Abstract

State governments establish pension systems to provide retirement benefits to public employees. State governments as sponsors, state legislatures as policy makers, and public-sector unions as representatives of public employees may exert considerable influence over the decisions made in pension systems. This study applies a system framework to examine these influences. It focuses on four decisions in pension systems: benefits, employer contributions, employee contributions, and the asset smoothing period. The findings show that changes in the short- and long-term financial conditions of a state government have different influences on pension decisions, and that legislatures and public employee unions play important roles that affect these decisions.

Introduction

Most employees in state governments in the United States are covered by government-sponsored defined-benefit pension systems (Munnell & Soto, 2007). As participants in those systems, public employees receive retirement benefits that are determined by a preset formula that links their retirement benefits to their years of service and their average salary over the last several service years before retirement. In these systems, retirement benefits are usually prefunded by contributions from both governments and public employees and by investment returns from pension assets. Accurate estimations of pension liabilities and costs, timely contributions from the sponsoring governments and employees, and sufficient investment returns from assets are all important for the financial sustainability of public pension systems.

Over the past decade, the growing costs and unfunded liabilities of state and local pension systems in the United States have received a significant attention (The Pew Center on the States, 2010, 2012; U.S. Government Accountability Office [GAO], 2012). Many studies link this underfunding problem with economic, political, and institutional factors (Chaney, Copley, & Stone, 2002; Coggburn & Kearney, 2010; Eaton & Nofsinger, 2004; Giertz & Papke, 2007; Kelley, 2014; Marks, Raman, & Wilson, 1988; St. Clair, 2013; Thom, 2013; Wang & Peng, 2016). Prior studies and anecdotal evidence also suggest that the sponsoring government’s financial condition is correlated with the funding status of pension systems (Chaney et al., 2002; Coggburn & Kearney, 2010; Eaton & Nofsinger, 2004; Giertz & Papke, 2007; Johnson, 1997; Marks et al., 1988; Schneider & Damanpour, 2002). In this study, I employ a system framework to examine the influence of state government’s financial condition on decisions in pension systems. I also discuss the roles of state legislatures and unions in influencing these decisions.

The ways in which a state government’s financial condition affects the decisions in the pension systems it sponsors is an important and interesting topic. On one hand, public pension expenditures account for an average of 7.9% of a government’s budget and compete with other public needs for funding (Munnell, Aubry, Hurwitz, & Cafarelli, 2013). One would expect that state governments have the motivation to cut pension expenditures or postpone expenditures to a future time, especially when governments are experiencing a decrease in their financial resources. In fact, insufficient contribution from governments is one of the most important reasons to explain the underfunding problem of public pensions. The Pew Center on the States (2010) study finds that many states consistently pay less than 90% of the required contributions to pension systems. A Congressional Budget Office (CBO; 2010) report also suggests that governments tend to postpone contributions to pension systems when facing fiscal stress. The most notable example is the state of Illinois. Bunch (2010) shows that Illinois consistently pays far less than the required amount to fund its pension systems. In 2016, Illinois pension systems are only 41.9% funded, resulting in multiple downgrades of its credit rating (Kilroy, 2016).

On the other hand, to protect pension benefits for public employees, responsible decisions in pension systems should be made based on consistent benefit and contribution policies, rather than be influenced by the wax and wane of a sponsoring government’s financial condition. For this reason, many pension systems have established specific institutions to ensure their relative independence from sponsoring governments. In almost all states, public pension systems are administered by trustees who have a fiduciary duty to act in the interests of system members (Peng, 2009). Such institutions may reduce or eliminate the influence of a government’s financial condition on pension decisions.

Legislatures and unions may also influence decisions in pension systems. Legislatures, as policy makers, review and approve important benefit, contribution, and investment policies for public pension systems. Legislators may support or resist state governments’ proposals to reform pension systems depending on their political views or party affiliations. Unions, as representatives of public employees, elect members to the board of trustees to represent employee interests. In the event that governments attempt to reduce pension costs when facing a change in financial condition, unions are more likely to resist changes unless such changes are made in exchange for increases in other forms of compensation.

This study adopts Levine, Rubin, and Wolohojian’s (1981) cutback management framework to examine the influences of sponsoring governments’ financial conditions, legislatures, and unions on decisions in state pension systems. Levine et al. suggest that the combination of financial resources, formal authority, and interest groups interactively determines the administrative responses adopted by a government under fiscal stress. In this study, this framework is referred to as the “system framework.” Based on this framework, the first research question for the study is as follows:

Four pension management decisions are discussed: benefits, employer contributions, employee contributions, and the asset smoothing period. The second research question is as follows:

The rest of the article is organized in four sections. The next section describes how decisions are made in state pension systems. Possible influences from state governments, legislatures, and unions on those decisions are also discussed. Then, the system framework and its application to pension system management are briefly introduced, and research hypotheses are developed based on the system framework. Following that, data, models, and findings are presented and discussed. Finally, the research is concluded with implications for practices and for future studies.

Decisions in State Pension Systems

There are 299 state pension systems in the United States (U.S. Census Bureau, 2015). These pension systems are sponsored by a single employer or multiple employers (Governmental Accounting Standards Board [GASB], 2016). In a single-employer state system, the state government is the sole employer that sponsors the pension system, and only state employees participate in the systems. A multiple-employer system usually covers both state and local employees, and receives contributions from both state and local governments. Typically, the state government is still the biggest sponsor in these systems. A multiple-employer system is either a cost-sharing system or an agent system. In a cost-sharing system, all employers pool their assets and liabilities. In an agent system, employers share only services and have separate accounts for their assets and liabilities.

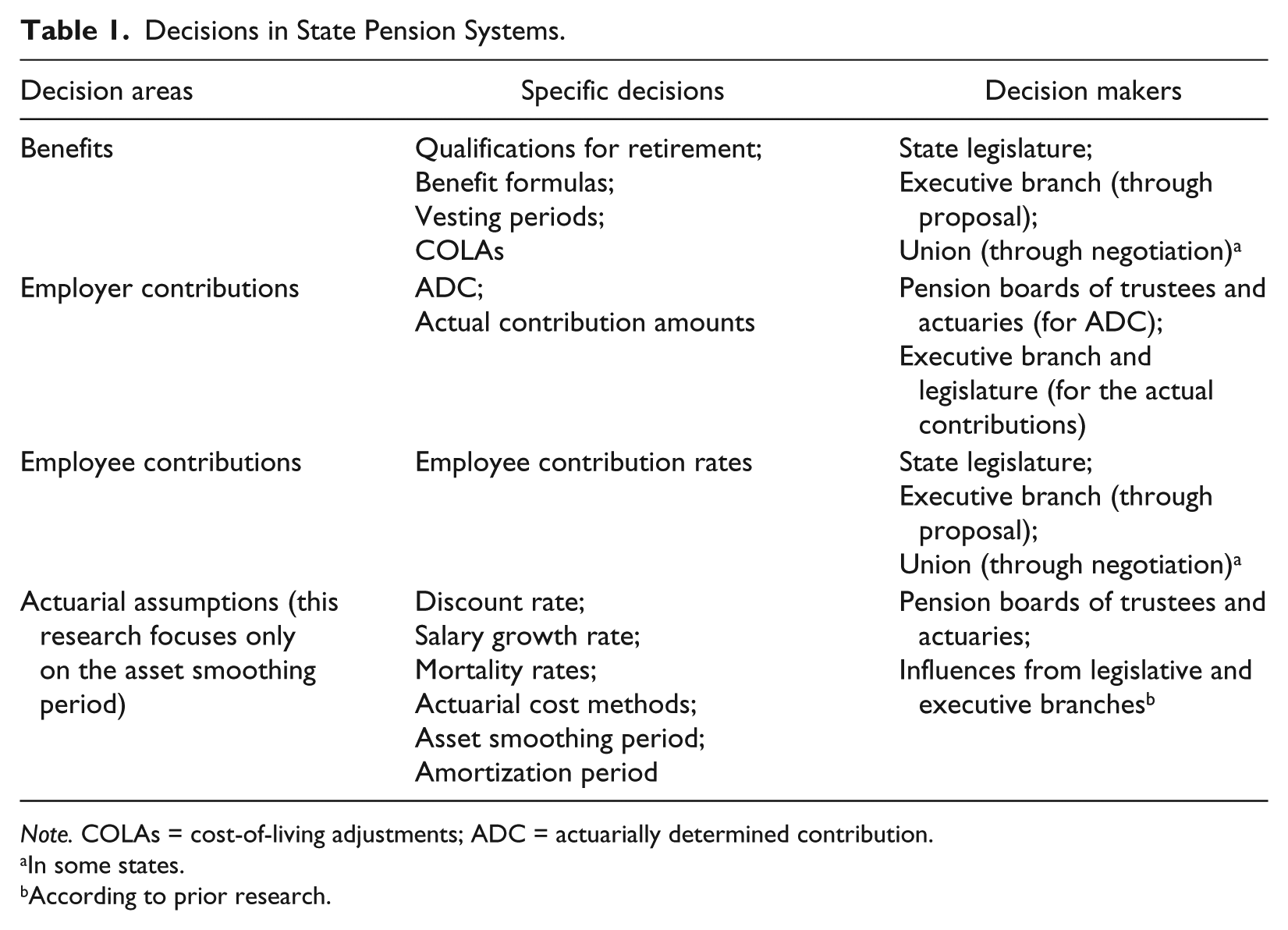

In both single-employer and multiple-employer systems, decisions are made and influenced by many individuals and entities. Table 1 lists important decisions in pension systems and how these decisions are made or influenced by the boards of trustees, sponsoring governments, legislatures, and unions.

Decisions in State Pension Systems.

Note. COLAs = cost-of-living adjustments; ADC = actuarially determined contribution.

In some states.

According to prior research.

Decisions Regarding Pension Benefits

Decisions regarding benefits include qualifications for retirement (normal retirement age and service requirements), the formulas to calculate retirement benefits, vesting periods, and postretirement benefits (cost-of-living adjustments [COLAs]). Pension benefits, and thus pension costs, could be reduced by postponing retirement age, reducing the benefit factor in the formula, increasing the vesting period, and/or reducing COLAs. In state pension systems, pension benefits are usually specified in state statutes and in some states are also protected by constitutional provisions (Monahan, 2010). Under these legal protections, it is extremely difficult, if not impossible, for governments to cut pension benefits for current employees. Governments can propose changes to benefits for new employees, but it is up to legislatures to review and approve such changes. In some states, according to collective bargaining processes, governments are also required to negotiate with unions regarding pension benefits (Steffen, 2001). Depending on different pension statutes, state governments might be able to reduce COLAs or alter the methods of calculating the final average salary, but such actions are usually challenged by unions (Inklebarger, 2011; Snell, 2009, 2010).

For active employees, pension benefits are accrued in each service year as the annual normal cost of the pension system. Adjustments on retirement age, benefit formula, vesting period, or COLAs will be reflected on the normal cost for those employees who are affected by the adjustments. If the adjustments only affect new employees, the impact on the whole system’s normal cost is small when the changes are made but will gradually increase as more employees are covered by the adjusted benefits.

Decisions Regarding Employer and Employee Contributions

In state pension systems, contributions usually come from both employers and employees. Employer contributions are usually determined in a two-step process. The first step is to calculate and report the actuarially determined contribution (ADC), which is the amount required to fully fund pension liabilities in the long term (Eaton & Nofsinger, 2004; Munnell, Aubry, & Haverstick, 2008; Peng & Boivie, 2011). The ADC is calculated by professional actuaries and reported by the pension board of trustees. The second step involves determining the actual contribution amount made by the government in a specific year. A number of governments are required by law to fully pay the ADC, but others are not (Munnell, Haverstick, Aubry, & Golub-Sass, 2008; Peng, 2009). For states that do not have legal constraints on the actual contribution amount, the actual contribution that goes into pension systems is determined as part of the annual budgetary decisions over which state governments and legislatures have discretion. Some governments have fixed or capped the annual contribution rate (Peng, 2009). Such fixed rates or caps potentially reduce the adequacy of contributions to pension systems (Munnell, Haverstick, et al., 2008).

Employee contributions are usually fixed at certain rates that are also specified in the state statutes or contracts that establish pension plans. Decisions regarding employee contribution rates are subject to legal constraints similar to those for benefits because increasing employee contributions is another means of cutting pension benefits. The same influencing factors that affect benefits, including executive proposal, legislative review, and negotiation with unions, also affect decisions relating to employee contributions.

Decisions Regarding Actuarial Assumptions

Pension liabilities and costs are calculated using a set of actuarial assumptions, including the discount rate, salary growth rate, mortality rates, actuarial cost methods, asset smoothing period, and amortization period. The reported pension costs can be reduced by underestimating liabilities or overestimating assets. In a state pension system, actuaries set assumptions according to professional standards and their own evaluation of the system’s historical experience. The board of trustees reviews and adopts the actuarial assumptions suggested by the actuaries.

Professional standards, including Society of Actuary (SOA) guidelines and Governmental Accounting Standards Board (GASB) standards, allow pension systems some discretion in choosing the methods they use to evaluate assets and liabilities. Flexibility of regulations provides opportunities for governments or legislatures to influence the selection of a certain assumption or the timing of adopting new assumptions. This influence is possible through their representatives on a system’s board of trustees. Prior research shows that governments and legislatures influence the actuarial process based on political and financial considerations (Chaney et al., 2002; Eaton & Nofsinger, 2004; Giertz & Papke, 2007; Johnson, 1997; Marks et al., 1988; Romano, 1993; Schneider & Damanpour, 2002; Stalebrink, 2014).

While all actuarial assumptions are important, the asset smoothing period receives a particular attention in this research. Pension systems have considerable flexibility to make decisions regarding asset smoothing. GASB Standards 25 and 27 1 do not place constraints over the kind of smoothing techniques or the length of smoothing periods for public pension systems (GASB, 1994a, 1994b). For governments that are required to make contributions based on their ADCs, changing the asset smoothing period during recession years can be a way to reduce their contributions or reduce contribution volatility. A recent research (Boyd & Yin, 2016) notes that asset smoothing can be “attractive to elected officials or others focused on the near term,” because “asset smoothing could defer contribution increases to periods when government tax revenues have recovered from cyclical declines” (p. 9). Observers of public pension systems also note that systems use asset smoothing to justify benefit increase or to reduce contribution volatility (Baert, 2016; Hardgrave, 2011; Norcross, 2012).

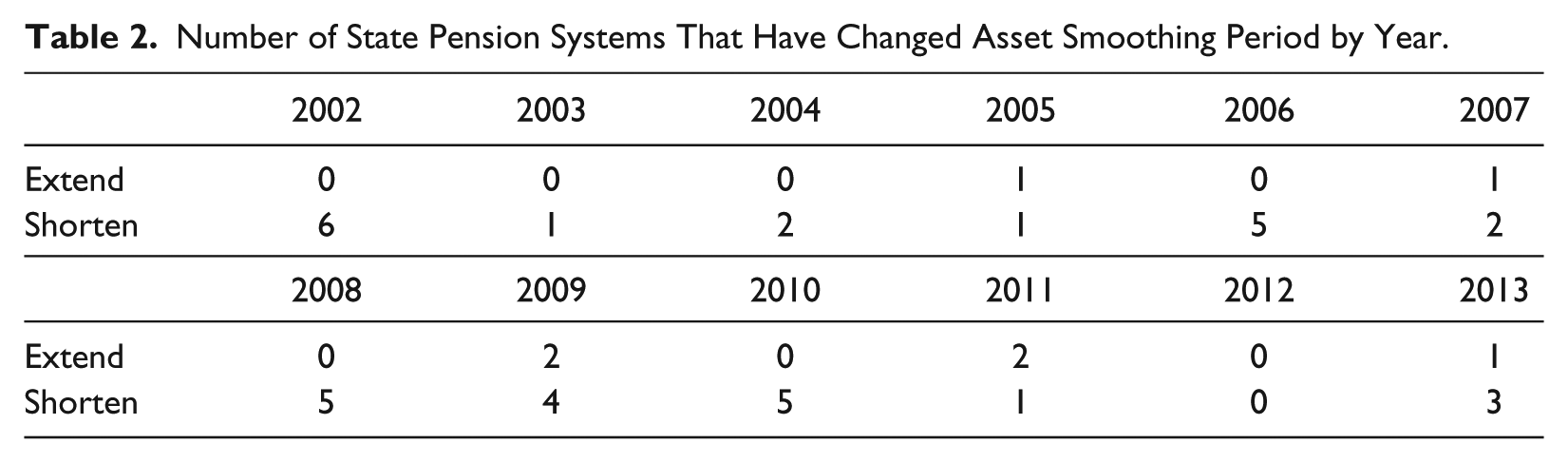

Asset smoothing is widely used in state pension systems, and the smoothing period ranges from 3 to 10 years. According to the author’s calculation using data available from the Public Plans Database, 94.25% of state pension systems report their assets using smoothed values. Of these plans, 42 systems (36.84%) changed their asset smoothing periods during 2002-2013, with 35 systems extending the period and seven systems shortening the period. The distribution of changes in the asset smoothing periods for each year is shown in Table 2.

Number of State Pension Systems That Have Changed Asset Smoothing Period by Year.

State Governments’ Influence on Decisions

As shown in Table 1 and discussed above, state governments exert important influence over decisions regarding pension benefits, contributions, and actuarial assumptions. This influence is typically applied in two ways: (a) through executive proposals to the state legislature and (b) by appointing trustees to the governing boards of pension systems.

First, state governments usually play an important role in proposing pension reforms. For example, in 2011, New York State Governor Cuomo proposed creating a new tier (Tier VI) in the New York State retirement system for newly hired employees with an increased retirement age, lower benefit factor, and higher contributions from employees (Governor Cuomo’s Pressroom, 2011). Tier VI was subsequently adopted by the New York State Legislature (Governor Cuomo’s Pressroom, 2012). In 2010, Governor Christie in New Jersey introduced plans to cut COLAs for all current and future retirees following similar actions by the states of Colorado, Minnesota, and South Dakota, but these plans were challenged in the courts (Governor Christie’s Newsroom, 2010).

Second, state governments influence pension decisions by placing trustees on pension boards. According to a GAO (2008) report, on average, 19.1% of the trustees on pension boards serve because of their positions in state governments (ex-officio trustees), and 51.7% of trustees are appointed by politicians from both the executive and legislative branches. Ex-officio trustees and political appointees from the executive branch represent the interests of state governments. Although these trustees have a fiduciary duty to make decisions that are in the interests of pension beneficiaries, they might still have their own considerations relating to the government’s overall needs.

State Legislatures’ Influence on Decisions

State legislatures establish, review, and approve state statutes that prescribe general policies for pension benefits, contributions, investments, and financial reporting activities. Legislators, depending on the interests they represent, may have different preferences for policies related to public pension systems. Republicans in the legislature may be more concerned with the tax burden pension systems bring to their constituents, while Democrats may support unions and have preferences for employee benefits and retirement security (Munnell, Golub-Sass, Haverstick, Soto, & Wiles, 2008; Thom, 2015). Full-time and well-supported legislators are probably better informed about the issues related to pension systems, which may affect their positions in those issues. When the legislative and executive branches are controlled by the same political party, the legislature may be more likely to support the executive branch for pension reforms.

Public Employee Unions’ Influence on Decisions

A stronger public employee union may be more effective in informing employees about issues relating to pension systems and may be more aggressive in exerting pressure on governments to make policies that ensure public employees enjoy sufficient and sustainable retirement benefits. The influence of unions on pension systems is possible through the representatives of unions on pension boards of trustees. According to the GAO (2008), nearly one third of public pension board members are directly elected by public employees. Unions often play an important role in selecting those board members. Some unions can also negotiate with the government regarding pension benefits. In states where collective bargaining is required or allowed, pension benefits are an important item in the negotiation between the union and the government. Most studies on this topic measure the strength of a union by the percentage of the workers who are covered by its union contract, and studies have tested a union’s impact on pension system funding and generosity; however, these studies have shown mixed results (Bahl & Jump, 1974; Chaney et al., 2002; Johnson, 1997; Marks et al., 1988; Mitchell & Smith, 1994; Munnell, Aubry, Hurwitz, & Quinby, 2011).

A System Framework for Understanding Pension Decisions

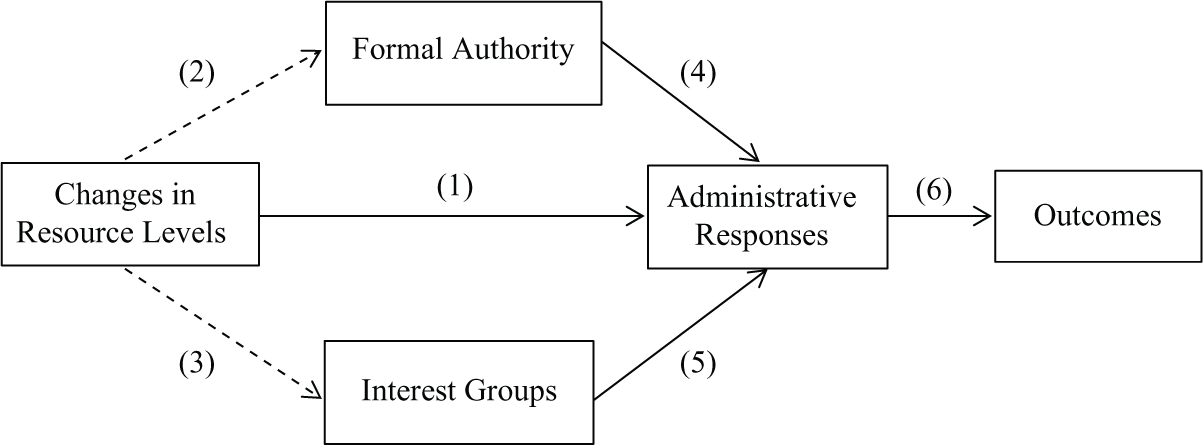

Levine et al. (1981) suggest that a government adopts certain strategies depending on the interactions of several factors: changes in financial resource levels, the formal authority of governments, and the power of interest groups. This model is shown in Figure 1.

System framework of administrative responses to changes in resource levels.

In this framework, administrative responses depend on Changes in resource levels, formal authority, and interest groups. As defined by Levine et al. (1981), Changes in resource levels refer to the strength of growth or the severity of decline of a government’s financial resources. Formal authority refers to the scope and power of the decision-making authority. Interest groups refer to the presence of interest groups, their activity, and the degree of coalition (Levine et al., 1981). As shown in Figure 1, Levine et al. assume that administrative responses are directly associated with changes in resource levels (Relationship 1). The changes in resources also affect the activities and the structures of the formal authority and interest groups, which further create pressures on the administrative responses (Relationships 2, 3, 4, and 5). The combined effects of these three factors determine the administrative responses adopted by the government. Finally, the administrative responses determine outcomes (Relationship 6).

There are three basic arguments in Levine et al.’s framework that are applicable to the analysis in this research 2 :

There are several patterns of administrative responses corresponding to different levels of changes in financial resources. When financial resources decline, but only slightly, governments tend to either ignore problems or postpone spending to the future—thus using the so-called “denial and delay” strategy. With a moderate decline in financial resources, governments use revenue stretching strategies or across-the-board cuts. Finally, when the decline in financial resources becomes severe, governments begin to use targeted cutting strategies, such as layoffs, service cuts, and organizational changes.

With a stronger authority, officials are able to make deeper and more targeted cuts. The strength of formal authority depends on the scope and amount of power granted to administrators and elected officials in the government (Levine et al., 1981). As Levine et al. (1981) expected, if decision makers have a stronger formal authority, dramatic changes in pension policies are more likely to occur.

Stronger and more active, organized interest groups are more effective in protecting their programs or departments from deep cuts.

This system framework can be used to analyze decisions in pension systems. I am interested in whether the three arguments still hold in the context of public pension systems. The following three hypotheses are tested in this research:

Levine et al.’s theory predicts that governments respond to different levels of financial resource changes by using different administrative responses. In state pension systems, changing the asset smoothing period is one accounting trick that can be used to reduce the impact of investment losses, and it can be viewed as a “denial and delay strategy.” Increasing employee contributions can be view as a “revenue stretching strategy.” Unlike employer contributions, employee contributions are external revenues that are outside the government finances. Increasing employee contributions actually reduces a government’s pension costs, so I assume that governments would do so before adopting “targeted cutting strategies.” Finally, the “targeted cutting strategies” in pension systems include cutting employer contributions or cutting pension benefits. Levine et al.’s theory predicts that any “targeted cutting strategy” will face resistance from interest groups, and thus will occur only when the resource decline is acute. Prior studies find that public pension systems facing fiscal stress are likely to reduce employer’s contributions or change actuarial assumptions (Chaney et al., 2002; Eaton & Nofsinger, 2004; Mitchell & Smith, 1994). No prior research has examined the influence of sponsoring government’s financial condition on pension benefits or employee contributions.

In this hypothesis, I assume that the characteristics of a state legislature are associated with decisions in state pension systems but the directions of those associations vary. First, I assume that a liberal position in a state legislature is associated with policies that support the sufficiency of pension benefits and the sustainability of pension systems, which implies increased pension benefits, increased employer contributions, reduced employee contributions, and shorter asset smoothing periods. Second, I assume that when a state legislature is dominated by the same political party that controls the executive branch, policies made by the legislature are more likely to reflect the interests of the sponsoring government, which implies reduced pension benefits, reduced employer contributions, increased employee contributions, and longer asset smoothing periods. These policies aim to reduce the fiscal burden or to reduce contribution volatility for the sponsoring governments. Third, I assume that when legislators receive more staff support, they are more aware of the issues with pension systems; however, the direction of the influence of legislative staff on pension decisions cannot be specified for each decision. In prior studies, Marks et al. (1988) find that legislatures with more staff have constrained the magnitude of pension underfunding, and that a unified government is more likely to reach agreement on policy changes. There is also some evidence to support the argument that political ideology and partisan representation are related to pension funding (Coggburn & Kearney, 2010; Johnson, 1997; Marks et al., 1988; St. Clair, 2013; Thom, 2013).

The most important interest group that supports public pension systems is the public employee unions. The third hypothesis is developed based on the discussion in the previous section regarding the role of public employee unions in pension systems. Prior studies show mixed findings on the relationship between public employee unionization and pension funding (Chaney et al., 2002; Coggburn & Kearney, 2010; Johnson, 1997; Marks et al., 1988; St. Clair, 2013; Thom, 2013), but no research has tested the impacts of unionization on pension benefits, employer and employee contributions, and the asset smoothing period. In the next section, I discuss the data and models used to test these three hypotheses.

Data, Methods, and Findings

The study variables are defined in Table 3, and the equation to test Hypotheses 1, 2, and 3 is given as follows:

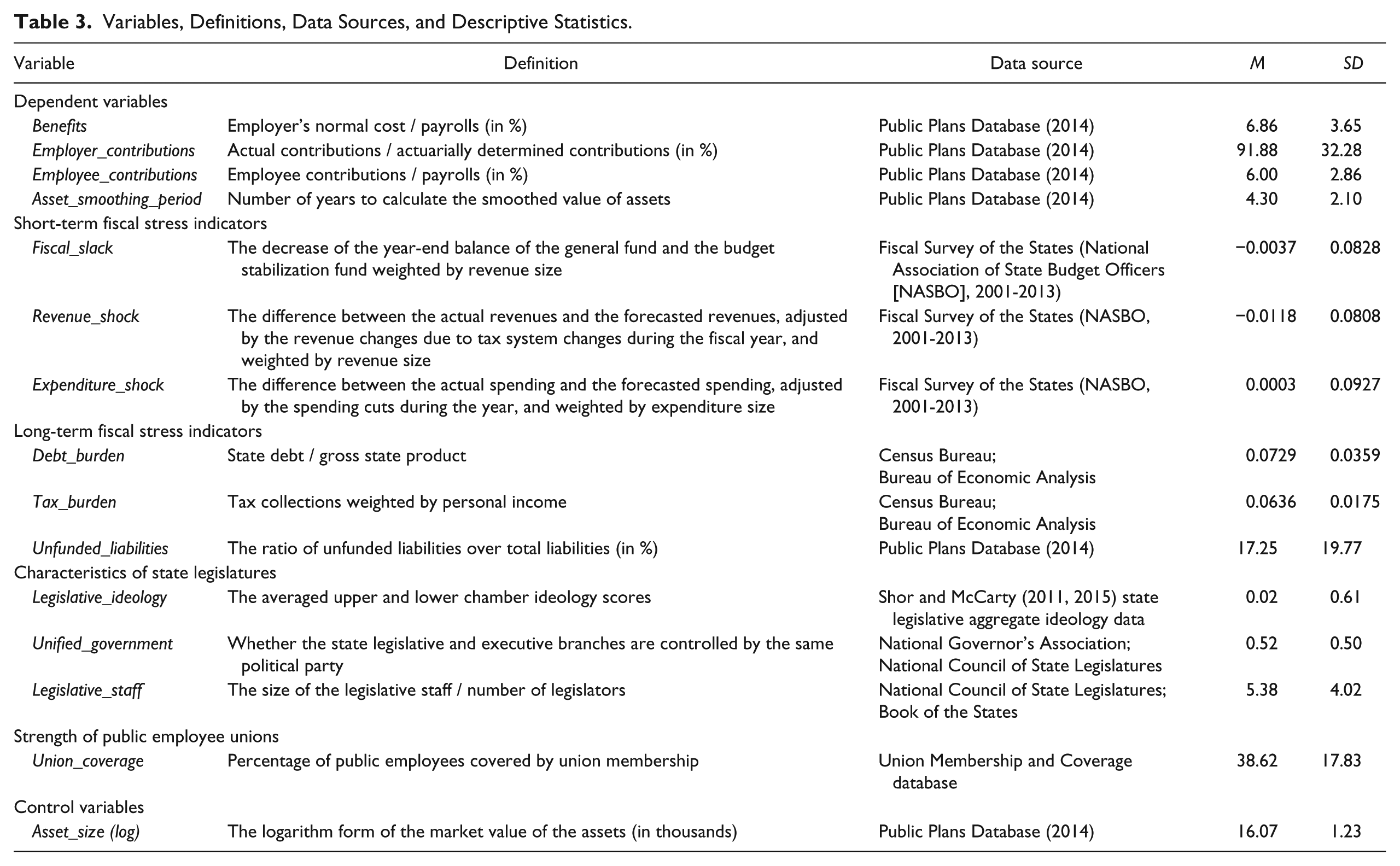

Variables, Definitions, Data Sources, and Descriptive Statistics.

Dependent Variables

Four dependent variables are included in the model. Benefits (Benefits) are measured as the normal costs accrued by active employees in a certain year, divided by total payrolls. The normal costs should capture any changes in benefit provisions. Employer_contributions measures the percentage of ADCs that is actually paid by the sponsoring governments. This is the “flow funding ratio” used by previous studies (Mitchell & Smith, 1994). Employee_contributions is defined as employee contributions compared with total payrolls. Asset_smoothing_period is used as the fourth dependent variable to represent actuarial assumptions for the calculation of pension assets.

Independent Variables

Short- and long-term financial conditions

Public finance scholars identify multiple dimensions of financial condition (Hendrick, 2004; Kloha, Weissert, & Kleine, 2005; Poterba, 1994) and use principal component analysis (PCA) to analyze fiscal indicators and construct indices to measure each dimension of financial condition (Cabaleiro, Buch, & Vaamonde, 2012). This study follows the PCA approach to measure short- and long-term financial conditions. According to Levine et al. (1981), short- and long-term financial conditions may have different impacts on governments’ responses.

Short-term financial condition reflects the decrease of fund balance during a year. It is also affected by the decrease of revenues or increase of expenditures that are out of the government’s expectation. Three variables are constructed to measure short-term financial condition: (a) Fiscal_slack, which is the decrease of the year-end balance of a state’s general fund and budget stabilization fund weighted by revenue size; (b) Revenue_shock, which is the difference between actual revenues and forecasted revenues, adjusted by revenue changes due to tax system changes during the fiscal year, and weighted by revenue size (Poterba, 1994); and (c) Expenditure_shock, which is the difference between actual spending and forecasted spending, adjusted by spending cuts during the year, and weighted by expenditure size (Poterba, 1994).

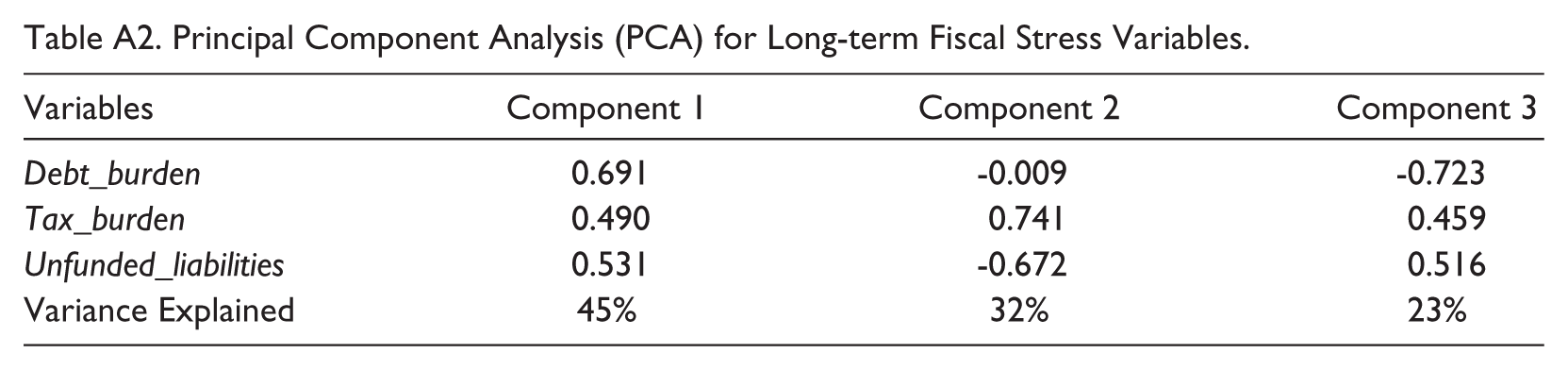

Long-term financial condition is affected by the size of long-term liabilities (including state debt and unfunded pension liability) and potential available revenue sources (tax burden). Long-term financial condition is the cumulative result of a state government’s decisions over many years. Three variables are used to measure long-term financial condition: (a) Debt_burden, which is measured by state debts divided by gross state product (GSP); (b) Tax_burden, which is tax revenues weighted by personal income; and (c) Unfunded_liabilities, which is unfunded pension liabilities divided by total pension liabilities. The third variable Unfunded_liabilities is the measurement of the “funding gap”—the portion of pension liabilities that are not funded by assets.

In the models, I use the declines of financial condition as independent variables and call them fiscal stress in the model. That is, an increase in the fiscal stress variables indicates a deterioration of the financial condition. Each set of fiscal stress measurements is analyzed using PCA.

The results for PCA are shown in the appendix. The weights for constructing the fiscal stress indices are shown in the following equations:

According to the PCA analysis results, the Short_term_fiscal_stress variable captures 44% of the information from the three original measurements, and the Long_term_fiscal_stress variable captures 45% of the information from the three original measurements.

Legislative characteristics

Prior studies of legislative influence on state policies measure legislative characteristics according to ideological positions, partisan composition, and staff resources (Marks et al., 1988; Schneider & Damanpour, 2002; Shor & McCarty, 2011, 2015; Thom, 2013, 2015). I borrow three variables from this literature to examine the influences of state legislatures: ideology of a state legislature, unified government, and legislative staff per legislator. The averaged upper and lower chamber ideology scores (Legislative_ideology) are used to measure the ideological position of state legislature (Shor & McCarty, 2011, 2015). 3 A dummy variable (Unified_government) is used to indicate whether a state’s legislative and executive branches are controlled by the same political party. Finally, the number of legislative staff per legislator (Legislative_staff) is used to measure the staff resources available to a legislature. In the model specifications, I also use legislative partisan composition (the proportion of Republicans in a legislature) and the full- or part-time status of state legislators to measure legislative characteristics.

Union strength

The coverage of employee unions (Union_coverage) is used to measure the strength of public employee unions.

Controls and Model Specifications

Plan size, measured as the logarithmic form of the asset value of the pension system (Asset_Size), is used to control for the possible scale effect. All independent variables are lagged by 1 year because decisions made in the current fiscal year will be reflected in the next fiscal year’s financial report. The models are estimated using both fixed effects and random effects. 4 The Hausman (1978) test is used to decide which estimation is most appropriate, and only the most appropriate estimation is presented and discussed in the “Findings” section. 5 For model specifications, I also estimate models under different benefit protections, contribution requirements, types of pension systems, legislator’s full- or part-time status, and under economic upturns and downturns. I also use the number of employees, instead of the asset value, to control for the size of pension system. The findings remain consistent when the number of employees is controlled. More discussion about model specifications is included in the “Model Specifications” section.

Data

Information on pension normal costs, employer and employee contributions, asset smoothing periods, pension assets, and pension liabilities was collected from the Public Plans Database (2014). I also compare the data with original financial reports from the pension systems to confirm the accuracy of the data. A total of 114 state pension systems are included in this data set from 2001 to 2013, representing more than 90% of all state pensions in terms of assets and members. Data for state finance, state legislature, and union variables were collected from various sources, including the Fiscal Survey of the States, the Book of the States, the U.S. Census Bureau, the National Conference of State Legislatures, the National Governor’s Association, and the Union Membership and Coverage Database. Definitions, data sources, and descriptive statistics for variables are shown in Table 3.

Findings

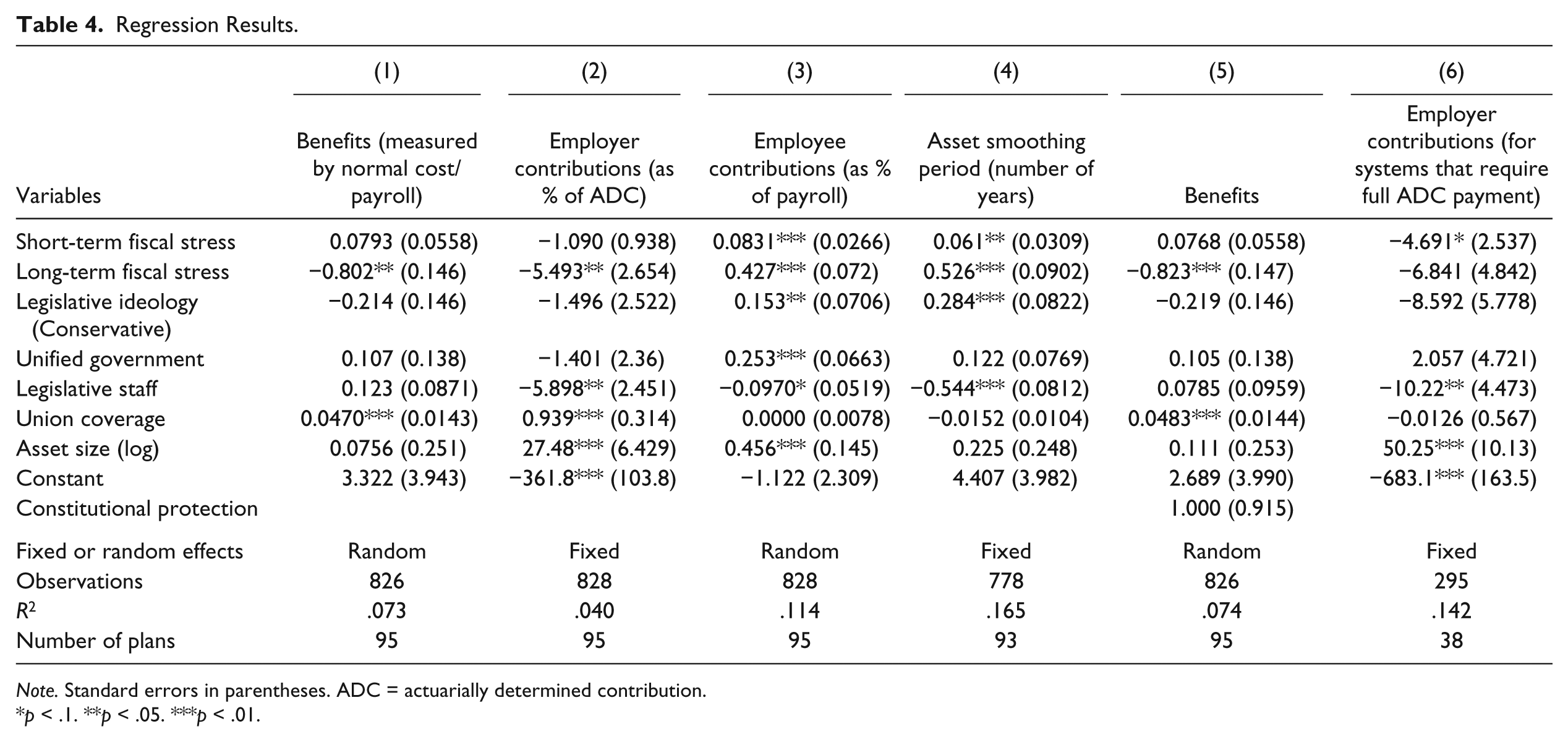

Columns (1) to (4) in Table 4 show the regression results for pension benefits, employer and employer contributions, and the asset smoothing period. Note that both the short-term and long-term fiscal stress variables are standardized. The results show that decisions in pension systems respond to different dimensions of fiscal stress, which supports Hypothesis 1. When state governments face long-term fiscal stress, all four pension decisions are influenced. For each one standard deviation increase in long-term fiscal stress, normal costs go down by 0.802% of payrolls, employer contributions decrease by 5.493% of ADCs, employees increase their contributions by 0.427% of payrolls, and asset smoothing periods increase by 0.526 years.

Regression Results.

Note. Standard errors in parentheses. ADC = actuarially determined contribution.

p < .1. **p < .05. ***p < .01.

When faced with short-term fiscal stress, state governments only increase employee contributions and modify the asset smoothing period but do not cut pension benefits or employer contributions. An increase of one standard deviation in short-term fiscal stress is associated with an increase in employee contributions of 0.0831% of payrolls and an extension of the asset smoothing period by 0.061 years. 6 The results confirm Levine et al.’s expectation that governments respond to different dimensions of fiscal stress with different strategies.

Findings also show some support for Hypothesis 2. First, a more conservative ideological position is associated with more employee contributions and a longer asset smoothing period. We know that increasing employee contributions and extending the asset smoothing period in a time of fiscal stress will reduce current pension costs for governments, which supports the assumption that conservative legislatures are more concerned with the financial burden of retirement systems. 7 Second, unified government is associated with a higher employee contribution rate, which also supports Hypothesis 2. Third, more staff support for state legislatures is associated with less employer and employee contributions, and a shorter asset smoothing period. The other results are not significant.

The strength of employee unions has a significant and positive influence on decisions regarding pension benefits and employer contributions. The results support Hypothesis 3 that stronger public employee unions are more likely to push for more pension benefits and request that state governments increase employer contributions to pension systems. Surprisingly, unions have no influence on employee contribution rates. This contradicts our knowledge of public pension management. If employees are paid the same level of benefits, increasing employee contributions is another way of cutting pension benefits, which is likely to face resistance from employee unions. Finally, there is no evidence to support the notion that unions have influence on setting the asset smoothing period. This can be generally explained by the fact that employees and unions are less involved in the actuarial process.

Model Specifications

I further include other specifications in the model to examine decisions in pension systems when different institutional arrangements are present.

First, when examining pension benefit decisions, I control for constitutional protections of pension benefits. Because a random-effect estimator is used in Column (1) of Table 4, a time-invariant variable can be included in the regression. The results are shown in Column (5) of Table 4. Data regarding legal protections of pension benefits were collected from Munnell and Quinby (2012). I assume that when pension benefits are constitutionally protected, pension benefits are less sensitive to external influences. However, as shown in Column (5), the dummy variable for constitutional protection is not significant, and the other results remain the same.

Second, I test whether the affecting factors on employer contributions vary when governments are constrained by legal requirements to fully pay their required contributions. Data regarding legal requirements were also obtained from Public Plans Database. Because the fixed-effect estimation is used in Column (2) of Table 4, the legal requirement, which is a time-invariant variable, cannot be included in the regression. To control for the effect of legal requirements, I separate out a subsample of 38 systems that have legal requirements and run regressions with this subsample. The results are shown in Column (6) of Table 4, and they suggest that legal requirements for employer contributions eliminate the influences of state governments and unions. Comparing Columns (2) and (6), the coefficients associated with fiscal stress and unions are no longer significant at p < .05 level when the systems are legally required to fully contribute to the ADC.

Third, I separate agent multiple-employer systems (16 systems) from other cost-sharing systems and perform regressions only for agent systems. Data for agent systems were also obtained from the Public Plans Database. In agent systems, I assume that state governments will have less influence on the costs, because participating employers have their own accounts. The results (not present here) indicate that for agent systems, state fiscal stress virtually has no influence on pension decisions, but state legislatures and unions still have influences.

Fourth, I perform regressions for 16 states with part-time legislatures to examine whether legislative influence changes because legislators spend less time involved with the policy-making process. Data were collected from the National Conference of State Legislatures. The results for the legislative variables are less significant with this subsample (results are not presented here). However, it is difficult to decide whether the lack of significant results is because there is no influence from part-time legislatures or because of the smaller sample size.

Finally, I perform separate regressions for economic recession years (years 2008 and 2009) and expansion years (the rest of the years). 8 I use National Bureau of Economic Research business cycle data to identify cutoff dates for recessions and expansions. The results for the expansion years are the same as those presented in Columns (1) to (4) of Table 4. The results for only the recession years show virtually no significant results. It is also difficult to determine whether the lack of significant results is due to no effect or because of the smaller sample size.

With the above model specifications, the testing results for Hypotheses 1 to 3 are consistent with regard to the sizes and the directions of influences from state finances, state legislative characteristics, and public employee unions. When institutional arrangements are included as dummy variables in the regressions, random-effect estimations show the same results. With fixed-effect estimations, institutional arrangements that are time invariant cannot be added as control variables. When systems with special institutional arrangements are separated into subsamples for estimation, the coefficients show less significant results, which is either due to a sample that is too small to show a consistent pattern or due to the lack of real effect in the subsample.

Conclusion

Levine, Rubin, and Wolohojian’s system framework is one of many cutback management theories that have been used to explain administrative responses to changes in financial conditions. In this study, the system framework enables us to systematically examine decisions in state pension systems. The findings generally support the system framework in two aspects: (a) there are multiple dimensions of a government’s financial condition, and each has different impacts on the decisions made in pension systems the government sponsors; (b) decisions in state pension systems are jointly influenced by the sponsoring government’s financial condition and by legislatures and unions.

In this study, a government’s financial condition is measured using six indicators that are divided into short-term and long-term dimensions. According to the findings, when state governments face short-term fiscal stress (i.e., less fiscal slack, more expenditure shock, and less revenue shock), they are likely to adopt strategies to expand revenues and to adjust accounting methods. They will not cut pension benefits or employer contributions until the fiscal stress turns into a long-term issue—that is, when a government faces high tax burden, high debt burden, and high unfunded pension liabilities.

In addition to fiscal stress, pension decisions are influenced by state legislatures and public employee unions. The research findings support the notion that state legislatures exhibiting a more conservative ideology are likely to increase employee contributions and adopt a longer asset smoothing period, while unified governments increase employee contributions to pension systems. In contrast, a strong employee union is likely to demand increased pension benefits and increased employer contributions. Unions, however, have no direct influence on setting asset smoothing periods. The results generally reflect the decision-making processes in public pension systems that are discussed in this study. Pension benefits and contribution policies (both employer and employee contributions) are debated and approved in state legislatures. Unions are more aware of the policy changes that directly affect the generosity of benefit provisions. The actuarial process is dominated by boards of trustees and professionals hired by the system, although governments and legislatures are potentially able to exert influence through the boards of trustees.

Despite the consistent findings, three limitations of the study should be noted when the results are used to inform policies. The first limitation is that I assume a linear influence from state’s financial condition on decisions in pension systems, but this influence could be nonlinear. For example, the findings suggest that states tend to cut contributions to pension systems when they have fewer resources. It is not clear, however, whether states would contribute higher than the required amount when they have more resources. In fact, prior studies found that states consistently underfund their pension systems (The Pew Center on the States, 2010, 2012). Similarly, when states have more financial resources than expected, they might be willing to increase pension benefits, but during declines, it might be difficult for states to cut pension benefits.

The second limitation is that I assume direct influences from state finances, legislatures, and unions, but these influences could interact with other variables. For example, it is possible that when strong fiscal stress interacts with a strong legislature or a weak union, decisions in pension systems are more sensitive to external influences. It is also possible that some omitted variables may interact with these influences. For example, political leaders, such as governors and majority leaders in legislatures, may play important roles in determining decisions related to state finances and pension systems. These individuals’ roles and the election cycle to select these individuals may interact with the influences examined in this study.

Finally, the analysis with a large sample of state pension systems may ignore the uniqueness and complexity of the decision-making process in each individual pension system. For example, I only use dummy variables to measure constitutional protections for pension benefits and legal requirements for employer contributions, but these variables do not fully capture the institutional constraints for pension systems. Some states may have implicit guarantees for its benefits or contributions. Informal institutions may be important but are overlooked in this research. These nonlinear and interactive influences, as well as the roles of informal institutions, could be examined in future studies.

Footnotes

Appendix

Principal Component Analysis (PCA) for Long-term Fiscal Stress Variables.

| Variables | Component 1 | Component 2 | Component 3 |

|---|---|---|---|

| Debt_burden | 0.691 | −0.009 | −0.723 |

| Tax_burden | 0.490 | 0.741 | 0.459 |

| Unfunded_liabilities | 0.531 | −0.672 | 0.516 |

| Variance Explained | 45% | 32% | 23% |

Acknowledgements

I thank Dr. Carol Ebdon and Dr. John Bartle of University of Nebraska at Omaha, and Dr. Kenneth Kriz of Wichita State University for their comments on earlier versions of this research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Faculty Research Awards Program at the University at Albany, SUNY.