienert, 2005). This latter electoral system, which improves party cohesion, may increase legislators’ political incentives to oversight budget executions (Santiso, 2005a).

From an empirical point of view, however, Wehner (2005) does not find a significant relationship between party discipline and legislative budgetary oversight.

Political competition

Political majorities have an important effect on parliaments’ role in the budgetary process (Leston-Bandeira, 1999; Young, 1999). When the interest of a legislative majority and the executive coincide, the majority has little incentive to oversee the executive. It is the opposition who has the greatest interest and incentive to oversee government, so the degree of political competition becomes essential as far as legislative budgetary oversight is concerned (Messick, 2002). Therefore, the strength of legislative opposition is a key factor to explain the effectiveness of legislative oversight. The executive dominates budget formulation and execution, so that the partisan participation in the budgetary process depends on parties’ relations with the executive (Santiso, 2005a). When there are minority governments, the legislature has relatively more budget powers, as the parties not represented in the government can force it to amend the budget (Lienert, 2005). Therefore, it is expected that legislatures exert more oversight power in countries with minority governments, as the difference of preferences between the legislature and the executive is widened. In fact, Wehner (2005) finds that legislatures invest in more complex scrutiny structures if the political system is characterized by protracted spells of divided government. However, this author cannot prove that divided governments have a positive effect on legislative budgetary oversight.

Socio-economic determinants of legislative budgetary oversight

Economic level

According to Wehner (2005), institutions may be shaped by the broader development context of a country. In this vein, Wehner (2005) states that the economic level of a country may affect the degree of legislative budgetary oversight over the executive. Nevertheless, this author fails to empirically show that the economic level have a positive effect on legislative budgetary oversight.

Degree of democracy

The democratic level of a country may also have an effect on the degree of legislative budgetary oversight. According to O’Donnell (1998), there is growing awareness of the weaknesses of governments’ oversight mechanisms and accountability and the consequent need to enhance “horizontal accountability” institutions. The ability of legislature to act as independent institutions for “horizontal accountability” is expected to be more developed in democratic countries than in authoritarian regimes or where democracy is weakly entrenched. However, from an empirical point of view, Wehner (2005) does not find a significant relationship between the democratic level and legislative budgetary oversight.

Other Determinants of Budget Transparency

Institutional and political determinants of budget transparency

Legal system

Laws on access to information are a powerful tool to enhance government transparency (Matheson & Kwon, 2003). Nevertheless, the effectiveness of these laws may depend on the type of legal system in place.

Common law countries are traditionally more market- and less government-oriented than civil law ones, so that the greater protection of property against the state found in the former improves various aspects of government performance. This may manifest itself directly on outcomes, or through increased attention paid to governance (La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 1999). In this way, Alt and Lassen (2006) find that common law countries are more fiscally transparent than civil law ones.

Political competition

Alt, Lassen, and Rose (2006) state that a high level of political competition encourages ruling politicians to promote transparency and reduce discretion, regardless of their partisan goals, as they want to tie other politicians’ hands, whether those others are potential successors or fellow incumbents with whom they are currently sharing the power. However, Messick (2002) argues that opposition party members are more likely to request information from the government than members from the governing majority as a way to criticize and scrutinize its actions. Thereby, a higher political competition may lead governments to disclose less information, as it could be used to scrutinize their actions (Wehner & de Renzio, 2013).

From an empirical point of view, whereas Alt et al. (2006) and Wehner and de Renzio (2013) find that political competition has a positive effect on fiscal transparency, Andreula et al. (2009) do not confirm it.

Ideology

According to Schick (2003), the budget process is politically neutral and it suits both left-wing and right-wing governments. However, Alt et al. (2006) state that politicians can change the level of transparency as a way to achieve their political goals. Ferejohn (1999) posits that politicians in favor of a larger public sector should increase transparency so as to make voters trust them with more resources (Alt et al., 2006). In this sense, the “partisan politics matters” (PPM) thesis, posited by Cusack (1997), states that left-wing parties favor public spending expansion whereas right-wing parties aim for budget reductions. Accordingly, if we connect both ideas, progressive governments, favoring a larger public sector, are expected to keep higher levels of transparency than their conservative counterparts as a way to account for the greater amount of resources they manage.

In this regard, Bastida and Benito (2007) find that progressive and conservative governments hold similar transparency levels. In the same way, Alt et al. (2006) do not show a statistically significant relationship between ideology and fiscal transparency.

Socio-economic determinants of budget transparency

Economic level

Grigorescu (2003) argues that richer countries (in terms of Gross Domestic Product [GDP] per capita) are less worried about the high cost of gathering, processing, and disclosing information. Therefore, they are more likely to adopt laws on access to information than poorer countries. However, this author also states that, in poorer countries, citizens have greater incentive to request information about government and policies, as the level of satisfaction with government actions is lower than that in wealthier countries.

In this respect, Hameed (2005) shows that the wealthier a country, the more transparent its budget reports. However, Alt et al. (2006) do not prove a significant relationship between economic level and transparency.

Degree of democracy

The idea that citizens have a right to fiscal information comes from a long-standing tradition. However, this right is unlikely to be fulfilled without a mechanism that helps ensure disclosure (Wehner & de Renzio, 2013). If there are free and fair elections, citizens as voters have access to such mechanism that allows them to get rid of bad incumbents. This, in turn, may affect the degree of fiscal transparency (Brender & Drazen, 2005). In this way, Rosendorff (2004) shows that a country’s democratic level has a significant impact on its degree of transparency: As democratic accountability rises, so does government transparency.

However, Martin and Feldman (1998) argue that a democratic political system expands the realm in which citizens can engage, but it is not itself a factor for promoting government transparency. In fact, some autocratic governments have enhanced their fiscal transparency as a way to attract foreign investment and development assistance. Moreover, democratically elected governments may have incentives to limit disclosure (Kono, 2006; Mani & Mukand, 2007). As Hollyer, Rosendorff, and Vreeland (2011) state, the greater vulnerability to citizens’ disapproval may make democratic incumbents more inclined to obfuscate or withhold information than their autocratic counterparts, who are less worried about citizens’ perceptions.

Fiscal performance

Instruments such as transparency and accountability are essential to obtain greater governments’ fiscal performance. These instruments are important not only to enhance authorities’ competent economic management but also to reduce their incentives to be fiscally irresponsible (Rogoff, 1990). Thereby, the larger debt and balance ratios over GDP, the more important the influence of the government on the economy. Consequently, the demand for budget transparency is expected to be greater (Benito & Bastida, 2009).

Moreover, according to the agency theory, politicians have incentives to reduce the cost of debt and this way increase the financial resources available for other programs that enhance incumbents’ welfare. This makes politicians disclose voluntary information to enhance creditors’ monitoring role (Zimmerman, 1977).

In this respect, Alesina and Perotti (1996) and Alt et al. (2006) show that higher levels of debt are associated with lower transparency. Nevertheless, Benito and Bastida (2009) find that there is no effect of government debt on budget transparency, whereas there is a positive correlation between national governments fiscal balance and budget transparency. Similarly, Alt et al. (2006) argue that both higher deficits and higher surpluses contribute to greater fiscal transparency.

Econometric Procedure

Sample

We use a sample of 94 countries as these are the only ones included in a survey on central governments’ budget transparency and accountability (Open Budget Survey) published by IBP in 2010. This information is crucial for our study, given that it is used to measure our main dependent variable (the degree of budget transparency) as well as to build the legislative budgetary oversight indicators.

One of the countries, East Timor, drops because after a preliminary descriptive analysis it is considered an outlier. East Timor has the highest government balance (239.27%). If we remove it from our sample, this variable takes a maximum value of 10.61%. Therefore, our final sample consists of 93 countries.

Open Budget Survey data were collected in 2009 (IBP, 2010). Accordingly, all institutional, political, and socio-economic data refer to 2009.

Econometric Model

This article aims to determine what institutional, political, and socio-economic factors promote central governments’ budget transparency, focusing primarily on how the budgetary oversight of the legislature affects budget transparency.

We run a 2SLS regression as a way to solve the endogeneity problem between legislative budgetary oversight and budget transparency. 2SLS ensures that estimators are consistent when endogeneity exists in the model, which is assumed according to the literature (see previous section). In a first stage, the endogenous variable is regressed on the instrument(s). The instruments have to be correlated with the endogenous variable but not with the error term of the underlying equation. In this way, the variation in the endogenous variable that is not correlated with the error term is isolated. In a second stage, the endogenous variable is replaced with the resulting predicted value (Bascle, 2008; Wooldridge, 2002).

In this regard, we first analyze the determinants of legislative budgetary oversight along all phases of budgetary process. Then, we use these determinants as instruments for legislative budgetary oversight in the budget transparency determinants’ regression, using 2SLS estimation.

To analyze the determinants of legislative budgetary oversight along all phases of budgetary process, we estimate the following regression:

where subscript i (i = 1 . . . 93) represents each country, α is the constant of the equation, and ϵ i is the error term. yi are the three indicator of legislative budgetary oversight according to each phase of budgetary process (ex-ante, during, and ex-post budgetary oversight) as well as the global legislative budgetary oversight indicator. Xji is the vector of explanatory variables (type of government, type of legislature, type of legal system, SAI budgetary oversight, party discipline, political competition, economic level, and democratic level).

We use ordinary least squares (OLS) estimation for three of the dependent variables: ex-ante, during, and global legislative budgetary oversight. These three variables are continuous, that is, they take values from 0 to 100. However, in the ex-post legislative oversight regression, we use an ordered probit estimation as this indicator is built based on one questionnaire item and therefore it has a discrete ordinal nature (Greene, 2003).

As noted above, to examine the determinants of budget transparency (budget.transparency), we use the 2SLS estimator. In this analysis, we only include the global legislative budgetary oversight indicator (leg.oversight), as it is a summary variable that considers the degree of budgetary oversight of the legislature over the executive along all phases of the budgetary process. Therefore, we estimate the following system of equations:

where subscript i (i = 1 . . . 93) represents each country, α is the constant of the equation, and ϵ i is the error term. As stated above, Xji is the vector of legislative budgetary oversight determinants (type of government, type of legislature, type of legal system, SAI budgetary oversight, party discipline, political competition, economic level, and democratic level). The leg.oversight variable in equation (3) is replaced with its predicted value from equation (2), using legislative budgetary oversight determinants as instruments. Wji is the vector of other budget transparency determinants (type of legal system, political competition, ideology, democratic level, economic level, government debt, and government balance).

Variables

We use the 2010 OBI, published by IBP in 2010, to measure the level of budget transparency (budget.transparency). The IBP collaborates with civil society around the world to use budget analysis and advocacy to improve governance and reduce poverty. The main aim of IBP is making government budgeting more transparent and participatory, more responsive to national priorities, better able to resist corruption, and more efficient and effective. In support of this collaboration, the IBP also provides national governments with technical and financial assistance, comparative research opportunities, information exchange, and peer networking. In fact, the IBP has released the Open Budget Survey biennially since 2006. It is based on an exhaustive questionnaire (Open Budget questionnaire) intended to gather a comparative data set on the public availability of budget information and other accountable budgeting practices around the world. The 2010 Open Budget questionnaire consists of 123 questions and has been conducted in 94 countries by independent budget experts who are not associated with national governments (IBP, 2010). Out of the total 123 questions, only 92 evaluate public access to budget information, which were averaged by IBP to build the 2010 OBI. This index ranges from 0 to 100, where the greater the score, the higher the degree of budget transparency.

This questionnaire also covers additional important topics for civil society, such as legislative oversight or the role of the SAI. Indeed, 22 of the 123 questions that comprise the 2010 Open Budget questionnaire assess how the legislature and the SAI can contribute to budget transparency and accountability in a country. The questionnaire therefore provides us data to build the other dependent variables, that is, legislative budgetary oversight indicators. We take those items that reflect the legislature’s ability to provide effective oversight over the budget (IBP, 2010). We organize them into three groups to capture the corresponding phases of the budgetary process. Thus, we get three indicators of the degree of legislative budgetary oversight, one for each stage of the budgetary cycle. Moreover, we build a global legislative budgetary oversight indicator. See Appendix A for a full description of questions included in each indicator.

The first indicator seeks to measure the degree of ex-ante legislative budgetary oversight over the executive. It consists of a set of seven questions from the Open Budget questionnaire. Each question takes a value (100, 67, 33, or 0) depending on the strength of the ex-ante legislative budgetary oversight. The responses to these questions have been averaged to build the leg.pre index for each country:

where leg.pre i stands for leg.pre Question Number i.

This index ranges from 0 to 100, where the higher the score, the greater the degree of ex-ante legislative budgetary oversight over the executive.

The second index (leg.dur) measures the degree of legislative oversight during budget execution. We average three Open Budget questionnaire items to build this index.

where leg.dur i stands for leg.dur Question Number i.

This variable also ranges from 0 to 100. The higher the score, the greater the degree of legislative budgetary oversight during budget execution.

To measure the level of ex-post legislative budgetary oversight (leg.post), we use a single question: Question Number 11 (Q. 120 in Open Budget questionnaire). This question, and thus, this variable, takes a value 100, 67, 33, or 0 according to the degree of ex-post legislative budgetary oversight (100 high ex-post oversight; 67 medium ex-post oversight; 33 low oversight; 0 scant or no ex-post oversight).

Finally, we build the variable leg.oversight that accounts for the global legislative budgetary oversight as it considers the degree of legislative budgetary oversight along the whole budgetary process. It is a summary variable that averages the scores obtained from Questions 1 to 11.

where leg.oversight i stands for leg.oversight Question Number i.

This variable ranges from 0 to 100. The greater the score, the higher the global legislative budgetary oversight.

Concrete values of leg.pre, leg.dur, leg.post, and leg.oversight for every country are available on request to the authors. See Table 1 for the description of dependent variables.

Definition of Variables and Descriptive Statistics.

Note. The aim is to test whether there is an effect of open list proportional representation, as this electoral system is often regarded as candidate-centered. IBP = International Budget Partnership; OBI = Open Budget Index GDP = Gross Domestic Product.

See Appendix B (Table B1) for a full description of the questions included in sai variable.

Electoral system has been taken as a proxy of party discipline, in agreement with previous studies (Wehner, 2005).

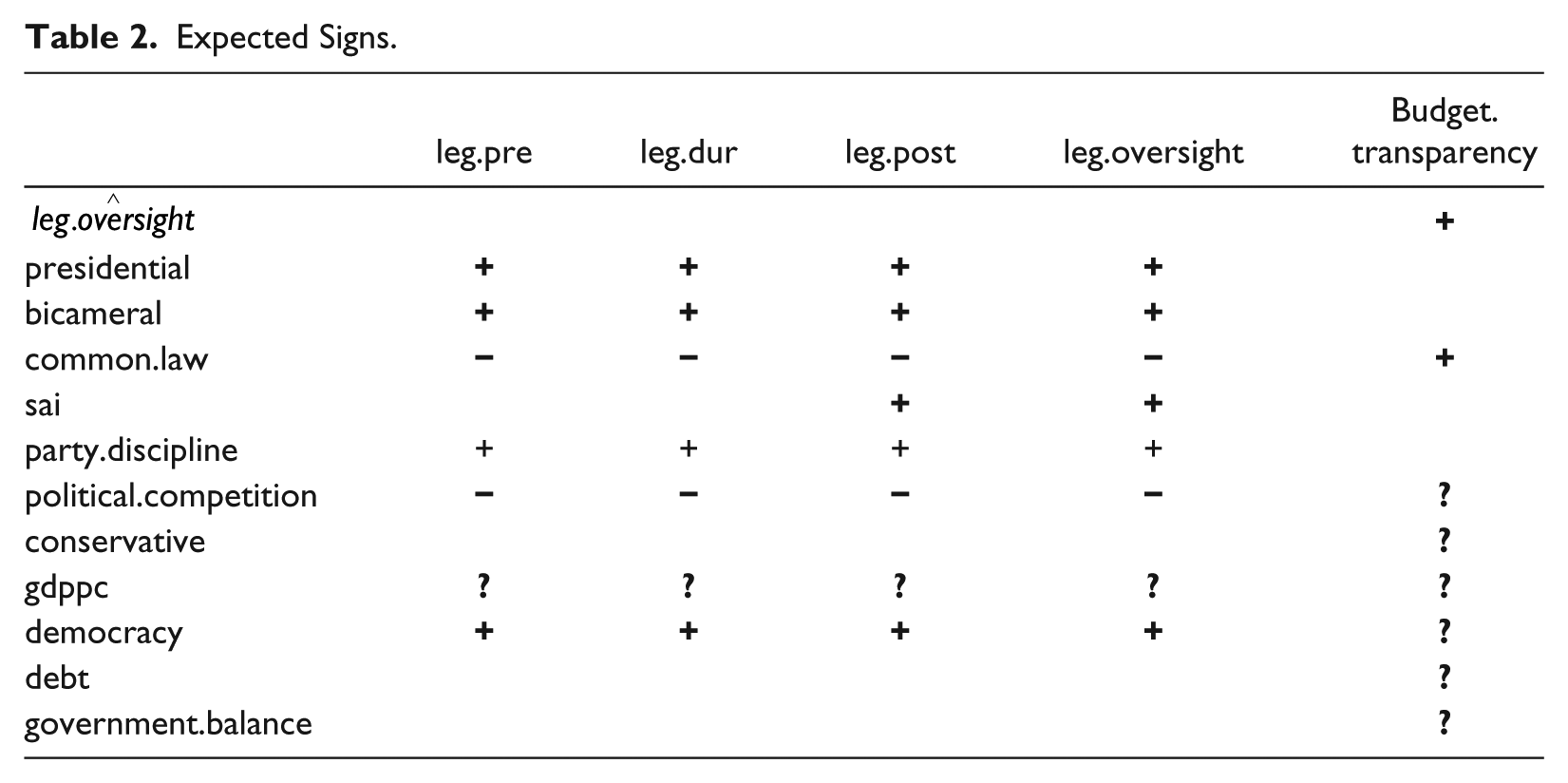

As for independent variables, they have been selected in agreement with the literature and taking into account the available data set. Table 1 also describes the independent variables. Table 2 presents expected sign for independent variables in each regression according to the literature.

Expected Signs.

Finally, Figure 2 shows the relationship between the two main variables at stake, that is, legislative budgetary oversight (leg.oversight) and budget transparency (budget.transparency). This preliminary analysis confirms the theoretical expectations about the relationship between these two variables.

Relationship between budget.transparency and leg.oversight.

Results

Determinants of Legislative Budgetary Oversight

Table 3 presents the results of OLS and ordered probit regressions.

Legislative Budgetary Oversight Determinants.

Note. OLS estimation. T-values in parentheses. Maximum VIF (Variance Inflation Factor

10%. **5%. ***1%.

Regarding institutional and political determinants of legislative budgetary oversight, the type of government (presidential) appears not to affect the legislative budgetary oversight in any phase of budgetary process. Thus, both in presidential and parliamentary systems, the legislature has the same opportunities for budgetary oversight. This finding agrees with Wehner (2005).

The positive and significant coefficient of bicameral in leg.post indicates that bicameral legislatures have a greater ex-post budgetary oversight over the executive than unicameral ones. Our results confirm previous literature such as Lienert (2005), who states that a second chamber of the legislature with budgetary powers enhances the budgetary powers of the legislative body. However, we can only prove this relationship partly, as it is significant only for ex-post legislative budgetary oversight.

Contrary to the mainstream literature, the positive sign of common.law in leg.pre, leg.post, and leg.oversight indicates that common law legislatures exert higher budgetary oversight than their civil law counterparts. Previous literature shows that in common law countries (Westminster), the delegation of budget authority to the executive appears to be higher than that in civil law countries (Lienert & Jung, 2004). However, our interpretation is that in common law countries, this higher budgetary discretion of the executive encourages legislatures to oversight it. This relationship is largely confirmed by our data, as it is significant in three of the four regressions, including leg.oversight regression, which comprises all stages of budgetary process.

The positive and significant coefficient of variable sai indicates the positive effect of SAIs on legislative budgetary oversight. We find a positive effect not only on ex-post legislative budgetary oversight, as previous literature states (Lienert, 2005; Stapenhurst & Titsworth, 2001; Wehner, 2007), but also on legislative budgetary oversight along all stages of budgetary process. A possible explanation is that if the audit process is effective, its findings are reflected in future budgets (Wehner, 2007) and thus, in future budgetary processes.

Our results indicate that legislative budgetary oversight does not depend on either party discipline (party.discipline) or political competition (political.competition). These findings agree with Wehner (2005).

Turning to socio-economic determinants of budgetary oversight, the positive sign of gdppc in leg.pre indicates that economic level has a positive effect on ex-ante legislative budgetary oversight. Regarding this phase of the budgetary process, our results are in line with Wehner (2005), who states that the economic level of a country may affect the degree of legislative budgetary oversight over the executive.

Finally, with regard to the degree of democratic level (democracy), we show an impact on leg.pre (ex-ante budgetary oversight) and leg.dur (legislative oversight during budget execution). Thus, our findings partly agree with O’Donnell (1998) that posits that the ability of the legislature to act as independent institutions for “horizontal accountability” is expected to be higher in democratic countries.

Determinants of Budget Transparency

In this section, we analyze whether legislative budgetary oversight, among other factors, affects budget transparency. The Durbin–Wu–Hausman endogeneity test confirms our theoretical assumption on the endogeneity of leg.oversight and budget.transparency. Thus, the proposed 2SLS regression is appropriate (see Table 4). Sargan test does not reject the validity of the instruments used.

Budget Transparency Determinants.

Note. First- stage regression not reported. 2SLS (two stage least squares) estimation. Z values in parentheses. 2SLS instruments: presidential, bicameral, common.law, sai, party.discipline, political.competition, democracy, gdppc, conservative, debt, government.balance.

10%. **5%. ***1%.

As expected, after controlling for endogeneity, legislative budgetary oversight over the executive (

The variable commom.law has a significant effect on budget.transparency. Thus, we can conclude that common law countries have higher levels of budget transparency than their civil law counterparts. Common law countries, in our opinion, seek to justify their commitment to greater protection of property against the government and, thus, to governance. This result confirms Alt and Lassen (2006), who show that common law countries are more fiscally transparent than civil law ones.

The variable political.competition affects budget.transparency. It demonstrates that when political competition is high, incumbents promote transparency, as they want to tie other politicians’ hands. Alt et al. (2006) and Wehner and de Renzio (2013) also find that political competition has a positive effect on fiscal transparency.

Regarding variable conservative, our results indicate that budget transparency does not depend on ideology, showing that both progressive and conservative governments disclose similar budget information. This finding contradicts the PPM thesis but agrees with Schick (2003), who states that the budget process is politically neutral.

With regard to socio-economic determinants, the estimates reveal that the higher the economic level (gdppc), the greater the budget transparency. This feature confirms Grigorescu (2003), who states that more developed countries are more likely to adopt laws on information disclosure, which enhances their transparency. Hameed (2005) also finds that economic level has a positive effect on budget transparency.

The variable democracy shows that the democratic level does not affect budget transparency. This finding agrees with Martin and Feldman (1998), who state that a democratic political system is not itself a factor for promoting government transparency.

Finally, regarding fiscal performance of the country, both government debt (debt) and government balance (government.balance) appear not to affect central government budget transparency (budget.transparency). Our results, however, are partly in line with Benito and Bastida (2009), who show that there is no effect of government debt on budget transparency.

Conclusion

This article aims to analyze the determinants of budget transparency in an international comparative approach, focusing primarily on how the legislative budgetary oversight over the executive affects budget transparency. We use a sample of 93 countries surveyed by IBP in 2010. We run 2SLS regression to examine the determinants of budget transparency as a way to solve the endogeneity problem between legislative budgetary oversight and budget transparency. In this respect, we first analyze the determinants of legislative budgetary oversight along all phases of budgetary process. Then, we use these determinants as instruments for legislative budgetary oversight in the 2SLS regression.

Our results show that there are many institutional, political, and socio-economic factors that affect legislative budgetary oversight along the different phases of budgetary process. With regard to institutional and political factors, we can only partly observe that bicameral legislatures have more opportunities for budgetary oversight than unicameral ones. In addition, we note that common law legislatures have a greater budgetary oversight over the executive than civil law ones. This may indicate that the excessive executives’ budgetary discretion in common law countries encourages those countries’ legislatures to oversight them. Finally, we conclude that higher SAIs’ budgetary oversight leads to greater legislative budgetary oversight, but not only ex-post also along all stages of budgetary process. As an implication for public policy, this finding supports the idea that a strong, independent SAI, properly provided with human and technical resources, is key to enhance the legislative oversight role.

In respect of socio-economic factors, economic level and democracy appear to have a positive effect on legislative budgetary oversight along some of the stages of budgetary process. Our findings are in line with previous literature, which states that institutions may be shaped by the broader development context of a country, namely, economic and democratic level.

All these findings are very important as further research was needed into the political and institutional determinants of parliaments’ role in the budgetary oversight, according to Santiso (2006). Moreover, we analyze the determinants of legislative budgetary oversight along all phases of budgetary process, whereas previous analyses focused on parliaments’ involvement in the initial phases of the budget (Saporiti & Streb, 2008).

The main finding of our article is that legislative budgetary oversight has a positive effect on budget transparency. This relationship, as far as we know, has never been empirically tested. Therefore, our results confirm the ambition theory, which suggests that legislative oversight is an essential tool to scrutinize executive policy making. Specifically, we confirm international organizations’ assumptions, which state that enhanced legislative budgetary scrutiny leads to deeper government accountability and greater transparency in public finances management. For example, OECD claims that Parliament should be able to examine any fiscal report it deems necessary (OECD, 2001). Concrete countries, such as France, Brazil, South Africa, and Uganda, are already enhancing legislative engagement in budgetary oversight. Our findings show that they are in the right way. However, some process remains to be made. For example, OECD 2003 survey shows that 99% of countries make few, if any, changes to the budget. Besides, legislatures with a greater involvement in the budgetary process need the capacity to analyze budgetary information. However, the same survey shows that 72% of countries do not have specialized budget organizations to advice legislatures in the budgetary oversight task (Barraclough & Dorotinsky, 2008). Our point, in light of our results, is triple. First, regarding practical issues, legislature involvement on budgetary oversight should be enhanced and facilitated as much as possible, as it affects positively the executive accountability and increases budget transparency. A specific budget office supporting technically the parliament would be useful in this respect. Second, the theoretical background indicates that agency problem would be diminished if legislatures exerted a closer oversight on governments’ budget. Third, an enhanced implication of the legislative throughout all phases of the budgetary cycle clearly improves budget transparency.

Regarding other institutional and political factors, our results show that common law countries are more transparent than civil law ones. This may indicate that common law countries strongly protect property against the government, increasing transparency as a way to check that the government is respecting private property. Moreover, we observe that higher political competition leads to greater budget transparency, which indicates that incumbents try to tie other politicians’ hands when closer elections are expected.

Finally, turning to socio-economic factors, only economic level appears to affect budget transparency. This indicates that developed countries’ governments, less worried about the high cost of gathering, processing, and disclosing information, are more fiscally transparent.

From our point of view, our article has two limitations. The first one refers to the process by which legislative budgetary oversight indicators are built. Our proxies for legislative budgetary oversight along the different stages of budgetary process (leg.pre, leg.dur, and leg.post) may suffer of measurement error, as they consist of a small number of items. This may create a bias that lowers the value of our results. However, we further aggregate our three indicators into one (leg.oversight) to obtain a broader synthetic measure of the legislative budgetary oversight. We think that leg.oversight is a relevant indicator of legislative budgetary oversight and is likely to produce stronger results due to the fact that there is more variation in that variable, because it summarizes 11 items. The second limitation has to do with the time ordering of the variables. In fact, various independent variables may cause budget transparency, but the path of the influence could sometimes move in the opposite direction. That is, budget transparency could sometimes be a cause of other variables apart from legislative budgetary oversight.

As future research, a new measure of legislative budgetary oversight along the different stages of budgetary process should be built to confirm the relationships found in this article. Moreover, we think it would be interesting to evaluate the long-term evolution of central governments’ budget transparency. Upcoming data collection on budget transparency practices by IBP will provide a panel data set that would allow in the future within-country assessment of some of the determinants identified in this article. Besides, time series data would allow us to control for the second aforementioned limitation, that is, endogeneity between budget transparency and other variables.

Footnotes

Appendix A

Appendix B

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study has benefited from the financial support of the Spanish National R & D Plan through the research projects ECO2010-17463 and ECO2010-20522 (Ministry of Science and Innovation). It has also received support from the Ministry of Education (University’s Teacher Training, under the National Plan for Scientific Research, Development and Innovation 2008-2011).

Author Biographies

![]()

![]()