Abstract

Born as a term with a critical connotation towards finance, financialization has been widely employed in social sciences, despite the vagueness often surrounding it. In this article we discuss the concept of financialization with a focus on three dimensions. First, we highlight the crucial role of theory in shaping the depth of one’s understanding of the term. Second, we discuss the merits and limitations of the term as a means for bringing together researchers from different communities. Third, we reflect on its future. We argue in particular that the various phenomena associated with financialization involve different boundaries and temporalities. These differences are important, first for appreciating the openness of possible outcomes, and second, for anticipating potential convergences in scholarly perceptions of financialization that might occur in the near future.

Introduction

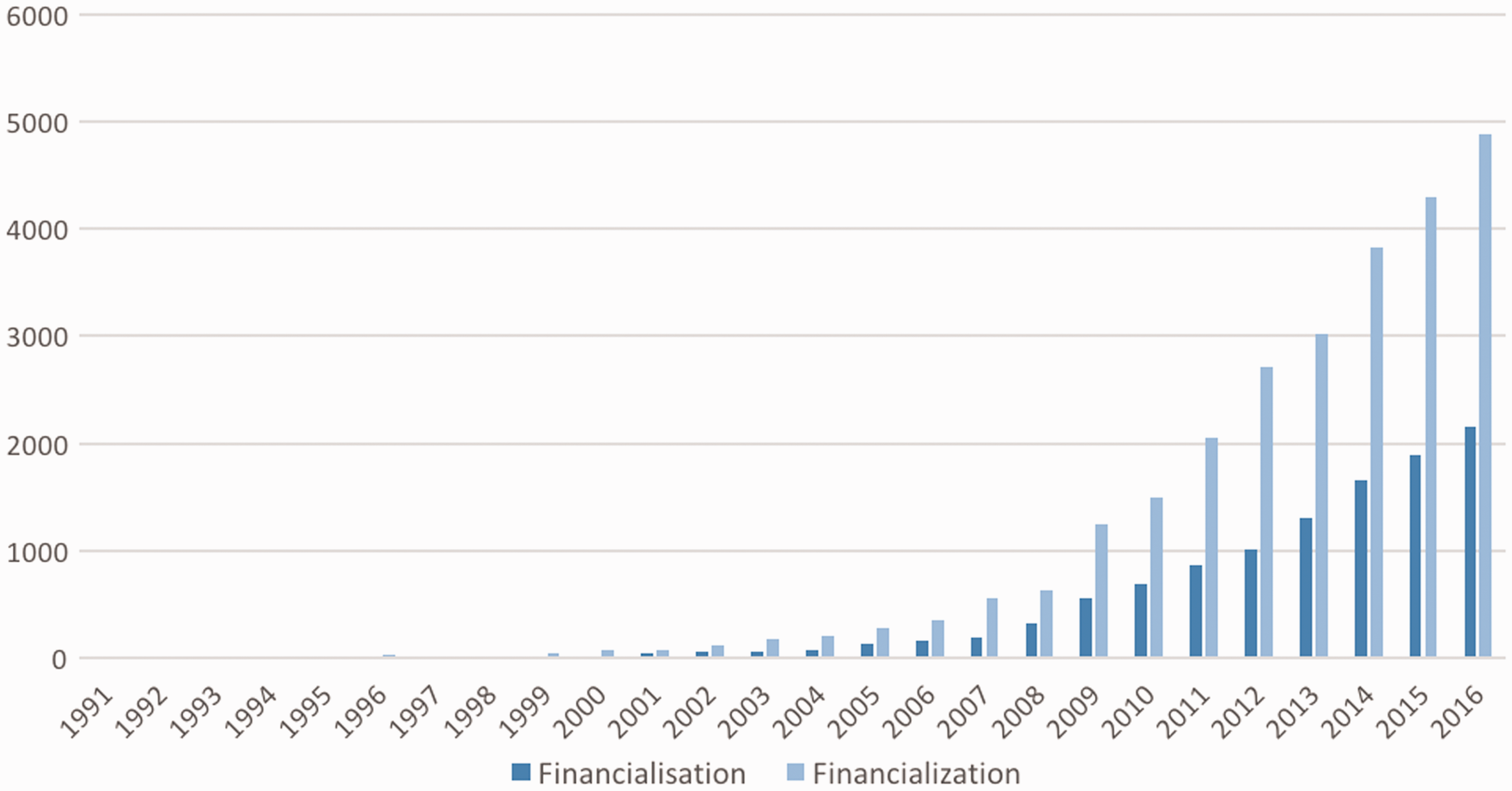

Like neoliberalism and globalization, financialization has emerged as one of the most popular buzzwords across social sciences, aiming at describing, in one way or another, phenomena associated with the expansion of finance in contemporary capitalism (the word contemporary is used here for describing capitalism since c.1980). Despite the variety of definitions attached to the term over time, Krippner’s definition of financialization as a ‘pattern of accumulation in which profits accrue primarily through financial channels’ (Krippner, 2005: 174), and Epstein’s definition as the ‘increasing role of financial motives, financial markets, financial actors and financial institutions’ (Epstein, 2005: 3) have become the most common denominations of the word. 1 As Figure 1 shows, while the term first appeared in the literature in the early 1990s, its use gained momentum throughout the 2000s, and sky-rocketed from the time of the global financial crisis onwards. 2

Use of the term financialis(z)ation in the literature. Source: Google Scholar and authors’ elaboration.

A question as old as the term itself is whether financialization constitutes a novel stage in the history of capitalism, or whether it describes historically repetitive dynamics, such as the recurring growth of the financial sector (on the latter view see, for instance, Christophers, 2015). The issue is very much a definitional one. Definitions such as those provided by Epstein and Krippner are so generic that they can be easily used to support the idea that financialization is nothing but a recurring phenomenon; this is acknowledged by Krippner herself (see Krippner, 2005: 199). On the other hand, was one to identify contemporary phenomena such as the creation of new financial instruments and markets, the acceleration of financial deregulation and the global reach in the expansion of finance as parts of financialization (as, for instance, in Fine (2012) and Sawyer (2013)), the latter becomes much more of a historically specific concept.

Providing a full review of studies related to financialization is a Herculean, if not impossible, task, given the voluminous literature coming from heterodox economics, sociology, political science, geography and so on (a survey of works which in various ways review literature on financialization could instead be a more realistic mission; see, for instance, Christopherson et al., 2013; French et al., 2011; Hein, 2009; Sawyer, 2013; Van Der Zwan, 2014). The aim of this article is rather to offer some critical reflections in three directions. First, we point out the important role of theory in shaping one’s understanding of financialization. Second, we highlight the usefulness of financialization as a focal point for cross-disciplinary dialogue and collaboration, using the FESSUD project as an example (acronym for ‘Financialisation, Economy, Society and Sustainable Development’). Third, we reflect on the future of financialization. To this end, we explore the differences in the boundaries and temporalities involved in the various phenomena associated with financialization.

The analytical spectrum of financialization

To facilitate discussion, in Figure 2 we sketch a simple scheme describing the various phenomena related to financialization, reflecting our own understanding of the term. We distinguish between three broad aspects of financialization. At the epicentre of our scheme is box 2, the group that encompasses phenomena associated with the contemporary world of finance (e.g. credit creation, shadow banking). On the left, we link financialization with its underlying structural transformations and processes, primarily referring here to developments associated with neoliberal capitalism. The role of such developments lies in generating structural necessities for financial expansion. These developments precede to some extent what is observed in box 2. The falling labour share of income and the corresponding need for debt in order to maintain consumption and growth is one relevant example (see Hein, 2011). Another is the globalized reach of trade and investment, a development related to the need for a more global financial architecture and the curtailment of financial regulation (see Harvey, 2010; Lippit, 2014). Shareholder value orientation and the corresponding rise of financial investment of non-financial corporations can also be pointed out as a third example (Lazonick and O’Sullivan, 2000; Stockhammer, 2004).

The analytical spectrum of financialization.

On the right-hand side of Figure 2 are implications that arise out of the processes presented in the first two boxes. Relevant examples include the rise of household indebtedness (Hein, 2011), the influence of finance on fiscal policy (Ioannou, 2016), the growth of current and financial account imbalances (Varoufakis, 2011), as well as the broader impact of finance on culture (Fine, 2012). Overall, in comparison with box 1, which describes factors facilitating financialization, box 3 captures some of its outcomes for the broader economy and society.

As with any typology, the scheme depicted in Figure 2 includes a dose of simplification. Aiming to capture the primary forces in play, our scheme does not portray the reverse causalities involved between these boxes, as well as the connections within the elements of each box. Despite such simplifications however, the scheme is suggestive enough for providing a point of reference for the discussion that follows. First, in providing a canvas for contrasting the reach of theories that study financialization. Second, for elucidating the multifaceted nature of financialization, and thus the need for collaborative research and dialogue. Third, and most importantly, for facilitating the discussion over the future of financialization.

On theory

Clarity over the meaning of financialization by the users of the term is crucial. The issue, however, is not so much the ‘ticking the box’ exercise of copying and pasting one of the many available definitions. Rather, what matters is precision over one’s theoretical starting point. Ultimately, it is the latter that elucidates the meaning of financialization, both at the level of designing a definition, and at the level of using it. Given that financialization is usually taken as a divergence from something, it is vital to be clear on what this something is. At the most basic level, there is a different story to be told, and correspondingly different policy implications to be drawn, if one was to identify stable banking as the abstract normality of the capitalist system, as against treating banking as an inherently destabilizing business. Equally, there is a difference in whether such destabilizing tendencies are for example attributed to the role of bankers as extractors of surplus value, as in Marx, or instead to their role as merchants of debt as in Minsky.

The strengths and limitations of a theory necessarily influence one’s perception of financialization. Based on Figure 2, alternative theories can be contrasted in terms of their reach across the three boxes, as well as the analytical depth each theory offers within each box.

To take one example, consider the differences between Marxian and post-Keynesian scholars in their accounts of financialization. On one side, Marxian economists and geographers have engaged with aspects associated with the first box of Figure 2 more consistently than anyone else. Relevant contributions include, for instance, the works of the Monopoly Capital (MC) and Social Structure of Accumulation (SSA) schools (indicatively, see Magdoff and Foster (2014) and Tabb (2010) for MC and SSA respectively), as well as the writings of David Harvey (e.g. Harvey, 2010). Such accounts, however, often lack the depth of post-Keynesian studies in their analysis of the phenomena associated with banking and finance, that is with the second box of the figure (most notably referring to the utilization of Minsky’s theory of financial instability and the post-Keynesian theory of endogenous money; for elaboration, see Lavoie, 2016).

In the case of Marxian geography, Dymski (2017) points out the conceptual limitations associated with the Harveyan premise wherein financial crises are not so much a product of the inherent financial fragility of the capitalist economy, but rather symptoms related with the deeper contradictions of capital. For a better understanding of monetary phenomena, Dymski highlights the importance of real time and uncertainty, two of the most fundamental pillars of the theories of Keynes and Minsky.

What is even more interesting is that in one of his earlier articles (Dymski and Pollin, 1992), Dymski criticizes Minsky from the opposite point of view, namely for ignoring the impact of the more structural issues related with production and income distribution (a more recent critique along similar lines towards some of Minsky’s followers can also be found in Palley, 2010).

Rather than taking it as a contradiction in Dymski’s writing, his dual critique towards Harvey and Minsky should be seen as indicative of the inherent symbiosis of strength and weakness in any given theory. In that respect, engagement with the various aspects of financialization is a much more demanding task than the mere extension of an existing theoretical device. Theoretical pluralism could instead be a more promising approach. Although such pluralism entails the risk of inconsistency, given that different theories are rarely fully compatible with one another, it is far from obvious that theoretical purity is a more appealing option. A trade-off is always in play.

Financialization and interdisciplinary research

Taking financialization as a multifaceted phenomenon, as sketched in Figure 2, highlights the need for interdisciplinary research. To be sure, such research is never a straightforward exercise, as there are a number of challenges involved, such as the question of which discipline forms the basis and which is invited to add insights (the sequence matters), as well as the risk of compromising disciplinary knowledge (for discussion, see Spencer, 2013). Nonetheless, it also forms an opportunity for mutual benefits for heterodox economists and other social scientists, at both the empirical and the theoretical front.

Especially since the crisis, this need and opportunity have turned financialization into a focal point for cross-disciplinary dialogue and collaboration. In that respect, financialization has performed a positive function, despite the vagueness often surrounding its meaning. One explanation for this merit of financialization is precisely its negligence by neoclassical economists. Being established as an alien notion to the dominant economics paradigm, financialization has been shielded against the traumas related with ‘economics imperialism’, referring here to the use of the core neoclassical tenets as the basis of engagement with ideas outside economics (Brown, 2015; Spencer, 2013). As a result, it has been relatively free of the suspicion of one discipline trying to conquer another.

Perhaps the most representative example of a financialization-based interdisciplinary project is FESSUD. 3 This is to the best of our knowledge the biggest project to explicitly study financialization so far. While heterodox economics formed its core, FESSUD maintained a strong interest in a variety of dimensions associated with financialization. For example, considerations over the links of financialization with the environment and with household well-being occupied 2 out of 12 work packages (for synthesis reports, see Vercelli et al. (2016) and Bayliss et al. (2016) respectively). Furthermore, the project maintained a broad spatial scope, with an independent working package dedicated to the study of financialization in the developing world (see, for instance, Tyson and McKinley, 2014). 4

The FESSUD project also represents a good example of some of the actual limitations and challenges in intra- and cross-disciplinary collaboration. Using FESSUD’s work package 2 (entitled ‘Comparative Perspectives on Financial Systems in the EU’) as a case study, Andrew Brown – one of the project’s leading members – argues that even in a large project like FESSUD, substantial differences remained present among participants (Brown, 2015). While the pluralist notion of ‘variegated financialization’ put forward by FESSUD (see Fine, 2012; Sawyer, 2013) was helpful in creating a common ground for collaboration between people coming from different traditions, this in itself proved inadequate for driving scholars outside their methodological ‘comfort zones’ and for achieving a unified theory at a more abstract level. As an example of the first, Brown points out the treatment of the cultural aspects of financialization by heterodox economists, who although friendly to the idea, were often at pains in capturing it using the quantitative methodologies many of them were accustomed to. Examples of theoretical differences that couldn’t be bridged include the different views of the participants on money, surplus value, capital and profit. Overall, Brown concludes that the collective development of a unified theory of financialization turned out to be a much more ambitious aim than the achievement of empirical gains out of pluralistic research. According to his view, obstacles in this respect are not just the large investment required in time and resources for organizing workshops and face-to-face discussions, but also the occasional difficulty in perceiving the usefulness and relevance of such debates by the different sides involved in such projects.

On the future of financialization

A relatively under-investigated question is whether financialization is seen as likely to develop further, come to a halt or retreat. Some preliminary evidence over what scholars expect comes out of a series of papers written in the context of FESSUD (see Fontana, 2016). Indicatively, out of a Delphi study conducted in 2016 (Ferreiro et al., 2016), the majority of respondents expected the current size of the financial system to either remain the same or increase. In addition, 94% of them anticipated a decline in the importance of banks in the financial system in the near future, while 88% believed that a new financial crisis out of the activities of the non-bank financial system will occur during the next decade.

For the remainder of this article we focus on two more generic questions in order to push the discussion a step further. First, what are the boundaries – if any – of the future development of financialization? Second, how can we classify various aspects of financialization in a way that allows for some anticipation of the future views of relevant scholars? For responding to both of these questions, the analytical separation suggested in Figure 2 can be of help.

Regarding the first question, some sort of tangibility in the boundaries of the first and third aspects of financialization could be expected to exist (left- and right-hand boxes of Figure 2). In the first aspect, for example, the spatial boundaries in the further globalization of trade and investment must create some limits in the further expansion of global finance. Equally, there must be a limit to the structural necessity of finance to support aggregate demand and prevent economic stagnation. In the third box, it should also be possible to identify some boundaries with regard to what can still be financialized and to what extent. The subordination of fiscal policy, for example, to the logic of financial markets can be maintained or overthrown; its further advancement, however, is hard to conceive.

Tangible boundaries as such do not exist in the second aspect of financialization, represented by the middle box of Figure 2. On one side, as pointed out by post-Keynesian scholars, banks do not face a physical constraint in their capacity to create credit, and correspondingly in their operations and profitability (e.g. Lavoie, 2012). As argued by Lavoie (2012: 225–226), ‘[t]here is no pool of loanable funds out there that limits monetary growth. Credit creation depends on the liquidity preference of banks and the confidence of borrowers’. Credit (i.e. debt) creation, in other words, is not governed by the ex-ante existence of savings, but by the expectations of those who supply and demand it. Although banking regulation and monetary policy can exercise indirect control over lending, these are policy choices, not natural constraints.

In a similar fashion, depending on the demand and acceptance of securitized assets, securitization is a process that can in theory reach infinite degrees. This is not just a concern over the length of the list of assets that can be securitized, but also a remark on the nature of securitization as a process of bundling and reselling existing financial assets. It might be easy, for example, to observe the inexistence of any sort of physical constraints in the creation and circulation of mortgage-backed securities during the pre-crisis period. Equally, apart from financial regulation, there is nothing to stop banks from designing ‘innovative’ products that ‘this time will be different’. If, for instance, the pooling, packaging and reselling of student loans feels a bit too risky, why not design a new product based on the pooling of pooled student loans? Or, why not diversify them by pooling them together with a pool of pooled university bonds? As long as there is a demand for products of this sort, such products will be created.

On what this has to do with financial regulation and policy, it suffices here to point out Trump’s unravelling of the Dodd–Frank Act as evidence against any kind of projection that would foresee the re-regulation of finance as something waiting ante-portas. 5 It is also worth mentioning the calls of caution voiced against quantitative easing, criticizing it as a programme capable of giving rise to new asset price bubbles (Fullwiler, 2013). To be sure, our aim is not to forecast a new financial catastrophe coming up, but instead to highlight the openness of possible outcomes.

In addition to the above, the schema offered in Figure 2 is helpful for capturing three possible convergences that might occur in the near future with regards to scholars’ perceptions of whether the global economy will have entered into a stage of de-financialization or not. Notice that by the word ‘near’ we mainly think of a time frame of about a decade from now, as against 30–40 years’ time, when a broader consensus might eventually be in place. Second, in our use of the word, de-financialization broadly describes the move towards an era in which finance, along with its political and economic power, will have been tamed. This, however, does not necessarily imply the exact restoration of the pre-1980s state of affairs.

Taken with some abstraction, what separates the three boxes identified here are the timings and interactions each involves for change to occur and be observed. For example, the structural side of financialization (left-hand side of Figure 2) needs much more time for change to be recorded as compared with the more tangible changes in credit creation or financial regulation. This is even more so if one considers structural developments, such as the distribution of income, not just as objects of interest in themselves, but also as prime movers of change in aspects related to boxes 2 and 3. Identifying threads that link observed structural processes and outcomes is an exercise that always comes with a notable time-lag.

Equally, a potential reversal of the implications included in box 3 of Figure 2 might not necessarily wait for a complete transition into a new era of capitalism to take place. The cleaning up of the balance sheets of the private sector for instance – that is, the reduction in the debt exposures of households and firms – might not wait for any structural conditions to be transformed.

All in all, there are three levels at which change might be recorded in the years to come, each associated with the three sides of financialization depicted in Figure 2. What is at stake is the transformation of the deeper factors which facilitate and ‘invite’ financialization, the re-organization of the financial system itself, and lastly the ‘updating’ of outcomes such as those listed in box 3. Change in each of these levels is of course not independent from the rest. Equally, though, such transformations will not necessarily be synchronized in their unfolding.

Future scholarly perceptions over the continuation or not of financialization will crucially depend on which of these levels different people will look at, and on the ways in which the observed changes will be brought together. Ultimately, this boils down to the theory or theories adopted for entering the financialization discourse.

Footnotes

Acknowledgements

The authors would like to thank Malcolm Sawyer, Giuseppe Fontana and Andrew Brown, as well as the rest of the people involved in the FESSUD project, for all the fruitful discussions held in the past. We are also grateful to Gary Dymski and two anonymous referees for their fruitful comments on earlier drafts of the paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The paper has benefited from funding from the European Research Council (European Union’s Horizon 2020 research and innovation programme; grant agreement no. 681337). The article reflects only the authors’ views and the European Research Council is not responsible for any use that may be made of the information it contains.