Abstract

Following the academic discourses that the International Business (IB) has not yet seen the levels of academic intrusions on decoupling a thorny ethical dilemma evident in other fields that explains why organizations when strive for conformity, they may attempt to preclude the necessity of their formal structure with an intention to show obedience towards institutional settings while at the same time actually practicing business in ways that they believe are more efficient. This study attempts to bridge this important gap and understanding of decoupling in the burgeoning stream of IB where export organizations decouple from the actual substantive conformity to the Intellectual Property Rights and the Protected Designation of Origin certification requirements. This policy to practice decoupling in the form of avoidance from institutional pressures and concealment manifest itself in the organizations zeal to placate the pressures of resource criticalities brought about by this unique isomorphic setting of the home and host country institutional landscape(s). Thus theoretically, tight coupling between institutional rules (and pressures) and export organizations does not necessarily translate from form to function but rather ceremonial conformity, which may further be heightened by onward problems of enforcement of these rules in the same institutional settings therein.

Keywords

Introduction

In the institutional environment, the International Business (IB) is the domain where organizations strive for legitimacy and growth (Boddewyn et al., 2004) exposed to multiple tensions and changes (Andrian and McKelvey, 2007). Faced with institutional pressures, organizations develop various responses. Institutional pressures may be exempted and disconnected (Djelic and Quack, 2003; Kostova and Zaheer, 2008) exhibiting a yo-yo movement (D’Aunno et al., 2000) or can be associated with decoupling (Maclean and Behnam, 2010; MacLean et al., 2014). Decoupling occurs where organizations striving to conform to institutional pressures may preclude the necessity of formal structures by practicing businesses that they believe are more efficient (Boxenbaum and Jonsson, 2008; Bromley and Powell, 2012; Kostova and Zaheer, 2008; Maclean and Behnam, 2010; Meyer and Rowan, 1977). Notwithstanding the widespread issues of decoupling in non-IB literatures, these discussions are vague in the IB and have not seen the level of academic interests (Doh et al., 2010; Leonidou et al., 2013), despite the role and importance generated through the economic activity of export organizations and institutions. Hence, decoupling is an important issue in our study and contributions. This brings us to ask ‘whether’ decoupling makes export organizations preclude the necessity of institutional pressures and ‘how’ export organizations avoid applying these formal rules showing ceremonial conformity through the use of misconduct. This brings us to our proposition that in contrast to where conformity to institutional pressures is predominant, there are two forces (in decoupling) aligning the policy–practice that display how organizations ‘avoid’ executing formal rules through ceremonial conformity (Bromley and Powell, 2012; Oliver, 1991) in the Home and Host environments. This study further proposes that export organizations preclude institutional conformity via ‘misconduct’ where institutional pressures and expected practices are disobeyed by organizations (Maclean and Behnam, 2010; Vaughan, 1999). The structure of this article is laid out as follows: theoretical background, methodology, research findings, conclusion, contribution, managerial implication and limitations therein.

Theoretical background

Policy–practice

In the IB literature, the groundwork and operation of organizations are affected by domestic and foreign regulatory pressures (Keupp et al., 2010). Due to strategic national and international expectations, organizations responses to regulatory pressures in the form of policy–practice relationships may conform to one set of institutional pressures such as international certifiable standards or may avoid others. Given the above view, although there are a reliable certification and indicator of the actual implementation of specified practices instituted by the institutions, there may not be conformity thus hampering the effectiveness of certifiable institutional pressures (Boiral, 2003; Christmann and Taylor, 2006; Yeung and Mok, 2005) for to remain competitive, organizations may bypass institutional policies and formal rules that compromise their competitiveness and economic positions (Papageorgiadis et al., 2013).

Avoidance

According to Bromley and Powell (2012) what translates from policy–practice is decoupling and together with Oliver (1991) this policy–practice decoupling can be described through the response of ‘avoidance’ to institutional pressures in the form of ceremonial conformity. An important response to institutional pressures, avoidance (Bromley and Powell, 2012; Meyer and Rowan, 1977; Oliver, 1991; Pfeffer and Salancik, 1978) is where organizations attempt to preclude institutional conformity via specific tactics of concealment, buffering or escape from institutional compliance (Oliver, 1991). Based on Oliver’s (1991) typology of organizations responses to institutional pressures, organizations respond to prevent conformity either through ‘concealment’ or through disguise, ‘buffering’ by loosening from institutional attachments or ‘escape’ by changing activities or domains. According to Oliver (1991) to determine the kind of tactics is crucial to address and answer questions: (i) (cause) why institutional pressures are exerted and why disagreement exists between institutional pressures and organizations; (ii) (constituents) who exerts institutional pressures; (iii) (content) what pressures, norms or requirements organizations are pressured to conform; (iv) (control) how or by what means pressures are exerted; and (v) (context) where these pressures occur, that is, the environmental context where institutional pressures are exerted. The presence of uneven export organizations responses arising from organizations dependence on institutional pressures, constituents, prompted IB scholars to explore the cause of these responses. Studies show that the asymmetric content between formal blueprints and practices hinders conformity, sustaining uneven practices of organizations. This highlights the gap between the control of institutional pressures and the alignment of organizations practices used to direct institutions away from these harmful activities.

Concealment

Due to the strategic national and international expectations of both domestic and foreign organizations; prior and post-research explains that given the choice of nonconformity, organizations may conform to one set of institutional pressures, deviate or avoid others (Christmann and Taylor, 2001; Stening and Zhang, 2017; Wang et al., 2013) via specific tactics that display they are already aware of how to preclude institutional conformity to the prevailing logic of institutional constraints (Aquilera et al., 2018). In particular, Christmann and Taylor 2006 and Wang et al. (2013) explain the variation in Chinese institutional pressures where the enforcement of pollution regulation is subject to variations not through the central government but through the ‘decentralization’ interpreted by the local and regional Chinese authorities. Deviation of the Chinese environmental protection shows that institutional failure to protect the environment might be remediated by the Foreign Direct Investment (FDI) adoption of environmental performance standards beyond the requirements of institutional pressures in developing countries (Christmann and Taylor, 2001). Similarly, deviation from the Chinese environmental protection shows that the FDI organizations adopt decisions, the control to emit pollutants, beyond the permitted official levels. Even if the institutions have the intention to protect the environment, lack of technical resources and differences in environmental regulation gives FDI organizations an advantage to move to locations having low environmental standards as an investment stimulus. Instead of showing voluntary conformity to moral standards and legislation, these variations (or concealment) are boosted with political connections with local officials or through paying fines. Thus, to avoid institutional pressures and disguise nonconformity, concealment tactics are used through misconduct with local governmental officials (Christmann and Taylor, 2001; Wang et al., 2013). The same can also be attributed by the high-ranking local Chinese officers interfering with regulatory enforcement (Gao, 2011). Hence, misconduct allows FDI organizations to conform to institutional pressures, alongside compromising conformity through concealment. Concealment is also found by Fung et al. (2011) in FDI organizations in China, given the market economy and fixed exchange rate with preferential tax treatment contrary to developed destinations, they are able to bypass institutional pressures using differential tax treatment via trade figure manipulation.

In every research investigating organizations responses in the context of taxation treatment, it is essential to establish conformity or nonconformity and whether it is acceptable to challenge institutional pressures by use of avoidance (Demirbag et al., 2013; Kottaridi et al., 2019). As countries have its economic and political rights, in the content of levy taxes; organizations are institutionally controlled to pay their share both in appearance and in substance (Dowling, 2014). Findings of Fung et al. (2011) display how the cause of this tactic to ‘unacceptably’ preclude conformity to formal structures and avoid coercive taxation pressures misleads regulatory institutions. For example, the improper communication of measures and press releases can mislead where excess capital offshore are sent by overstating the import invoice as FDI and return capital to China or to reduce tariff imbursements of imports by under-reporting from higher to lower tax categories. Due to regulatory systems’ loopholes, concealment is also present where FDI organizations mislead regulatory institutions to leave certain income or enter less than actual in accounting books (Hung, 2008). Both tactics overshadow the importance of coercive taxation via mispricing practices (Fung et al., 2011). In academic discourse, misleading is where organizations, at first sight, present themselves as law-obedient when they actually mislead the institutions from discovering the hard facts (Entwistle et al., 2006; Smieliauskas et al., 2018; Westphal and Zajac, 2001).

Buffering

According to Kavali et al. (2001) although institutional constituents should be treated by organizations as ‘the floor’, where institutional pressures are weak or improperly enforced, the nonconformity of organizations to institutional pressures creates a smokescreen that allows the unethical behaviour to increase. Organizations avoid the control of written codes using bribery to government officials to influence policies and secure public-sector contracts away from competition. Similarly, written codes are disregarded through tax evasion by not issuing invoices so that limited reported profits will cause in lower tax jurisdictions. In practice, organizations believe the country’s loosening institutional pressures lead to a reduction of conformity that increases whenever there are less scrutiny and evaluation by the authorities (Kavali et al., 2001). Failure of institutions to protect the domestic or foreign countries’ markets push organizations to misconduct unless the management of these organizations is supportive of its codes and ethical concerns to absorb regulatory pressures (Kavali et al., 2001). Export organizations can be a mechanism for arbitraging institutional weaknesses around the world in areas with relatively weak Intellectual Property Right (IPR) pressures (Ivu et al., 2017) but also can take the rational decision to unacceptably’ preclude conformity to formal structures by avoiding weak IPR pressures (Peng et al., 2017). That is, organizations do not simply avoid conformity, but they also need the ability to preclude institutional pressures in case their organizational structure and foreign identity empowers international experimentation (Edman, 2016). Jamali’s (2010) research on Multinational Enterprises (MNEs) shows conformity between International Accountancy Standards and organizational values; these standards provide opportunities for symbolic conformity where loosening institutional policy lead MNEs to bypass institutional pressures. Low efficiency and pressure produce avoidance of institutional standards through buffering of internal practices, while allowing organizations to operate independently from these pressures and remain unevenly adopted (Jamali, 2010).

On the African forefront, Luiz and Callum (2014) argue that African countries’ markets are perceived by many MNEs to be sources of ‘quick win’. Because institutions in developing countries have a direct impact on MNEs by raising or lowering the transaction costs to expedite businesses, organizations respond to institutional pressures either through replicating local business models or through sacrifice business performance where the probability of being caught and punished is higher (Luiz and Callum, 2014). The authors explained that the African countries are ‘grey areas’ for weak control in the regulatory and political systems lead to loosening relationships with institutional pressures. Organizations in grey areas free themselves from blame by disguising nonconformity for they see themselves as victims of higher uncertainties and costs contributed by weak institutional pressures. Thus to bypass institutional weakness and expedite business, MNEs use buffering and concealment that includes misleading the non-standard operational practices to reduce market costs, delays and risks of market efficiency to competitors (Luiz and Callum, 2014). MNEs do not simply decouple from Host institutional pressures; rather, they unilaterally bypass these constraints in the belief that it is the weak institutional policies and improper enforcement that lead them to nonconformity.

According to Chen et al. (2010), misconduct is present in the financial analyst organizations due to pressure, harassment and scrutiny of institutions causing loosening to institutional pressures where published forecasts are not politically accepted by ‘connected’ organizations. Thus, for ‘favourite’ organizations having political connections, their financial transparency is masked allowing them to misconduct at the expense of others. This institutional favouritism and double standards pressures financial analysts to avoid forecasting real earnings (Chen et al., 2010) creating a policy–practice decoupling, allowing favourite organizations to symbolically conform thus hiding secret reserves that cannot be justified officially.

Escape

The presence of escape can be seen where organizations act strategically to avoid institutional pressures reaping the benefits of formal rules existing abroad (Kottaridi et al., 2019). From the Mexican study of Gillespie and McBride (2013), the presence of escape can be seen in the context of the Korean and Chinese diaspora of wholesale and small retail businesses. Here, counterfeit trade in Mexico far exceeds other legitimate practices in Home destinations. As there is high discrepancy from institutions and enforcement, this increases the bypassing of institutional control via bribery within the customs department (misconduct/misleading) and the government (misconduct/misleading) causing in rapid Mexican economic growth. These practices enable organizations to escape by changing domains, avoiding conformity as with the rest of the Mexican economy, as there is just a small difference in performance outcomes between the well-behaved organizations and that of misconduct behaviour (Gillespie and McBride, 2013). Escape according to Bruton et al. (2011) is also prevalent in Guatemala and the Dominican Republic in Latin America where very small entrepreneurial businesses try to escape from institutional pressures when they borrow microloans (small, unsecured loans to generate trade within poor communities); avoid formal registration of licenses as legitimate organizations and escape from taxation thus precluding the necessity of conformity by starting out informally, staying out of formal institutional boundaries and refusing to change status even there is business registration reform (Bruton et al., 2011).

In relation to misconduct or misleading practices, the literature shows that the size of organizations and market experience are two material components of policy–practice decoupling. In particular, the size of (Medium/Large) organizations and Host market experience influence the likelihood of misconduct or misleading either through concealment or buffering (Table 1). The same is true for both (Micro/Small) organizations with Host market experience and that of (Micro) organizations without Host market experience to engage in misconduct or misleading by changing its activities or domains through escaping (Table 1).

Policy–practice decoupling.

IB: International Business; FDI: Foreign Direct Investment.

Organizations are also affected by competition where to remain competitive, they use misconduct or misleading practices. Competition pushes (Medium/Large) organizations to misconduct by concealing the emission of pollutants beyond the (Host) competitors’ official levels. Competition also highlights why (Large) organizations conceal misconduct to secure public-sector contractual arrangements from rivalry (Host) or misleading to increase the manoeuvre of (Host) competitors against institutional pressures. In the same manner, organizations (Micro/Small) misconduct and mislead through escape from institutional pressures and from being legitimate against other (Home/Host) market participants.

Methodology

Research background

Based on Oliver’s (1991) typology, this research attempts to display institutional pressures by a cluster of European Union (EU) member states. Greece the subject of investigation that has undergone a serious economic crisis the last decade (Manasse and Katsikas, 2018) holds the IPRs in the form of the Protected Designation of Origin (PDO) certification on its traditional Feta product (EC, 2006; EC, 2012), where it comes under the European Community Regulations No. 1151/2012, the Common Delegated Regulations No. 664/2014 and the Commission Implementing Regulation No. 668/2014. These regulations are institutional pressures on export organizations to maintain the designation of origin, that is, the product must be produced, processed and prepared in specific geographical locations (EC, 2012, 2014a, 2014b). This institutional pressure produces economic barriers in the form of resource constraint that impacts heavily on Greek exporters and its ability to compete domestically and internationally. This study fully complies with Ethical Standards. All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki declaration and its later amendments or comparable ethical standards.

Pilot study

This research follows a qualitative investigation (Creswell, 2009; Crotty, 2003) coordinated through previous academic research, observation, recording and analysis (Sinkovics et al., 2008). In the pilot study, six cases are used, three small and three medium, because a majority of the EU PDO organizations are small or medium with managers as key representatives because they are instrumental to plan and execute activities relating to export (Hackett and Dilts, 2008; Yin, 2009). Eventually, small organizations are taken out from the main investigation because they are inherently secretive and reluctant from revealing information due to fear of leaking trade secrets and business confidentiality. Similarly, small organizations are not engaged directly in exports as exports sub-contracted to market agents. Thus, research samples for the core investigation change from the small to medium and large units of analysis.

Main study

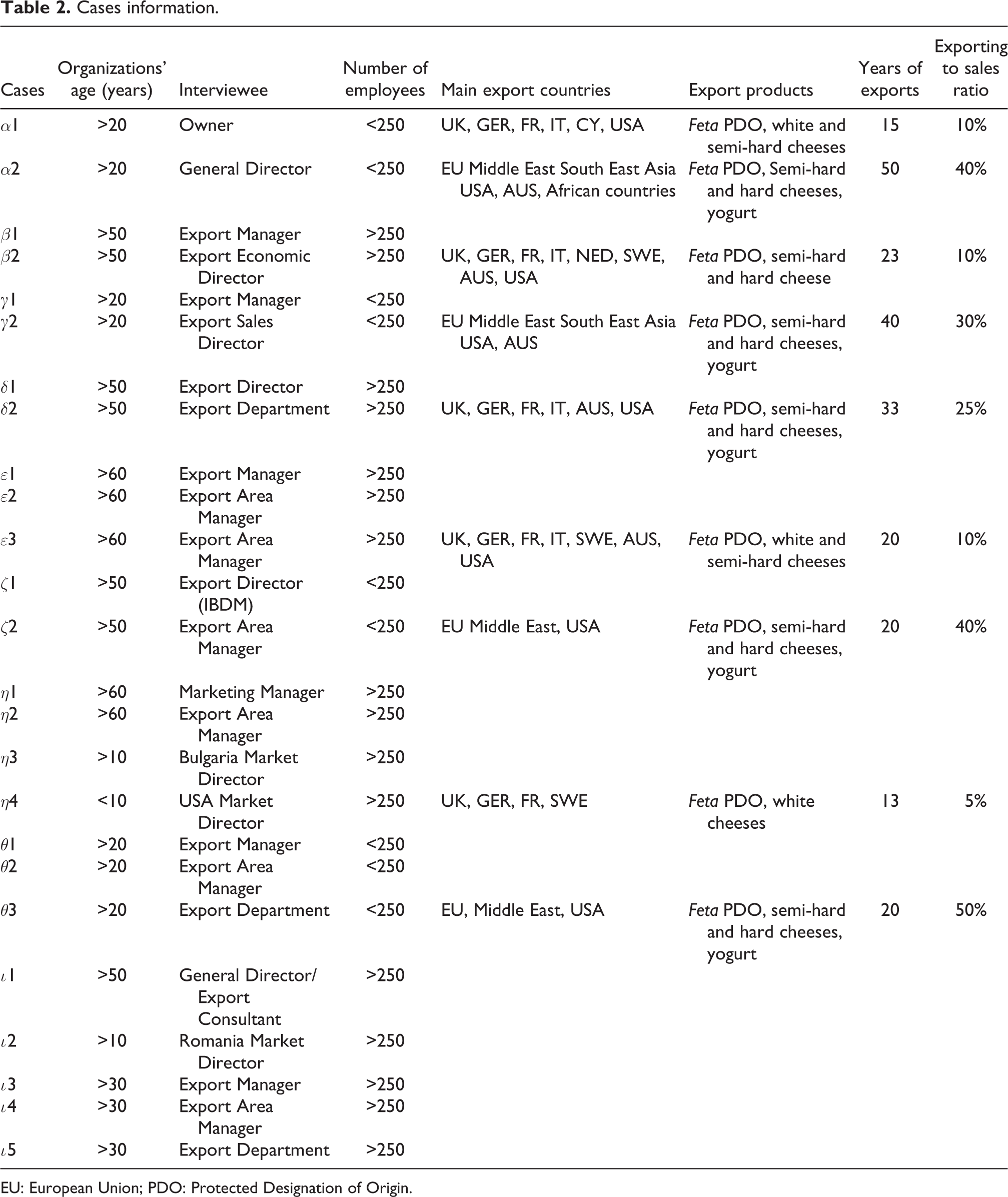

The two types of medium and large organizations are taken from the ‘Hellenic Milk Organizations’ (ELGO) registry database of buyers–processors, cooperatives and producers (Table 2). ELGO manages the production of resources and advisory services to Agencies on production and distribution of Greek resources; legislation of the EU and obligations of buyers towards organizations. This database is also used for sectoral studies of institutional departments of the EU and Greek Agricultural Economics and Sociology Institution. Of the 13 interested organizations, only 9 are chosen to participate in forming the reliable list of 25 respondents. The other four organizations decide to withdraw from this investigation. These organizations are the largest exporters as holders of the IPR/PDO certification issued by the EU carrying the right as the sole legal exporters worldwide. The 25 respondents are chosen to explore export organizations and management practices. The notion of management practices is important for the management is normally comprised of people with status and volitional control who execute final decisions on behalf of the majority (Welch et al., 2002).

Cases information.

EU: European Union; PDO: Protected Designation of Origin.

The aim of the study is to select information on rich cases that illuminate research questions (Gerring, 2004; Patton, 1990). To minimize the selection of extreme cases, the nine export organizations choose their own respondent lists from the sample of potential respondents (Gerring, 2001), thus confirming the perception of representative respondents selection as purposeful (Patton, 1990).

Interviews

The interviews in this study are conducted on 1 Owner, General Managers of 3 countries (USA, Bulgaria and Romania), 11 Export Managers/Directors, 6 Export Area Managers, 3 Export Assistants and 1 Marketing Manager (Table 3). To reduce potential bias and ensure a rich multiplicity of responses, interviews are limited not to the upper echelon of the managers but also to the headquarters’ staffs and external experts (Regnér and Edman, 2014). To avoid language barriers, interviews are strictly conducted in the national language (Krave and Brinkmann, 2008) for 40–80 min (Bernard, 2000; Patton, 2002). All interviews are recorded, verbatim transcribed, translated and analysed. The medium of Skype is used where physical interviews are impossible due to business obligations or where respondents find themselves attached with subsidiaries in foreign locations.

Interviews.

Coding/Analysis

The interviews are transcribed with Express Scribe software and 500 pages of transcripts are checked for translation data cleaning errors (Robson, 2011). Then we proceed with coding via the assisted qualitative data analysis software (CAQDAS) (Mason, 2008). However, as this qualitative investigation bears heavily on an interpretative approach, before CAQDAS is used; the researchers make coding manually to interpret and understand the data with a case-by-case clarification. The moment findings are formed into codes, and the data start breaking down into smaller parts (Miles and Huberman, 1994; Yin, 2009). This facilitates questioning by giving further critical evaluations without destroying meanings through intensive coding (Eisenhardt, 1989). This evaluation emerges from a zigzag exploration (Patton, 2002), which is a major characteristic of qualitative research. Coding is built via the NVivo code description (nodes, family nodes and themes) for further exploration and insights (Robson, 2011) following a thematic structure (Mason, 2008). Coding is based on the concept of open and axial coding and pattern matching (Gerring, 2004; Saldana, 2009) in which they correspond and interrelates with one another, the former where data are harvested and separated after examination and the latter to connect concepts or categories. For codes description, Mega Matrix is used to facilitate the flow and connection of events and to indicate and establish for every category its dimensions (Miles and Huberman, 1994; Yin, 2009). Initially, the first- and the second-level constructs are built. The NVivo analysis is then used with Mega Matrix to form the third- and fourth-level constructs. The initial step is to assemble cases inside phases to uniformly minimize the content of information from interviews. Then, this is reduced and narrowed as ‘Relevant Data’ which act to distinguish it. Then ‘Summary-Tables’ are constructed to list all distinctive factors and data for further comparison analysis (Sobh and Perry, 2006).

Data interpretation is done and analysed via cross-case comparison to increase generalizability, clarity and unambiguity (Gerring, 2004; Miles and Huberman, 1994; Ragin, 1987; Sinkovics et al., 2008). To validate results and increase trustworthiness, we combine multiple sources of evidence. Conceptual categorizations from present academic literature with data triangulation of interviews, secondary data and analysis help support the internal validity. Interviews are triangulated with other documental origins such as press releases, newspaper articles, annual reports and direct observations vital and imperative for the case study (Gerring, 2004). Secondary material important to ascertain the time of different events recounted in interviews provide further details together with field notes quotations, which are the hard evidence of this study. Thus, cross-pattern matching, the coherence of findings and how these concepts are connected systematically are essentially secured (Riege, 2003). The chain of evidence from the case–study protocol is also carefully maintained in various rounds of data analysis up to the study’s conclusion. Credibility through the case–study protocol and case–study database is assured following the principles of good practice to minimize potential error or bias in the study (Yin, 2009).

Findings and critical views

Right to PDO status

This research based on Oliver’s (1991) typology of organizations strategic responses is to find evidence of decoupling in PDO export organizations in Greece. The IPR attached to the PDO certification of the European schemes of geographical indications and traditional specialties control and protect the names of quality agricultural products and foodstuffs as α2 explains: …under the European law an EU member cannot produce feta outside Greece. Feta is a Greek name that should be produced in Greece” and the “…only thing that differentiates PDO is the origin of Greek milk […] raw material is what basically and mainly the characteristics and the production method. (∊2) …which means anyone who produces cheese with feta’s specifications, 70% or 30% goat and sheep milk allowed only for feta specifications, [under the PDO regulations…]; even though it meets the standards, in case (this) is produced in another EU country, cannot be called feta” (γ2) and “PDO product means sheep and goat’s milk only from Greece […]. (η1)

Resource criticality

However, to protect the product intrinsic value, rarity and undisputed originality resources must be produced, processed and prepared from certified geographical regions (EC, 2012, 2014a, 2014b) ‘…raw material is very important because the PDO is produced from specific milk that defines the PDO a component of its philosophy’ (β1). This squeezes the availability of resources for, without conformity, the certification shall be terminated or downgraded from the PDO certification to lesser certifications under the EU regulations. Our research findings show that since conformity is a must to certification ownership, resource criticality is continuously generated. The evidence is loudly presented: if you do not have the vital raw material you cannot do anything […] (for it) is essential to enable us to export this product” (ι2). This sentiment is repeated “uniqueness of feta is solely based on nutritional value of goat’s milk and the quantity of sheep and goats [and] there is not enough raw material available in our country, (θ1)

Policy–practice decoupling

The institutional pressures of IPR/PDO regulations impact heavily on export organizations for they are prevented from getting production raw materials elsewhere (Mandrinos and Nik Mahdi, 2016). As in our findings, to ensure survivability and interdependence of international exporters and certified producers in home and host markets; organizations misconduct in the form of avoiding institutional pressures. This presence of avoidance falls within the first tactic of avoidance outlined by Oliver (1991), which is concealment or disguise nonconformity to certification regulations. The fact that some export organizations, despite the so-called infringements continue to internationally export and market their products implies that conformity is only showing symbolic acceptance to institutional pressures. Thus, although the pressure to conform theoretically indicates tight coupling from form to function, this is not true for our findings shows that in the IB context there is a real likelihood of policy–practice decoupling through misconduct where the conformity programmes only serve as a legitimacy pretence for some of these errant organizations. Thus, we firstly propose that:

The findings below support our study that this gap in policy–practice decoupling in the form of concealment manifests itself in the drive of organizations to ease the pressures brought upon by the IPR/PDO regulations of the home and host country institutional landscape(s). Problems of resource constraint that ‘…there is not enough raw material available in our country’ (θ1) places export organizations in terms of competitors ‘at a disadvantageous position to sign contracts that will enable expansion’ (ι2) and if export organisations ‘…would not open and pave the products abroad, raw materials will tend to decrease, (because raw materials) is unpaid and through price you cannot provide employment incentive’ (ι1); this exerts great pressure in the Home environment and help small organizations to sustain uneven practices ‘outside the PDO logic’ (∊1). Additionally, the Host environment (EU) experience also forces organizations to face the international competition for we cannot compete with cheeses coming from Bulgaria, cheeses coming from other countries that cannot use the word feta, but essentially offer the same product. Unfortunately, the European market currently ignores the quality issue a lot; is more interested in the characterisation of a sheep and goat cheese provided that there is an analogous price and […] there is where the difficulty exists (∊2)

Following procedures outside the PDO logic indicates that the institutional pressures within the EU community are not adhered, meaning that exporters use double standards to create a disconnection between conformity and practice; thus, a response is used to symbolically comply with institutional pressures. This is decoupling where organizations disguise nonconformity and decouple from formal structures (showing obedience towards institutional regulations) at the same time practicing businesses in ways they believe are more efficient.

The presence of misconduct forming decoupling by errant Home organizations can be inferred by the low prices of products ‘Now some competitors I do not know how they can elaborate such low prices, and say they have authentic PDO feta’ (γ3) explains that some PDO organizations do not use the right raw materials which is ‘against the regulation’ (ι5). The same sentiment is echoed ‘…instead of using Greek authentic milk they use foreign milk’ (γ1), where ‘…companies who use bad, monkey practices, unacceptable practices’ (η4) leading some export organizations to use avoidance via ‘…not the right production practices’ (η4) and ‘…name some cheese feta without following the specific production procedures of feta’ (θ2). This is done for the purpose of directing institutional attention away from misconduct and remaining competitive (∊1–η4). Thus, export organizations instead of aligning institutional pressures and organizational practices, they conceal nonconformity as in ι5 …paradoxically and ‘absurdly’ found ways to sell very cheap ‘feta’. What they do I am not aware. But how is it possible to sale in lower prices from a company like ours when we have attained economies of scale and everything has been assessed and estimated […] they don’t use the right raw material which of course is against the regulation. …even the smallest dairy unit that makes two thousand illegalities is not audited, or has someone they know with auditing authority which can be due to corruption that exists to surpass fines and boundaries, because it has a sign that says PDO feta it can surpass all other internationalisation difficulties. (∊1)

Conclusion

This study sheds lights on the presence of policy–practice decoupling in the IB where export organizations decouple from actual substantive conformity to institutional pressures. When export organizations are bound with tight application to regulations they avoid applying institutional pressures via ceremonial conformity and change responses by favouring decoupling and concealment tactics where to remain competitive the size of organizations and market experience increases the likelihood of engaging in misconduct behaviour.

Contribution and managerial implications

This article investigates the presence of decoupling in export organizations in a given country of study. The presence of decoupling is of crucial importance as an addition to the burgeoning annals of the IB literature for nowhere has the subject been discussed if at all, notwithstanding that the management of export organizations legally subsist within the domestic and international institutional pressures for conformity to the institutional policies (Doh et al., 2010; Leonidou et al., 2013). This significant understanding of the IB literature is heightened considering that this study is the first where data and findings are conducted from interviews of the management of export organizations forming the largest group of exporters not only from a single industry or country but also from worldwide for they are the sole IPR/PDO exporters (EC, 2006, 2012). This brings us to the fact that decoupling in as much as it is the standard academic observation of organizations strategic responses to the institutional pressures (Bromley and Powell, 2012; Kostova and Zaheer, 2008; Maclean and Behnam, 2010) it also bears heavily on managerial ethical issues and that just because there seems to be much ‘shyness’ in the IB intellectual discourse to delve in decoupling does not mean that it has no material value. Thus, an important implication is acknowledging that there is decoupling through organizational concealment and misconduct for the management of the export organizations is the first step towards addressing the problems of policy–practice decoupling for the equitable benefits of stakeholders concerns in the domestic and international environment. To develop the conformity background, these stakeholders will support despite the size of organizations their market experience and competition components that pushes exporters to misconduct in both unethical and illegal conduct norms. These norms can be unethical because it violates management ethical issues and illegal because it breaches the institutional, national and international regulatory expectations (Gorsira et al., 2018).

As there is merit in acknowledging the presence of decoupling in the IB, our findings serve to enrich the IB in the IPR landscape where a comprehensive explanation of resource constraints shall contribute to highlight the internationalization process of export organizations. Consequently, another suggested implication is that the move by the management of errant organizations to bypass certification regulations possibly show the existence of contractual agreements with third parties that borders on nonconformity through ceremonial conformity. Thus, by inference, it is legitimate to academically infer that in the drive to ease resource constraints, the management of the errant export organizations may form strategic alliances that are outside the fold of the law. In short, failure to redress and contain this erroneous behaviour of organizations may have a cyclical effect on other export organizations to do likewise which shall ultimately defeat the existence and purpose of the institutional pressures to preserve and sustain export traditional industries with its primary goal that is to contribute to the country’s economic development.

Finally, this research found decoupling to be present in an export country and, thus, is important to determine its impact on all the recipients involved. The lawmakers would significantly gain from this research because institutional pressures of the IPR/PDO certification does not necessarily translate into conformity that should go into preserving the authenticity and sustainability of the traditional products; rather, the strict requirements of sourcing the raw materials only from the named and licensed geographical locations serve to push the management of export errant organizations to the regulations yet retaining the use of the certifications and symbols in both the Home and Host countries where products are sold and marketed. The findings of this study shall be useful to the lawmakers to re-evaluate the effectiveness of the relevant laws and regulations and the Home country enforcements, for problems associated with enforcement will further increase the grievances and sentiments of export organizations that their so-called ‘problems’ are not heard of institutionally and that these might act as a catalyst for export organizations to break free from conformity but rather they will be ‘pressured’ to breach it.

Limitations

This research has its limitations; in particular, this study is a qualitative research in which deductions are based on hearsay and observation of export organizations that is subjective and highly opinionated. This study touches on the sensitive issues of misconduct and as can be seen from the prior research on topics of organizational misconduct, data do not come from the admissions of misconduct organizations. Specifically, data come from other sources of hearsay or secondary data pointing towards the likelihood of misconduct or from legal judgements, for no entities would admit that they have breached or persist committing what is against the law. Notwithstanding this study does raise credible questions in the existence of decoupling in export organizations and the probable reason why and how they occur. Finally, the findings of this research focus on the specific context-bound export organizations from a single country of study; thus, its findings may not be applicable to all types of export organizations or imply transferability to other international markets. Although care has been taken to eliminate the potential bias in the sampling of interviewees, a mixed-method approach shall provide a better representation of policy–practice decoupling that forms the basis of this study. However, the findings of this research arising from the world’s biggest and sole exporters under the IPR/PDO certification that may be used as a good starting point to address the same issues in other export industries, for the requirement of resources remains the same therein.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.