Abstract

The article explores reasons for the lack of success of digital electronic shelf labels (ESLs) in US retail settings. It suggests that these reasons can be traced by referring to the triple meaning of ‘digital’: ‘Digital’ now means electronic, but the word also long encompassed numerals – a digit is a number – and body parts – digitus is the Latin word for the finger, that is, the index we use to point at things or manipulate them. The current fate of ESLs is linked to a long history that combined these three dimensions. The study unfolds along a twofold narrative. First, it reviews the recent introduction of ESLs in the United States based on the reading of papers and advertisements published in Progressive Grocer, a leading trade press magazine. Then, it goes ‘back to the future’ by exploring the roots of ESLs over a century. This historical study is based on the analysis of the evolution of US price tag patents (through a network study of patents citations and their evolution); the network analysis is complemented with the history of the US price tag market (through the knowledge gained from Progressive Grocer). The results show that digital price fixing depends on past and present systems and infrastructures, cost constraints and payback schemes, legal frameworks, and social projects.

One of the most striking developments affecting contemporary markets is their digitalization (Cochoy et al., 2017). The current process of digitalization spreads like a technological plague: big data, electronic devices, digital platforms, computerized networks and other IT infrastructures move everywhere, from hi-frequency trading in financial markets (MacKenzie, 2017) to RFID chips (Simakova and Neyland, 2008) and then to phone apps in mundane consumption settings (Fuentes et al., 2017).

Within the realm of the digitalization of market devices, the case of electronic shelf labels (ESLs) deserves particular attention for at least two reasons. First, on the consumer side, price tags frame the core of the market relationship. By establishing a single link between each product and its economic valuation, both in terms of price and quality, price tags work as key ‘qualculative devices’ that inform, equip, and even nudge consumer choice (Cochoy, 2019). Second, on the retailer side, the digitalization of price tags conveys important promises, in terms of both productivity and strategy, by providing a means for instant price management and by offering greater price clarity and flexibility, in both cases leading to better adaptation to changing market conditions. In this respect, studying ESLs, their contribution, and their evolution merges with other works on the economic sociology of prices.

The social sciences have long shown that prices are not the abstract expression of the power relationship between supply and demand, but rather, they are the outcome of complex structural, cultural and relational forces (Beckert, 2011). More recently, authors with STS backgrounds have shown that prices are prosthetic devices engineered to meet the needs of specific professions and institutions (Çalişkan, 2007) and that price display technologies play a prominent role in the functioning of the market economy (Cochoy et al., 2018a, 2018b, 2019). ESLs are puzzling in this respect. On the one hand, they represent one of the latest and most sophisticated evolutions of price tag technologies. On the other hand, their presence is still marginal, particularly in the United States. In a previous contribution, based on the ethnography of a Swedish store and interviews with professionals, we explored the present local and spatial reasons behind this paradox, particularly the problematic articulation between electronic and paper labels (Soutjis et al., 2017). In the present paper, we complement our former spatial explanation with a temporal one based on archival materials and a corpus of patents about the US market for electronic shelf labels.

We hypothesize that the digital is better understood if we refer to its full threefold etymology. Digital now means electronic, that is, ‘all that which can be ultimately reduced to binary code but which produces a further proliferation of particularity and difference’ (Miller and Horst, 2012: 3). But digital has also long encompassed numerals – a ‘digit’ is a number – and body parts – digitus is the Latin word for the finger, that is, the index we use to point at things or manipulate them (Cochoy et al., 2018a). Our hypothesis is that all three meanings are embedded in price tag history and that this embeddedness explains the absence of a radical contribution of ESLs and the persistence of former alternatives.

We will support this hypothesis through a twofold narrative. First, we review the recent introduction of ESLs in the United States based on the reading of all papers and advertisements related to ESLs in Progressive Grocer, a leading American trade press magazine. This review will show both the promises attached to ESLs and the modesty of their implementation. Then, we will attempt to understand this paradox. To do so, we will go ‘back to the future’ by exploring the roots of ESLs over a century. The current study is based first on the analysis of the evolution of US price tag patents, through a network study of patents citations and their evolution, and then the network analysis is complemented with the history of the US price tag market (through the knowledge gained from Progressive Grocer). As we show, patent citations account for just a small part of the history of technology, and should be complemented with external data and their qualitative analysis. This anamnesis (or recursive history) will help justify why ESLs should be seen as an incremental rather than discontinuous innovation and why knowing the history of price display technology matters for understanding how contemporary markets work. We will thus show that the digitalization of markets, far from being reducible to the radical novelty of electronic screens, should rather be conceived of as a dynamic agencement of combinable technologies that have evolved at different paces; in some cases, the apparent modernity of the most recent devices even hides a return to old technological features and practices.

The ambivalent introduction of ESLs in US retailing: Insights from Progressive Grocer

How did ESLs enter the American market, and to what extent did they enter this market? We answer these questions through the lens of Progressive Grocer. This major trade magazine was launched in 1922 to help American grocers improve their business, and it has been continuously published since then. From its origins, the magazine has mostly been financed by its advertisers, who have ceaselessly promoted various devices that are supposed to increase retailing efficiency and profitability, such as cash registers, scales, shopping carts and, of course, all sorts of digital devices. As such, reading the magazine is one of the best ways to trace the evolution of retailing technologies over a long period (Cochoy, 2015). Throughout the article we use (Year, Month, Page) to refer to the source material from Progressive Grocer.

Unsurprisingly, from the 1970s onward, the number of articles about new computerized devices and other digital gadgetry have increased in the magazine; these articles chronicle innovations ranging from major innovations such as electronic cash registers, computers and data centers to more special or uncertain tools, such as fingerprint recognition (2000, 04, 90 sq.; 2002, 02, 20; 2004, 15, 34 sq.), shopping cart assistants providing services store directories (2001, 01, 58) and RFID tags (2004, 16, 62). Paradoxically, however, the digitalization of retail prices – that is, the most important information about goods and services from the perspective of economics – occurred as a late and marginal evolution, coming after the digitalization of the retail environment (e.g. cash registers, scales and computers) and after the digitalization of the surrounding elements of prices themselves: barcodes are close to the prices, but the prices themselves have tended to remain hard matters without a digital dimension. For this reason, ESLs occupy a central and puzzling position: central because with them the price becomes digitalized, and puzzling because this form of digitalization is the last one, and yet it is marginal, slow and discrete.

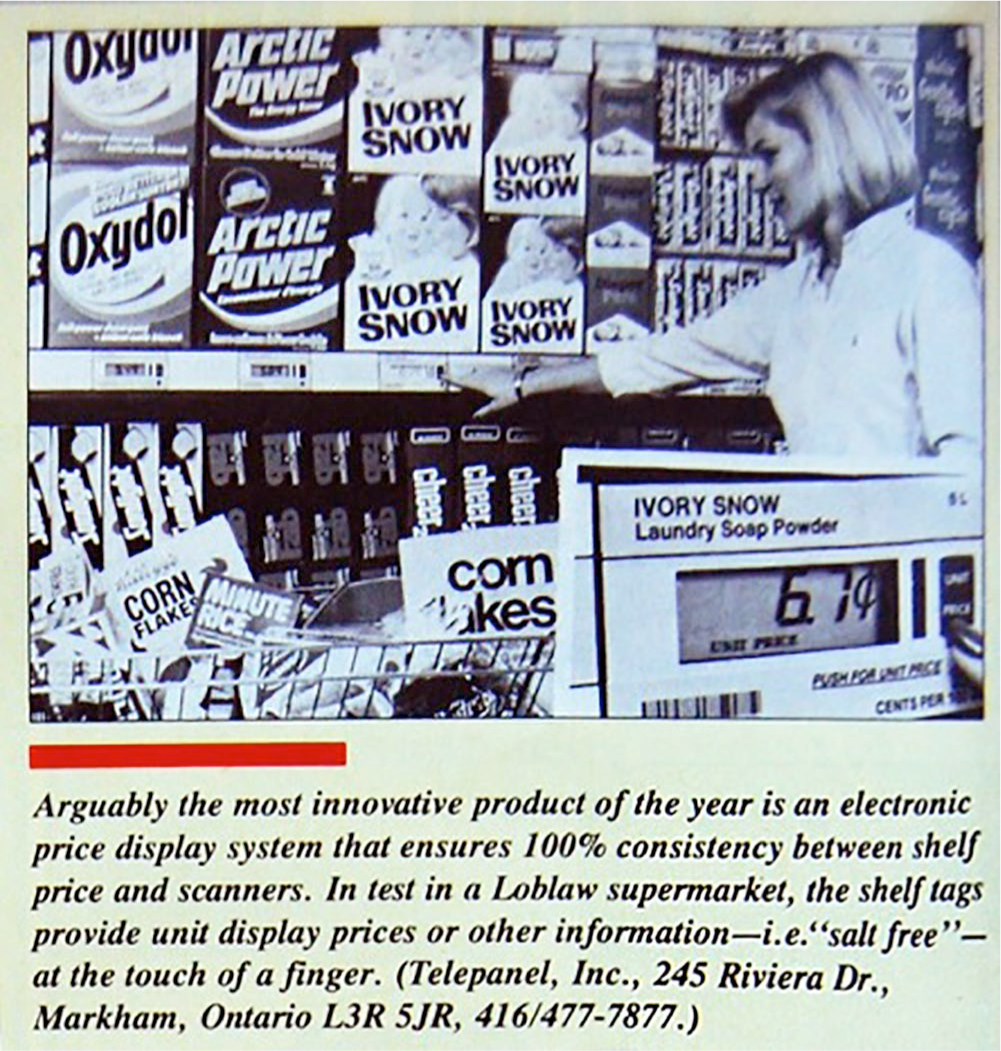

ESLs appeared in the magazine quite early, showing up in 1985 in a small follow-up that presented this innovation as ‘Arguably the most innovative product of the year’ (Figure 1). From their introduction, ESLs have been continuously presented in positive and promising terms, with titles like ‘ESL up and running’ (1993, 12, 23-24). Later statements said, ‘Connectivity is about to change the way retailers think about consumer relationship’ (2002, 02, 14) and ‘Every time we think there is nothing else to improve, there is additional data for digitizing the store’ (2015, 12, 26). Prophetic titles or subtitles proliferate throughout Progressive Grocer, describing ESLs as part of the ‘Supermarket of the future’ (2015, 12, 22 sq.), as a ‘technology that will be driving your store – and your customers – within the next five years’ (2002, 02, 13). Three contributions of ESLs have been proposed to support these views.

Electronic price display, Telepanel, Inc. (1985, 11, 54).

First, the promoters of ESLs stress the device’s ability to improve shoppers’ experiences. ESLs are supposed to meet these objectives through a combination of in-store tags and data-mining methods: ‘Shelving technologies can help brands and retailers drive customer engagement and loyalty’ (2016, 01, 98). New technologies of information would ‘bring back to retailers what massification of marketing took away’ (2002, 02, 13). In this respect, Progressive Grocer connects ESLs to larger conceptual shifts such as the advent of relationship marketing or experiential and collaborative marketing based on the figure of the postmodern consumer (Cova and Cova, 2012). Hence, ESLs would improve consumer satisfaction by being easier to read; they would be more securely attached than paper labels and ‘cleaner looking’ (1994, 08, 136); and they would allow for changing prices several times a day, hence adjusting instantly to market fluctuations and retail price competition (i.e. 1993, 12, 23; 1991, 07, 100). ESLs are supposed to develop the transparency of product information (i.e. 1991, 07, 102; 1990, 01, 66) and thus express the awareness in the retail sector of a growing consumer interest in ethical concerns (such as fairness and sustainability) (Dubuisson-Quellier, 2013) and food safety issues (Frohlich, 2017). Animated shelf displays could provide more information to consumers (1991, 07, 102; 1990, 01, 66), show time-sensitive promotions (1991, 07, 102), and enhance consumer–product interactions (1991 07 102; 1994, 08, 136; 1995, 12, 14). For instance, the advent of ESLs based on electronic paper promises provides more complete visuals in this respect. If this latter technology is recent, Progressive Grocer introduced it as soon as in 2002: ‘Electronic papers, shelf labels, and plasma signage bring to the shelves promotional and pricing power never before imagined’ (2002, 02, 14).

Second, ESLs are also presented as a means to simplify logistic operations (in particular, through the coupling between ESLs and RFID technologies) and to dramatically increase the speed of inventory management and checkout services. As such, they should be able to solve long-lasting issues in retail settings, such as the time and cost of price changes (1971, 06, 5) – ESLs are about ‘displaying price instantly on command’ (1990, 01, 61) – and the old problem of price discrepancies between shelf price and checkout price. The device ‘ensures 100% consistency between shelf price and scanners’ (1985, 11, 54), ‘price integrity between shelf and scanner is assured’ (1990, 01, 62), and ‘people came to the [equipped] store because they believe prices to be right’ (1994, 08, 135).

Third and most importantly, the different testimonies gathered and reported by the magazine outline the idea of a continuous interconnectivity between all sorts of technologies. Retailers think about digital devices not only as independent entities, but also as a global market ‘agencement’: ‘a form of arrangement [made of various human and non-human resources] that acts and at the same time imposes a certain format on the action’ (Callon, 2016). In this respect, the fate of ESLs is clearly related to their coupling with other in-store innovations. ESLs have been seen as extensions and outcomes of the growing use of computerized databases in the retailing sector. A more recent articulation between ESLs and wider market infrastructures is their possible coupling with smartphones: Progressive Grocer reported that by integrating Bluetooth beacons into smartphones, ESLs could provide more product information to the consumer by sending real-time and targeted promotions to clients and helping them navigate the store (2016, 01, 96). On the logistic side, ESLs coupled with wireless communicative technologies could provide store staff members with digital mappings of the store, planograms and alert professionals to restock shelves when empty. In a sense, this is not new. In the 1990s, former versions of electronic labels were also used to provide additional information. Yet the latter was obtained through buttons that had to be pushed manually, and the shared data were limited (mainly unit prices). By contrast, current second-screen technologies could enhance the convenience of such practices and the amount and diversity of shared data (e.g. nutritional data, allergens and manufacturing conditions). Hence, through this coupling, ESLs are presented as the missing link of fully connected stores; if other technologies outplayed ESLs in the 1990s, those innovations are about to render ESLs more interesting today through the articulation of the potentialities of different technologies.

In December 2015, Progressive Grocer reported on a Kroger store that implemented this kind of articulated innovation. Brett Bonner, the vice-president of research and development of the Kroger Company, explained that paper labels had been replaced by ESLs in one of the chain’s stores. According to him, ESLs rendered prices bigger and brighter, facilitating the management of the shelves via digital planograms. In this store, ESLs were a piece of a wider innovative machine, where shelf motion videos and smartphone self-scanning pointed toward the future (2015, 12, 22 sq.). Kroger had also pioneered the adoption of barcodes by adopting a cash register equipped with such a device as early as 1967, well before the development of the Universal Product Code in 1974 (Kato et al., 2010; Kjellberg et al., 2019). The ‘fully digitized’ retail environment implicitly conceives of digital devices in opposition to paper and traditional non-digital retail methods. Here, paper is seen as an archaic material that needs to be replaced by a more flexible technology.

In fact, the situation of ESLs can only be understood when replacing them within a larger technological system combining traditional devices with new digital technologies, such as electronic paper, electronic signage, in-store plasma screens, handheld scanners, data-mining, Point of Sale systems (POS), self-checkout systems, mobile phones, wireless communication programs, smartcards, fingerprint payments, Bluetooth and RFID beacons (2002, 02, 52). Recently, the focus has been placed on smartphones, which are depicted as ‘the linchpin of most in-store technologies’ (2016, 01, 96), especially if coupled with other devices, loyalty programs and big data. Today, many retailers have started mobilizing customers’ smartphones via apps used for digitalizing loyalty programs, collecting data, sending targeted marketing campaigns, providing further product information (allergens, nutritional data, provenance, carbon footprint, etc.), and dealing with virtual coupons and recipes.

Progressive Grocer published a survey that is very useful to contextualize the place of ESLs among other available technologies. From 2005 to 2009, the magazine reported the evolving result of the same yearly poll about how top executives of companies operating ten supermarkets or fewer envision the future of digital technologies. Figure 2 aggregates the results of this survey (2005, 02, 52; 2006, 01, 63; 2007, 01, 86; 2008, 02, 65; 2009, 02, 83). The middle part of the figure reports the percentage of respondents who rated each listed application as the most or second-most promising technology among many (on a scale of 1 to 5). The right-hand part reflects how respondents use or view the same technologies (row total = 100%). The evolution of the survey is very interesting, helping to assess the situation of ESLs within the larger world of digital devices and promises. It shows the contradiction between a statistical approach that requires stable categories and the monitoring of innovations, which always has been difficult to measure because of new entities entering the picture – the list of items has been updated continuously by rephrasing some categories, removing others, and adding new ones (see the bottom of the list, which should be interpreted this way).

How executives view digital retail technologies (2005–2009). For readers of print versions of this article, please see the online version for color figures.

Among the top-ranked innovations, we regularly find ‘POS hardware/software’, ‘back-office applications’, ‘mobile wireless applications’ and ‘electronic payments’ (even if this latter system was introduced in the ranking only in 2007). By contrast, ESLs occupy the lower half of the ranking, along with ‘RFID’, ‘fuel automation’ and ‘self-checkout’. Clearly, ESLs are not considered the most promising and interesting technology. Even more surprising, in 2009, ESLs were removed from the list, almost as if they had become insignificant, pushed aside for new promising topics such as the use of digital solutions for merchandising, loss prevention, and so on. Since then, the diffusion of ESLs has remained problematic and slow. In a 2016 post on the magazine’s website, Progressive Grocer journalist John Karolefski (2016) reports on the important discrepancy between the European and US markets in terms of ESL use, concluding: ‘Grocers around the world are enjoying [the] benefits [of ESLs] for store performance, coupled with an improved shopper. In the United States, ESLs have been talked about for a long time, and while a few pilots have been staged over the years, no widespread deployment has taken place. That may change soon’. A recent article about a business report on the market for ESLs confirms this persistent asymmetry in favor of the European market: ‘Sales of electronic shelf label are likely to remain concentrated in the developed countries of Europe, especially, France, Germany and the United Kingdom. Demand for electronic shelf label in Europe is largely driven by price compliance that has resulted in retailers adopting the technology to avoid penalties’ (Choudhuri, 2019).

Of course, the future is never certain. But returning to this uncertainty, let us instead outline what the journalist invites us to reflect on regarding the relative failure of ESLs in the United States and the reasons behind it. It is worth noting that ESLs did not provoke the one-way praise of the broader digitalization of retail food markets described above. In fact, the presentation of ESLs in Progressive Grocer appears ambivalent. Enthusiastic accounts have always been counterbalanced by the expression of some doubts; these doubts are first visible in some questioning titles chosen by the journal: ‘Will supermarket play electronic tags?’ (1991, 07, 99 sq.) or ‘Are ESLs worth it?’ (1994, 08, 135). Doubts also emerged from other reflections ‘questioning technology’s promises’ (2002, 02, 52): ‘How often will labels that aren’t hard-wired require battery changes and will that create havoc? Don’t LCD units wear out in five years anyway? What happens to hard-wired systems when a shelf is damaged or becomes embedded with syrup, for example? Are hard-wired systems cumbersome to install and operate?’ (1990, 01, 62). This skepticism was fueled by hard facts. The competition among ESLs providers in the early 1990s provided a first clue: among six key providers presented by Progressive Grocer in 1990 (1990, 01, 61 sq.), three had already bowed out one year later (1991, 07, 99 sq.). Numerous chains had tested the device but ended up deciding not to roll it out. A supermarket in New Jersey decided to pull its ESLs after having tested them in 1988 (1990, 01, 63). In 2002, a survey showed that most retailers were unsatisfied with the available in-store technologies: ‘In general technology overpromises and underdelivers’, stated a chief executive (2002, 02, 52).

How could we explain these skeptical discourses and actual difficulties? An obvious explanation is the gap between the promises of the technology and what it can deliver in practical use. As with any new device, early ESLs faced technical flaws: ‘Some of the early failures of electronic shelf labels have been almost comical. There were labels that exploded upon impact with shopping carts, labels that attached themselves to the bottom of skids not to be found for months, labels that displayed test patterns seemingly at whim’ (1990, 01, 61). As a consequence of these failures, Progressive Grocer ranked ESLs twenty-seventh on a list of the new retail technologies in terms of CEO satisfaction, with only 20.2% of the few users who had tried the device considering it to be ‘satisfying’ or ‘very satisfying’ (2002, 02, 52). One of the main arguments against the technology was its cost and the resulting relatively long payback: In 1991, the unit cost was around $10 for a payback in at least 2.5 years. The investment was all the more problematic because it could appear unnecessary, since retailers ‘can get along with paper’ (1991, 07, 102). Between 1990 and 2010, many retailers saw innovations such as electronic payments, POS software or back-office applications as more urgent matters. Second, a lack of robust and standardized communication network seems to have weakened retailers’ confidence for the innovation. Third, another possible hypothesis is the application of item-pricing laws in the United States. This type of regulation – first introduced in 1970 in Massachusetts as a way to avoid discrepancies between shelf prices and checkout prices that could be unfavorable to the consumer – required retailers to stick the price on each product (Kjellberg et al., 2019). In 1991, item-pricing regulations were applied in seven states: Connecticut, Minnesota, Michigan, Massachusetts, Rhode Island, North Dakota, California, and New York (1991, 07, 100). ESLs were initially presented as a way to fight this regulation, using the argument that they could eliminate price discrepancies by electronically linking shelf price and checkout price. However, item retailers who worked in these states had little interest in implementing ESLs, given that they still had to stick prices manually on every product; until 2008, among states subject to item-pricing laws, only Connecticut allowed retailers equipped with ESLs not to mark every item (Bergen et al., 2008). Meanwhile, in other states, the investment in ESLs would have been seen as risky, given the threat of a possible item-pricing ruling or law.

All in all, the recent introduction of ESLs in the United States is marked by an enduring oscillation between hype and skepticism. ESLs and their promises were praised and then confronted with previous deceptive facts; optimistic discourses were reactivated and updated according to new improvements and related innovations. A striking pattern, however, is the repeated formulation of hopeful comments after the expression of disappointments. In 2002, the magazine noted that, despite the difficulties faced some years earlier, ‘there is life in ESLs those days’ (2002, 02, 14). Fourteen years later, similar statements were reiterated: ‘[ESLs] might not become standard fare in US grocery stores any time soon, but the pace at which technology is advancing suggests that even such futuristic scenarios may be plausible one day’ (2016, 01, 99); ‘no widespread deployment has taken place. That may change soon’ (Karolefski, 2016). In other words, if ESL manufacturers presented the device as a ‘path to the future’ (1993, 12, 22), the subsequent evolution has shown that this future has been an ever-delayed one: the future and its promises have been systematically announced and then postponed, as if the future were always escaping, but also as if one could not but give it another chance (see Figure 2). Year after year, informants expressed a modest yet stable confidence that ESLs were an important topic for the immediate future (next year) and an even more valuable topic for a midterm one (next three years), even if this latter figure shows a continuous decline. Everything looks as if ESLs work for retailers like the classic carrot for a donkey: Each time the donkey makes a step forward to get closer to the carrot, it moves the carrot farther away. But in these circumstances, the donkey gets tired.

In the remaining part of this article, we explore some more fundamental reasons behind the modest development of ESLs in the United States. We start by looking at the long-term history of price tags. We follow this by analyzing a recursive chronology, starting from the present and going back to the future of ESLs, step by step. This anamnesis will show what digitalizing really means: digitalizing price tags is about showing numbers (digits) with one’s finger (digitus), be it electronically or not (digital). If the former solutions succeeded in performing the same task, ESLs might be less radical than they pretend to be; as a consequence, moving to the so-called digital world (in the narrow sense or electronic) may be less necessary than it may seem.

Back to the future of ESLs: Exploring price tag patents and price tag history

The history of price display went from coded to open prices. Until the end of the nineteenth century, prices were hidden or sometimes manually encrypted on the bottom of products by grocers who could then bargain and adjust them for each consumer (Spellman, 2009). At the beginning of the twentieth century, however, prices began to be disclosed and displayed. This evolution paralleled the adoption of new merchandising techniques such as windowed showcases that favored a more direct interaction between consumers and the goods, which then came with the demand for open prices (Cochoy et al., 2018a). Price display devices proliferated in the form of various price cards and price tags. In a growing self-service environment, the technical challenge behind these innovations was to design cheap and practical systems able to display prices clearly and firmly so that consumers could read them but not move them, while also allowing grocers to easily change the prices quickly. The most successful solutions invented to solve this dilemma combined simple features, such as sets of interchangeable price cards, and subtle placement systems, such as ‘clamping’ and ‘swinging’ tags (Cochoy et al., 2018b). Because detailing the complete technical history of price tags would be too long, we propose a synthetic approach that combines a network analysis of US price tag patents starting in 1890, and a complementary knowledge of the surrounding history based on the systematic reading of Progressive Grocer from 1922 to date.

Method: A dynamic network analysis of the citations between price tag patents

We collected price tag patents using the Google patents search engine. We looked for all US patents having the expressions ‘price tag’, ‘price ticket’, ‘price card’ or ‘price label’ in their title. This search returned 328 items. With ad hoc scraping software, we harvested the complete raw text, PDF version, and citations of this population. We then performed a dynamic network analysis of the patent citations with Gephi, software that offers the necessary features for such treatment. The study of dynamic networks helps trace the gradual introduction of new technologies and how they relate (or not) to each other through cross-citations. However, it is important to stress that patents provide only a partial view of a technology. First, patents are literary proposals presenting virtual solutions; patents are generally badly performative because patent designers are good at developing novel ideas, but they are often bad at having them manufactured and marketed. As a consequence, most patents are dead on arrival: They fail at a commercial life after their publication and just remain as abstract corp(u)ses of technical knowledge buried in the large cemeteries of patent databases. Sometimes, one of these corpses is lucky enough to have one of its later fellows visit its grave and celebrate its memory by depositing a citation flower on the tombstone. But here again, this ritual remains in the limbo of the afterlife of technological souls. Second, the full collection of patents about a given technology is always smaller than this technology itself, since many innovators do not patent their inventions.

In our case, the systematic reading of Progressive Grocer over almost a century is a good way to (partially) overcome these two difficulties. Over the years, price tag manufacturers have largely and continuously advertised their goods in the magazine, sometimes by explicitly referring to the underlying patents. These ads help identify which solutions came to the market, which of them have been patented or not, and (by subtraction) which patented solutions went nowhere. Of course, some devices that were not advertised in Progressive Grocer may have been promoted or marketed elsewhere, and some devices advertised in the magazine may have failed commercially. This said, the position of Progressive Grocer as the main retail publication in the twentieth century ensures the presence of the main players of the price tag markets. Additionally, the visibility of price tag systems in real stores photographed in the magazine as illustrations confirms the circulation of many price tag solutions beyond the advertisements.

In the following pages, we focus on ESLs, but also on other innovations that prepared for or anticipated them. On the one hand, this approach is highly debatable, given its non-chronological character: Reading the past based on knowledge of the present tends to favor hindsight bias (i.e. the idea that the events that occurred were more probable than other possible outcomes that did not) (Fischhoff and Beyth, 1975). However, this approach will show that the project of developing price-tagging technologies has always been there and that innovators did not wait for ESLs to develop varied solutions to meet this objective. We can thus understand that innovative price display is less a matter of technical progress than a matter of technological agencement. What matters is to find the proper means and solutions to build compromises between an eternal concern – fixing prices by setting, hanging and changing them (Cochoy, 2018) – and various temporal conditions, such as working with the available technological resources, coping with cost constraints, and adapting to the existing legal and material retail environments. In other words, price tag solutions cannot be isolated from the available technologies and market surroundings. In this respect, an electronic price display should be considered just one element of many. Whether it represents the future is far from certain. To some extent, it paradoxically moves backward, diving back into the past. To understand it, let us first consider a picture of the complete price tag patent network as it appears in 2017.

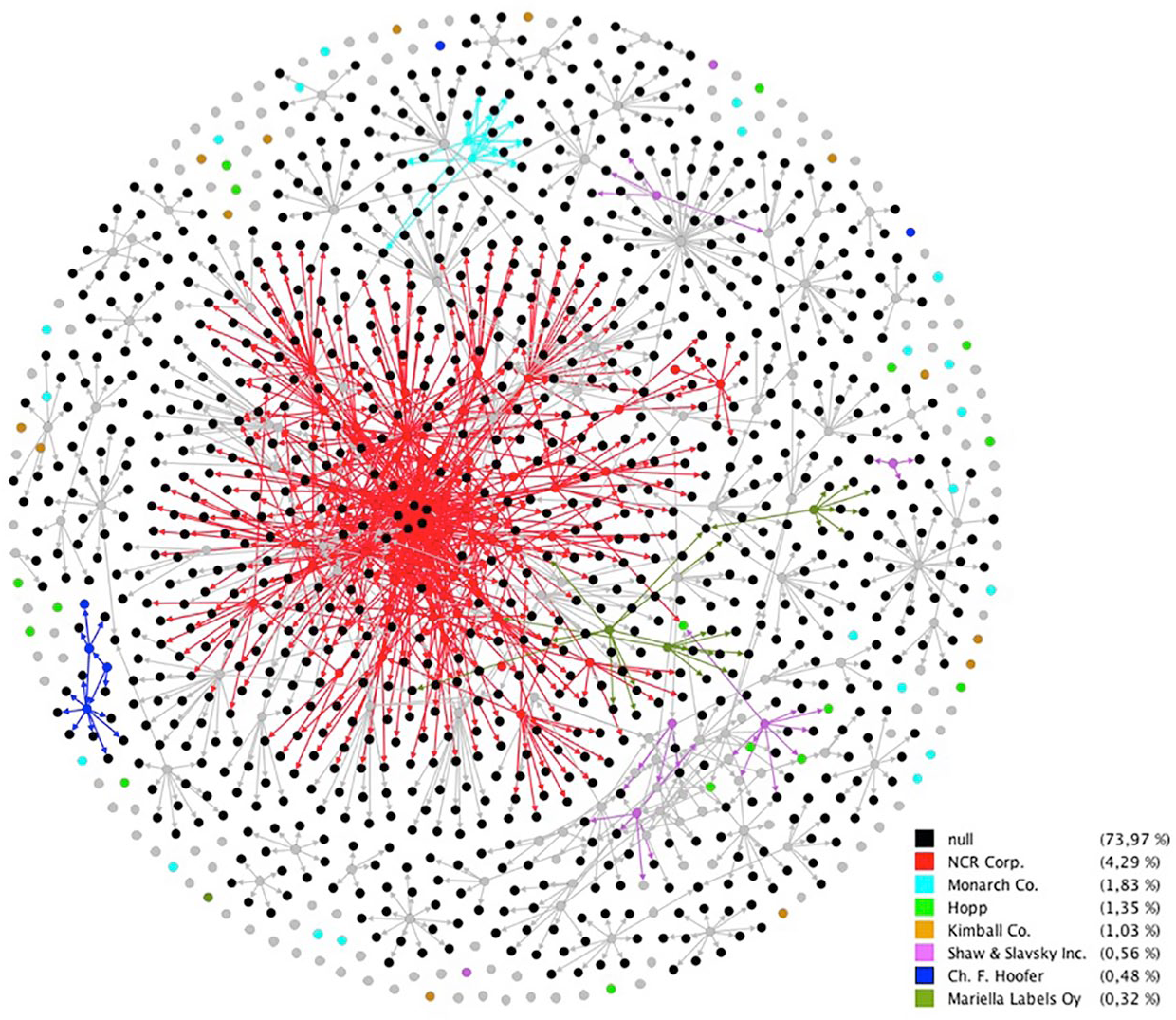

Figure 3 presents the complete citation network of price tag patents in 2017. The image gives the impression of a rich, populated, complex, and highly interconnected universe. The figure shows 1,260 individual patents and 1,575 citations between them, resulting in an average number of 10.6 citations per citing patent. However, a closer look shows that this richness is misleading. First, we note that almost 75% of the 1,260 patents are black dots (i.e. patents quoted by the original population but external to it). This means that when a price tag patent quotes another one, the quoted item is rarely another price tag patent but rather another resource it relies on, such as materials, parts, machines, and so on. Second, the network gathers a very small number of active players. Only 149 of the 328 patents of the original database (45.4%) quote 1,010 others, with a majority quoting none (54.6%). Among the quoting patents, there are few key players; the color scale refers to an oligopoly-like group of companies (Hopp, Kimball Co., Monarch Co., NCR, Shaw & Slavsky, etc.). Apart from Ch. F. Hoofer and Mariella Labels Oy, all of these companies have been regular, and sometimes massive, advertisers in Progressive Grocer (especially Hopp, Monarch Co., NCR, and Shaw & Slavsky), meaning that the most active manufacturers are also the ones who protect their products. At the periphery of the graph, we observe a high number of colorful or gray patents from the original population that quote no patent and that are quoted by none (179). When patents quote others, we note that the quoting paths are very short. The most frequent patent citation structure is by far the star-like one, which is a characteristic of ego-centric subnetworks: at worst, a price tag patent quotes only external resources without paying any attention to similar technologies; at best, when the citation paths become longer, the quotations are often restricted to patents issued by the same company, as in the red cluster of NCR patents, the light blue cluster of Monarch patents, the pink cluster of Shaw & Slavsky patents, or the dark blue cluster of Ch. F. Hoofer patents. Here, 218 self-citations among the patents of a same assignee are made over the total of 1,576 citations, representing a high percentage of 13.8%. Given these first observations, it seems clear that the population of price tag patents is far less interconnected than it first seems.

The complete network of price tag patents. For readers of print versions of this article, please see the online version for color figures.

To confirm this impression and obtain a clearer view, it is worth performing a threefold operation. We propose first eliminating all irrelevant information that obscures the picture, then examining the red population of NCR patents, and finally studying how the network evolved over time to unpack the simplified web of meaningful citations and identify how this web changed.

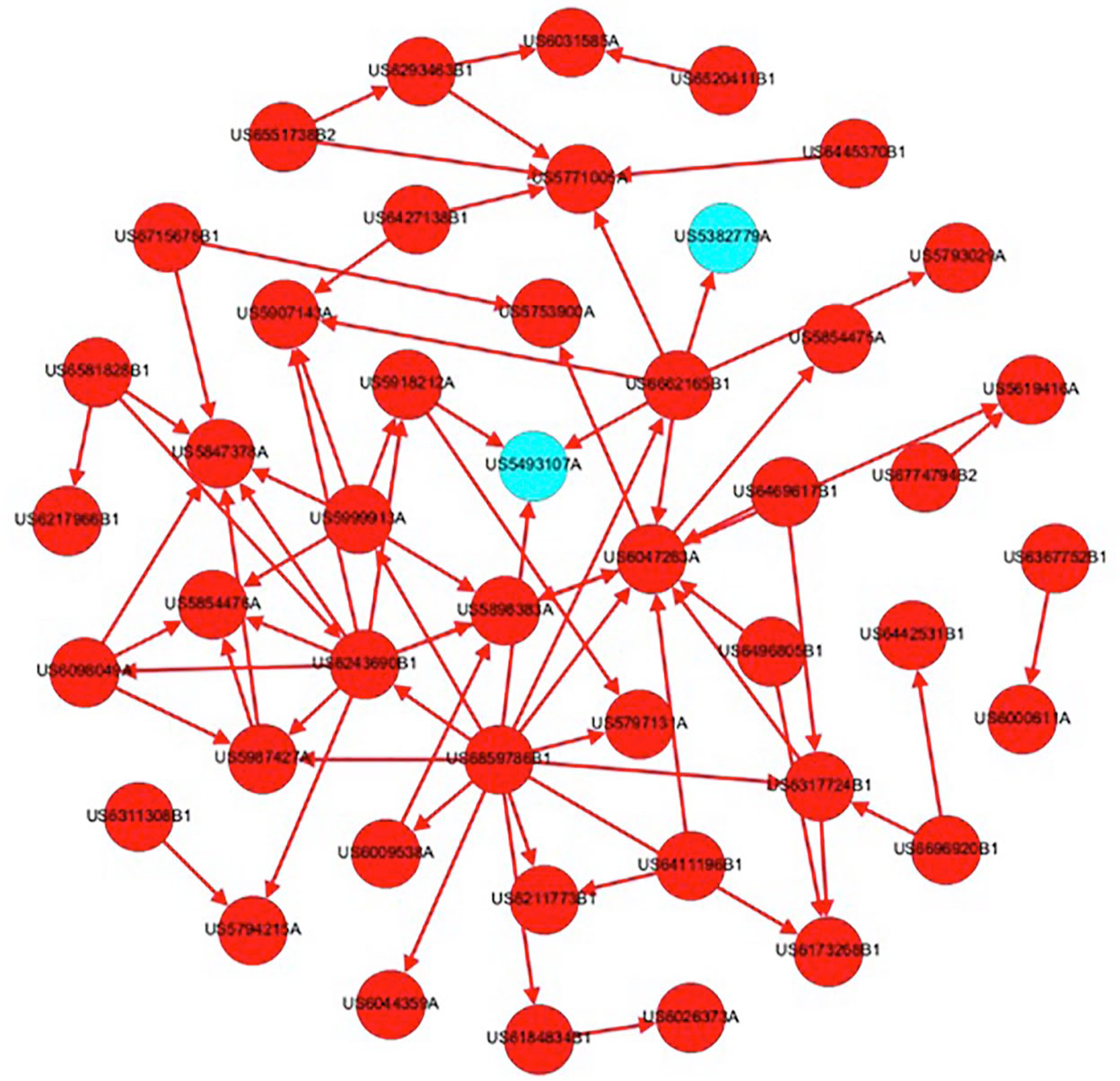

There are three types of irrelevant information. The first type is made of ‘patent outsiders’ (black nodes) that relate to other technologies than price tags per se. Eliminating them means adopting a complete network approach, where one observes only how price tag patents from the original complete population quote each other. The second type of irrelevant information is made of patents that do not quote any other. Filtering the network according to these first two criteria ends up in a drastic reduction. There is almost nothing left, except for 55 patents and 122 citations between them. The third category of irrelevant information is the self-citations defined as quotes between different patents but belonging to the same assignee. These citations are a large majority, representing 76 of the 122 total (62%). Eliminating them eventually results in a network of 47 patents and 46 citations between them. Before analyzing this residual network, let us look at the NCR subnetwork (all patents quoted by NCR, with self-citations and outsiders included, Figure 4).

NCR patent network.

We already know that the red cluster of NCR patents dominates the general network. Apart from three earlier patents from the company, all these patents are about ESLs and were introduced in 1997 and after. Among the 74 citations made by the 54 NCR citing patents, 70 are self-citations to patents from the same company (94.6%), be they about price tags or not, meaning that all the black dots quoted by NCR could have been colored red as well. The four citations made for patents external to NCR refer to two patents from the Digicomp Research Corporation (5.4%). These patents are not any price tag patents: they both belong to the field of digital display and present two different versions of the same barcode reading system (Pat. no. US5382779A, January 17, 1995; Pat. no. US5493107A, February 20, 1996). In other words, even in rare cases where they quote other price tag devices, the NCR patents restrict their references to very recent digital systems.

The lesson is clear: NCR enters the field of price tags without paying any attention to the previous history of these devices. The proliferation of NCR patents amounts to the well-known strategy called ‘picket fencing’, which aims at building ‘patent thickets’. This strategy is widely used in high-tech industries such as electronics. In such fields, companies create large collections of overlapping patents to discourage competitors from entering their market. Indeed, such thickets make it extremely difficult to identify who controls which right (Guellec et al., 2007; Von Graevenitz et al., 2013). All in all, the NCR cluster appears dramatically disconnected from the historical population of price tag patents. Digital price tags present all the characteristics of a world in itself: disconnected and isolated, as if it had nothing to do with the previous generations of similar technologies. Everything happens as if NCR, despite its long and even foundational presence in the field of retailing (Spellman, 2009), was pretending to be a complete outsider in the price tag business and as if its ESLs were not commensurable with anything that preceded it but instead introduced a radical shift, a discontinuous innovation and a technological revolution.

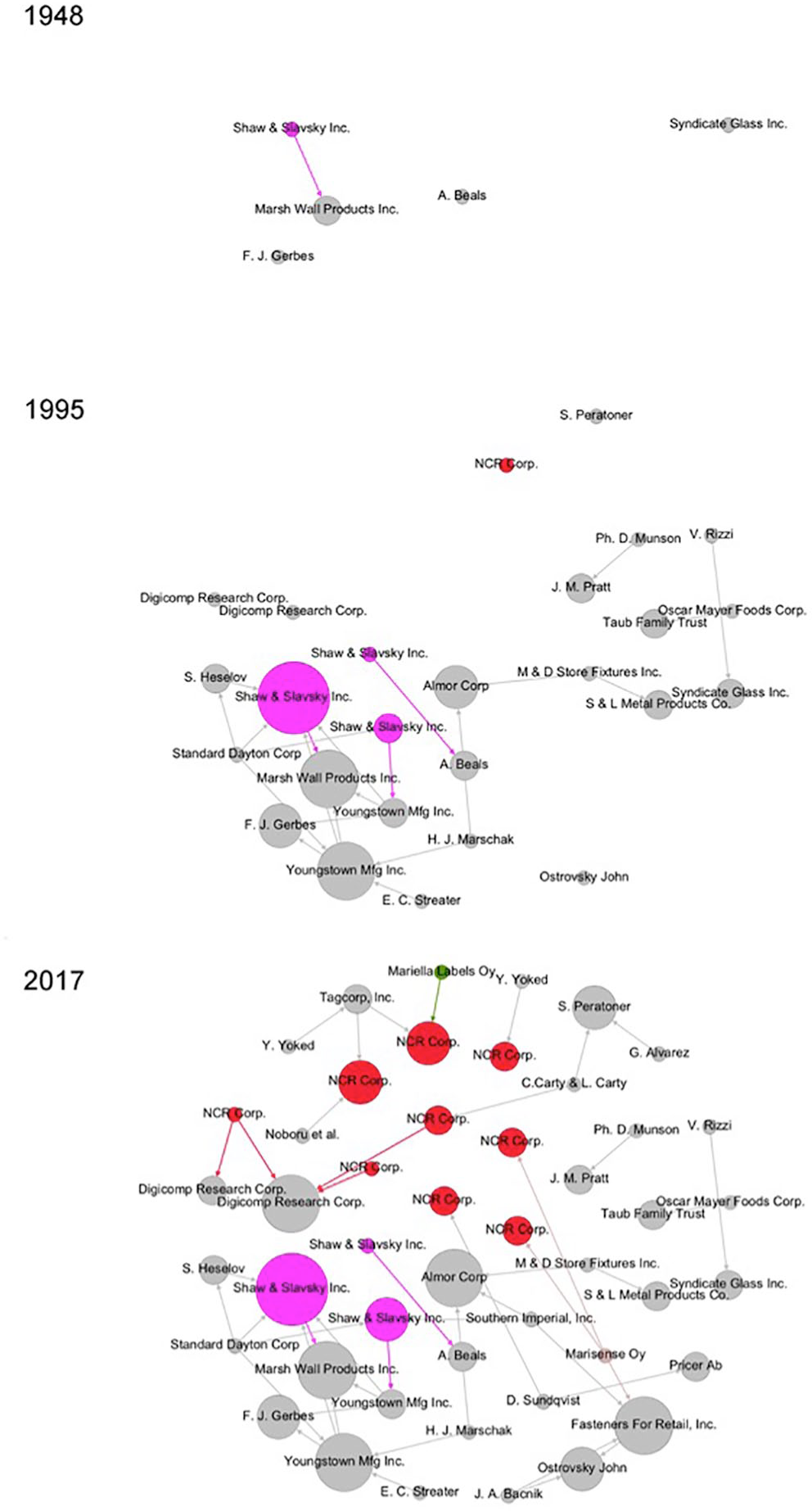

However, we must ask if this makes sense. To better see how ESLs fit (or not) with their supposed non-digital parents, we propose moving from the static analysis of the present patent network to its dynamics; this approach will show how different innovators paid attention (or not) to others. Figure 5 offers three snapshots taken from the continuous transformation of this web of patent citations over time. The chosen dates are 1948 (the appearance of the first cross-citation between two price tag patents), 1995 (the introduction of the first NCR ESL patent), and 2017 (the present). From one snapshot to another, each patent remains in the same place over time. The size of the nodes increases depending on the number of received edges, and to make sense of these data, we propose relying on two opposite strategies.

Dynamic network of price tag patents (snapshots: 1948, 1995, and 2017).

The first strategy involves looking at the graphs along a Weberian comprehensive approach to identify patents and citation patterns that mattered for the actors. Observing the three snapshots first shows that the patent citation is a late practice. The first cross-citation appears in 1948, after 73 years of development (the first price tag patent was filed in 1875) and after the filing of 180 preceding patents (i.e. 54% of the complete population). This pattern is analogous to what can be observed in the scientific literature: the increasing pressure of competition and the growing symbolic value attached to public exposure led actors to increasingly refer to each other and lengthen their reference lists (Bornmann and Ruediger, 2014).

A second strategy mitigates the first. If the number of cross-citations increases over time, then it has remained surprisingly small. And even this small number of citations is less meaningful than it might seem, since patent citation is largely a forced process imposed by patent examiners who suggest which patents should be quoted. As a consequence, it is uncertain whether patent designers really paid attention to the references made at the bottom of their texts. This probably relates to the price tag technology itself. Most price tags are ‘low-tech’ devices and, more importantly, they are devices whose construction is publicly accessible. These two characteristics favor easy reverse engineering and consequently led many price tag developers to pay less attention to the underlying literature. Two other results stem from the observation of the patents and citations that remain in the network. First, unfolding the dynamic network clearly confirms the lack of continuous citation paths between the most recent patents and the oldest ones. In particular, there is a clear disconnection between classic price tag patents and ESLs patents, as if they have formed two separate generations. If, as already noted, NCR patents quote none of the previous generation and NCR patents are quoted by other companies, then these patents are all about ESLs and would quote no patent of the previous generation (see the periphery of the 2017 map: patents from Mariella Labels Oy, Marisense Oy, Noburu et al., Tagcorp, Inc., Y. Yoked). Second, and unsurprisingly, some of the main price tag manufacturers, such as Shaw & Slavsky and Youngstown Mfg Corp., who have heavily and regularly advertised in Progressive Grocer, are present in the network and repeatedly quoted by other players. Indeed, the companies that care the most about the technology patent their products, pay attention to the related literature, and receive attention from their competitors (but this is far from being an absolute rule, as seen in the case of Hopp Press below). Last but not least, the number of influential patents is limited, and this influence is modest: Over the years, only five patents have received at least three citations and none received more than four.

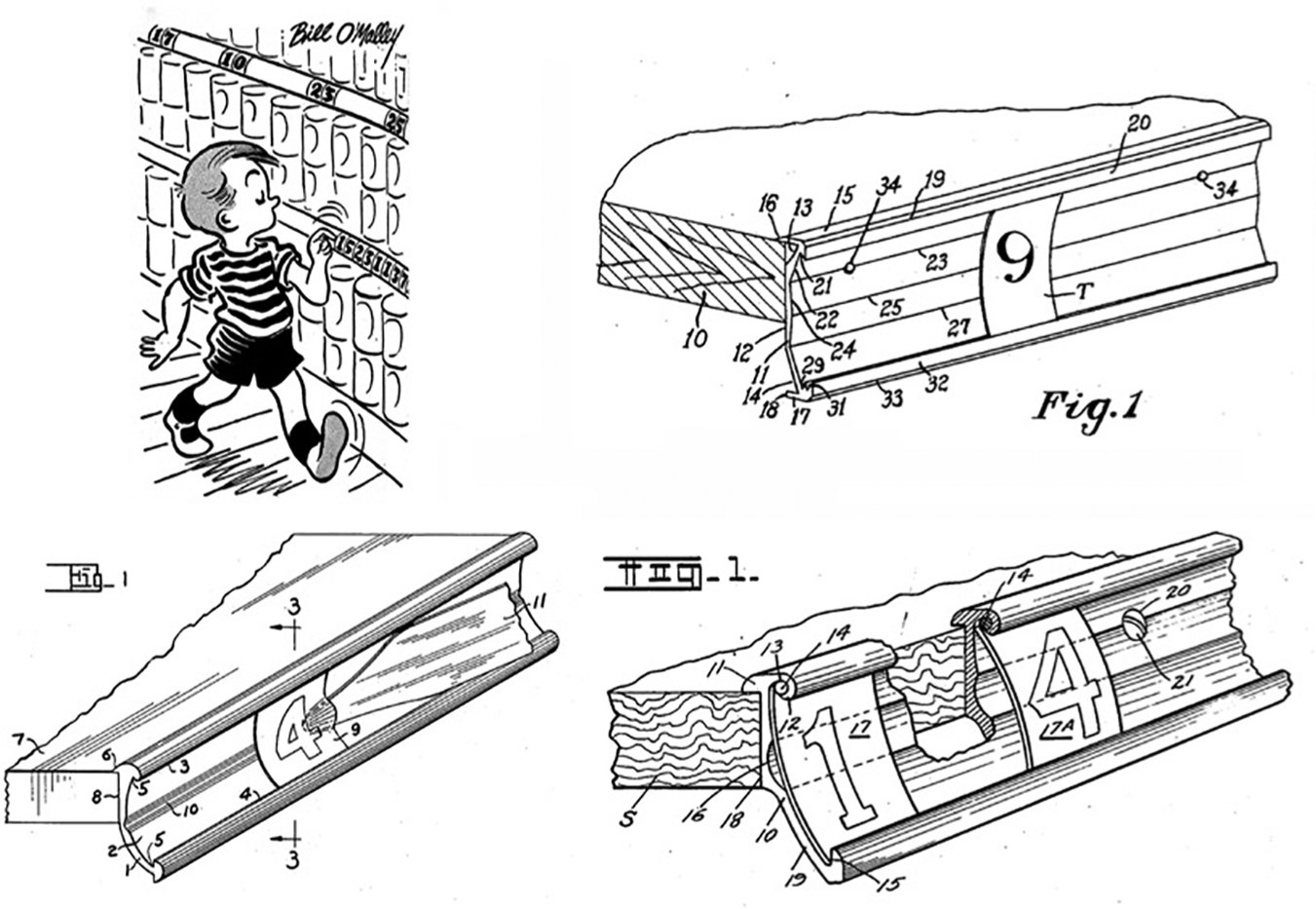

It is highly significant that all the most-cited patents focus on the proper ways to fix either price tickets on the price rail (said ‘molding’) or the rail itself on the shelf. In other words, these patents make it clear that price tag technology is foremost about addressing a fundamental and permanent dilemma: prices should be easily changeable when needed (to implement pricing decisions and save grocers’ time, effort and money) and firmly attached once applied (to avoid them being removed or displaced accidentally or by indelicate consumers, notably children, see Figure 6). This pertains to the ‘digital’ dimension of price tags: Because price tags can be manipulated with fingers, it becomes of utmost importance to discriminate between the fingers of consumers (that must remain powerless) and the fingers of market professionals (that should be able to adjust prices as smoothly and quickly as possible). Developing an appropriate solution for this problem means creating for price tags what binders are to skis: the device should be easily open or firmly closed, depending on the required conditions.

Top left, Progressive Grocer (1946, 10, 182); top right, Marsh Wall products, US2489089A, November 22, 1949; bottom left, Shaw & Slavsky, US2507937A, May 16, 1950; bottom right, Youngstown Mfg Inc., US2608777A, September 2, 1952.

The first three patents of this sort were published within a very limited time frame, between 1949 and 1952, and offer highly similar solutions. The two other most-cited patents appeared later and are of secondary interest: they focus not on price tags per se but rather present easy ways to hang and remove the entire molding, one for classic price tags (Almor Corp., US2950554A, August 30, 1960) and the other for ESLs (Fasteners For Retail, Inc., US6553702B1, April 29, 2003). We will disregard these two patents and focus on the first three.

The problem to solve is well staged by the first of the most quoted patents, as follows: The invention relates to molding adapted to be attached to the edge of a shelf in a grocery store … and adapted to removably hold price tags or tickets designating the price of the goods displayed upon the shelf … there are certain objections to such moldings, one of the greatest difficulties being that they do not hold the price tags firmly in place. This causes considerable trouble and annoyance to merchants as price tags may be either accidently or intentionally slidably moved from one position on the molding to another so as to erroneously indicate a lower price for a higher priced article. Great confusion is frequently caused by children removing or changing the positions of all or a great number of the price tags. … The present invention therefore contemplates the provision of a price tag molding which will overcome the above mentioned objections and difficulties. (Marsh Wall products, US2489089A, November 22, 1949)

Marsh Wall’s patented solution consists of designing a molding ‘having longitudinal grooves near opposite edges of its front face for receiving the upper and lower edges of a price tag’. On the one hand, the concave structure of the molding secures the position of the tag when clipped: ‘the flexible price tag will bow inwardly and lay against the central high point 25 of the molding … the tag being held firmly under compression so that it cannot be slidably moved in the molding.’ On the other hand, the void between the curved tag and the angles between the flat segments of the concavity ‘[permits] a sharp instrument, such as a pointed knife blade or the like, to be inserted behind the price tag at one of these points to remove the same from the molding’ (Marsh Wall products, US2489089A, November 22, 1949). Shaw & Slavsky and Youngstown focused on the same problem and proposed highly similar solutions, although, of course, the engineers stressed the differences of their patent. They allude to their competitors, point the drawbacks, and praise the newness and advantages of their own distinctive contributions. Shaw & Slavsky introduced two novelties: a transparent film that secures the placement of tags and a special tool to remove them. Youngstown’s alternative consists of inserting a ‘resilient material such as rubber’ behind the tags to prevent them from sliding.

But what the patents focus on sometimes matters less than at what they do not directly point. The most interesting feature of the three patents is that they all implicitly refer to the same way of displaying prices, where showing the prices consists of selecting tags with preprinted single numerals and combining them laterally on a rail. In other words, they acknowledge that modern price display has always been fully digital: It is about selecting digits among 10 discrete possibilities and gathering them in the proper order to display – with one’s fingers – a desired price. At first sight, this remark seems tautological, since price tags are about prices, and prices are made of numerals. But a closer look shows that combining cards with printed numerals drastically limits how goods can be qualified on the shelves. The set of cards focuses the tags on prices only, with little possibilities to complement them with qualitative information. Indeed, writing other information with the same system would require too many cards – there are 10 digits but 26 letters – and, more importantly, too much space on the shelf – in most cases, writing a word would require more space than the width of the package display. As a consequence, the technology of tag combination has long introduced a division of labor between manufacturers and grocers. Whereas the first can deal with quality by printing information on the product’s package, the second must care about prices only.

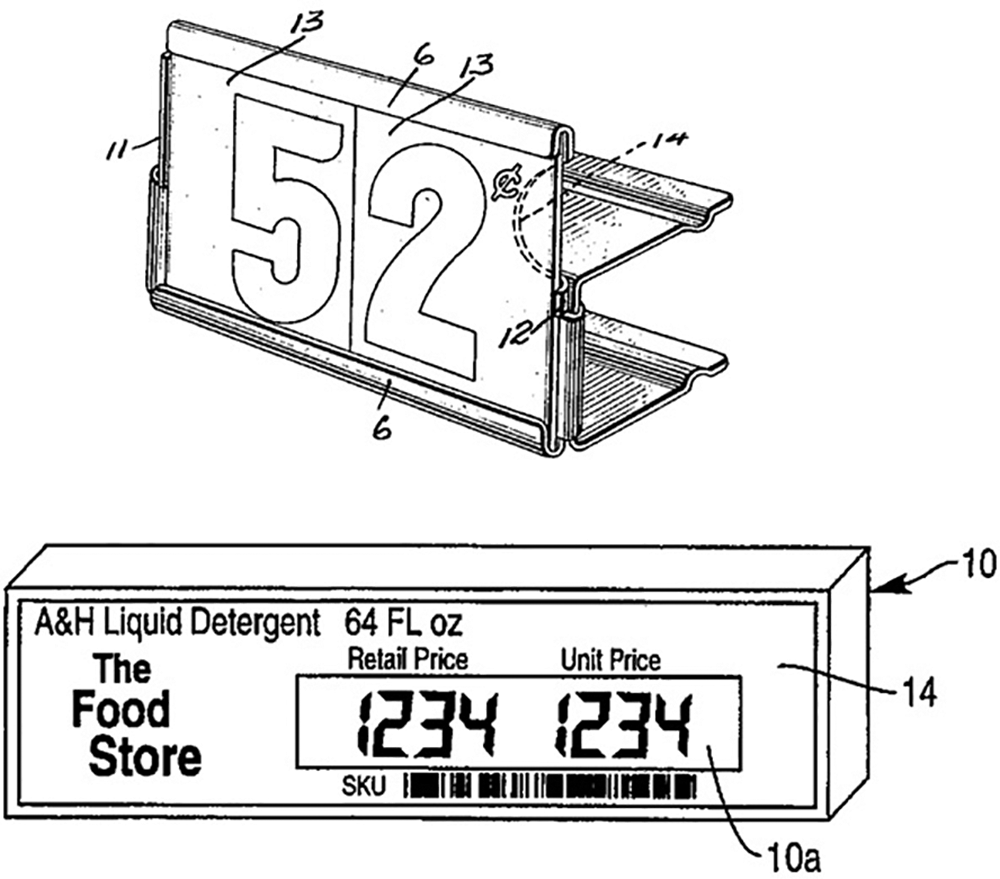

This division of labor can be traced back to one of the very first price tag patents, one of which was introduced by the Hopp Press Company. Hopp Press invented the price ticket approach, as shown in Figure 7. This patent is a milestone in price tag history, but is it part of the dynamic citation network? The answer is no. The Hopp Press patent is one element of our original population, but however important it might have been, it is also part of the uncited patents we have eliminated. Accounting for these patents moves us to our second research strategy. If the first research strategy is about following the graph, the second strategy relies on the whole population of patents and on our knowledge of the price tag market to see if the patents that (could) have mattered have been overlooked and then to consider why. Several such patents exist, and the fact that they have been ignored deserves attention.

Top: I. and H. Hopp, patent no. US1398782, November 29, 1921; bottom: NCR Corporation, patent no. US5619416, April 8, 1997.

The oblivion of Hopp Press’s patent does not mean that the latter has not been influential – it is rather to the contrary. It just illustrates the strength of the reverse engineering process we mention above: The price-ticket combination approach could be easily identified in stores where the solution had been implemented and duplicated without referring to the underlying patent literature. We may even wonder if it is not the huge success of Hopp Press and its original solution (with Shaw & Slavsky, Hopp Press has been one of the main price tag advertisers in Progressive Grocer) that paradoxically explains this omission. The device has been considered generic and dominated price tag technology until the 1980s, resting along a path dependency process where any given improvement paradoxically reinforced the underlying structure of price tag tickets and moldings. Now, we would like to stress the puzzling parenthood between Hopp Press’s original price tag and ESL technology (Figure 7).

Hopp Press’s patent introduced both price ticket combination and the insertion of price tickets into an appropriate holder. As a consequence, price displays ended up as displays of prices only. In 1997, NCR published its first ESL patent. Paradoxically, despite the huge temporal gap – 76 years – strong similarities exist between the two. Instead of leading toward the future, electronic displays brought retailing back to the past, because with the segmented technology of early liquid crystal displays, the only changeable information were numerals, like with Hopp Press tickets. Moreover, the graphic aspect of electronic numerals was far behind the clear and elegant fonts of the early twentieth century! Of course, the full NCR device was more sophisticated than Hopp Press’s price ticket holder, since it complemented numbers with qualitative information. However, it is important to stress that NCR’s ESLs partly reiterated the division of labor between qualitative and quantitative information described above. On the one hand, with the NCR device, the grocer could now adjust prices electronically and also complement them with qualitative information. On the other hand, controlling prices and quality was still asymmetric: If the prices could be adjusted automatically, the qualities would remain fixed at the periphery and displayed with classic paper stickers stuck around the screen, and whose (re)placement took much more time and effort. As a consequence, chances were great that, as before, grocery management would first focus on prices and – to some extent – give back full control of quality to manufacturers.

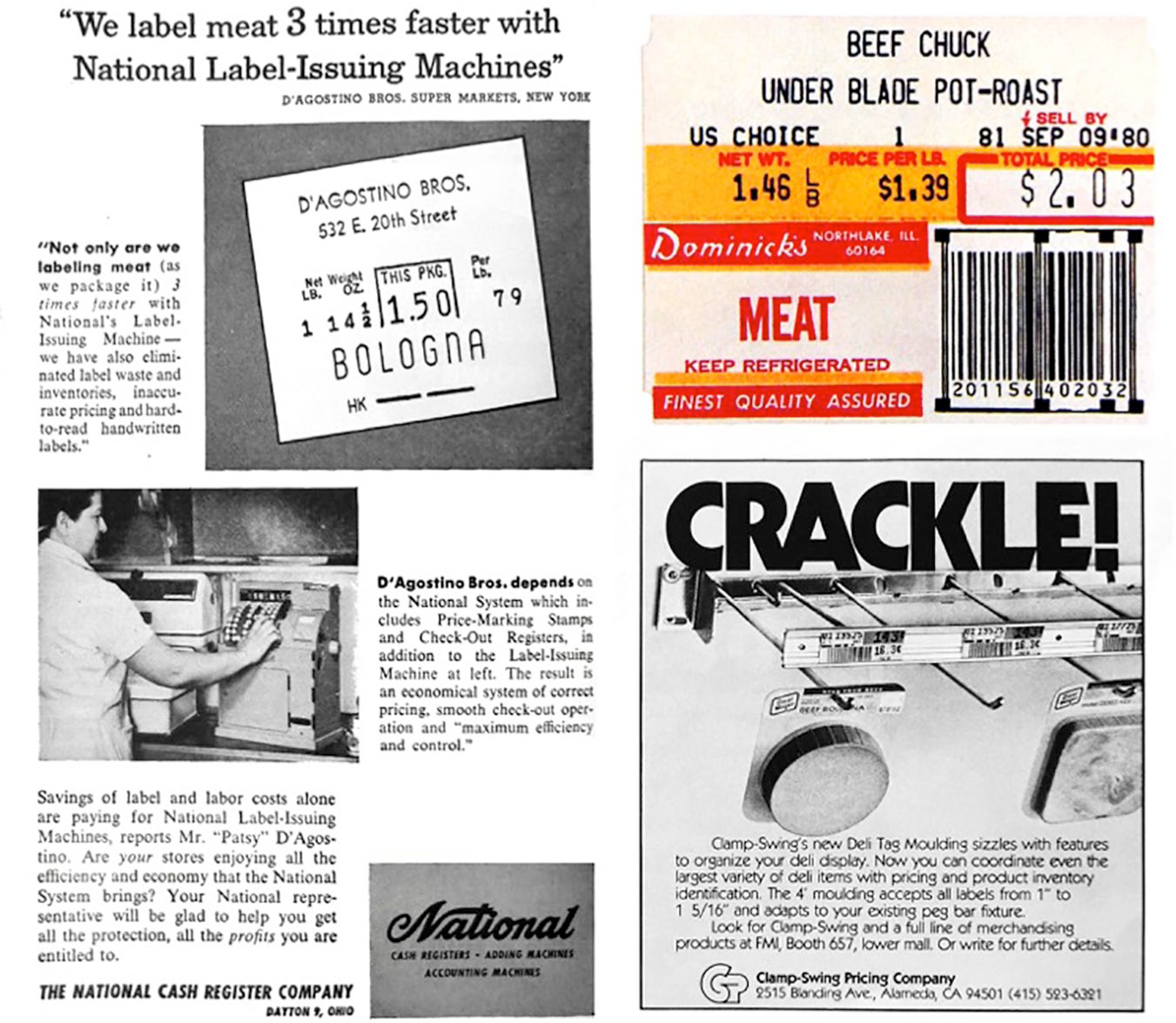

Quality control was indeed given back because between Hopp Press and NCR, another evolution had occurred: the replacement of price tags by paper stickers. These paper stickers represented a progress that ESLs came to partially ruin. The intermediary innovation appeared after World War II, when cellophane, new glues, and printing technologies merged, thus favoring the new business of prepackaged goods. With prepackaging, retailers for the first time received full control over qualities and prices, thanks to the pasting of printed labels where they could describe the goods and price them, all while doing it symmetrically, that is, with an equal ease and attention (Figure 8, upper right). In the 1980s, the stickers migrated from the prepackaged goods department to the other aisles of the shop and replaced classic number-only price tags with full price-quality information (Figure 8, lower right). The irony of this evolution is twofold. First, the price sticker technology was largely developed and promoted by NCR itself, which designed and sold prepackaging machines with the view that anything that could secure the consistency of the price chain within the shop was good for the business of cash registers. These machines introduced a new and easier type of ‘digital’ price display system, in the Latin sense of being connected to fingers. With these devices indeed, retailers had simply to dial prices with their fingertips, instead of tediously removing and combining price cards as before (Figure 8, left). Second, it is clear that the contribution of NCR’s ESLs to the subsequent evolution of price display involves losses. It reduces finger-handled operations to the minimum, because innumerable prices are changed at once, by simply selecting them with a click of the index finger on a computer screen. But by reintroducing an asymmetry between instant price changes and delayed quality information, ESLs are far less flexible in terms of product qualification than printed stickers.

Left: NCR Label-Issuing (1952, 08, 28); upper right: (1980, 11, 59); lower right: (1981, 05, 95).

If the Hopp Press patent belonged to the category of forgotten patents that nevertheless had a tremendous impact because of their commercial success, imitations and improvements, other patents are then members of a less fortunate family of forgotten patents that (to our knowledge) were not marketed, copied, or even noticed. We close our account with the resurrection and celebration of three such unknown soldiers lost in the field of the century-long price tag battle.

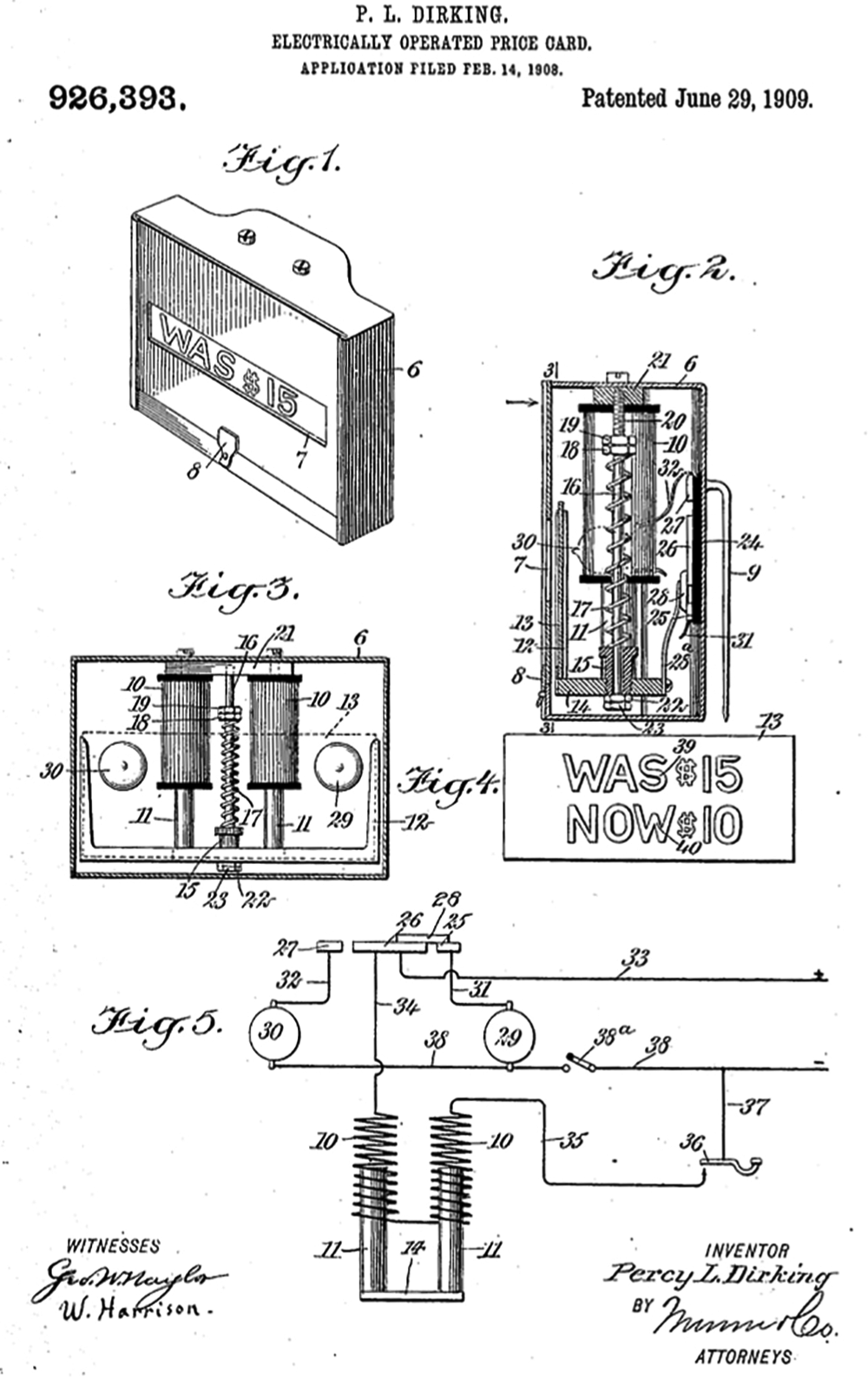

The first patent of this sort was issued in 1909 (Figure 9). This patent is extremely innovative, both economically and technologically; it is one of the very first price tag patents, and it relies on electricity at a time when electric grids were just in their infancy (Bakke, 2016). Better than contemporary ESLs, this ‘electric shelf label’, made continuous use of self-powered instant price changes. By means of an astute mechanism, it proposed to alternate the display of two translucent backlit price cards, for instance, to outline a promotion (‘was $15’ vs. ‘now $10’).

P. L. Dirking. Electrically operated price card. Patent no. US926393, June 29, 1909.

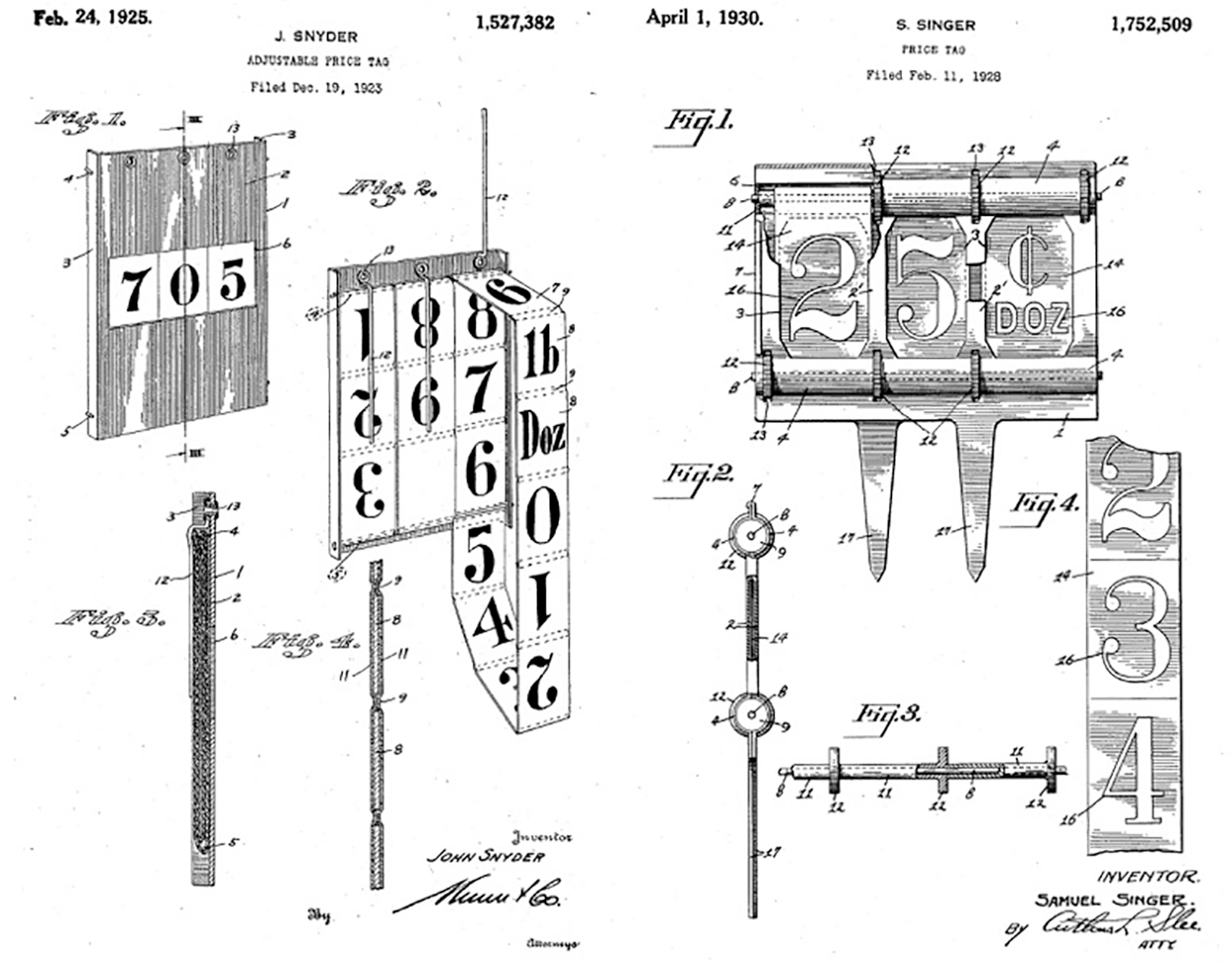

The two other patents were proposed in the 1920s. Even if they were not electrically powered devices, the logic behind them was surprisingly close to that of contemporary ESLs. Both proposed ways to adjust prices without using any other means than the device itself: like with ESLs, all the needed signs were internal, and nothing was added from the outside. The first patent did so through the rotation of a plurality of bands displaying all the needed numerals through an appropriate window (Figure 10, left), and the second patent proposed ‘a plurality of webs bearing price marking characters … arranged to be independently wound onto pairs of mounting reels to display desired characters’.

Left: J. Snyder, Adjustable price tag, patent no. US1527382, December 19, 1923; right: S. Singer. Price tag, patent no. US1752509, February 11, 1928.

Once again, history proves to be ironic. What is closest to ESLs is what has never been acknowledged by them. No ESL patent quotes its closest ancestors and what never went on the market; we have seen no advertisement, no paper on, and no pictures of these devices. Of course, several hypotheses can be evoked to explain such failure. Being designed by individual innovators without the support of companies, these inventors may have lacked the financial and social resources needed for their development. More certainly, the clumsiness, complication, and – more importantly – cost of each device may have hampered their successful development. Moreover, each of the first patents and the pair made by the two others control half of the problem: the first is about automatically displaying signs with an electric signal, but the signs are fixed; the others are about shifting numbers, but the shift is done manually. Contemporary ESLs have succeeded in articulating the two. ESLs have also succeeded in miniaturizing self-price adjusting devices at a reasonable cost. However, this is not enough to present them as the end-result of a long history. They also have their drawbacks: For a long time, segment LCD displays brought ESLs back to the age of ‘price only’ tags. New ‘electronic paper labels’ solve this issue, but their cost is problematic, as is their black and white appearance, which fits badly with the colorful environment of contemporary supermarkets. More importantly, ESLs have to cope with the competition of paper labels, which are much cheaper, much more attractive, much more flexible in terms of size and design, and whose continuous presence compromises one of ESLs’ main advantages: the possibility of adjusting prices quickly. Indeed, when prices are duplicated throughout the store, the speed of a price change cannot but adjust to the slowest media (i.e. the paper one) (see Figure 11 and Soutjis et al., 2017).

Paper price labels, New York, April 2016, © Franck Cochoy.

Concluding discussion

If patents that matter have been forgotten, if technical innovations rest on reverse engineering, and if new solutions do not pay any tribute to their ancestors, does it mean that these patents are pointless? The history of price tag patents shows that the effort to engineer fast and easy price-tagging devices has been there from the start while also showing that addressing this effort has followed an erratic trajectory, with little concern for what preceded, except in the form of the path-dependent renewal of some basic features, such as price tickets and shelf moldings. Throughout this history, we can see that the digital, in the sense of electronic, was preceded by the digital, in the sense of numerals (digits) manipulated by fingers (digitus). And we can understand that these early meanings of the digital are still embedded in contemporary solutions and thus explain part of their difficulties. Prices cannot be reduced to abstract electronic figures, are still defined and manipulated with fingers, and are a part of a hand-operated material environment made of numerals but also qualitative signs.

The success of innovations is a problem of timing and environment. Technologies do not come in isolation, but should fit with wider contexts, systems, and infrastructures – or ‘market agencements’ (Callon, 2016). In fact, innovation is more the expression of a material web than a matter of single inventions. Successful novelties fit with previous innovations and push them further. According to this view, we should abandon linear and progressive views of technology. For instance, ESLs can be presented as the future of paper price tags … or vice versa, as the recent proliferation of paper stickers in US supermarkets shows (see above). New technologies do not simply replace old ones, but rather there is a combination process that gathers various resources, constraints and devices. ESLs succeed at articulating solutions that rise from the past: they brilliantly prolong and value barcodes and data centers at the shelf level (Kjellberg et al., 2019), but other solutions of yesteryear are still there and succeed in hampering ESLs, perform better than them, and so on.

More precisely, our results show that the spread of price tags takes the dual form of path-dependency and what we propose calling an ‘interlocking pattern’. New features paradoxically recycle previous schemes and reinforce them (see how the introduction of easy price-locking systems reinforced classic price tags and price tag moldings). Our anamnesis also unveiled amnesia. Indeed, history proved to be less a matter of cognitive memory than a matter of material traces. The temporal links between technologies do not take the shape of networks but rather that of machineries. A network is like a flexible web (it rests on embedding immaterial relationships), but a machine is like a jigsaw puzzle: new elements have to fit exactly with the previous design (it rests on interlocking tangible entities). Technologies interlock with the past but also with existing devices. It is in the retailer’s best interest to associate the different tools he or she may count on if he or she wishes to get the most out of them. In this respect, innovation is a sideways movement: the current in-store digitalization and the peripheral innovations that gradually invade the retail sector (smartphones, beacons, POS systems, etc.) are likely to have effects on the retailer’s interest for ESLs, provided that what interlocks with current infrastructures also fits with older ones. But this is not an easy matter.

The jigsaw puzzle of price display technologies is a complex and dynamic one, made of pieces whose nature and shape evolve constantly. Often, actors evaluate the changing costs of these technologies and their promises in terms of savings and profits: brilliant, functional, and innovative devices have little chance to succeed if the same effects can be obtained at a lower cost or if the cost is higher than the payback, all the more so that costs are immediate whereas benefits are postponed to an uncertain future. This constraint probably explains the failure of the most sophisticated price tags of the early twentieth century, as well as the difficulties met by the latest technologies such as ESLs, electronic paper, or RFID chips. Other changing pieces of the puzzle are legal rules. What technology can or cannot do is heavily framed by external rules, as we saw with the item-pricing regulation in the United States. When goods have to be price-marked individually, the need for instant shelf price display decreases dramatically. Last but not least, evolving social configurations also take part in the overall agencement: The digitalization of the food retail market sector is linked to the advent of new forms of marketing and consumer practices.

All in all, the history of ESLs tells a lot about the technological dimension of prices. Price valuation is not just a matter of hydraulic-like adjustments between supply and demand, as economists think; it is not just a matter of managerial decisions, as management theorists believe; it is not just the expression of cultural, structural, and relational frameworks, as sociologists pretend; and it has not become just a matter of digital speed, as contemporary engineers dream. The history of ESLs shows that digital price displays depend on past and present systems and infrastructures, cost constraints and payback schemes, legal frameworks, and human behavior. The same history also shows that equipment providers play a hidden yet decisive role and that their contribution to the definition of what a price is (or is not) deserves to be made public beyond the well-known but somewhat secondary contributions of socio-economic forces and managerial decisions.

Footnotes

Acknowledgements

We warmly thank Progressive Grocer for granting us permission to reproduce some of the images this article refers to. We owe a lot to the librarians of the New York Public Library. We are very grateful to Michel Callon for his precious advice on patent literature and Béatrice Milard, Guillaume Favre and Michel Grossetti for their invitation to present an earlier version of this article at the Savoirs, Réseaux and Médiations seminar of the SMS Labex, and for their helpful feedback. We are greatly indebted to Sergio Sismondo, Stephen Turner and the reviewers of Social Studies of Science for their helpful advice, comments and suggestions. We also express our deep gratitude to Guillaume Brocard, Guillaume Cabanac and Mario Vieilledent for their invaluable IT contribution.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Financial support was provided by The Swedish Research Council, project Digcon, i.e. Digitalizing consumer culture (Grant number 2012-5736) and the Labex Structuration des Mondes Sociaux (ANR-11-LABX-0066).