Abstract

The purpose of this article is to understand what drives social enterprises in bottom of the pyramid (BOP) markets to stick to or drift away from their social mission. Based on an analysis of 192 microinsurance operators in 26 emerging markets, we find that (1) when donors are involved in the operations of the social enterprise, this leads to a greater commitment to the social mission and (2) social enterprises located in countries with poorly performing governments tend to have a lower commitment to their social mission. Given the need for social services in such countries, we offer some suggestions to increase the chances of social enterprises staying committed to their social mission.

Keywords

Introduction

The need and means to reduce poverty and empower the poor in bottom of the pyramid (BOP) markets has been a challenge for nations worldwide (Karnani, 2007; Prahalad, 2005). One of the means to achieve this goal is through financial inclusion. According to the World Bank (2018), “Financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs—transactions, payments, savings, credit and insurance—delivered in a responsible and sustainable way.” This study’s focus is on one of the key enablers of financial inclusion in BOP markets, namely microinsurance providers. Like other social enterprises, microinsurance organizations face major contradictions, namely, they are expected to be financially viable and sustainable, while at the same time, they must remain committed to their social mission. Such dual pressures make it a managerial challenge for these organizations to stick with their social mission.

Microinsurance provides many social benefits, including the following. First, microinsurance enables low-income individuals to make less risk averse and more efficient decisions with respect to their livelihood. Microinsurance allows low-income individuals to recoup their investments in the event of a catastrophes. Additionally, microinsurance allows them to secure access to microloans without collateral and obtain access to capital through microloans by giving lenders confidence in the borrower’s ability to repay if there is an accident, illness, or death to borrower. This increased access to capital allows low-income individuals to purchase market inventory, buy farm animals, start small business, or purchase higher quality seeds, and inputs. Microinsurance provides further social benefits beyond compensating policy holders in the event of a loss. In the event of a claim, microinsurance allows low-income families to continue with their life by serving as lifeline in the event there is an accident or illness of a breadwinner, loss of property/crop loss due to floods or drought. Without this lifeline, low-income individuals and their families may be forced to make undesirable decisions such as untimely selling off of assets (such as livestock) or removing children from school and hiring them out as laborers to repay loans or be forced to become migrants to urban areas, leading to many negative social consequences.

At the same time as microinsurers seek to achieve these social goals, they also need to be financially sustainable through the application of commercial and business activities (Sabella and Edi, 2016). While donors may offer support to such organizations, the assumption is that in due time, the operation would be self-sustaining. However, such an expectation, which is also one of the goals of financial inclusion, could lead to drift from the original mission of microinsurance, which is “protection of low-income people against specific perils in exchange for regular premium payments proportionate to the likelihood and cost of the risk involved” (Churchill, 2006: 12). Typically, microinsurance operators seek to fulfill this mission by charging nominal premiums and offering coverage in these high-risk markets. They face two underlying pressures, namely, the need to charge a reasonable premium to compensate for underlying risks covered and remain sustainable in the long run, while at the same time keeping the premiums charged within the affordability range of their target customers. For instance, if microinsurers charge too low a premium, they may not be able to honor the claims of policy holders, leading to bankruptcy. On the other hand, if they charge too high a premium, they may not have enough customers, leading to a narrow risk pool that is not viable.

Such pressures could result in microinsurers either offering lower coverage or charging higher premiums and thus moving them away from their social mission. The cost/benefits of microinsurance should not be so disproportionate that policyholders would be better off self-insuring. Such a choice would be detrimental to needy customers in BOP markets. Hence, the importance of microinsurance on the welfare and social well-being of the lower segments of the markets is broadly recognized and has been validated in many low-income economies. While extant research has investigated the performance of microinsurers using data envelopment analysis (Biener and Eling, 2011) or beneficial aspects of microinsurance (Hochrainer-Stigler et al., 2012), little is known as to how closely these microinsurers stick with their social mission. Such a drift from the core mission is worth investigating, as this phenomenon is not limited to the microinsurance sector alone but to all kinds of social enterprises (Cornforth, 2014). The study attempts to address this knowledge gap by seeking to understand under what circumstances microinsurance providers deviate from their social mission orientation. Based on earlier work on mission drift (Cornforth, 2014), this study integrates two theoretical perspectives, namely, resource dependency and institutional theory, to hypothesize factors driving the social mission of microinsurance providers.

Such a study will help leaders of social enterprises to understand the factors driving mission drift and plan for managing such enterprises more effectively. This information is also critical for donors and public policy purposes, as it offers valuable insights into how best to support these social enterprises. This study is divided into five parts inclusive of this introductory section. In the next section, the theoretical framing of the article is presented and the hypotheses are developed. The third section presents the methodology, while the fourth section presents the results. The final section concludes by discussing the findings and drawing implication for managers of social enterprises.

Conceptual foundations

Microinsurers are social enterprises that are hybrid in nature, as they seek to achieve social purposes through business activity. Such organizations have a social mission (akin to nonprofits); yet they need to operate successfully as businesses in the marketplace (Cornforth, 2014). Such organizations experience conflict, as they need to meet competing logics (Evers, 2005; Gidron, and Hasenfeld, 2012). Such conflicts could result in instability, as too much emphasis on business rationales could lead to mission drift, while too much emphasis on social goals could end in bankruptcy (Young et al., 2012).

One of the papers that has addressed this inherent conflict conceptually is Cornforth (2014), in which it is explained that the dual pressures such enterprises face can be visualized using resource dependency theory and institutional theory. Resource dependency theory highlights the fact that organizations are dependent on other actors in the environment who control key resources needed by the organization (Pfeffer and Salancik, 1978). Institutional theory stresses that organizations in an environment face pressures to adapt to the local norms by conforming to them (DiMaggio and Powell, 1991). In both perspectives, the extent of choices is limited by the external environment, requiring organizations to respond and meet multiple expectations to survive (Oliver, 1991).

Applying Cornforth’s conceptualization to microinsurers, it is possible to visualize the conflicting expectations they face, namely profit making and trying to do good (i.e. serve the poor). On the one hand, based on the resource dependence perspective, it is quite possible to visualize pressures exerted by donors on microinsurers. On the other hand, institutional forces may require a microinsurer to adapt to local conditions of BOP markets. While these two forces may not be consistent with one another, microinsurers still need to accommodate both of them to ensure survival in these environments. Therefore, in the following section, three hypotheses are developed to test for the influence of these forces. The first hypothesis focuses on donors using a resource dependence rationalization, the second focuses on institutional environments using institution-based rationalizations, and the third focuses on the confluence of both factors. The relationships that will be tested are shown in Figure 1.

Research model showing the relationships tested.

Resource dependence perspective

Microinsurance providers are dependent on donors for resources, and in many cases, donors not only provide financial capital but also may be involved in operations. These donors are not-for-profit entities, non-governmental organizations (NGOs), foundations of for-profit firms, or mutual or cooperative organizations. Donations from such donors typically serve as original seed capital to start and sustain operations. Moreover, donations may be the only way that microinsurers can serve markets that are not profitable. Donor support or participation will be contingent on the degree to which a microinsurer focuses on the social mission orientation of microinsurance. Therefore, based on rationalizations of the resource dependence perspective, involvement of the donor will lead to a greater focus on social outcomes in a mutually reinforcing manner. First, donors are likely to support initiatives which are targeted toward the goal of helping the lower end of the market in a cost-effective manner. Donors can help a microinsurer in many ways. For instance, donations can potentially be used for setting up operations and toward the cost of operations (e.g. distribution channels). Additionally, they can enhance social mission orientation by subsidizing losses under specific contingencies or underwrite certain expenses incurred by the microinsurer. Second, the microinsurance provider will be less likely to vary its social mission (i.e. mission drift) in the presence of donations, as such choices can have negative implications, leading the donor to stop supporting the organization. Additionally, in circumstances where the donor may have expertise in the insurance value chain, the donor can serve as a resource to enhance the overall effectiveness of the organization, as management capacity is a critical factor in the success of the microinsurance provider (McCord and Osinde, 2005). Finally, the backing of the donor may also increase the confidence of the microinsurer to price policies in line with the social mission without undue fear of liquidity risk or failure. Most importantly, donations become a critical resource in the event of major catastrophes, as most microinsurers with lower capital requirements would be stretched thin to make their commitments to the policy holders. Therefore, given the resource criticality of donors in microinsurance, both initially and later in times of need, using rationalizations of resource dependency theory (Pfeffer and Salancik, 1978), it is proposed that

Institutional theory perspective

Institutional theorists (e.g. North, 1990) have identified numerous functions of the state, such as property rights protection, third-party contract enforcement, policy stability, and the provision of a general rule of law, that influence the risks and opportunities for businesses in different countries. Researchers testing these assertions empirically have found that institutional factors affect business operations in BOP markets (Elango and Lahiri, 2014). Among institutional variables, a measure that is most relevant in the context of this study is state fragility. State fragility was chosen primarily due to its strong showing in prior research in institutional contexts of countries similar to the study sample as a moderating influence in impacting microfinance lending social outcomes (Ault and Spicer, 2014). A fragile state has been defined as a state that “has weak capacity to carry out basic governance functions, and lacks the ability to develop mutually constructive relations with society” (OECD, 2013:15). Measures of state fragility have been used extensively in studies of international development to distinguish the world’s least developed countries (e.g. Somalia and Sudan), not only from more developed countries but also from developing countries that seem to be advancing much more rapidly, such as the BRIC countries (Brazil, Russia, India, and China).

It has been widely known that the impact of international aid on poverty reduction would be greater in fragile states. However, aid agencies have found that, even after controlling for the level of poverty within a country, high levels of state fragility have a negative effect on improvements to the living conditions of the poor as a result of aid (Baliamoune-Lutz and McGillivray, 2011). Therefore, the effectiveness of aid programs appears to be dependent not only on the level of demand for aid but also on the capacity of the state to provide an environment for that aid to achieve its aims (Ault and Spicer, 2014; Collier, 2007). Based on the above reasoning, it seems that, while microinsurance has the potential to grow most extensively in those countries where there are large numbers of poor people who need small loans, the ability of microinsurance providers to address that need is likely to be tempered by the fragility of the state. In many studies of economic development, the state plays a powerful role in providing the institutional environment that facilitates economic activity. In more fragile states, the lack of institutional support limits the ability of businesses to carry out regular operations due to a lack of stability and consistency in the environment. In the case of microinsurers, this means charging higher premiums or reducing coverage to compensate for the inherent risk in operations. Therefore, it is proposed:

Moderating relationship

In this section, the joint influence of donor involvement and state fragility on the social mission orientation of microinsurers is presented. Using a resource dependence perspective, hypothesis 1 called for a positive relationship of donor involvement with social mission orientation, while hypothesis 2 called for a negative relationship of state fragility with social mission orientation, based on the institutional perspective. While both forces impact outcomes on microinsurers, albeit in different directions, they operate at different levels of the environment, namely, task environment and general environment. Task environment refers to particular elements with which the organization interacts directly to achieve its goals, while general environment represents elements that indirectly impact outcomes for an organization (Daft, 2006). The external pressure imposed by the resource dependence perspective is related to the task environment, whereas the external pressure imposed by the institutional environment is related to the general environment (Oliver, 1991). Typically, the general environment may not have a direct influence on the day-to-day operations of a firm, but it will have an indirect influence on the outcome (Daft, 2006). Therefore, in more fragile states, while donor support will help microinsurers remain oriented to their social mission, its effectiveness could be reduced due to the constraints in the institutional environment. Therefore, the following moderating relationship is proposed:

Methodology

In this section, the following are elaborated: study context, sample information, operationalization of variables, and the statistical technique employed.

Study context

Microinsurance refers to a risk-pooling product specifically intended for low-income segments of markets (McCord, 2012). Stated differently, it is insurance that targets individuals with a meager income. Microinsurance seeks to give coverage with low premiums to low-income families. Premiums can range from amounts that are less than a dollar to more than a couple of dollars (Afonso and Sepulveda, 2010). These products serve as a safety net to a certain extent by preventing individuals from falling into deeper poverty.

Insurance services are available to the well-off segments in most parts of the world, enabling them to manage risks. Prior to the availability of microinsurance, the poor typically had to face catastrophic risks on their own, with a few exceptions where social welfare programs offered some backup. Sadly, the poor not only face these risks with greater frequency, due to the nature of their livelihood in high-risk tasks and neighborhoods, but they also have fewer means to cope with such exposures (Afonso and Sepulveda, 2010). In recent decades, microinsurance has grown in many parts of the world, serving the BOP markets (Brau et al., 2011). Microinsurance has served to decrease asset inequality among households and, overall, minimizes the impact of calamitous events (Akotey and Adjasi, 2015).

To a certain extent, microinsurance is taking root and seems to show much promise in many markets around the world (Chmielewski et al., 2015). Although microinsurance is growing in many parts of the world, it has been pointed out that only about 3% of the world’s poor have access to some kind of insurance product, even though there is demand for such products from this demographic class (Churchill, 2002; Cohen et al., 2005). More recently, there has been an improvement in these figures, giving reason for much hope. For instance, it is estimated that about 5.4% of the population is covered in Africa and about 7.8% in Latin America. A recent survey shows microinsurance premiums in Africa total US$ 756 million, representing about 1.1% of the insurance industry premium of US$ 6.9 billion (Biese et al., 2016). It is widely believed that this growth trend will continue given the latent demand and need for such services in poverty alleviation.

In the context of microinsurance, within each country three major groups of players exist. The first group consists of microinsurance providers themselves. While the underlying market impetus of these microinsurers are similar, the capitalization of these microinsurers is quite varied and varies by country. Examples include independent firms that focus exclusively on microinsurance, quasigovernmental organizations, cooperatives, microfinance institutions seeking to help reduce their lending risks, traditional insurers wanting to extent their business into lower income individuals, and so on. The second group consists of the donor organizations, which is made up of varied NGOs, aid organizations, private foundations, and/or public companies, who see the beneficial effects of microinsurance and encourage the creation of such organizations through material and nonmaterial support. The third group consists of the institutional regulators who supervise the insurance industry. Microinsurers are typically given special regulatory “sandboxes” allowing them much leeway to innovate to permit the development of this product that is aimed at helping the lower income who traditionally do not have access to insurance. While microinsurers have regulatory oversight, given the evolutionary stage of microinsurance, they are lightly supervised. Therefore, in this article, the focus is on the first two groups, namely microinsurance providers and donors.

Sample

This study is based on a sample of microinsurers, taken from data collected by the MicroInsurance Centre. The MicroInsurance Centre is a highly reputable organization specializing in microinsurance, and its data collection efforts have been recognized or funded by organizations such as the African Development Bank, MicroInsurance Network, Federal Ministry of Economic Cooperation and Development of Germany (BMZ), MunichRe Foundation, World Bank, and so on. The following steps are undertaken by The MicroInsurance Centre in the data collection process in all countries across Latin America and the Caribbean and Africa. In the first step, using local representatives, it identifies all providers of microinsurance within the respective countries, using regulatory and industry list of insurers. Given the emerging nature of the microinsurance industry, effort is taken to ensure every microinsurer is included in the survey. Second, it has a team of researchers who contact microinsurers regularly to request them to participate in the questionnaire survey. To maintain integrity, confidentiality of names/companies is promised to the respondents. While the primary means of data collection is through a survey, it is supplemented with phone interviews as needed. Third, once the data are collected, the MicroInsurance Centre also cross-checks the data collected with other sources (e.g. industry experts, regulators, distribution channels, previous surveys) using techniques such as trend extrapolation to ensure integrity in the data (McCord et al., 2013). The data collected are considered both comprehensive and reliable by industry peers and their Landscape of MicroInsurance series is considered to be one of the unique sources of data on microinsurance on countries around the world. The data used are proprietary to the MicroInsurance Centre, and the investigators of this study were allowed access to use it for the specific study variables after signing confidentiality agreements. Additional information on the MicroInsurance Centre can be gained from http://www.microinsurancecentre.org/.

This study’s sample consists of 192 microinsurers operating across 26 emerging countries (Benin, Burkina Faso, Cameroon, Comoros, Cote d’Ivoire, Dem. Rep. Congo, Egypt, Ethiopia, Ghana, Kenya, Madagascar, Mali, Mauritius, Namibia, Nigeria, Rwanda, Senegal, Sierra Leone, South Africa, Sudan, Swaziland, Tanzania, Gambia, Togo, Uganda, Zambia) during the years 2009–2011, after elimination of firms with missing values along with extreme outliers. The type of microinsurance providers in this study sample includes accident (9: 4.66%), agriculture (16: 8.29%), credit life (55: 28.50%), Health (41: 21.24%), life (50: 25.91%), property (9: 4.66%), and unknown (13: 6.74%). Table 1 indicates that, on average, these countries’ per-capita incomes were less than 4000 LCUs, had more than three incidents of political violence, had an average unemployment of 9%, and were relatively fragile states. The sample of microinsurers had an average loss ratio of 0.460 and about 61% of them sold group policies or tied policies. On average, these microinsurers carried between one to two products and deployed technology in five or more of the value activities within their firm. Donors are involved with about 33% of the microinsurers and close to 37% of the microinsurers used reinsurance in their operations.

Means, standard deviation, and data sources.

LCU: local currency unit.

Variable operationalization

Dependent variable

The dependent variable for this study is social mission orientation. The key social mission of microinsurers is to offer insurance services that provide adequate coverage at low levels of premiums that the poor can afford (Churchill, 2006; Hulme, 2000). While for-profit insurers could offer similar products, they would need to charge a high premium to cover the same risk. Therefore, social mission orientation of microinsurers is measured by the ratio of total sum insured relative to the premium charged. Operationally, the total value insured is divided by the premium charged (both values measured in local currency) to empirically measure coverage value. As this formula uses the same currency in both denominator and numerator, this measure allows for comparison across countries. For instance, in case A, if a customer can get coverage for assets worth 100 units of local currency after payment of 10 units of local currency, then the coverage value would be 10 (i.e. 100/10). In case B, if a customer can get coverage for assets worth 100 units of local currency after payment of 5 units of local currency, then the coverage value would be 20 (i.e. 100/5), indicative of case B’s higher coverage per unit of cost compared to case A.

Independent variables

This study uses two independent variables: donor involvement and state fragility. Donor involvement is measured based on the response to the question, “Please indicate the involvement of donors in the development, redesign or upscale of this product.” If the respondent chose “no donor involvement,” they were coded zero, and 1 otherwise. To measure state fragility, a multidimensional measure, the State Fragility Index (Cole and Marshall, 2014), published by the Center for Systemic Peace, is used. This is referred to as the degree to which a state power is unable/unwilling to fulfill obligations to the majority of the people and is a variable that has been shown to be related to the efficacy of social outcomes in microfinance and social entrepreneurship (Ault and Spicer, 2014).

Control variables

This study uses five control variables at the country level and seven control variables at the firm level, based on prior research in the insurance sector of emerging markets (Elango and Jones, 2011). At the country level, country wealth differences are controlled for by factoring gross domestic income per capita in constant local currency units (LCUs). To control for sporadic episodes of violence (incidents of political violence: civil wars, coups, political turmoil, etc.) prevalent in emerging markets, which could cause disruptions to the stability of business operations, the Polity IV database measure is used (Marshall et al., 2015). Additionally, the economic size of a country needs to be controlled for, as the size of a nation impacts the potential opportunities available to firms. As such, country size is measured as gross domestic product at market prices (current US$) to control for size-based differences (Elango, 2003). To capture the influence of foreign competition in the finance and insurance sector (Khandker et al., 2013), the percentage (%) of imports of commercial insurance and financial services is incorporated as a control. This study also controls for population density, which is likely to constrain opportunities and cost of operations to microinsurers, and this is measured as people per square kilometer of land area.

At the firm level, the amount of loss suffered by microinsurers would vary by the market they operate in, and therefore is accounted for using the loss ratio. This variable is operationalized using conventional practice, wherein the loss ratio is measured by the claims paid by a company divided by the premium collected. Microinsurers who have a larger number of products will be able to have higher economies of scale and scope and therefore this study controls for number of microinsurance products using the simple number count of microinsurance products sold. Many microinsurance products are tied to another product and need to be factored in the model tested. For instance, one of the conditions of a microfinance loan could require the purchase of microinsurance by the loan provider. This study controls for this using the variable tied product. When the microinsurance policy sold was linked with some other product, it was coded 1, zero otherwise. In many instances, microinsurance policies are sold to consumer groups collectively. These policies need to be differentiated from those sold to individuals. Therefore, this study coded the variable group policy 1 when a policy is targeted to a group, zero otherwise.

The extent of technology utilized can be used to control operating expenses; therefore, this study controls for technology deployment. Technology deployment is measured by adding the number of times the respondent answered positively to the question, “Please indicate the use of technology for the following insurance processes: Product Development; Marketing; Sales; Premium Collection; Claims Payment; Customer Service; Policy Management; and Data Transfer with Partners.” For this measure, the score a microinsurer could receive will be in the range from 0 to 8. Microinsurers can either use microinsurance specific distribution or use common distribution channels and this therefore needs to be controlled for. Distribution channel is measured as a dummy variable, wherein if the respondent claimed to have “Differentiated distribution channels for microinsurance products,” they were coded 1, zero otherwise. Finally, microinsurers can mitigate risk by transferring portions of their risk portfolios to other third parties by purchasing reinsurance. As a control, Reinsurance usage was coded based on the response to the question, “Is this Product Reinsured?” If the response was positive, this study coded this variable as 1, zero otherwise. All firm-level data are based on data from the MicroInsurance Centre, while country-level information, unless noted specifically earlier, came from the World Bank. Table 1 provides the means and standard errors of the variables along with the data sources.

Methodology

Given the hierarchical nature of the data, wherein microinsurers were nested within countries and countries within years, multilevel models were used to test the hypotheses. In these models, the whole sample effect (i.e. fixed) of the independent and control variables listed above is tested, with random intercepts and slopes for the effect of each calendar year, which could vary from one country to the next. Such models are appropriate, as they account for within-group dependencies that need to be factored in due to the nested structure of the data for the varied country-effects across the years studied. This allows for valid inferences given the sample distribution across countries and time periods. The next section presents the study results.

Results of this study

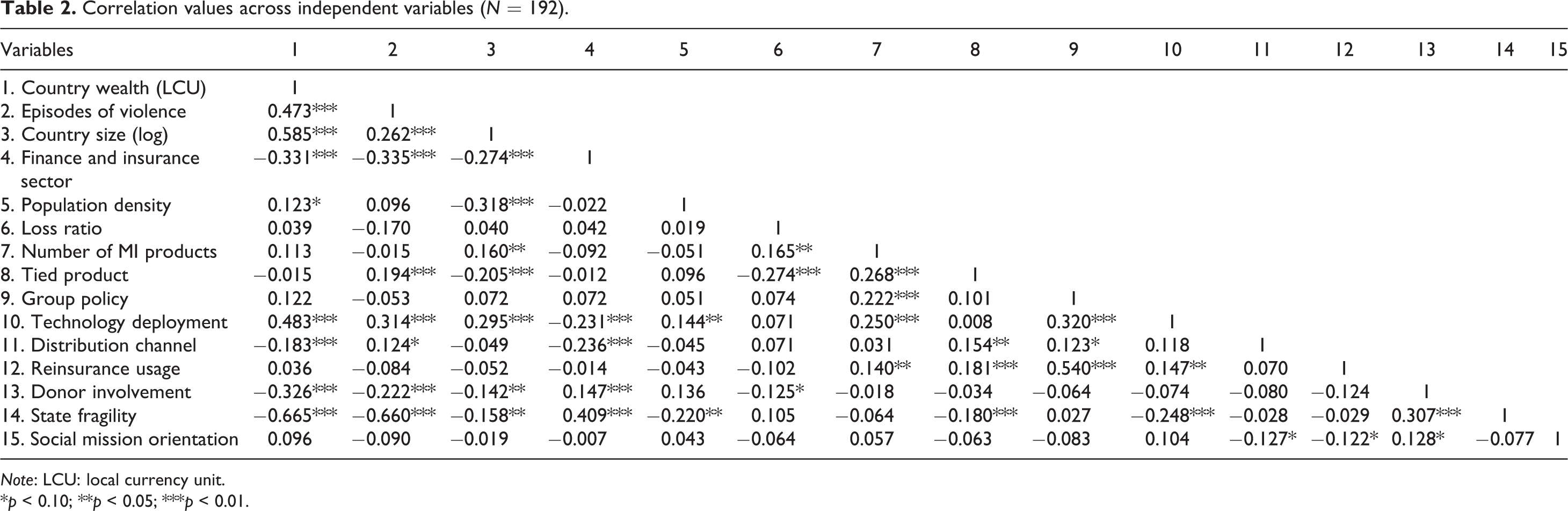

Table 2 reports the correlation coefficients of the variables. A review of the correlation values indicated several of them to be high, even though all of them were below the conventional threshold of 0.7. The first high correlation was between state fragility and country wealth (β = −0.665; p < 0.01). The second high correlation was between state fragility and episodes of violence (β = −0.660; p < 0.01). Conceptually, one would expect this to be the case, as more fragile states would have more incidents of violence and be economically less well off. Additionally, country wealth and country size and country wealth and episodes of violence were correlated (β = 0.585 and 0.473, respectively; p < 0.01). Given these issues, several additional models for robustness checks are employed in this study, using conventional research procedures. Table 3 which presents the results of the paper.

Correlation values across independent variables (N = 192).

Note: LCU: local currency unit.

*p < 0.10; **p < 0.05; ***p < 0.01.

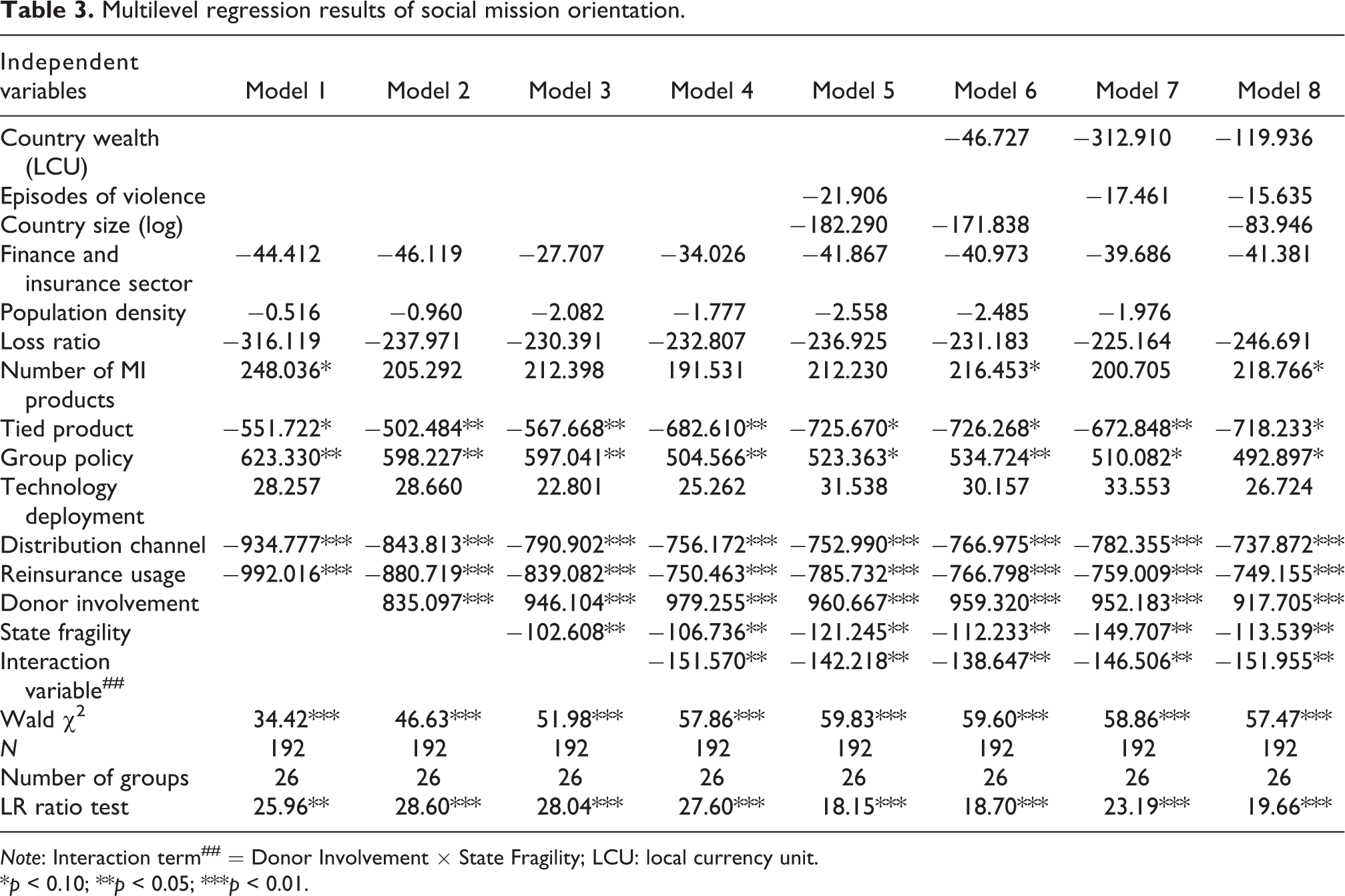

Multilevel regression results of social mission orientation.

Note: Interaction term## = Donor Involvement × State Fragility; LCU: local currency unit.

*p < 0.10; **p < 0.05; ***p < 0.01.

Model 1 is the base model with the control variables alone, whereas models 2 and 3 add variables related to hypotheses 1 and 2 in a stepwise manner. Model 4 adds the interaction term between donor involvement and state fragility to model 3. Models 5–8 are used for robustness testing and the relationships pertaining to the hypotheses were stable across models 4–8. Chi-square results (as well as LR ratio tests) indicated that all models are statistically valid. As model 4 includes all the hypothesized parameters and control variables, it is used to make inferences regarding the hypotheses. In brief, this study proposed three hypotheses, all of which were supported. Hypothesis 1 proposed that donor involvement would be positively related to social mission orientation, which was supported with a positive loading of 979.2 (p < 0.01). Hypothesis 2 argued that state fragility would be negatively related to social mission orientation. This hypothesis was supported, indicating that microinsurers in countries that are fragile tend to have less social mission orientation (β = −106.7; p < 0.01).

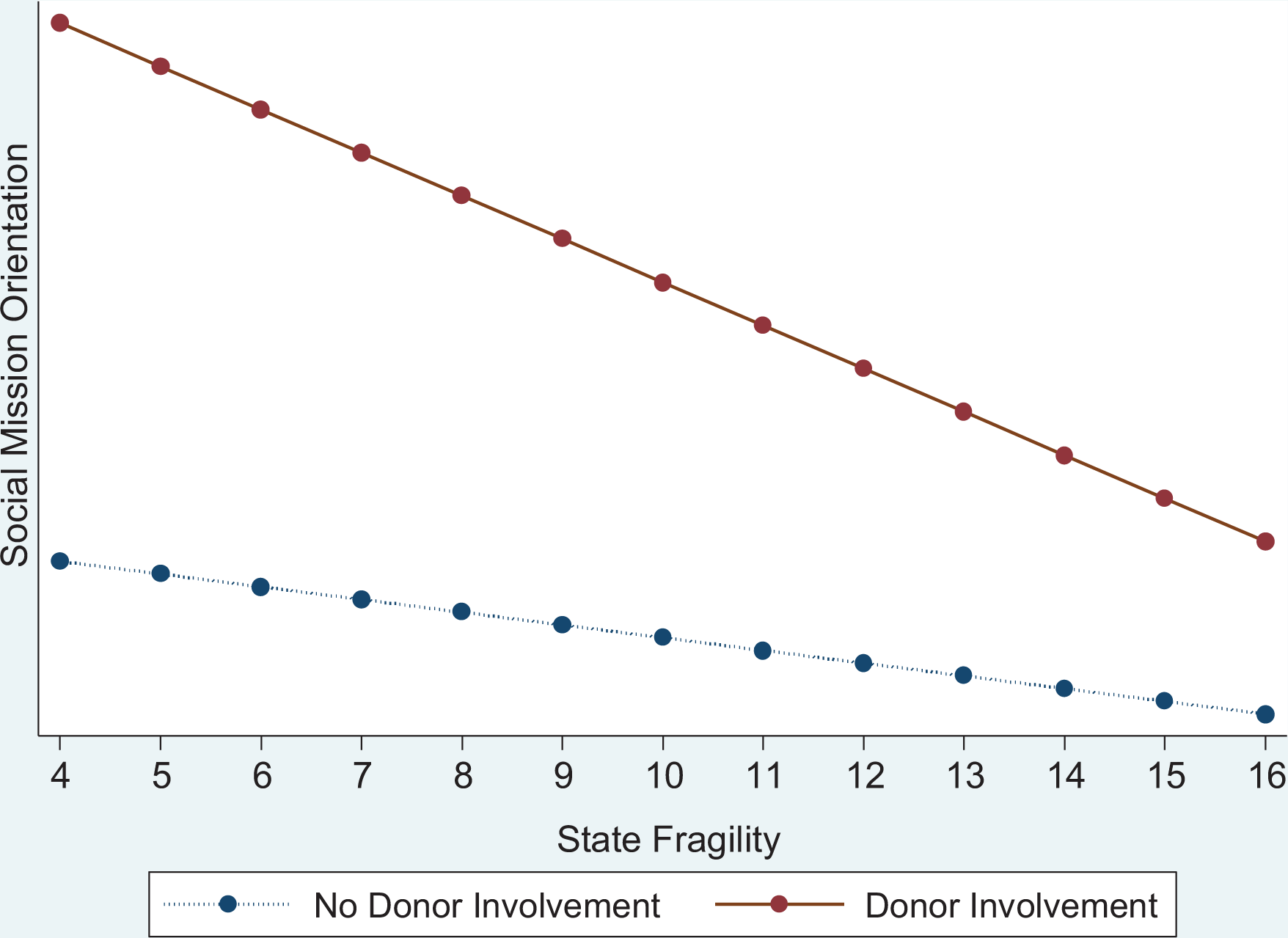

Model 3 adds an interactive term to model 2, namely, the interaction of donor involvement with state fragility. Consistent with hypothesis 3, the interaction term was negatively related to social mission orientation (β = −0.151.6; p < 0.05) and the results suggest that country-level variables impact social mission orientation outcomes at the firm level. This relationship is graphically illustrated in Figure 2, which shows the interaction between donor involvement and state fragility on social mission orientation. While it seems that donor involvement leads to improved social mission orientation, irrespective of state fragility, increasing state fragility decreases the effect of donor involvement.

Moderating effect of state fragility on donor involvement and social mission orientation.

Among the firm-level control variables, tied products was negatively related to social mission orientation (β = −682.6; p < 0.05). In instances when there was a tied product, it seems that customers do receive policies of lower value. Group policies lead to greater social mission orientation, indicative of the benefits of collective choice of microinsurance (β = 504.6; p < 0.05). The usage of an exclusive distribution channel for microinsurance or the usage of reinsurance were both negatively related to social mission orientation (β = −756.1 and 750.5, respectively; p < 0.01), indicative of the costs incurred by the microinsurers. The number of microinsurance products were significant in two of the models, preventing particular claims on the importance of this variable.

Robustness tests

Models 5–8 check for the robustness of the study findings by deploying varied models, as there were pairings of the country variables that were highly correlated. Model 5 adds country size and episodes of violence to model 4. Model 6 drops episodes of violence and adds country wealth to model 5. Model 7 drops country size from model 6 and adds episodes of violence, whereas model 8 drops population density and adds country size to model 7. Despite the change in the mix of variables in models 5–8, the findings were very similar for the variables of interest relative to what was found in model 4, giving great confidence in the stability of the findings reported. Next, the limitations of this study are presented.

Limitations

This study has several limitations that are highlighted here. First, while this study used one of the best sources of firm level data on microinsurers, the data collected do not necessarily capture all the microinsurers or characteristics of microinsurers in the countries studied. It is limited to firms which responded to the MicroInsurance Centre survey on the specific questions of interest to this study. Second, the study relies on data from multiple countries that are characterized by a great degree of variation. While it uses several known control variables to incorporate such differences, no study can capture all potential nuances across multiple nations. Therefore, readers are urged to factor in this study’s underlying boundary conditions while interpreting its findings. This study calls for future research to replicate these findings in varied single country settings to allow for more detail and fineness in measures, as well as the usage of different time frames and larger samples segregated by product lines. In the next section, the key implications of this study’s findings for research and leaders of social enterprises are presented.

Study implications

This study’s major goal was to understand the drivers of the social mission orientation of social enterprises, using one of the most comprehensive datasets of microinsurers from emerging markets. It conceptualized two opposing forces which these firms face based on two theoretical drivers, namely, resource dependence and institutional factors. This study makes the following three conceptual contributions. First, findings highlight the need to understand the impact of these dual forces on the social mission orientation of social enterprises. Second, it highlights the inherent conflicting nature of these forces that pull the organization in different directions. Finally, this study validates the need to incorporate both of these theoretical perspectives in BOP market contexts. While there is a variation in the assumption of the extent of free choice between the resource dependence and institutional perspectives, both of them do concur that organizations face multiple pressures, and survival depends on the response to external demands. Recognition of these dual forces could be a good starting point for all stakeholders involved in decision-making in these social enterprises. In such situations, Pfeffer and Salancik (1978) suggest managers use social coordination/linkages to generate desirable behavior. They highlight that such linkages provide managerial benefits such as information exchange for all parties involved, serve as channel for leverage, and provide legitimization of the organization. Therefore, in the following paragraphs, several suggestions for leaders of social enterprises are presented for each of these forces, using examples from the microinsurance sector.

Managerial implications

This study’s findings indicate that organizations having greater donor involvement tend to be more committed to their social mission orientation. This creates an interesting dilemma for donors, as on the one hand, they would prefer their funded organizations’ operations to become self-sustaining, thereby allowing them to shift their resources to other valuable causes. On the other hand, our research indicates that it might be worthwhile for donors to stay engaged for a longer time, encouraging and building the ability of such organizations to remain committed to their social mission. During this period, such donors may choose to reduce their commitment in a phased manner, while not severing their linkages. For instance, donors serving on the board have a greater ability to influence microinsurers in staying close to their social mission. For microinsurers, even when the donor is no longer supporting it finally, having donor involvement in its board of directors could serve as badge of legitimacy in their dealing with external stakeholders, while also serving as a link with a provider of critical resources.

However, we also find that the efficacy of donor involvement is weaker in more fragile states, although sadly, these are the countries where the need for microinsurance services is greatest. We offer three suggestions for managers of social enterprises in these countries. The first is that in countries where the state is fragile, microinsurance operators should promote group policy offerings and make greater use of technology. Our results show that these factors have a large and significant positive effect on social mission despite state fragility. The usage of group policies and technology can potentially serve the microinsurer by reducing the costs of administration and monitoring, as well as the overall risk due to collective monitoring by group members.

Our second suggestion is to attempt to deal with the fragile environment by making greater use of external partners. While the ability of any organization to change such an environment is rather limited, microinsurers may be able to co-opt local players and stakeholders to generate social support for microinsurance, through extensive information sharing in the community and by building connections highlighting the positive social role played by such organizations. In our sample, we found microinsurers co-opt local organizations and stakeholders that have a social orientation such as microfinance institutions, community-based organizations (CBOs), cooperatives, and savings and credit cooperative organizations (SACCOs). These organizations, with a social mission, play a role in the marketing, distribution, consumer education, and even indemnification of policyholders of microinsurance. In such volatile environments when there are rapid changes, local stakeholder support could minimize potential risks as well as provide timely information, allowing such organizations to focus more on their social missions.

Finally, to increase survival in hostile environments, microinsurers must quickly increase the pool of independent risks (policyholders) to achieve a viable level of diversification and income (Cohen et al., 2005). One way to achieve this is to offer their product with an existing fast-growing product such as mobile phone service in the BOP markets. Some microinsurance organizations such as BIMA (http://bimamobile.com) and ACRE (http://acreafrica.com/) partner with mobile phone services, allowing phone customers to get insurance by exchanging minutes for insurance premiums. They also are able to administer claims service and make payments via mobile phones, allowing microinsurers to capitalize on the phone company’s technology infrastructure and distribution system. The underlying logic here is that quicker growth could lead to coverage for a larger number of customers across market segments, allowing for a greater diffusion of risk. This diffusion of risk could reduce the chances of sudden claims bankrupting the microinsurer, potentially enabling a virtuous cycle wherein the microinsurer can hold rates low while also ensuring survivability.

Conclusion

In closing, our study offers initial insights toward a sustainable model of social enterprise in BOP markets. In these markets, where there is a latent demand for products/services, in order to ensure sustainability, it is important to offer such services at a price point which is adequate to cover costs and risks yet is of value to the user, allowing demand growth and permitting the firm to scale up quickly. To enable this price point, the model requires a simple product that will allow users to understand the benefits offered and be able to use them effectively. Examples include firms such as Tigo Family Insurance in Ghana (https://www.tigo.com.gh/), who have come up with products that sell for about 3–4 U.S. cents and can be purchased using low-end cell phones.

Many social enterprises operate in an environment fraught with political challenges, poor infrastructure, lower quality institutions, and populations with marginal purchasing power. Despite these many constraints, these organizations have taken the challenge of operating in these bottom of segment markets to provide critical services to an important segment of the population. Our study highlights the paradox faced by these social enterprises in dealing with the two major forces in fulfilling their social missions, in addition to offering some possible solutions to the challenges.

Footnotes

Acknowledgements

The authors thank the MicroInsurance Centre for sharing the data used in this project. In particular, the authors thank Michael J. McCord for his encouragement with this project, Dawn White for exceptional office support, and Katie Biese in educating us on the usage of variables. The authors also acknowledge the extensive efforts of Ama Ampadu-Kissi in the preparation of this dataset for this study. The authors thank Chris Anderson, Adem Firinci, and Bastian Braukmann for their research support.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful to the Katie School of Insurance and Financial Services and the Hinderliter Endowed Professorship for their support. All opinions expressed are of the authors alone. All other disclaimers apply.