Abstract

In the recent years, the Portuguese Real Estate Market has been increasing exponentially. This growth, has generated, in the real estate companies, the need to implement effective project management tools and frameworks in order to provide important metrics of budget control, deadlines and increase risk management. This study aims to understand the different causes of risks in real estate projects and to measure the risk factors that provoke deviations, in terms of cost, time and quality in the real estate market in Portugal. To measure these risk factors, a new methodology has been implemented, namely a new real estate risk plan model for predicting the risks inherent to new construction projects. This methodology aims to produce new and more accurate strategies and plans so as to effectively respond to potential risks and thus achieve the proposed objectives through the desired success. This methodology allows companies to effectively implement a project in a timely manner in order to reduce and mitigate the probability of risk failure based on risk management tools and techniques. The results of this case study have shown that implementing a risk management project is crucial to highlight and measure the risk of project failures and that Companies must implement risk indicators or triggers that give visibility to potential risks/losses that impact company objectives and, on the other hand, establish metrics that translate the organization’s appetite and tolerance into critical risks.

Introduction

The increasing boom in real estate market in Portugal during the years 2017 and 2018 led to an increasing market demand both domestic and foreign, and due to the crisis in the construction industry in recent years, we are with a deficit of new construction. To cope with this increased demand and for prices not to become speculative (given the lack of supply, which translates into a shortage of product), it was urgent to increase the constructions to fulfil the incoming requests.

To satisfy customers and to be ahead of the competition, promoters must know how to handle good governance principles and chosen procedures (Gross and Źróbek, 2015) in order to accomplish all the customer’s needs and fulfil their constructions obligations. Unfortunately, real estate projects in Portugal still suffer from serious shortcomings and fail to become a product of excellence which could offer a system that builds interrelationships between three essential components of real estate management systems: legal, fiscal, and administrative components (Gross and Źróbek, 2015).

Throughout the years, management of real estate projects has been facing difficulties which led to systematic deviations from the initial project plan. One of the main axes impacted by these deviations is the cost. It is important to point out that an efficient cost management is one of the principle factors that can ensure sustainable development of the real estate business projects (Liu and Li, 2011) and that construction projects are exposed to risks at the time of their coming into existence (Schieg, 2006). Thus, cost is effectively one of the main elements that should be carefully planned in terms of real estate project management. Besides the variable cost, there are other factors that provoke unsuccessful management of estate projects such as overdue deadlines, budget overruns, security failures and poor quality. These shortcomings are usually attributed to the economic situation, the phased development of projects, the low-skilled workforce, the need to use external suppliers and even the weather conditions. To become more competitive, residential real estate projects need to focus on efficient and effective risk management through the implementation of a consistent project management strategy which addresses, throughout its development life cycle, the four principles: cost, time, quality and safety (Khandekar et al., 2017).

The main objectives of a real estate project should consist in the delivery of the housing fractions within the expected time, without deviations from the budget and with the desired quality. This will only be achievable with the correct use of risk management processes which is often neglected in this industry. It is important to highlight that the risks taken by a property developer are different from the risks taken by a consultant or a contractor in a different field as mentioned by Gehner et al. (2006). It is also important to understand the risk and which are the main causes of risk in real estate market. Thus, it is needed to be clear, which type of risk management strategy should be implemented in this market based in which are the main causes of risk in residential real estate projects. For instance, a poor organization is linked with project failure, incorrect definition of project scope, lack of risk identification, lack of planning and monitoring failures and control (Khumpaisal et al., 2012).

To overcome these risk analysis differences and how they impact the real estate management, Gehner (2003) proposed a risk analysis framework exclusively adjusted to the real estate development process in order to mitigate the existing risks. Also, Morrison (2007) proposed and implemented an acronym called Social, Technological, Economic, Environmental and Political, which identify the main causes of risk in real estate development and how they impact the real estate management projects. Nevertheless, this assumption of risk management in real estate projects is often limited (Pyhrr et al., 1999; Whipple, 1988); it should be established as an essential part of project management in architect’s and engineer’s offices (Schieg, 2006) in order to guarantee a comprehensive and successful risk management. It is very important that property developers further strengthen their risk management controls to maintain their discipline and to execute projects successfully (Newell and Steglick, 2006). Some of the risks in the real estate market, according to Khumpaisal (2011), are project schedule delays, cost overrun and reduced project quality.

Since the concept of risk is different in the real estate market, as mentioned by several authors, there is the current need to understand which are the main causes of risk in residential real estate projects and if companies are successfully adopting risk management tools. To understand what types of risks are involved in a real estate development process and how strategic decisions regarding the development process affect the risk profile of a project (Gehner and Peek, 2008), it is fundamental to determine the main causes of it (Khumpaisal, 2011).

This study attempts to answer two research questions:

These research questions, outlined above, will lead to the presentation of a proposal for the prevention of risk, inherent in a real estate project, increasing this way the probability of achieving the established objectives.

After diagnosing the causes of failure in the real estate projects in Portugal, it is hoped to be able to contribute to the minimization of the risks associated to the activity under study and to the maximization of the opportunities, unexplored until the moment.

Theory and hypothesis development

A comprehensive literature research has been made in order to identify the potential risks in the real estate and how it answers and argues the research questions. There are several authors such as Schieg (2006) and Newell and Steglick (2006) who have mentioned the concept of risk management in the real estate industry. Despite these authors touching on real estate market risk, Gehner and Peek (2008) affirm that there is a considerable gap regarding risk in real estate market, having conducted an exhaustive overview of risks in real estate development. Another existing gap in the literature lies between the operational management of risks and the management of risks on portfolio level of a project-driven real estate development company (Gehner and Peek, 2008) where there isn’t any evidence of such risk management. This article aims, as mentioned previously, to explore such gaps in the literature. The following information pretends to provide balanced arguments for the research questions mentioned previously and emphasize the theoretical contribution to this field of study.

Project risk management

A project is a temporary effort undertaken to create a unique product, service or result. Projects and operations differ mainly in the sense that projects are temporary and exclusive while operations are continuous and repetitive (PMI, 2004). Each project is unique, although some have their similarities. Project management is defined as the aggregate planning, identification and preparation for project risks (Raz et al., 2002). The starting point for effective risk management in projects is a systematic examination of the participants’ roles, responsibilities and motivation (Van Scoy, 1992). Risk management techniques are not yet implicit in all organizations although project risk management should be part of the culture of organizations (Raz et al., 2002) and measured by the project success (Bowers and Khorakian, 2014).

Success factors and failure causes in real estate projects

Risk management has become an essential competence for construction companies. The importance of the concept of risk in the pre-construction phase is reflected in a large number of risk management strategies, namely with 32 specific strategies that were established by Newell and Steglick (2006) Real estate projects deal with a multiplicity of local and temporal unknown factors and that is one of the main causes for why risk management becomes critical in the real estate market. Real estate projects follow long-term economic/financial feasibility studies and therefore are subject to enormous uncertainty (Zimmermann and Eber, 2014). From the bundle of known risk factors, the real estate projects involve several of them mostly based in hypotheses that could be the inception phase to the closure phase, especially large projects that are complex and characterized by a series of uncertainties that can negatively influence the entire project (Boateng et al., 2015).

Risk management is a vital, continuous and iterative process. It allows the parties concerned to recognize the existence and impact of uncertainties and, therefore, to consider the appropriate strategy to mitigate its effects on the project. Due to complexity, large resource needs and long time horizons, large projects are faced with unique risks and tend to stretch available resources to the limit, sometimes causing project failure (Boateng et al., 2015). The project’s mission, management support, calendar planning, client consulting and acceptance, technical and personal aspects, monitoring, communication and feedback are defined as success factors. In other words, a poor organization, an incorrect definition of the project scope, an incorrect identification of risks, a lack of planning and failure to monitor and control are the main cause of project failure (Krane et al., 2010).

Several authors have studied and analysed the critical factors for delays in construction projects. Delays cause an inability to meet the schedule, which leads to increased costs, customer dissatisfaction and other inherent problems. The guarantee of the completed project within the agreed deadline has been considered as an important milestone for the success of the projects (Chua et al., 1999; Hwang et al., 2013). Beside these factors, a poorly qualified project manager, lack of coordination between teams and stakeholders, changes in scope during project execution, unavailability of materials and suppliers and, finally, the lack of capacity of the team to manage the project are also critical factors.

According to Hwang et al. (2013), a low-skilled project manager and lack of monitoring and control are two of the main causes of failure to meet construction completion deadlines (Chan and Kumaraswamy, 1997). A good planning and a competent project manager are two of the key determinants of project success in terms of budget, time and quality and are generally related to the good architectural performance and critical success factors of construction projects. According to Hwang et al. (2013) and Chan and Kumaraswamy (1997), the involvement of the project manager is crucial to the overall performance of the project, while the economic factors are directly linked to the project’s budgetary performance. In turn, as regards architectural works, the human factor, namely the choice of the contractor and suppliers, is crucial to the achievement of the proposed objectives. In conclusion, for the overall performance of a construction project, the most important critical success factors are the constructive elements, good planning, a qualified and competent project manager and a clear and realistic definition of the proposed objectives (Kog and Loh, 2012).

Methodology

The aim of the present work is to contribute to the increase of theoretical and practical knowledge about risk management in real estate projects, namely in Portugal since its use is somehow neglected and has not been properly explored or, at least, many companies still use very unprofessional means. This study has as main objective to investigate the real estate projects in Portugal, to understand the main risks faced by our promoters and/or owners and whether the risk management practices are already implemented in the majority of the companies in the sector.

In this way, a qualitative approach was chosen to assess and identify the main risks inherent to a real estate project, as well as the causes and impacts of these same risks and mitigation strategies.

The objectives of this research will be described, the population characterization will be carried out and an exposition of the methodologies and instruments used in the data collection will be made. Based on the results obtained, a proposal for a risk prevention plan for a residential real estate project will be elaborated based on the following goals: identification and registration of project risks; qualitative risk analysis; quantitative risk analysis; and risk management and response plan.

Sample

The sample selected for this study, although small in size containing only 20 people, has carefully taken into consideration the market segmentation in order to be compliant and representative of the market characteristics. Currently, the market is segmented in three different levels based on the number of employees. For instance, small and family-oriented (<50), medium-sized organizations (>50; <500) and big companies (>500). The respondents represent each level of segmentation, thus guaranteeing at least more than one representative of the market characteristics.

The profiles of the real estate sample enrolled in this process were Real Estate Developer, Civil Engineer, Project Manager, Business Owner and Real estate agent which represent the typical structure of the real estate market (Table 1). Although the sample is representative of the market segment, the fact that only considers 20 people is somehow limited and centred in one main geographical region. Thus, the results will illustrate the scenario in one region and will be extrapolated to different areas.

Sample.

Data collection method

For the data collection, 20 interviews were conducted to the target audience mentioned previously.

The area of intervention was mainly Lisbon, apart from three interviewees who reported projects, one in Porto and two in the centre region. From the total number of interviews, in terms of gender, only one respondent was female, all others were male.

A relevant parameter for the data characterization of the sample is the structure of the company to which the interviewees belong. Seven of the participants reported projects carried out by small and even family-oriented companies in the construction sector. These companies have a small structure and are not yet adopting project management tools, and more specifically, risk management. Four of the participants belong to medium-sized organizations, with some successfully completed projects that already are adopting some management techniques; the remaining interviewees rely on big companies where the risk management techniques have a more in-depth knowledge about the subject under study. These real estate development companies have been in the market for several years and they already have under their belt projects of reference which involved a considerable amount of cash flow.

To collect the data, individual interviews were conducted. The interview guide was created to serve as a basis for the present study, and the questions were elaborated based in open answers. The interview questionnaire was divided into three sections. The first one refers to the project framework and sociodemographic characteristics of the sample, the second concerns the problem and is composed of questions about project risks, causes and consequences. The third section is intended to suggest or present mitigation strategies, namely solutions for the prevention and correction, for the risks presented in real estate projects.

Results

Risks may affect a project’s vitality through income loss, increased time consumption resulting in project delays and reduced customer satisfaction with the quality of the product. Risks also affect the return of investment, which may vary or fluctuate despite the investor’s expectations. Additionally, longer investment periods result in greater opportunity costs with respect to other investments as well (Hjelmbrekke et al., 2015).

The starting point for this analysis includes the main risks that we may face at the time of a real estate project (Table 2).

Risk identification.

In the first question, the interviewees are asked to remember a certain project in which they were involved and mention the main risks (threats or opportunities) they had found.

The analysis of the presence of risk factors in projects is an important step to prevent damage in the performance. It is assumed that all projects have risks associated (Table 2). The risk factor with the highest index of presence in the interviews was the external risks (17), followed by the management risks (11), technical risks (9) and financial and economic risks (5).

According to Table 2, the risks with more impact for the projects are the external risks; these risks were reported by 17 respondents, and they are associated with suppliers, the real estate market and the government regulations. Depending on supply and demand, the market may prove to be a threat or an opportunity. In other words, the suppliers and the government regulations could be a risk factor as it may lead to deviations from the objectives of the project.

According to 11 respondents, management risks include deviations from the scope of the project, inadequate project conception and inadequate stakeholder’s management. Such situations affect the project and can result in impacts in cost, quality and schedule. Technical risks were referred by nine respondents. These risks are associated with construction issues, an inadequate design and unrealistic technical plans. These kinds of risks have an impact in the quality of the project. With, less relevance, respondents identified financial and economic risks, albeit in contradiction with the conclusions of several authors (Gehner et al., 2006; Khandekar et al., 2017).

The scale risk identification in Table 2 is in line with what Hjelmbrekke et al. (2015) has pointed out regarding risk identification. According to Hjelmbrekke et al. (2015), real estate activity, especially construction, has a great dependence on external suppliers, which generates significant uncertainties in the strategy and performance of the project. These uncertainties are attributed to poor project design, poorly implemented resources, poor communication and limited accountability in results.

Table 3 presents that there are several causes and sources of risk: about 40% of participants stated that the main sources of risk are suppliers and licensing entities; the market and the financial/economic crisis are another risk factor for a project, according to six respondents. At this point, it is important to understand that the market could be a threat or an opportunity. For five of the participants, the real estate market itself was a negative cause for the success of the project, but for one of the respondents, it was an opportunity to be explored. This divergence is visible since the respondents mentioned projects that report different periods, so the answers to this question reflect different realities, times of crisis and, in the most current context, of prosperity. Five of the interviewees reported that the main cause of project failure relates to the project manager and the project team, which means that a low-skilled project manager and a project team without experience can be responsible for the project failure.

Risk factors.

Regarding the impact and consequences of the risks in the projects (Table 4), the clear majority of the respondents (16) responded cost overruns, which is in line with the literature and the replies to the first research question; the causes of this impact will be described at the end of this paragraph. The second higher risk impact mentioned was schedule delays, identified by 10 respondents. Only two participants reported the lack of the quality as a negative impact of risks. Project failure and increased sales were identified by one respondent each. Increased sales were identified as a positive market risk, that is, an opportunity. Based on these replies, real estate projects experience cost and schedule overruns and most of them occur in the initial phase of the project, before the execution. Based on the replies from the respondents, the main causes for cost escalation and schedule delays are unrealistic initial estimates; changes in project scope; uncertainties about the building structure; uncertainties about suppliers, contractors and materials; legislation and regulations. After identifying the risks, the sources of the risks and the impacts caused, the interviewees were asked to give some suggestions for future trends in real estate projects. The referenced projects, which did not always perform well in terms of management, allowed the interviewees to draw some conclusions or lessons learned.

Risk impact.

According to Table 5, more than 50% of respondents stated that one of the risk mitigation strategies of the project would involve hiring a qualified project team and a qualified project manager. Also, above 50%, identified in 11 responses, were the suppliers, which were described to be of great significance to the success of the projects. To ensure quality, special attention should be paid to the suppliers’ history and the budget presented. The latter should be viewed and reviewed by the project team so that the estimates are not unrealistic, so as to avoid deviations during execution.

Risk mitigation strategies.

Monitoring and control was also referenced by six interviewees. This measure, according to the interviewees, allows the anticipation of many risks of the project. Monitoring and control allows project optimization by avoiding errors and deviations, resulting this way into gains in time, cost and quality. Another important strategy for the improvement of future projects is the overall review of the project. For three participants, the project should be reviewed by the project manager so that errors are found and resolved in a timely manner. Projects tend to suffer unexpected results such as delays, deviations and unsatisfactory results; companies should learn to accept the reality of projects and have to be prepared to minimize these occurrences. This should be done systematically and in accordance with risk management techniques. Also, according to the interviewees (see Table 5), the use of management practices should be adopted by the organizations to reduce the risks and failure of the projects.

Other measures mentioned by the participants were the realization of a market study aiming to understand the needs of the client, a good planning and definition of the project scope aiming to the success of future projects and, finally, the after-sales service that can help in customer loyalty. The answers presented in Table 5, regarding mitigation strategies, are in line with Khandekar et al. (2017) and Raz et al. (2002), which concluded that, for the overall performance of a construction project, the most important critical success factors are the constructive elements, good planning, a qualified and competent project manager and a clear and realistic definition of the proposed objectives (Kog and Loh, 2012).

Real estate risk model

Based on the results and the assumptions made, it has been developed a new approach for the real estate risk plan mitigation. This new methodology of a plan risk management based in the main risks presented both in the literature and the interview responses obtained previously. The objective of this new methodology for risks includes their identification, their understanding and analysis, their quantification, their prioritization and the development of a plan aiming to minimize the negative consequences and explore the opportunities for the benefit of the project.

The example provided will be the integral rehabilitation of a residential building in the historical centre of Lisbon. The aim is to preserve the existing characteristics and building structure and to assess the viability of the project implementation.

The implementation of this new approach is presented in two major chapters: the analysis of the assumptions where all the requirements of the projects procedures are defined and adopted and the analysis of the results.

In the analysis of the results, the main risks will be identified and prioritized, and a qualitative analysis will be elaborated through the probability and impact matrix; then, the quantitative study will be carried out to allow the desired conclusions to be drawn. For this, the expected monetary value (EMV) analysis will be used, where: EMV = Probability × Cost of Impact.

Assumptions

Completion deadline – 12 months

Budget – €1,936,000 (€1,250,000 for building acquisition + €686,000 for rehabilitation costs);

Quality – high quality; and

Risk tolerance – not more than 70 on a 0–100 scale.

Risk identification

Identifying risks is the process of determining which risks may affect the project and documenting their characteristics. The key benefit of this process is the documentation of existing risks and the knowledge and ability it provides to the project team to anticipate events.

From the results obtained, five threats and one opportunity have been identified (Table 6). These threats and opportunities are likely to occur and have different scales of impact throughout the project life cycle; it is extremely important to register all risks so that preventive and/or corrective measures can be taken before they occur. The data presented were collected through real estate professionals and based on interviews conducted for the present study. From a constructive point of view, there is one main risk for this project; the fact that it is an old building with a wooden structure means that the probability of having to reinforce the entire structure is very high, which will have a great impact on the cost. Mostly, such constructive pathologies are not directly visible, so this risk has to be contemplated in the risk management plan. Another external risk with negative impact on the project objectives is the contracting of suppliers; if the quality and deadline requirements are not respected by these suppliers, the customer will not reach satisfaction; Licensing entities are also a risk to the project’s success. Without the approved designs and licenses, the project cannot proceed, resulting in a negative impact to the time frame estimated. According to project design and stakeholder management, the main causes of risk presented are the lack of a market study, inadequate project team and project manager and scope changes introduced by the sponsor or client.

Risk assumptions.

In this real case, the real estate market is presented as an opportunity or a positive risk. When there is a high demand for properties in a certain city or state and a lack of supply of quality properties, the prices of houses tend to rise.

In the following case, it has been analysed the qualitative risk, as mentioned previously. The qualitative risk analysis is the process of prioritizing risks, combining their probability of occurrence and impact. The key benefit of this process is that it enables project manager to focus on high-priority risks. Thus, the risks identified above are presented in Table 7.

Probability and impact matrix.

Quantitative risk analysis

The quantitative analysis is the process of numerically analysing the effect of identified risks on overall project objectives, which means the following:

– Best case: cost of the project, if only the opportunities materialize.

– Expected value: cost of the project, considering the EMV of the risks (budget + EMV).

– Worst case: cost of the project, if only the threats materialize.

Conclusion of real estate risk model

The first step in the project risk management is the risk identification, which means risks are prioritized according to their potential effect on the objectives of the project.

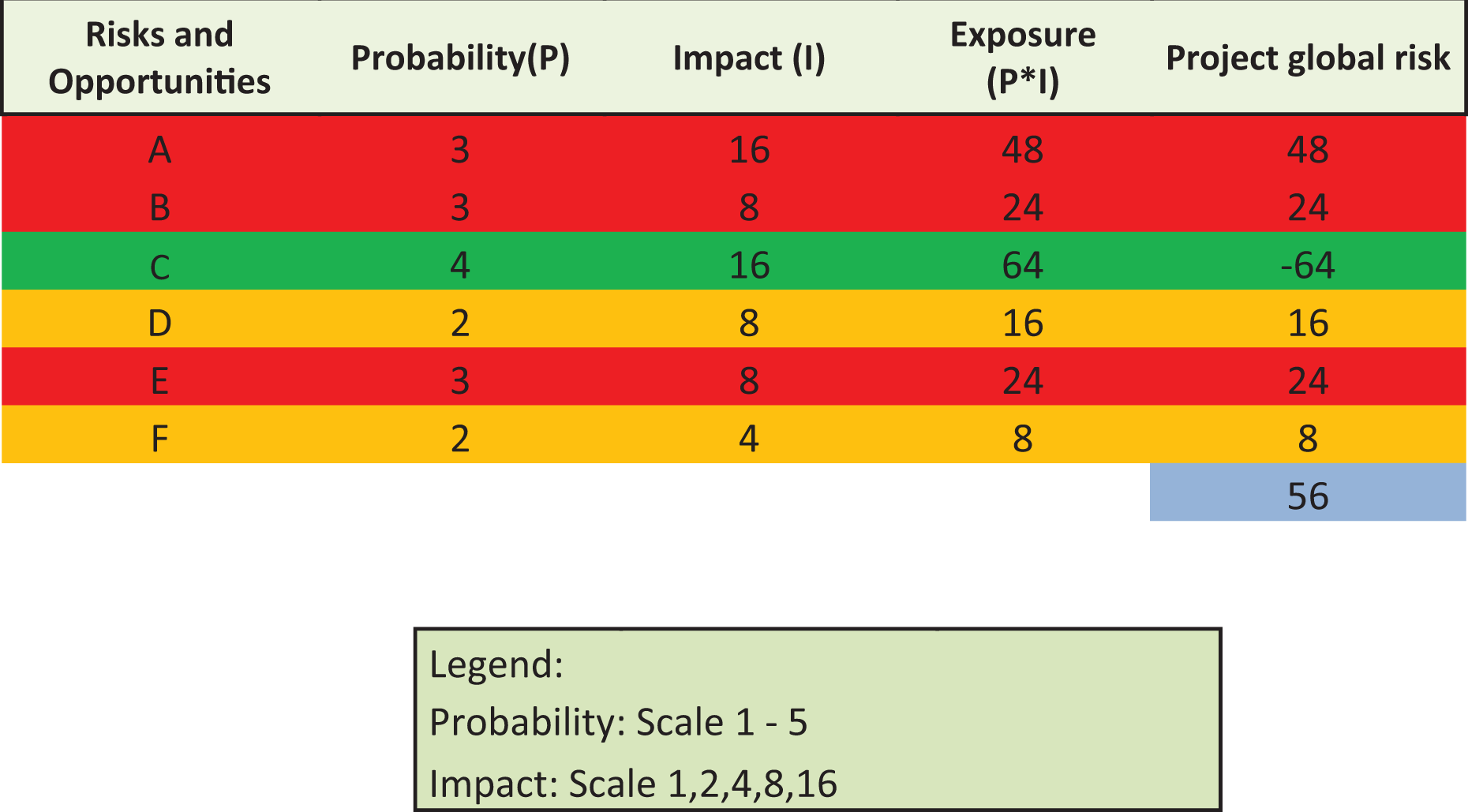

According to Table 6, it is concluded that threats A, B and E are in the high-risk zone of the matrix (Table 7) and may require priority action and response strategies. Threats D and F represent a lower risk, although they require a prevention strategy. Opportunity C represents a positive risk, which need to be exploited. The overall risk of the project (Table 7) leads us to a concrete question and a crucial decision: Should we continue with this project? Is it within the risk tolerance established by the organization?

Based on the qualitative risk analysis, this project should move forward since the stakeholders have established a risk tolerance not more than 70 on a scale between 0 and 100, and according to the qualitative analysis results, the overall risk of this project was 56 (Table 8), which means that this project should move on. For the quantitative risk analysis, the technique used was the EMV analysis (Table 9), which is a statistical concept that calculates the average result when the future includes scenarios that may or may not occur (analysis considering uncertain conditions); the conclusions of the quantitative risk analysis highlight the fact that the project could cost between €1,136,000 and €2,526,880 and the EMV, taking into account the identified risks and their impacts and probabilities of occurrence, is €1,662,180. The next step is to plan risk responses (Table 10); according to the importance of each risk, strategies are planned for negative or positive risks. For the negative risks (threats), the available strategies are avoid, transfer, mitigate, accept and escalate. For the positive risks (opportunities), the strategies are exploit, enhance, share, accept and escalate. When appropriate contingent responses are created for the risks.

In the case of the risks D and F, which are of a lower severity, a risk mitigation strategy was chosen; the actions adopted were application of due diligence, periodic meetings, hiring of more credible suppliers and risk monitoring and controlling of the teams. Defining and deploying mitigation strategies can lead to the reduction of the likelihood and/or impact of an adverse risk, to levels below the acceptable threshold. Anticipating such actions allows also a further reduction of the threats of the project. For the risks A, B and E, a response and a contingency plan was required. For residual risks, a contingency reserve may also be allocated, and it can include the definition of the conditions that trigger its use. For the Opportunity C, the strategy should be to exploit and improve the opportunity. In this case, we should opt for a good marketing plan, maybe international marketing plan or even the realization of partnerships with marketing companies.

Conclusions

The focus of this study is to investigate the main causes of risk in real estate projects and to understand the importance of risk management tools inside organizations in order to mitigate and reduce the risk and increase the project success. It is important to highlight that this article, besides mentioning the main causes of risk in real estate projects, it also identifies several risks and impacts of not having a risk plan. Although this research is based on the Portuguese market, it can be extrapolated to other countries where we can observe the same behaviour and an absence or reduced adoption of a risk plan associated with the real estate market. Hypothesis 1 research question has been mentioned previously, and according to this study, it can be assumed that the relevance that companies give to risk management in Portugal is beginning to emerge; and the implementation of risk management is increasing in different segments. The uncertainty and risks that can occur throughout the project life cycle should be considered by organizations. A real estate project consists of several phases, commencing with planning, execution and closure, and in all of these phases, several risks can occur that can put in danger the success of the entire project. A project should aim to maximize profit and minimize losses, which, without conscious planning and without a risk management plan, may not be possible. Regarding the underlying question, it was concluded that the use of management tools has been exploited by some Portuguese organizations. It is fundamental that real estate companies adopt risk management policies, especially in growing markets where the impacts are reinforced. Implementation of such risk strategies goes beyond the desire to increase efficiency, it derives from the dear need to avoid cost increases and project delays. Risk strategy implementations can be easily adapted to small and large organizations.

Some interviewees stated that they use risk management tools, and the analysis concluded that the projects in these companies have been having a considerable success in terms of controlled cost and time management. Furthermore, it was identified that small companies tend to not have such a well-organized structure and do not have the financial capabilities or even the expertise to bet on risk management techniques.

Based on the information from the interviews, the following conclusions have been taken, regarding the hypothesis 2 research question of ‘which are the main causes of risk in real estate projects?’. The main causes of risk in real estate projects, gathered from the interviews conclusions, are government regulations and licensing entities (e.g. delays in work approvals), inadequate suppliers experience, inexperienced project team or inadequate project manager, real estate market conditions, scope changes, complexity of design and constructive characteristics or type of building structure, poor contract management and lack of communication between the stakeholders. The financial and economic risks, especially the risks related to financial markets, volatility of the housing market or liquidity management were referenced by many of the interviewees as a negative impact, especially in companies with a smaller structure and with fewer resources, as main impact factors. These causes represent the Portuguese reality, and despite they are mentioned in this article, they are not mentioned in the literature as described previously; thus, this can be extrapolated into a new level of criticality and applied to other European countries. This investigation allowed to conclude that the great majority of the companies, in this study, are segmented by different classes, provided a better overview about the market characteristics and is not oriented to the opportunities. Only one respondent reported a positive risk to the project; in this case, the real estate market has become an opportunity thanks to increased demand which made sales increase exponentially. All other participants reported negative risks. This situation allows to conclude that the companies are very oriented to the failure and not to the success due to the several risks existing. They do not view risks as opportunities but rather as threats. This principle should change so that success is increasing in the real estate sector. A threat could be an opportunity and this principle should be implemented in the culture of organizations in Portugal, namely in the class of small and family-oriented and medium-sized organizations, where this principle of risk management is ambiguous. Based on these assumptions, it is considered very important to develop strategies for the implementation of risk management in the Portuguese organizations and to overcome their initial risk. Other European countries are already implementing several risk analysis but for some of them the risks they face are slightly different from the ones which affect Portugal. For instance, the climate impact and seasonal variations are completely different from the North and the South of Europe; thus, the risk methodologies adopted to face this challenge should follow the country climate variations. In the end, a complete risk assessment analysis is crucial to mitigate time and budget deviations and to provide a final product which can have the desired quality and can satisfy all the stakeholders.

Recommendations

The present study allows concluding that risk management is critical to the project’s success. The benefits from adopting a risk management policy are countless, for instance, adequate management of company resources, compliance with laws and regulations, control or minimization of costs, maximization of economic results, correct identification of company deficiencies. Risk management also allows the identification of interesting opportunities for the project. Rigorous and proactive management of the stakeholders involved is a good tool to convert potential threats into opportunities for the project. Communication between all stakeholders is one of the most important factors to achieve the project success; with a good coordination between all parties, it is possible to prevent problems before they happen.

Companies must implement risk indicators or triggers that give visibility to potential risks/losses that impact company objectives and, on the other hand, establish metrics that translate the organization’s appetite and tolerance into critical risks. Risk triggers should be identified during the risk analysis and understanding them helps to develop a more efficient risk response. In the case where risk triggers are unknown, a risk will occur as a surprise, reducing a project manager’s ability to reduce the negative impact or increase the positive one.

At least, it could be interesting to implement and test the model in other markets and in different types of construction.

Limitations

Despite its important theoretical and practical contributions, this research suffers from some methodological limitations. The principal limitation of this article is related to the sample, which is limited. Thus, future research might test our propositions on a wider number of people related with the real estate market besides from different geographic areas to test the generalizability of our results. Another limitation of this article is related with the fact that a real case of risk management in different typologies of buildings will in fact reduce the risk assumption. Other studies focused in different types of constructions will be interesting and complement this project in terms of risk perception and management.

Overall risk project.

Expected monetary value analysis.

Plan risk response.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.