Abstract

This study examines the effect of earnings quality on the cost of debt, for a sample of French listed firms from 2005 to 2015. Using accruals quality (AQ) as a proxy for the quality of financial reports, the results obtained confirm the research hypothesis formulated, showing that the quality of financial reports is negatively related to firms’ interest cost. The results also support that the innate component of AQ has a greater impact on the cost of debt than the discretionary component. The findings of this study may be of interest to managers by providing evidence on the economic consequences of improved earnings on the cost of debt and the factors that determine debt pricing in making decisions to minimize it. The results of this article are also important for creditors, that is, banks, showing that earnings are important in predicting firms’ reimbursement capacity (i.e. future cash flows) and that less estimation error in accruals improves the ability of earnings to predict future cash flows.

Introduction

This study examines the effect of earnings quality on the cost of debt for a sample of French listed firms. Theoretical literature (Bhattacharya, 2003; Easley and O’hara, 2004; Lambert et al., 2012) postulates that information risk is a priced risk factor affecting the cost of capital of firms and there is a wide empirical evidence to support this relationship (Francis et al., 2004, 2005; García Lara et al., 2014; Gray et al., 2009). To the extent that earnings affect firms’ information risk, companies that report high-quality earnings should benefit from a reduction in their information risk, which will affect the cost of external capital for both debt and equity.

Previous studies analyzing the relationship between earnings quality and the cost of capital are mainly conducted on US listed firms, addressing both the cost of equity and the cost of debt. The pioneering work of Francis et al. (2004, 2005) show that better earnings quality, measured through multiple attributes such as accruals quality (AQ), conservatism, persistence, predictability, smoothness, value relevance, or timelines, reduces the cost of capital. Bharath et al. (2008) and Zhang (2008) also examine the relationship between the cost of debt and earnings quality of US firms. Their results reveal a negative association between the cost of debt and the earnings quality, measured, respectively, using AQ and accounting conservatism. Similarly, Gray et al. (2009) and Aldamen and Ducan (2013) confirm that a better earnings quality, as measured through AQ, reduces both the cost of equity and the cost of debt of Australian listed companies.

Most of this previous research has so far been conducted for common law country companies. Our research extends previous studies and attempts to provide empirical evidence of the effect of earnings quality on the cost of debt, based on a sample of firms in a “code-law” country, namely France. The study focuses on the cost of debt because bank loans are the main source of financing for French companies. France is a code-law country with a legal environment structured as “code-law” in the sense described by Ball et al. (2000). The majority of companies are micro, small, and medium-sized enterprises, which means that the banking system is their main provider of capital.

It is widely recognized that many features influence financial reporting practices, including the country’s legal environment, capital market forces, ownership structure, and corporate governance (Ball et al., 2000; Leuz et al., 2003; Soderstrom and Sun, 2007). In this respect, the reporting practices of French companies are influenced by the specificities of the country. First, as the French legal environment is structured as a “code-law,” the accounting and tax systems are closely aligned. Second, there is a strong alignment between ownership and management, which means that most firms are owner-managed and, therefore, not affected by traditional agency problems but rather by conflicts between minority and majority shareholders (Houcine, 2017). Third, the main sources of corporate finance remain banks and are not constrained by formal debt covenants.

To investigate the effect of earnings quality on the cost of debt, we consider an accounting-based proxy, namely AQ for a sample of 220 French nonfinancial-listed firms over 2005–2015.

Our results show that the AQ is associated with decreased interest rates and that the innate component of AQ has a greater impact on the cost of debt than the discretionary component.

This study contributes to the existing accounting literature by extending rare evidence on the effect of earnings quality on the cost of debt in a code-law market and provides new and complementary evidence on this relationship in a different context with a different regulatory and institutional environment. Our research allows interaction among two comprehensive research areas: earnings quality and cost of debt and adds to the literature on the economic consequences of earnings quality primarily conducted on common-law countries (Biddle et al., 2009; Carma et al., 2016; Francis et al., 2005).

Our study reinforces the view that missing some earnings attributes has undesirable economic consequences on the financial markets, such as downward valuations of stock markets (Barth et al., 1999; Kasznik and McNichols, 2002), rating downgrades, or rising interest rates (Jiang, 2008).

The article is organized as follows. The second section presents a review of literature and develops hypotheses. The third section describes the research design, including variables definitions, and empirical models. The fourth section presents the sample and descriptive statistics. The results are provided in the fifth section, while the sixth section presents the sensitivity analysis and the seventh section concludes the study.

Earnings quality and cost of debt: Literature review and hypotheses development

According to the agency theory (Jensen and Meckling, 1976), debt contracts may give rise to conflicts of interest between managers and creditors due to asymmetric information and adverse selection problems, which lead to agency cost of debt (Jensen and Meckling, 1976; Myers, 1977).

Previous literature shows that financial reporting can resolve the agency cost of debt, as it plays an informative role in lending decisions. Lenders, and especially banks, use earnings to assess the risk of business default (Carmo et al., 2016) since accounting earnings provide more information on the characteristics of a company’s financial performance (Dechow et al., 2010).

The association between financial reporting and the cost of debt is based on the theory that information risk is priced. Francis et al. (2005) describe information risk as the probability that the company-specific information relevant to investors price decisions is of poor quality. Since information risk is a priced risk factor (Diamond and Verrecchia, 1991; Easley and O’Hara, 2004; Lambert et al., 2007; 2012), lenders should value the decrease in risk reflected in interest rates. Earnings that increase the accuracy of the company’s estimate of future cash flows would reduce this information risk (Francis et al., 2005). Therefore, improving earnings quality is likely to lower the cost of debt.

The relationship between financial reporting quality (FRQ) and debt pricing has been widely demonstrated in studies dealing with information risk through earnings quality (Aldamen and Duncan, 2013; Barath et al., 2008; Carmo et al., 2016; Francis et al., 2005; Gray et al., 2009; Vander Bauwhede et al., 2015; Zhang, 2008). Most of these studies were conducted for firms in common-law countries and the results documented a negative association between earnings quality and the cost of debt.

Although it has been widely demonstrated, both theoretically and empirically, that there is a negative association between earnings quality and the cost of debt, some features of the French context may prevent such evidence. In the French context, loan granting is still based on informal and personal relationships since banks have better access to information, which makes it possible to convey more information via a private channel. This may reduce the importance of earnings in assessing corporate risk credit, as banks have the ability to reduce the costs of adverse selection for borrowers. Loukil and Yousfi (2012) and more recently Houcine (2017) reported that in a code-law country, namely Tunisia, investors do not trust public financial information and rely more on private information to reduce information asymmetry. Similarly, Talbi and Omri (2014) show that voluntary disclosure reduces the cost of debt for Tunisian listed companies.

It seems that, in the France context, relationship-based lending tends to replace the role of financial reporting in assessing the risk of business default and in decreasing the cost of debt. However, recent works conducted in comparable code-law markets have confirmed a negative association between earnings quality and the cost of debt. Van Caneghem and Campenhout (2012) report for a sample of Belgian small and medium-sized enterprises (SMEs) a positive relationship between corporate debt and FRQ proxies.

Similarly, using a large sample of Belgian SMEs, Vander Bauwhede et al. (2015) show that firms’ FRQs have a negative relationship with the cost of debt. Likewise, Carmo et al. (2016) for a sample of Portuguese and Beltrame et al. (2017) for Italian firms find a negative relationship between the information risk proxied by earnings quality and the cost of debt.

Based on the above analysis, we expect that earnings quality will be important for French lenders in predicting companies’ reimbursement capacity, which will reduce the information risk and the cost of debt. Our prediction could be formalized in the first hypothesis:

As in previous literature (Carmo et al., 2016; Gray et al., 2009; Triki et Omri, 2010; Vander Bauwhede et al., 2015), we use AQ as a proxy for earnings quality. AQ has become synonymous with overall earnings quality (Cascino et al., 2010; Dechow and Dichev, 2002) as it represents a characteristic of the FRQ that focuses on the accuracy of financial information and provides a better predictor of future cash flows (Houcine, 2017). This will help lenders in assessing companies’ credit risk in the debt contract process.

Accruals consist of two components: the innate and discretionary parts. According to the earnings management literature (Dechow and Dichev, 2002; Jones, 1991; McNichols, 2002, etc), Francis et al. (2005) state that the innate component reflects the business models and operating environments in which a company operates. While the discretionary component reflects management choices, including intentional reporting choices, forecasting errors, and implementation errors. Based on this assumption, the authors examine whether the innate and discretionary components of AQ have different effects on the cost of equity for US firms. Their findings show that both the innate and the discretionary components impact the cost of capital. Gray et al. (2009) examine the same association on the Australian market and find that the association between the total quality of accruals and the cost of equity is dictated by the innate component, with no evidence that the discretionary component influences the cost of equity. However, the findings of Aldman and Ducan (2013) reveal that higher innate accruals increase the cost of debt, while higher discretionary accruals reduce the cost of debt.

French accounting standards are based on the International Accounting Standards. The adoption of the International Financial Reporting Standards is mandatory for publicly traded companies, which offer certain flexibility that could lead to earnings management practices. In addition, as a code-law country, French accounting regulation is closely connected to the tax system, which creates incentives for earnings management. As a result, if lenders expect to reduce the business information risk in the debt contract process, they will give more weight to the innate component of earnings quality than to the discretionary component. This leads us to formulate the following hypothesis:

Research design

Models specification

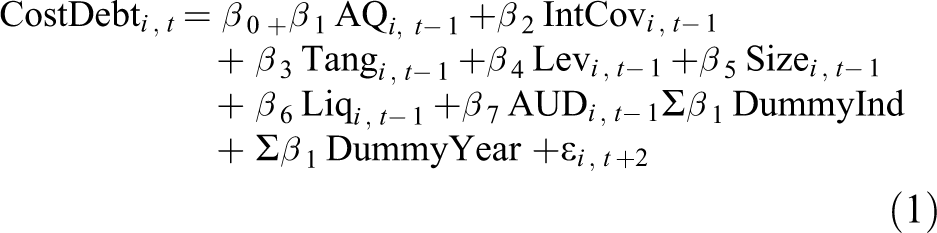

To examine whether earnings quality is related to the cost of debt, we estimate the following model:

where

CostDebt i , t represents the cost of debt of firm i in year t. In line with prior studies (Carmo et al., 2016; Francis et al., 2005; Minnis, 2011; Vander Bauwhede et al., 2015), the cost of debt is computed using the ratio of interest expense to the average interest-bearing debt. AQ i , t−1 is the measure of earnings quality of firm i in year t−1 proxied by AQ. We will explain this measure in more detail in the next section. IntCov i , t−1: it represents the interest coverage ratio of firm i in year t−1and is calculated as earnings before interest, taxes, depreciation, and amortization divided by interest expense. Tang i , t−1 represents a measure for tangible assets of firm 1 in year t−1 and is calculated as the ratio of property, plant, and equipment to total assets. This ratio represents a proxy for assets that can be pledged as collateral by firms to the banks. Lev i , t−1 is the leverage ratio of firm i year t−1. This ratio is calculated as total debt divided by total assets. Size i , t−1 is the size of firm i in year t−1. The size is calculated as the natural logarithm of total assets. Liq i , t−1 is the liquidity ratio of firm i in year t−1 and is calculated as current assets divided by current liabilities. AUD i , t−1 is a measure of external audit quality of firm i in year t−1 proxied by a dummy variable that takes value 1 when the auditor belongs to BIG 4, 0 otherwise.

∑ β 1 DummyInd is a set of dummy variables coded 1 if the observation belongs to the industry and 0 otherwise. We do not formulate expectations regarding the sign of these variables.

∑ β 1 DummyYear is a set of dummy variables coded 1 if the observation belongs to the year and 0 otherwise. We do not formulate expectations regarding the sign of these variables.

Industry and years dummies are included in the model to control for potential industry-specific and time-varying macroeconomic effects on debt pricing (Carmo et al., 2016). εi , t denotes the residuals of the model.

All explanatory variables are lagged 1 year because it is assumed that the definition of the contractual terms of a bank loan, as interest rate, is based on the financial information of the previous year (Carmo et al., 2016).

Consistent with prior literature (Carmo et al., 2016; Cascino et al., 2010; Vander Bauwhede et al., 2015), we include as control variables various firm characteristics identified as influencing the cost of debt. We control for interest coverage ratio, tangible assets, leverage ratio firm size, liquidity ratio, and external audit, to the extent that these characteristics can be associated with higher or lower cost of debt.

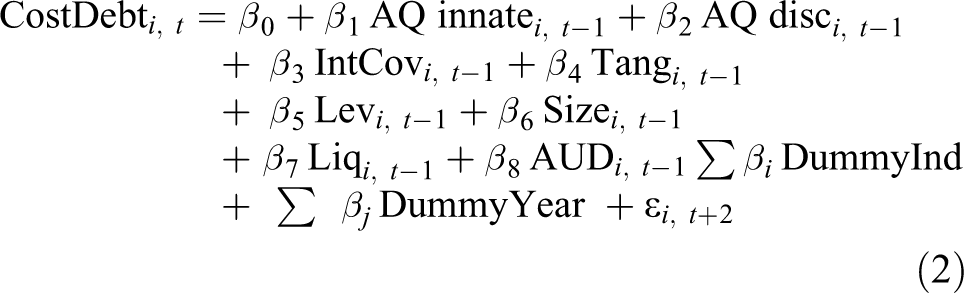

The second hypothesis predicts that the innate component of AQ has a stronger effect on the cost of debt of French firms than the discretionary component. To test this hypothesis, we introduce the two components of AQ in equation (1) as shown below:

where AQ innate i , t−1 innate is the innate component of AQ for firm i in t−1 and AQ disc i , t−1 is the discretionary component of AQ for firm i in year t−1.

We expect that the coefficient β 1 will be negative, whereas we expect that the coefficient β 2 will be less in magnitude in reducing cost of debt, as French lenders price more the innate components of AQ.

The models are estimated by ordinary least squares (OLS) in pooled data. All variables are winsorized at the 1st and 99th percentiles to reduce the effects of outlier observations and are computed with standard errors that are adjusted for heteroskedasticity and clustered at the firm level.

Earnings quality measure

To investigate the effect of earnings quality on the cost of debt, we consider an accounting-based proxy, namely AQ. We are interested in AQ as a measure of the earnings quality, as accruals are estimators of future cash flows and provide information about the activities of the company (Subramanyam and Wild, 1996), which is essential for assessing creditors “risk in the process of debt contract” (Vander Bauwhede et al., 2015). In addition, most of the previous literature ( Francis et al., 2004, 2005; García Lara et al., 2014; Gray et al., 2009) has largely demonstrated that AQ better explains the change in the cost of equity.

To estimate AQ, we use the measure derived from Dechow and Dichev (2002) and modified by McNichols (2002), which has been used extensively in the prior researches (Aldman and Duncan, 2013; Carmo et al., 2016; Francis et al., 2005; Gray et al., 2009; Vander Bauwhede et al., 2015). Dechow and Dichev (2002) rely on evidence that earnings that are more closely related to cash flows are more desirable and their model takes into account the expected accruals given a specific cash flow stream.

The DD (2002) model is a regression of working capital accruals on lagged, current, and future cash flows plus the change in revenues and property, plant, and equipment (PPE). The following model is estimated cross-sectionally in each industry-year with a minimum of eight observations per year in any industry (Mansali et al., 2019) using OLS regression. Industry is defined according to Campbell’s (1996) industry classification of 11 groups.

where WCA i , t represents the working capital accruals for firm i in year t measured as the change in noncash current assets minus the change in current liabilities, minus depreciation, and amortization expense for firm i at year t. CFO i , t−1; CFO i , t ; CFO i , t+1 represent the operating cash flows for firm i at year t−1, t, and t+1, respectively. ΔRi , t is the change in accounts receivable for firm i at year t. PPE i , t is the gross value of property, plant, and equipment for firm i at year t.

All variables are scaled by lagged total assets to prevent heteroscedasticity problem (Garcica-Lara, 2011) and consistent with prior studies, all variables are winsorized at the 1st and 99th percentiles.

The residuals from the regression reflect the accruals that are not explained by cash flows of the previous, current, and subsequent periods nor by change in revenue and PPE. The higher the absolute value of unexpected working capital accruals, the greater the accrual estimation error and, consequently, the lower AQ. We use the absolute value of the residuals as a measure of AQ multiplied by (−1). Thus, a larger value corresponds to a better AQ.

To test our second hypothesis, we need to distinguish between the innate and discretionary components of AQ. The innate component is given by the predicted values obtained from the regression of equation (3) applied to firm-year variables to the industry-specific parameters.

Sample selection and descriptive statistics

The initial sample consists of all French listed firms from CAC All Tradable index during the period 2005–2015. Following prior literature, we exclude financial firms (standard industrial classification (SIC) codes 6000–6999) and regulated utilities (SIC codes 4900–4999) due to the specific characteristics of the structure of their assets and liabilities and the nature of their accruals (Houcine, 2017). As per Bond and Meghir (1994), we exclude firms that do not have suficient data for five consecutive years. The screening process results in a total of 220 firms making 2420 firm-year observations. Accounting and financial data are collected from Worldscope.

Table 1 reports the frequency of firms by industry using Campbell’s (1996) classification.

Industry classification.

Note: SIC: standard industrial classification. This table provides the distribution of firms by industry using Campbell’s (1996) classification.

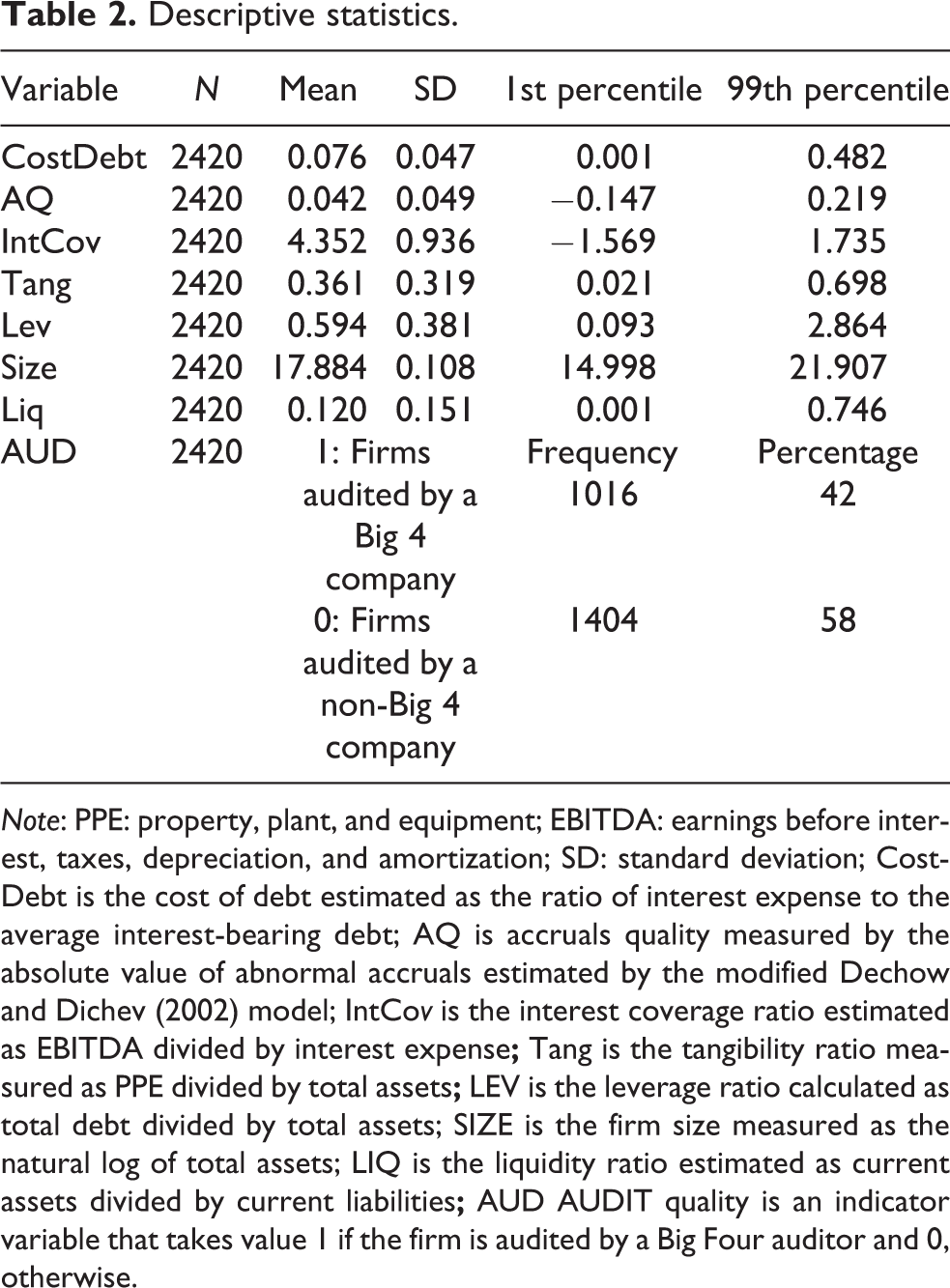

Table 2 presents the descriptive statistics for the dependent and explanatory variables. The mean of the cost of debt variable is about 7.6% and is lower than the values reported by Vander Bauwhede et al. (2015) and Caramo et al. (2016), which are, respectively, 9.6% and 11.1% for samples of Belgian listed firms and Portuguese private companies, but similar to the value reported by Minnis (2011) for a sample of US private companies, that is, 7.3%. For AQ, the table presents a mean of 0.042 in absolute value. Comparing these values with those reported in the existing literature in some code-law countries (Bauwhede et al., 2015; Carmo et al., 2016; Garcia-Teruel et al., 2009), French companies have a lower AQ than Belgian companies (0.006), Portuguese (−0,03), or Spanish firms (0.0144), as higher absolute values indicate lower AQ. As the French context is characterized by a high concentration of ownership, this result is consistent with the conclusion of Fan and Wong (2002) that Firms with concentrated ownership have less incentives to provide high-quality accounting information and tend to keep it because the perceived benefits of sharing information with third parties are low.

Descriptive statistics.

Note: PPE: property, plant, and equipment; EBITDA: earnings before interest, taxes, depreciation, and amortization; SD: standard deviation; CostDebt is the cost of debt estimated as the ratio of interest expense to the average interest-bearing debt; AQ is accruals quality measured by the absolute value of abnormal accruals estimated by the modified Dechow and Dichev (2002) model; IntCov is the interest coverage ratio estimated as EBITDA divided by interest expense; Tang is the tangibility ratio measured as PPE divided by total assets; LEV is the leverage ratio calculated as total debt divided by total assets; SIZE is the firm size measured as the natural log of total assets; LIQ is the liquidity ratio estimated as current assets divided by current liabilities; AUD AUDIT quality is an indicator variable that takes value 1 if the firm is audited by a Big Four auditor and 0, otherwise.

Compared with Italian listed firms (Cascino et al., 2010), French companies seem to be larger (17.884 vs. 12.880), which means they invest more. Tangibility ratio is equal to 0.361, which means that more than a third of assets can be pledged. This ratio is slightly higher than the value (0.29) reported by Carmo et al. (2016) for Portuguese companies or Vander Bauwhede (2015) for Belgium firms (0.282). French companies also seem highly indebted, with a mean for the leverage ratio equals to 60%, which is significantly higher than that reported by Cascino et al. (2010) for Italian companies or Vander Bauwhede (2015) for Belgium companies but slightly lower than reported by Carmo et al. (2016) for Portuguese companies. It should be noted that creditors have significant assets that can be pledged as collateral, as reflected by the tangibility ratio. It also appears that French firms have a liquidity problem since the liquidity ratio is very low (0.120), but it is similar to that found by Carmo et al, (2016) for Portuguese firms. However, the interest coverage ratio is equal to 4.352, which means that French companies can meet their current interest payment obligations. This ratio is slightly similar to that found by Carmo et al. (2016) for Portuguese companies but lower (15.81) than that revealed by Vander Bauwhede (2015) for Belgium firms. We also note that 42% of firms are audited by BIG 4 auditors.

Empirical results and discussion

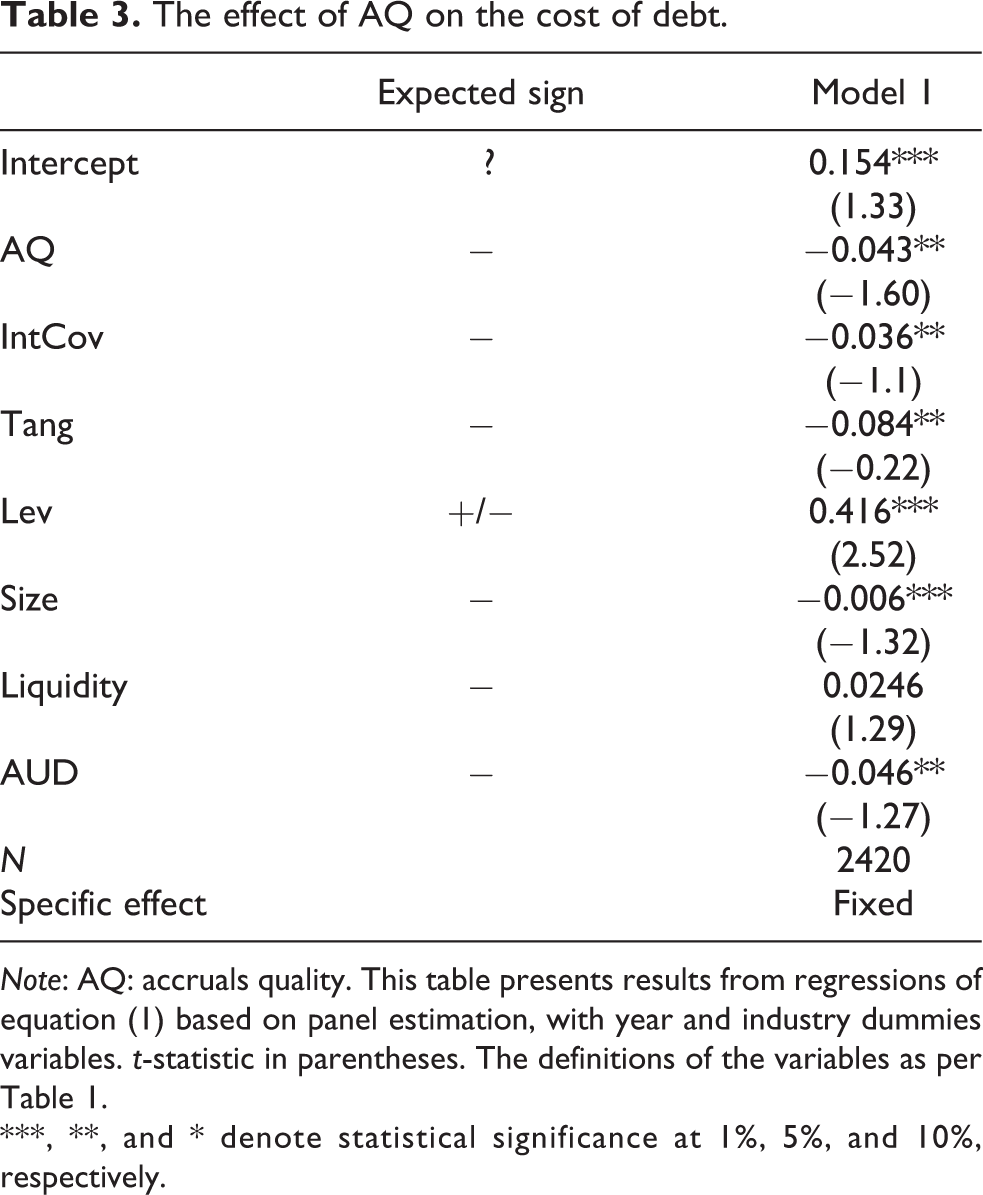

Table 3 presents the estimation results for model 1, which is designed to test whether earnings quality leads to a decrease in the cost of debt. The estimation of equation (1) is based on panel regressions. We use panel data regressions to account for both heterogeneities across firms and for dynamic effects that are not visible in cross-section regressions.

The effect of AQ on the cost of debt.

Note: AQ: accruals quality. This table presents results from regressions of equation (1) based on panel estimation, with year and industry dummies variables. t-statistic in parentheses. The definitions of the variables as per Table 1.

***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively.

Before starting the regressions, we perform a series of required tests. We first did the homogeneity test to examine the presence of individual effects and the Hausman test to choose between the fixed model and the random model. We also performed heteroscedasticity and autocorrelation error tests. The homogeneity test shows the presence of individual effects in the different specifications. In addition, the Hausman test reveals fixed effects in all specifications. Finally, the results led us to use the feasible generalized least squares (FGLS) method to adjust standard errors for heteroscedasticity and serial correlation and clustered at the firm level (Peterson, 2009).

Table 3 presents the estimation results of model 1. As expected, the results show a negative and statistically significant coefficient for the variable AQ. This finding corroborates the existence of a negative relationship between the earnings quality and the cost of debt for French listed firms, similar to that found in previous studies (Barath et al., 2008; Beltrame et al., 2017; Carmo et al., 2016; Francis et al., 2005; Vander Bauwhede et al., 2015). This result means that French lenders price the information conveyed through accounting earnings to reduce agency cost of debt. This finding also suggests that relationship-based lending is not a substitute for the role of financial reporting in assessing firms’ default risk and that FRQs impact on firms’ access to credit.

For control variables, firm size, interest coverage ratio, tangibility, and audit have a significant negative relationship with the cost of debt. Size and tangibility coefficients indicate that large firms have a higher proportion of tangible assets that imply a higher liquidation value of the firm, which can lead to lower interest rates (Minnis, 2011).

The negative interest coverage coefficient suggests that companies with a high values interest coverage ratio have a lower financial risk, which is priced by banks. The negative audit coefficient variable indicates that French banks value the quality of audit when determining the interest rate to charge, which is in line with the conclusions of Minnis (2011) and Carmo et al. (2016). The coefficient of liquidity does not appear to be statistically significant, suggesting that French lenders do not price the liquidity of companies to assess credit risk. As expected, the leverage ratio has a significant positive effect on the cost of debt, which means that higher interest rates are charged to highly leveraged companies because of the increased financial risk associated with leverage.

Table 4 presents the estimation results of model 2, which examines whether the innate component of AQ has a greater impact on the cost of debt than the discretionary component. The estimation of equation (2) was also based on panel regression using the FGLS method and computed to adjust the standard errors for heteroskedasticity and serial correlation and clustered at the firm level (Peterson, 2009).

The effect of the innate and discretionary components of accruals on the cost of debt.

Note: AQ: accruals quality. This table presents results from regressions of equation (2) based on panel estimation, with year and industry dummies variables. t-statistic in parentheses. The definitions of the variables as per Table 1.

***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively.

As expected, the results show that the innate component of AQ is larger in magnitude than the effect of the discretionary component of AQ. In economic terms, the effect of the innate component of AQ reduces the cost of debt by five basis points, while the discretionary component is less than one point. The results are consistent with those of Francis et al. (2004) for US firms and suggest that, in determining the cost of debt, French lenders give more weight to the innate component of AQ based on economic fundamentals, compared to the discretionary component that depends on management’s choices. Regarding the control variables, as expected, the sign of the coefficients for interest coverage ratio, tangible assets, size, and audit have a statistically significant negative coefficient. The coefficient of the leverage ratio is significantly positive and the coefficient of the liquidity ratio remains insignificant.

Sensitivity analysis

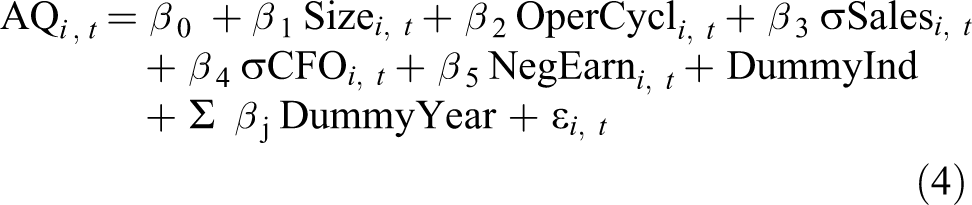

As a sensitivity analysis, we examine the endogeneity of the earnings quality and leverage. According to Gosh and Moon (2010), one of the potential motivations for earnings manipulation is to avoid the violation of the bank agreement. As a result, highly leveraged companies are more likely to engage in earnings manipulation practices, which should reduce FRQs. To address this potential problem of endogeneity, we use a two-stage least squares (2SLS) model. AQ is estimated endogenously in the first-stage regression, and the cost of debt is estimated in the second-stage regression as the dependent variable. Following Beltrame et al. (2017), in the first stage, we estimate AQ using the following model:

where Size is firm size, OperCycle is the length of the operating cycle, σ(Sales) is the standard deviation of sales, σ(CFO) is the standard deviation of cash from operations, and NegEarn is the number of years in which earnings are negative.

In the second stage, we use the predicted value of AQ from the first-stage regression. The results of the 2SLS regression are presented in Table 5 and show that the measurement of AQ metric is negatively and significantly related to the cost of debt, which confirms our main finding.

AQ and the cost of debt: a two-stage regression.

Note: AQ: accruals quality. This table presents results from regressions of equation (4) based on panel estimation, with year and industry dummies variables. t-statistic in parentheses. The definitions of the variables as per Table 1.

***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively.

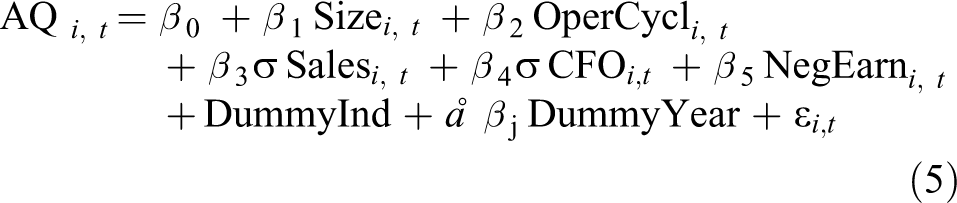

As an additional sensitivity test, we also test the endogenous problem of the second hypothesis, concerning the innate and discretionary component of AQ with the cost of debt. To address this potential problem of endogeneity, we use a 2SLS model. The innate and discretionary components of accruals metrics are estimated endogenously in the first-stage regression, and the cost of debt is estimated in the second-stage regression as the dependent variable using equation 2.

Following Beltrame et al. (2017), in the first stage, we estimate the innate and discretionary components of accruals using the following model:

whereas the predicted values from model (5) reflect the quality of innate accruals and the residuals from the same regression reflect the discretionary component of AQ.

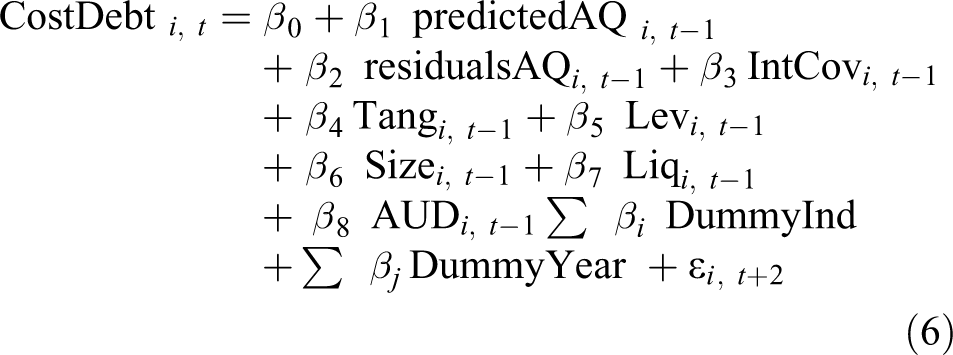

In the second stage, the predicted value and the residuals of the first-stage regression are used in the following model:

The results of the 2SLS regression concerning the innate and discretionary component of AQ with the cost of debt are presented in Table 6. We note that the results remain the same and that the innate component of AQ remains larger in magnitude than the effect of the AQ discretionary component.

The innate and discretionary components of AQ and the cost of debt: a two-stage regression.

Note: AQ: accruals quality. This table presents results from regressions of equation (5) based on panel estimation, with year and industry dummies variables. t-statistic in parentheses. The definitions of the variables as per Table 1.

***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively.

Conclusion

This study examines the effect of earnings quality on the cost of debt. It extends the relevant literature by analyzing the relationship between financial structures, earnings quality, and information asymmetry on the French market. Previous studies were mainly conducted in common-law countries, while our study is based on a code-law country, with a different regulatory and institutional environment, in which relationship-based lending tends to replace the role of financial reporting in reducing information asymmetry.

The empirical results confirm the research hypotheses formulated, showing that firms that observe better AQ support a decrease in their cost of debt. This result tends to prove that relationship-based lending does not replace the role of financial information in mitigating information asymmetry and that French banks price the information risk.

This article contributes to the existing literature in many ways. First, it highlights the effect of earnings quality on the cost of debt in the context of publicly traded companies in a code-law country and shows that FRQ has economic consequences in such a context, which would incite managers to prepare better quality of financial reports. Second, this article extends the literature on the agency cost of debt (Jensen and Meckling, 1976; Myers, 1977) and provides evidence on how agency conflicts between firms and creditors could be overcome with a better FRQ. Third, to our knowledge, this article is the first empirical study examining the relationship between earnings quality and the cost of debt in the French context.

The implications of this study may be of great interest to managers, banks, and regulators. The results are valuable to managers who use debt as the primary source of capital funding to better understand the economic benefits of FRQ. It is important to know the factors that determine debt pricing to help managers understand how banks assess the lending process to make decisions that minimize the cost of debt. In addition, to the extent that opportunistic earnings management reduces FRQ, managers may learn from these results that managing earnings may have the potential disadvantage of increasing the effective cost of interest and, therefore, consider financial reporting strategies to minimize the cost of debt. Preparing high-quality financial information could, therefore, be useful for assessing debt pricing.

The results also suggest that banks price earnings quality and that companies could reduce debt pricing by offering better earnings quality. Thus, the results can be useful for banks to properly assess the terms under which they are allocating loans to companies and to decide on the interest rate to be granted.

The findings are also interesting for regulators as they show that the information contained in the financial reports is used by stakeholders and therefore relevant to them.

Overall, the findings may be of interest to banks and companies’ managers in code-law countries with an institutional environment similar to the French market. To the extent that the flexibility allowed by the accounting rules affects FRQ, our results could be interpreted as a call for tighter accounting regulations with less managerial discretion, as this could help companies to obtain low interest rates for bank loans.

However, this study has limitations related to the exclusively use the AQ as the sole proxy for earnings quality. In future research, it would be relevant to address other measures of earnings quality, such as conservatism, persistence, predictability, and earnings smoothing.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.