Abstract

This paper presents a novel understanding of the changing governance structures in global supply chains. Motivated by the global garment sector, we develop a geographical political economy dynamic model that reflects the interaction between bargaining power and distribution of value among buyer and producer firms. We find that the interplay between these two forces, in combination with the spatial specificities of global production and consolidation, can drive governance structures towards a more symbiotic position.

Keywords

Introduction

‘Globalization’ – specifically the globalizing of production and trade – brought with it new analysis and a new language. The global value chains (GVC) framework played an essential role in understanding the governance of a now globalized production. GVC analysis emerged out of the global commodity chain (GCC) framework of Gereffi and Korzeniewicz (1994), but went beyond the commodity by introducing governance categories that attempted to map the asymmetrical relationships between the various actors in the chain. Gereffi’s (2002) original conception divided supply chains into two distinct categories of governance – producer-driven and buyer-driven – while Gereffi et al. (2005) identified five types: market, modular, relational, captive and hierarchical.

These frameworks have been an important means by which to analyse global production, upgrading, trade and the developmental process. Despite these successes, the GVC approach has been criticized for being static and not accounting for geographical, social and institutional specificities. These critiques were addressed by the introduction of the global production networks (GPN) approach (Coe and Yeung, 2015; Coe et al., 2004, 2008; Dicken et al., 2001; Henderson et al., 2002; Yeung, 2009). In addition, GPNs aimed to capture how different actors, including states and institutions, influence global production. They emphasize three variables: (a) value, (b) power relations that affect the distribution of value and (c) territorial embeddedness that takes account of the various social and institutional implications of global production. While GPNs added much-needed complexity by including both co-constitutive and contingent factors, this approach has been criticized for lacking the explanatory power of the GVC framework. 1

This tension between complexity and explanatory power opens up a major gap and can, in part, explain the absence of a framework that captures the dynamics of GVC governance structures. The present paper aims to fill this lacuna by utilizing variables from the GPN framework and introducing a formal dynamic model in which: (a) governance structures are shaped by the bargaining dynamics between producers and buyers in the chain; (b) bargaining power is contingent on the geographic possibilities of production; and (c) this bargaining affects the distribution of profits between buyers and producers.

Our model, being the first of its kind to analyse governance dynamics, offers a novel means of studying the evolution of governance structures by taking into account the effects of geography in bargaining between global buyers (brands/retailers) and suppliers/producers (manufacturers). Our analysis draws on some, but not all, elements from both GVC and GPN literature. As such, we do not claim that our model is a formalization of either GVC or GPN frameworks, while sharing key components of both. Thus, we refer to the structure of our model as a global value network (GVN).

Our GVN assumes two types of firms that we call buyer(s) and producers. Simplifying the firm types allows us to more easily link power relations with governance types. Within this context, what we call producers are the outsourced manufacturers, sometimes referred to as ‘suppliers’ in the literature. What we call buyers includes brands, retailers or even producers that are ‘buying’ a good from an outsourced manufacturer.

We introduce the concept of degree of monopsony power (DMP) as essential in determining the share of value captured by buyers in the GVN. Drawing on Mahutga (2012, 2014), we relate governance structures on producers’ entry–exit dynamics and on buyers’ bargaining power captured by DMP. As we demonstrate in our model, higher DMP leads to a greater share of value captured by buyers, resulting in increased downward pressure on producers. In this way, if DMP rises then the ‘buyer-driven’ dynamics of the GVN are intensified. Conversely, when DMP falls the GVN takes on a more ‘producer-driven’ character.

In our framework, the DMP of a buyer depends on the number of producer firms able to compete for the production of a commodity. Due to the geographic dispersion of producers, there is a distribution of costs among them, which depends on the local institutional specificities. In this way, geographic dispersion of production affects the variance of the distribution of costs among the producers. Furthermore, the number of firms able to produce a commodity will depend on the share of total value obtained by the buyer firm. Thus, an increase in the share of profits that the buyer obtains leads to a smaller number of producer firms able to compete, causing consolidation and growth in the size of those firms.

The formal model herein is motivated by an explicit call from Sheppard (2001, 2011), Bergmann et al. (2009) and Plummer et al. (2012), among others, for the development and use of formal disequilibrium models within geographical political economy. For this reason, our model does not rely on the methodological framework of neoclassical economics, where the properties of the economy result from the optimal decisions of agents (e.g. firms). Rather, it uses behavioural equations that capture the relevant properties of the economy (in our case of global production). Our framework belongs to the family of the dynamic disequilibrium models frequently used in post-Keynesian and neo-Marxian traditions, 2 and also has similarities with the evolutionary economic geography framework. 3

Even though our approach shares some of the main methodological assumptions of the post-Keynesian models, it also abstracts from others that are characteristic of the post-Keynesian tradition, like effective demand, or the role of capacity utilization. While these assumptions are important when analysing the macroeconomy, our approach is able to abstract from these issues since our level of analysis is the value chain and not the national economy. However, the choice of this framework lays the ground that can allow for synergies between post-Keynesian and GVC/GPN approaches within the broader field of critical political economy.

The paper is structured as follows. The next two sections motivate the key features of our modelling framework, namely allowing (a) for a continuum of governance types, (b) for the types to change over time and (c) for us to understand DMP as the principle constituent of these dynamics. The first of these sections briefly examines how governance structures relate to power dynamics and demonstrates the usefulness of treating these governance structures as a continuum, while the second (a) builds on previous studies that reveal the dynamism of governance structures in which the specificity of relations cannot be understood through overarching categories, and (b) highlights the centrality of the monopsonistic structure of the market and introduces the concept of DMP. In the fourth section we present our formal model, followed in the fifth section by the results of the model and relating them directly to a number of examples in the garment sector. The following section discusses several of the model’s assumptions and proposes directions for future research, before the final section concludes the paper.

Global value chain typologies

In recent decades, GVC literature has in large part focused on the relevance of the original buyer-driven versus producer-driven governance dichotomy. Producer-driven chains are those in which large transnational manufacturers play a central role in coordinating value chains. These chains are predominantly in high-technology, vertically integrated, capital-intensive sectors such as automotive, aeronautic and heavy machinery industries. Here, value capture at the point of production is greatest because of high barriers to entry, limited competition and enhanced ‘control over backward linkages with raw material and component suppliers, and forward linkages into distribution and retailing’ (Gereffi, 2002: 3). Gereffi’s theory is based on the assumption that ‘lead firms’ in producer-driven chains typically belong to international oligopolies (e.g. Ford, Airbus, Caterpillar, etc.). These large, often transnational and oligopolistic firms, have greater access to finance and self-finance (through the retention of profits), and are therefore capable of substantial technological enhancement. Increased investment in fixed capital simultaneously raises the firm’s liability while helping it to be dominant in the value chain, exerting a great deal of influence on smaller and highly dependent subcontracted firms.

At the other end we find ‘buyer-driven’ GVCs, which are in low-value, low-technology, vertically dis-integrated sectors such as garments, footwear, toys, furniture and light electronics. These sectors maintain a high degree of ‘fragmentation’ (Arndt and Kierzkowski, 2001) and a wide spatial spread. This extensive geography is an outgrowth of low barriers to entry at the producer-end, since manufacturing costs are low with minimum capital investment, resulting in mostly small and mid-size firms competing intensely at ‘lower end’ GVC phases.

While Gereffi’s category of ‘producer-driven’ resembled the Fordist model of production that embodied capitalist modernity, the novelty was found in his introduction of the buyer-driven GVC (Gibbon et al., 2008). A key intervention is the recognition that the relationship between buyer and producer is asymmetrical without a formal hierarchy. In the absence of a formal hierarchy, power becomes the central driver in shaping the GVC (Bair, 2009).

Many studies built on Gereffi’s original binary, in which powerful actors dictated the size, capacity and upgrading of outsourced manufacturers (Knutsen, 2004; Kumar, 2014; Kumar and Mahoney, 2014; Lee and Cason, 1994; Tokatli, 2004). Among the most influential of these has been the work of Sturgeon (2001, 2002, 2003). 4 Sturgeon (2001) builds on the original framework of Gereffi by focusing on the degree of standardization of production and how this is reflected in the GVC. As Sturgeon (2001: 15) states, ‘we need to link our terms not to firms, sectors, or places but to the specific bundles of activities that firms are engaged in’. To that end he constructs five types of value chain/production network ‘actors’, defined by their ‘scope of activity’: integrated, retailer, lead firm, turn-key supplier and component supplier.

As a response to these challenges to Gereffi’s original types, Gereffi et al. (2005: 79) generated a framework to capture the ‘shifting governance structures’ to move beyond the duality of the buyer- and producer-driven frameworks. In particular, they focus their attention on the ‘possibilities for firms in developing countries to enhance their position in global markets’, and in theory we are motivated by a similar purpose. Where we part ways is in what is proposed. Gereffi et al. (2005) propose a five-part typology to value chain governance taking account of the evolving nature of GVCs and upgrading potential. By taking account of the degree of explicit coordination and increasing power asymmetry, these governance categories are understood in the following order: market, modular, relational, captive and hierarchy.

In market GVCs, both buyers and suppliers are able to switch partners with relative ease. In modular GVCs, similar to Sturgeon’s (2002, 2003) ‘turn-key’, the supplier firm produces exclusively for lead firms, with higher liability for the supplier. Relational GVCs have a high degree of capability at the supplier-end, contributing to a mutually dependent relationship. In captive GVCs there is a clear dependent relationship between small suppliers and large lead firms, with the lead firm maintaining a high degree of control. Hierarchical chains are vertically integrated, with a high degree of managerial control.

Furthermore, Gereffi et al. (2005) go beyond the buyer/producer dichotomy by adding complexity of transactions, codifiability of information and capability of suppliers in determining GVC governance structures. We are indebted to their proposed typology, which explains the conditions of industrial upgrading and its effect on the GVC. Our work extends on this in two directions. First, while the governance categories of Gereffi et al. (2005) express a discrete spectrum of GVC governance characteristics, our model recognizes the spectrum as continuous. Second, while the aim of Gereffi et al. (2005) is to more accurately describe the characteristics of each of the categories, our focus is to understand the forces that drive the change from one structure to another and to identify any long-run trend.

Both Gereffi et al. (2005) and the present paper place power central to understanding the changes in GVC structures. In what follows, we draw on the work of Mahutga (2012, 2014), who argued that ‘the original buyer/producer-driven governance scheme is a continuum running between the buyer and producer-driven ideal types’ (Mahutga, 2012: 9).

Mahutga (2014) utilizes Gereffi’s binary to highlight the significance of barriers to entry in determining the bargaining power of actors within the global supply chain. He argues that the relative supply of manufacturers and buyers in a given chain is an indication of a manufacturer’s barrier to entry and therefore their bargaining power. Supporting this claim empirically through cross-national data, Mahutga shows that a manufacturer’s bargaining power is inversely related to the available alternatives. Simply put, for a manufacturer, fewer alternatives mean greater bargaining power, more alternatives mean less bargaining power, and vice versa for buyer firms. Critically, ‘the main point of similarity across buyer/producer-driven chains is that their structures reflect the most optimal location of activities, both inside and outside of the lead firm, from the perspective of the lead firm’ (Mahutga, 2012: 6; original emphasis).

Degree of monopsony power in a dynamic context

Degree of monopsony power and governance dynamics

Within our framework, we assume imperfect competition, and DMP is a key variable of our model. Imperfect competition is a standard assumption in both the GVC/GPN and post-Keynesian literatures 5 but also is often found within the neoclassical microeconomic literature. To reiterate, our modelling framework has key methodological differences to the neoclassical approach, but is not ‘strictly’ post-Keynesian due to differences in our level of analysis.

Monopsony, according to Robinson (1969), refers to a market with many sellers and a single buyer, or in the case of labour markets, a single firm and more workers than the ones needed by the firm. Here we consider – instead of one employer and many workers – a single buyer firm and many producer firms. Note that on this level of analysis, the concept of the degree of monopoly power of a producer firm vis-à-vis the buyer captures exactly the inverse relationship of the DMP of the buyer vis-à-vis the producers. Based on this, we could focus on the degree of monopoly power rather than on the DMP; however, this would make the analysis more complicated and would not allow for a tractable analytical model.

More concretely, in our framework we define monopsony power as the ability of the buyer firms to extract higher value from the producers than what would be the case in a perfectly competitive market. Furthermore, the DMP aims to capture the level of this ability, such that a relatively high DMP results in a greater share of value obtained by the buyer firms. In low DMP GVNs, producers are the drivers of the GVN and tend to retain direct control over capital-intensive phases of the GVN, while subcontracting out more labour-intensive functions to suppliers that are organized hierarchically and managed by the producer firm.

Within GVC analysis, the concept of monopsony has been used, albeit more descriptively, to understand the asymmetry of power between buyers and producers (see Abernathy et al., 1999; Anner, 2015; Anner et al., 2015; Azarhoushang et al., 2015; Mayer and Phillips, 2017; Milberg and Winkler, 2013; Nathan et al., 2007). We maintain that the relationship between the number of producers able to compete in relation to the number of buyers in the market shapes and circumscribes the dynamics of the GVN. As Nathan and Kalpana (2007: 4) outline: The lead firms in buyer driven chains have enormous, oligopolistic market power. As buyers the volume of their purchases gives them monopsonistic power. On the other hand, with the spread of manufacturing and processing capabilities around the world, the suppliers are in very competitive markets. This asymmetry of market positions, oligopoly/monopsony vs. competitive, leads to a corresponding asymmetry in bargaining power. Lead firms are able to utilize their buying power to beat down suppliers’ prices.

However, even bound by the MFA straightjacket, value nonetheless accrued to buyers sitting at the top of the chain. As the MFA came to a close, this power gap between buyers and their suppliers began to widen further. Anner et al. (2015: 7) observe that the price paid per square metre in the international market dropped as the MFA was being phased out (1995–2005). They explain this phenomenon through two factors both linked to the end of the MFA. First, buyers, no longer bogged down by the same quota constraints, began shifting production from regions with relatively high labour costs, such as Mexico and Central America, towards those with lower labour costs, such as China and Southeast Asia. Second, they claim that these changes reflect the ‘growing concentration of retailer power vis-a-vis suppliers, where, as a result of monopsonistic supply chain structures, retailers and major brand manufacturers are increasingly able to squeeze lower prices from their ranks of global suppliers’. In particular, this latter contention corresponds with our model, which shows that lowering the restrictions on trade results in higher DMP and a greater share of value to the buyer.

This coheres with Feenstra (1998), who linked the ‘disintegration of production’ in the international economy with the ‘integration of trade’. As Gereffi et al. (2005: 80) state, ‘the rising integration of world markets through trade has brought with it a disintegration of multinational firms, since companies are finding it advantageous to “outsource” an increasing share of their non-core manufacturing and service activities both domestically and abroad’.

As we moved into the post-MFA era in the mid/late 2000s, the heightened DMP reached its zenith. With increased downward pressure and falling source price offered by buyers, increasingly fewer suppliers were able to compete. This process has seen globalized competition weaken, with an almost endless number of small firms across the globe disappearing, absorbed into larger rivals or forced to merge. What is emergent is a coterie of mega-producers in a handful of labour-rich countries (Appelbaum, 2008; Azmeh and Nadvi, 2014; Lopez-Acevedo et al., 2012; Merk, 2014). Meanwhile, large retailer/brand oligopolies simultaneously benefit from growing profits brought on by economies of scale and integration, while becoming gradually dependent on increasingly oligopolistic outsourced manufacturers. Thus, the transition away from high DMP is a move away from the ‘buyer-driven’ end of the spectrum.

Consolidation and symbiosis

As part of the logic discussed above, the result of falling sourcing prices by buyers was the vanishing of uncompetitive firms, and the mergers and acquisitions of firms into mega-firms. The rise of consolidated firms in the global garment sector has a material basis in the logic of capital itself. Producer firms in ‘buyer-driven’ sectors and the states where they reside are placed under constant downward pressure by global buyers to cut costs, produce greater volumes of goods at quicker turnover times, stock less inventory, ensure labour discipline and so on. As such, what remains constant within capitalist development is the increasing efficiency, size and reliability of firms. Over a relatively short period of time, this downward pressure left fewer and fewer firms able to compete. Consequently, these firms would produce more, having absorbed the production capacity of smaller firms.

Marx’s economic writings – particularly volumes 1 and 2 of Capital and Grundrisse – argue that the increases in speed, scale, size and cost-efficiency of production are motivated by competitive pressures. This is part of the inner logic of capital accumulation. Therefore, consolidation is not an anomaly but part of the structural dynamics of capitalist development. Consolidation also assists in shortening the time of production, circulation and distribution. Recent decades have seen firms associated with the ‘developing world’ become increasingly adept at generating ‘value-added’ activities across the value chain.

There is an increased recognition of garment manufacturing firm growth, particularly in Asia, in the post-MFA world (Appelbaum, 2008; Azmeh and Nadvi, 2014; Gereffi, 2014; Merk, 2014). The sector’s low value and low technology established low barriers to entry, which began to change with the end of the MFA. Consequently, the trend towards consolidation has accelerated. Global brands have dramatically reduced the number of producers in fewer countries and reduced associated costs of logistics, warehousing and turnover time. For example, in Sri Lanka between 2005 and 2014 the number of garment factories has contracted by 50%, while the share of exports to the USA and EU remained constant, and larger Sri Lankan suppliers, such as Brandix or MAS Holding, grew significantly. These are similar to trends in other ‘labour-rich’ countries (Kumar, 2019b).

Gereffi’s (2014)recent research goes even further in recognizing the growing role of increasingly consolidated contractor firms, such as Foxconn in electronics, Li & Fung in apparel and Yue Yuen in footwear. This growth of larger producers is contributing to declining DMP for buyers. Crucially, we identify contracting DMP as leading directly to low-value small and mid-size firms morphing into higher-value large supplier firms. This move into value-added phases of the GVC transforms the decidedly buyer-driven character of the GVC into something markedly different.

We call this different intermediate phase buyer–producer symbiosis, recognizing the growing ‘symbiotic’ market power relationship in garment and footwear between large transnational buyers and large transnationalizing producers. Crucially, consolidation has played the central role in these new relations of power. As we have established, GVCs are not static, and just as ‘the increase[ed] disaggregation of value chains … allowed new kinds of lead firms to capture value’ (Pickles and Smith, 2016: 25), so too the mergers, acquisitions and consolidation of supplier-end capital into large capital-holding producers allows new kinds of garment and footwear supplier firms to capture value.

‘Buyer–producer symbiosis’ is not limited to the calculable relationship (i.e. transaction costs) between buyer and producer, but resembles one-half of Gereffi’s (1994: 95) original formulation, which was to ‘show how “big buyers” have shaped the production networks in the world’s most dynamic exporting countries, especially in the newly industrialized countries of East Asia’. As Starosta (2010: 437)observes, ‘the concept of governance was originally devised to depict the diversity of authority and power relationships that give overall coordination to the division of labor within the commodity chain’. In this vein, the introduction of ‘symbiosis’ is an observation of the power relationship, through an analysis inter alia of changes in structure, technology and geography, as the consequence of the emergence of giant capitals on either side of historically low DMP GVCs.

Model

We consider a very basic GVN structure in which a single buyer firm outsources (part of) the production of a product. We assume that there are N > 1 producer firms in the market, where N varies due to reasons we discuss in detail below. Following Mahutga (2012, 2014), we can relate the governance structures with the number of competing firms.

Assume that the buyer outsources the production of a good to firm Fi, where

A producer firm would only be able to, or have an incentive to, enter the market if their potential profits are positive. For this to be true, costs have to be sufficiently low for a given v and s – that is, the following relationship should hold

Based on this reformulation, equation (3) can also be understood as a type of market entry condition for producer firms. From equation (3), it follows that the number of producer firms that are able to compete for the production of a good with given v depends on s and the distribution of the costs ci.

Note that the costs ci vary across firms due to a number of reasons, such as transportation cost differentials, network externalities 6 and other conditions of production that remain contingent on specific local cost considerations such as taxes and/or labour laws. It is evident that the distribution of ci depends on these factors. For example, if all possible producer firms had close geographic proximity within the same country, then given the same transportation costs, and legal framework, ci would not vary significantly across firms. However, if high geographic proximity is not assumed, then the variance of ci would be greater.

Hence, the number of producer firms able (or with incentives) to join the market, N, will depend not only on the buyer’s profits s, but also on the geographical distribution of production through its effect on the distribution of ci. Furthermore, the costs of production are also influenced by the available techniques. This means that on average technological change will lead to production costs diminishing over time, thus allowing more producer firms to join the market. Let:

γ capture the geographical concentration of firms, such that high γ means that firms are spatially concentrated and hence low variance in the distribution of ci, while high values of γ would correspond to the opposite situation; and δ capture the positive effects of technological change on increasing N by reducing costs across firms on average,

such that N increases if

This condition is related to the intuition of equation (3), as the less geographically dispersed firms are (high γ), the more concentrated ci will be. This will then mean on average that fewer firms will be able to compete. Based on this, we can formally express the change in the number of producer firms in the market,

Equation (5) captures the interrelated effects of technological change and the geographical possibilities of production on the number of producer firms in the market. For given s, if production is highly spatially concentrated (high γ), then technological improvements may not necessarily have positive effects on reducing costs as these improvements may not ‘reach’ that specific place of production. Alternatively, if production is spatially dispersed then it is more probable that at least some of the firms will benefit from technological improvements.

As Mahutga (2012, 2014) has convincingly argued, governance structures can be related to the number of competing firms. Specifically, when the ratio of buyers to producers is low (high), he has shown that the governance structure is buyer-driven (producer-driven). By assuming a single buyer in our framework, the relative position of the governance structure within the buyer-driven/producer-driven spectrum is dictated by N.

Let d be the DMP of the buyer firm. Following from our definition of DMP, a change in d is positively related to a change in N. Given that the DMP of the buyer is positively related to N, it follows that relatively high (low) d means that the governance structure is relatively buyer-driven (producer-driven). In this way, changes in d capture changes in governance. Then, from equation (5), the change in d can be expressed as

Up to now we have focused on changes in DMP and have assumed the profits of the buyer firm s (given v) as fixed. However, as we have already discussed, s depends itself on the DMP of the buyer firm. More specifically, from the definition of DMP, it follows that a change in s will depend on the level of d at that point in time. Given that a change in s can be either positive or negative, we assume that there exists a level for d; call this for if if

Based on this, we can express the change in s as

The level of

Then, from (7) and (8), we get

Results

The system of equations (6) and (9) fully describes the dynamics of our GVN. In this section we will analyse the evolution of the two endogenous variables d and s. Defined as the steady state of equations (6) and (9), the values of d and s such that

However, the most interesting question is how the variables behave if their values are not the steady-state values. In the type of systems such as the one here,

9

the behaviour of the variables out of the steady state can take three forms:

converge to the steady-state values, which means that the steady state is stable; diverge from the steady-state values; or move around the steady-state values in a cyclical manner without converging or diverging.

Furthermore, in the first and second cases, convergence or divergence can be realized in a cyclical way. The specific behaviour of the system, which represents a GVN here, depends on the relative values of our exogenous variables and parameters. Proposition 1 describes the dynamics of our GVN:

has a steady state at the steady state is always stable; and the steady state is a spiral node if

The key insight from Proposition 1 is that the steady state is stable. This results from the fact that model is characterized by two opposite forces that depend to each other and counteract one another. Given that the steady state is always stable, the GVN governance will be converging to an intermediate structure of the buyer-driven/producer-driven continuum. This convergence captures what we previously defined as buyer–producer symbiosis. Hence, we can refer to the steady state here as a symbiotic steady state. As we can see from Proposition 1, the symbiotic level of profits of the buyer firm (as a share of value) depends on the level of technological progress and the spatial concentration of producers. This follows closely from the fact that high spatial concentration of production may impose limitations on being able to take full advantage of technical change.

Proposition 1 also shows that the convergence to the symbiotic state can happen in two different ways: smooth or through cyclical oscillations (spiral node). Interestingly, the type of convergence depends on the geographical dispersion of production. The last part of Proposition 1 argues that low geographical dispersion (high γ) will ceteris paribus lead to a smooth transition to the symbiotic state. The transition is also smooth when the effects of consolidation are important (high β1).

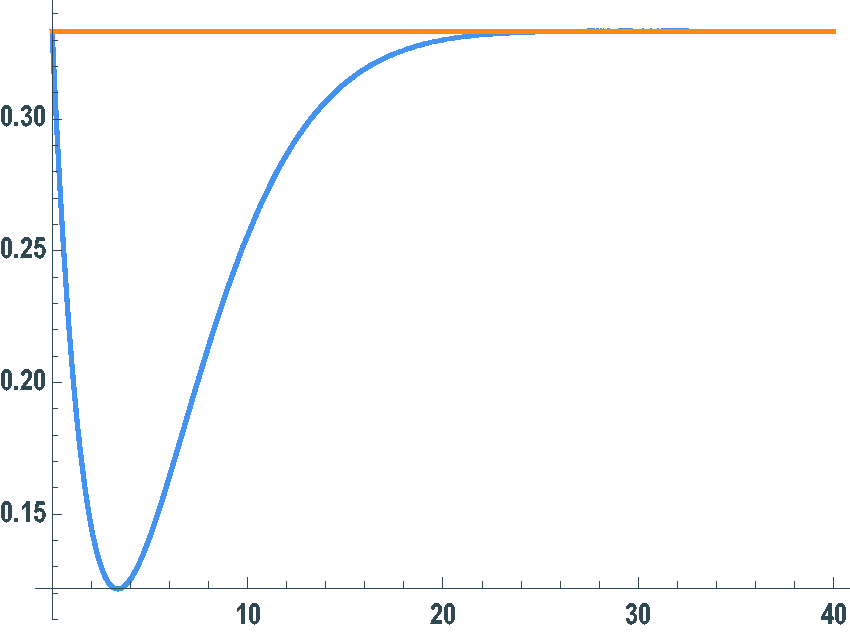

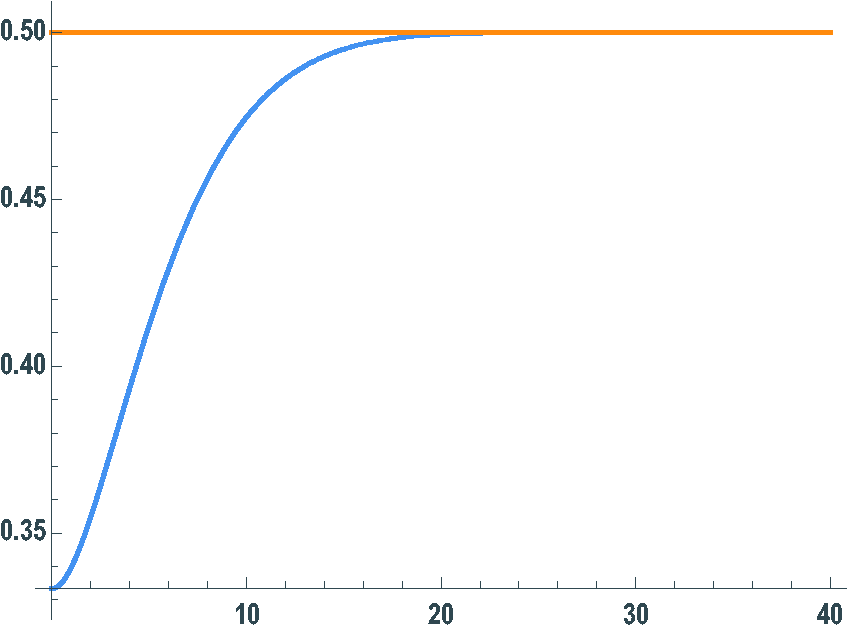

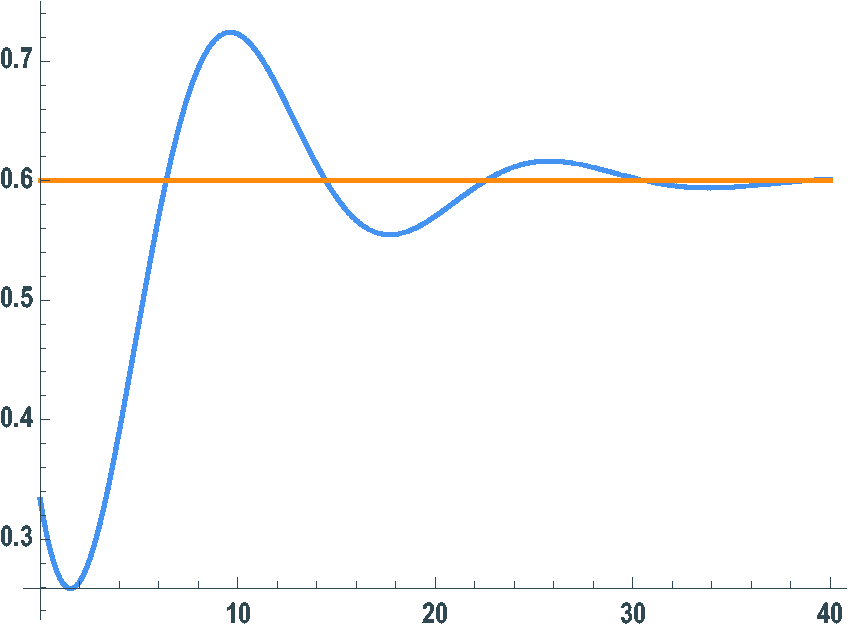

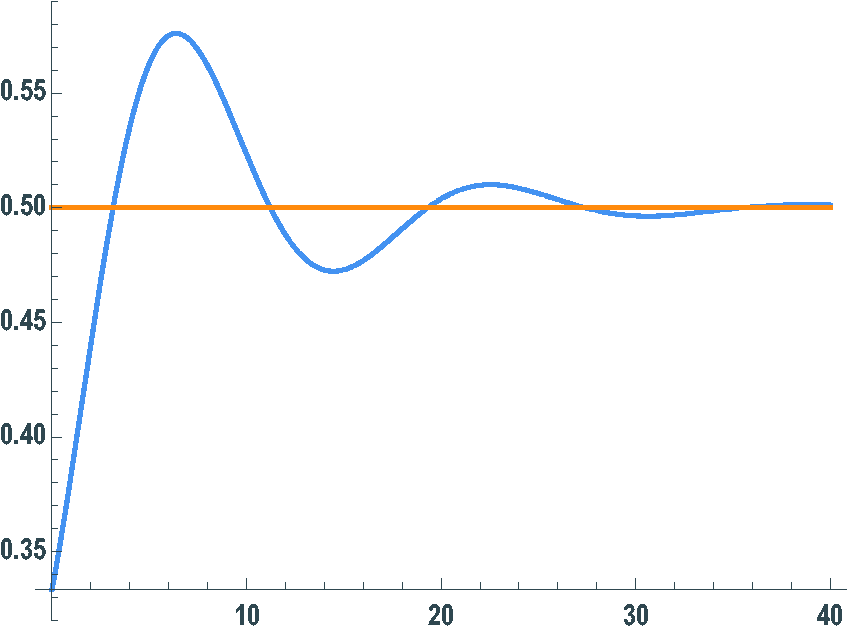

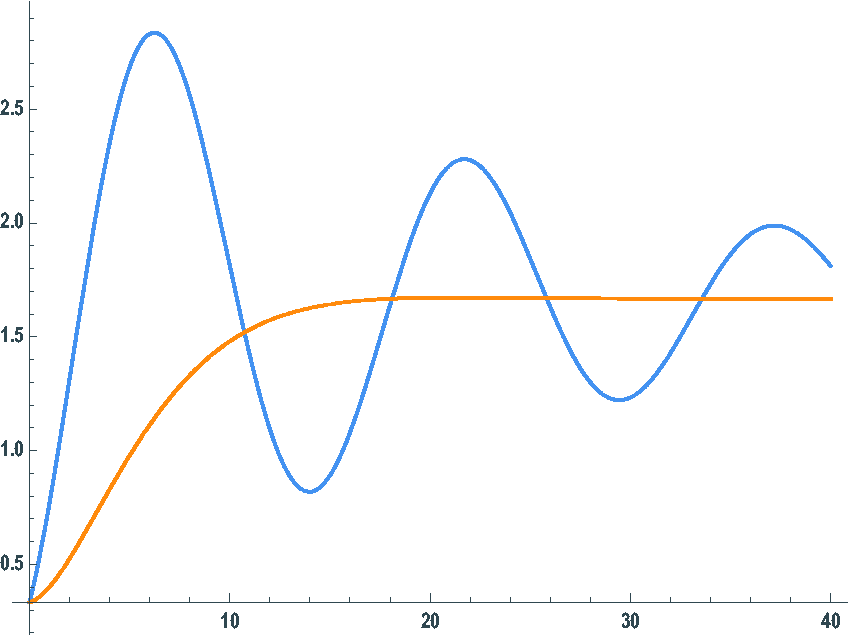

While the key result from the model is the transition to the symbiotic state, Proposition 1 shows that when the transition is not smooth, the governance characteristics of a GVN might change over time. For example, before a producer-driven GVN reaches the symbiotic steady state it may, for a relatively short period, become more buyer-driven compared to the symbiotic steady state and vice versa. The two different cases regarding the transition to the symbiotic state are shown in Figures 1–5. The horizontal axis is time, while on the vertical axis are the values of our variables. In the four first graphs the orange lines correspond to the symbiotic values, while the blue lines correspond to the variables when these do not start from the symbiotic state values. Specifically, in all cases the initial value for the variables is

Blue line: s; orange line: steady-state value for s.

Blue line: s; orange line: steady-state value for d.

Blue line: s; orange line: steady-state value for s.

Blue line: s; orange line: steady-state value for d.

Blue line: N for low γ; orange line: N for high γ.

The first and second figures show the evolution of s (Figure 1) and d (Figure 2) when production is spatially concentrated (high γ). Figures 3 and 4 show the dynamics of s and d, respectively, when production is spatially dispersed (low γ). For Figures 1 and 2, the parameter values are

Figures 1–5 represent the two different types of dynamics that can be observed in our model, as shown in Proposition 1. In all cases we can see a convergence to the steady-state value of each of the variables. The difference has to do with how dispersed production is. As Figure 5 shows, high geographical dispersion (low γ) allows for a higher number of firms able to compete, which means that N can get a greater range of values than in the opposite case (high γ). As N is directly related to DMP, d will follow similar dynamics to N. Hence, given the stability of the steady state, a high range of values for d will lead to cyclical convergence. This highlights the potential instability of governance structures due to potential changes in the geographic extent of production.

The purpose of this paper has been to put forward a disequilibrium model able to capture the changes in governance in global production. Our model reveals that, given our assumptions, a GVN converges to a symbiotic state. Gereffi et al. (2005) cite the garment sector, among others, which they identify as moving from a high DMP structure (captive) to a lower DMP one (relational), and predict the emergence of consolidated ‘full package’ suppliers may move it further to an even lower DMP structure (modular). This is reflected in our model, as high DMP immediately followed the unrestricted free flow of goods from sellers to buyers. However, afterwards DMP steadily falls due to competitive pressures and consolidation.

An indicative example within the garment sector is denim value chains, whose developments are barometers of the sector as a whole. Denim remained relatively inoculated from fashion-sensitivity and seasonality that plagued other parts of the sector. This allowed it to remain vertically integrated well into the 1990s. However, in the 2000s and following the end of the MFA it became fragmented. Recent years have seen denim become consolidated faster than other parts of the sector (Kumar, 2018). This evolution of the denim sector from low to high DMP and now back to low DMP follows the intuition of our model highlighted in Figure 4. This is also mirrored in the highly standardized production of men’s underwear (Kumar, 2019b).

Another illustrative example, adjacent to the garment sector, is found in global footwear. Footwear is an object lesson in these long-term trends because it was the sole clothing industry unencumbered by the MFA. The relatively untrammelled growth and globalization of footwear production resulted in greater oligopoly of buyers. They were able to accomplish this because they had a highly monopsonistic relationship with manufacturers in markets with low barriers to entry (Schmitz and Knorringa, 2000). Eventually, competition compelled smaller manufacturers to consolidate. This caused a fall in DMP, producing an increase in the share of value for manufacturers, giving them more weight in negotiations with buyers. Fast-forward to the present day, and Adidas and Nike, who together control over 50% of the world market for sport and casual shoes (Merk, 2008), have announced that they will be opening fully automated production facilities in Germany, France, the USA, and the UK (Kumar, 2019a). This can be read as a response to a symbiosis in the footwear industry that has created a crisis in profitability and left the major brands exposed.

Extensions

By keeping our model general, we have necessarily assumed several variables as being exogenous and we have focused on a simplified production network. We have shown that the convergence towards the symbiotic steady state does not depend on any assumptions regarding the relative strength of the different forces described in the previous section. Thus, even though our results are quite general regarding the convergence to the symbiotic state, our framework can be extended in different directions, which could on the one hand allow for a more detailed exploration of the dynamics of the model while on the other help explain other phenomena. Below we identify four possible directions of future research, each of which relaxes at least one of our current assumptions and creates the possibility of disequilibrating dynamics.

Space

In our model, space plays a key role in having heterogeneous producer firms. The spatial dispersion of production affects both the level of the symbiotic state and the dynamics towards this. This component of our model (at least partially) fills the lacuna identified by David Harvey regarding the state of modern (macro)economics: ‘macroeconomists, even those with interests in development, have a weak grasp of how to handle the production of space in their theories and models’ (Harvey, 2001: 23). In the present paper we have assumed our main spatial variable γ to be exogenous. However, as we know from Harvey’s (2001, 2006) notion of the ‘spatial fix’, the geographic dispersion of production changes over time due to capitalism’s attempt to ‘fix’ its inner crisis tendencies by geographic expansion or restructuring. Hence, a natural extension of our model would be to endogenize γ by making it contingent on the profitability of the buyer firm(s). This will on one hand provide an explicit spatial structure to our model, while on the other it introduces a force that can make the variables move away from the symbiotic steady state.

Technological change and labour bargaining

Technological change and labour bargaining are both implicit in our framework, and their effects are captured by the exogenous variables δ and ci respectively. Participating in global production can have positive effects on technological improvements and can also lower unemployment, which in turn can positively affect the bargaining power of workers. For this reason, technical change can have opposing effects on the costs of producers. The overall effect will depend on the relative strength of these two different forces, which mainly depends on the assumptions regarding (a) the influence of technical change to labour and capital productivity; (b) the substitutability between capital and labour in the production process; and (c) whether the factors of production are fully employed (Tavani and Zamparelli, 2017). Hence δ and ci could be endogenized in different ways based on assumptions 1–3. The key question that arises from this is how the different model closures will affect the symbiotic steady state and whether there will be multiple ones.

Post-Keynesian insights

As we have already mentioned, despite our model sharing the same methodological framework used in post-Keynesian (and other heterodox) models, our model is not strictly post-Keynesian. This is mainly due to our level of analysis being a value chain rather than a national economy and our focus being the power dynamics between two levels of production. Our specific focus has allowed us to abstract from several of the key insights of post-Keynesian economics, like the role of effective demand and capacity utilization. However, the role of effective demand could be used to extend our model for analysing how participation in a GVC/GPN would have different impacts depending on (a) the governance structures and (b) whether the growth regime of the country of production is profit-led or wage-led. 10

Network effects

The GVN presented here corresponds to probably the most simple network possible regarding global production. Extending our framework to more than two levels of production would necessarily lead to a more complicated network structure. In this situation, the DMP of the buyer would not only depend on the number of competing producer firms, but would also depend on the network structure itself (Mahutga, 2014). Based on this, another possible extension of our framework would be an agent-based model in which the market power of any firm is a function of its centrality in the production network.

Conclusion

GVC dynamics reflect the tensions and contradictions between producers and buyers. As Inomata argues: ‘The main objective of GVC studies is to explore the interplay between value distribution mechanisms and organization of the cross-border production consumption nexus’ (Inomata, 2017: 19). The aim of our paper has been to contribute to this objective by analysing the governance structure dynamics. We have done this by using a simplified GVC framework in which the governance structures are affected by variables used frequently in the GPN literature.

We have analysed this evolution by developing the first, to our knowledge, formal dynamic model of governance structures. Despite our model drawing on both GVC and GPN research, we do not claim that ours is a general model capturing the GVC and/or GPN frameworks in their totality. In order to highlight this point, we have named our modelling framework as GVN and we have constructed a dynamic disequilibrium model of bargaining and distribution of profits. We have introduced the degree of monopsony power as the key variable that affects bargaining, such that higher DMP leads to an increase in the share of value obtained by the producer firm. The spatial specificities of production along with changes in the distribution of value lead to consolidation and also influence DMP.

Building on Mahutga (2012, 2014), we have analysed governance structures as a continuum and related the bargaining power of buyers vis-à-vis producers to the relative position of governance in the buyer-driven/producer-driven spectrum. Our key results can be summarized as follows: (a) GVN governance will move towards an intermediate structure within the buyer-driven/producer-driven continuum, which we call the symbiotic state; (b) the relative strength of the effects on firm entrance due to the geographical concentration of production on one hand, and the decrease of the total number of firms on the other, affect the distribution of value between buyers and producers at the symbiotic state; and (c) the transition dynamics towards the symbiotic state depend on the effect of consolidation on buyers’ bargaining power and on the spatial dispersion of production.

The model used here provides a synthesis between the formal disequilibrium framework used traditionally in neo-Marxian and post-Keynesian economics, the governance structure dynamics within the GVC framework, and variables used in the GPN literature. In this way, our paper contributes towards what Barnes and Sheppard (2010) refer to as ‘engaged pluralism’ in Anglophone economic geography. It also contributes to the ongoing line of research that creates links between formal radical political economy and economic geography (Milberg and Winkler, 2013; Stockhammer, 2017; Stockhammer et al., 2016). The dynamic nature of our framework highlights the importance of studying the evolution of governance structures and shares some common features with the evolutionary economic geography approach. Incorporating more ‘evolutionary’ characteristics into our model will further strengthen these links and is a possible direction for future work.

Footnotes

Acknowledgements

We are grateful to Liam Campling, Yannis Dafermos, Ourania Dimakou, Ben Selwyn, Adrian Smith and seminar participants at Birkbeck, Greenwich and the University of the West of England for comments and suggestions. The usual disclaimer applies.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper was written in part with the generous support of the Leverhulme Trust.