Abstract

Participants in the U.S. maker movement generate market-worthy consumer goods from the bare bones of novel ideas and simple production equipment. For cities and policymakers, making thus represents the opportunity to develop new manufacturing industries and employment. For makers to transform themselves into large-volume producers, however, they must negotiate significant financing, production and distribution barriers without recourse to the capabilities of the large manufacturing firm. Drawing on 137 interviews with makers and maker-supporting organizations, we call attention to the challenges of “manufacturing without the firm,” as well as the extent to which the localized institutional ecosystems in which makers are embedded may help them circumvent these challenges. Our findings indicate that the maker movement's generative prospects rest on these firms' ability to negotiate problems of production and markets that have beset clusters of small firms for many decades.

Introduction

The maker movement promises the revolutionary change of allowing artisans, tinkerers and digital-era inventors to move products from the workshop to mass production — without the infrastructure of the large manufacturing firm (Dougherty, 2012; Waller and Fawcett, 2014). In doing so, creators and entrepreneurs can potentially free themselves from the costs, conservatism and constraining bureaucracy of large industrial organizations (Aldrich, 2014). Freedom from the need to conceptualize product innovations for the large consumer markets favored by vertically integrated firms opens many new market opportunities. As small-scale and potentially emergent manufacturers, makers have the potential to decentralize innovation, add to the national pool of entrepreneurs, strengthen manufacturing supply chains and generate new industries and propulsive firms. Their ability to do so, however, rests on the viability of making as a stable manufacturing production model – the ability to manufacture without the firm.

Using minimal capital investment and, increasingly, the distributed infrastructure of the internet, individual maker-entrepreneurs apply their ingenuity to technical problems and respond to growing consumer demand for products characterized by authenticity and quality. However, manufacturing without the firm means finding a way to replace the firm's machinery for financing, producing and distributing products (Williamson, 1981). Even as conventional manufacturing firms constrain many types of innovation, they provide capital, production equipment, access to production networks, and a range of specialized and diverse skillsets for designing products and bringing them to market. While outsourcing has greatly shrunk the core of large manufacturing firms, those cores maintain resources and relationships of both a scale and a scope far beyond what individual makers possess (Herrigel, 2010). Thus, the speculative project of manufacturing without the firm requires makers to fulfill basic finance, design, production and distribution needs through alternate channels. With public resources for makers and makerspaces joining innovation-themed programs for smart cities, co-working spaces and manufacturing innovation, the ability of makers to justify public support for their efforts hinges on their heretofore undocumented capacity to expand from product design to manufacturing (Clark, 2013; Shelton et al., 2014).

Drawing on 137 interviews with makers and maker-supporting organizations, this paper evaluates makers' strategies for accessing capital, production networks and mass markets without the infrastructure of the manufacturing firm. We document a range of creative strategies and tactics makers use to circumvent, displace, mitigate or transform these problems over the short term. We argue that collectively, these tactics push makers towards niche production strategies that become significant barriers to makers' ability to scale up production over the long run. In particular, niche-market approaches generate short-term profit and stability at the cost of tying down the capital, labor, time and organizational resources needed to scale up to mass-market production.

From making to manufacturing

The maker movement's technical drivers remain simple in comparison to the technologies on which highly specialized manufacturers rely. A basic 3D printer, for example, consists of an injection-molding canister and guide rails, and retails for $500 or less. The printer's value lies both in access and in process: the low price point expands the pool of potential manufacturing entrepreneurs, and easy use allows tinkerers to experiment, iterate and adapt product prototypes with few barriers (Berger, 2013; Clark, 2013). Laser cutters, lathes and other basic production equipment also sell for increasingly low prices.

Like prior rounds of technological invention, the changes behind making potentially rearrange the processes of entrepreneurship, firm growth and regional economic differentiation (Harrison, 1994; Piore and Sabel, 1986; Scott, 1988a). The maker movement's outspoken advocates point to the prospect of substantial changes in manufacturing economies. They note that proliferations of makers can enhance regional pools of entrepreneurs, thus providing indispensable opportunities to develop new firms, industries and technologies. More subtly, but perhaps more important, proponents of making note the possibility that numerous new, small maker enterprises will strengthen the social, material and organizational ties on which strong regional manufacturing complexes currently rely (de Propris, 2013).

Thus, makers need not scale up for local economies to benefit from their activities. Tinkerers, failed entrepreneurs and makers with little or no interest in earning a living from their work still disseminate innovations in design and production knowledge, thicken relationships between suppliers and producers, and contribute to the sense of place increasingly vital to luring firms and skilled migrants (Donald et al., 2013; Markusen and Schrock, 2006). Equally important, making provides a coping mechanism for entrepreneurs and creative professionals who lose payroll jobs and professional opportunities during periods of economic contraction and technological upheaval (Donald et al., 2013). A large and perhaps majority share of makers consists of individuals with these limited commercial aspirations (Dougherty, 2012). Such small-scale and non-commercial making has a potentially broad geography, one rooted in basements, garages, suburbs and rural areas, in addition to large cities.

Making's most substantial economic potential, however, emanates from individual producers’ ambitions to scale up. They aspire to use specialized technical knowledge and batch production methods to create and then sell unique products. In doing so, they find that democratized access to technology does not ensure democratized access to capital, nor to interfirm relationships and other inputs. Like firm networks in Northeast-Central Italy, Southern California and other “new industrial districts” that achieved stability amidst mass job loss in the 1980s, makers draw on urban agglomerations. Cities offer many production assets external to the firm, including low-cost production equipment, specialized design knowledge, dedicated commercial real estate, and manufacturing advocacy institutions devoted to helping makers develop and sell products (Piore and Sabel, 1986; Scott, 1988b; Teece, 1986, Wolf-Powers et al., 2016). 1 Beyond the shared traits of small size and reliance on network resources, however, makers differ substantially from the small manufacturing firms featured in the literature on new industrial districts. A fundamental difference originates in machinery. The need and ability to reset machines for short production runs provided the impetus to flexible specialization, and launched a decade of scholarship that assessed firms' ability to expand sales by tacking back and forth between short product runs (Hirst and Zeitlin, 1991; Scott, 1988a). Makers, however, typically use craft methods or simple machinery. And while analysis of new industrial districts emphasized the smallness of thriving firms, the objects of study were nevertheless still firms, which enjoyed capital, clout, routines and internal diversification extending far beyond what most makers possess (see Harrison, 1994). Finally, new industrial districts centered on particular types of specialized products or technologies: aerospace in Southern California, fashion in Emilia-Romagna, photonics in Rochester. By virtue of their craft and small-batch production processes, and the modest start-up barriers they face, makers within a given region produce a broad range of heterogeneous products, and rely much less on standards-setting institutions and government contracts (Wolf-Powers et al., 2016). While a region's prior industrial specializations shape the types of goods makers conceptualize and produce, makers within a given city nevertheless make products ranging from foodstuffs to fashion items, electronic devices, and consumer durables (Harrison, 1994).

Equipment matters less, too. While commercially successful making typically depends on the miniaturization of production equipment (Dougherty, 2012), the maker movement's vitality arguably depends more on the knowledge and connections made available by the Internet (Marsh, 2012). Internet connections provide knowledge on production methods and processes; access to equipment and materials; connections to crowdsourced funding; directories of suppliers and contract manufacturers; and perhaps most important, wholesale, retail, niche and direct-to-consumer sales outlets. In addition to these instrumental contributions, the Internet and social media have strengthened “place-propinquity”: commercially powerful, affective identification with cities and their performed cultures and social networks (Jurjevich and Schrock, 2012).

To manufacture successfully without the infrastructure of the firm, makers must find a way to move from prototyping to scale. Their ability to do so with success appears to rest on the contributions of the local, collaborative social infrastructure – specialized producer services organizations and retailers, low-cost real estate, and not-for-profit support – that distinguishes making from other forms of entrepreneurship (see Wolf-Powers and Levers, 2016). Such organizations have improved makers' access to (comparatively) low-cost real estate in particular. This paper argues that the larger-scale conversion of making into fully fledged manufacturing requires responses to a more complicated set of problems regarding financing, supply chains, production networks and organizational development.

Manufacturing without the firm

Selling consumer products at scale necessitates resources and assets that lie beyond the immediate reach of individual makers. In principle, makers seeking scale-up can acquire such capabilities through the market, to which the dissolution of vertically integrated firms has pushed design and product development services (Christopherson and Clark, 2007b; Dicken, 2003). Kickstarter and crowdfunding sources take the place of third-party investment (Mollick, 2013); supply chain intermediaries (such as Makerbiz, Makers Row and Britehub) provide access to parts; contract manufacturers make the goods; and internet retailers, including Amazon, Etsy and Shopify, allow makers to reach consumers without developing their own distribution infrastructure.

Along with publicly supported makerspaces, these organizations represent key components of maker-specific entrepreneurial ecosystems. Entrepreneurship scholars conceptualize these ecosystems as containing a large and varied mix of services, infrastructure and social relationships upon which entrepreneurs draw as they develop products (Spigel, 2017). However, capitalizing on such opportunities requires makers to identify, price and monitor numerous and diverse market mechanisms without overwhelming their scarce organizational resources. This problem of organizational limitations, and the related problem of transaction costs, constitutes a central barrier to makers becoming successful entrepreneurs.

The organizational infrastructure with which to incorporate these ecosystem components must come from makers themselves. Makers typically have two or fewer employees, and lack organizational infrastructure with which to mitigate the transaction costs involved in negotiation with external organizations (Powell, 2003; Williamson, 1981). The firm's routines and diverse skills allow production functions to remain in-house at high efficiency, and provide diverse capabilities (research, market knowledge, production experience) that make external transactions cost-effective (Nelson and Winter, 1973). Like large manufacturing firms, makers operate in urban agglomerations that provide a large and varied range of flexibility-enhancing resources for financing, innovation, production and distribution (Christopherson and Clark, 2007a).

Yet individual makers lack the organizational capacities, relationships and power large manufacturers use to bend market relationships to their advantage (Markusen, 1999). Makers also incur steep costs as they struggle to navigate supply chains whose architecture remains opaque as a matter of lead-firm strategy (Christopherson and Clark, 2007b). Similarly, short production runs restrict makers' ability to benefit from the economies of scale vital to the use of these networks (Coe and Hess, 2013). The search and transaction costs of identifying contract manufacturers and suppliers often overwhelm firms with significantly more financial capital and organizational resources than makers possess (Berger, 2013; Phelps and Fuller, 2016).

Makers also have minimal resources with which to confront basic financing problems. The large firm provides a means of funding product research, production and delivery, especially for products that require mass-market penetration to pay off. Through credit, equity investment and retained earnings, large manufacturing firms enjoy multiple means of accessing comparatively low-interest-rate capital (Hart and Moore, 1990). By contrast, entrepreneurs must risk personal assets to obtain capital, and often struggle to find venture capitalists with the knowledge necessary to evaluate specialized innovations (Motoyama and Wiens, 2015; Stiglitz and Foss, 2009). As entrepreneurs who sell novel goods for which end markets are either splintered, unique or unformed, makers face exaggerated versions of these problems.

Making's potential to generate industry growth rests on makers' responses to the many barriers they face in scaling up. Optimistic accounts of making, such as Anderson's (2012) claim that it will spur a “new industrial revolution,” argue, in effect, that the combination of cheap production equipment and entrepreneurship resources will allow makers to establish successful manufacturing firms. In order to do so, however, makers will need to devise business strategies that simultaneously address problems of production, procurement, organizational structure and market fragmentation (Hudson, 2001). In short, their entrepreneurial success will depend upon the strategies they devise to overcome the business problems they face. Accordingly, we ask basic questions about how makers' business models work. What strategies do makers undertake to move from product design to mass production? How do those strategies position them within consumer markets? And how do emergent competitive strategies draw on local entrepreneurial resources?

To answer these questions, we identify and evaluate makers' responses to challenges in scaling up finance, production and distribution. At the level of individual products, makers' quality-based competitive strategies resemble the paradigmatic niche-market approaches of post-Fordist manufacturing (Amin, 1994; Harvey, 1989). However, extreme organizational nimbleness and radically reduced prototyping costs allow individual makers to compensate for the limited size of individual product markets by producing several niche products at a time. This approach provides enhanced stability within currently limited consumer markets, but entails the distinct costs of (1) tying up the time and finances needed to develop new organizational capabilities and (2) favoring the development of products with limited consumer appeal. As in the flexible specialization model, makers' prospects for thriving and scaling depend on localized networks of auxiliary producer services firms as well as supply chain and property market intermediaries working to bind firms into clusters and existing social networks.

Data and methods

We answer questions about scale-up barriers and makersr competitive strategies with evidence from a database on makers in New York, Chicago, and Portland, and 137 total interviews with makers and maker-supporting organizations in those cities. We selected these cities to maximize the range of likely maker challenges and outcomes within a pilot study. Exploratory fieldwork indicated differences in the focus of maker activities within each city, with New York makers developing fashion and design goods, Chicago makers specializing in industrial products, and Portland makers specializing in craft-based products. These characteristics, combined with existing manufacturing research connections and ability for the principal investigators to maximize the number of completed interviews, led to the selection of these sites. The resulting database and interview data provide what is to our knowledge the most extensive source to date of empirical information on this much-discussed but little-documented movement. Our selection of these three cities comes at the cost of evaluating the growth of maker enterprises in smaller, less industrially diversified cities that provide makers with fewer resources for design, production and distribution.

We define makers as individual producers engaged in both the design and the production of physical products, and active in efforts to sell their goods (citation redacted). This definition differentiates makers from conventional entrepreneurs in methodologically useful ways. It excludes entrepreneurs specialized in services, retail or software applications (who do not have to contend with the distinct problems of making things). At the same time, this definition excludes contract manufacturers or craft producers who make goods to order for others. In addition to narrowing the object of study from entrepreneurship, these conditions focus us on a subset of makers seeking economic gain, and exclude hobbyists and software engineers. 2 Our definition accounts for the entrepreneurial lifecycle, and provides the advantages of falsifiability and external verification.

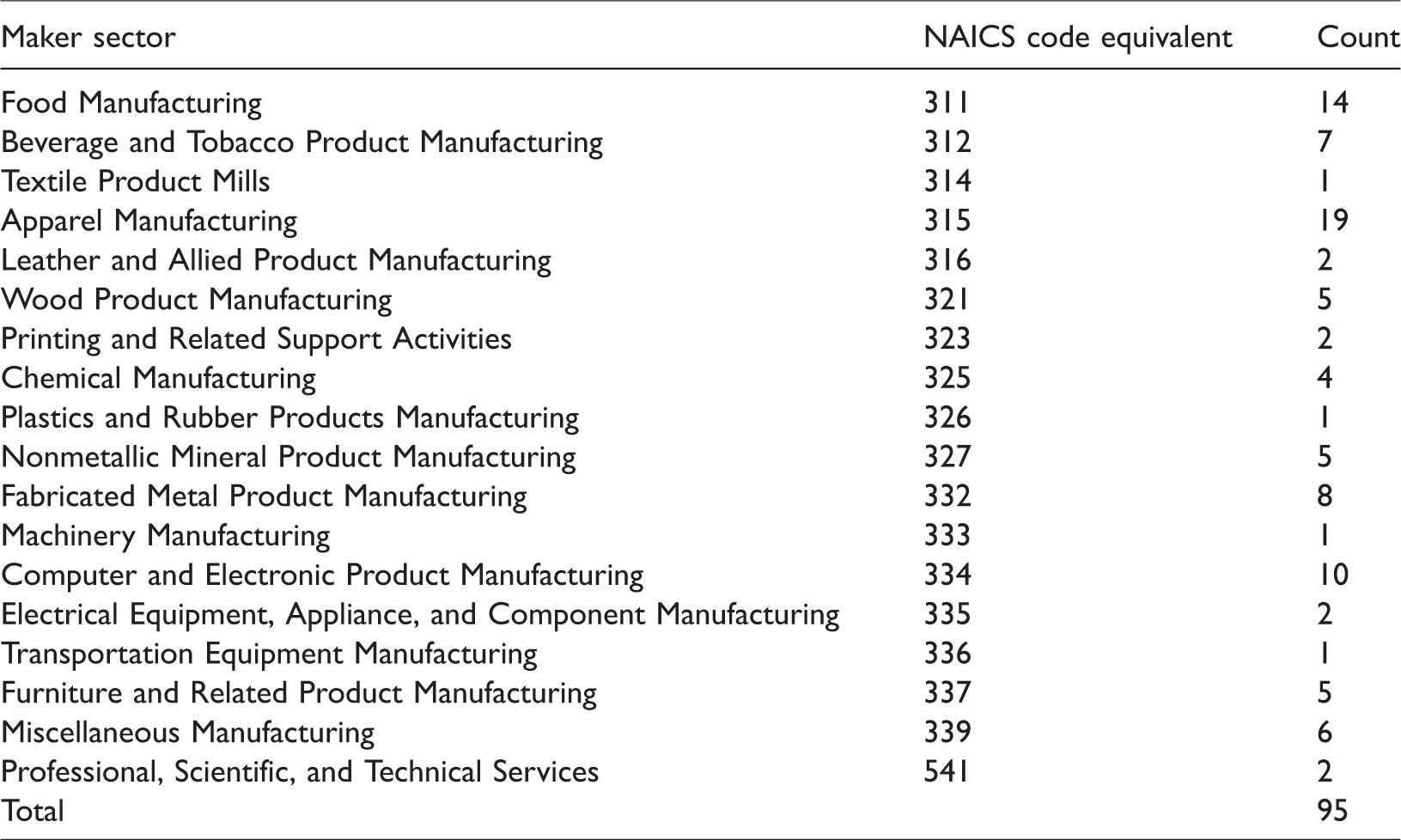

Using these criteria, we developed a three-step process for compiling a database of makers. We identified more than 1900 “candidates” from (a) lists of past and present participants in maker spaces and maker faires, (b) internet searches for craft and artisanal manufacturers, and (c) existing databases of makers, craft and artisanal manufacturers. Second, we identified web sites and social media accounts for each maker, and used those resources to confirm the maker remained active. Each active maker was then categorized according to product type. Working from a list of more than 200 makers in each city, we conducted a total of 137 research interviews between May 2015 and April 2016. We conducted the interviews at sites of the makers' choosing, typically a maker space, business office or nearby cafe. Interviews lasted between 20 minutes and 3 hours, with the median interview lasting more than 45 minutes. Makers specializing in food products and apparel were more likely than others to respond to our interview requests. The purposive sample drawn from our database minimizes the potential measurement error from non-response by ensuring minimum coverage thresholds for different types of products in each city. The broad distribution of interview participants across product categories reflects this approach (Table 1). While we sampled makers to ensure a broad coverage of product types (and thus production problems), our sample necessarily reflected the relative infancy of maker businesses. Based on the interviews with makers, we identified a list of 90 maker-enabling institutions – maker spaces, entrepreneurship programs, incubators, financiers, etc. – and interviewed a minimum of 10 in each city.

Industrial distribution of makers interviewed in Chicago, New York City and Portland, OR.

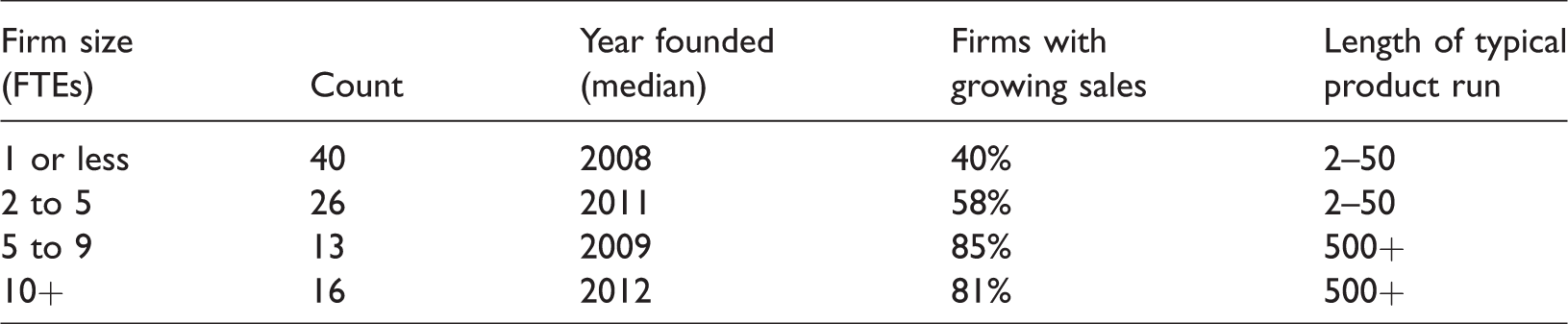

As our definition of making suggests, and our research questions specify, our interview subjects consisted primarily of relatively new businesses attempting to expand their operations. Nearly half (48%) of the maker businesses we interviewed were less than five years old at the time we conducted field work. Nearly, three-fifths (58%) of the makers in our sample had experienced sales growth in the prior year. Growth was the rule rather than the exception for makers in every size category except for those with one full-time-equivalent employee or less (Table 2). Regardless of their sales trajectory, however, the overwhelming majority of the makers in our sample were actively negotiating scale-up problems. Our analysis combines findings about makers who succeeded in overcoming scale-up challenges with findings about makers who were currently struggling with those same challenges, or who had failed in their attempts to do so. As systematically as possible in the sections that follow, we provide information on the size and scale-up status of the individual makers we interviewed.

Size, age and sales trajectory of maker firms.

We found that makers rely on a range of practices to overcome business barriers. These practices yielded short-term successes. Cumulatively, however, makers' creative problem-solving steered them toward niche and luxury markets. This suggests limits on the types of goods, markets and practices makers can pursue as they attempt to scale innovations into commercial products. Thus, we argue that makers’ tactical responses to scale-up challenges carry the price of adding to the barriers to scaling up over the long-term.

Access to capital: Kickstarter, family funding and alternatives to corporate finance

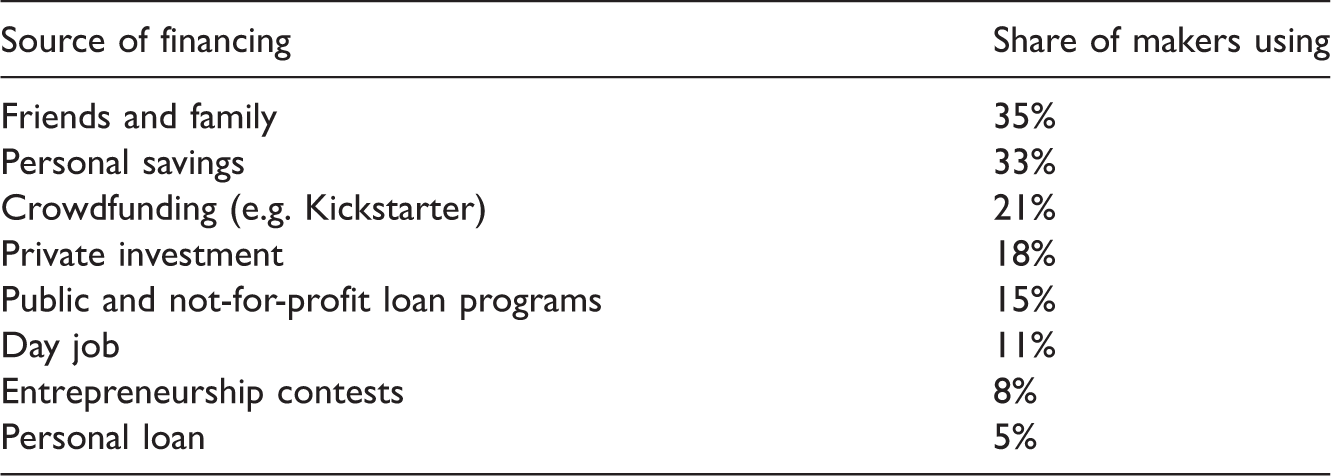

Prototyping equipment, printers, makerspace memberships and most of the raw materials necessary to build prototypes of consumer goods come cheaply. However, production equipment, office space, inventory and distribution relationships require significant investment capital and extensive institutional relationships (Gilson et al., 2009). Makers resemble non-maker entrepreneurs in requiring outside investment to finance the move from product prototyping to business and market expansion (Motoyama and Wiens, 2015). As such, they face the small entrepreneur's familiar problems in accessing capital on favorable terms: There's so much I don't know about right now. Small businesses need more funding and easier access to loans, since a lot of large banks aren't willing to give small businesses loans. We then have to go elsewhere, with higher interest rates. [food maker, New York] We financed the business ourselves. We never borrowed money. We had a line of credit at some point. We did a little credit card finance [and] we put a little in ourselves, but mainly we got money by collecting on what we shipped. [food maker, New York]

Sources of maker financing.

Source: Maker Interviews. Because most makers use multiple forms of financing, totals do not add to 100.

Makers use three basic strategies to overcome capital formation challenges. As is the case with entrepreneurs generally, these strategies draw on personal connections and relations of trust (Spigel, 2017). First, more than half of the makers we interviewed used personal and family finances. This has the benefit of versatility: More than 35% of the makers used a combination of multiple loans, gifts or investments from close friends and kin to support their businesses. Additionally, one-third self-financed their operations.

Access to these sources of capital reflects a class position that benefits makers in other ways. For example, several makers in the sample identified — without prompting — freedom from undergraduate and graduate student debt as a crucial factor enabling them to launch a maker business. Among other benefits, avoiding student debt allowed individuals to save money while working jobs they held prior to entering making, as a New York-based food maker explains: We were always able to self-fund. We have no debt. We're lucky that way. We both came from very high paying careers – when we left our jobs, we were making a combined income of $250,000, so we were lucky enough to be in the position to save.

As a second financing strategy, makers turn to crowdfunding platforms. Kickstarter, Smallknot and similar sites link makers to pools of investors with the cumulative resources to fund speculative products and prototypes poorly fitted to investment and venture capital. However, these sources come with their own limitations. Kickstarter campaigns primarily fund consumer goods with mass-market appeal – clothing, electronics, board games. The site's mandate to deliver a prototype to individual investors further limits the types of goods it covers – viable Kickstarter campaigns require low consumer prices and the deliverable of an easily understood consumer product. Kickstarter's recent decision to raise requirements for the number and quality of prototypes available to investors, and the speed with which they are delivered, adds to these problems.

These factors limit crowdsourcing models to a narrow subset of maker products and product markets. In a representative case, the co-founder of a New York industrial equipment maker considered using Kickstarter to finance 3D printing equipment, but determined the service was better suited to consumer goods. “You essentially have to promise large amounts of people the delivery of a product before knowing its cost or how long it will take to produce,” he explains. A Chicago industrial equipment maker quickly reached a similar conclusion: “Kickstarter only works for consumer products… And it deals with prototypes, not getting to scale.” As an alternative to using Kickstarter to raise funding, many makers treat it instead as a market test, “the easiest way to test a product's market viability,” [consumer goods maker, Chicago] or a way to represent broader interest and market viability to potential funders, suppliers and retailers, even though “we knew it wouldn't be a source of money,” [electronics maker, New York]. Notably, some local maker crowdfunding initiatives, such as Portland's Crowd Supply, have chipped away at this problem.

Entrepreneurship and design contests present a third path to funding maker businesses. These contests reward students, innovators and would-be businesspeople with financing and advice on products and business plans. Each event targets and benefits a different sub-set of prospective makers. Entrepreneurship contests prize market reach over technological innovation, and favor market-ready products. Maker Faires support small, comparatively simple innovations producible from modest inputs and equipment. And design competitions privilege products favorable to their sponsor industries (fashion, furniture, consumer electronics). Cumulatively, these competitions provide an uneven but viable path to winning exposure and financing.

All three main financing strategies – self and family, crowdfunding and contests – contribute to makers' difficulties in scaling up. Each source provides short-term funding tied to individual products, rather than general support for maker businesses. Without exception, the makers who won Kickstarter funding or product competitions were struggling to take their inventions to broader consumer markets. These challenges have multiple origins: in the material properties of manufactured products, in technology, equipment needs, in industry structure and in market composition. As industrial geographers have long noted, manipulation of the production process itself constitutes the central variable, the agentive human activity, through which the producers of goods attempt to adapt to and solve these diffuse problems (Hudson, 2001; Sayer and Walker, 1992). Maximizing the returns to the production process, however, requires producers to find markets to which to sell.

Getting products to market

The technological changes that propel making have also transformed consumer markets, a development that benefits makers in principle. Online retail outlets, including Amazon, Etsy and Shopify, provide the means to reach broad national and international markets. Social media complements this breadth with depth, allowing makers to build markets from existing social networks. More simply, digital technology expands opportunities for wholesaling, and makes wholesale distribution channels easier to find.

Yet while social media and internet retail proved valuable to the 44% of makers who targeted consumers directly as their principal marketing strategy, the cost of maintaining multiple social media and other consumer distribution channels quickly exhausts makers' energy, time and finances. In response, makers typically focus on a single, primary distribution approach. Given that each type of distribution favors particular consumer markets and sales strategies, this choice further ties makers to limited business models, most of which trade the potential scope of national markets for the certainty of higher margins on goods branded as local.

Social media

Social media provides several unique sales advantages. First, personal use of Instagram, Facebook and similar platforms yields ready-made sales networks, and limits the need to acquire platform-specific skills. Second, the finely grained social niches reached by social media networks provide a means of matching maker products with strong but narrow appeal – custom-made shoes; high-end bicycle messenger bags; wooden toys – to potential customers by accentuating the aesthetic character of maker goods. Third, social media platforms entail minimal up-front expenses.

Makers weave together multiple social media platforms to expand sales. Yet each platform requires distinct approaches, media and updating strategies. Expanding to additional platforms requires linear increases in work effort, but generates diminishing returns. Craft-focused makers in particular favor Instagram, whose prioritization of images fits well with the appeal of design-intensive products [interviews, multiple makers and cities]. This makes Instagram “a new business model for reaching customers,” [fashion maker, New York] even though its reach is narrow. Thus, although Instagram constitutes a necessary vehicle for reaching customers, it is not by itself sufficient to generate sales: “Lots of people ‘like' us on Instagram. But it doesn't drive sales. So we'res really looking at a ‘layering' of social media platforms [in order to drive sales]” [design maker, Portland].

Compensating for this limitation by layering multiple social media platforms carries few cash costs, but requires as much as half the time of actual production work. Maintaining social media followers requires consistent posting of new pictures, products and specials – demands that fit poorly with other claims on makers' time [multiple makers, multiple cities]. The repeated but intermittent attention required by social media platforms also adds complexity and switching costs to makers' other business obligations. The problem is especially severe for craft-oriented makers who must constantly monitor their social media sites to remove postings for one-of-a-kind products that go out of stock with each sale. Each product requires both its own page, and the kind of sustained attention that inventory systems eliminate for standardized products. Because the time involved makes individual sales costly, these platforms push you to craft-based approaches. “Everything else you do, is [done] to push yourself towards mass production” [electronics maker, Portland]. Like other outsourced approaches to a maker business, social media's short-term advantages come at the cost of locking makers in to niche-based competitive strategies.

Internet retail

Mass-market on-line platforms – particularly Amazon – provide a way around these problems. However, their benefits are limited to standardized, mass-consumer goods. Thus, few of the makers in our sample used Amazon, even though most expressed a desire to do so. Success with Amazon sales requires wares to stand out enough to be viewed and purchased – challenges that add to the high price point of maker goods relative to others. For the small sub-set of makers producing products with broad appeal (e.g. barware, personal accessories, electronics) this makes Amazon an ideal solution to sales and distribution challenges: Amazon is like the best wholesale partner. A lot of people who've had issues with them, haven't scaled yet. [consumer goods maker, Chicago]

Local distribution

Despite their limited consumer reach, local outlets for wholesale and retail remain makers' most commonly used and effective means of reaching customers. Just one maker out of eight relies completely on local sales, but locking in local demand is essential to all makers' competitive strategies.

More than 40% of makers identified local wholesalers as their primary customers. Wholesaling improves sales efficiency by creating pooled access to multiple types of buyers, and by ensuring some stability in month-to-month orders. Although there were no recorded successes, several makers pointed to the potential for wholesaling to introduce mass retailers to their products, which in turn could lead to direct relationships with the retailers. In the short term, however, wholesaling pushes makers towards the same trade-offs that characterize other efforts to scale up. For craft-focused makers, developing wholesale relationships requires finding ways to standardize the production of products that are by definition one-off. The ensuing business changes cause their own problems: I used to make more wholesale stuff – in an ideal world, I could take more wholesale jobs and hire some new employees. But still, to keep my prices the same, I'd have to underpay my employees - $12/hour or something like that, which isn't something I want to do. [consumer goods maker, New York]

Production dilemmas: Constraints of contract manufacturing and in-house production

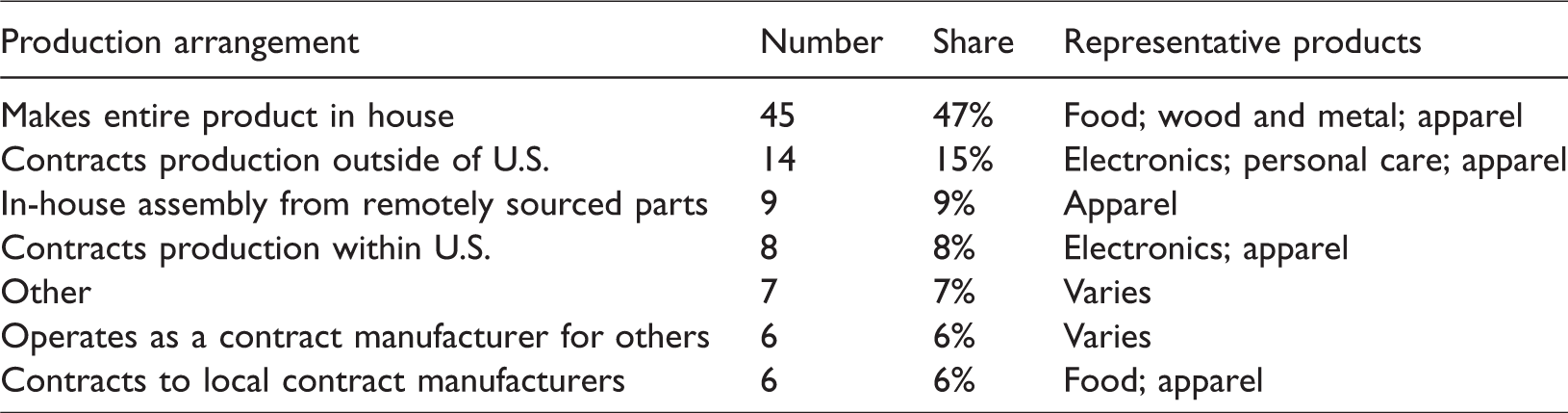

The major options entrepreneurs have for expanding production often deepen their scale-up challenges. Approximately, one-third of makers we interviewed used contract manufacturing arrangements to produce their products (Table 4). These makers cluster in consumer-durable industries (electronics, personal accessories) with extensive market reach and high potential for growth.

Maker production arrangements.

In addition to isolating the barriers makers face in using contract manufacturing, our research highlights two currently overlooked characteristics of makers, each with implications for policy. First, contra making's do-it-yourself ethos, contract manufacturing constitutes a common goal for makers not engaged in artisanal production methods: It provides long product runs without significant up-front investment. Second, when contract manufacturers are unavailable, makers use in-house production as a tactically safe fallback option.

Offshore contract manufacturing

Makers typically have strong ethical commitments to local sourcing and production. Scaling up maker businesses into self-sustaining, profitable entities, however, requires makers to produce high volumes of goods – at mass-market prices, and without the benefit of capital to invest in production equipment. This pushes them to contract manufacturing: In terms of wood fabrication, Chicago is great. But for metal casting, we've gone offshore. To be blunt, it came down to cost. [Accessories Maker, Chicago] As soon as we were ready to go to our first 5,000-unit order, we had to go to China. [Electronics Maker, New York] [Quality] is terrible if you ask them to do something because they'll do it not how you expected them to do it… There's a giant fucking opportunity cost [to purchasing from China] — excuse my French — and nobody talks about that because people that can afford those opportunity costs, it works out for them. [electronics maker, Portland]

Local production networks

Of the 32% of makers in our sample who used the services of contract manufacturers, 17% used U.S.-based contract manufacturers. These makers generally favored regional production due to either available manufacturing capacity, or due to the desire to improve product quality by moving freely between prototypes, designs and test runs (Berger, 2013; Clark, 2013). However, the opacity of manufacturing supply chains attaches significant costs to the task of finding local manufacturers to whom to contract production: The issue is that manufacturers really rely on word of mouth for new business. They hardly have an on-line presence. So we had to find online registers for manufacturers. The most important thing, though, was just to find on-line registries or boards with lists of magnet manufacturers. There would just be lists of hundreds of companies, poorly laid out, with no examples. [accessory maker, Chicago]

Some maker-focused entrepreneurs, such as the business Makers Row, respond to this problem by offering fee-based supply-chain mapping services. However, few of the makers in our sample used these services, and those who did were reluctant to pay the limited fees charged. For makers who do succeed in overcoming such information gaps, using local contract manufacturing brings about several prospective advantages: So there's a couple more reasons to manufacture locally. One is, now people expect quicker turnaround time. Apple releases a new cell phone once a year, so people produce lower volume. The development cycle has to be much faster. Also, shipping from overseas can take at least a month. There could be issues with the ports. So you lose 1/12th of your development cycle in shipping, and it's not cost-effective to overnight or airship a lot of these products. [electronics maker, Chicago]

Makers' choices of production technology and location stem from the physical nature of the good being made. For heavier products with high transport costs (metal, glassware), makers rely on local production. Craft approaches, which prioritize design and skill over the cost efficiencies of automation, likewise remain local. However, cost-competitive apparel markets induce heavy pressure to take advantage of low-cost contract manufacturing and outsourcing, as do markets for computer and electronics products easily and efficiently manufactured through global production networks. As a result, the real but limited benefits to using local production networks are themselves limited to a small sub-set of makers. These barriers can be circumvented through efforts to connect high-end producers to local suppliers, and to intentionally create interfirm clusters, as in the case of New York City's Manufacture New York, a hybrid enterprise with for- and not-for-profit arms (Wolf-Powers and Levers, 2016).

In-house production

As a third option, a siginificant sub-set of makers operates its own production equipment. Such in-sourced production provides strategic flexibility by allowing makers to respond quickly to market needs, work closely with suppliers, and outsource other business functions [multiple makers, multiple industries and cities]. It also provides control and stability for makers whose bargaining position vis a vis offshore contract manufacturers yields poor quality and high unit prices. Many makers producing in-house followed the path outlined by a Portland personal goods maker, who “found that things were always easy – the answer was always ‘yes'” when negotiating (during a prior career) in China on behalf of a corporate employer. As a maker, this same individual moved production and sourcing from abroad back to Portland after finding himself a low priority on overseas manufacturing contracts.

The ability to establish in-house production depends on product type and personal resources. Makers whose approaches emphasize custom production in-source most frequently, due to limited equipment costs, modest space needs, and the vital role of customized and hands-on work in their business strategies. Falling costs for mills, lathes, Computer Numerically Controlled (CNC) routers and other pieces of formerly difficult-to-obtain production equipment provide other business advantages. For example, makers in Portland's growing furniture production industry use CNC routers (priced at $10,000) that require comparatively modest capital outlays. Their businesses now revolve around deploying this technology. Across product lines, the rapidly falling cost of machinery leads to constant recalibration in business plans and goals: When I was talking about it at [college] and the end of high school, people kind of laughed and said ‘you need $7 million to start a design firm, to get equipment, a warehouse—there's no way you can do that!'… Times move fast, technology grows exponentially, and by 2010 which was literally 3 or 4 years later, I bought my first 3D printer… from my bar tips I had saved up, which was $2,000. [industrial equipment maker, Chicago]

As these cases demonstrate, makers' ability to in-source production reflects the intricacies of products and production, rather than advances in strategy. Products dictate production technology, which in turn leads to wide differences in equipment costs. When production relies on comparatively low ratios of capital to labor, or when the production process and technology are simple, makers can take charge of production themselves. These same barriers mean that most makers – five out of every six in our sample – have little choice but to produce through market-mediated networks.

Transaction costs, production strategies and path dependence

As makers and manufacturing firms develop relationships, routines and intangible assets tied to particular production approaches, the short-term costs of altering production techniques, locations or end products grow so great that only the largest and best-resourced firms can afford to change methods (Sayer and Walker, 1992). For the 64% of makers in our sample who identify business expansion as a goal, these short-term decisions lock growing firms into specific markets, technologies and types of expertise.

The choice among offshore contract manufacturing, local production networks and in-sourced production shapes organizational resources, routines and relationships in ways that commit the organization to that particular production mode over the long-term. These differences in production technique quickly condition competitive strategy, with makers constrained by high production costs and short product runs fitting product design and sales to fragmented, often higher-income consumer populations capable of paying retail prices that cover production costs (Harvey, 1989; Sayer and Walker, 1992; Scott, 1988a).

Makers' limited use of global production networks and opportunistic use of local production capacity to support product differentiation suggests they are taking on the small-run, niche-market production strategies that were previously the domain of flexible manufacturing firms offering high-quality products (Dicken, 2003). Whether in their vertically integrated or networked form, firms provided resources, economies of scale and scope and access to specialization, all of which supported vital efficiencies in producing, sourcing and selling small runs of related products (Scott, 1988a, 1988b). The niche-based production models that allow makers to utilize local production networks require an individual maker to replicate to some degree all of the functions that enabled large manufacturing firms to extract profit from fragmented production runs and lower sales volumes. The resulting competitive model locks makers into the production of: Luxury products – that's the only way you can make it locally, make it low volume, and make a living. The best margin boosts are making and selling it yourself. Think of all the margin you keep. That's how you can compete against Chinese made goods. [design instructor, Chicago]

These competitive models allow makers to expand sales over the short term. However, the maintenance of production relationships demands significant amounts of makers’ time and energy, limiting their capacity to expand beyond current markets and products. Many makers in our sample identified making’s time demands as a “push” factor that forced them to attempt scale up in order to maintain their businesses. These time limitations grow as makers turn their attention to the demanding business of building the broader market visibility necessary to scale up production and routinize their work.

Incremental growth and piecemeal production: The maker’s scale-up challenge

The question of how to scale up production looms for makers seeking a full-time living from their inventions. Scale-up constitutes so central a challenge that it represents a key “part of the maker movement: …. figuring out how to get from a prototype to making hundreds of products at scale” [Electronics maker, Portland].

A process rather than a single activity, getting to scale requires makers to build relationships with financiers; to find industrial space, suppliers and distributors; to render prototypes and individual products manufacturable at scale; to advertise and develop product awareness; and, eventually, to hire payroll employees. These challenges fall simultaneously on the business proprietor. The majority of the makers in our sample drew on their prior professional experience, knowledge and connections to mitigate these problems. Experience and skill, however, offer limited resources for dealing with the problem of dealing with many problems at once: I think it’s especially hard with a maker business, because you’re designing, manufacturing, selling to business and customers. That’s several businesses wrapped into one, so you have to learn how to manage several kinds of businesses…. We’re designing the [production] processes, the [machine] tools…. It’s so much to keep up with. [Apparel maker, Chicago] I found myself alone in my apartment struggling to build this product and then locate manufacturers willing to take a chance with an entrepreneur on a small run with no line of credit…. We finally got the product prototyped using other facilities, calling in favors, people that still worked at my old office, people with access to university tools, and we built the prototype, tested it. It worked. Then we went to manufacture and had to pay upfront for all the parts. So there was a challenge raising money. Our team lacked skills to launch and distribute a product, we didn't have all the channels lined up. We struggled with certification barriers. If we had a bit more mentorship early on we would have seen these challenges.

While makers’ responses to financing, production and distribution challenges often succeed on their own terms, these short-term tactics push makers towards niche-market competitive models premised on shorter product runs, niche and luxury markets, and higher profit margins (Piore and Sabel, 1986; Sayer and Walker, 1992; Scott, 1988a). Such approaches by definition restrict makers’ capacity to become larger-scale manufacturers.

Conclusion

The maker movement emerges from technological and organizational developments that change the barriers to starting and expanding a manufacturing business. However, simulating a vertically integrated manufacturing firm’s activities without the benefits of the firm’s infrastructure, pooled resources and routines burdens makers with excessive transaction costs that limit their market reach. Our in-depth interviews with 137 makers and maker-supporting institutions highlight four key implications of these challenges.

First, makers and their small start-up businesses access external, market-based manufacturing infrastructure with clear disadvantages. The market resources through which makers replicate the capabilities of the firm favor large firms with long product runs, and push makers towards low-volume, high-margin niche competitive strategies. These barriers are most visible in financing and contract manufacturing, yet pertain in every facet of makers’ businesses.

Second, makers respond to these limitations by duplicating resources and products, rather than lengthening individual product runs. For example, the typical maker in our sample combined crowdsourcing, personal finances, family finances and loans or support from public entrepreneurship programs to simulate traditional financing. Makers likewise use social media and online retail to add to a market base of local sales and wholesaling. Pooling approaches in this way comes at significant cost, because negotiating multiple agreements, contracts and relationships consumes the time and resources needed to develop other business specializations and capabilities.

Third, makers’ production process choices add to their long-term challenges in scaling up. The production process provides little room for maneuver: first because the physical characteristics of the product being made shape the benefits and downsides of using contract manufacturing, and second because commitments to artisanal, overseas, in-house or local production tie down makers’ capital, organizational resources and routines. By consuming resources and attention at every level of the organization, production choices shape makers’ options and limit flexibility. Significantly, the makers in our sample who scaledup their businesses began with products whose simplicity yielded either large consumer end-markets or simple production processes.

Fourth, these organizational limitations collectively push makers towards competitive strategies based on low-volume, high-margin production. Producing distinctive goods with niche appeal allows makers to maximize margins on products that reach consumers through the comparatively inefficient means of local retail, niche websites, and artisanal or limited-run production. But building up a business around large volumes of high-margin niche products pushes makers away from the high-volume, lower-margin sales central to scaling up in a U.S. consumer market built for cost-conscious consumers facing (in the aggregate) stagnant incomes and high levels of personal debt. Writ large, these approaches allow makers to achieve limited business stability at the cost of limited market reach. They restrict the cumulative output and impact of making.

The technological and social changes that produced making initially may in the future provide solutions to some of these problems. For example, future drops in equipment prices and advances in financing and distribution platforms, as well as experimentation and social learning by makers, may eliminate some of the capital barriers or market bottlenecks that work against scaling up. And while the hoped-for growth in production employment that currently authorizes public support for the maker movement remains in most cases aspirational, the measurable outputs of revenue and employment growth constitute just a portion of making’s contributions to regional economies.

Regardless of their instrumental value, creative industries and making contribute to the regeneration or stabilization of manufacturing via means other than job creation (de Propris, 2013). Our findings call attention to the localized institutional ecosystems in which makers are embedded, and the extent to which local resources enable makers to overcome the barriers to scale. By disseminating technology, thickening relationships between designers, manufacturers and entrepreneurs, and otherwise expanding regional engagement in translating innovation into production, making may help, however diffusely or indirectly, to support and develop other industries (Berger, 2013; Clark, 2013; Essletzbichler, 2015). The extent to which the maker movement will directly lead to new firms, jobs and industries, however, rests on makers’ ability to negotiate the classic problem of carving out stability and growth from fragmented, unstable markets and products.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.