Abstract

To better evaluate the effectiveness of overhead-free donations on giving behavior, we seek to further investigate the robustness of the findings from Gneezy et al. using a nonstudent population. In an online experiment, we test whether (a) the level of overhead costs affects giving decisions and whether (b) overhead aversion disappears once donors are informed that an anonymous donor has already covered all overhead costs. Results show that donations decrease as overhead spending increases when donors have to pay for overhead. However, unlike the original article, we find mixed results when someone else covered overhead costs. Participants exposed to a nonprofit with a 33% overhead ratio where overhead was already covered still displayed overhead aversion. However, this aversion disappeared at a high overhead ratio of 67%. The overall results remain unchanged after controlling for demographics. Our results hold important implications for nonprofit organizations who must find a careful balance between appealing to donors for short-term financial gain and addressing the need to alter skewed donor expectations toward financial efficiency in the long run.

Introduction

The overhead ratio, measured by the proportion of a nonprofit organization’s expenses devoted to administration and fundraising, that is, resources not being spent to direct mission-related work, has emerged over the years as an important efficiency indicator for nonprofit organizations. Although the overhead ratio provides a concise snapshot of an organization’s short-term financial position, the indicator is regularly criticized on various grounds, such as its inability to comprehensively capture financial health (Knowlton, 2016), efficiency (Coupet & Berrett, 2019), effectiveness (Gregory & Howard, 2009), or its inaccuracy due to deliberate manipulation (Krishnan et al., 2006). Despite such criticism, some nonprofit stakeholders continue to strongly focus on overhead ratios. For instance, charity watchdog agencies, such as Charity Navigator and CharityWatch, assign ratings to charities based largely on their relative spending on overhead. Some federated giving campaigns even provide lists of donor information including solely the names of the organization along with its overhead ratio, making claims like, “every dollar you donate goes directly to ____________ (fill in the blank with whatever program they offer).” A recent study also finds that many governmental agencies continue to use flat-rate indirect cost policies, whereby project grants only allow for reimbursement of administrative costs between 0% and 10% of the entire grant (Eckhart-Queenan et al., 2019). Similarly, nonprofit organizations themselves promote their fiscal soundness in donor communication by touting low overhead ratios.

First and foremost, however, nonprofit scholars have long explored the relationship between overhead ratios and giving decisions among private donors. Although a comprehensive stream in the literature provides evidence of a negative relationship between overhead and donation revenue based on archival financial data (Greenlee & Brown, 1999; Tinkelman, 1999; Weisbrod & Dominguez, 1986), scholars have in recent years turned to experimental research methods to clearly isolate a causal effect between cost reporting and giving behavior (Gneezy et al., 2014; Newman et al., 2019; Portillo & Stinn, 2018; Ryazanov & Christenfeld, 2018).

In a seminal contribution to this literature, Gneezy et al. (2014) found in a laboratory experiment that participating students gave significantly less frequently to organizations with a high overhead ratio, but that this effect disappeared once participants were informed that overhead would be covered by an anonymous donor. Based on their findings, the authors derive as a practical implication that fundraising practitioners should adopt a dual strategy by soliciting overhead-free donations from the general public as well as overhead-only donations from a few key major donors.

To better evaluate the effectiveness of overhead-free donations, we seek to further investigate the robustness of the findings from Gneezy et al. (2014). We argue that intensifying the solicitation of overhead-free donations needs to be reflected upon carefully, because it could also be harmful for the nonprofit sector in the long run by tightening donors’ expectations toward legitimate overhead spending (Gregory & Howard, 2009; Lecy & Searing, 2015). In this study, we revisit the laboratory student experiment by Gneezy et al. (2014) with a nonstudent population, and deviate from Gneezy et al. (2014) who chose 5% and 50% in their overhead ratio manipulation. We argue that assessing effects of giving at a 33% overhead ratio is more relevant from a practical perspective. It is closer to the real overhead ratio of many charities, and it is just below the accepted limit by established charity watchdogs, such as the Better Business Bureau. We further chose 67% overhead to assess the effects of a value that exceeded accepted benchmarks in the sector.

Not only the study by Gneezy et al. (2014) but also a number of other experimental studies on the topic rely on student samples (McDowell et al., 2013; Portillo & Stinn, 2018). We conduct an online survey-based experiment with Amazon Mechanical Turk participants (n = 660), and test if (a) the amount of overhead expenses impacts individuals’ giving likelihood and giving amount and (b) how information about an anonymous donor covering overhead influences giving decisions. Our findings generally support the previously noted overhead aversion of donors, however they provide mixed evidence regarding the impact of anonymous donor information on giving decisions.

Our study contributes to nonprofit literature in two regards. First, we answer to calls for more studies in nonprofit research to assess the generalizability of key findings (Calabrese & Gupta, 2019; Helmig et al., 2012). This is not only valuable to assess the validity of previous findings but it also allows nonprofit scholars to more confidently inform practitioners about research implications. Second, we contribute to the growing number of experimental studies investigating the relationship between financial efficiency ratios and giving (Gneezy et al., 2014; Newman et al., 2019; Portillo & Stinn, 2018; Ryazanov & Christenfeld, 2018).

In the following pages, we discuss the background for the study and prior relevant literature. We also address the technical aspects of creating the survey, presentation of sample descriptive statistics, and the interpretation of the study results.

Background and Prior Literature

Background on Financial Efficiency Ratios

Charities are required to classify their spending into three primary categories: fundraising, administrative, and program activities (Financial Accounting Standards Board [FASB], 1993). Program expenses are the expenses incurred in directly furthering a nonprofit’s mission while administrative and fundraising are collectively referred to as “overhead” expenses or operating expenses and include expenses for the organization’s overall operations and management.

Although oversight organizations draw on overhead and other financial ratios to assess nonprofit accountability, the suitability of these measures to capture financial health (Denison & Beard, 2003; Greenlee & Bukovinsky, 1998; Greenlee & Tuckman, 2007; Tuckman & Chang, 1991) or organizational performance (Hager & Flack, 2004) is debated in the academic literature.

Brief No. 5 of the Nonprofit Overhead Cost Project (Hager & Flack, 2004) discussed the growing use of financial ratios as an assessment tool for nonprofits by outside funders, watchdog groups, and the media. Particularly focusing on the program spending ratio and fundraising efficiency ratio, the report encouraged caution when interpreting these numbers due to what it terms “technical flaws” and “unintended consequences”; however, the report also admitted that such ratios, when assessed critically, offer a “useful piece of information” for donors and outside agencies. Other scholars in the early 2000s discussed both the positive and negative roles of the overhead ratio in organizational assessment (Pollak & Rooney, 2003) along with caution regarding other financial measures, which emphasize efficiency over effectiveness (Hager & Greenlee, 2004; Lammers, 2003).

More recent work on overhead expenses considers its value to the overall accomplishment of nonprofit mission in terms of organizational capacity, emphasizing that organizations consistently cutting overhead expenses can enter a dangerous “starvation cycle” leading to financial stress and impaired organizational effectiveness (Chikoto & Neely, 2014; Gregory & Howard, 2009; Lecy & Searing, 2015; Mitchell, 2017; Schubert & Boenigk, 2019). Scholars refer to the belief that less overhead is somehow better for mission accomplishment as the “overhead myth” (GuideStar, 2013). Some overhead spending is necessary for organizations to survive and thrive relative to accomplishing their missions, and increasing overhead spending can foster organizational growth and better position organizations to achieve success relative to their missions. For example, if an organization needs to hire additional staff to manage grant activities, the administrative overhead could increase as a result. In addition, higher compensation for an organization’s leadership in a competitive marketplace could translate into better management, in which case such compensation, if appropriate for the organization’s overall financial picture, may be a worthy trade-off for the organization and may enable the organization to better absorb the overhead expenses associated with other operational and program expenses.

At this point, there is consensus within the academic community that overhead ratio should not be the sole measure of an organization’s financial fitness, but should rather be considered within the context of a bundle of financial measures and should vary according to nonprofit subsector and the type of work being accomplished by an organization. However, within practice there is some persistence to the usage of the overhead ratio, sometimes in isolation, as a measure of fiscal strength and programmatic accountability shared with potential donors. Although some popular figures, such as Dan Pallotta, present justification for organizations to spend more, not less, on administrative expenses, the rallying cry still falls on some deaf ears and closed pocketbooks (Pallotta, 2008).

The Effect of Financial Ratios on Charitable Contributions

Due to the lively debate around financial efficiency ratios, nonprofit scholars have long been concerned with the relationship between financial ratios and private giving. Scholars have taken three different approaches to investigate this relationship. A first stream adopts an organizational-level perspective and draws on archival financial data to assess the link between reported financial efficiency ratios and giving through econometric modeling (Charles, 2018; Greenlee & Brown, 1999; Tinkelman, 1999; Weisbrod & Dominguez, 1986; Yan & Sloan, 2016). As highlighted in recent reviews of this literature (Garven et al., 2016; Wong & Ortmann, 2016), most studies find overhead ratios and giving to be negatively correlated suggesting that donors are indeed to some degree sensitive to financial ratios. However, effect sizes and overall explanatory power of the regression models in these studies vary widely, making it difficult to prove clear causation between financial ratios and giving. Most importantly, analyses of archival data are limited in their ability to capture donor motives and hence do not provide sufficient evidence that donors truly look up financial information before making giving decisions (Garven et al., 2016).

In response to the shortcomings of organizational-level studies, scholars have increasingly focused on the impact of financial ratios on giving from an individual-level perspective, and done so through either survey or experimental methods. The second relevant stream therefore constitutes a more practitioner-oriented set of survey studies conducted to capture donor expectations toward financial ratios and their relevance for giving decisions (for a recent review,see Wong & Ortmann, 2016). Overall, surveys have delivered mixed results (Bagwell et al., 2013; Barclays Wealth, 2010; Grey Matter Research, 2018). While in a survey by Barclays Wealth (2010) donors identify spending on overhead as one of the most important giving criteria, Grey Matter Research (2018) finds that few donors consider efficiency criteria and that they rarely know the overhead ratio of their favorite charity. Although surveys help with assessing general donor expectations and preferences, it remains unclear to what extent self-reported preferences translate into actual giving behavior and whether donors are really sensitive to different levels of financial ratios.

The third stream of research addresses the methodological challenges of the other two streams by drawing on experimental research methods. Experiments promise to better isolate a causal relationship between financial ratios and giving behavior than analyses based on survey or archival data. That said, laboratory and online experiments are regularly criticized for suffering from low external validity because they oftentimes create artificial settings that reduce complexity of real-life decision-making. Despite somewhat neglecting the context in which real-life giving occurs, scholars have nevertheless in recent years embraced experimental method in research on giving determinants (Adena & Huck, 2019; Karlan & Wood, 2017; Metzger & Günther, 2019; Newman et al., 2019). As noted by Kim and Van Ryzin (2014), one advantage of using experimental research designs is that the careful manipulation of an independent variable in a controlled environment increases the internal validity of the study by being “especially strong studies for demonstrating causal relationships” (p. 913). Hence, although experiments only test effects in very specific contexts, these studies can collectively provide a better understanding of the underlying mechanisms of giving and inform organizations about adequate fundraising and accountability communication strategies.

This stream of experimental studies has grown significantly over the past years and has delivered three key insights. First, experimental studies provide compelling evidence that donors base their giving decisions on overhead ratios once confronted with financial data from more than one organization (Buchheit & Parsons, 2006; Gneezy et al., 2014; Metzger & Günther, 2019; Portillo & Stinn, 2018; Stout, 2001). Within this strand of the literature only McDowell et al. (2013) find no statistical evidence that participants integrate financial information into their giving decisions.

Second, more recent experimental studies show that the effect of overhead ratios on giving behavior differs depending on various factors, such as comparison scenarios (Van der Heijden, 2013), giving variables (Ryazanov & Christenfeld, 2018), donor characteristics (Newman et al., 2019) or types of overhead (Portillo & Stinn, 2018), and information about other donors (Gneezy et al., 2014). Van der Heijden (2013) finds a “flight to extremes” where only the organizations with the highest and lowest overhead ratio were affected by giving decisions once participants were provided with three organizations to compare. Ryazanov and Christenfeld (2018) highlight differences in giving variables and find that overhead ratios affect donors’ charity choice but not absolute giving amounts. Newman et al. (2019) show that donors’ cause commitment is an important moderating variable as study participants with a high cause commitment were more accepting of higher overhead ratios than participants with a lower cause commitment. Portillo and Stinn (2018) provide first evidence that donors’ overhead aversion might be associated with specific types of overhead. Specifically, study participants showed a preference for supporting fundraising expenses, as opposed to salaries. Last, Gneezy et al. (2014) find that aversion toward high overhead ratios disappears once participants are informed that another, anonymous donor would cover all overhead-associated costs.

The third insight from the stream of experimental studies is that only a fraction of donors considers financial information before donating. While Bowman (2006) draws this conclusion from the low explanatory power of his regression models, Buchheit and Parsons (2006) incorporated a choice for participants to compare organizations based on financial information into their experimental design (and only 39% of the study participants chose to do so). More recent studies corroborate that many donors show a preference to compare organizations based on nonfinancial data, such as an organization’s mission and programs (McDowell et al., 2013) or its cost-effectiveness (Caviola et al., 2014). Table 1 provides an overview of experimental studies investigating the effect of financial ratios on giving behavior.

Overhead of Experimental Studies on the Effect of Overhead on Giving.

Note. The studies used varying DVs to assess giving behavior. Giving choice here refers to scenarios when study participants had to donate all funds to one among several organizations. When instead investigating gift amounts, participants had to allocate specific amounts of a fixed sum between several organizations. Last, giving intention refers to situations where participants did not make allocation decisions directly, but instead were asked whether they intend to give in the future. IV = independent variable; DV = dependent variable.

Hypothesis Development

Previous literature has discussed several theoretical arguments why donors might prefer organizations with lower overhead ratios. The most widespread argument is that overhead increases the price of giving by reducing the portion of the marginal dollar that is passed on as final output (Bowman, 2006; Weisbrod & Dominguez, 1986). Similarly, once solicited, how much donors give will depend on how close the charity is to their ideal price (Andreoni & Payne, 2003). Therefore, if the logics of rational consumption apply to the charitable context, donors should prefer giving to the organization with the lower price.

Certainly, overhead ratios have been used frequently as a substitute for true measures of output and efficiency by nonprofit watchdog agencies and are readily available to donors looking to identify their ideal and most efficient organization (Lecy & Searing, 2015). This ties in with the alternative argument presented by Caviola et al. (2014) who contend that donors are subject to an evaluability bias. According to this cognitive bias, donors’ giving decisions are sensitive to overhead ratios (and not to more sophisticated performance measures) because such ratios are easy to evaluate. Both of these arguments suggest the following hypothesis:

However, Gneezy et al. (2014) find giving decisions are no longer affected by different levels of overhead spending when overhead spending is covered by an anonymous donor although under both scenarios (with and without an anonymous donor) the overhead information signal is the same. They hence provide an alternative explanation, referring to impact philanthropy theory (Duncan, 2004). This theory posits that giving is driven by a desire to personally make a difference and can explain why donors would view overhead costs as a misappropriation (Duncan, 2004). When donations go entirely toward program spending, donors might hence have a higher perceived personal impact. From a rational accounting perspective, this distinction should be irrelevant, but by framing the connection between the donor’s gift and the resulting benefit differently, although the objective benefit remains the same, the tangibility of the benefit is viewed differently (James, 2017). If this theoretical argument holds, we should corroborate the finding from Gneezy et al. (2014) and therefore hypothesize:

Based on the prior literature and theory as presented, we hypothesize that donors will be more likely to give to our Brighthouse Society scenario because it has no overhead expenses as compared with The Justice Project which has varying levels of overhead. In addition, we are testing whether the mean donation without overhead will be greater than the mean donation with overhead. We anticipated this mean donation would have an inverse relationship with overhead and that this tendency would persist even in light of the overhead not applying to an individual donor’s gift. Therefore, we anticipate that donors will favor organizations that have lower overhead expenses relative to organizations that demonstrate some overhead even when that overhead is covered by a donor or seed funding.

Method

Description of the Study

Participants in the study (n = 662) were recruited, consented, tested, and compensated using the Amazon Mechanical Turk (MTurk) service. Amazon MTurk is an online web-based platform for recruiting and paying subjects to perform tasks (Berinsky et al., 2012). Vanhove et al. (2018) conclude that MTurk participants are an appropriate population for studies that are not dependent on strict group criteria. This population has been utilized in published studies across the last decade and findings indicate that MTurk participants are slightly more demographically diverse than are standard internet samples and are significantly more diverse than typical American college samples (Buhrmester et al., 2011). Registered users of Amazon MTurk browse a list of available tasks and view a description of the work and compensation before selecting a particular task to complete. All participants in our study received US$1.00 upon completion of the survey; median time of completion was 9 min. Data were collected from April 16 to June 26, 2018.

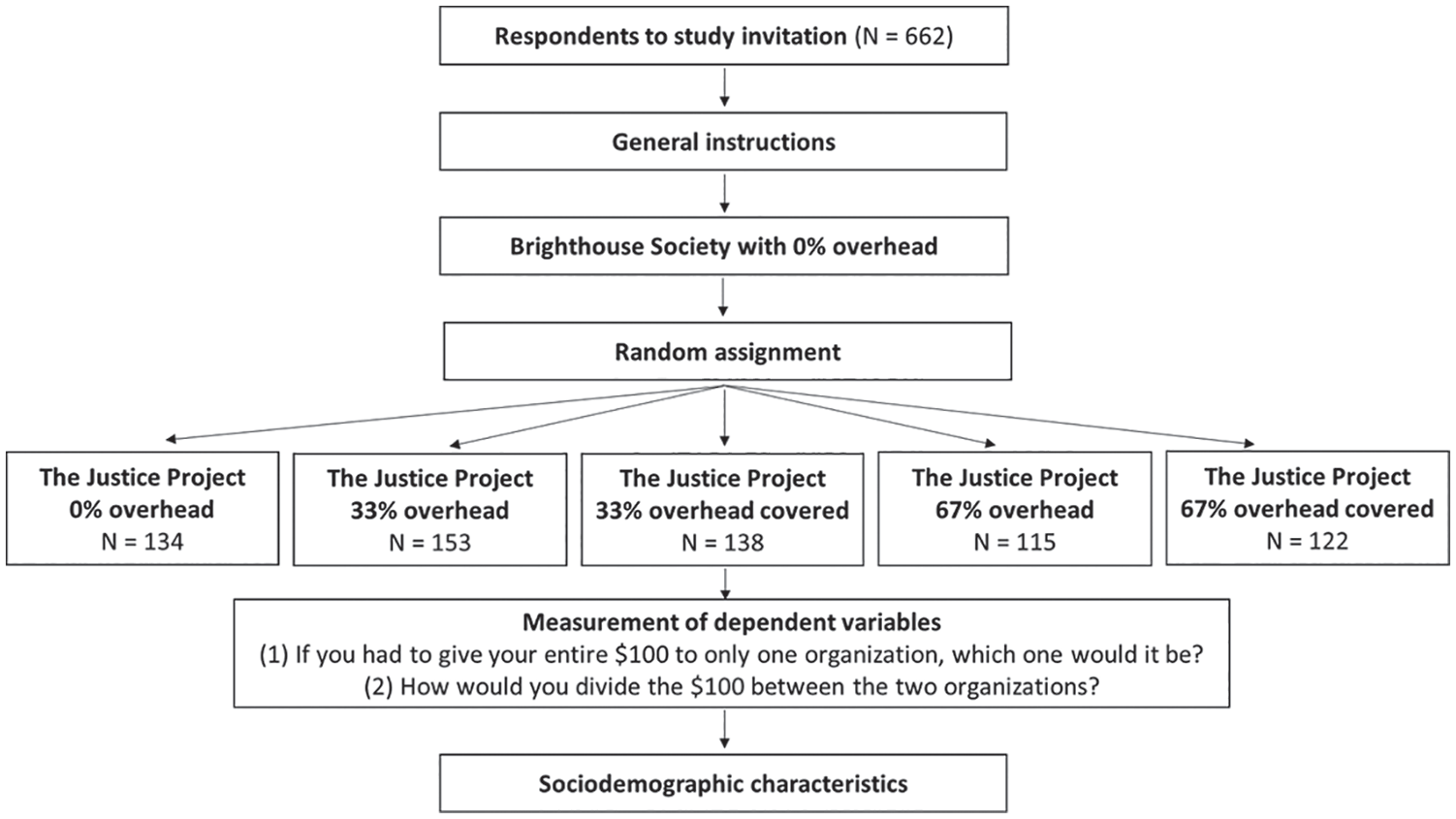

The design of the donation decision was based on the experimental design proposed and used by Gneezy et al. (2014). We used a between-subject design, and survey respondents were randomly assigned to one of the five treatment groups. All participants were presented with two charities: (a) Brighthouse Society described as a “non-profit organization that helps formerly incarcerated individuals become positive, contributing members of society” and (b) The Justice Project described as a “non-profit organization that offers opportunities for individuals who have been in conflict with the law to transform their lives through innovative, effective, and replicable programs that serve the community by reducing crime and its human and economic costs.” These two organizations were intentionally similar in purpose and mission so that treatments would be the primary distinction. All participants were told that Brighthouse Society operated with no overhead expenses and therefore all donations made to Brighthouse Society would go only to programs and mission. All participants received the same Brighthouse Society scenario plus one of the five different overhead scenarios for The Justice Project.

Appendix provides the language for each scenario. For The Justice Project, the overhead expenses associated with donations were manipulated and randomly distributed as follows:

Treatment 1: There was no overhead cost associated with donations to The Justice Project.

Treatment 2: The overhead associated with the donation was 33%.

Treatment 3: The overhead associated with the donation was 67%.

Treatment 4: The overhead associated with the donation was 33%, however an anonymous donor covered all overhead expenses, therefore 100% of the donation would go toward programs and mission.

Treatment 5: The overhead associated with the donation was 67%, however an anonymous donor covered all overhead expenses, therefore 100% of the donation would go toward programs and mission.

We followed the approach used by Kim and Van Ryzin (2014) where all participants were told based on a hypothetical US$100 budget to decide how much they would donate to each of these two nonprofit organizations if they had US$100 of their own money to give. Participants were initially advised that the whole US$100 needed to be allocated between the two organizations but could be divided however they chose. In addition, at the end of the survey, all participants were also asked the following question, “If you had to give your entire $100 to only ONE organization, which one would it be.” Figure 1 shows our experimental design in an overview and also details the number of observations for each treatment.

Design of survey experiment.

Results

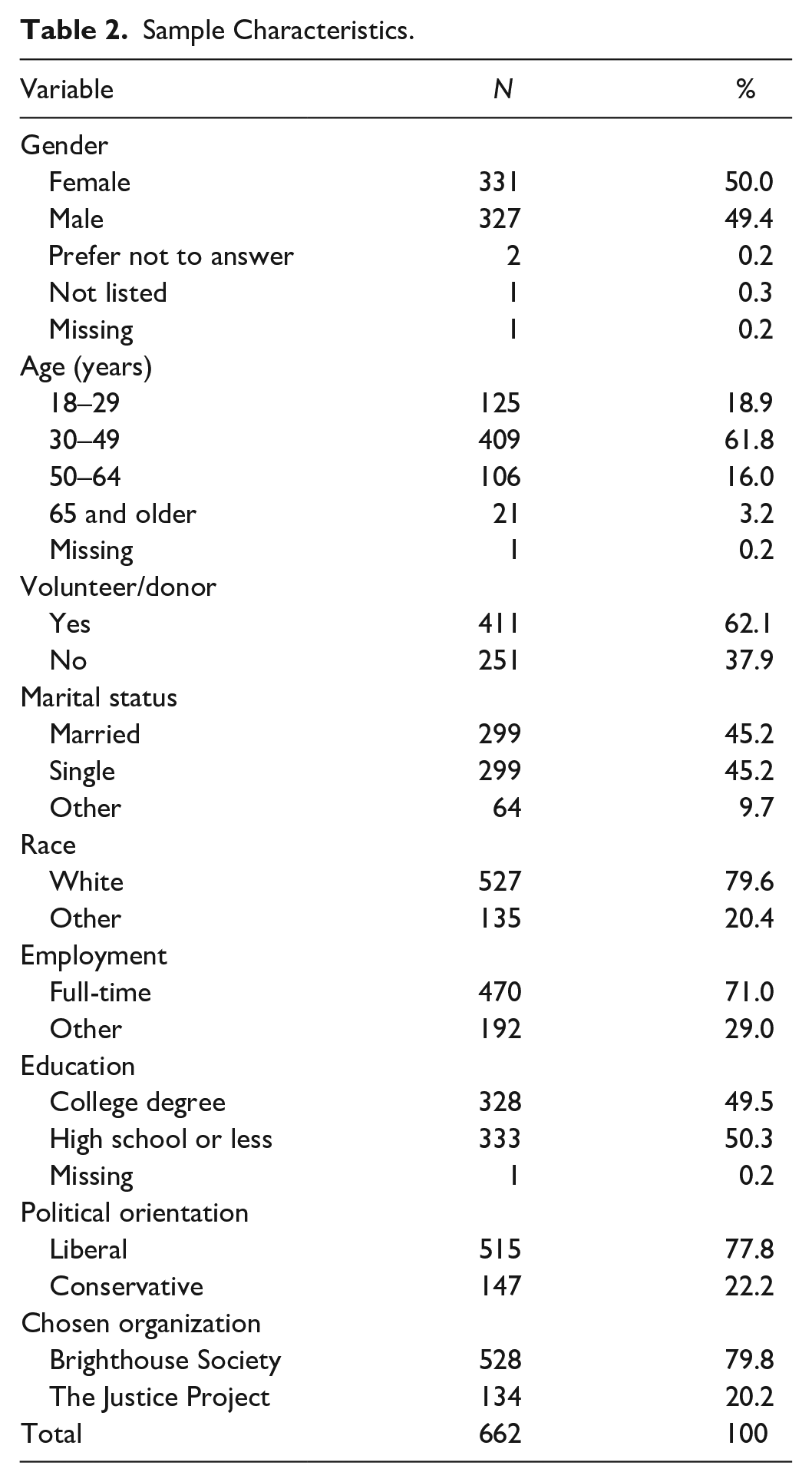

Table 2 shows the characteristics of our study sample. Sixty-two percent of respondents had donated to or volunteered with a charity in the past year, indicating that they were good proxies for individual donors. Females comprised 51% of the sample. Concerning their marital status, 46% of the sample was married or in a domestic partnership. Eighty percent of the sample identified as primarily White and 22% of the sample described their political views as conservative or very conservative. Seventy-one percent of the sample was employed full-time and 49% had at least a bachelor’s degree. We conducted Chi-square tests for each of our sociodemographic variables across the five different experimental conditions. We did not find any significant differences (all ps > .05), indicating that our randomized treatment assignment was effective.

Sample Characteristics.

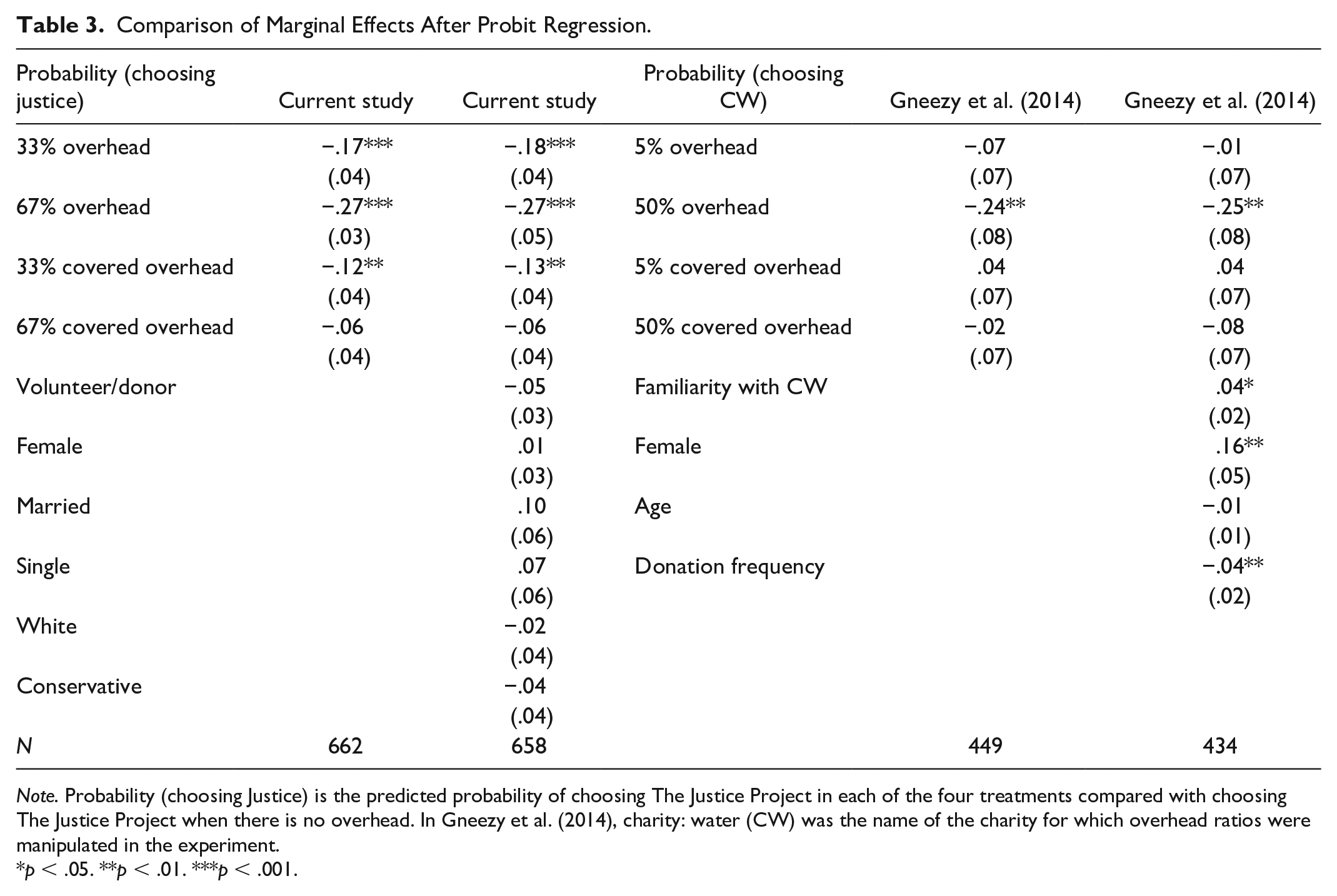

We used a probit model to regress the likelihood of choosing to donate to The Justice Project on dummy variables for the various treatments. This lets us test whether or not an individual is likely to give their entire donation to either Brighthouse Society or The Justice Project based on their answers to the last survey question. Table 3 shows the estimated marginal effects of our probit regression analysis and compares our results with the study by Gneezy et al. (2014). Our results show that participants in the 67% overhead treatment were significantly less likely to choose to donate to The Justice Project than participants in the no overhead treatment. When the overhead cost was covered (67% covered overhead), although participants were less likely to choose to donate to The Justice Project than participants in the no overhead treatment, the results were not statistically significant. Specifically, participants in the 67% overhead treatment are 20% less likely to choose The Justice Project than participants in the no overhead treatment. Participants in the 33% overhead treatment (33% covered overhead) were 15% less likely to choose The Justice Project than participants in the no overhead treatment without the anonymous donor and 11% less likely with the anonymous donor. All results were statistically significant at the 1% confidence level. Marital status is the only demographic variable to impact results (z = 1.77) indicating that results are robust across age, education, volunteering, race, and political persuasion.

Comparison of Marginal Effects After Probit Regression.

Note. Probability (choosing Justice) is the predicted probability of choosing The Justice Project in each of the four treatments compared with choosing The Justice Project when there is no overhead. In Gneezy et al. (2014), charity: water (CW) was the name of the charity for which overhead ratios were manipulated in the experiment.

p < .05. **p < .01. ***p < .001.

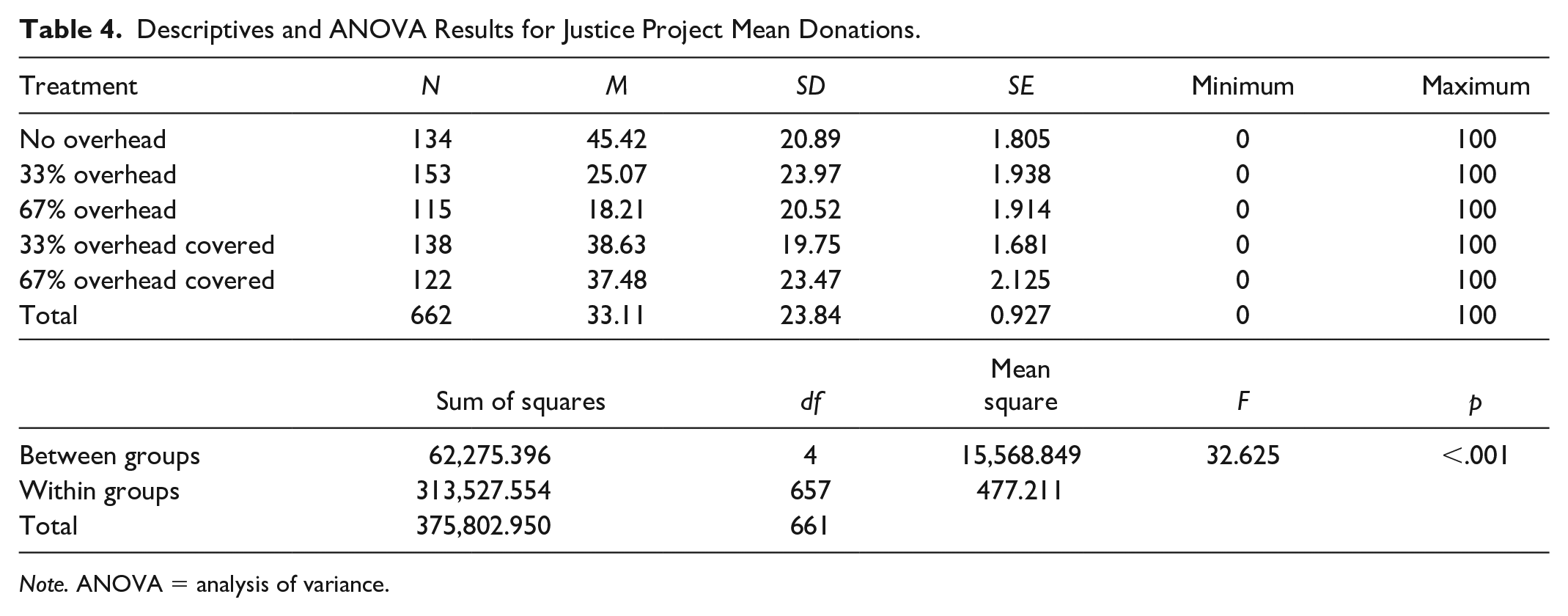

When respondents were asked to select only one organization to give their entire US$100 to, they chose Brighthouse Society 79% of the time. As Brighthouse Society came first in the survey, we suspected some ordering bias and examined the mean donations between Brighthouse Society (no overhead) and The Justice Project no overhead scenarios (N = 128). Of those who responded to The Justice Project no overhead scenario, t-tests confirmed a significant difference between the Brighthouse Society and The Justice Project no overhead scenarios (t-value = 3.49, p = <.001) confirming ordering bias. Therefore, we further tested our hypotheses by examining mean donations made to The Justice Project across the different groups using an analysis of variance (ANOVA). In this robustness test, The Justice Project no overhead scenario served as the control with the various overhead scenarios as treatments. Regarding the donation amount as our focal dependent variable, there was a statistically significant difference between groups as determined by one-way ANOVA (F = 32.880, p < .001). See Table 4 for detail on those results.

Descriptives and ANOVA Results for Justice Project Mean Donations.

Note. ANOVA = analysis of variance.

According to expectation, a Bonferroni post hoc test (Bonferroni was used rather than Tukey due to unequal sample sizes) revealed that the donation amount in the no overhead scenario was significantly higher than in the 33% overhead condition (US$20.41, standard error = 2.574, p < .001), the 67% overhead with donor condition (US$7.99, standard error = 2.724, p = .035) and 67% overhead condition (US$27.26, standard error = 2.767, p < .001). If a donor was covering overhead, the mean donation was higher for some overhead groups. Donation was statistically significantly higher for the 33% overhead with donor group when compared with 33% overhead (US$13.57, standard error = 2.564, p < .001), or 67% overhead (US$20.42, standard error = 2.758, p < .001) without a donor covering that cost. For the 67% overhead with donor group, the mean donation was significantly higher than both the 33% overhead group (US$12.42, standard error = 2.651, p < .001) and 67% overhead group (US$19.27, standard error = 2.839, p < .001). There was no statistically significant difference between the 33% overhead with donor and 67% overhead with donor (p = 1.000), 33% overhead and 67% overhead (p = .112), or no overhead and 33% overhead with donor (p = .098). Table 5 provides detail on the pairwise comparisons.

Multiple Group Comparison of Justice Project Mean Donations.

p < .05. **p < .01. ***p < .001.

As a final step of our analysis, we tested whether our results remain unchanged if we only consider those participants who indicated that they gave or volunteered (62% of the sample, N = 410). Only considering participants who actually display prosocial behavior can to some degree address concerns over limited external validity of online experiments. The results remain unchanged.

These results are as expected and support the assertion in early literature regarding donor overhead aversion. When donors are aware of the overhead expenditures, they choose to donate larger amounts to organizations having lower overhead expenses with the amount of donation declining the higher the overhead ratio. These giving decisions were modified when the overhead cost was covered by an anonymous donor and would not impact the individual’s gift; however, even in circumstances where the overhead cost was covered by another donor, donors preferred organizations with less overhead cost even if their gift was helping to cover overhead expenditures.

Conclusion and Discussion

Recent years have seen an uptick in experimental studies investigating the relationship between financial efficiency ratios and private giving. Experimental studies hold the potential of establishing clear causality between financial ratios and giving, which has been identified as a shortcoming of earlier studies that explored the relationship by means of organizational-level archival financial data (Garven et al., 2016). The goal of our study was to reexamine the experiment by Gneezy et al. (2014) with a nonstudent sample to further assess the effectiveness of advertising overhead-free donations. In general, our study provides support for Hypothesis 1 and confirms previous findings that donors give less to organizations with higher overhead ratios, once two organizations can be compared based on financial data. However, regarding Hypothesis 2 and the impact of an anonymous donor covering overhead expenses, our study yields mixed results. Informing donors about an anonymous donor covering overhead had a strong effect on donations amounts.

However, regarding the likelihood of giving, we can only confirm the findings by Gneezy et al. (2014) in the 67% overhead treatment, where overhead aversion indeed disappeared in light of an anonymous donor. However, in the 33% overhead treatment, donors were still significantly less likely to give in the presence of an anonymous donor. Based on Duncan’s impact philanthropy argument that we use in our theory section, a higher covered overhead might lead to even more perceived donation impact, which might explain why donors were more inclined to give at “67% covered” compared with “33% covered.”

Against this backdrop, we argue that organizations should consider carefully the solicitation of overhead-free donations as a strategy to circumvent overhead aversion. First, our findings only partially support the strategy, and second, overhead-free donations can create unrealistic donor expectations and overhead aversion in the future (Gregory & Howard, 2009).

In recent years, sector advocates like CalNonprofits have argued that the use of overhead spending as a primary proxy of financial health and stability is intensely flawed and has brought a number of unfortunate consequences to the nonprofit sector. For example, reducing spending on overhead can negatively impact a nonprofit’s ability to initiate fundraising campaigns, invest in long-term planning, sufficiently support overall infrastructure which can ultimately undermine efforts to fulfill the mission effectively (Hager et al., 2004). In addition, it may encourage dysfunctional behavior by managers like hiding administrative expenses as a part of programmatic expenditures and underreporting of fundraising expenses (Krishnan et al., 2006; Parsons et al., 2017). Furthermore, Hager and Flack (2004, p. 4) argue that competition to show low overhead expenses “induces nonprofit managers to under-invest in good governance, planning compliance, and risk management, collection of data for service performance evaluations and staff training.”

Donor aversion to large overhead expenditures puts nonprofits under immense pressure to reduce overhead spending and spend more on direct program expenses. Many foundations and government agencies refuse to include a nonprofit’s overhead calculations in grant awards which has resulted in nonprofits squeezing out overhead expenditures or hiding administrative expenses as part of programmatic expenditures (Ashley & Faulk, 2010; Ashley & Van Slyke, 2012; Eckhart-Queenan et al., 2019). These funders believe, that somehow, nonprofits should be able to operate programs without an administrative structure to manage, measure, and execute and implies that, by some as-yet-unknown magic, nonprofits should be able to achieve their mission without dedicated and systematic fundraising efforts to pay for it. (Knowlton, 2016, p. 3)

Marwell and Calabrese (2014) illustrate that government nonprofit relations are characterized by a “deficit model”: Governments commonly do not fund the full costs of nonprofits’ program delivery and nonprofits therefore have to raise additional private resources to sustain their operations. Decision makers in governmental agencies and public administration scholars should carefully reflect on this model because it potentially harms nonprofit financial health and service delivery.

Against this backdrop, Mitchell and Calabrese (2019) argue that minimizing overhead constitutes a fundamental paradigm that guides nonprofit financial management. Although public administration scholars continuously reevaluate the dominant managerial paradigms within the public sector (such as new public management and more recently new public governance), so far the guiding principles of nonprofit management are less frequently questioned in scholarly work. Nonprofit scholars therefore need to follow suit and more proactively engage in a debate on alternative accountability mechanisms to govern the relationship between nonprofits and their resource providers.

Our study is subject to a number of limitations. First, although the experimental environment offers advantages in terms of isolating the effect of overhead, donors in an experimental environmental may behave differently from the way they would in real life when faced with a similar choice (see for instance Benz & Meier, 2008). Giving is motivated by many factors not the least of which is a personal link to the activity being funded (Sargeant & Woodliffe, 2007). Such motivations may supersede giving decisions based on overhead plus organizations may not present high overhead the same way they currently publicize low overhead expenses (Sloan, 2009). Second, donors will not always have complete information regarding a charity’s overhead ratio in which case only a few will seek it out. Without knowledge of overhead, donors will make their giving allocations based on other factors (see findings from Buchheit & Parsons, 2006).

On the positive side, results indicate that donors are willing to allocate funds to organizations with some overhead expenses, the more so when those expenses seem reasonable or not extreme. We can conclude that because all respondents viewed the Brighthouse Society scenario first, which had no overhead expenses indicated, and some donors chose to allocate some money to The Justice Project when given the opportunity, even when The Justice Project scenario indicated higher overhead expenses. However, when given a stark choice between no or lower rates of overhead, donors rewarded organizations those organizations having less overhead with higher donations.

Caution is warranted when equating increased program spending with increased accountability because the ratio offers a snapshot of an organization at a particular moment in time and does not necessarily indicate broad accountability practices across an organization. Furthermore, organizational leaders must find the appropriate ratio for their specific organizational mission, stage of organizational growth, and administrative capacity.

Results of this analysis affirm the persistent evidence of overhead aversion exhibited in the literature and underscore the need to educate donors regarding the purpose of overhead expenses in the overall fiscal health of nonprofit organizations.

With regard to future research, we call for more studies that test potential strategies by which organizations can cope with overhead aversion of their donors. Most experimental studies to date have focused on establishing the existence of overhead aversion. Now that we have a better understanding of donor attitudes and behavior, future research should instead focus on testing different tactics and strategies, for instance, different options of framing overhead expenses. Such studies could test whether framing overhead costs more positively—for instance, as investments into organizational capacity and mission achievement—leads to more positive donor attitudes and giving behavior. Alternatively, future experiments could test whether informing donors up front about the need for overhead, that is, raising awareness for its vital role changes donors’ response patterns. To address the limitations of laboratory and online experiments with respect to their external validity, field experiments would greatly contribute to the robustness of our findings in a more natural giving context. Future research could also further explore the roots of overhead aversion. Is overhead aversion a result of the overhead myth, that is, a persistent norm in the nonprofit sector perpetuated by watchdogs, media, donors, and organizations themselves? Or is overhead aversion instead more deeply rooted in the cognitive processes that underlie giving decisions, as suggested by Duncan (2004)? Providing answers to these questions could be of great practical relevance for the nonprofit sector.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research and/or authorship of this article: This study received funding from the Rutgers SPAA Faculty Research Funds AY17-18.