Abstract

This article explores the development of statist transnational capitalism in China by examining the economic activity of large state-owned economic units in energy, finance and manufacturing and their relationship to other transnational capitalists through links in foreign direct investment, joint ventures and stock investments. It also analyses the divisions within China between the neoliberal export sector and the neo-Keynesian transnational fraction that advocates higher wages and more internal consumption, and how this links to other fractions of the transnational capitalist class globally.

Keywords

Will China rule the world? Or, more precisely, will the class that rules China rule the world? It’s an important distinction. The class question turns our attention to transnational capitalism, while posing the question as ‘China’ asserts the primacy of nation states in international relations. Most students of China take a nation-centric viewpoint, and western observers constantly worry about the changing balance of power. But if we take the class approach to China’s global economic integration, we find a transnational capitalist class with Chinese characteristics.

In analysing the ruling class, we can identify different power networks that interconnect and often overlap. These networks divide into four nodes. The most important sector is the capitalist class, those who own and control the means of production and, to a large extent, determine the relations of production and the relations of power between classes. The political elite are responsible for the state and can moderate the relations of production, guide social and environmental reproduction, regulate production and, through state ownership, control essential aspects of the physical and social infrastructure as well as determine the economic conditions for public workers. The governing elite also include the political and technocratic leadership of transnational institutions such as the World Trade Organization (WTO), International Monetary Fund (IMF) and World Bank. The military-industrial complex (MIC) should be considered a separate network of power, a hybrid of the state and war industry with an internal culture that sets it off from other institutions. The fourth network lies within the cultural and ideological sphere, which includes media, entertainment, thinktanks, public intellectuals and academics.

What is unique to China is that all networks are tied closely to the state and therefore constitute a statist transnational capitalist class (TCC). China is not alone in this transnational statist formation, 1 but it is the most important and influential model. There is also a vigorous private sector that has produced more billionaires than anywhere except the US; 117, according to Forbes. But 117 individuals don’t constitute a ruling class – perhaps in Monaco, but not in China. However, before plunging into an analysis of the Chinese TCC, we need to discuss the relationship of the transnational economy to the nation state.

The central dialectic in the present era is the ascent of the global economy and the descent of national economies. This is a complex process, played out over an extended period of time, with as many variations as there are nation states. The political economy of globalisation is characterised by an array of developments. Some of these include: foreign direct investment (FDI); cross-border acquisitions and mergers; cross-border stock investments; the growth of foreign affiliates; outward-bound capital from sovereign wealth funds; global assembly lines and value chains; joint ventures and joint research and development; the growing network of global cities; and the composition of corporate boards. When national economies were dominant, the majority of a corporation’s assets, employment and sales were in its country of origin; today, the balance of these factors is found abroad. Even among firms that have few connections outside their country, we find most are tied to transnational corporations (TNCs) through supplier networks. Capitalist accumulation operates through globalised circuits, and few remain untouched in either the commodities they buy or those they sell.

Although globalised circuits of accumulation define capitalist relations throughout the world, each country integrates into this system through its own unique conditions. For the TCC, there is no national economic strategy that stands outside of transnational integration. Growth cannot take place based on a national industrial policy delinked from global investments. National development, job growth, profits, a healthy GDP and a sharp competitive edge are synonymous with globalisation. Therefore, a common political and economic project of the TCC is to re-engineer the state and the economy to facilitate transnationalisation. This takes place at the level of world governance in bodies such as the WTO and IMF. But also, importantly and perhaps decisively, at the national level.

Just as the TCC wages a daily war to transform all social institutions to its needs, class forces opposed to globalisation fight to maintain their hold over society. Working-class rights and privileges, won in the Fordist industrial era and inscribed in social contracts, are not easily abandoned. Market shares, taxation rules and subsidies for national firms are not given up without demands for concessions or outright opposition. Within the TCC, different sectors have their own priorities and preferences in policy. All these conflicts are mediated by the historical conditions and social context found in each country. How strong is the tradition of government planning and industrial policies? What is the level of technology, education and health care? Is there a tradition of resistance, a democratic culture or legal protection for opposition politics? What is the relation of class forces, the strength and size of the TCC fraction, and what has been the country’s place in the world system for the past 150 years? All these questions and relationships affect how fast and deep a country will align with transnationalisation. They also affect the political and social structure of that alignment, giving each country its particular national characteristics within the globalising process. Therefore, drawing too sharp a distinction between the TCC and national capitalist fractions misses the main point. Both sides are involved in a dialectic that is forming the transnationalised synthesis. One side does not exist without the other, and globalisation takes form and exists within the contradiction between the two.

Some see globalisation as a neoliberal project foisted on the world by a hegemonic US. 2 This western-centric view ignores two essential features of capitalism. The first is the deep global economic integration of production, investments and finance, which gives rise to a competitive, but co-dependent, TCC; and, second, are the commonly held ideologies that unite elites across borders, redefine national interests and trump nationalist economics. Globalism, in both its neoliberal and neo-Keynesian manifestations, aligns TCC members regardless of their country of origin. Consequently, the transnational project did not arise solely from the US ruling class, but was a response by capitalism to a transformative era in technology, production and accumulation. Different models of transnational capitalism are fought over, and policies are debated, in forums from Davos to the trade courts inside the WTO. While these differences are based in the history and corporate culture of countries or regions, the common project remains the same: to construct a working and stable system of global capitalist accumulation.

Given this framework, we can now begin to look at China. The defining feature of China’s last 100 years is its determination to be free of imperialist control, to insist on self-determination and its own path of development and to occupy a respected place on the world stage. This history certainly moulds the contours of China’s insertion into globalisation. But today’s ruling class lies at the polar opposite end of Mao’s approach to self-reliance. Mao’s peasant socialism looked inwards, to the shoulders of its own farmers and workers to transform the country. Not only was China isolated from the capitalist world, the Soviet Union also pulled out long before the Cultural Revolution. Today’s statist TCC has a vision of China’s modernisation through its strategic engagement with global capitalism. This strategy is in harmony with TCC ideology the world over. But integration will not happen through the dictates of the Washington Consensus, but through a project conceived and designed in China. As noted in the Financial Times:

China wants to accelerate the integration of the global economy, but on its own terms … it is not seeking a rupture with the international economic system … it is looking to mould more of the rules, institutions and economic relationships that are at the core of the global economy. It is trying to forge post-American globalisation.

3

Energy, resources and manufacturing

We can start our survey of transnational capitalism in China with the energy and natural resource industries. These industries cause the greatest concern for those who fear China’s rise as a new hegemon. Chinese TNCs visit continent after continent, seemingly gobbling up resources in a nationalist drive to prevent access to national competitors. Moreover, China’s three major energy TNCs are all state owned. PetroChina, with its subsidiary the China National Petroleum Corporation (CNPC), is the world’s fifth largest oil producer and the world’s first trillion-dollar enterprise. The China Petroleum & Chemical Corporation (Sinopec) has the world’s third largest refinery capacity. It attracts international and private capital through listings on the Shanghai and Hong Kong stock exchanges, but its parent company is wholly government owned. Lastly, the China National Offshore Oil Corporation (CNOOC) is 70 per cent government owned, incorporated in Hong Kong and traded in Hong Kong and New York. All three TNCs have ample access to state-backed loans from China’s Development Bank. Among major metal resource TNCs is state-owned Chinalco. It’s the controlling shareholder of the world’s second largest aluminium producer, Aluminium Corporation of China (Chalco), listed in both Hong Kong and New York. State-owned China Metallurgical Group Corporation is also world class and one of Fortune’s Global 500.

Since these are all majority-owned state corporations, should we consider them national champions or transnationalised corporations? There are three questions to consider in evaluating their character and economic strategies: the first is their integrated relationships with other TNCs; the second is the effect of their international investments on supplies and competition; and the third is, who benefits from their control of resources?

As we examine China’s twenty-three largest natural resource deals between 1996 and 2010, we find deep ties to other transnational actors. 4 Starting with PetroChina/CNPC, we see annual acquisitions of $2–4 billion between 2005 and 2008. Then, in 2009, the government called for an expansion of outward-bound capital, and PetroChina responded by buying $7 billion worth of refineries and reserves in Australia, Canada, Singapore and Central Asia. In late 2010, PetroChina expanded again, with a $5.4 billion deal for a 50 per cent partnership with Canada’s gas company, EnCana. Plans for the next decade include $60 billion for overseas expansion. 5 CNPC’s first major overseas venture was in 1996 with the Greater Nile Operating Company in Sudan. The joint production partnership had CNPC holding a 40 per cent share; Arakis Energy Group, a Canadian company, with a 25 per cent share; state-owned Malaysian Petronas at 30 per cent; and a Sudanese state-owned firm, Sudapet, with 5 per cent. Another deal in Sudan was struck in 2001, incorporated in the British Virgin Islands, and included the exploration and production of 29,000 square miles. CNPC held 41 per cent, Petronas 40 per cent, Sudapet 8 per cent, Sinopec 6 per cent and Al Thani, from the United Arab Emirates, had 5 per cent. CNPC’s first full acquisition came in 2005 in a $4.18 billion deal for PetroKazakhstan, although one-third of the shares were sold back to the Kazakh national oil and gas company. In 2009, CNPC made two large investments in Iranian oilfields. The first was a $4.7 billion development contract for the giant Pars gas field, to be paid back with production. The second was a 70 per cent stake in the South Azadegan oilfield in joint partnership with the National Iranian Oil Company’s Swiss-based subsidiary Naftiran Intertrade Company and Japan’s Inpex. CNPC is expected to invest $4.26 billion in the development of South and North Azadegan, relinquishing rights when payments in production have been completed. Moving to Australia, we find CNPC working with western oil majors to develop various gas resources. In 2010, PetroChina and Shell bought Arrow Energy for $3.2 billion. They struck a $41 billion contract with ExxonMobil to supply Australian liquid natural gas for the next twenty years. And, finally, there was a $4.7 billion joint venture between Chevron and PetroChina to exploit natural gas in Western Australia.

Next, we can examine Sinopec, beginning with its 2004 ventures into Angola. Entering into partnership with Angola’s state-owned Sonangol, it completed a $2.4 billion deal for oilfield blocks previously owned by Shell. In 2009, Sinopec partnered with CNOOC to buy into another block for $1.3 billion jointly owned by Marathon, Total, Sonangol, ExxonMobil and Portuguese Galp Energia. Sinopec turned to Iran in 2007 to invest $2 billion in the Yadavaran oilfield, holding a 51 per cent stake, with Naftiran Intertrade holding 49 per cent. In the largest corporate takeover by a Chinese TNC, Sinopec acquired Swiss/Canada’s Addax Petroleum for $7.22 billion in cash in 2009. Addax held properties in Nigeria, Gabon, Iraq and Kurdistan and is listed on both the Toronto and London stock exchanges. In another 2009 deal that rivalled the Addax acquisition, Sinopec paid Spain’s Repsol $7.1 billion for a 40 per cent stake in its Brazilian unit. This is a joint venture with Petrobras to develop Brazil’s giant offshore oil discovery. Furthermore, in return for a low-interest $10 billion loan from the state-owned China Development Bank, Petrobras will supply Sinopec with oil for ten years. Lastly, in 2010, a contract was signed with ConocoPhillips for a $4.65 billion stake in Syncrude, which is digging oil sands in Canada.

The last energy giant to review is CNOOC, which, in 2002, got involved in one of the world’s largest gas projects, located in Australia. This partnership included BHP Billiton, BP, Chevron, Shell, Japan Australia LNG and Woodside Energy. In 2006, CNOOC paid $2.27 billion for 45 per cent of the Akpo offshore oilfield in Nigeria. Other owners include Total, Petrobras and Nigeria’s state-run Sapetro. In 2010, CNOOC extended its global spending spree with a $2.16 billion deal for a Texas oilfield from Chesapeake Energy. And in its largest venture to date, CNOOC secured its first South American beachhead, paying $3.1 billion for stakes in Argentina’s Bridas Energy with fields in Argentina, Bolivia and Chile.

Other important ventures in natural resources would include two state-owned enterprises, China Railway Engineering Company and Sinohydro, forming a joint venture with the Congolese government for 10 million tons of copper. As part of the arrangement, a $9 billion loan from China’s Export Import Bank will help build 24,000 miles of roads, 2,000 miles of rail, thirty-two hospitals, 145 health centres, two universities, two airports and two dams. This pattern is also seen in the $3.4 billion agreement by the China Metallurgical Group (MCC) in Afghanistan for copper. MCC will also build schools, roads and mosques, investing hundreds of millions in infrastructure improvements. Promising to staff the entire project with Afghan workers and management, MCC will be the government’s single largest source of tax revenue and its most important business partner. Meanwhile, Chinalco, alongside Alcoa, obtained a 14 per cent stake in Australia’s Rio Tinto for $14 billion and is now its largest shareholder. The purchase was China’s biggest overseas acquisition. Another contract of note is China’s Development Bank loan of $25 billion to Russia’s state-owned Rosneft and Transneft to build an oil pipeline to China. The loan will be repaid in oil, with China receiving no equity in the infrastructure.

So, let’s puts all this data into the context of the three questions posed above. First, we see that Chinese state capital is transnational in character and has grown significantly more so in the last few years. Its investments have merged Chinese economic interests with other statist TCC fractions as well as private TCC sectors. There is little evidence of acquiring controlling positions, but rather a pattern of partnerships and joint ventures creating unified networks of common TCC concerns. Furthermore, as Theodore Moran argues in a study for the Peterson Institute, the large majority of these ventures do not tie up resources for China’s own national interest, but rather ‘expand and diversify the global supplier system, making it more competitive’. 6 In another study, Rosen and Houser show that the majority of oil bought by Chinese TNCs never reaches China, but is sold in international markets. No energy from Canada, Syria, Venezuela or Azerbaijan is used inside China, and ‘only a fraction’ from Ecuador, Algeria and Colombia is used. 7 Therefore, China is not tying up resources for its own use, but is involved in joint projects producing mutually shared global profits. Lastly, consider the energy and resources brought into China. In large part, these feed China’s great export machine, whose engines are TNCs from around the world. When Nigerian oil powers the assembly lines at Honda and Volkswagen, or Iranian energy lights up FoxConn so computers for Dell and HP can flow off the assembly line, just who is benefiting? This is part of the vast transnational value chain; it doesn’t simply serve the Chinese national economy. All contingents of the TCC benefit in the densely interconnected networks of global capitalism.

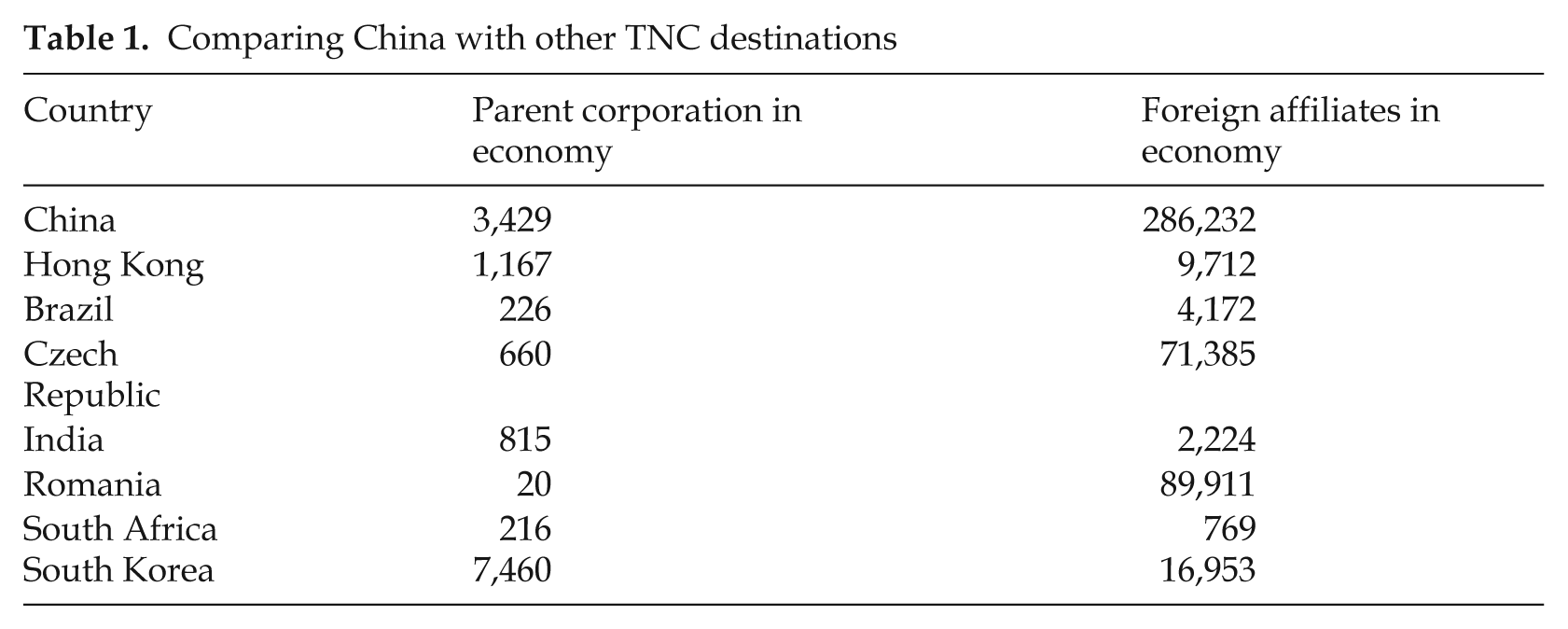

Of the world’s top 500 TNCs, 483 operate in China. Globally, there are 82,000 TNCs with 810,000 foreign affiliates. Of these, 286,232 are present in China. China continues to grow as a source for both inward- and outward-bound FDI. In 2008, China attracted $108 billion, placing it only behind the US ($316 billion) and France ($118 billion) as a destination for FDI. About half of all inflows go to manufacturing. If we include Hong Kong figures, China’s FDI soars to $171 billion. 8 In 2008, China’s outward-bound FDI surged by 132 per cent, reaching $52 billion, but adding in Hong Kong makes the figure shoot up to $112 billion. This compares to FDI outflows from the UK at $134 billion and Japan at $128 billion in the same period. In terms of greenfield investments, outward FDI from China and Hong Kong represents 28 per cent of the total from the developing world between 2004–2008. 9

To understand just how dominant China is as a TNC destination, Table 1 compares it to other leading countries. 10 The Table makes clear China’s role in transnational accumulation. TNC incorporation into the Chinese economy is, in part, due to requirements to source materials from, and form joint ventures with, Chinese corporations. Such laws serve a number of purposes: they ensure the national economic development of both Chinese private and state capitalist sectors; they develop a broad network of subcontractors bound to TNCs; and, they strengthen the ties between transnational capitalists from abroad with private and state capitalists in China. The result is to combine China’s national development with foreign TNCs and integrate global sectors of the TCC.

Comparing China with other TNC destinations

Finance

Transnational networks also exist in the major state-owned banks and financial institutions. Although China has been careful to protect its capital from speculative runs, transnational financial groups can partner with and buy into Chinese firms. The first step was taken by transforming the largest state-owned banks. This meant cleaning up bad debt, overhauling management systems, imposing strict corporate governance standards and then selling stakes to global investors. This was accomplished by establishing a foreign advisory council that included: Sir Edward George, former governor of the Bank of England; Gerry Corrigan, former president of the New York Federal Reserve; Andrew Crockett, former general manager of the Bank of International Settlements; David Carse, former deputy chief executive of the Hong Kong Monetary Authority; and Sir Howard Davies, former head of the UK’s Financial Services Authority. Morgan Stanley did the initial public offering (IPO) for the China Construction Bank, and Goldman Sachs and UBS did the IPO for the Bank of China. Credit Suisse First Boston helped list the Industrial and Commercial Bank of China, which set an IPO record by attracting $21.9 billion. The Agricultural Bank of China, with 24,000 branches and 350 million customers, was the last to list in 2010.

To invest in the Shanghai stock market, foreign firms need to partner with local investment banks, but are limited to 49 per cent ownership. Among the most important investors are: Barclays, BlackRock, Capital Group, Credit Suisse First Boston, Deutsche Bank, Fidelity, HSBC, Invesco, JP Morgan, Massachusetts Mutual Life Insurance, Morgan Stanley, Schroders, Vanguard and UBS. Additionally, Goldman Sachs has the largest non-government stake in the Industrial and Commercial Bank of China.

A study by David Peetz and Georgina Murray lists the thirty largest shareholders in the world’s top 250 industrial corporations and the fifty largest financial corporations. The Chinese government ranked third, reflecting its dominant stock position in large state industries. Peetz and Murray also measured asset holdings. Of the 300 largest TNCs, ten are Chinese, owning $2.2 trillion in assets or 7.6 per cent of the total. Japan, with forty-eight TNCs, held 6.1 per cent, and Germany, with twenty TNCs, held 6.9 per cent. 11 Obviously, the ten state-owned Chinese TNCs have a huge footprint in global economic affairs. An additional indicator of global power is Fortune’s list of the world’s 500 largest corporations based on revenues. China ranked number three (with forty-nine), behind Japan (with seventy-one) and the US (with 139). Six of these Chinese TNCs ranked within the top thirty-two most profitable corporations in the world. 12

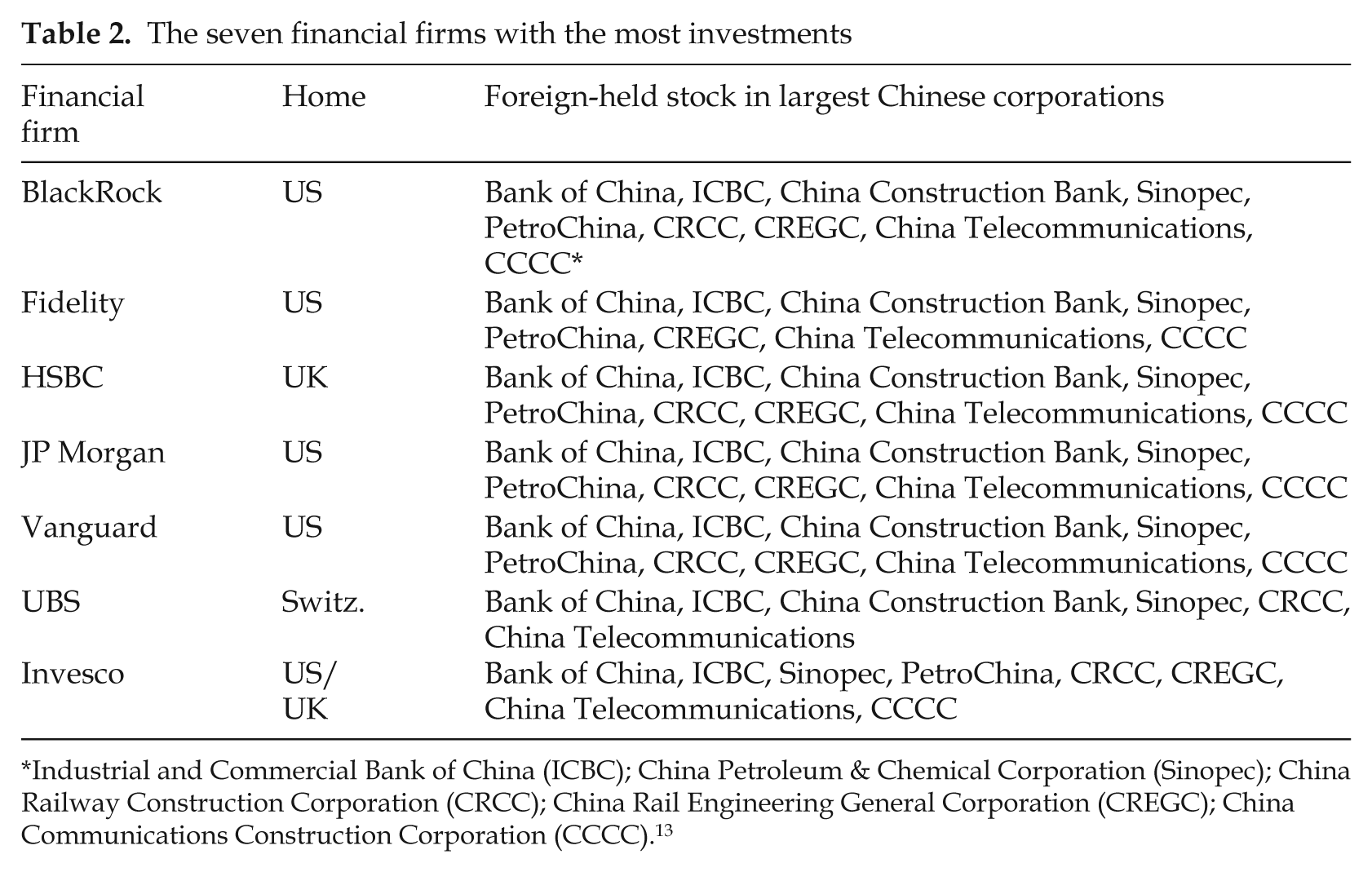

In examining the nine largest Chinese TNCs by assets, we find 112 major investors, of whom fifty-nine are foreign investment and banking firms holding 158 investments out of a total of 271. In all, the Chinese TNCs, the government and Chinese investment firms owned between 56–81 per cent of the total stock. Nevertheless, there exist important relationships with some of the largest and most influential western financial institutions. Table 2 lists the seven financial firms with the most investments.

The seven financial firms with the most investments

Industrial and Commercial Bank of China (ICBC); China Petroleum & Chemical Corporation (Sinopec); China Railway Construction Corporation (CRCC); China Rail Engineering General Corporation (CREGC); China Communications Construction Corporation (CCCC). 13

Other important stockholders include Barclays, Capital Group, Deutsche Bank, Franklin Resources, Hong Kong’s HKSCC Nominees Limited, Massachusetts Mutual Life Insurance, Schroders, State Street Corporation, Waddell and Reed Financial and the French banks Axa and BNP Paribas. Some financial institutions with strong positions sold shares due to their weakened condition from the global crisis. The Royal Bank of Scotland offloaded its entire stake of $2.3 billion in the Bank of China, and Bank of America reduced its position in China Construction Bank by $7.3 billion. Of course, all these investment firms represent a broad network of transnational investors, so we shouldn’t simply think in terms of just eighteen firms, but understand the deep links that are being established.

The investments of western transnational capital in the state-owned financial sector help to integrate the TCC. In these entangled networks, western money facilitates the global expansion of Chinese banks, sharing in profits and power. Although lacking controlling stakes, perhaps more essential is a common ideology about the role and function of TNCs in the global economy and universally held business practices. Consequently, national identities, as well as the nature of statist and private capital, are secondary. This is not to say that competition ceases or that different visions of the global system aren’t important, or even sometimes primary. But to understand global capitalism, one must appreciate the underlying phenomenon of integration. 14

David Rubenstein, co-founder and managing director of the Carlyle Group, speaks to this common business culture as a lure for China’s state capitalists. Rubenstein explains:

What makes the Chinese government encourage companies like The Carlyle Group to come invest there? It isn’t the capital … They have $2.4 trillion in foreign reserves … It’s the management that private equity firms have … I think the government is trying to get contacts, expertise, technology and skill sets, not capital.

15

If business expertise draws China to private equity firms, what is the draw for Rubenstein and his cohorts? As he remarks:

China is going to set the tone for private equity because a large number of their sovereign wealth funds are going to be investing large amounts of money outside of China, and they’re going to be setting the rules and the patterns for what some of those investments are going to be … The United States has been the dominant player in private equity for the last 30 or 40 years. China will soon be almost as important as the United States in the world of private equity, and may replace the United States at some point because of the enormous amount of money that’s being invested – not only in China but the amount of money China is investing through CIC and other organizations outside of China.

16

Transnational capitalists like Rubenstein aren’t worried about the national origin of money; rather, their main concern is the availability of huge pools of capital for investments. It’s through the merger of business culture and money that the TCC takes formation. As Dealbook points out: ‘All of the major Wall Street banks have sought closer ties to China, probably the one foreign market they want to be in above all else.’ 17

To appreciate what Rubenstein is so excited about, we need to examine Chinese finance capital. China Development Bank (larger than the World Bank and Asian Development Bank combined) has made over $300 billion in foreign loans, invested $3 billion in Barclays and entered into partnership with Nigeria’s United Bank for Africa. Its activity between 2009–2010 exceeded lending by the World Bank. Ping An Insurance has emerged as the leading shareholder in Fortis, investing $2.7 billion. China Construction Bank is the fifth most profitable TNC in the world. The Industrial and Commercial Bank of China (ICBC) is the world’s third most profitable TNC and the largest bank by market capitalisation. In the biggest foreign acquisition by a Chinese bank, the ICBC bought 20 per cent of South Africa’s Standard Bank for $5.56 billion, opening up opportunities for other state-owned TNCs. For example, China Railway Construction Corporation is negotiating a $30 billion high-speed rail project in South Africa, arranging loans from Standard and Chinese state banks. This same pattern is seen in Europe where, in 2009, $13 billion in Chinese financing went to public works projects across Italy, Greece, Poland, Hungary, Moldova and the Ukraine. Work goes to state-owned manufacturing and construction TNCs that often have western stockholders. Consequently, the line between Chinese state capital and transnational capital blurs in respect of their mutual interest and joint investments.

This pattern is also seen in the role played by investment and equity firms. In the financial sector, TPG Capital and Kohlberg Kravis Roberts jointly acquired Morgan Stanley’s 34 per cent stake in China International Capital Corporation (CITIC), the leading investment bank in China. TPG also established a $1.5 billion investment fund in partnership with the city governments of Shanghai and Chongqing and holds equity stakes in Lenovo, the Shenzhen Development Bank and China Grand Auto. BlackRock, the largest investment TNC in the world, has holdings not only in ICBC, China Construction Bank and Bank of China, but also in CITIC, China Pacific Insurance, China Life Insurance, as well as major state energy and oil TNCs. CIC, which is China’s sovereign wealth fund, has a $1.7 billion stake in Morgan Stanley and a $3 billion investment in Blackstone. Although CIC lost money on the Blackstone deal, Blackstone has deepened its commitment to China by establishing a local investment fund with the Shanghai government. Blackstone, alongside significant private investors from China, also created a $15 billion buyout fund for acquisitions in emerging markets. 18

Another important relationship is that between Prudential, the Carlyle Group and the Fosun Group of Shanghai. Carlyle is among the biggest private equity TNCs, with about $2.5 billion invested in China. Fosun is one of China’s largest privately owned conglomerates, with holdings in real estate, steel, mining and pharmaceuticals. Early investors included Hong Kong billionaire Li Kashing, the government of Singapore and AIG. Expanding globally, Fosun joined with Prudential and Carlyle, establishing funds to invest in emerging companies and overseas acquisitions, tapping private Chinese capitalists for equity investments. 19

A further financial factor to consider is that both Chinese state and private corporations raise billions through IPOs on world stock markets. In just the first half of 2010, Chinese companies launched 214 deals bringing in $34.7 billion, accounting for one-third of global IPOs. In comparison, the US offered sixty-two IPOs raising $9.2 billion. By the end of the year, on the Nasdaq and New York Stock Exchange, China accounted for 23 per cent of all IPOs in the US; up from just 1 per cent in 2000.

In all the above statistics, the main characteristic that stands out is financial integration. TNCs, whether state or private, don’t work as singular national champions. Global networks are thick and integrative. As a result, examining the manner and level of integration is key to understanding the TCC. Unfortunately, literature and data banks still list TNCs by where they are headquartered, thereby immediately casting a national framework on all analysis. But such identifiers often hide the deeper nature of TNCs and the character of the transnational capitalist class.

Lastly, we need a closer consideration of CIC, China’s $300 billion sovereign wealth fund (SWF). One of the largest SWFs in the world, CIC is an important avenue for China’s statist TCC to invest around the globe. As noted above, CIC has large holdings in Blackstone and Morgan Stanley, but additionally CIC has shares in AIG, Apple, Bank of America, Citigroup, Coca-Cola, Johnson & Johnson, Motorola, News Corp and Visa. By 2010, CIC had $9.63 billion in equity stakes in more than sixty US corporations and had added Morgan Stanley’s CEO to its advisory council. In Canada, it has positions in Research in Motion, the maker of BlackBerry mobile phones, and a $3.5 billion stake in the mining company Tech Resources. 20 Additionally, CIC invested $1 billion in Oaktree Capital Management, $1 billion in JSX KazMunaiGas in Kazakhstan, $956 million with the UK’s private equity firm Apax and $850 million for a 15 per cent stake in Hong Kong’s Noble Group, a commodity-trading powerhouse. Its total foreign investment portfolio sits at $98 billion. 21 CIC has also aided Europe’s financial crisis by buying government bonds in Greece, Portugal and $7.9 billion in Spanish debt.

As Fortune notes:

A big part of the future will involve China investing in financial assets and real estate. Look only at the number of trips that the world’s leading hedge fund managers have been making to Beijing this year. They go for the same reason Willie Sutton robbed banks, but they arrive at the headquarters of CIC as supplicants on bended knee, desperate for investable capital in the one place in the world where that is very much in surplus.

22

Such supplication worries TCC fractions that have long held to free-market ideology. There is about $9.2 trillion held in SWFs internationally, with $3.9 trillion in assets under management. This represents a substantial amount of wealth under government control. Such great pools of capital mean a transfer in power and decision-making that clashes with western private sector traditions. Most SWF wealth resides in the emerging South, which has had little say in shaping the framework and governance of global capitalism. We have already begun to see a power shift with the G7 transforming into the G20 and some rebalance of voting strength inside the IMF.

Edwin Truman writes that there are further fears

that governments would use their SWFs to buy control of large ‘national champion’ firms in key sectors. This dynamic would contribute to the creation of ‘sharecropper societies’ in the West as foreign government investments would pour into industrial countries that had lost control over their own affairs.

23

Such fears have had political ramifications, with a number of transnational deals being cancelled. In part, this reflects fractional lines between the TCC of emerging and developed economies. But to leave our observations there would be shallow and incomplete. Many corporations in the West welcome inflows of SWF capital. As Fortune points out, ‘The U.S. ought to set aside its current economic insecurity and answer a simple question correctly: If the Chinese want to park more of their money in American assets (besides Treasury bills), why wouldn’t we open our pockets and take it?’

24

Truman adds:

For decades, the traditional industrial countries have preached doctrines of open markets and receptivity to capital flows, particularly in the form of foreign direct investment … the shoe is now on the other foot on openness, with the important qualification that many of the new breed of foreign investors are governments. Hypocrisy in international finance is no more attractive than in other areas of human and sovereign interaction.

25

Implicit in Truman’s remarks is a recognition that SWF funds, whether controlled by Abu Dhabi, Singapore or China, are an important element in transnational circuits of accumulation. As such, statist transnational capitalism is as much a part of global capitalism as western private TNCs. The acceptance of SWF capital undercuts arguments that globalisation is a US or western project. Rather, it points to the growing integration of the TCC and the crystallisation of a common project.

Business and the state

China has 143,000 government-owned enterprises. Among these are 129 world-class conglomerates that answer to central government, with one-half of their chairmen or chairwomen appointed by the central department of the Party. Among the 100 largest publicly listed TNCs, ninety-nine have majority state ownership. These corporations occupy the commanding heights of the economy and are concentrated in finance, construction, infrastructure, communications, energy, the military and some key manufacturing sectors. More open to foreign TNCs and private capitalists are light industry, retailing and the huge export sector. Although some view state TNCs as national champions, as we’ve seen throughout, the largest state-owned enterprises (SOEs) are involved with global TCC networks at many levels. In reality, private and state capital are two wings of the Chinese TCC, with the statist fraction in a dominant position.

The relationship between Party corporate executives and the state-centred political leadership is one of a blending of mutual interest and tensions. State-owned TNCs compete with each other, arm themselves with lobbyists and focus on making profits, not political strategy. Party rules now separate military, government and corporate officials, leaving executives free to maximise profits. When Beijing’s policies conflict with profits, executives are not shy about fielding their political clout and lobbyists. Corporate leaders expect the government to protect and extend their interests, creating powerful connections within the statist TCC fraction. Western TNCs make similar demands on their governments, but not with the same bonded relationship that comes with Chinese state ownership. Political leaders ensure preferential treatment for state corporations, and many of the CEOs sit on the Party’s Central Committee.

Since the onset of the global crisis, Chinese officials have been more open in challenging neoliberal market policies. This has meant a return to stronger government involvement and greater economic support for state TNCs. According to the World Bank, investments by state corporations surged with the influx of stimulus money, as did industrial production by state manufacturers. In 2009, municipal governments set up 8,000 new SOEs, which have also gained in popularity among university graduates, offering better job security and rising salaries.

As China scholar Huang Yasheng stated: ‘In 2009, there was a huge expansion of the government role in the corporate sector.’ Victor Shih from Northwestern University made similar observations: ‘China’s always had a major industrial policy. But for a space of a few years, it looked like China was turning away from an active and interventionist industrial policy in favor of a more hands-off approach.’ Now Professor Shih sees the Jiang-era market reforms being partially reversed, with private capitalism playing only a supporting role to statist economic management.

26

As pointed out in the New York Times:

Mr. Wen and President Hu Jintao are seen as less attuned to the interests of foreign investors and China’s own private sector than the earlier generation of leaders who pioneered economic reforms. They prefer to enhance the clout and economic reach of state-backed companies at the top of the pecking order.

27

While the Chinese TCC is a mix of private and state fractions, it’s also important to consider the role of Hong Kong and, to a lesser extent, Taiwan. These questions deserve greater attention, but we can make some preliminary observations. Among the top 100 non-financial TNCs from the developing world, China and Hong Kong dominate with a combined total of thirty-nine. Eleven are from the mainland and twenty-eight from Hong Kong. Taiwan is second with fourteen. In terms of Taiwan, although political tensions remain high, economic integration is great. In the future, if Taiwan rejoins China, one can imagine the combined economic power of Chinese transnational capital and the blending of private and state interests. This is particularly true in the field of information technology. Taiwanese factories on the mainland make 85 per cent of the world’s desktop monitors, 90 per cent of all laptop computers and 70 per cent of the motherboards for desktop PCs. Taiwan has invested $150 billion in the mainland and employs 14.4 million workers, a figure equal to 60 per cent of the entire population of the island. 28 Most manufacturing jobs in China come from Taiwan, Hong Kong and South Korea, and about 60 per cent of Chinese exports are produced by foreign affiliates. Accordingly, links to global markets through Taiwanese capital are substantial. If politically united with the mainland, Taiwanese capitalists would be a significant fraction within the Chinese TCC and are already influential on issues like labour law.

Hong Kong’s economic data are usually separated from that of the mainland in international business journals, although Fortune’s Global 500 now combines both. From a class and political standpoint, Hong Kong capitalists are becoming ever more integrated with the mainland. The official relationship and policy are of one country, two systems. While important differences in how people live and do business remain, the statist ruling class in China constructs the governance and economic realities in Hong Kong. The differences are historic, but also designed to benefit a mutual relationship. There is no question that huge amounts of money flow between the two and that Hong Kong is a global outlet for Chinese finance. In return, large investments move into China, in finance, manufacturing and real estate. There are 320,858 Hong Kong-funded projects in the mainland and a total of $446.49 billion in FDI. That figure accounts for 43 per cent of all FDI in China. 29 This affects Hong Kong’s transnationality index (TNI) as measured by the United Nations. TNI is the ratio of foreign-held assets, employment and sales to national assets, employment and sales. Hong Kong TNCs have an average TNI of 72.8, mainland corporations a TNI of 25.7 and Taiwan a TNI of 53.4. 30 Although significant investments in China push up Hong Kong’s TNI, its global orientation is high even compared to western TNCs. Consequently, Hong Kong is an immensely important avenue for the statist TCC to link with worldwide capitalist networks.

There are other interesting ties between Hong Kong and mainland capitalists. There are 875,000 people worth over $1.5 million in China. The China Reform Foundation estimates that 10 per cent of the population is hiding about $870 billion in corrupt ‘grey money’. One place this money flows to is London real estate. Since no Chinese citizen can invest more than $50,000 per year overseas, the wealthy bypass restrictions through foreign bank accounts and trust funds often situated in Hong Kong. As the New York Times reports, ‘mainland Chinese investors have already replaced those from Russia and the Middle East as the busiest real estate buyers with deep pockets, looking for trophy assets and pushing up prices’. 31 Hong Kong real estate, with prices that rival those of Manhattan, has also attracted mainland millionaires. Deposits of renminbi in Hong Kong grew by 246 per cent in 2010 and the city is used as a testing ground for financial liberalisation.

TCC political divisions

On a world scale, the TCC is divided into neoliberal and neo-Keynesian wings. While an analysis of the Chinese TCC needs to be more complex, such divisions do offer a starting point. Beginning with the economic reforms of the 1980s, the Chinese state built a developmental model that sacrificed workers’ rights and interests. Privatisation of SOEs reached its peak in the late 1990s, resulting in 30 million lay-offs. Under Jiang Zemin and his Shanghai cohort, their growth-at-all-costs policy led to widespread environmental damage and corruption. Jiang also opened the Communist Party to private capitalists and, by 2000, businessmen accounted for 19.8 per cent of its membership. At the same time, universal health care was ended and tuition fees instituted at schools. China did see enormous growth, but Jiang’s policies of mass privatisation, low wages and lay-offs left serious social problems.

If Jiang’s policies were typical of the neoliberal Washington Consensus, the Beijing Consensus developed under President Hu Jintao and Prime Minister Wen Jiabao can be understood as a neo-Keynesian reaction. Their policy of building a ‘harmonious society’ was an attempt to address growing inequalities, rapidly spreading labour unrest and peasant rebellions. An indication of their split with Jiang was his early removal from the important Party post that he maintained after Hu became Party general secretary. There were also attacks on Jiang’s Shanghai base, with the arrest of Zhou Zhengyi, a powerful capitalist with holding and investment companies in Hong Kong. Zhou was sentenced to sixteen years in jail for illegally acquiring state land and bank loans. Other protégés of Jiang, including Shanghai mayor Huang Ju, also landed in jail. Afterwards, Jiang himself was seen in public less.

In 2007–2008, Hu and Wen proposed labour legislative reforms that developed into a major confrontation for different TCC fractions. There was the Labour Contract Law, Labour Arbitration Law and the Employment Promotion Law. All were met with strong opposition from foreign and private business interests. Both the American Chamber of Commerce in Shanghai and the European Union Chamber of Commerce went to the National People’s Congress to argue against the laws and threaten to withdraw investments and operations. The private telecommunications TNC Huawei attempted to undermine the new legislation by forcing several thousand long-term employees to resign and sign new short-term labour contracts. Eventually, Huawei, along with McDonalds, Kentucky Fried Chicken and Pizza Hut, backed down from such violations. 32

Another struggle over labour law broke out when a wave of 100 strikes in the automotive industry erupted. Guangdong’s leading Communist Party official supported workers’ demands and issued a directive sanctioning the democratic election of factory unions, shop-floor bargaining rights, an expanded role for unions in determining contracts and the election of union delegates for wage negotiations. 33 When the Guangdong government moved to draft legislation to establish a collective wage negotiating system, Hong Kong business groups ‘mounted a sustained and increasingly alarmist and vitriolic lobbying campaign against the bill … howling in protest’. 34 The Hong Kong fraction was joined by private capitalist, Taiwanese investors and neoliberal fractions inside the Guangdong government postponing the reforms. As these conflicts show, private/state ownership divisions don’t exactly line up as neoliberal/neo-Keynesian political splits. Many provincial Party leaders and SOE executives benefit from the most exploitative forms of neoliberalism, working with Hong Kong and foreign TCC fractions against the social democratic efforts of other state leaders.

Besides labour laws, Hu and Wen instituted other changes. These included an increase in the minimum wage, extending the minimum subsistence allowance to 17 million people, abolishing the agricultural tax, offering free health care to 400 million people and free education to the rural poor. Serious and sustained investments in green technologies also became an important part of their economic programme. 35 These reforms must be seen within the context of growing mass protests. According to the Party, protests increased by 50 per cent in 2008 to 127,467 incidents. And, once the Labour Contract Law and Labour Arbitration Law were passed, factory disputes doubled to 693,000.

The Hu-Wen era reforms reflect a Keynesian social democratic approach similar to that of the Roosevelt administration in the 1930s. As the China Labour Bulletin explains:

The unprecedented wave of labour legislation in this period was no accident. It was a direct response to the pressure exerted by the workers’ movement over the previous decade. A government committed to maintaining social order and harmony could no longer afford to ignore the strikes and protests staged by workers on an almost daily basis across the country. It sought to create a comprehensive legislative framework that could help mitigate labour conflicts and better protect the legal rights of individual workers.

36

We can view China’s large $601 billion stimulus programme in the same vein, a Keynesian governmental response to spreading lay-offs caused by the global crisis. Spending on infrastructure absorbed 20 million unemployed migrant workers and supported state sector enterprises. Exports to China from Germany, Australia, Africa and Latin America jumped, and Beijing helped global financial stability by buying $50 billion in IMF bonds. Praise came from many quarters. As Nicholas Lardy from the Peterson Institute, in testimony to the US-China Security Review Commission, stated: ‘China is the gold standard in terms of its response to the global economic crisis.’ 37 The New York Times wrote that China ‘really did save the world from recession’. 38

In part, the neoliberal/neo-Keynesian split revolves around the export model of development versus internal growth generated by greater consumption. The export model was built on low-wage assembly work, while the consumption model looks to higher wages and higher value-added manufacturing. Consumer spending accounts for 36 per cent of China’s GDP compared to 70 per cent in the US; 25 per cent of people have no health insurance and pensions cover less than one-third of workers. For all the talk about equality and social harmony, labour’s share of income has dropped from 56 per cent in 1983 to 37 per cent in 2005. 39 This represents a huge transfer of wealth from the working class to the government and corporations (i.e. the Chinese TCC). The result is that most families save much and spend little. In the West, neo-Keynesians are debating with their neoliberal brethren over the need for government stimulus, but China is where the great debate is really occurring, and perhaps sharpening as a leadership change approaches in 2012. The current economic plan emphasises public services, an expansion of health care and a stronger social security system. But some, like Rubenstein, are convinced that China will privatise another 100,000 SOEs and that Jiang maintains influence over top positions.

While differences do exist, there has been general agreement over what Joshua Cooper Ramo termed the ‘Beijing Consensus’. Ramo argues that China’s development has three major principles: constant innovation, self-determination and using ‘economics and governance to improve society’ by lifting millions out of poverty. 40 This developmental approach holds great attraction throughout the developing world and may pose a political split within the TCC. But we need to reiterate that such a split crosses all borders, and advocates of both market fundamentalism and neo-Keynesianism exist in every country.

Differences within the Chinese TCC may be no greater than the differences that President Obama and Lawrence Summers had with Wall Street over financial regulation; after all, no one is rejecting global capitalism. While export capitalists don’t want to see higher wages, the neo-Keynesians don’t want massive lay-offs in the export sector. Consequently, both resist the US push for a rapid rise in currency value that would make Chinese products more expensive. Furthermore, a consensus is growing among leaders that the period of industrialisation is coming to a close and that the internal market needs to expand.

This stance is supported by most of the western TCC. For the last decade, leading economists have been advocating greater social spending and more internal consumption, but see a steep increase in currency value as disruptive. Stephen Roach, head of Morgan Stanley in Asia, stated that: ‘forcing a currency realignment would be a blunder of historic proportions’. 41 The US-China Business Council, which includes 220 of the largest US corporations, stated that it is ‘important to note that US companies selling to China never cite the exchange rate as a competitive barrier … Every year, USCBC surveys its members on the barriers that impact their business with China. The exchange rate never comes up as an issue harming their sales.’ 42 The American Chamber of Commerce in China, with 1,200 business members, took the same strong stand, opposing a currency exchange rate bill moving through Congress.

Having a deep consumer market in China would offer vast opportunities for growth, helping to replace diminishing markets in the US weighed down with debt and a shrinking middle class. Such a historic rebalance in the global economy is not at all ensured. But it uncovers the strategic thinking of the transnational capitalist class, in China, the US and globally. Thus, national development in China is an essential feature of transnational capitalism. Both the private and state sectors of the capitalist class are embedded in transnational accumulation and transnational class networks. It is simply globalisation with Chinese features.