Abstract

The location patterns and organizational networks of both advanced producer services (APS) and cultural industries have attracted extensive attention in geography and other related disciplines. However, most research on these two sectors has examined each one in isolation, without paying attention on how they are engaged with each other. Drawing on a network analysis of the inter-firm service provision relationships between 245 cultural firms and their APS providers during the firms’ public listing processes in mainland China, this paper presents a pilot study of the functional interactions between cultural industries and APS from a geographical perspective. Our purpose is to expand the research on these two economic sectors from the simple mapping and ranking of their individual industrial activities to an investigation of the city-based spatial relationships between them. The outcome reveals that while the leading cultural firms and their APS intermediaries have demonstrated similar location patterns across major Chinese cities, the spatial interactions and connections between them are much more complicated than their co-location tends to suggest. This paper enriches our understanding of the functions of local clusters and trans-local networks in the establishment of inter-industrial linkages between the different sectors of knowledge economies. The paper also sheds light on the impacts of institutional context on the (spatial) development of cultural industries in a transitional economy.

Introduction

Over the past two decades, there has been a surge of interest in the spatial organization and developmental consequences of knowledge economic activities in the urban and regional context. Advanced producer services (APS) and cultural industries, as two of the most dynamic segments of the new economic regime, have become a focus of attention in geography and other related disciplines (Amin and Thrift, 2007; Currid and Ravid, 2012; Hoyler and Watson, 2013; Krätke and Taylor, 2004; Pratt, 2011; Sassen, 1991; Taylor et al., 2013, 2014; Zhao et al., 2015). Both of these sectors are subject to strong agglomeration economies – above all, the ‘urbanization economies’ of Jacobs (1970). Therefore, these sectors tend to concentrate in a limited number of large cities that are endowed with favourable labour conditions, market demand, infrastructure and urban amenities, and other advantages (Florida, 2002; Kong et al., 2015; Sassen, 1991; Scott, 2012). Through their location choices and various intra- and inter-firm, local and trans-local production networks, these economic actors have significantly restructured the spatial organization of economic development processes at different geographical scales (Hall and Pain, 2006; Hoyler and Watson, 2013; Taylor et al., 2013, 2014; Zhao et al., 2015), which makes them major shapers of urban growth and transformation in the contemporary era (Amin and Thrift, 2007; Scott, 2012).

While the location patterns and organizational networks of both APS and cultural industries have been widely explored in the literature (cf. Hall and Pain, 2006; Hoyler and Watson, 2013; Krätke and Taylor, 2004; Liu et al., 2013; Taylor et al., 2013, 2014), most research has examined each of these sectors in isolation and has failed to explore their engagement with each other. A few recent studies have begun to look at the urban relationships between some sub-sectors of APS (e.g. finance) and cultural industries (e.g. arts) by investigating the resemblances between their location patterns in major global cities (Caset and Derudder, 2017; Skórska and Kloosterman, 2012). Underlying this work is a theoretical assumption that the co-location of APS and cultural activities in major cities may demonstrate or stimulate intensive interactions between them and generate positive externalities. However, simply measuring and ranking industrial activities within cities still sheds relatively little light on whether (and to what extent) such inter-sector functional interactions have actually happened and, if so, how they have been organized across space. To develop a better understanding of the relationships between APS and cultural industries, we need a more subtle analysis of the processes by which the major actors in these two sectors interact (Pratt, 2011).

Against this backdrop, this paper provides a pilot study on the spatial interactions between cultural industries and APS based on the case of mainland China. Drawing on information (from the firms’ public listing processes) about inter-firm service provision relationships between cultural firms and their APS providers, we move beyond the simple mapping of firm locations and investigate the service-based spatial connections between these firms at both the local and trans-local scales. The major concerns of our study are two-fold: First, is there any spatial overlap between the location patterns of cultural industries and APS at the sub-national level? Second, do cultural firms prefer to obtain listing-related services from their co-located APS intermediaries or from intermediaries in other locations, and which cities receive the most consideration? While the functional connections between APS and their clients is not a new topic (cf. Hanssens et al., 2013, 2014; Shearmur and Doloreux, 2015), some unique attributes of cultural industries make this sector an interesting case for further investigation. First of all, as sectors that produce goods or services that are infused in one way or another with aesthetic or semiotic content, cultural industries – compared with other economic sectors – tend to demonstrate higher levels of territorial embeddedness and stronger linkages to local social and market factors (Coe, 2015; Pratt, 2011). The competitive advantages of most cultural industry sectors are often tied to the qualities of particular places (Scott, 2004). Therefore, the location factors important to cultural industries are not always identical to those that are important to APS and other new economic sectors. The extent to which this local embeddedness will have an influence on the location patterns of cultural firms and their selection of APS providers remains a largely unexplored question.

In addition, as members of a typical ‘post-Fordist’ economic sector, most cultural industries are organized through a vertically disintegrated, project-based flexible production system (Gibson and Kong, 2005). The production processes of cultural industries thus often involve the participation of different actors and intensive cooperation between them. Prior research has revealed the significance of both local clusters and trans-local ‘pipelines’ (Bathelt et al., 2004) for cultural firms to establish co-production projects and realize intra-industrial complementation (cf. Coe, 2001; Mould, 2008; Watson, 2012). However, it remains to be seen how these two channels function in the formation of cooperative relationships between cultural industries and other industrial sectors.

Finally, for both economic and ideological reasons, cultural industries are also one of the most highly regulated and protected sectors in many countries. State intervention and regulatory policies are important shapers of industry dynamics (Coe, 2015). This is especially true in mainland China, where the cultural sector is still in transition from a completely state-controlled into a market-oriented system. In this context, cultural industries function both as ideological propaganda apparatuses and as profit contributors in China (Su, 2015). Both the central and the local governments have been actively involved in the development of China’s cultural industries. On the one hand, these governments strictly control the content of cultural production, while on the other hand, they formulate (often at the local scale) a wide variety of financial incentives and subsidy schemes to stimulate and sustain the growth of cultural industries (Ren and Sun, 2012). Cultural industries have been included in the development agendas of nearly all provinces and cities and have become a major target of interurban competition (Webster et al., 2011). How this special transitional context may affect the spatial organization of cultural industries is also rarely discussed. By tapping into these questions, our study aims to advance current research on industrial clusters and urban networks in knowledge economies and contribute to economic geography and urban studies literature.

The paper is structured as follows. We begin with a brief, theory-informed discussion of the locations of APS and cultural industries as well as the potential urban relationships between them. Next, we elaborate on how the process of public listing has linked the firms in these two sectors and how we have used this type of information in our analysis. After that, we present the major findings of our empirical work. We first compare the location patterns of major cultural firms and their APS providers in general, and then we investigate – in detail – the spatial connections between them within and across major Chinese cities. In the last section, we present our conclusion, discuss its theoretical implications and offer some potential directions for future research.

Cities as centres of APS and cultural industries

The relevance of APS for contemporary cities, especially often-cited global or world cities, has been amply documented and theorized in the existing literature (Daniels, 2004; Hall, 1966; Sassen, 1991; Taylor et al., 2014). According to Sassen (1991: 325), the mutually reinforcing tendencies of globalization and post-industrial transformation ‘have contributed to the growth of centralized service nodes for the management and regulation of the new space economy’. The geographical dispersal of economic activities, along with the simultaneous integration of these activities on a larger scale, has fuelled the growth and importance of both central coordination functions and a series of dedicated supporting producer service activities. Due to the ‘complexity of the services they need to produce’, the ‘uncertainty of the markets they are involved with’ and the ‘growing importance of speed in all these transactions’, these specialized APS firms are strongly subject to agglomeration economies. Therefore, they are prone to locate in a limited number of cities that offer certain types of urban functions and environments (Sassen, 1991). Through an extensive network of branch offices, affiliates or partners, the leading APS players are able to provide services for their widely distributed clients, strengthening cross-border city-to-city transactions and leading to the formation of a transnational urban system (Taylor et al., 2014).

The concomitance between cultural industries and cities has also been widely discussed. In an early seminal work, Hall (1966) observes that the world’s major cities are not only the centres of trade, finance and business services but also the hosts of a variety of cultural, creative and entertainment industries. Scott (2012) also identifies creative and cultural industries as a pillar sector of the ‘cognitive-cultural economies’, which, he argues, have underpinned the resurgence of cities and city-regions in the contemporary era. The relationships between cultural industries and the city are reciprocal and circulatory (Markusen and Schrock, 2006). On the one hand, the prosperity of cultural industries relies on the urbanization economies, including a finely grained division of labour, a critical mass of potential clients, well-developed transport and communication infrastructure, and openness to creativity and newcomers. These attributes are most likely to be found in the metropolitan context (Florida, 2002; Glaeser, 2011; Hall, 1998; Jacobs, 1970). On the other hand, cultural industries can also generate, either directly (e.g. creating jobs and attracting visitors) or indirectly (e.g. place improvement and city branding), a wide range of benefits to the cities in which they are located (Florida, 2002; Kloosterman and Trip, 2011; Mommaas, 2004). For these reasons, the world’s leading cities also tend to be the major clusters of cultural, creative and entertainment activities.

Given the putative co-location of both APS and cultural industries in a selected number of large cities, an intuitive inference would be that there is a positive interaction between these two sectors (Caset and Derudder, 2017). For instance, APS firms could offer strategic intermediate inputs (i.e. specialized services) to firms in cultural industries, whereas the concentration of high-income APS workers may also generate high demand for the consumption of the symbolic products or services that are provided by the cultural sector. Although such functional intersections between APS and cultural industries in the urban context have been repeatedly asserted, empirical analysis of such intersections is still rather thin. Skórska and Kloosterman (2012) and Caset and Derudder (2017) have investigated the correlation between contemporary global financial centres and global arts centres. Other scholars have also compared the inter-city networks created by some typical APS (e.g. accountancy, finance, law) and cultural (e.g. advertising and media) industrial sectors (cf. Krätke and Taylor, 2004; Taylor and Derudder, 2016). However, the focus of these studies is still on the resemblances and differences between APS and cultural industries in terms of location patterns or organizational structures rather than on the actual interactions between them. It remains unclear how cultural firms obtain business-related services from APS intermediaries and whether geographical proximity matters for the establishment of such culture–APS relationships. For a better understanding of these questions, we need to ‘move beyond measuring co-location and into measuring flows not only of material goods, but of non-material and un-traded knowledge’ between APS and cultural industries (Pratt, 2011: 271). Such an exploration could enrich our knowledge of the functioning of urban networks and industrial clusters in the modern economic system.

For this purpose, we use the information about service provision activities that is produced during the cultural firms’ public listing processes – processes that constitute a link between these firms and their APS intermediaries – to explore the spatial relationships between these two economic sectors. In the next section, we will introduce the methodological basis of our empirical work.

Public listing: Linking cultural and APS activities

One of the most sophisticated and high-end economic activities that intensively involves both APS and non-APS firms is the process by which corporate shares are publicly listed; a clear example of this is Initial Public Offerings (IPO) (Pan and Brooker, 2014; Wójcik and Burger, 2010). Firms choose to list their shares on a stock market not only to raise capital from investors but also to obtain other benefits such as access to external resources, expanded networks of relationships and greater visibility to potential customers (Burton et al., 2006). This is a highly complex and costly process that requires specialized services from a variety of APS intermediaries, ranging from securities and legal services to accountancies, assets assessment, clearing and more (Wójcik, 2009a). These APS intermediaries are responsible for due diligence inspections concerning the development history, operational conditions and financial situations of the issuers to ensure that they comply with the listing standards. They also have to study the feasibility of the share offering plan, audit and appraise the assets of the enterprise, sign the sponsor agreement with the issuer, and draft the articles of association and other corporate documents (SZSE, 2017). While the type of services provided and the timing and location of service provision may vary from sector to sector, all services involve intensive interactions between the stock issuers and their APS providers, generating bidirectional flows of information and knowledge. As such, every public listing project of a cultural firm represents an interactive process linking the cultural firm with a variety of APS intermediaries (cf. Pan et al., 2017). This process offers a strategic window through which we can investigate the connections between these two sectors.

Geographically, when a firm plans to go public, it may select APS intermediaries from a variety of potential locations. The first location is the city where the issuer’s management centre – its headquarter – is located (case I). In this case, the issuing firm and its APS providers could enjoy many advantages of geographical proximity, such as lower transaction costs, better access to each other’s information and easier establishment of mutual trust. Proximity also helps the issuer maintain its relationships with its APS providers at the post-listing stage (Wójcik, 2009a). The second location is that of the top-level APS centres (case II), including major global/world cities and national services hubs (Sassen, 1991; Taylor and Derudder, 2016). These cities have a concentration of prestigious APS operators (the services complex), which not only implies a guarantee of the quality of services but also makes the issuers more recognizable to potential public investors. The third location is the host city of the stock exchange where the firm’s stock is to be listed (case III). APS intermediaries proximate to a stock exchange could be more familiar with its specific operational process and regulatory rules; they may also have an advantage in acquiring tacit information and knowledge about market changes and investor demand, etc. (Wójcik, 2009b). The last location is the minor APS centre, such as a less significant service hub at the local or regional level (case IV). In these cities, the number and reputation of APS intermediaries may be relatively inferior compared to those in the leading service centres. However, on the other hand, these APS intermediaries have often accumulated rich knowledge and resources related to a specific regional market (e.g. a province in China), which constitutes an advantage when they offer services to clients in the same region (Zhang, 2018).

In reality, the geographical patterns of service provision may be further complicated by the specialties of the issuing companies and the diversity of APS activities. For instance, we may expect that in sectors with a high level of local embeddedness (e.g. cultural industries), firms may be more inclined to obtain services from local (or regional) APS providers because those providers are more familiar with the local business environment and institutional context. In addition, intermediaries in different APS sectors may have rather diverse location patterns and participate in the listing process in different ways, which are likely to influence their spatial interactions with the issuing companies. However, current literature has shed relatively little light on this complex interaction between APS and non-APS sectors in general (except Pan et al., 2017) and on cultural industries in particular.

In this paper, we investigate the spatial interactions between major cultural firms and their APS providers in mainland China during the firms’ IPO or share transferring processes. We will examine whether such interactions are organized primarily at the local or trans-local scale and which of the above four locations are most significant in the formation of service connections between cultural and APS firms. Following the commonly adopted definition, we define cultural industries as ‘a set of activities that produce and distribute cultural goods or service’ with ‘high levels of aesthetic or semiotic content’ (Scott, 2004; UNESCO-UIS, 2009). The identification of specific cultural firms is based on the Industry Classification of Listed Companies (ICLC) of the China Securities Regulatory Commission. According to the ICLC, each listed firm is assigned an industrial code that indicates its core businesses. 1 Because cultural industries involve a diverse set of economic activities, we focus on four major sub-sectors of cultural industries, namely press and publication (R85); radio, television, film and video recording (R86); culture and arts (R87) and culture-related business services (some sections of I64 and L72). These are four typical cultural industry sectors that could also be relatively easily identified using the ICLC information.

The specific procedures of our study were as follows. We first identified all the listed firms belonging to the above four sectors that went public between 2010 2 and June 2017 in mainland China. This information was collected from several different sources, including the website of the National Equities Exchange and Quotations (NEEQ), the Shanghai Stock Exchange and the Shenzhen Stock Exchange, and two professional financial websites, CNFOL and EastMoney. In total, there were 245 firms that fit our definition of cultural industries, 207 of which were listed on the NEEQ, 3 15 on the Main Board, 16 on the ChiNext market and 7 on the Small Medium Enterprise (SME) Board. Most (91%) of these firms went public between 2014 and 2017. Next, we used the listing prospectus of the cultural firms to collect the information on the locations of the firms’ headquarters, the APS intermediaries that participated in their IPO or share transferring processes, and the locations of those intermediaries. We looked at five types of APS activities, including securities, law, accountancy, assets assessment and registration and clearing. 4 Because many APS firms had multiple branches in more than one city, we focused on the branch that directly participated in the listing process, which could be identified from the contact information (primarily the area code of the contact number) of the APS intermediary provided in the prospectus. This database enables us to identify the major centres of cultural industries and APS in mainland China and to measure the service connections between pairs of them.

The service connection (

The gross inward service value of a city i, which reflects the amount of services its cultural firms have received from APS intermediaries in other cities, is calculated as

The net service value of a city i, which reflects the extent to which the city is a net exporter or importer of APS for cultural industries, is calculated as

All five sectors are calculated separately, which generates five city-to-city service matrixes. The locations of major cultural and APS centres and the connections between them are visualized using GIS technology. In addition, some literature and second-hand materials are used to interpret the results of our analysis. This explanatory section is, by necessity, incomplete and tentative in nature, which is a major limitation of large-scale quantitative research. Next, we will elaborate on the findings of our empirical work.

Spatial interactions between cultural industries and APS in mainland China

The locations of cultural and APS firms

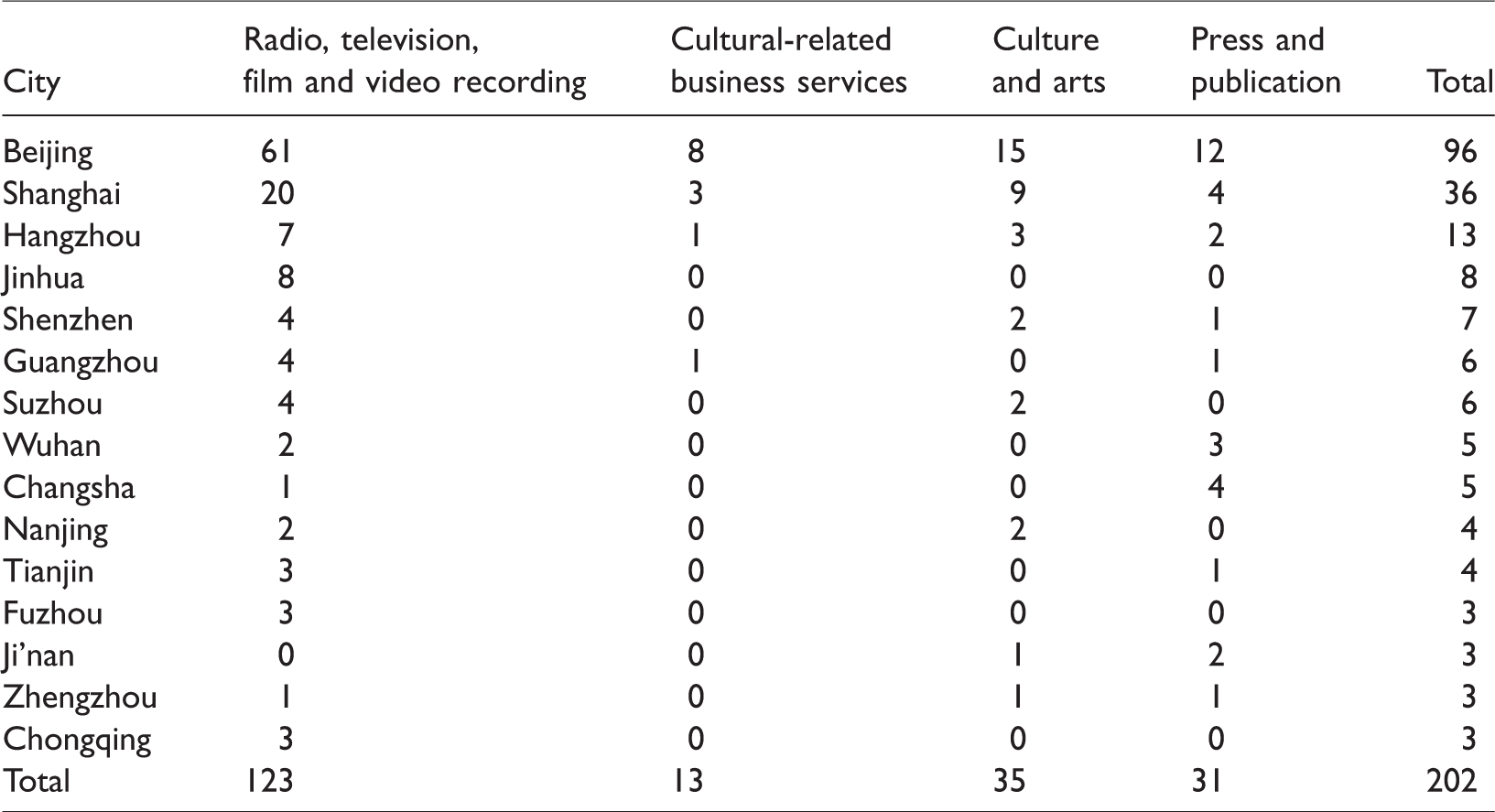

We start by comparing the location patterns of firms in two sectors. Figure 1 outlines the distribution of the headquarters of the 245 listed cultural firms and their 363 APS providers. A first general observation is that both sectors are highly concentrated geographically. While the 245 cultural firms and the 363 APS intermediaries are located in 45 and 33 cities, respectively, most of them are concentrated in just a few cities at the very top of the list. Beijing, as the national capital, has a concentration of the largest number of firms in both sectors, followed by Shanghai but at a relatively large distance. Together, these two cities have hosted over half of all the listed cultural firms and nearly two-thirds of their APS providers. The exceptional concentration of both cultural industries and APS in Beijing is not only subject to the general factors of agglomeration economies in the capital city, such as historically formed cultural roots, a large pool of talented workers, a concentration of educational and scientific institutions, and a robust demand from both corporate and personal consumers (cf. Chou, 2012), it is also facilitated by some non-market forces, including a concentration of high-level state institutions and strong support and intervention from both the central and the municipal governments (Lai, 2012; Pan and Xia, 2014). Apart from Beijing and Shanghai, only one city (Hangzhou) has hosted over 10 firms in the cultural sector and only four cities have achieved this level in the APS sector. This pattern is consistent with our earlier discussion that both cultural industries and APS tend to concentrate in a limited number of large metropolitan areas (cf. Caset and Derudder, 2017; Scott, 2012).

Distribution of the headquarters of the listed cultural firms (up) and their service providers (down) in mainland China.

The second finding is that there is a high degree of overlap between the geographical distributions of cultural and APS firms in mainland China. The major centres of listed cultural firms also tend to be the major places where those firms’ APS providers are concentrated. For instance, 13 of the top 15 host cities of cultural firms have also appeared on the list of the top 15 cities for APS firms (Figure 1). The only two exceptions are Jinhua and Suzhou, whose ranks are much higher in the cultural sector than in the APS sector. These two cities have a special advantage in hosting several large, nationally famous film and TV production bases or studios, which have attracted some large players in this sector (Table 1). Apart from these two special cases, all other prominent cities are China’s major national or regional economic hubs, and many of them are also the administrative centres (provincial capitals) of their respective regions. With a few exceptions (e.g. Changsha, Wuhan and Ji’nan), the composition of cultural firms in these cities is dominated by the radio, television, film and video recording sector (Table 1) – a sector that is relatively easier to attract and thus has received extensive support from local governments (Zhang and Li, 2018). The resemblance of the distributions of leading cultural and APS firms reflects the uneven spatial development of high-end service economies and a certain degree of industrial duplication among major cities in mainland China. Although the industrial assets, major clients and labour skills of cultural industries and APS are not always identical (cf. Pratt, 2011), they are all highly concentrated in a small number of large cities with great economic and political significance, leaving few opportunities for lower level cities to attract high-end activities in either sector.

Sector composition of the cultural firms in the top 15 cities.

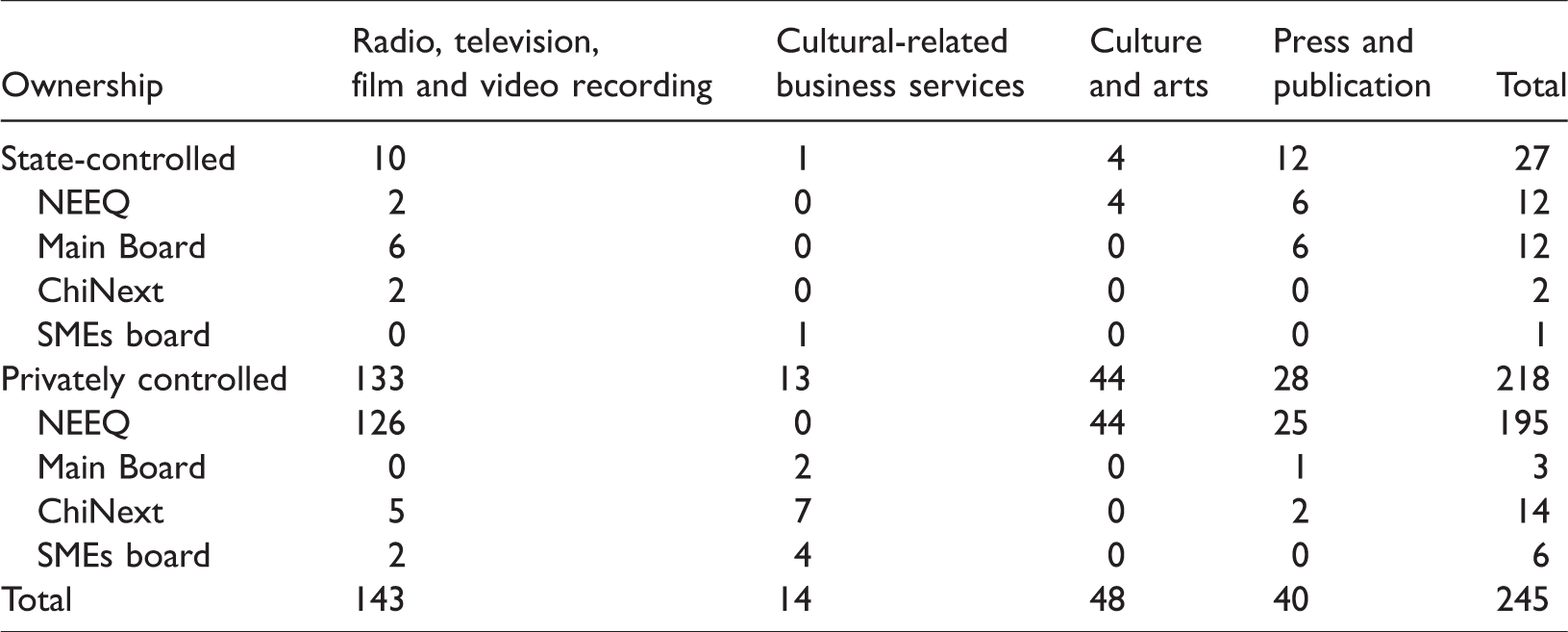

Some remarkable divergences can also be observed among the cultural firms with different types of ownerships (Table 2). While there are only 27 state-controlled listed cultural firms, the average registered capital of these firms reaches 496 million Renminbi (RMB), which is 14 times larger than that of their privately controlled counterparts (34.2 million RMB). Most state-controlled firms are in the press and publication sector (a sector that performs important propaganda functions) and are listed on the Main Board, whereas the privately controlled firms are highly concentrated in the radio, television, film and video recording sector (61%) and are primarily listed on the NEEQ (89%). Geographically, the state-controlled cultural firms are concentrated in only 17 cities, all of which are either municipalities directly under the central government (Beijing and Shanghai) or provincial capitals, with only two exceptions (Jilin and Wuyishan). In comparison, the locations of privately controlled cultural firms are more diverse and widespread (in 40 cities). These contrasting patterns demonstrate the continuing influence of state power in China’s cultural industries. Through controlling the key subsectors and dominant players, the Chinese government not only maintains its gatekeeper status in cultural production (Wang, 2004) but also shapes the agglomerative tendencies of cultural industries in the country.

Profiles of the state-controlled and privately controlled cultural firms.

The spatial connections between cultural and APS firms

We now move on to the inter-firm spatial interactions between cultural industries and APS. This section is primarily concerned with where cultural firms obtain listing-related services from their APS providers. Above, we have indicated four potential locations where a stock issuer may look for APS intermediaries. We first examine the significance of co-location in the formation of service connections (case I). Table 3 compares the service connections between cultural and APS firms that are located within the same city (intra-city connections) and between those located in different cities (inter-city connections). At an aggregate level, co-location seems like an important factor in shaping the formation of inter-firm service connections. Nearly half of the listed cultural firms have selected their APS providers from the same city where their headquarters are located, which points to a high level of co-location between the cultural issuers and APS intermediaries. However, this figure is strongly distorted by a special city, Beijing, where both cultural and APS firms are heavily concentrated. If the capital city is excluded, a rather different picture emerges: Only a quarter of all service connections are organized at the intra-city scale. Most cultural firms outside the dominant APS centres (primarily Beijing, Shenzhen and Shanghai) prefer to employ non-local APS intermediaries to provide services for their listing programmes. Although local embeddedness is widely recognized as a major feature of cultural industries, co-location is not an essential condition when cultural firms are selecting their listing-related APS providers.

Profiles of intra-city and inter-city service connections.

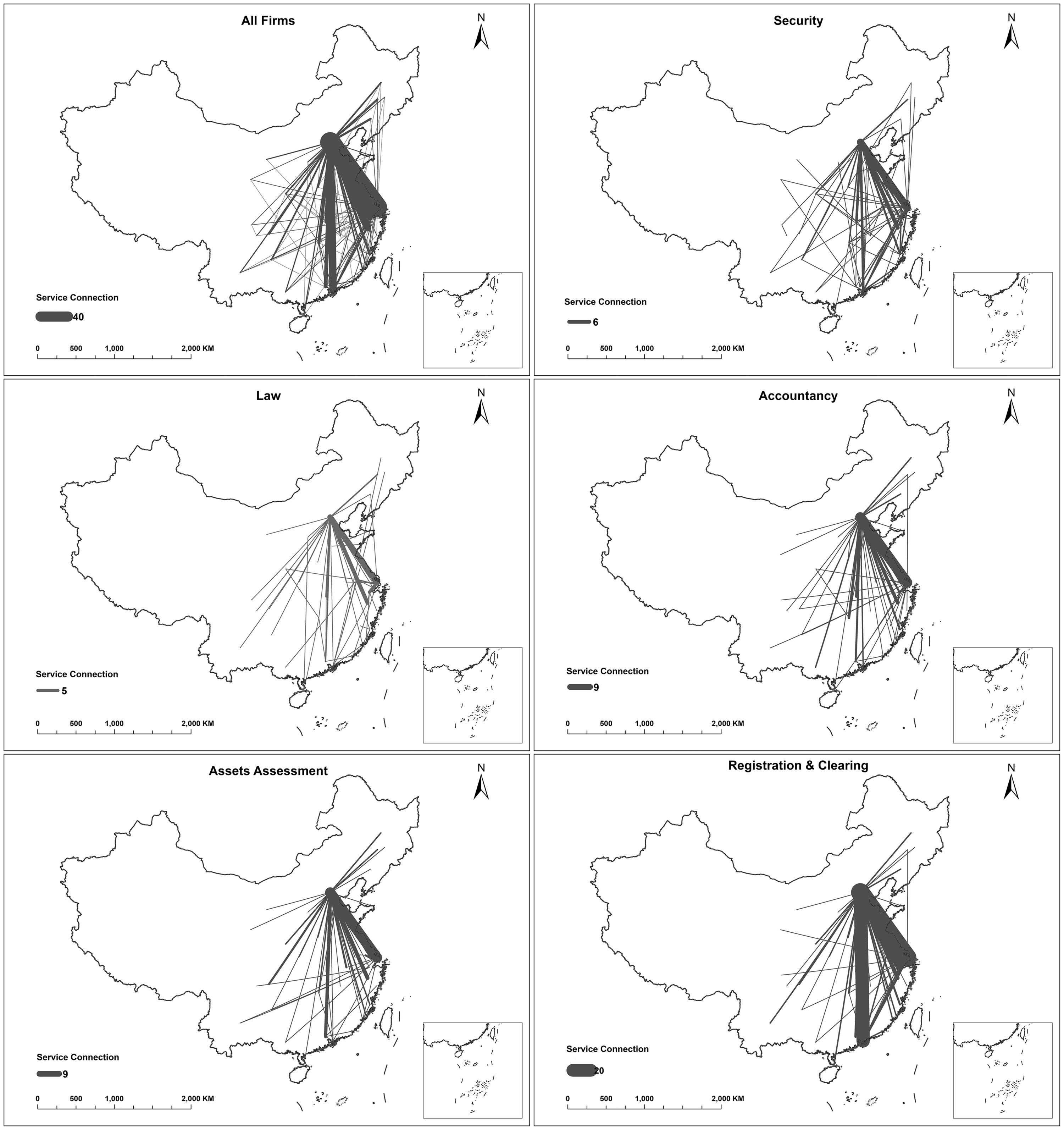

There are also some obvious variations across the different sub-sectors of APS. Legal services tend to be the most localized APS activity. Over 60% of all cultural firms have selected local law firms to provide listing-related services. Even if Beijing is excluded, this figure still reaches 43% for the remaining cities (Table 3). Accountancy and assets assessment also demonstrate a relatively high level of intra-city connections if all cities are considered, followed – at some distance – by securities. However, the significance of co-location for these three sectors declines sharply if Beijing is excluded. Registration and clearing is the most agglomerated sector. Only 31% of all cultural firms have obtained registration and clearing services from local APS providers and, for firms outside the capital city, the proportion is only 2%. Mapping the inter-city connections between firms further confirms our finding: The inter-city connections between cultural and registration and clearing firms are much stronger compared to the connections between cultural firms and other types (especially law) of APS firms (Figure 2).

Inter-city connections between cultural and APS firms.

One major factor that leads to this diversity is the structure of the APS supply market in mainland China, including the number of intermediaries and the features of their geographical distribution in different APS sectors. There is a large number of law and securities firms (127 and 95, respectively in our database), many of which are distributed at a wide range of lower level cities. Therefore, cultural firms can more easily find law and securities service providers in their local markets. In contrast, all registration and clearing businesses in mainland China are handled by a state-owned company – the China Securities Depository and Clearing Corporation Limited (CSDC) – through its Beijing headquarter and three branches in Shanghai, Shenzhen and Beijing, respectively. Thus, firms can only select relevant APS intermediaries from these three cities.

In addition, the features of APS activities and the frequency of interactions needed in service processes may also play an important role in shaping the patterns of spatial interactions between cultural firms and different APS intermediaries. For instance, cultural firms may employ law and accountancy intermediaries not only for public listing services but also for other daily, non-listing-related services that are closely related to their local businesses. These services require more frequent interactions between the customer and the service intermediaries as well as certain types of local-specific knowledge from the intermediaries (cf. Dezalay, 1995). Therefore, there is strong potential for cultural firms to hire local APS firms in these two sectors, thus improving the significance of local service connections. In contrast, registration and clearing is more of a one-off service, which is used only during the listing process and does not require frequent, long-term interactions between the issuers and the intermediaries (CSDC, 2013). Hence, co-location is unlikely to be an important factor when cultural firms are selecting their registration and clearing service providers.

If cultural firms do not obtain listing-related services locally, are they more likely to search for such services from the major national APS centres (case II) or from smaller, regional-focused ones (case IV)? Next, we examine the significance of major and minor service centres in the formation of inter-city cultural–APS networks. Here, we treat Beijing, Shanghai and Shenzhen – the three largest clusters of APS firms, which also host the only three stock exchanges in mainland China – as the major service centres and other cities as minor ones. Table 4 provides a comparison of the gross service connections of these two categories of cities at the inter-city level. On average, four-fifths of the gross inter-city service connections have involved service intermediaries from the three major APS centres, this figure includes all the connections concerning registration and clearing activities and over 80% of the connections concerning accountancy and assets assessment activities. The contribution of the three major APS centres to the gross inter-city service connections is relatively lower in the sectors of securities and law, but it still reaches 60% and over 70%, respectively. This pattern reveals that most cultural firms prefer to acquire listing-related services from the major APS centres instead of the minor ones. Compared to the quantity of APS operators that they host (Figure 1, also see Zhao et al., 2015), the leading APS centres in mainland China have an even more prominent advantage in exporting high-end business services to clients in other locations. The APS intermediaries in smaller APS centres, in contrast, mainly provide (mostly) regular business services to clients in their local markets (cf. Zhang, 2016).

Profiles of inter-city service connections involving APS intermediaries located in different cities.

Lastly, we look at the impact of the stock exchange in the formation of cultural–APS connections at the inter-urban scale (case III); the results are presented in Table 5. In general, approximately 60% of all the inter-city service connections have involved the APS intermediaries located in the city where the issuer’s stock is listed, indicating a significant positive relationship between the presence of the stock exchange and the outward service capability of the APS providers in a particular location. However, because the city where a stock exchange is located (e.g. Beijing, Shanghai and Shenzhen in mainland China) often tends to be a major global or national services centre (case II), it is rather difficult to isolate the impact of the stock exchange from other general factors that contribute to the attractiveness of the city’s APS intermediaries. Considerable variations among different APS sectors can also be observed. The inter-city connections created by registration and clearing activities have the highest (92%) participation of APS intermediaries from the cities where the cultural firms are listed, whereas the presence of such APS intermediaries is much lower in the connections generated by securities (29%) and law (45%). We speculate that the type of services involved, the ownership of APS intermediaries and the connections of APS intermediaries with the stock exchange are several important factors that lead to such differentiation. Because securities registration and settlement is more like a state-managed administrative procedure that can only be completed through the stock exchange (CSDC, 2013), 5 the APS intermediary’s familiarity with the regulatory rules and settlement procedures of the stock exchange should be a major consideration of the issuers. Therefore, cultural firms are likely to select the CSDC branch from the city where their stocks are listed. Securities and law, on the other hand, are more commercialized and decentralized sectors. There are more APS intermediaries available in a variety of locations for the stock issuers to select (Table 3). Accordingly, the quality of services and the convenience of communications, rather than whether these APS providers are in close proximity to the stock exchange, are likely to become the issuers’ primary consideration when selecting their APS providers.

Profiles of inter-city service connections that involve APS intermediaries from the cities where the issuer’s stocks are listed.

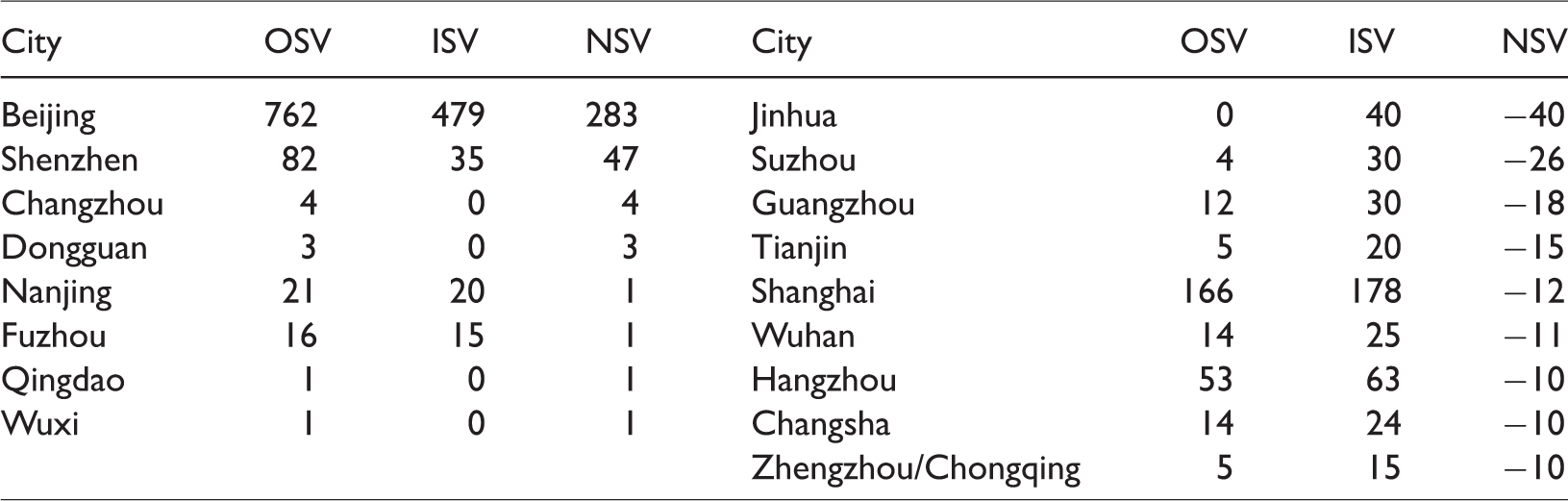

The net service values of cities

Because a large proportion of listing-related services are consumed by local cultural firms, the sheer number of APS intermediaries in a city (Figure 1) cannot fully reveal its functional significance in the national cultural–APS network. The net service value, in comparison, reflects the extent to which a city is a net exporter or importer of APS for the cultural industry. Table 6 lists the cities with positive net service values and those with large negative net service values in mainland China. Only eight cities have a positive net service value and (as most values are negligibly small) only Beijing and (to a much lesser extent) Shenzhen are the real net exporters of APS for cultural firms. All other cities, including the second largest APS centre, Shanghai, import a large amount of business services (registration and clearing services in particular) from non-local APS intermediaries located elsewhere (primarily in Beijing). The major clusters of cultural firms, such as Jinhua, Suzhou, Guangzhou and Tianjin, are also the large net importers of APS. This pattern re-confirms a highly selective geography of APS and the dominance of the capital city in mainland China. Moreover, the pattern also demonstrates that while cultural industries and APS have similar distributions across major Chinese cities, their spatial interactions are much more complicated than simple co-location would suggest.

Cities with positive net service values and large negative net service values.

Conclusions

Drawing on information about the public listing processes of leading Chinese cultural firms, in this paper, we present a pilot study of the service connections between cultural industries and APS from a geographical perspective. Our purpose is to expand research on these two knowledge economic sectors from the simple mapping and ranking of individual industrial activities to an investigation of the city-based functional interactions between them. The major findings can be summarized as follows.

In terms of location patterns, both cultural industries and APS tend to concentrate in a limited number of large cities that have great economic and political significance in China’s national urban system, reflecting the substantial influence of urbanization economies and administrative economies on the development of these economic activities in the Chinese context. The distribution of the two sectors also demonstrates a high level of similarity, with the major centres of leading cultural firms overlapping with the major cities where most high-end APS are concentrated. This highly selective and exclusive geography reveals a new wave of services-led uneven development in mainland China (cf. Yang and Yeh, 2013). Contrary to the state’s policy of promoting more balanced spatial development, cities at the top of the urban hierarchy have established a monopolistic position in most new economic sectors, leaving few opportunities for their lower level counterparts.

The spatial interactions between cultural industries and APS, however, are much more complicated than their co-location would suggest. Most cultural firms outside the dominant APS centres prefer to employ non-local APS intermediaries – instead of local ones – to provide services for their listing programmes. Cultural firms also tend to search for such service suppliers from the major national APS centres (usually the ones hosting the targeted stock exchange) instead of the smaller, regional ones. Under this circumstance, the vast majority of cities in mainland China become net importers of high-end services for their cultural industries. The reputation of the APS intermediaries, the quality of services provided and the familiarity of the intermediaries with the stock exchange are several factors that are likely considered by the listed cultural firms, in addition to the geographical proximity of the service providers. In addition, the patterns of cultural–APS connections also vary according to the type of APS activities. A large portion of the cultural firms’ listing-related legal services are provided by local law firms, followed by securities, accountancy and assets assessment at some distance, whereas registration and clearing activities are highly concentrated in the three APS centres in mainland China. This diversity is arguably shaped by the distinctions among different APS sectors in the structure of their supply markets, the features of their service activities and the frequency of interactions needed, the ownership of the service intermediaries and the connections of the intermediaries with the stock exchange.

By looking at the location patterns of two particular ‘post-Fordist’ industrial sectors and their interactions in a transitional economy, our paper enriches the current economic geography and urban studies literature in the following ways: First, while local embeddedness is widely recognized as a typical feature and a source of competitiveness for cultural industries, its impacts on cultural firms’ selection of high-end business services are not prominent, except in a few top-tier cities and some specific service sectors (e.g. legal services). Trans-local networks, in contrast, prove to be an important (even more important than local embeddedness in some cases) channel for cultural firms, especially those located in smaller cities and non-metropolitan areas, to establish inter-sector relationships and to access the specialized knowledge and skills of other industrial actors. Therefore, the functions of ‘local buzz’ and trans-local ‘pipelines’ (cf. Bathelt et al., 2004) vary considerably according to the economic actors, types of interactions and places that are under examination.

Second, institutional contexts also matter for understanding the (spatial) development patterns of post-industrial economic activities, particularly in cultural industries. In a transitional economy like that of mainland China, state intervention still plays a crucial, if not decisive, role in shaping the landscape of cultural industry development. On the one hand, the state’s tight control over some key cultural sectors and their dominant players has led to a concentration of these sectors and firms in a limited number of large cities (often at higher political/administrative levels), exacerbating the uneven development of cultural industries in the country. On the other hand, the inter-urban competition for newly emerged cultural industries has also led to a proliferation and duplication of some cultural economic activities (often those that are relatively easy to attract) across many medium- and small-size cities. The underlying dynamics of the development of cultural industries in China are not identical to the dynamics of cultural industries in advanced economies.

While our paper has offered some new insights into the urban relationships between cultural industries and APS, it has also opened up several questions that warrant further research. In this paper, we have focused on the cultural–APS connections generated by some specific types of service activities, namely listing-related business services. As mentioned previously, these are the most complicated and high-end service activities, and they have mainly involved leading firms in China’s cultural and APS sectors. This limited but necessary choice has inevitably left many smaller operators in these two sectors, as well as their interactions via relatively low-end, routine and daily service activities, out of view. We expect that these interactions should be more frequent and largely organized at the local or regional scale, which would lend more importance to local APS intermediaries and intra-urban service networks. However, to test this hypothesis, and to develop a more comprehensive picture of the different patterns of (spatial) interactions between cultural and APS firms, new types of data and methods are clearly needed. Moreover, we provide some tentative explanations for the outcomes of the analysis based on our empirical observations and some second-hand materials. For a more in-depth understanding of the underlying dynamics that shape the formation of such cultural–APS networks and the types of interactions that are actually occurring through these ‘pipelines’, more case-oriented, qualitative-information-based research should be conducted in the future.

Footnotes

Acknowledgements

We would like to thank Robert Kloosterman, Nicholas Phelps, the editor and the anonymous referees for their useful comments on an earlier version of this paper. The usual disclaimers apply.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (Grant Number 41601163, 41601127) and the Fundamental Research Funds for the Central Universities (WUT: 2017IVB014).