Abstract

This paper elaborates on the interactions between digital technologies and financial practices and how they contribute to the ongoing process of financialization. We focus on the circumstances of blockchain-based token offerings and their contribution to reshaping existing systems of investment in startups. We show how future clients become investors via the initial coin offering (ICO) process. The paper is based on interviews with blockchain and industry practitioners during 2018 and 2019 and focuses on an in-depth case study of a specific ICO in early 2018. We suggest a framework consisting of catalysts, cracks and voids to analyze the financialization process and to inform theories of how financialization advances through the new spaces afforded by socially constructed technologies upon which entrepreneurs capitalize. With this framework we provide a better understanding of the mechanics behind financialization, particularly the ways in which business processes, and larger social relations such as the role of investors and clients, are reimagined and reworked.

Introduction

This paper focuses on how interactions between digital technologies and financial practices contribute to the ongoing process of financialization. Theories of financialization have been used in economic geography to understand the global financial crisis (Engelen, 2008) and the spatiality of finance more generally (Pike and Pollard, 2009; Sokol, 2013). Critiqued as overstating both the current uniqueness and reach of the financial sector (Christophers, 2015) the theories nevertheless remains useful for analyzing how and where financial practices gain footholds and expand in the economy. Building on Aalbers’ (2016) definition as the “ … increasing dominance of financial actors, markets, practices, measurements and narratives”, that help bring about “structural transformation of economies”this paper grounds a moment of financialization via the experience of blockchain-based coin/token offerings in 2018 and 2019. Our research goal is to better understand how a particular moment of financialization, the creation of initial coin offerings (ICOs) and other token events unfolded, and apply this insight to the larger theory of financialization. To do this we develop a framework consisting of catalysts, cracks and voids to analyze this process and better conceptualize the mechanics or “nitty-gritty” (Christophers et al., 2017) of financialization. To illustrate our findings we present a detailed case study of how a ICO reconfigured existing financing practices and allowed a startup firm to restructure ties to its products, customers and investors. Originating in the decision to adopt the financial logics and technological affordances associated with blockchain coin/token funding, we chart the financialization of the firm’s operations.

Within our proposed framework catalysts comprise enabling forces – such as technology, ideologies and money – whose presence provides the means and inspiration to alter existing systems according to existing or new financial logics. In the case of ICOs, the relevant catalysts include the technology of blockchain and distributed ledgers, associated ideologies valorizing decentralization and the new sources of capital, e.g., Bitcoin and other cryptocurrencies. The presence of catalysts enables actors engaging with finance (entrepreneurs, technologists, investors) to create cracks in existing value chains: in this case circumventing firms as the target of investment, and instead positioning products, specific technologies or larger technological ecosystems as investment spaces. In turn, these cracks generate voids in which the practices enabled by catalysts provide space for objects, actions and structures that largely fall outside existing regulation. While these voids are temporary, there is considerable short-term opportunity for entrepreneurs and investors to profit from lack of oversight afforded by the regulatory uncertainty created. As these voids evolve from relatively ungoverned to regulated space, actors shuffle between territories for desirable (or at least codified) regulations, which can serve as examples that may influence regulatory approaches more broadly.

The paper proceeds as follows. First, we sketch out the emergence of blockchain and distributed ledger technologies including a review of the ideologies and motivations of its creators. We next outline our theoretical framework in more detail with particular attention to how our conceptualization of concepts of catalysts, cracks and voids can contribute to a more generalizable understanding of how financialization evolves alongside new technologies. The third section provides a detailed case study of the savedroid ICO from early 2018 until mid-2019 and the moments in which catalysts, cracks and voids are readily observed. The paper concludes by reviewing the insights from the case study and suggesting how our theoretical framework can help better understand the process of financialization.

From Bitcoin to token events

In less than a decade blockchain-based cryptocurrencies such as Bitcoin have achieved a combined market capitalization of more than a quarter of a trillion dollars, an amount on par with all venture capital investment worldwide in 2018 (KPMG, 2019). Much attention has been given to this astronomical rise in value as well as questions surrounding whether cryptocurrencies are “real currency” (Yermack, 2015) and its potential to “revolutionize business” (Tapscott and Tapscott, 2016). In this vein Muellerleile (2019, 19) argues “If any contemporary money form threatens to rearrange today’s financial geographies, it is cryptocurrency.” Much less well understood is how these new sources of capital contribute to the “nitty-gritty” (Christophers et al., 2017) of financialization in new, tech-based firm formation (Armington and Acs, 2002; Saxenian, 1996) and related investment (Samila & Sorenson, 2011). While not denying their volatility and speculative qualities, new capital investment and entrepreneurial practices have emerged alongside cryptocurrencies (Rhue, 2018) most notably via initial coin offerings (ICOs) and other blockchain token events such as security token offerings (STOs) and initial exchange offerings (IEOs). In addition to raising funds, these practices have restructured firms and value chains 1 according to new financial logics and narratives, i.e., financialization.

While all three types of token events are public sales designed to raise funds, there are a number of key differences. ICOs are described by Strategy& (2019: 8) as “Token based funding in its ‘raw’ form” meaning that they are run by the companies issuing the tokens and operate under relatively little regulatory oversight. Almost all token events prior to 2018 were ICOs but as concerns about malfeasance and scams (Casey et al., 2018) arose, the number of ICOs fell relative to other structures. One alternative, rarely used prior to 2019, is an initial exchange offering (IEO) run by cryptocurrency exchanges on behalf of the issuing company – thus providing some vetting – and subject to some regulations determined by the locale in which the exchange is based. Another, and much more regulated approach, are Security Token Offerings (STOs) that carry the hallmarks of traditional securities including 3rd party due diligence and legally binding investor rights. STOs became more popular in the second half of 2018 and have continued through 2019. Overall, this change-over from ICOs to IEOs and STOs represents the evolution from relatively ungoverned to regulated space.

Origin of blockchain based capital

Before analyzing the new financial practices associated with token events, it is important to understand the origin and ideologies of blockchain and cryptocurrencies. Bitcoin, the original cryptocurrency, was designed as a cyberlibertarian project that viewed digital technologies as inherently liberating forces and promoted market solutions over state involvement, characterized as fundamentally undesirable (Golumbia, 2016). As a result, the architecture design of Bitcoin was highly decentralized in order to create an alternative, global system of payments and exchange that bypassed centralized control systems and removed the need to trust financial and state institutions. This focus is readily apparent in the foundational document of Bitcoin that notes “Completely non-reversible transactions are not really possible, since financial institutions cannot avoid mediating disputes” and advocates for “cryptographic proof instead of trust” that provides the “ability to make non-reversible payments for nonreversible services” (Nakamoto, 2008:1). The resulting blockchain technology used by Bitcoin (and later cryptocurrencies) is built around a distributed database (the actual blockchain), a network of miners or validators governing the addition of new records and cryptographic proofs (see Zook and Blankenship, 2018 for a fuller review). Combined, these technical elements of blockchain create a decentralized system of record keeping that tracks the ownership and exchange of digital items, e.g., cryptocurrencies or coins/tokens from ICOs, based on an ideology that values decentralization and lack of human oversight.

While the Bitcoin project has fallen short of its grand goal of serving as a global medium of exchange (Zook and Blankenship, 2018), blockchain cryptocurrencies have succeeded in creating an enormous store of value. From a market capitalization value of zero in 2009, Bitcoin was valued at over US$300 Billion in December 2017 before dropping to US$125 Billion in mid-2018 and rebounding to US$175 Billion in mid-2019. Similar growth patterns are evident for other “established” cryptocurrencies that have a fair degree of liquidity (Figure 1). Importantly, for the development of ICOs, these newly minted Bitcoin millionaires were motivated to reinvest into projects related to the larger blockchain ecosystem. As one investor reflecting on ICOs noted, “People were chasing the blockchain dream. You didn’t see that much interest in being properly informed about the actual business plan. If it was blockchain, that was good enough.”

Market Price Index for “Established” Cryptocurrencies.

Blockchain as a catalyst for ICOs and other token events

In short, the increased capital availability via cryptocurrencies acted as a catalyst for the creation of an alternative means of fundraising known as initial coin offerings (ICOs). Leveraging the decentralized security and validation offered by blockchain, ICOs also included the ability to facilitate automated interactions responding to user or software input via smart contracts and decentralized applications (Dapps) available in newer cryptocurrencies like Ethereum (Ethereum Foundation, 2017). This automated the investment process and also restructured the premise of investment further expanding financialization. That is, entrepreneurs received capital (often in the form of cryptocurrencies) not for an equity stake in their company but in exchange for a firm-issued utility coin or token that represented a voucher for a future service or product that was tradable on secondary markets (Rhue, 2018). This restructuring of firm financing represents a key moment of financialization. Since 2013 there have been over 2,000 token events raising an estimated US$30 billion (Strategy&, 2019). The amounts raised by each ICO can be extremely significant, the largest raising billions of US dollars and with many others raising hundreds of millions (Figure 2).

Largest Token Events since 2016.

Functions and the rights attached to coins/tokens vary but three main categories (Strategy&, 2019) can be distinguished: First, coins can function as fungible cryptocurrencies (similar to Bitcoin, Ether, Litecoin and others) intended to be used for facilitating transactions or as a store of value. This was the original intent of blockchain cryptocurrencies (Nakamoto, 2008) and in theory most if not all of the coins resulting from token events could be used in this manner. Second, coins resulting from an ICO or IEO can act as a “utility token”; these resemble a voucher that is bought first and could be used to buy products of the voucher-issuer later. Usually the proceeds of the sale are specifically targeted for creating the product in the first place, although prototypes may exist. The third main category are known as “security tokens” and share many characteristics with more traditional securities, e.g., paying dividends. When these kinds of tokens are used in a sale it is called a Security Token Offering (STO) and is closer to more classic securities including some regulatory oversight. Given the short and dynamic history of ICOs and STOs there remains a high level of variation in how entrepreneurs structure their coins and introduce financialization logics into their business plans, products and relationship with customers. All sorts of combinations are possible, each which opens different kinds of cracks in existing value chains creating new regulatory voids that can be exploited. Well-established and tradeable cryptocurrencies like Bitcoin and Ether were larger sources of investment than “fiat currencies” such as US Dollars or Euros.

In early 2018, the number of token events (primarily ICOs) skyrocketed (Figure 3), driven in part by the popularity of ERC-20 tokens on the Ethereum cryptocurrency system that standardized interactions and functions such as providing a token for service in exchange for payment (Ethereum Foundation, 2018). This allowed entrepreneurs to easily create their own coins, based on providing utility tokens that could be readily purchased from the company and traded between holders on exchanges, opening the possibility for Bitcoin-like wealth. This innovation made investing (and tracking investments) easier and more importantly opened cracks in the space of investment; in effect separating the investment in the technology or larger ecosystem from the investment in the company. From the entrepreneurial perspective this had the dual advantage of retaining control and using the void opened by the cracks to side-step regulations designed for publicly traded companies but not well equipped to deal with these new kinds of investments. From the investors’ perspective these cracks and voids allowed them to back products in which they believed (akin to crowdfunding pursued by artists and nonprofits seeking to raise money for projects) as well as speculating on coins/tokens that could be tradeable on exchanges and might echo the meteoric rise of Bitcoin.

Monthly Volume (US$Millions) of Token Events Worldwide.

The sharp decline in investment volume in token events during the second half of 2018 was often referenced by interviewees as “crypto winter” (see also Strategy&, 2019). Tied to over-exuberant investments in ICOs during the previous 12 months as well as dropping exchange value of cryptocurrencies (Figure 1) this period also saw a shift in the nature of token events. ICOs with some kind of utilizable functionality accounted for 99 percent of the volume in the first half of 2018, but dropped to 50 percent for the last six months of available data ending May 2019 (Strategy&, 2019). A combination of security token offerings (STOs), using the new technical standard ERC 1400 (allowing fractional ownership and restricted use of tokens), and Initial Exchange Offerings (IEO) grew in popularity and volume during this time.

In summation, token events represent a dynamic moment in financialization centered around a decidedly novel approach to financing startups that is in between equity offerings such as initial public offerings (IPOs), venture capital, debt financing and voucher sales. Catalyzed by the new source of capital coming from cryptocurrencies, entrepreneurs used token events to restructure existing value chains and traditional categories of investor and consumer to alter how players could engage, e.g., investing directly into a new technology or technological ecosystem rather than a company. The resulting cracks opened up voids of yet to be regulated space in which entrepreneurs eagerly sought profit and tried to provide proof of concept that the dream of decentralized finance was achievable. Not surprisingly, decentralized and unregulated fund-raising brought a number of serious issues (Casey et al., 2018); the shift from ICOs as the primary model for token events to IEOs and STOs during 2019 represent the movement of regulatory practices to occupy the newly created voids.

Methodological overview

In order to analyze the processes and practices behind the creation of ICOs and other token events unfolded we conducted thirty-two formal interviews with entrepreneurs, cryptocurrency investors, analysts and regular venture capital investors in Berlin and Frankfurt, Germany during 2018 and 2019. Frankfurt and Berlin were selected as field sites as they are both locations of significant blockchain firm activity including many ICO and other token events (Cohen, 2018; Chain.de, 2019). As with any human activity (Massey, 2005) the spaces of ICOs extend beyond these physical sites including, but not limited to: networks of remotely located developers (Garcia et al., 2014), hospitable regulatory regimes and incoming flows of cryptocurrency capital. Unfortunately, it is extremely difficult to measure the assemblage of ICO activity across space due to lack of comprehensive data sets, quickly evolving practices and a source of capital designed specifically to confound tracking.

To address these challenges, we adopted a case study approach as it allowed us to analyze the complexity of the new phenomenon of ICO via a rich and detailed explication grounded in the specifics of a single experience. From this anchor we identify more generalizable concepts and frameworks such as our articulation of catalysts, cracks and voids in the next section. To gather data and help identify an appropriate case study, we conducted a wide review of business and industry specific press and related documentation. This included blockchain-community documents such as online discussion boards, social media postings, industry and regulatory reports and the white papers for ICOs (roughly equivalent to a company prospectus). In addition to providing important data on ICO activities and geographies (see Figures 2 and 4), we used these documents to identify key topics – sources of capital, nature of due diligence, nature of investor rights, post ICO actions by firms, etc. – around which to structure interviews. We also identified a number of firms and ICOs that could serve as concrete examples and provide a useful focus for illustrating larger processes we identifyied. We selected savedroid AG, 2 which held an ICO in early 2018, as our case study as it exemplified a number of common trends we identified and was referenced by multiple informants.

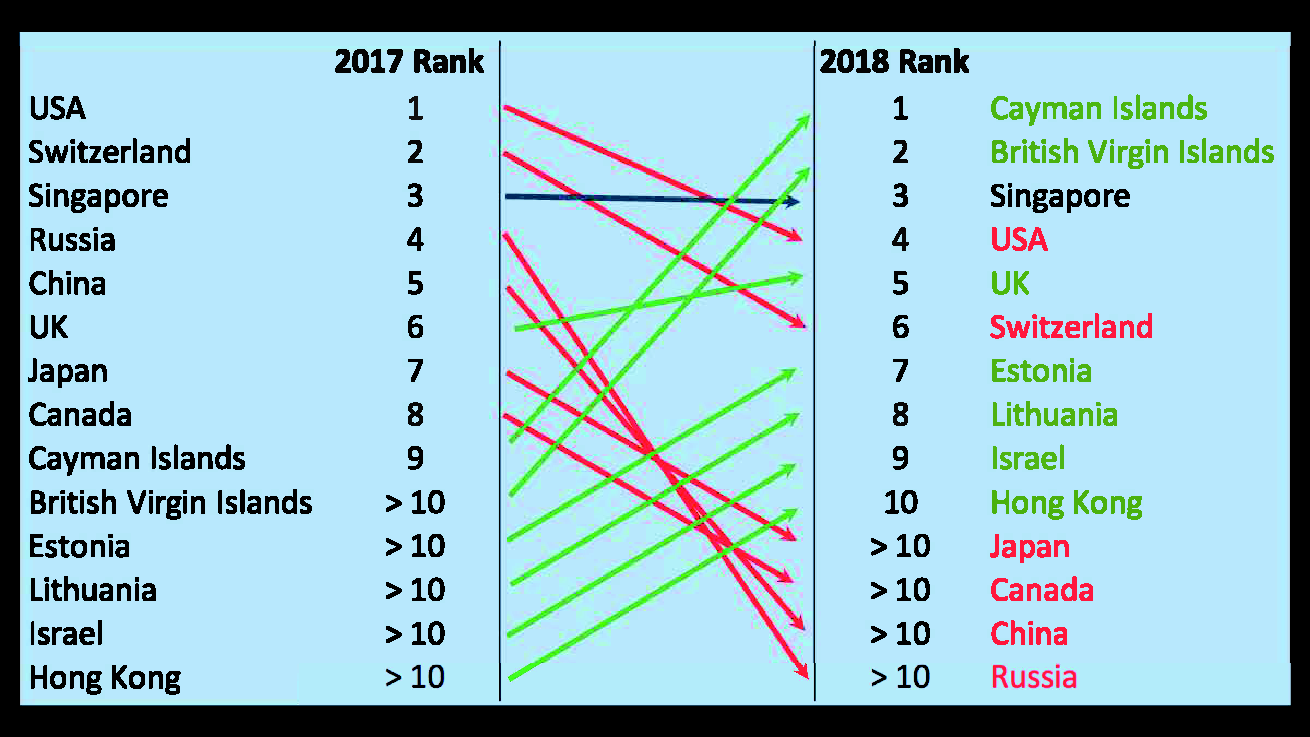

ICO Country Rankings by US$.

Interviews were divided between blockchain company founders and key personnel (60%), investors in blockchain companies (20%) and traditional venture financing and service providers (20%). Prior to each interview we gathered relevant information on each informant including a review of professional background (generally via LinkedIn), relevant white papers, news articles, about the individual’s business and investment experiences. Interviews were semi-structured and followed a set of guiding questions to ensure consistent coverage while also allowing informants to freely follow topics they deemed most relevant. Regular questions included: Why do people choose to conduct and invest in ICOs? How do entrepreneurs and investors come to agreement on valuation? By what mechanism(s) do ICO tokens/coins gain or lose value? How do ICOs differ from other types of investing? How has it affected the scale, scope and spaces at which startup financing takes place? How do investors address lack of ownership rights? How were these issues addressed in your experience? What are important regulatory and tax issues with ICOs? How have entrepreneurs and investors addressed this? How would you change it?

To meet human subject requirements all interview subjects were guaranteed anonymity. This also encouraged more candid conversations and observations from informants used to promotional rhetoric (important for fund-raising) rather than reflexivity. That said, however, we still approached interview material cautiously and with a critical eye, particularly if statements were self-aggrandizing. While this limits our ability to tie comments practices observed within specific ICOs it does allow us to achieve the more important goal of better understanding the motivations and expectations of these actors. Our interviews are supplemented by more informal conversations with people at cryptocurrency/ICO conferences within Europe as well as meetups for the blockchain startup community 3 in Berlin between 2017 and 2019. These interactions, approximately 50 in total, were not recorded but notes of key ideas and attitudes were written down immediately following each event. Interview subjects were identified through online listings of companies and investors, our own personal networks and snowballing techniques. Interviews lasted approximately an hour and were face-to-face except for six conducted via phone or video call at the request of the interviewees. The data and quotes presented here are based on our notes and transcripts (we requested and were granted permission to record all interviews). Contacted individuals were eager to talk and readily made time in their schedules.

Theorizing the spaces of financialization and blockchain technologies

Financialization can be situated across multiple dimensions including: the influence of financial markets and finance sector on national political decisions and firms’ strategies; changes within financial institutions themselves (see French et al., 2011; Hall, 2012; Lai and Daniels, 2017; van Loon, 2017), and, lastly, the increasing prevalence of monetary and financial considerations that changes the behaviours of individuals and families (Martin, 2002; Van der Zwan, 2014). The first two expositions largely focus on redistributive processes, i.e., from the state to private owners or from labor to investors, and the latter focuses more on the cultural process through which individuals are reimagined as investors. This shift to citizen-investors emphasizes “individual responsibility alongside risk-taking” (van der Zwan, 2014: 103) and often focuses on changing social practices within firms’ and individuals’ economic behavior (Hall, 2012; Lai, 2017). Thus, financialization considers both the specific details around organizational and process changes but also the cultures, spaces and political ideologies from which ideas of money and finance originate (Leyshon and Thrift, 1997; Zelizer, 1997; Golumbia, 2016).

Financialization also has strong ties to the process of technological change, particularly digital communications and data handling which enable faster money circulation and lower transaction costs (see Pryke, 2017). These abilities allow for more diverse financial instruments and practices across scale and scope making technology a key enabling factor in the creation of the spaces in which financialization operates. French et al. (2011) document the growing integration between global financial markets and local/retail markets (e.g., the securitization and tranching of US mortgage) and propose a “financial ecology approach” that emphasizes the interrelatedness of finance, geography and technology. In the case of blockchain, one good example of this interrelatedness is the vast need for electricity (de Vries, 2018) which shapes the geographies of miners according to energy costs (Fairley, 2017). Likewise, while capital flows into ICOs are virtually impossible to track spatially, geography can be readily seen in the clustering in certain regulatory regimes (Figures 2 and 4).

Some critics argue that financialization has been too widely applied (Engelen, 2008, Christophers, 2015, Mader et al., 2019) or that it discounts the important role of finance pre-1971 (Muellerleile, 2019). While we are convinced that financialization delivers a useful framework for understanding the role of technology in expanding the space of investment, we are also aware of the many other ‘elephants in the room’ that are sometimes brushed aside in favor of the more ‘meta’ explanation of financialization. These include, but are not limited to: commodification, marketization, globalization, neoliberalization, privatization, digitalization and precarization (Mader et al., 2019) and represent additional and perhaps more detailed lenses through which these processes can be studied. Although we find these theoretical concepts relevant for our case study – most notably digitalization and marketization – we nevertheless use financialization as our theoretical lens and use our empirically grounded work to help clarify how financialization advances through new investment spaces.

The financialization process within token events

The focus of our study is the actual financialization process within token events, particularly ICOs, and the specific changes in the relationship between clients and investors on the one side, and firms on the other. We argue that ICOs are designed to blur the difference between clients and investors and in so doing, contribute to a further financialization of the client-firm relationship. In other words, the fairly straightforward relationship of clients buying products from vendors is complicated by the adoption of new financial logics that echo those seen within crowd-funding platforms for business such as RocketHub, Crowdfunder or FundingCircle. While these platforms generally employ traditional equity and debt structures with clearly specified payback schedules (Gray and Zhang, 2017; Langley and Leyshon, 2017) they represent financialization in organizational terms in that funds are sourced directly from retail investors rather than banks. More significantly, financialization is also evident in the ways crowd-funding restructures the value chain in terms of what constitutes the object of investment. For example, one of the most prominent platforms for crowd-funding, Kickstarter, markets itself as “an opportunity to create the universe and culture you want to see, [ … ] the technology you wish someone was building — on Kickstarter, people work together to make those things a reality” (Kickstarter, 2018). In this formulation, future clients become sort of venture capitalists, often with an emotional connection to the firm, enabling the development of products that they are waiting for. This is exemplified by the fact that almost all of the top-funded projects at Kickstarter are (video) games and personal gadgets (Stimmel, 2020).

In the case of ICOs, this future client-venture capitalist duality is also emphasized, albeit with neither the rights of actual shareholders nor necessarily a strong connection to the firm or product in question. Most significantly, the ability to trade voucher-style utility tokens on cryptocurrency exchanges (often before a product or service is available) represents a further financialization of the value chain as it alters the relationship between clients and firms. In short, the value of vouchers is not based simply on the value of a future product or service but market expectations of customer demand and uptake. This deepens the financialization evidenced in the case of Kickstarter as client-venture capitalists anticipate access to trading on the secondary market that comes pre-equipped with many ICOs. The possibility to trade the token (or voucher) - the financial connection to the firm in question - on an exchange shifts the focus from the product itself to the monetary value of the token. This is very similar to the position of a shareholder who is mostly interested in the value of the shares as opposed to the products the firm is selling. Importantly, the ability for ICOs to participate in secondary markets is predicated on the specific technology of ERC-20 tokens allowing vouchers to function as readily tradable blockchain-based financial instruments.

It is important to understand that these vouchers are not merely a disguised form of an investment channel. Precisely because many blockchain-based businesses are based on platform-type business models, building the client base in the ecosystem around start-ups is critical for success. More users make the platform more attractive for further users - a currency that is of very limited use is also of very limited attractiveness to users, and vice versa. Securing a number of users even before the product is tested is a major improvement for start-ups and emblematic of the most successful blockchain endeavors such as Ethereum. In short, this marks the financialization of the relationship between future clients and the firms.

The catalysts, cracks and voids of ICOs

With this grounding in a particular moment in financialization, we abstract from our case study to conceptualize how entrepreneurs blended new technology and finance to create novel financial spaces as they fund-raise for their projects. To do this we develop a more generalized understanding of how digital technology is used to create new financial spaces and highlight the role of what we call catalysts, cracks and voids through which the capabilities of new technologies, ideologies and capital are leveraged by entrepreneurs.

In our approach catalysts are the enabling forces – blockchain, cyberlibertarianism and new cryptocurrency wealth for our case study – that provide the means and inspiration for an expansion of financialization within an industry or practice. While the cyberlibertarianism ideologies behind blockchain are not new, e.g., the desire for decentralized and encrypted transactions date back at least to the Cypherpunks of the early 1990s (May, 1992), their association with early Bitcoin activity are an apt demonstration of the “power of ideas and imaginaries” to catalyze action, in this case attempts to decentralize finance via ICOs (Christophers et al., 2017: 27). Or, in the words of a Berlin-based entrepreneur/investor, “Decentralization is deep in genetics of the internet, it was the original vision that individuals should control their own data without trusting another party.”

This idea of decentralization is strongly steeped in cyberlibertarian and anti-corporatist ideologies (Golumbia, 2016; Swartz, 2018) and inspired some entrepreneurs to work in particularly political ways. As one company founder in Berlin described his goals for an ICO during 2018, “Everywhere I looked I saw problems with security and privacy, centralized systems can be censored so easily. Algorithms can be manipulated … My enemy was Facebook. I wanted to fight Facebook. … It was a pure ideological movement.” Ideologies alone, however, is only part of the story. Many entrepreneurs and firms were catalyzed by the opportunity to tap into newly created wealth from existing cryptocurrencies (Figure 1) and the demonstrated ability for ICOs to raise large amounts of money (Figure 2). As the same Facebook-fighting company founder noted with dismay, “Last year, no one was building, people were just raising money because it was so easy to find”.

Building upon these catalysts of inspiration and material resources, entrepreneurs searched for opportunities to open what we term cracks in existing value chains. The cracks could be thought of as a continuation of the forceful “money flows like mercury” metaphor introduced by Gordon Clark (2005) - but instead of money flowing to where it can, in our concept entrepreneurs actively crack existing value chains in order to create new space for money to flow into. The creation of initial coin offerings (ICOs) shifted the locus of investment from the firm – with its board, funding, and governance mechanisms in place – to the technology, project or larger blockchain community directly. Within these cracks it was possible to advance the ideological agenda of decentralization by building attractive places for Bitcoin millionaires to invest, e.g., one blockchain developer described an ICO as “creating your own money that no one can track … [that] … grabs the attention of Bitwalla [a cryptocurrency exchange].”

This has a number of consequences, most importantly that entrepreneurs now have an alternative funding source, a point that overlaps nicely with the importance placed on decentralization. For example, the company in our case study argues that wider participation, i.e., including small scale retail investors, is a key feature of their ICO. “By launching an Initial Token Sale … we would like to give the crypto community the amazing opportunity to participate in savedroid’s success story, instead of limiting access to a small number of traditional venture capital funds.” (savedroid, 2017). While the expansion effect is undoubtedly true, it also means that funding will come from much less sophisticated investors with limited experience in evaluating risk and likely fewer resources to absorb a loss. For example, it is unclear how well investors understood that investing in an ICO did not entail any claims on the firm’s actions or finances.

Another useful feature of ICOs for entrepreneurs is the ability to sell utility tokens that are exchangeable for future services or products. This both raises money but also potentially builds “buy-in” and creates community (or “a project’s ecosystem”, in crypto-speak) around a technology. This previously rare financial practice was a standard option of ICOs during 2017 and 2018. As described by a Berlin based entrepreneur this means that “… you build the community from the start, so the people participating in your sale are hopefully … the first users of your product. It is about building your community. It’s putting everybody in your ecosystem and so they can stay up with the things that are going on in all of your progress and milestones.” Moreover, the fact that ICO tokens are tradable means that startups (and their investors) have a strong incentive to list them on cryptocurrency exchanges. When an ICO is listed, company founders (who generally control the bulk of the tokens), can also gain financially if the exchange value of coins increases. Since most utility tokens from ICOs were vouchers for the future delivery of a product or service, represents a new kind of financialization in which the relationship between clients and firms becomes tradeable.

The flow of capital through these cracks, however, depends upon the regulatory voids that temporarily appear as products and financing are designed to skirt existing regulatory regimes. As Dörry (2017, 427) notes, this is fairly typical for financial innovations: “New financial subsystems have created financial spaces largely outside regulation and surveillance.” By defining ICO tokens as vouchers for future goods or services – rather than a form of equity in a company – founders sought to avoid oversight by existing state regulators such as Bafin in Germany or the SEC in the US. Pursuing voids often goes hand in hand with shifting geographies as regulators come to grips with new practices. This point is aptly made in a statement released by the company Telegram (the second largest ICO to date, see Figure 2). “The Telegram team had to leave Russia due to local IT regulations and has tried a number of locations as its base, including Berlin, London and Singapore. We’re currently happy with Dubai, although are ready to relocate again if local regulations change” (Telegram, 2018). Industry reports document the often-unexpected locales (Figures 2 and 4) where ICO activity takes place (Strategy&, 2018). For example, during the first half of 2018, there was a marked shift of ICOs from countries discussing or implementing more regulatory oversight, such as the US and China, to locations such as the Cayman Islands and Estonia.

While the light regulatory regimes of offshore finance are a pull, our interview subjects argued that these location choices were not simply about lack of regulation but tied to the kinds of regulation in place. As one entrepreneur noted. “It is harder to use crypto because there are no regulations so far. We need some kind of official statements from the countries, what the rules are. Currently you don’t know what the rules are. And you see what’s happening in the US with some people going to jail because they made a decision and were told that this was OK. And then a different decision was made. We need clear rules.” The founders of two other companies (registered in Gibraltar and Malta for their ICOs) emphasized the same point, noting that the ability to get a “no action letter from the regulator” or “meet directly with the Finance Minister” were key factors in their decisions. In short, as states and central banks come to terms on how to treat cryptocurrencies, e.g., are they assets, securities or something else, firms are using differences between country-level policies to structure the organization of their ICOs. However, the voids initially resulting from cracks in the value chain are filling with regulation. As one investor notes, “It is going from the wild west to a more normal world.” This is evident in the evolution of token events from the largely unsupervised ICOs to more vetted and regulated forms of investments like IEOs and STOs.

Our proposed framework of catalysts, cracks and voids is not limited to ICOs but can also usefully be applied to other technology-driven financialization phenomena. For example, the case of high frequency trading (HFT) – now dominating activities at stock exchanges worldwide – was catalyzed by a decidedly market-oriented ideology seeking to do away with quasi-monopolist exchanges, and the technology of ever faster transfer of information and automated trading software. High-frequency trading firms worked to create cracks in current systems by installing computers at the closest spot to the matching engine of exchanges, setting up new information transmission infrastructure (such as cables and microwave-towers) between exchanges, all in an effort to obtain information a tiny bit before anyone else (see Zook and Grote, 2017). This made “public” information about trades and prices temporarily – on the order of several microseconds – private and enabled some traders new ways and spaces for profit. These cracks in the value chain of stock trading have been an unregulated area, i.e., void, for many years, and still the regulation is considered very light.

We also recognize the limits of these concepts. It might be that not all steps – catalyst, cracks and voids – are necessary for technology to induce further financialization and the form of catalysts is likely broader, e.g. including cultural and other drivers. And of course, catalysts can be present, as well as entrepreneurial action, without any development of new, or unregulated, business opportunities. Also, of interest are how feedback-effects between the technology of finance and ideology are structured. While correlation is relatively easy to identify, the direction of causality is much harder to establish.

In summation, we argue that financialization theory can be usefully strengthened by better understanding how new technologies are used to change existing financial practice through our conceptual framework focused on catalysts, cracks and voids. In the case study that follows, we highlight how the catalysts of capital availability and the new technology of blockchain, incentivized a firm with an existing product and VC funding to reorient towards creating a crack in its value chain. By creating a crack via a new product/technology that itself could be funded, “savedroid AG” took advantage of the resulting void and instituted a governance structure with little to no oversight governance from investors. As time post-ICO extends the managers of savedroid are steadily shifting to regulatory spaces that can further safeguard and secure their financial gains.

Tracking an actual existing ICO

Many financialization studies have focused on macro-phenomena such as the increased significance of capital markets for firms and individuals. In contrast, and in response to Christophers et al. (2017: 27) call for “engagement with the nitty‐gritty of how, in practice, they [money and finance] ‘work’” we take a decidedly micro-perspective in our case study of a specific Frankfurt-based ICO in 2018. Case studies can deliver deep insights into a specific firm or a specific event that larger-scale studies cannot, and uncover the generalizable micro-level formations taking place. Here, we deliver a perspective that analyzes how a new moment of financialization works “in vivo” in the design, organization and conduct of a single ICO.

Introducing savedroid

The German fintech start-up savedroid AG was founded in September 2015 by three entrepreneurs and as of mid-2018 had about 15 employees. Two of the founders were former McKinsey consultants and the savedroid’s CEO was the co-founder of another fintech company previously. Different from many companies pursuing an ICO, savedroid had an existing product, namely a savings-app based on Euros, and existing venture financing. The app allows for setting individual if-then-rules (so-called “smooves” in savedroid-speak) that trigger micro-payments from the owner’s bank account to a savedroid-run savings account. Savedroid claims to use “emotional gamification”, based on machine learning and artificial intelligence, to trigger savings: Pre-configured rules include saving whenever the user enters a certain bar, or whenever Donald Trump tweets, etc. These services are free; savedroid’s strategy for revenue was based on analyzing a user’s bank account and suggesting ways to save money, e.g., choosing a cheaper mobile phone contract, and receiving a payment from the new vendor as a “finder’s fee”. Although there are no figures out on the actual usage of the app it has been downloaded about 200,000 times making savedroid one of the better known fintech-start-ups in Germany. In addition to the founders’ own money, savedroid secured one million Euro “seed” financing in the summer of 2016 from a public business development bank (“Investitions- und Strukturbank Rheinland-Pfalz”) and several business angels (VC-Magazin, 2016). A similar round of venture capitalists invested again in 2017, and another round of €1.5 million in early 2018 (Penn 2018) resulted in a total estimated amount of about €3.5 million between 2016 and 2018 (Ksienrzyk, 2018).

Shifting from traditional to ICO financing

From this foundation, the founders of savedroid began to explore the possibility of an ICO in 2017. Although we are unable to categorically name the catalyst for this decision, this period coincides with sky-rocketing values of cryptocurrencies as well as many successful ICOs. According to savedroid’s whitepaper, the main reason for the ICO was to develop an app similar to its original one but focused on savings within cryptocurrencies. The app was aimed at non-specialists - or, in savedroid’s words they sought to enable, “crypto saving and investing for the masses” (savedroid, 2017). In its ICO, savedroid managed to secure an estimated €35 million Euros between January and March 2018, about ten times the VC investment it received, making it one of the largest German ICOs to date. A key outcome of the ICO was the creation of savedroid’s own currency (acronym “SVD”) that users would use to buy services from savedroid (primarily envisioned as this savings app) in the future. In this way, the savedroid crypto savings app took advantage of the crack afforded by ICOs to rework the company’s value chain and contrasted sharply with its original Euro-based savings app which was free for users. Moreover, the crypto-app and its service did not exist at the time of the ICO.

Although commonly referred to as an initial coin offering, technically, savedroid was issuing a “token”, not a “coin”. “Coins” and “tokens” are both considered types of cryptocurrencies; sloppy usage and some grey areas makes the distinction between them less sharp than it could be. Coins are the digital equivalent of money; usually running on their own blockchain, and with the ability to mint their own coins. Tokens run mostly on other blockchains like Ethereum and are best thought of as digital assets. They might be used as a method of payment for the firm’s products or ecosystem, but not as a general means of payment or exchange (although many firms and investors are hoping for this outcome). In general, tokens are easier to create than coins; as the ERC20 standard on Ethereum significantly simplifies the process. Therefore, the savedroid event was actually an “Initial Token Sale; ITS” and this is the terminology used in the whitepaper (savedroid, 2017).

In contrast to Initial Public Offerings (IPOs) where share price is negotiated between investment banks and buyers, ICOs in 2018 generally had a pre-set price. In savedroid’s case, the price for the savedroid token (“SVD”) was set at 1 Euro = 100 SVD with prices in other currencies (US dollars, Bitcoin, Ethereum, etc.) relative to their value to the Euro. Savedroid planned to issue up to 10 billion SVD tokens (nominal value of €100 million), of which 6 billion tokens (nominal value €60 million) have been for sale. The remaining SVD would be distributed as follows: 15 percent of SVDs to savedroid’s early equity investors and the savedroid team; 10 percent to community initiatives, business development, and expansion; 10 percent to advisors, community managers, smart contract developers and legal, and 5 percent to the bounty program for ITS [ICO] participants (savedroid, 2017). This kind of distribution schemes were a common practice in ICOs with a significant portion of the tokens held back for stakeholders who have not financially invested in the ICO project. While technically these tokens could be used to purchase firm services, in practice this was largely a means of motivating stakeholders to promote the ICO as they could make money if the token was listed on an exchange and experienced demand.

As is also common practice, the savedroid ICO was structured as a two-stage process, a “pre-sale” and a “main sale”. During the pre-sale, running from January 12th to 26th, 2018, up to 5 percent of all SVD, i.e. up to 500 million SVD (nominal value of €5 million) were sold. 4 During this pre-sale, discounts or bonuses were offered to encourage participation. In savedroid’s case, every investor got an additional 30 percent of the ordered SVDs for free (i.e. 1,300 instead of 1,000). The main sale took place from February 9th to March 9th, 2018, with up to 5.5 billion SVD for sale. The main sale also stipulated a lower threshold, unless a minimum of 50 million SVDs were purchased, the entire ICO would be void and money would be returned to investors. The ICO set the minimum buy-in at 1,000 SVD (or €10) and the maximum purchase “of 10 million SVDs ([i.e., a nominal value of €100,000] per ITS participant for purchase in the savedroid ITS” are allowed (savedroid, 2017: 40)

Results of the savedroid ICO

In the two sales’ rounds, a total of 4.2 billion SVD were sold, roughly 70 percent of the maximum number of tokens available for sale (savedroid, 2018). The remaining unsold tokens were “burnt”, i.e. they were made unusable, as stipulated in the whitepaper. The tokens designated for distribution to other stakeholders were also reduced by about 30 percent, resulting in a total of 6,997,578,543 SVD. This practice of burning coins is fairly common within ICOs and is used to signal commitment to the long-term project of an ICO as well as reducing the supply of coins (thereby theoretically increasing the price). Press statements at the time of the ICO indicated about €40 million in proceedings, or about USD 50 million. Our own more conservative estimate (taking into account likely discount rates for large buyers) places the amount raised by savedroid at approximately €35 million. Figures are somewhat blurry, as the regulatory void in which the ICO was held means that no official statement from the company about this number is required. An exact amount is further complicated by investments in Bitcoin or Ether: any change in the Euro-value in these currencies after the initial purchase changes the overall ICO’s valuation in Euros.

According to our interviews, there were about 35,000 participants in the ICO, with an average investment of about €1,000 with the largest investment of €3.5 million coming from a consortium of investors. Large investments, values of €50,000 and more, were mostly made using Bitcoin and Ethereum; accordingly, the large investors were almost exclusively the so-called “bitcoin millionaires”. These long-term bitcoin holders benefitted from the strong increase in bitcoin value over the last years and acted as catalysts for ICOs. Large investors also got a bonus (discount), the amount of which has not been disclosed, and which might not be uniform. It is probably fair to assume that this discount would be at least in the order of magnitude that pre-sale participants received. This demonstrates the flexibility offered by voids as this is very different to an IPO in which companies are legally obligated to treat all shareholders equally. According to an Etherscan, a search on the Ethereum blockchain for transactions, performed by a journalist on June 19, 2018, about 2.15 Billion SVD were allocated to only 19 buyers (technically defined as cryptocurrency wallet address) with three buyers receiving 500 million SVD, twelve buyers receiving 50 million SVD, and four getting between 16 million and 19 million SVD. Combined these large buyers represent about 50 percent of all SVD sold (Dohms, 2018). A general feature of this ICO - and, according to our interviews, many others - is the small amount of due diligence that investors pursued before investing. Our interview informants confirmed that it would not be unusual for an investor of €50,000 and more to decide “I like this project and will invest” based on a casual read of a company’s whitepaper accompanied (but not always) by a short Skype interview with the CEO. In short, the crack that ICOs created in value chains created a void of yet to be regulated space in which opportunistic fund-raising could flourish.

Analyzing product development

Savedroid was blunt 5 with regard to the usage of SVD in the immediate future: “At the beginning, the tokens will not have any features. The use as a means of payment for crypto services on the savedroid ecosystem will only be possible after the launch of such features according to the roadmap below. The dates of the roadmap depend on external factors such a partner set-up or regulation and can thus not be guaranteed.” (savedroid, 2017: 40). Moreover, during the time of the ICO, savedroid made almost no announcements about its original app (Penke, 2018). In short, savedroid severely limited the use cases for SVD and provided no real timeline against which an investor could measure good progress.

And progress has been slow, especially given the sizable financial resources at the firm’s disposal after the ICO. The first beta-version of savedroid’s cryptocurrency savings app came out in August 2018 and was distributed to only a few users. Only in mid-September 2018 did the firm start ramping up its hiring activity by posting positions (including some fairly senior ones, Performance Marketing Manager, CMO - Chief Marketing Officer and Senior Mobile Developer) on its Facebook account. Given that the entire premise of the ICO was financing the development of the new app, this lackadaisical timeline is surprising, as is the entire savedroid’s team taking a holiday trip to Thailand in May 2018, not to mention the firm’s relocation to posh new offices in October 2018 (Penke, 2018). The new app for saving in crypto currencies was finally publicly released at the end of February 2019 and as of August 2019 there have been some minor updates, mostly bug fixes, but very few positive reviews submitted by users to the IOS and Google app stores. The tweets and Facebook entries posted by the company are now mostly about generic topics and parties. In short, this behavior is consistent with Jensen’s (1986) argument about the “agency costs of free cash flow” when managers’ and investors’ interests are not aligned. This means that the SVD tokens designed only for paying for the services on the app have no ready outlet for use, even after being listed on exchanges.

Investors’ and company motives

This leads to the serious question of why anyone would buy a token/voucher for a future service of an unknown quality from a high-risk start-up in the first place? We posed this question repeatedly in interviews and generated some of the longest discussions with many people making a comparison to the crowd-source funding platform Kickstarter. Our interview subjects stated that building the crypto-community (or ecosystem) is an important part of the agenda of many “bitcoin millionaires” working to catalyze the blockchain space both for ideological reasons (promote the goals of decentralized finance) and profit. This was also evident in the specific case of savedroid’s ICO, as some of the larger investors advised the company on problems, answered questions in online community fora, and otherwise worked to promote the company.

Remarkably, we could find very little evidence that investors had any interest in the actual future services of savedroid, the only actual use of the SVD tokens offered in the ICO. The details or timeline of the cryptocurrency savings app were of relatively minor interest compared to questions of when the SVD token would be listed on cryptocurrency exchanges, and on which. This strongly supports the interpretation that pure speculation in the future appreciation of the SVD token – enabled by the regulatory void around ICOs – was the major motivation for investors. Indeed, our interview subjects argued that many large investors in ICOs - investing almost exclusively via Bitcoin or Ethereum - are primarily seeking to diversify their larger cryptocurrency. These investors were investing in many ICOs in order not to miss the next Bitcoin and to hedge against a downfall in their holdings of more established cryptocurrencies. Indeed, savedroid stated that there was a strong correlation between interest in the savedroid ICO and the price for Bitcoin: on days when the price of Bitcoin in Euro went up there were more larger investments in the ICO than on days when the price of Bitcoins went down.

The regulatory void around ICOs has also been useful for the savedroid company. The regulation in place in Germany regarding ICOs primarily focuses on controlling outright fraud and stipulating varying degrees of know-your-customers (or in this case know your investor) information and otherwise delivers few protections to investors. Locales with more laissez-faire traditions than Germany (Figure 4) have even less robust standards. Savedroid has its headquarters in Frankfurt and a branch in nearby Mainz, the latter to tap into special funding opportunities for start-ups there, and two subsidiaries in Liechtenstein (since 2018) and Luxembourg (since 2019), respectively (Lhoft.Com, 2019). The Liechtenstein office is responsible for the crypto-app and the “savedroid.com” website and the Luxembourg office has been set up to apply for a payment institution license (savedroid job offer; indeed.com 2019). This regulatory arbitrage, common in the finance sector, becomes relevant for blockchain start-ups due to the “catching-up” of regulation in the crypto-sphere, with regulators eager to fill the void again.

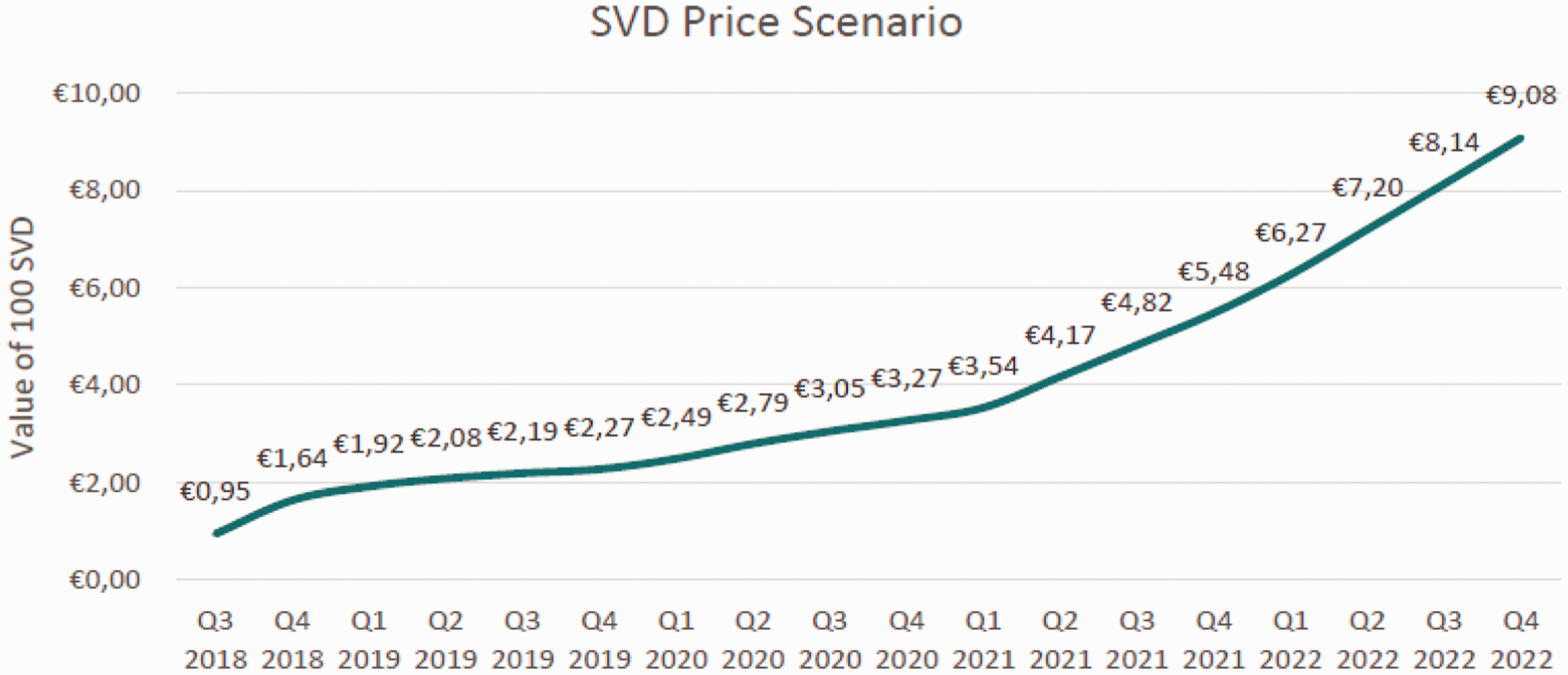

It is also clear that ICO firms catered to investors’ expectations of fast, very high returns. Figure 5 shows a graph from the savedroid white paper titled “SVD Price Scenario”. According to this chart, 100 SVDs would increase in value from €0.95 in the third quarter 2018 (a slight initial drop after the ICO) to more than €9 in the fourth quarter 2022 - an almost 10-fold increase within four years. This kind of extremely optimistic, forward looking statement without corresponding statements of risk would not exist in the prospectus for a regulated investment. Granted, the savedroid whitepaper lists this as a “possible outcome”, but it is the only one on display in the paper and there is little explanation about how this price increase will come about beyond stating that SVD tokens will be burnt - i.e., taken out of circulation and retired, according to a pre-specified formula. The unspoken message of the graph is the tantalizing possibility of the appreciation of exchange value of the self-created token, SVD. This also points to the major difference between ICOs and Kickstarter-like investments: in an ICO, people can sell their tokens on one of the 200 to 500 organized exchanges (Cryptocoincharts, 2018; Sedgwick, 2018) for more established cryptocurrencies or even traditional fiat currencies. With speculation as the major motive for investors, the listing of the currency/token on an exchange becomes a fundamentally important part of the ICO rather than something in the distant future. Once listed on an exchange, investors would be able to sell their tokens, and new investors would be able to buy them, albeit at market-determined prices rather than ICO prices.

SVD Price Scenario.

Despite the key role of exchanges, savedroid did not specify a certain exchange for trading SVD in the ICO. Rather the whitepaper simply stated “The commencement of trading is planned a few days after the end of the ITS [Initial Token Sale] depending on the listing speed of token exchanges. SVD will be transferable on the first day of trading” (savedroid, 2017, 40). It took savedroid a few months instead of “a few days” and this delay caused considerable anger in the comments section of Facebook and other social sites, e.g., “bitcointalk”, where users repeatedly asked (often quite heatedly) about when SVD would be listed. This laser like focus, combined with relative few (if any) questions about the cryptocurrency savings app, further supports the notion that investors did not want to actually use the token, but simply to sell it. There is an ongoing concern amongst (apparent) investors on different news boards about the quality of the exchanges that so far list SVD. High-quality crypto-exchanges only list selected currencies and tokens, and charge sizeable fees, in the order of millions of Euros, to list a new currency. Savedroid’s (apparent) investors publicly asked for a top-ranked exchange that would attract more investors, thus creating more demand, higher prices and opportunities to resell SVD tokens.

However, thus far listing on an exchange has not proven a ready means of cashing-out. The SVD token dropped sharply by about 80% relative to its ICO price when it first started public trading and as of August 2019, the loss stands at about 97.5% with little volatility during the year (coinlib 2019). This serves a powerful example for Muellerleile’s claim that “[ … ] it is imperative to remember that all money is a form of social claim or debt in the sense that the holder is dependent upon others, such as their community, society, or state, to redeem its ‘face’ value for other commodities.” (Muellerleile, 2019, 8). Interestingly, there seems to be little trust in the value of SVD – or any other cryptocurrency – by the firm savedroid itself. It still calculates all its fees in Euros: “All fees stated in our fee schedule are quoted in EUR and will be charged in SVD. The exchange rate for the conversion of EUR to SVD is the average exchange rate [ … ] on the day on which the fees are due.” (savedroid 2019).

Conclusion

While the path taken by savedroid’s ICO profiled in this case study is unique, it provides a useful and grounded example of how a particular moment in financialization unfolded: The relationship between future buyers of services and the respective firms became formalized via vouchers (coins) that are afterwards traded on exchanges. Clients-investors in savedroid’s case were much more interested in trading opportunities for the vouchers than in the actual future product. The demand for a reconfigured and tradable client relationship opened up new financing strategies for startups such as savedroid. Despite having venture capital backing and an existing product with market presence, the opportunity to hold an initial coin offering motivated savedroid’s founders to radically alter their financing models, and rework their business processes and relationships to clients.

From the empirics of our case study we develop a more generalized understanding of how digital technology enables the creation of new financial spaces. This allows us to highlight the role of what we call catalysts, cracks and voids through which the capabilities of new technologies, ideologies and capital are leveraged by entrepreneurs, to expand financialization to new parts of business processes. Technology, capital availability and ideology acted as catalysts behind the company’s ICO. Without blockchain technology, most notably the ERC 20 standard, savedroid would have had to expend enormously more effort to conduct a token sale for tens of thousands of investors. In short, the technology of blockchain allows for a decentralized ledger that is able to track the ownership and exchange of digital items, e.g., cryptocurrencies or coins/tokens from ICOs, based on ideological concerns about human oversight and the valorization of algorithmic governance. If Bitcoin and other cryptocurrencies had not provided early Bitcoin adopters with wealth seemingly overnight, there would have been much less blockchain-investment-seeking-capital to pursue. And finally, without an ideology that regarded the decentralizing power of blockchain as crucial and worthy of support (Zook and Blankenship, 2018), Bitcoin millionaires would not have dogmatically invested in related startups to support expansion of the ecosystem.

Savedroid’s management (and other entrepreneurs pursuing ICOs) used these catalysts to crack the relation between (future) clients and services/products on offer. Future customers became investors, and most importantly were able to speculate on the value of the voucher issued by savedroid on exchanges. One of the most remarkable aspects of savedroid’s ICO (and ICOs more generally) is investors’ lack of control over the firm’s behavior and management decisions. While payment for the vouchers went to the firm, coins represent only a stake in the firm’s future product or technology rather than a claim on the firm itself. This is very different from venture capital backed startups, in which the investors (VCs) release cash little by little, often only after the firm reaches a particular goal – and of course acquire ownership of and control rights in these firms along with the payments. ICO investors are more similar to retail shareholders in established firms in the sense that those de facto also have no say on management decisions. But there is a formal right, to be executed in mandatory annual general meetings, and many shareholders together (or a few large shareholders) could block or force decisions. Furthermore, all shareholders have to be treated equally but there are no such rights for coin/token investors.

Due to the largely missing regulation of ICOs

We are well aware of the potential limitations of this formulation: Not all steps – catalyst, cracks and voids – might be necessary for technology to induce further financialization. Several or all elements might be present without any financialization occurring. In addition, the direction of causality between the different elements should be of interest in future research based on case studies or measures of labor and capital flows as better data on activity across space are developed. Nevertheless, we argue that the grounded insight represented by this case study analyzed via the concepts of catalysts, cracks and voids offer important illumination on how the complexities of new technologies furthering financialization via entrepreneurial action.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the National Science Foundation (Award # 1853718).