Abstract

This study sheds light on the effects of policies that introduce competition into the marketplace of the provision of government services. The outcomes indicate that both nonprofit and government market share in a state are negatively affected by for-profit entry, a substitution relationship. The framing of the article in the New Public Management era and the Balanced Budget Act (BBA) of 1997 provides context in which to assess the policy consequences in hospice care. Given the budgetary challenges and growing cost of health care, this analysis begins a discussion of the effects of for-profit entry into the provision of government services, providing a glimpse into what the future holds for hospice care in the reforms of the Affordable Care Act (ACA) of 2010.

Introduction

This article’s objective is to explore the impact on nonprofit and government hospice care organizations resulting from for-profit hospice care organizations entering the market and providing hospice care services. The question driving this article is how does federal budgetary policy billed as a tool to control costs and increase competition impact the market share of hospice care organizations? Of particular interest is the Balanced Budget Act (BBA) of 1997, which was passed during the Clinton Administration. We contend that the BBA of 1997 was an example of the Clinton Administration’s policy prescription to the principles of New Public Management (NPM) under the auspices of “Reinventing Government” as offered in the 1992 work of Osborne and Gaebler. Framing the article in the NPM era and the BBA of 1997 provides context in which to assess the policy consequences of NPM in hospice care and offers a glimpse into what the future holds for hospice care post the reforms of the Affordable Care Act (ACA) of 2010.

The answers to these questions are important to policy makers, provider organizations, current and future Medicare beneficiaries, and more important for hospice patients and their families. The answers offer a look at the future implication of policy in the provision of health care services. This is particularly poignant at a time when the Medicare Hospice Program is to see a surge of beneficiaries as approximately 80 million baby boomers transition to retirement and subsequently to end-of-life care in the next 30 years. The empirical outcomes provide support for the idea that competition will change the market composition of service provision. What the results indicate is a substitution view: For-profits are substitutes for both nonprofit and government providers. Neither of the alternatives, supplementary or a complementary view, is indicated in the analysis. What this points toward for health care provision in the future could be construed as follows: When government policy enhances competition in the marketplace, the result is that for-profit firms will enter this marketplace as substitutes for other organizational types.

The article begins with a look at hospice care policy over time, linking NPM, the BBA of 1997, and Hospice Care. The article then assesses the changing market share of hospice provision in a regression analysis based on the for-profit–government–nonprofit provider relationship. The article continues with a discussion of the public policy implications, and ends with the conclusion. Immediately below, in the “Hospice Policy Background” section, evidence regarding the underlying mechanisms in Medicare legislation that has advanced hospice care policy is explored.

Hospice Policy Background

The reality of death and dying in the United States is a subject that has not yet gained prominence with policy researchers and society. This topic has traditionally been explored from the ideological perspective of the patient’s right to a good death (Byock, 1997; Field & Cassel, 1997), the failure of the medical establishment to play a key role in the dying experience (Singer, Martin, & Kelner, 1999), and the implications of “fairness” in the well-being of individuals at the end of life (Imhof & Kaskie, 2008). Hospice care was developed as an answer to the judgment of poor conditions for terminally ill patients who were suffering in hospitals. The slow onset of individual mortality (Halper, 1979) was placed in a setting characterized by “unawareness of prognosis,” “depersonalized care,” “isolation,” “neglect,” “pain and discomfort,” and “overzealous treatment by physicians” (Paradis & Cummings, 1986).

In 1974, the founding principles for hospice care emerged from a committee of the International Work Group on Death and Dying. U.S. organizers modeled their standards after the ones set forth by the international work group. In February 1977, the U.S. organizers and colleagues formed the National Hospice Organization (NHO), which later became the leader in promoting the causes of hospice care (Paradis & Cummings, 1986). According to Mor and Bimbaum (1983), it was the late 1970s pressure from the public, patients, and their families, as well as from hospice advocate organizations, that resulted in Congress mandating the National Hospice Study (NHS).

Government Responds

Beginning in 1981, Congress’s interest in extending Medicare benefits to hospice care recipients grew. In 1982, Congress introduced hospice into the Medicare program as a cost saving provision after a Congressional Budget Office (CBO) study asserted that hospice would result in sizable savings over conventional hospital care (Mor & Masterson-Allen, 1987). The idea that hospice could cut costs was not new, but it gained favor post-1977 (Siebold, 1992) as more hospice providers agreed that integrating with the current health care system would stimulate program growth.

The benefit of hospice in Medicare was created so quickly, representing a new area of health care, that Congress included two special provisions in the legislation. The first provision was a sunset clause that stipulated that without congressional intervention, the law would expire in November 1986. The second provision mandated an evaluation of the impact of the benefit. The hospice benefit was designed so that most services were provided in the patient’s home. To support this focus, the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) contained a provision that limited a provider’s total inpatient care days to 20% of all care delivered during any given year. The 20% provision did not apply to each individual hospice patient because some patients might need to stay far longer in an inpatient setting. Individual patient benefits were restricted to a benefit period structure. A hospice patient could elect hospice for a 90-day coverage period, followed (if necessary) by a second 90-day period and a subsequent 30-day period. Once this 210-day period was exhausted, Medicare’s coverage ceased. Both provisions were intended to control costs, prevent the program from becoming an exclusively inpatient model, and preserve hospice’s philosophy of care within the home environment.

In 1986, the Consolidated Omnibus Budget Reconciliation Act (COBRA) of 1985 was signed into law. COBRA repealed the sunset provision for Medicare’s hospice benefit, placing hospice-eligible beneficiaries into Medicare Part A. The COBRA legislation stated that terminally ill patients residing in nursing facilities could elect Medicare hospice care. Under COBRA, Medicare would reimburse hospice providers based on Medicare’s routine home care rate, a capitated per diem. Underpinning these changes within the COBRA legislation, COBRA provided the states with the option of adding a hospice benefit to state Medicaid programs.

The hospice amendment to Medicare was passed during the Reagan administration and was understood by Congress to be both a cost containment mechanism to limit the program’s high costs for beneficiaries in their last year of life, and a quality improvement tool to improve care for the dying. The hospice literature focuses on hospice as a gatekeeper to manage treatment of the terminal condition, where hospices specialize in pain and symptom management and provide greater levels of aide services than otherwise available under Medicare, including counseling and bereavement services for family members (Greer, Mor, & Kastenbaum, 1988; Greer, Mor, Sherwood, Morris, & Birnbaum, 1983; Mor & Masterson-Allen, 1987; Siebold, 1992). The authors and supporters of amending Medicare within Congress-enacted legislation based on patient stories communicated through anecdotes and vignettes. The estimates provided by the CBO were preliminary and based on isolated case studies of organizations that were neither homogeneous nor part of an established industry (Mor & Bimbaum, 1983).

Approximately one decade later, in 1997, the BBA established unlimited coverage for hospice beneficiaries by changing the hospice benefit periods to include two 90-day periods, followed by an unlimited number of 60-day period renewals. The benefit periods are not required to be consecutive on condition that the patient is certified as terminally ill at the beginning of each period, thereby allowing hospice election to be canceled at any time and reelected at any later date. The underlying change to perpetual hospice coverage was assumed to be in response to the difficulty of predicting death in the ever-changing medical environment, ensuring that access to hospice is available.

NPM, the BBA of 1997, and Hospice

The motivation for this article is to consider the changes in hospice policy and effects on changes in market share of this particular service within the context of the impact of NPM policies of the 1980s and 1990s and to connect to the present shifts in health sector reform. NPM as conceptualized by Hood (1991) removes several of the foundations that ensure neutrality and honesty in public service. Particularly of interest for this article is the blurring of the clear lines of division between the public and private sectors (Hood, 1991). In a more poignant criticism, Moe (1994) characterizes the NPM work associated with Osborne and Gaebler as

a heady brew-many of the ideas of free market economics, as refined in the voluminous privatization literature of the 1970s and 1980s, with the most popular of the current business motivational literature and dashed it with their own journalistic style. (p. 111)

Moe (1994) focuses on pointing out that the work of Osborne and Gaebler (1992) is designed to be appealing to liberals that support selective government interventions in the economy as it is in the case of the national healthcare program. In furthering our framing of this article, Moe’s review connects Osborne and Gaebler (1992) to then presidential candidate Bill Clinton. In retrospect, Moe’s (1994) prediction that

[t]he root cause of the problems afflicting the federal government today will not be solved by the “four bedrock principles” of entrepreneurial management or “cascading” behavioral modification sessions. Indeed, over the long term, they may be exacerbated as private parties and their values displace governmental institutions and their values [is an interesting insight]. (p. 118)

Similarly to Moe (1994), Weiss’s (1995) review of Osborne and Gaebler’s Reinventing Government highlights the business sectoral principles embedded and advocated in the 10 principles. In hospice as well as across the economy, the 10 principles limited government to “steer rather than row,” “inject competition,” and drive change through “the market.” Looking back into the market distribution of hospice organizations, we must consider the likely impact of a government led by market principles and behaviors. Unlike government and nonprofits (i.e., hospice care of the 1990s), “[b]usinesses may choose to focus and clarify their mission by divesting themselves of unprofitable or distracting lines of business” (Weiss, 1995, p. 232).

In lieu of cost controls, the BBA of 1997 was designed in line with the NPM of the times to restructure the Medicare Program including hospice care. Examples of this are the establishment of the Medicare + Choice program, reduction of the hospice payment annual update, and reporting of cost data (O’Sullivan et al., 1997). Specifically, the Medicare + Choice program expands private plan options to include preferred provider organizations, provider sponsored organizations, and private fee-for-service plans. Although the BBA of 1997 allows beneficiaries to keep curative Medicare services rather than having to elect hospice-only benefits, the BBA of 1997 “shows that substantial support exists for trying to restructure Medicare to make it work more like the large group private insurance market” (O’Sullivan et al., 1997, p. 6). The Medicare hospice cost containment measure in the BBA of 1997 “reduces the hospice payment update to market basket minus 1 percentage point for each of FY1998 through FY2002” (O’Sullivan et al., 1997, p. 19 ).

According to Moynihan (2003, 387), “[t]he Clinton administration provided a window of opportunity for National Performance Review (NPR) policy adoptions in three ways: executive mandates, the willingness of agencies and staff to voluntary adopt reinvention principles, and legislation” (p. 387). Under President Clinton, the NPR translated policy proposals via the use of executive orders. During the Clinton years (Moynihan, 2003), 55 executive orders implemented recommendations directly linked to the NPR. Prior to the BBA of 1997 (Gage et al., 2000), the Medicare hospice benefit covered 78% of hospice patients, up 22% from 1988, whereas

Medicare spending for hospice care increased dramatically. Spending reached about $13 billion in calendar year 2010, more than quadrupling since 2000. This spending increase was driven by greater numbers of beneficiaries electing hospice and by longer stays among hospice patients with the longest stays. (Medicare Payment Advisory Commission [MedPAC], 2012)

Kilgore et al. (2009) conclude that the

[i]ncreased use of hospice services observed in this study may be a result of direct hospice policy changes under the BBA of 1997, indirect effects from home health policy changes under the BBA of 1997 (which restricted eligibility for home health services). (p. 284)

At the same time of the BBA of 1997, NPM, and NPR, a national campaign to promote hospice was undertaken.

Organizational Tax Status and Hospice

When the use of Medicare and Medicaid as funding mechanisms for hospice care was realized, the institutional structure of hospice providers was dominated by nonprofits. Providers of the hospice services were focally grounded in nonprofit organizations, the initiators and supporters of the changing legislation in the 1970s. The first nonprofit hospice in the United States, the Connecticut Hospice, began providing services in spring of 1974. A decade later in 1984, after the implementation of the hospice Medicare legislation, 44 hospices were Medicare certified. 1 During the next 5 years, 789 organizations became Medicare certified, indicating an almost fivefold increase generally attributable to nonprofit hospice organization growth in absolute numbers. The Omnibus Budget Reconciliation Act of 1989 (OBRA) increased Medicare hospice reimbursement rates by 20%, possibly attributable to the hospice efforts during this almost fivefold growth period.

During the 1980s, nonprofit hospice was about 78% of all certified Medicare hospice providers, with for-profit making up about 14%, and the government at about 4%. The 1990s brought forward a remarkable shift in certified Medicare hospice providers. According to the General Accounting Office (GAO), the absolute number of for-profit Medicare-certified hospices increased about 300% after OBRA of 1989, whereas nonprofit Medicare-certified hospices numerical growth was around 43% for the period. The GAO (2000) report indicated a substitution effect in organizational tax status, moving hospice from a nonprofit provided health service to a for-profit provided health service.

For-Profit–Government–Nonprofit Market Size Frameworks

To describe the changing composition of hospice providers, we examine several explanations. We begin with the market entry conceptualization. For-profits enter marketplaces in which a return to the investor is identifiable, an outcome richly offered in the hospital sector literature. In this approach, for-profits are more careful financial and operational managers than their nonprofit or government competitors (Frank & Salkever, 1994; Silverman, Skinner, & Fisher, 1999). Given that for-profits have a focus on identifiable returns, provider goals and objectives differ (Duggan, 2000; Gaynor & Haas-Wilson, 1999; Sloan, 1998; G. J. Young, Desai, & Lucas, 1997).

Debate surrounding identification of the investor return (usually in the form of a cash dividend) has motivated this conceptualization not as an inefficiency in production issue, but as an attenuation of property rights surrounding the nonprofit or government provider in paying out the cash dividend in an inefficient way. Some identify the payout by nonprofits and governments as a dividend-in-kind 2 to employees, managers, and decision makers (Danzon, 1982; Pauly, 1987), a less efficient allocation than a cash dividend.

Under the market entry conceptualization, holding service provision and quality constant, substitutability of organizational type occurs, as Hansmann’s (1980) argue, when the consumer identifies the differences in incentives within each organizational type. The consumer’s identification of incentives leads the consumer to choose the organizational type that comes closest to the consumer’s most preferred option. This can be reinforced by public policy, as argued by Kilgore et al. (2009), where direct hospice policy changes under the BBA of 1997 are seen to influence consumer choice. As an example, the Medicare + Choice program expanded consumer choice under the BBA of 1997 by including preferred provider organization as a private plan option. This result is a substitution effect where the consumer has led to the growth of specific organizational types. This explanation leads to the following relationships:

In hospice care, an alternative to organizational substitution is the supplementary outcome. In the supplementary outcome, differing from the effect relating for-profits market share to both nonprofits and government, nonprofits fulfill a demand for public goods that is left unsatisfied by government provision (D. Young, 1999). The supplementary thesis follows the works of Weisbrod (1977) where nonprofit organizations provide goods on a voluntary basis in response to government failure. In hospice, there is some historical underpinning for the supplementary point of view. In the 1980s, as the hospice movement gained momentum, the call for government provision was present given the demand for hospice care. Whether this was a call due to under-provision of a good (the underutilization of hospice-type terminal care, as Hyman & Bulkin, 1990, noted) or an alternative to address underfunding is not explicitly clear. However, as seen in Figure 1, the growth of nonprofit hospice providers in the 1980s and 1990s was remarkable. Some of the early literature, including Rossman (1977) and Klagsbrun (1983), implied a cost saving potential for alternative funding through Medicare; however, this call for alternative funding was identified due to the under-supply of government-based hospice care. Whether the focal driver was funding or the lack of supply by the government, the supplementary explanation leads to the following hypothesis:

Number of Medicare-certified hospice providers by organizational tax structure 1983-2014.

In the complementary view, nonprofits are seen as partners of government, helping to deliver public goods largely financed by government (D. Young, 1999). As identified by MedPAC (2012), Medicare spending for hospice care reached about US$13 billion in calendar year 2010, a fourfold change over hospice spending in 2000, indicating governments’ desire to provide financial support for this service. The increase was partially driven by consumer choice, where greater numbers of beneficiaries opted into hospice (MedPAC, 2012).

Lester Salamon (1995) has forwarded the complementary view that nonprofits and government are engaged primarily in a partnership. Using the theory of public goods together with the theory of transaction costs suggests why government and nonprofits engage in a complementary relationship, in which government finances and nonprofits deliver services.

The complementary view can be observed in areas such as social services, given that free riding has a potentially significant effect, where direct public production of a good, such as hospice, is likely to require bureaucratic operations, whereas local preferences favor some differentiation of services to locales and consumers (D. Young, 1999). As Najam (2000) describe, the defining purpose for both nonprofits—in Najam (2000) nonprofits are non-governmental organizations (NGOs)—and government is not a simple resource allocation; the provision of services indicates the focus, which is on the ends or goals. To address the complementary view, the following hypothesis is forwarded:

Data and Measurement

To assess the implications of the relationships hypothesized for hospice providers, data from the Centers for Medicare and Medicaid Services (CMS) Healthcare Cost Report Information System (HCRIS) and Provider of Service (POS) files are used (CMS, 2016). Our sample requires all reporting freestanding hospice providers to accept Medicare reimbursement for services.

We chose freestanding hospice to differentiate from hospitals, skilled nursing facilities, and nursing facilities. Freestanding hospices are inpatient facilities who are primarily engaged in providing hospice care and services. These hospices are not precluded from providing services to terminally ill individuals who have not elected the hospice benefit or providing services to individuals who are not terminally ill. To be eligible for freestanding under CMS, a hospice is required to have as their primary activity the provision of hospice services to terminally ill individuals and to meet all requirements for participation in Medicare. We chose the HCRIS data because providers receiving Medicare reimbursement must provide adequate cost data based on financial and statistical records that can be verified by qualified auditors. The cost data are based on the accrual basis of accounting.

Data are for the time period 2002-2012. We chose 2002 as the beginning year of analysis because this is the first year that the prospective payment system (PPS) was fully in effect and end our analysis with the year 2012 because CMS reporting forms changed due to the ACA. The PPS is the method of Medicare reimbursement where payment is made based on a predetermined, fixed amount. The payment amount for a particular service is derived based on the classification system of that service, for example, diagnosis-related groups (DRGs) for inpatient services. CMS uses separate PPSs for reimbursement to acute inpatient hospitals, home health agencies, hospice, hospital outpatient, inpatient psychiatric facilities, inpatient rehabilitation facilities, long-term care hospitals, and skilled nursing facilities. Between the implementation of the BBA of 1997 and calendar year 2002, CMS allowed an interim payment system. In 2000, the transition from the interim payment system to the PPS began and was completed in 2002. Given that we are controlling for financial effects due to the BBA of 1997, we use data after the full implementation of the PPS.

The POS data are used because they contain data on characteristics of each type of health care facility, including the name and address of the facility and the type of Medicare services the facility provides. The POS data are collected through the CMS’s Regional Offices.

The final data file contains an individual record for each Medicare-approved provider. The data used in the analysis contain full information for 1,892 providers, which leads to 9,045 total observations over the time period.

Method

This study employs panel-based regression analysis because our interest is in the change in market share within each hospice provider due to the introduction of competition over time. In the analysis, the standard errors are clustered on the state in which the hospice is located. This is due to the fact that hospice providers cross county boundaries in some states, thereby providing services to multi-county areas and that state laws affect hospice care through Medicaid programs. The standard error clustering increases the absolute size of the standard error for each of the independent variables, thereby reducing spurious correlations.

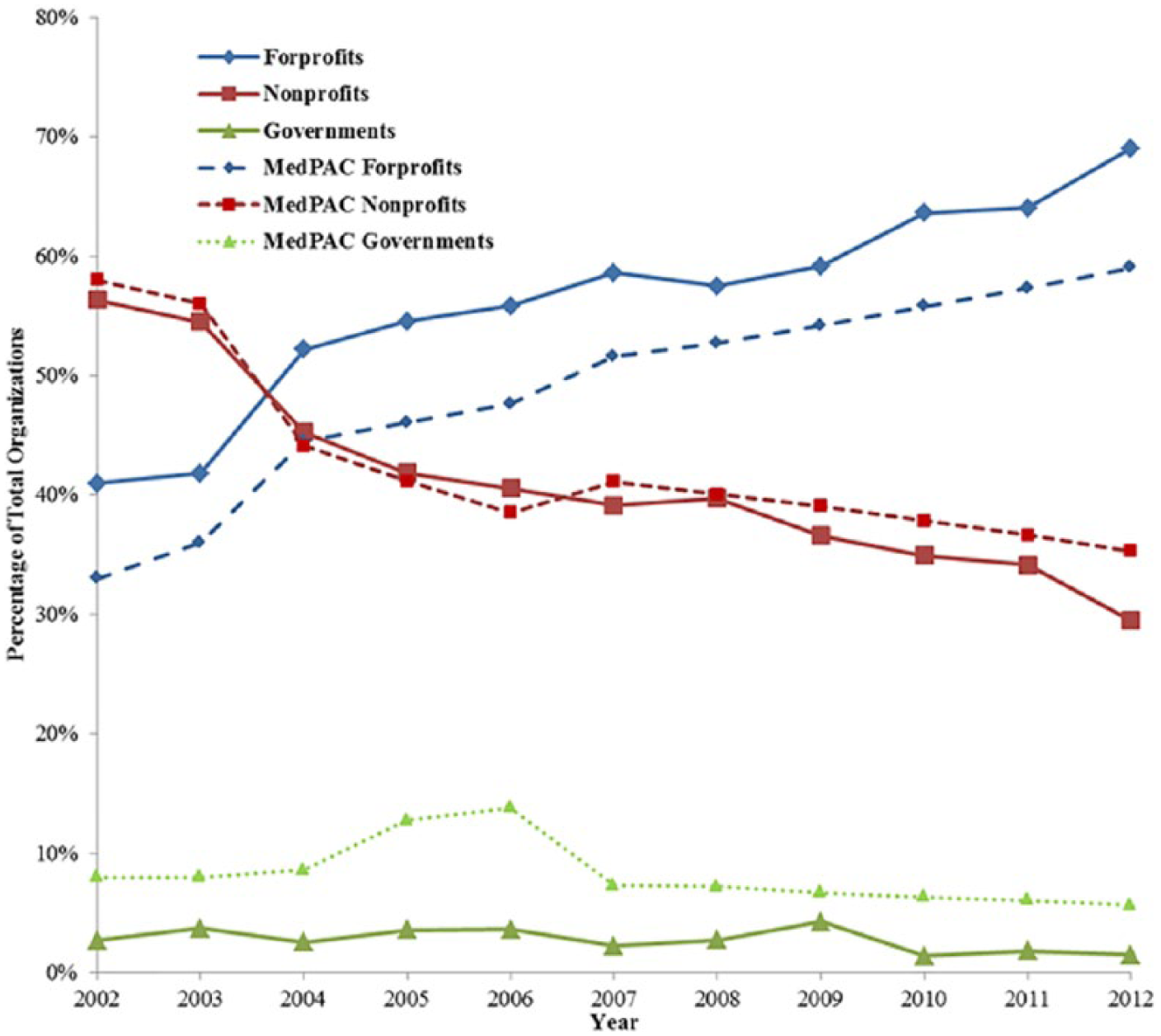

Generalizability

Data gathered from CMS for freestanding hospice providers include those that report partial information on our variables of concern, leading to a potential skew in observed behaviors. To address the generalizability of the 1,892 providers present within the data for our time period, we look at the composition of provider by ownership type. Figure 2 shows the percentage over the time period for all three ownership types. The figure indicates that all three ownership types are present in similar composition as the population of hospice providers identified in the MedPAC Report to Congress for each time period. MedPAC is an independent congressional agency established by the BBA of 1997 to advise the U.S. Congress on issues affecting the Medicare program. MedPAC is considered an authoritative source for Medicare hospice information. As identified in the figure, the composition of ownership indicates a reduction in the percentage of nonprofit hospice providers, a constant percentage of government hospice providers, and an increasing percentage of for-profit hospice providers.

Percentage of Medicare-certified hospice providers by organizational tax structure 2002-2012.

Variables

The dependent variable is constructed as the proportion of hospice patients in the sample controlled by an individual freestanding hospice provider. This allows an individual freestanding hospice provider to attract hospice patients from outside of any arbitrarily set political boundary, and allows hospice recipients to change providers as they deem appropriate. The independent variables of interest are market share variables based on provider type and reimbursements as identified in our hypotheses.

To reduce the potential for alternative explanations, this study uses several control variables that are focused on financial position, efficacy, quality, collection efficiency, patient mix, and a series of controls for organizational form.

Our first two control variables focus on the hospice provider’s financial position. Our first financial position control, total book assets, is seen in the literature as a proxy for the size of the organization in both the corporate literature (Altman, 1968; Leary & Roberts, 2014) and the nonprofit literature (Aggarwala, Evans, & Nanda, 2012; Gordon, Fischer, Greenlee, & Keating, 2013). Given that size of the organization may be linked with market share (D’Aveni & Ilinitch, 1992), total book assets should provide a macro control for the financial position of each freestanding hospice provider.

Our second financial position control is a micro control, net income. Net income is a key component of financial management in corporate firms and a critical measure of performance in both governments and nonprofits, where net income is usually described as unrestricted reserve funds or unrestricted fund balance, respectively. Hospice market share may be directly linked to the organizations’ ability to derive a net profit, because organizations cannot continue operations without net income or a subsidy (Silverman et al., 1999; Woolhandler & Himmelstein, 1997).

Next, we control for efficacy of the hospice organization through respite care. Respite care is considered an efficacy measure that can affect consumer choice. The offering of respite care to support caregivers of patients with advanced disease, such as found in hospice, may be critical in the patients’ decision to choose a specific type of hospice provider (Ingleton, Payne, Nolan, & Carey, 2003). To address the issue of quality variation, we control for length of service (LOS) as a proxy for the quality of care needed for the hospice patient, because LOS has been linked to quality (Noe & Smith, 2012). Quality of care can affect consumer choice, which will influence market share. The ability to collect for service costs will influence market share because collection of service revenues directly influences the cash position of any organization, which may affect timing of purchases linked to quality of care. We use reimbursement from Medicare interacted with organizational type to control for collection efficiency of each organization type (Danzon, 1982).

Following the work of Plante (2009), who examines whether for-profit hospitals may show a higher efficiency just due to their ability to admit healthier, younger, or more affluent patients, we control for patient mix, using both the percentage of Medicare and the percentage of Medicaid patients under care at the hospice organization. This allows us to follow Plante’s (2009) inference that patient mix can influence market perceptions of efficiency. Controlling for patient mix provides an opportunity to address market-based perception influence on market share for freestanding hospice providers.

Our final set of controls, dummy variables for organization type and facility form, allows us to address the issue of specialization in hospice. We note here that Noe and Smith (2012) identify differences between nonprofit and for-profit providers regarding quality of service. Little research has been done that addresses the specialization of the organization, although some literature (Grabowski & Town, 2011) has promoted the idea that there is a lack of competition in many nursing home markets, which will directly affect our market share measure.

Table 1 lists the name and description of each of the variables used in the analysis and its role in the regression analysis.

Variable Description.

Note. LOS = length of service.

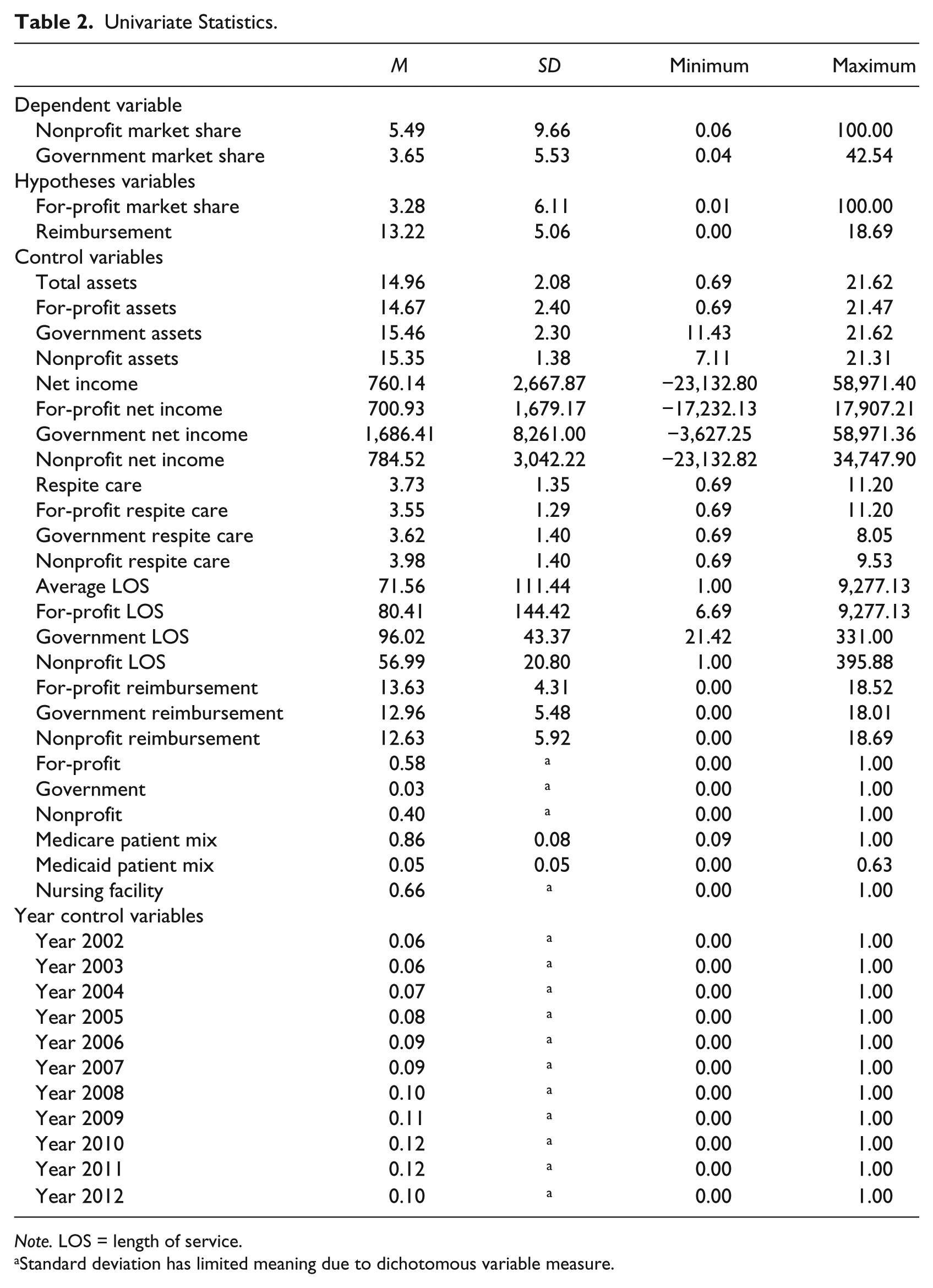

Univariate Statistics

The simple statistics are presented in Table 2. As observed in the table, the average nonprofit hospice agency has a market share of state hospice patients of about 5.5%, whereas the average for-profit has a hospice patient market share of about 3.3%, with the average government provider showing a market share of about 3.7%. Looking at the size of each ownership type, the average total book assets for all three groups is about US$69 million, with nonprofit providers having average total book assets of about US$15 million, whereas for-profit providers have average total book assets of about US$103 million over the time period. Average LOS for all providers is about 72 days, with nonprofit providers having the lowest average LOS of about 57 days and government providers have the largest average LOS of about 96 days. Average reimbursable services are about US$5.3 million annually for all providers, with government and nonprofit providers having an average of US$6.8 million in reimbursable costs, whereas for-profit providers have an average of US$4.1 million in reimbursable costs. Medicare patients compose about 86% of the hospice population within the states on average, whereas Medicaid hospice patients are about 5% of the hospice population in the states. Nursing home providers (also known as skilled nursing providers) constitute 66% of all providers in the data. Looking at our year variables, we see that freestanding hospice providers are, in general, increasing each year over the time period.

Univariate Statistics.

Note. LOS = length of service.

Standard deviation has limited meaning due to dichotomous variable measure.

Results

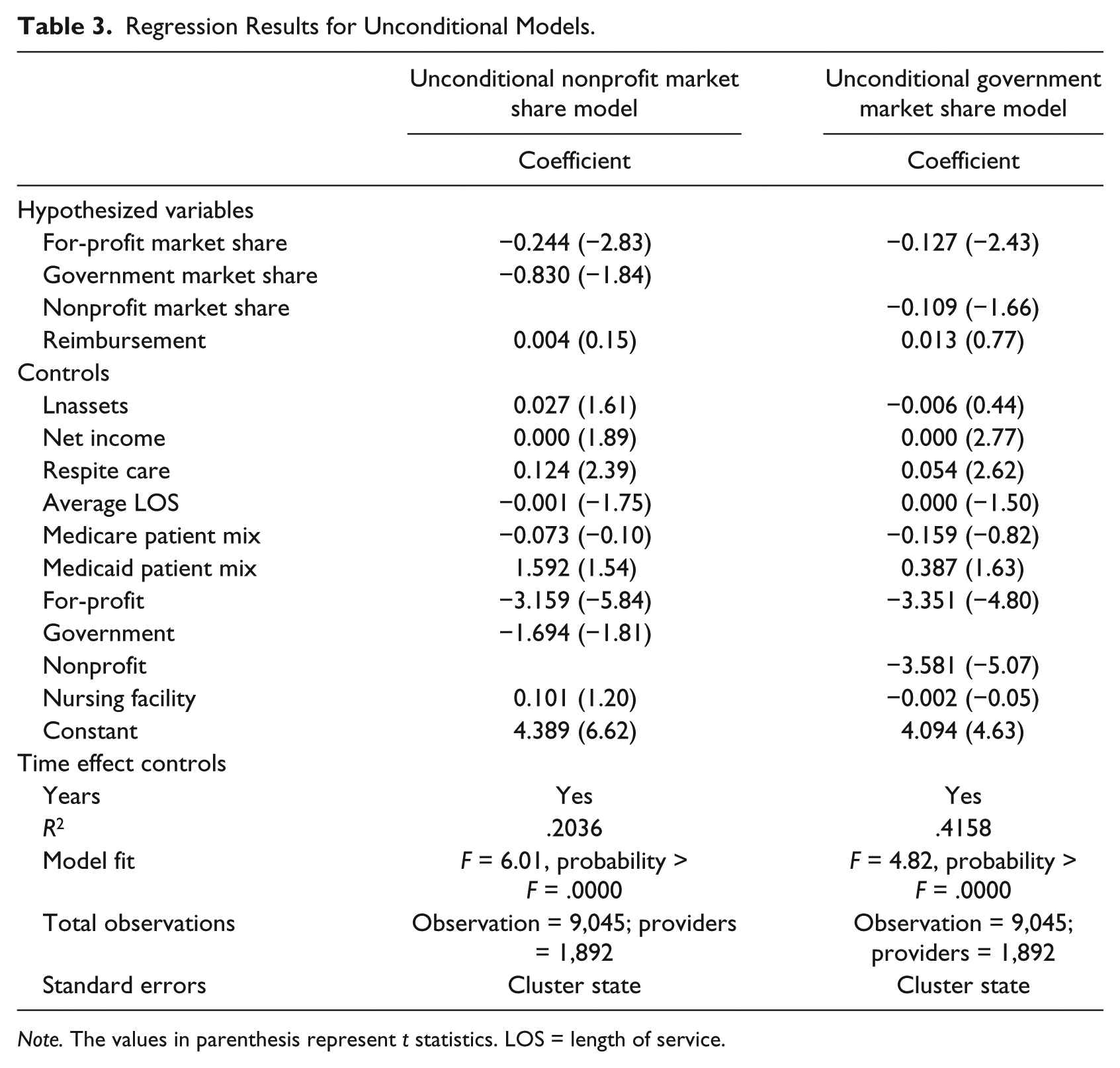

We begin our break down of the regression results by looking at each hypothesis under the unconditional (Table 3) and the conditional (Table 4) regression results. The results in both tables provide statistical impacts on average within each organization. Our results discussion is focused on the conventional statistical significance level of p < .05. Although the significance level is an arbitrary choice, we offer all the results and the t statistics in each of the tables. This statistical level coincides well with our large number of observations, in excess of 9,000.

Regression Results for Unconditional Models.

Note. The values in parenthesis represent t statistics. LOS = length of service.

Regression Results for Conditional Models.

Note. The values in parenthesis represent t statistics. LOS = length of service.

The first two hypotheses, H1a and H1b, focus on the premise that an increase in for-profit providers decreases both nonprofit and government market shares. Although hospice has been growing in the total number of providers, we are testing the substitution of both nonprofit and government providers by for-profit providers. Looking at the effect of for-profit providers on nonprofit provider market share, we see that a 1% increase in for-profit hospice market share reduces nonprofit provider market share by about 0.25% all else constant. This outcome is also present in the government market share model, where a 1% increase in for-profit market share reduces government provider market share by about 0.13%. Turning attention to the conditional results offered in Table 4, we see a similar outcome where increasing for-profit market share reduces both nonprofit and government provider market shares with a similar magnitude as found in the unconditional model. We observe that the average effect on nonprofits is larger than the effect on government providers in both the conditional and unconditional models.

Using the mean outcome for nonprofits, an increase in the average for-profit market share of 1% would reduce nonprofit market share from 5.49 to 5.24 on average. The economic effects of substitutability indicates that after the BBA and the PPS were firmly in place, for-profit entry into the hospice market provided an organizational substitute for nonprofit and government providers. This is a similar outcome as found in Hansmann (1987) and Gulley and Santerre (1993), where market share substitution by organizational type is observed and can be deduced as an important outcome of NPM reforms.

There are consequences to shifts in market share from nonprofits to for-profits. These shifts have been linked to changes in service provision. In the hospital literature, Horowitz and Nichols (2007) empirically show that nonprofit hospitals located in markets with high for-profit market share are more likely to offer only relatively profitable services when compared with markets with low for-profit penetration. This results in nonprofits being less likely to offer unprofitable services when the market share for nonprofits falls. Plante (2009) identifies differences between both for-profit and nonprofit hospital providers, where organizational type changes both the service offerings and the financial ability to sustain operations as measured by cash flow.

Similar to Plante (2009), who found no difference in efficiency between for-profit and nonprofit hospitals, we test the additive effect of for-profit market share and for-profit net income, where net income is a proxy efficiency measure for more careful management and operations. We find no statistically significant additive effect 3 indicating that the efficiency of for-profit providers is similar to nonprofits and governments.

The second hypothesis is focused on the impact of government market share upon nonprofit market share, where government is a supplement for nonprofit hospice providers. Both Tables 3 and 4 indicate no statistical support for the supplementary hypothesis that an increase in government market share reduces nonprofit market share, an outcome that is counter to that of Hansmann (1987). Although we find a lack of a statistically significant outcome for government substituting for nonprofit provision, supporting evidence based on our Figures 1 and 2 shows that government hospice providers are stable in count and market share over the time period. This provides evidence that the idea of increasing competition through policies such as the BBA and NPR had little effect on governments, whereas the effect of competition changed the market share of nonprofit providers, further supporting the substitutability of for-profits for nonprofits.

The third hypothesis tests whether or not reimbursements from government increase nonprofit hospice provision, a proxy for a complementary relationship, where government provides funding and nonprofits provide services. In Tables 3 and 4, government reimbursement for hospice services on average have no statistical effect on nonprofit market share. The results do not support Hypothesis 3 or the complementary view as proposed by D. Young (1999), where government is the financial supporter and nonprofits provide services. In addition, government reimbursement is not statistically significant for either for-profit or government providers.

The market share controls are important in our model because they provide a mechanism to correct for alternative explanations. Our first control is total book assets. The results are unsurprising in that as assets increase nonprofit market share increases as observed in the conditional nonprofit market share model. The statistically positive relationship between market share and asset size follows the literature in both the nonprofit and for-profit literatures. In Table 3, we note that changes in net income have no economic effect on market share. The lack of an effect for net income could be attributed to hospice care itself, because hospice care is provided in a PPS environment of fixed reimbursement, which can control profit margins. Alternatively, book assets may provide sustaining power, as opposed to net income, to the hospice provider in this relatively young market where growth, thus market competition, began in the 1990s.

Giving consideration to our result for caregiver support, as measured through respite care days, our results in Tables 3 and 4 point out that caregiver support has a positive effect on market share. This result provides support for Ingleton et al. (2003) where patient provider choice may be affected by organizational support for their caregiver’s well-being. In the LOS controls, the results indicate that average LOS has no statistical effect on nonprofit market share in Table 3; however, when conditioned on the interactions, we see that as average LOS increases for nonprofit providers, market share declines, although the economic effect is quite small. The controls for patient mix, the percentage of Medicare and Medicaid patients under care, have no statistical effect in any of our regressions. This may be due to the nature of the service where patient mix has little effect, because the majority of reimbursement is Medicare funded. In our final set of controls, the indicator variable for organizational type has an effect in the unconditional models; however, the statistical effect is reduced to zero in the conditional models. Our indicator for facility form shows no statistical effect on market share, indicating that nursing facilities do not impact market share in the hospice market. This can be interpreted as competition for market share in the hospice market does not differentiate the form of hospice provider between nursing facility providers and other types of providers.

Discussion

This article has focused on exploring a substantive evaluation of the implications of competition through policy prescription on freestanding hospice care providers. Using the relational role of for-profits, nonprofits, and government, the effects of these relationships in hospice service provision supports the substitution view. The findings detect a substitution of for-profits for both nonprofits and government providers based on hospice market share. Our outcomes provide no statistical support for a substitution effect between nonprofit and government providers. The resulting outcome of the analysis has introduced a set of potential effects that may provide insight into the changing health care policies in the United States. Although the foundation and provision of hospice care was originally focused on the nonprofit ideological orientation of providing finite life patients with a potential for a “good death,” the changing focus in the BBA of 1997 in conjunction with the NPM mantra introduced the potential adverse effect of moving the number of nonprofits out of the marketplace and substituting for-profit providers. If, as observed in this study, for-profit is a substitute for nonprofits and government providers, assessment of the specification and quality of service is needed to assess the potential impact on hospice services. The hospital literature in effect warns of a potential where for-profit providers induce nonprofit providers to only offer “profitable” services. If nonprofit providers offer only profitable services, this raises a larger question regarding the tax advantages of nonprofit firms vis-à-vis for-profit firms.

Conclusion

As in general health care services, little is known about the potential relationship between supply and demand for hospice services. In 1982, there were 25,000 hospice patients, or about five individuals considered terminally ill, as defined in hospice care, for every 1,000,000 in the population. In the most recent figures, provided by the National Hospice and Palliative Care Organization (NHPCO) report in 2014, there were about 1.54 million hospice patients in 2013, or about five individuals considered terminally ill for every 1,000 in the population (NHPCO, 2014). The number of hospice providers also grew from 44 providers in 1984 (NHPCO, 2010) to more than 5,800 providers in 2013 (NHPCO, 2014). This hospice growth is from a “grass roots movement” to a projected US$18.2 billion federal program in fiscal year 2014. NHPCO (2014) statistics show the use of hospice care for the dying is increasing in the United States, but the increase does not appear to be reducing the cost of treatment in the final months of life, an outcome that was promoted as the focal support for hospice care in Medicare at the inception of the program. With costs rising, the diagnosis of the terminally ill increasing, and changes occurring in market share, what are the implications to both provision and quality?

We posit that the ACA is a continuation of the principles discussed in the context of hospice care. When considering the context of NPM, BBA of 1997, and NPR, the ACA policy is conceptually similar to hospice care. For example, the ACA guarantees private insurers a market for health insurance while promoting competition, an unwritten aspect that was identified in hospice care in its developing years. With ACA, competition is expected to set the price of health insurance products as well as to drive product innovation. In a way, ACA is the deregulation of publicly funded health insurance, transferring the government monopoly to the private sector.

The role of states in creating health insurance exchanges is parallel to the principles of devolution and decentralizations found in NPM. For example, the ACA transforms Medicaid from an underserved and undesirable insurance product to an example of what is likely to become the norm for the industry similar and parallel to Medicare provision in hospice. This also applies to the policy innovation option as states such as Michigan expanded Medicaid in a liberal manner while anchoring their expansion option to fiscally conservative mechanisms. Previously uninsured beneficiaries are seen as customers rather than recipients who can search for health care coverage products from competing private insurers giving citizens freedom and choice. Similarly, uninsured customers can exercise the option to search and purchase coverage regardless whether employed at the local, regional, state, or national government level.

Insurers and health care providers alike agreed to move away from fee-for-service into a payment system driven by quality, cost controls, and value while accepting the risk of penalties and payment reductions for failing to meet new standards of care. This not only echoes the performance and pay-for-performance standards prescribed by NPM but also appears similar to the PPS of Medicare as applied in hospice care. Finally, the creation of the Patient-Centered Outcomes Research Institute as mandated by the ACA parallels the need to assess costs and benefits found in NPM core principles.

Our previously stated concern allows us to draw lessons from the hospice care policy realm and relate them to what may await the rest of the health care industry in the post reform years of the ACA. Are for-profit firms going to replace all other organizational types in the health care industry? Will nonprofit health care providers offer only “profitable” services? Is this the policy prescription that benefits users and providers? These concerns can inform policy makers, insurers, and beneficiaries alike, potentially raising the issues of health care providers to a nationwide discussion.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.