Abstract

This study analyses the gaps in financial centres' competitiveness and their impact on regional economic convergence in 23 European Union Member States during the period of the Global Financial Crisis. In particular, we explore the economic convergence and divergence patterns among regions from two different perspectives across the selected European Union Member States and within each country. From a methodological viewpoint, we apply a fully non-parametric framework to the club convergence model and address the endogeneity problem between financial centres' competitiveness and regional economic convergence. Our results show that the large and internationally-oriented financial centres experienced a diverging trend in terms of the competitiveness of financial centres' business environment during the peak of the crisis. We also find evidence that the convergence of financial centres reduces regional economic inequalities between the regions where financial centres are located. In contrast, the increase in the competitiveness of financial centres only serves to widen existing inequalities at the national level. Finally, we examine and discuss the impact of competitiveness drivers of financial centres on the convergence pattern of European Union regions.

Keywords

Introduction

The process of economic convergence across European Union (EU) Member States and regions has attracted considerable attention from researchers and policymakers in the last two decades. A number of recent studies have contributed to academic discussions on economic convergence and growth patterns in the EU (see Ezcurra et al., 2009; Le Gallo and Dall'Erba, 2008; López-Bazo et al., 1999; Petrakos et al., 2005; Tselios et al., 2012). The common thread that runs through all these studies is that EU regions display significant and persistent disparities. Such findings raise questions as to whether the convergence process is achievable in the near future within EU regions and consequently within Member States.

Drawing on the regional convergence theory (López-Bazo et al., 1999), this study explores the convergence process within EU regions during the period of the Global Financial Crisis (GFC) by extending the previous empirical research on financial development and economic growth (e.g. Aghion et al., 2005; Henderson et al., 2013; Petrakos et al., 2005, 2011). The contribution of this paper can be summarised as follows. First, we advance the current research on financial development and regional studies by analysing the effect of financial centres’ competitiveness on interregional economic dynamics. Current empirical research has not extensively investigated the influence of financial centres on the convergence trend of EU regions. Up until now, contemporary studies have analysed only individual financial centres (Amsterdam, London and Frankfurt) in the period before the GFC (Engelen, 2007; Engelen and Grote, 2009; Karreman and Van der Knaap, 2009; Klagge and Martin, 2005; Poon, 2003). 1 Instead, the period that we examine spans from 2008 to 2012. In this way, we contribute to the understanding of regional convergence dynamics and policies during the ‘shock period’ of the GFC.

Second, we investigate how financial centres' competitiveness explains the trend of economic convergence (divergence) at national and regional levels. In particular, one part of our analysis focuses on the effect of financial centres on the economic convergence of the regions in which financial centres are located. Another part investigates the effect of financial centres' development on regional inequality levels within countries. We also discuss and examine the factors that drive economic convergence of regions where financial centres are located.

Third, this is, to the best of our knowledge, the first study that applies a local linear estimator (Li and Racine, 2004, 2007) to the club convergence model of Chatterji and Dewhurst (1996). The proposed methodological framework allows us to estimate the convergence of financial centres' competitiveness on regional economic convergence in a fully non-parametric setting. This approach is more flexible and overcomes several limitations of the traditional parametric techniques commonly used in the convergence literature. We also address the potential endogeneity problem between the competitiveness of financial centres and the regional economic convergence/divergence. We introduce a new non-parametric instrumental regression in the context of this analysis (Horowitz, 2011). The applied estimator deals directly in a fully non-parametric framework with potential endogeneity problems. Finally, as a robustness check of our empirical findings, we apply probability transition matrices (Hammond and Thompson, 2002; Pittau and Zelli, 2006; Quah, 1996).

The structure of the paper is as follows: Section ‘Financial centres and economic regional convergence’ discusses the convergence of the European financial centres; Section ‘Data and methodology’ describes the database and methodology; Section ‘Empirical results’ discusses the empirical findings; Section ‘Concluding remarks’ sets out our conclusions and outlines directions for further research.

Financial centres and economic regional convergence

The economic convergence and integration of European regions have been addressed in several recent studies (e.g. Ezcurra and Rapún, 2005; Ezcurra et al., 2009; Le Gallo and Dall'Erba, 2008; Petrakos et al., 2005; Petrakos et al., 2011; Tselios et al., 2012, among others). In particular, the high variability of economic resources and the uneven geographical growth within European countries has drawn a lot of attention. The main research questions are aimed at understanding regional growth patterns and to what extent regional economic dissimilarities are intrinsically structural, or rather cyclical. This is an important issue because the catch-up process has not always been deemed effective or fast enough, even though the European Commission has promoted European economic integration through several key policy initiatives (the Single Market, Monetary Union, and, more recently, through the European Regional Development Fund, the Cohesion Fund, and the European Social Fund).

In addition, opposite dynamics appear to prevail for national and regional economies in Europe, namely a converging trend at the national level and a diverging trend at the regional level. As some authors have emphasised (Longhi and Musolesi, 2007; Petrakos et al., 2011), the main driver of this paradox can be traced to the development of metropolitan areas. The New Economic Geography (NEG) developed by Krugman (1981, 1991) can explain part of the above mentioned paradox. In particular, the NEG accounts for the existence of a diverging trend in the process of economic integration in Europe. The reason is that the combination of agglomeration forces and market size creates the conditions in which leader regions can develop and grow, and it predicts the process of geographical agglomeration of production, high quality resources, and services in specific locations. The rationale is that agglomeration economies on the local allocation of resources favour the polarisation of regions into different ‘clubs’: poor peripheral regions and rich central-core regions. Metropolitan areas have played a pivotal role in this process as they are strategic nodes of the modern economy because they offer high-level innovation services and a large labour market with a wide range of specialised qualifications (Longhi and Musolesi, 2007). These are all conditions that are crucial for both the stability and viability of firms. Large metropolitan areas therefore attract an increasing number of firms and tend to absorb resources from the surrounding areas.

In this context of increasing metropolisation, our first research question is based on whether the competitiveness of financial centres can explain the opposite trends between national and regional economies. Our investigation is motivated by the fact that financial centres are well-integrated in metropolitan areas that are major international hubs of business (Daniels, 2002). The headquarters of the majority of financial firms and services are also concentrated in international financial centres (Amin and Thrift, 1992). This is because it is almost imperative for financial institutions to be close to clients. A tight spatial proximity to financial institutions located in international financial centres appears, in fact, to still facilitate the process of knowledge creation and dispersion (Engelen, 2007; Faulconbridge et al., 2007). This is crucial for conducting profitable trade despite the advancement in information and communication technology (ICT) and the consequent reduction of the costs of communication and trading across space. Our hypothesis is, therefore, that the convergence of competitiveness of financial centres could help to explain the two opposite dynamics (regional economic convergence and divergence) at the European level. However, the way through which financial centres affect the regional economic convergence trends is not straightforward, especially during periods of financial turmoil.

On the one hand, a structural convergence of European financial centres can increase the international business cycle correlations of European regions and therefore could lead to convergence in per capita income. This view is consistent with Wacziarg (2001), who suggests that structural sector convergence within regions can lead to convergence in their per capita income. In this case, we argue that the increasing appeal of a financial centre can contribute to explaining the catch-up process of regional economies. However, we maintain that peripheral regions in a certain country can further lose their competitiveness because of a sort of draining process of capital and technological resources towards the regions where financial centres are located. Financial centres have been widely recognised to work as catalysts for labour forces, business, specialised corporate services and major financial institutions, and to promote technical innovation (Cassis, 2007). While regions where financial centres are located have a greater capacity to attract businesses and human resources, peripheral regions do not exert the same appeal. The distance from advanced regions can in fact discourage location decisions by firms operating mainly in national and international markets (Limao and Venables, 2001). As a result, this outlook could explain the uneven spatial distribution of economic and financial firms and services and explain the existence of different regional clubs.

On the other hand, the correlation and the increasing international profile of financial centres can make them more exposed to external shocks. Previous research acknowledges that there are some limits regarding the financial development and economic growth nexus during financially unstable periods. For example, Dell’Ariccia et al. (2008) show that financial development does not always lead to economic growth in periods of financial turbulence. Kroszner et al. (2007) argue that those sectors that are highly dependent on external finance are more vulnerable to bank crises and experience a greater contraction in the valued added, especially in more developed financial systems.

Fiinancial centres have played a pivotal role in originating and spreading the GFC to domestic financial systems, ‘real’ economies, and everyday households (French et al., 2009). Therefore, we assume that the convergence of financial centres could have further weakened the regional economic convergence at the European level during times of crisis. In this case, the regions of leading financial centres would not be in a position to widen their existing spatial disparities with respect to less advanced regions. In addition, one may question whether we can observe a diverging trend between regions at the national level. In fact, the potentially negative impact of the GFC on international financial centres could have slowed the transfer of resources from other regions to the regions where financial centres are located. However, such an impact depends on the connectivity and specialisation of financial centres. European global financial centres (such as London, Frankfurt, Luxembourg and Paris) rely more on global and international relations with, for example, each other rather than on their national city systems (Z/Yen Group, 2010). Instead, second and third-tier financial centres are more orientated on the transnational and local businesses, and act primarily as producer service centres, rather than dealing with large-scale and global financial transactions (Lee and Schmidt-Marwede, 1993). This makes second and third-tier financial centres less exposed to financial crises, which in turn would suggest that these latter financial centres can diverge from their growth pattern at a slower rate compared to financial centres that are more connected to each other.

A second question that emerges here is what factors contribute to the attractiveness of financial centres and, in turn, what explains the regional convergence at the European level and regional divergence at the national level. This issue is important because there are still relevant dissimilarities among financial centres, such as local financial regulations, corporate governance practices, and the business environment (Karreman and Van der Knaap, 2009; Klagge and Martin, 2005). In particular, previous studies have extensively investigated the organisational structure of the European financial system and the factors that contribute to the success of the stock exchange and financial market, and richness of local economies. While economic theory has traditionally attributed regional difference between financial centres to initial endowments (such as reputation, openness to foreign banks and accessibility; Jones, 1992), comparative advantages do not provide enough explanation for the spatial concentration of activity in specific financial centres with similar production structures. Financial centres benefit from a combination of agglomeration forces and market size to attract more businesses and financial services firms, high quality human resources, and services (Grote, 2008). Agglomeration mechanisms allow financial centres to improve their competitiveness through economies of scale, increasing inter-sectoral linkages, technological spillovers, and reduced transaction and transportation costs. Furthermore, Thrift (1994) and Porteous (1999), and more recently Faulconbridge et al. (2007), have emphasised that regulations and administrative procedures clearly matter for the spatial distribution of financial activities. The Bund-future market offers a clear example of the importance of regulation. In particular, due to the prevention of derivatives trading in Germany until 1990, the Bund-future market was initially traded and regulated in London even though it was primarily based on German federal bonds (Laulajainen, 2001). Subsequently, as a result of the re-regulation process, the Bund-future market moved to Frankfurt because of the advantages of the German electronic trading system, especially its cost-efficiency (Faulconbridge et al., 2007). Other examples in this regard are Luxembourg and Dublin, who appeal to hedge funds and other money managers because of their competitive fiscal systems.

The attractiveness and comparative advantage of a given financial centre is also determined by sectoral specialisation. Historically, London and New York are the main global financial centres that attract a high number of firms because of their agglomerations of financial institutions, and specialised and timely services (Wójcik, 2013). However, national or local financial centres still preserve their comparative advantages. These latter centres tend to compensate lower economies of scale and reduce asymmetric information provided by nationally-oriented firms with a higher focus on specific financial products or services (Karreman and Van der Knaap, 2009). This can favour an in-depth knowledge of supplier and costumers, which is important to conduct complex and sophisticated trades.

Aside from market characteristics, the attractiveness of financial centres is also determined by the local institutional, social, and environmental settings (Engelen et al., 2010; Gertler, 2010; Karreman and Van der Knaap, 2009). In fact, these factors exert a pervasive influence on the economy as a whole as they influence the business objectives and conduct of firms, managers, investors, and workers through an ensemble of formal regulations and legislation as well as informal societal norms (Gertler, 2004). The existence of an advanced environmental and institutional setting, together with the attraction of high-skill labour and innovation, are all factors that can specifically increase the success of financial centres and favour the agglomeration of financial services. As a result, the combination of all these factors will give rise to higher regional economic growth rates over time and further enlarge the gap between more and less advanced regions where financial centres are located. Arguably, as the relevant literature suggests (e.g. Crescenzi and Giua, 2016; Crescenzi and Rodríguez-Pose, 2011; Petrakos et al., 2005, 2011), structural socio-economic conditions in terms of productive structure, labour market, innovative capacity, and infrastructural endowment act as important determinants of regional economic growth. In particular, more advanced regions – where financial centres are typically located – can better benefit from higher economies of scale, agglomeration economies, higher level of innovation, more skilled human resources, and a more advanced market structure, compared to less advanced regions (Petrakos et al., 2011). While the attractiveness of financial centres is affected by regulatory, institutional and technological environments, financial centres are not merely passive recipients of the geography of uneven development (Lee and Schmidt-Marwede, 1993). They in fact contribute themselves to the development and growth of the economic context wherein they operate. This reciprocal effect generates a potential endogeneity issue that is typical of the economic growth-financial development relationship (e.g. Aghion et al., 2005; Henderson et al., 2013). This issue needs to be fully addressed from a methodological viewpoint.

Data and methodology

Data sample

The data on the competitiveness of European financial centres is provided by the Global Financial Centres Index (GFCI), which is produced by the Z/Yen Group in association with the City of London Corporation. The GFCI provides profiles, ratings and rankings for 75 financial centres, drawing on two distinct sources of data: external indices available at the country level (e.g. the Global Competitiveness Index (GFI), Business Environment, the Centres of Commerce Index, the occupancy costs index, and the corruption perception index) and responses to an online survey. The index encompasses five key indicators as reported below: people, business environment, market access, infrastructure and general competitiveness. People refers to the availability of good personnel, business education, and the flexibility of the labour market; business environment measures the regulation system (e.g. tax rates, levels of corruption, economic freedom and the ease of doing business); market access includes the level of securitisation, volume and value of trading in equities and bonds, and the number of firms engaged in the financial service sector; infrastructure takes into consideration the cost and availability of buildings and office space; and finally, general competitiveness refers to the overall competitiveness of the city and quality of life.

The uniqueness of the database is that the GFCI index 2 incorporates all the essential aspects identified by the economic geography literature to be important for productivity growth, agglomeration economies and increasing returns, such as a skilled and flexible labour market, access to capital, infrastructure efficiency and quality, transportation costs, and regulatory and institutional settings. We collect data for these five key indicators from the GFI Database provided by the World Economic Forum. 3 Based on the reports produced by the Z/Yen Group, the GFI displays a high correlation with the GFCI. Furthermore, it encompasses the most relevant and recurrent (listed as an important source for the GFCI for at least three years) sources of competitiveness at the country level for financial centres. We consider as drivers of the economic convergence/divergence of European regions the following indices of the GFI database: infrastructure (infrastructure); higher education and training, and labour market efficiency (people); market size and goods market efficiency (market access); business sophistication, innovation, institutions, macroeconomic environment and technological readiness (business environment), health and primary education (overall competitiveness).

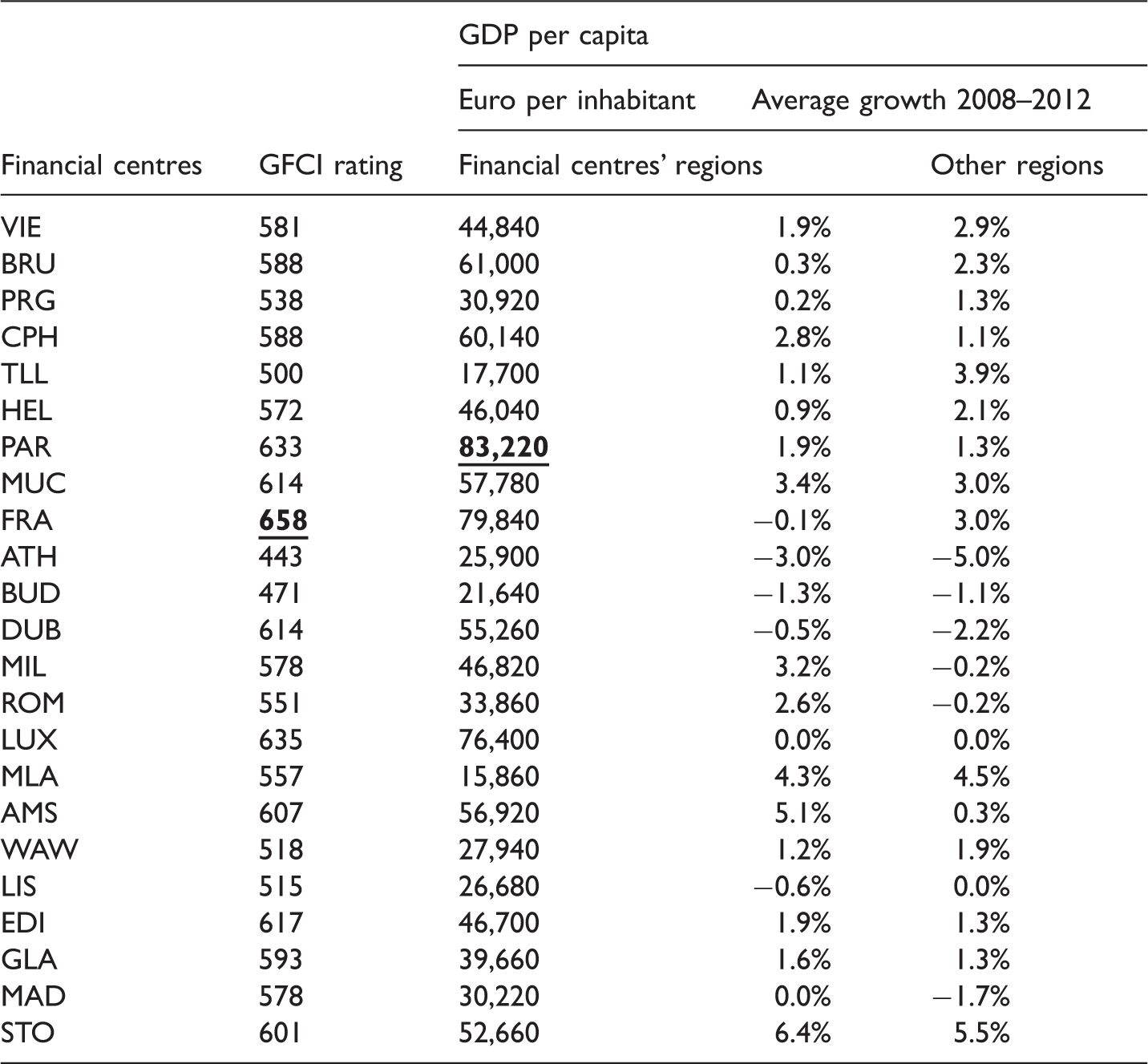

We then assess the level of welfare in terms of regional GDP per capita (GGDPPC) at the NUTS3 level. We collected the data on GGDPPC from Eurostat. Our sample covers the period 2008–2012. We exclude the City of London from our sample. Clark (2002) and Faulconbridge (2004) show that London has a different type of financial system compared to continental Europe. It has a high volume of institutional and pension fund assets, privileged interchange with the US, diversification, and different services and product ranges. London acts as an outlier in our sample because it shows a very high rating and GDP compared to the other European financial centres and regions.

Descriptive statistics.

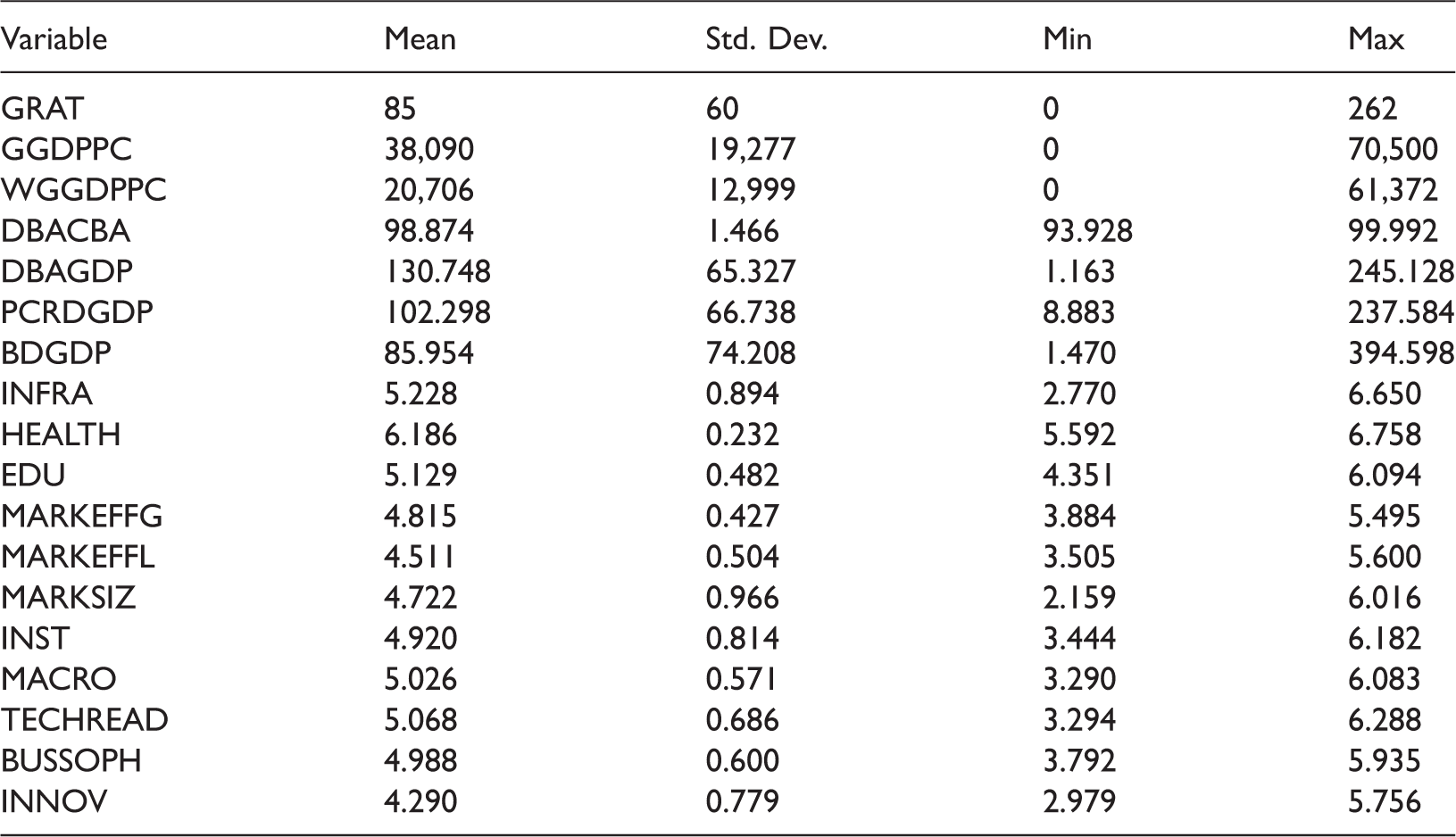

Note: GRAT: Financial centres' rating gap; GGDPPC: Economic gap between EU regions where financial centres are located; WGGDPPC: Economic gap between the region where a financial centre is located and other regions within the same country; DBACBA: Deposit Money Bank Assets/ (Deposit Money + Central) Bank Assets; DBAGDP: Deposit Money Bank Assets/GDP; PCRDGDP: Private Credit by Deposit Money Banks/GDP; BDGDP: Bank Deposits/GDP. Appendix 2 for the other abbreviations.

GFCI and GDP per capita: average over the period 2008–2012.

Note: GDP per capita: Gross domestic product (GDP) at NUTS 3 level. Appendix 1 for financial centres' abbreviations. The numbers in bold are the highest value.

Methodological approach

The methodological approach refers to the notion of a club that can be traced back to Baumol (1986). This framework examines the long-run growth determined by different tendencies in regional patterns of growth and convergence.

Differing from previous studies, we extend the club convergence model proposed by Chatterji and Dewhurst (1996) by applying for the first time a local linear non-parametric technique (Li and Racine, 2004, 2007). The majority of previous studies on club convergence use parametric estimation in order to examine the non-linear specification of convergence clubs with a few exceptions (Ezcurra et al., 2009). Our approach is more flexible as it does not require several necessary assumptions, such as the relationship form between the estimated initial and final gap, the existence of equilibria points, as well as monotonicity, concavity and homogeneity. Furthermore, the data directly determines the shape of the relationship between initial gaps and final gaps, and consequently the speed and size of convergence/divergence. We describe the main steps to replicate our analysis as follows.

We start by formalising the technology gap between a leading region and other regions, following Chatterji (1992) and Chatterji and Dewhurst (1996). Specifically, I and F are the initial and final period under investigation. The GGDPPC in a final year

By subtracting and re-arranging (3) from (2), we obtain:

Equation (4) can be re-written as:

We then apply the local linear non-parametric regression (Li and Racine, 2004, 2007) that takes the following form:

4

Equation (6) refers to the club convergence-divergence of GGDPPC gaps (GGDPPC) using the local linear estimator, whereas equation (7) analyses the club convergence-divergence of financial centres' rating gaps (GRAT). In equations (6) and (7), m(.) represents the unknown smooth function that can be interpreted as the conditional mean of the dependent variable given the independent variable, whereas

However, it must be mentioned that the analysis of the regional gaps does not allow us to identify whether the divergence/convergence is driven by the leading or lagging regions. Furthermore, the divergence/convergence process between the GDP can also be driven by further characteristics of both the regions where financial centres are located and the other regions. The relevant literature analytically explains the mechanisms of converging/diverging patterns between EU regions (e.g. Crescenzi, 2005; Crescenzi and Giua, 2016; Le Gallo and Dall'Erba, 2008; Petrakos et al., 2005, 2011). However, and given the potential limitations of the adopted methodology, one of the advantages of the non-parametric model is that it is robust to potential omitted variables (Frölich, 2007; Li and Racine, 2007). Therefore, we are still able to get robust results of the included variables without including specific regional variables for lagging regions.

Regardless of this potential advantage, and as a further robustness check, we apply a probability transition matrix (inter alia Hammond and Thompson, 2002; Pittau and Zelli, 2006; Quah, 1996) in order to examine the probability of divergence/convergence of GRAT, GGDPPC, and WGGDPPC. As a first step of the analysis we separate the estimated gaps (i.e. GRAT, GGDPPC and WGGDPPC) into four discrete states (i.e. from State 1: lower gaps to State 4: largest gaps) over the period 2008–2012 (see Appendix 3 for details).

As discussed in the literature review, there can be an endogeneity issue between financial centres' competitiveness and regional economic convergence. Such an issue should be tackled by the non-parametric regression analysis. As pointed out by Frölich (2007), non-parametric approaches permit a better treatment of the effect of heterogeneity (over the parametric specifications) since the local linear estimator gives the value of the regression function at a given point by using neighbouring observations. As a result, it minimises possible endogeneity problems that can affect the relationship between the financial centres' gaps and regional economic gaps. We also address the endogeneity problem by running a non-parametric instrumental variable regression. This is important because the vast majority of the previous empirical investigations do not include endogenous regressors in their non-parametric regression analysis. In particular, by following Horowitz (2011), we employ a methodological framework that directly incorporates the instrumental variables into the estimation. This framework is based on a local polynomial kernel regression. Specifically, the applied estimator allows – under the presence of instrumental variables – m in equations (8) and (9) to be defined as a Fredholm equation of the first kind, which is the solution to an ill-posed inverse problem. 5 This enables us to directly address the endogeneity issues without imposing any functional form on, and linearity between, the variables. For the choice of the instrument variables to be included in our model, we follow the procedure introduced recently by Henderson et al. (2013). They propose a rigorous and innovative approach to select appropriate instrumental variables in a non-parametric regression framework. As a result, we first regress the potential instruments on the regional economic gaps by employing a local linear least square regression (Li and Racine, 2007). We then select only the variables that are not related to the dependent variable (regional economic gap, see equations (8) and (9)). A further step of our analysis is to examine the correlation of the selected instruments with the endogenous regressors and we use them as instrumental variables in the non-parametric IV regression. After applying the described procedure, consistent with Henderson et al. (2013), we use the following instruments: Deposit Money Bank Assets/ (Deposit Money + Central) Bank Assets (DBACBA); Deposit Money Bank Assets/GDP (DBAGDP); Private Credit by Deposit Money Banks/GDP (PCRDGDP); and Bank Deposits/GDP (BDGDP).

Empirical results

Convergence clubs for financial centres and regional GDP per capita

In this section, we discuss the results that we obtain for the club convergence of our sample of 23 EU financial centres. In particular, we assess how various global financial centres (such as Frankfurt, Luxembourg and Paris), and second and third-tier financial centres were differently affected by the GFC. This analysis also allows us to better understand whether the reduction of economic regional inequalities where financial centres are located is explained by a loss of competitiveness by top-tier financial centres rather than the catch-up process of second and third-tier financial centres.

Figure 1 shows the convergence of the GFCI index (Figure 1a) and GGDPPC between the regions where the financial centres are located (Figure 1b) in 2008 compared to 2012. In Figure 1(a), we see that there are two clubs of financial centres in Europe, which indicates the existence of multi-equilibria points. Specifically, the first club encompasses the financial centres that have the highest GFCI, such as Frankfurt, Luxemburg, Paris, Dublin, Edinburgh and Munich, and those with a mid-high level GFCI. The group of leading financial centres in terms of competitiveness, which includes Dublin, Edinburgh, Luxembourg, and Paris, shows a diverging pattern from Frankfurt over the period 2008–2012. In a borderline position between the first and second club, there are the financial centres in western Europe with a mid-high GFCI, such as Amsterdam, Stockholm, Copenhagen, Munich, Glasgow, Helsinki and Vienna. Among them, the Nordic financial centres, Helsinki, Copenhagen and Stockholm, converge toward the top club.

Convergence clubs for financial centres and EU regions where they are located.

The second club includes the financial centres in Western Europe (such as Milan, Rome, Madrid, and Brussels) that have a transnational profile. These centres maintain a leading position with respect to the other Eastern and Western financial centres such as Lisbon and Athens. Several Eastern European financial centres, such as Warsaw, Prague, Budapest, and Tallinn exhibit a careful increase in competitiveness during the period 2008–2012. The existence of multiple clubs among financial centres aligns with the findings of Poon (2003), who shows that the global system of world financial and capital centers (WFCC) is characterised by different tiers. Moreover, our findings suggest that regardless of the increased trend of competitiveness among the cross-country regions in which the financial centres are located, there are still consistent intra-country regional discrepancies. This is due to the fact that industrial production and financial activities have been mainly concentrated in the capital cities in which financial centres are located. This finding aligns with the view held by Klagge and Martin (2005), who argue that financial markets operate in a non-neutral way. This means that the concentration of capital markets in a specific region has a detrimental effect on the allocation of funds and resources with respect to other (non-central) regions.

Figure 1(b) shows the convergence and divergence patterns between the GGDPPC gap of European regions where financial centres are located and the leading city, Paris. What emerges from Figure 1(b) is that the speed of convergence and divergence of regional economies is slower and characterised by more steady states as suggested by previous studies (e.g. Le Gallo and Dall'Erba, 2008). This finding confirms that there is a persistent inequality within European regions with two convergence clubs within the wealthier EU regions. Among the second club of rich regions, Brussels and Dublin show a diverging trend from the leading centres. In contrast, Stockholm, Amsterdam, but also Munich appear to catch up with the richer regions in terms of both competitiveness, as seen earlier, and welfare. Furthermore, it is evident that the financial crisis has slowed the economic growth of the majority of financial centres. In contrast, we find that the regions of Frankfurt, Paris and Luxemburg, where the top European centres are located, grew at a constant rate over the entire period. These results are consistent with several empirical studies (Corrado et al., 2005), which state that economic convergence is more likely to happen for highly developed economies.

A third club consists of the western European regions that exhibit a decreasing trend compared to the leading regions. A diverging trend is also evident for low-productivity eastern regions, such as Tallinn, Budapest, Warsaw and Prague. This in turn suggests the existence of a persistent trend rather than a cyclical trend for some eastern European economies. The dynamics of financial centres' inequalities during the examined short-term period appear to slow down regions' economic growth prospects.

Estimated average of annual transition matrixes for 2008–2012.

Note: The numbers in bold are the diagonal elements. State1 = Smaller Gap (1st Quartile) to State 4 = Larger gap (4th Quartile); GRAT: Financial centres' rating gaps; GGDPPC: Economic gap between the EU regions where financial centres are located; WGGDPPC: Economic gap between the region where a financial centre is located and the other regions in the same country.

Financial centres' competitiveness and the European economic converging trend and national diverging trend

This section addresses our first research question, namely whether the convergence of competitiveness of financial centres could help to explain the two opposite dynamics (economic regional convergence and divergence) at the European level.

In particular, Figure 2 examines the effect of the convergence of the financial centres' ratings gaps (GRAT) on the regional inequality measured in terms of GGDPPC of the regions in which financial centres are located.

8

The impact of financial centres' rating gap on the economic gaps of European regions.

Figure 2(a) shows the results for the non-parametric regression (Li and Racine, 2007) (red dash-dotted line). To take into account the possible endogeneity issue between the GFCI rating's (GRAT) gaps and the gaps in terms of GGDPPC between the regions where financial centres are located (GGDPPC) we also run a non-parametric instrumental variable regression (Horowitz, 2011) (blue dashed-line). Our findings suggest that an increase of the gaps of financial centres' rating levels (GRAT) has a positive effect on the in-terms GGDPPC gap between the regions where financial centres are located (GGDPPC), as indicated by the increasing non-parametric line. A similar trend is also confirmed by the non-parametric instrumental variable regression. These two findings provide strong support for the fact that the competitiveness of financial centres contributes to explain the economic converging trends of the regions where financial centres are located. However, this relationship appears to follow a non-linear pattern especially when we focus on the non-parametric instrumental variable regression (dashed line).

Figure 2(b) focuses on the relationship between the GRAT's gaps and the gaps in terms of GGDPPC between the regions where financial centres are located and the other regions within the same country (WGGDPPC). In a similar manner, our findings suggest that WGGDPPC decreases as the GRAT increases, which indicates that an increase in financial centres' competitiveness contributes to the enlargement of existing inequalities between regions within countries (WGGDPPC). Furthermore, we note that in this case the line of the non-parametric instrumental variable regression has a remarkable curvilinear pattern. Overall, this result shows that financial centres also contribute to determine the diverging trend between regions at the national level. This would suggest that the regions where financial centres are located attract resources from more peripheral regions in this way enlarging their existing gap with them. Poor regions therefore become poorer, while rich regions can reinforce their prevailing position. This finding again verifies the non-neutrality hypothesis described previously. It means that the allocation of resources is concentrated only on the regions in which the financial markets are located (Klagge and Martin, 2005).

F-statistics and estimated p-values of the nonparametric regressions.

Note: GGDPPC: Economic gap between the EU regions where financial centres are located; WGGDPPC: Economic gap between the region where a financial centre is located and the other regions in the same country. Appendix 2 for the other abbreviations.

p<0.1.

p<0.05.

p<0.01.

Non-parametric regressions between GDP gaps and the main drivers of financial centres' competitiveness.

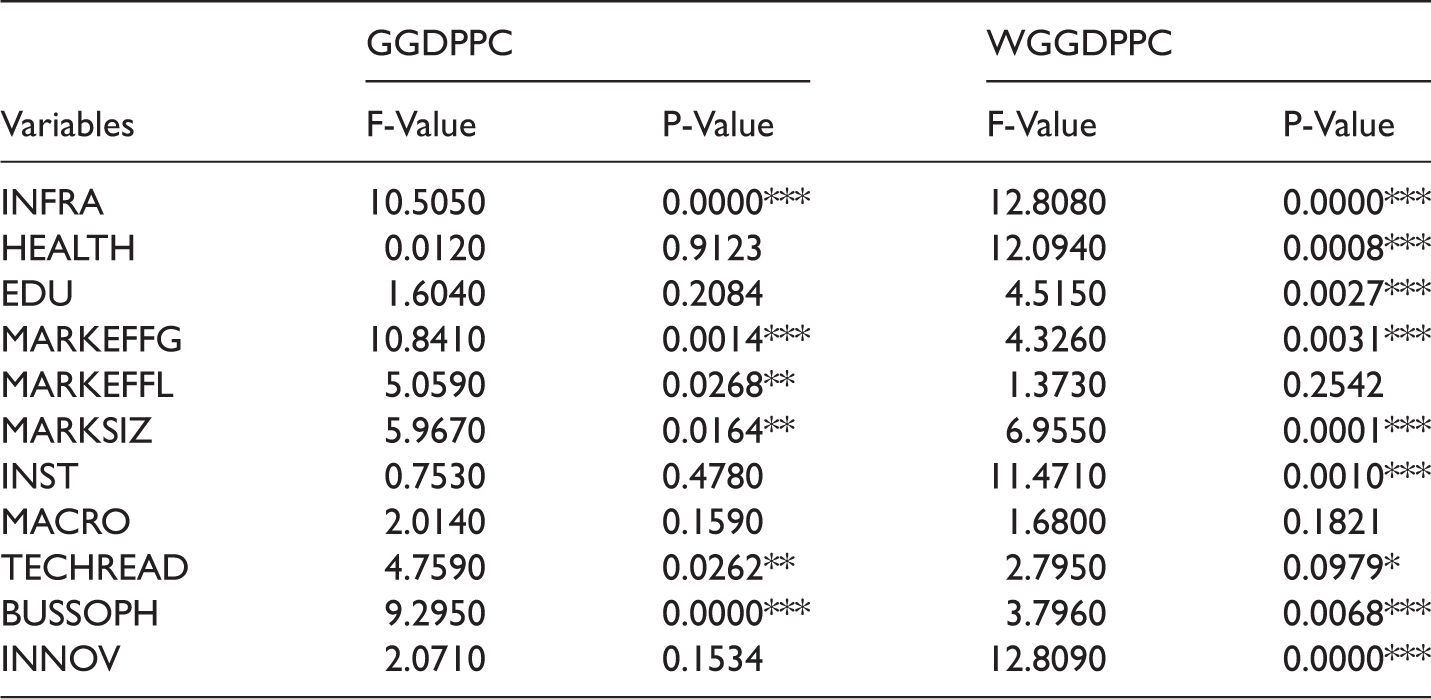

From Table 4, we observe that the competitiveness drivers of the GFCI exhibit a contrary impact on WGGDPPC and GGDPPC. This is plausible since the GFCI exerts a diverging impact on WGGDPPC and GGDPPC. As depicted in Figure 3(a,1–2), our results provide evidence that infrastructure (INFRA), goods market efficiency (MAREFFG), market size (MARKSIZ) and business sophistication (BUSSOPH) contribute to the economic catch-up process of regions where financial centres are located. These findings provide further support for existing studies (e.g. Petrakos et al. 2011) that find similar sources to be important factors for economic growth, especially in the case of wealthier regions. These regions are more likely to benefit from agglomeration economies, positive externalities and a high-skilled labour force. As a result, they grow faster and tend to accelerate their interregional divergence pattern with respect to less wealthy regions. When looking at the role of key drivers of WGGDPPC (Figure 3b,1–2), we find that infrastructure (INFRA); health and primary education (HEALTH); higher education and training (EDU); goods market efficiency (MARKEFFG); market size (MARKSIZ); institutional quality (INST); technological readiness (TECHREAD); business sophistication (BUSSOPH); and innovation (INN) all have a highly significant impact (Table 3). Consistent with previous studies (Crescenzi and Giua, 2016; Crescenzi and Rodríguez-Pose, 2011; Petrakos et al., 2005, 2011), our findings confirm the importance of structural socio-economic conditions, such as market forces, policy factors, and infrastructural endowment for regional economic convergence. In particular, we find that the quality of transport, electricity and telephony infrastructure (INFRA), 9 high levels of efficiency of the institutions (INST) (in terms of adequate property rights, low undue influence, government efficiency and security), ITC use, technological adoption (TECH READ), and business sophistication (BUSSOPH) reduce regional disparities within a country. In contrast, market size and efficiency, health and primary education, and capacity of innovation appear to enlarge the interregional gaps within a country (WGGDPPC). In line with Crescenzi (2005)'s argument, freely available technological knowledge (such as TECHREAD) can favour convergence among regions, while innovative activities acquired through education, R&D investment and other innovation activities (such as INN) can lead to regional disparities, due to the accumulation of knowledge in wealthier regions. This can therefore explain the contrasting trend between TECH READ and INN.

Furthermore, as suggested by Rodríguez-Pose and Fratesi (2004), an increase in market access and the opening of borders could help wealthier regions to compete in integrated markets as they are able to attract more innovative firms and high-skilled labour. In contrast, poorer regions within a country cannot usually rely on the same entrepreneurial activities as wealthier regions. They depend more on public employment, State and European support and are therefore less capable of competing in more integrated markets. An open market, MARKEFFG and MARKSIZ, can thus contribute to the catch-up process of regions where financial centres are located on an international basis, but at the same time can harm the economic converge process within a country.

Concluding remarks

This paper provides further insight on the role of financial centres in the creation of the opposite convergence dynamics that appear to prevail for national and regional economies in Europe. In particular, we examine this issue from two different perspectives. First, we analyse the economic converging process between the regions of financial centres at the cross-country level. Second, we investigate the converging process among the regions of financial centres and the other regions in the same country. From a methodological viewpoint, we extend the club convergence model proposed by Chatterji (1992) and Chatterji and Dewhurst (1996) by applying for the first time a local linear non-parametric technique (Li and Racine, 2004, 2007).

Our results show that the convergence of financial centres' competitiveness reduces the economic inequalities of the regions where they are located. As a counter effect, we find that the reduction of the gaps of financial centres' competitiveness sharpens the inequalities between the regions of financial centres and other regions within the same country. This result is consistent with the view of Klagge and Martin (2005), who argue that the relationship between finance and the real economy is non-neutral. This means that the spatial structure of the financial system can lead to a geographical bias for resource and investment allocation. This can be explained by the fact that the regions of financial centres can absorb investments and skilled labour from other regions. They therefore grow in a disanalogous mode with respect to the other regions. As a consequence, this can initiate a diverging process between the regions of financial centres and the rest of the country's regions.

We also provide evidence that the drivers of financial centres' competitiveness such as market efficiency, market size, education and innovation can reduce the existing economic gaps between regions where financial centres are located. This is line with Poon (2003), who argues that broad and deep markets, human capital, and market efficiency contribute to the development of a financial and capital centre. We however find that the same factors enlarge the existing economic gaps between the regions of financial centres and other regions. Conversely, technological readiness, the efficiency of institutions, business sophistication, and infrastructure can speed-up the convergence process between the regions of financial centres and the other regions. Finally, our findings remain the same also when we control for potential endogeneity problems between the competitiveness of financial centres and the regional economic convergence/divergence.

Some key limitations should be considered when interpreting these results. The adopted convergence model does not clearly allow us to identify whether the gap is driven by leading or lagging regions. We are also aware of the fact that there are other characteristics of leading and lagging regions alongside specific growth mechanisms, such as R&D expenditure, patent intensity, productivity growth, spillover effects, and European Funds (Crescenzi, 2005; Crescenzi and Giua, 2016; Le Gallo and Dall'Erba, 2008; Petrakos et al., 2005, 2011; Tselios et al., 2012) that could affect the converging/diverging patterns between regions. We do not include them in our analysis. Furthermore, national factors can explain the regional within-country convergence/divergence only when these factors also reflect those of the regions where financial centres are located. Finally, our analysis focuses solely on the period of the GFC.

Nevertheless, our findings still provide relevant policy considerations. Policy interventions that are aimed at maximising the sources of competitiveness of the GFCI may penalise the regional economic catch-up of less advanced regions. This can occur when resources, e.g. investments and labour, are centralised towards more advanced regions in which financial centres are typically located. It is therefore crucial that interventions for regional development take into account both the international needs and pressures of the regions where financial centres are located along with the needs of more peripheral regions. The increase in the competitiveness of financial centres might therefore require counterbalancing the aggregation of financial services in a specific location with a network of financial institutions and services dedicated to the support and stimulation of the local regional demand and economies. In this context, regional development policies can play a pivotal role in supporting a more decentralised financial system. As suggested by Klagge and Martin (2005), this can be achieved through the development of local capital markets in terms of institutions, networks, and agents. Furthermore, national-level interventions that improve the quality of infrastructure, the skills and knowledge of human resources, market access, efficiency of business environment, and overall competitiveness can also contribute to regional convergence dynamics. In accordance with Crescenzi and Giua (2016)'s arguments, this suggests that EU policies aimed at reducing regional inequalities should take into consideration not only territorial conditions, but also the national socio-economic environment.

The paper can be further extended in several directions. One of these might be by focusing on possible spill-over effects between regions by collecting additional data at the regional level to examine the convergence pattern of EU regions. Alternatively, an additional extension of our study might explore the ways through which resources move between regions to better understand the factors underlying the regional economic dynamics. Finally, Brexit is likely to alter the existent equilibrium and competitiveness of EU financial centres. It would be therefore be of great interest to analyse how Brexit could affect the regional economic dynamics in continental Europe.

Footnotes

Acknowledgements

We would like to thank Professor Jessie Poon and the three anonymous reviewers for their helpful and constructive comments on an earlier version of our manuscript. Any remaining errors are solely the authors’ responsibility.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.