Abstract

Population aging has led to the establishment of Healthcare Real Estate Investment Trusts (HC-REITs) to boost the supply of nursing homes, but these initiatives have met with contrasting success in different countries. This paper bridges two strands of research on financialization, social welfare and the built environment, to explain the uneven geography of HC-REIT development in France, the UK and Japan. It argues that nation-specific processes of nursing home securitization are shaped by the interrelationships between three crucial factors: (i) the regime of retirement income, (ii) public policies dedicated to long-term institutional care and (iii) the power relations between the REITs and care providers themselves. Drawing on discussions with experts in these sectors, the paper demonstrates that liberal welfare states such as the UK have an especially attractive profile for Healthcare REIT investors due to the advanced state of financialized pension reforms, significant state disengagement in the provision of long-term care and REIT-friendly regulations that facilitate investment operations and leases. On the one hand, these tendencies are driving financial investors to satisfy a growing demand for retirement savings in niche markets such as Healthcare REITs. On the other hand, value extraction is being increasingly sought through the capture of care-dependent residents’ home equity. By linking social benefit provisioning to later life housing accommodation, this article casts important light on current debates on the political economy of real estate financialization, while also emphasizing the need for continued state support for long-term institutional care.

Introduction

Ageing populations are driving increased demand for long-term care. With the baby boomer generation expected to reach 80 years of age and over by 2030, there is a growing need to accelerate the development of nursing homes – i.e. facilities designed for high dependency residents who require full-time care delivered by qualified nurses. Many governments have turned to the private sector to meet this challenge, and for which financial investors have sought to gain a foothold.

In the late 2000s, several governments in Western Europe and East Asia worked to create a new type of REIT segment, known as ‘Health Care Real Estate Investment Trusts’ (hereafter HC-REITs). Originally established in the United States in the 1980s, HC-REITs are publicly traded entities that specialize in the long-term provision and management of leased properties for health care providers, including facilities used for care (nursing homes) and cure (clinics and hospitals). In the nursing home sector, it was assumed that transferring the ownership of the facilities to specialized real estate management structures through sale and leaseback arrangements would encourage providers to develop their core business services (Harrington et al., 2011); in turn, investors in HC-REITs would enjoy stable and attractive risk-adjusted returns driven by ageing demographics and long-term leases. Given the success of HC-REITs in the United States, there was little doubt that these vehicles would also thrive amid Europe and Asia's ageing population.

However, the securitization of nursing homes has fallen far short of expectations. Of the top 25 HC-REITs identified globally in 2019, only 13 were involved in long-term care, including 9 listed in the United States (GFM, 2019). Even Japan, an ageing country and a pioneer in developing the largest REIT market in Asia, has not performed well in this area. How can we explain this cross-national variation in long-term care provision? The scarce literature addressing the financialization of nursing homes from an institutional perspective sheds little light on this issue, although it does provide important insights into the restructuring of nursing home ownership in the United States and the UK (Harrington et al., 2011; Horton, 2019, 2021; Kaffenberger, 2001; Kitchener and Harrington, 2004).

This article contributes to the debate, but takes a different approach by focusing on the conditions that enable, or hinder, the securitization of long-term facilities in situated markets. To this end, it compares the patterns of HC-REIT development in three large REIT markets, where the long-term care segment has undergone significant growth (UK) and weaker development (France and Japan). In doing so, the analysis combines insight from two bodies of work on financialization that are usually considered separately: the financialization of welfare, with a focus on the welfare sectors involved in long-term institutional care and the financialization of real estate. The three case studies exemplify a diversity of welfare regimes (Esping-Andersen, 1990), with the UK representing a ‘liberal’ model, France a ‘conservative’ model, and Japan an East Asian developmental hybrid (Esping-Andersen, 1997; Lee and Ku, 2007). Considering the path-dependent nature of welfare provisioning and the variegated pattern of built environments, I argue that the securitization of nursing homes in each national context is shaped by three interrelated factors: (i) the regime of retirement income; (ii) state policies towards long-term institutional care; and (iii) the specific power relations between REITs and care providers themselves.

The remainder of the paper follows in two main parts. First, I discuss the literature on the financialization of both welfare state and real estate, which I use to develop a comparative framework to address the nexus between finance capital and long-term care facilities. In the second section, I apply this framework to explain the different trajectories of long-term care in the selected case studies.

The changing structure of nursing home ownership amid the financialization of welfare benefits and real estate markets

Financialization refers to a variety of structural changes driven by the increasing dominance of capital markets and financial actors in the operation of national and international economies (Epstein, 2005). In this paper, financialization is understood as the gradual concentration of capital in the hands of institutional investors – of which pension funds are key players (Engelen, 2003; Dixon, 2008) – who push for the maximization of shareholder value in an increasing number of sectors (Froud et al., 2002), including the transformation social services and facilities into financial assets through increased liquidity of capital (Gotham, 2006).

The financialization of welfare from solidarity-based principles to individual insurance schemes

Extensive scholarship has highlighted the proliferation of financial markets into social welfare systems. Justified as necessary to fill shortfalls in public funding (Fine, 2012), finance capital has extended its influence into public education (Eaton et al., 2016) and even early childhood social services (Tse and Warner, 2020). Therefore, it is no wonder that financialization has gained in three areas sustaining long-term welfare: pensions, healthcare and social care.

The financialization of pensions plays a crucial role in post-industrial economies because it not only affects retirement income but contributes to the increasing centrality of pension funds in global financial markets, presaging an era of ‘pension fund capitalism’ (Clark, 2000; Dixon, 2008). It is widely acknowledged by scholars that the major impetus for the financialization of pensions came in the 1990s with a general move away from public pay-as-you-go (PAYG) pension systems towards greater reliance on private funded pension schemes (Engelen, 2003). This ‘paradigm shift’ (Orenstein, 2013) was initiated by international organizations – the World Bank, the OECD and the European Union – through narratives about the inevitable fiscal crisis that a ballooning, ageing demographic in PAYG countries would cause. According to many welfare scholars, this official discourse was a useful pretext for privatizing public services (Berry, 2016; Pierson, 1996) and for developing national financial markets (Engelen, 2003; Naczyk and Palier, 2014). In turn, this massive expansion of savings capital managed by pensions funds and other retirement income institutions fuelled demand for new financial products and webs of investment intermediaries (Dixon and Sorsa, 2009).

A further impulse to the financialization of pensions has been the shift from ‘defined benefit’ (DB) to ‘defined contribution’ (DC) pension schemes. While both funding mechanisms are closely linked to capital markets, the risk and management burden historically borne by the employers in DB plans shifted to employees in DC schemes (Wainwright and Kibler, 2014). Under the latter system, individual workers are forced to behave as ‘entrepreneurial investor-subjects’ (Langley, 2006) even though many often lack the skills to understand market dynamics. Originating in the United States, DC plans have made their way into OECD countries. However, studies in European countries have found that the strong involvement of non-financial firms and trade unions in the management of occupational funds has helped to limit the influence of the financial industry (Hassel et al., 2019; Naczyk, 2016). The UK is a notable exception, with a significant shift to defined contribution schemes that have exposed workers to the vagaries of financial markets (Langley and Leaver, 2012; Natali, 2018; Van der Zwan, 2020). An unintended consequence of this development has been to discourage an increasing number of employees from joining pension schemes: with a poverty rate of 15% amongst people aged 65 years and over, the UK share is less than the US share (23%), but is well above the OECD average (3%–8%) (Geppert and Reilly, 2019).

Structural reforms promoted by the World Bank have also channelled finance capital towards the health sector in OECD countries (Hunter and Murray, 2019). Although the state still provides broad coverage of medical services in advanced economies (except in the United States, see Wendt, 2014), the principle of universal access to health care has been challenged by the encroachment of financial logics and metrics in the provision of medical services and infrastructure (Wainwright and Kibler, 2014). According to Cordilha (2021), there has been a shift from the traditional ‘private corporate sector’, composed of companies specialized in the production and trade of health services and goods, to the ‘private financial sector’, which is not health-oriented and seeks low-risk investment returns guaranteed by tax revenues. Even in France and the UK, two countries with historically some of the most comprehensive health care systems in the world, Cordilha (2021) and Bayliss (2016) have shown how the development of debt-refinancing investment vehicles for health expenditure (France) and partnerships between public and financial actors for healthcare (the UK) have undermined the core principle of solidarity-based prevention and healing. Nevertheless, this process has been more advanced in the UK as a result of the financialization of the NHS's medical services and infrastructure (Pollock, 2004).

The long-term care sector has also experienced a shift from the traditional private corporate sector to the private financial sector. Yet, unlike healthcare, where the state bears a large part of the cost for services and infrastructure, a significant co-payment for care is required from nursing home residents as well as additional accommodation costs, which reduce the potential subsidies financial investors might capture. However, as Horton (2019) and Strauss (2021) have pointed out, opportunities for rewarding investment returns in this labour-intensive sector can be offset in other ways: by exploiting the highly gendered and radicalized caregiver workforce, and even more so by maximizing rents derived from care facilities.

Welfare properties as a new frontier for investment in liquid financial assets

For financial investors, as well as real estate economists, HC-REITs are part of an alternative real estate sector where nursing homes coexist with self-storage facilities (Newell and Wen Peng, 2006). Such entities have resulted from the transformation of real estate as an asset class for institutional investment (Coakley, 1994; Van Loon and Aalbers, 2017).

At the core of the financialization agenda is the quest for liquidity, or the ease by which commodities are exchanged and traded on the market (Gotham, 2009; Theurillat et al., 2016). In property markets where commodities are spatially fixed and heterogeneous, liquidity is obtained by unbundling capital ownership rights from the underlying property assets (Corpataux and Crevoisier, 2005), thereby allowing financial investors to manage large portfolios of properties. These vehicles open up new avenues for real estate investment by combining the benefits of diversification across borders, economic sectors and property cycles (Aveline-Dubach, 2020).

Of the range of investment vehicles available in real estate, publicly traded REITs best embody the finance-real estate nexus by offering the highest degree of liquidity; investors enjoy regular dividend pay-outs provided by stable rental income streams, which serve to decrease their taxable income and reduce overall taxes paid (Newell, 2011). Because restrictive rules govern REIT activities (relating to ownership control, leverage ratios and commercial operations), REIT shares are seen as ‘defensive’ investment vehicles, which make them attractive to both institutional and individual investors. This is especially the case for HC-REITs, which are considered one of the safest ‘bond-like’ classes of traded investment vehicles as they are in a recession-proof sector with a lease structure that guarantees regular, long-term income flows to fund managers (Parker, 2018).

Access to REIT markets is provided by mutual funds managed by global financial intermediaries who have an increasing influence on public policies at different levels (Sanfelici and Halbert, 2015; Wijburg and Waldron, 2020), which is part of a wider alignment of interests between financial actors and state authorities. Indeed, the establishment of REIT channels requires significant effort by central governments – inter alia, the creation of dedicated legal and regulatory frameworks, the transparent mediation of information and standardization of performance metrics and assessments. However, the vehicles can also be efficiently used to pursue macroeconomic goals, such as deleveraging a failing banking sector (Aveline-Dubach, 2020, 2022; Waldron, 2018) or creating an environment conducive to foreign and domestic investment in a national or urban economy (Aveline-Dubach, 2017). In the context of fiscal austerity, REITs offer state authorities ready-to-use solutions to release public capital through the large-scale privatization of welfare properties. Research on the sale of social assets to REIT structures has revealed how investment managers strive to create shareholder value by optimizing property portfolios through long-term strategies including, ‘asset enhancement initiatives’, divestment of less profitable ‘non-core’ properties and the active lobbying of local governments to make planning regulations more accommodating to investor interests (Aveline-Dubach, 2017; Bernt et al., 2017). Such ‘financialized privatization’ (Aalbers, 2016) may involve equity firms or hedge funds in the initial phase, using debt-financed engineering to seek short-term high risk-adjusted returns. After a period of 4–6 years, the properties will be sold to REITs, often as part of a pre-planned exit strategy (Wijburg and Aalbers, 2017; Wijburg et al., 2018).

While the vast majority of studies on the securitization of welfare properties focus on affordable and social housing, a few authors have pointed to the emergence of financial landlords in the long-term care sector. In the United States, Harrington et al. (2011) documented how private equity firms bought the top ten nursing home chains in 2004 and then sold them to REITs in 2008. A similar trend was observed in the UK, after most public nursing homes were privatized by successive governments (Whitfield, 2012). Horton (2017: 99) estimated that in 2011, at least 20% of the UK's residents in nursing homes had come under the control of these financial structures – including a majority of domestic and US private equity firms. Horton also gave a detailed account of the unsustainable business models used by financial players, showing how they led to the collapse of two major UK care providers (Southern Cross and Four Seasons Healthcare), which jeopardized the well-being of tens of thousands of elderly residents. According to her analysis, the failure was due to both the high leverage of the care providers and the increasing rents due to the financial landlords at a time when public demand for long-term care was being reduced. In a more recent study, Horton (2021) also observed that HC-REITs have become large-scale landlords in UK nursing homes, replacing private equity firms with more sustainable, less leveraged business models that rely on residents paying higher care fees. However, she argues, the imperative to secure capital liquidity has led HC-REITs to turn nursing homes into standardized, hotel-like facilities. Hence a growing mismatch can be observed between this supply of ‘liquid homes’ and resident's illiquid demand for situated care relationships and personalized home environments.

Research design and method

This section provides a comparative framework for analysing the different dynamics by which liquid capital anchors the real estate assets of long-term care providers. Based on examples from current research, the framework focuses on three key variables:

The regime of retirement income: While most advanced countries provide universal health care coverage for the elderly, the cost of social care and accommodation in institutional long-term care is generally means tested, leaving a significant share to be paid by a large proportion of the elderly (the ‘care fees’). The financial capacity of older residents to meet these costs depends primarily on their retirement income. In low-spending welfare states, such as liberal and East Asian developmental types, older people are forced to tap into their accumulated assets – especially home equity – to fill such gaps (Ronald et al., 2017). This has strong implications for how care providers and HC-REITs develop strategies to capture value from the sector. State policies in long-term institutional care: To grow their real estate portfolios and achieve economies of scale, HC-REITs must make sale–leaseback arrangements with care providers. State policies regarding institutional long-term care largely determine the contours of this ‘investable universe’. In liberal welfare states where public/not-for-profit ownership of nursing homes tends to be residual, HC-REITs have a wide field of opportunity to make lucrative arrangements with for-profit providers. The problem, however, is that they have limited demand from relatively affluent end users. While more diverse nursing home ownership structures offer financial investors a larger market potential and a greater amount of state subsidies available for capture, HC-REITs must still find ways to maximize investment returns from their care-based assets. The power relations between REITs and the care providers: As operational structures, HC-REITs’ link to health care providers goes beyond the conventional landlord–tenant relationship. The lease terms are much longer than in other sectors and the partnerships are typically designed for an even longer duration (Figure 1). While physical property is an important factor in the investment strategy, operational considerations (capacity and reputation of the healthcare operator) are even more crucial. While REIT regulatory frameworks are expected to converge globally to create a more unified global market, differences in national regulations continue to affect the operational scope of trusts and their ability to meet tenants’ needs. The size of the trust, its financing and governance structure, as well as the asset strategies of the care providers, all have an impact on landlord–tenant relationships and the investment potential of an HC-REIT.

Organisational structure of a HC-REIT.

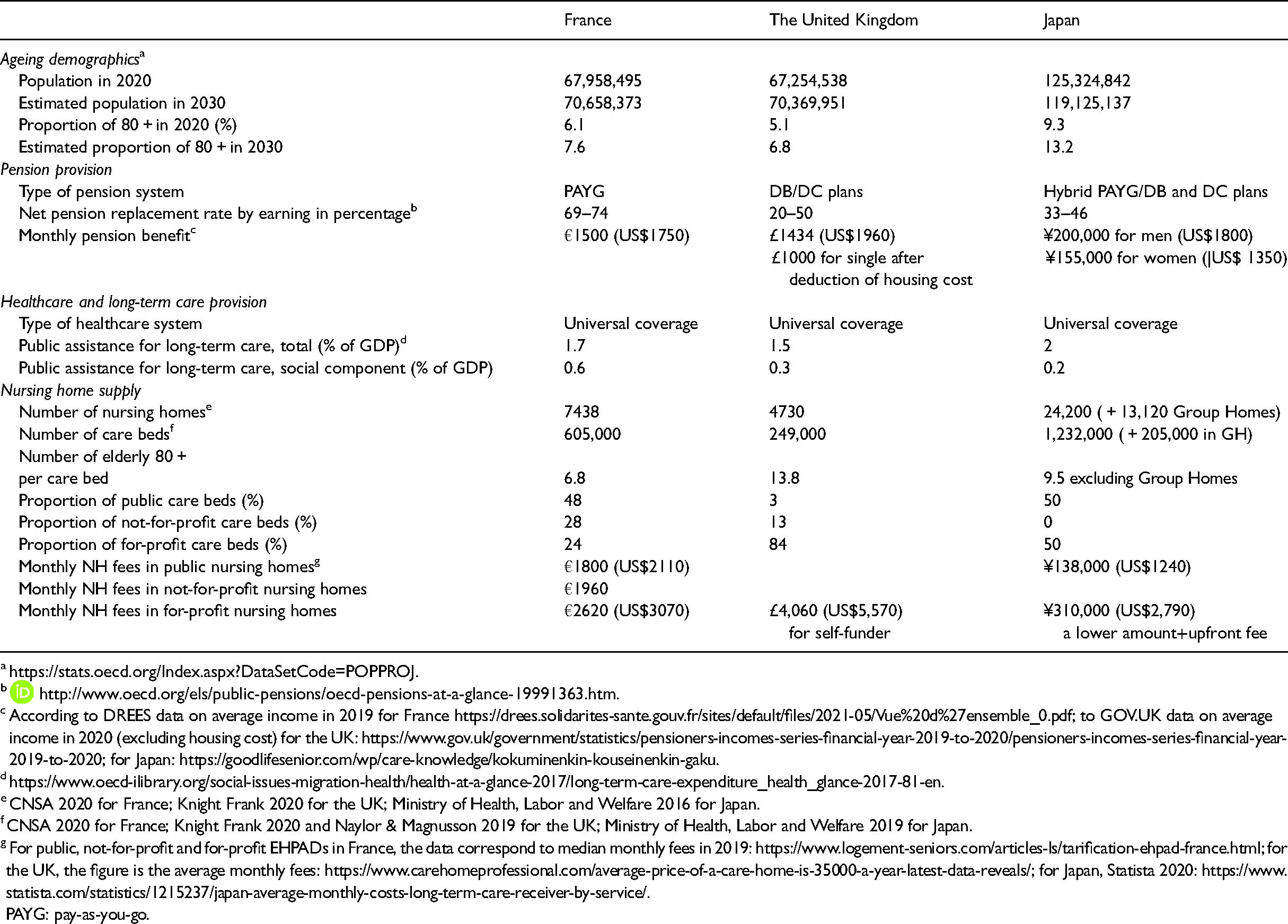

Comparative characteristics of the ageing context in the three countries.

According to DREES data on average income in 2019 for France https://drees.solidarites-sante.gouv.fr/sites/default/files/2021-05/Vue%20d%27ensemble_0.pdf; to GOV.UK data on average income in 2020 (excluding housing cost) for the UK: https://www.gov.uk/government/statistics/pensioners-incomes-series-financial-year-2019-to-2020/pensioners-incomes-series-financial-year-2019-to-2020; for Japan: https://goodlifesenior.com/wp/care-knowledge/kokuminenkin-kouseinenkin-gaku.

CNSA 2020 for France; Knight Frank 2020 for the UK; Ministry of Health, Labor and Welfare 2016 for Japan.

CNSA 2020 for France; Knight Frank 2020 and Naylor & Magnusson 2019 for the UK; Ministry of Health, Labor and Welfare 2019 for Japan.

For public, not-for-profit and for-profit EHPADs in France, the data correspond to median monthly fees in 2019: https://www.logement-seniors.com/articles-ls/tarification-ehpad-france.html; for the UK, the figure is the average monthly fees: https://www.carehomeprofessional.com/average-price-of-a-care-home-is-35000-a-year-latest-data-reveals/; for Japan, Statista 2020: https://www.statista.com/statistics/1215237/japan-average-monthly-costs-long-term-care-receiver-by-service/.

PAYG: pay-as-you-go.

The analysis draws upon qualitative data from 17 semi-structured and in-depth interviews with HC-REIT asset managers and care providers conducted in France, the UK and Japan in 2016 and 2017, with several follow-up interviews from 2019 to 2021 (see Table 3). The discussions focused on HC-REIT business models, the managers’ strategies to develop their asset portfolios, the regulatory environment in which they operated, and the particular relations they had with respective care providers. These data were supplemented by the annual reports and websites of the surveyed companies. To set the analysis in the changing context of welfare regimes, a detailed study was conducted on pension and long-term care policies in each of the selected countries based on government reports, national statistics and industry publications. The analysis relies on a comparison of documentary sources and informant statements to present a comprehensive account of the transformations arising from the securitization of nursing homes.

The next sections examine how HC-REITs implement portfolio growth strategies across different welfare and real estate investment contexts.

Financialization, welfare regimes and HC-REITs’ investment universe

The limited scope of nursing home securitization in France

With 7.6% of its population expected to be 80 years and over by 2030, France is ageing at a pace close to the European average (Table 1). The supply of nursing homes is around 600,000 beds across 7000 institutions known as Etablissements d’Hébergement pour Personnes Agées Dépendantes (EHPAD) facilities. Although this supply only meets half of France's current and future needs (108,000 beds to be filled between 2019 and 2030 – DREES, 2020), the country is the best equipped in nursing homes of the 3 cases studied, with currently one care bed for every 6.8 persons aged 80 years and over. Though decreasing and under threat by ongoing reforms, the French welfare state also offers the most generous pension benefits owing to a PAYG system that cumulates mandatory state and occupational pension provisions. For average full-carrier earners, the net pension replacement rate by earnings ranges from 69% to 73% 1 compared to 20% to 50% for the UK and 33% to 46% for Japan. As such, France has one of the least developed private pension fund markets in Europe (Naczyk, 2016). State support for long-term institutional care is therefore comparatively strong. Social care is subsidized by local authorities 2 in accredited EHPAD facilities through a ‘personal autonomy allowance’ (allocation personnalisée d’autonomie – APA) calculated in inverse proportion to an occupant's income. Occupants with monthly incomes below €2486 benefit from a significant reduction in their care co-contribution. As the average pension level is €1500, and an individual's main residence is excluded from the calculation of their assets, the personal autonomy allowance supports a large proportion of elderly residents. Similarly, accommodation cost may also be subsidized through a ‘personal housing grant’ (aide personnalisée au logement), but the benefit is only eligible for low-income occupants.

In addition to assistance for social care and accommodation, the state is heavily involved in the ownership and management of public EHPAD facilities, supplying almost half of all care beds nationwide. Alongside the public option, private not-for-profit EHPADs offer affordable monthly care at a much lower fee than their for-profit counterparts (€1960 compared to €2600 median rates) and also allow their residents to remain eligible for welfare benefits. Unlike many countries where private not-for-profit facilities have not been able to keep up with the necessary modernization of facilities and equipment, nor the improvement of care and management services, this sector has thrived in France, comprising 28% of the total supply of care beds. Such surprising resilience can be explained by two related factors: on the one hand, the consolidation and emergence of large investment groups – mutual companies, secular and religious associations or foundations, and on the other hand, (para)statal financial support for the renovation of not-for-profit EHPAD facilities, notably the National Solidarity Fund for Autonomy (Caisse Nationale de Solidarité pour l’Autonomie – interview 16, 2021). The powerful public bank Caisse des Depôts et de Consignation (CDC) is also involved in the financing of the largest not-for-profit care provider ARPAVIE.

For-profit providers are left with a relatively small portion of the market (23% of care beds compared to 80 and 50% for the UK and Japan, respectively), but consolidation dynamics have also led to the formation of medium- and large-sized commercial groups. Forty per cent of EHPAD facilities run by for-profit providers are accredited for state-financed social care. Such conditions offer financial investors clear potential for sale-leaseback, especially since many of facilities are located in coastal zones and the suburbs of major cities.

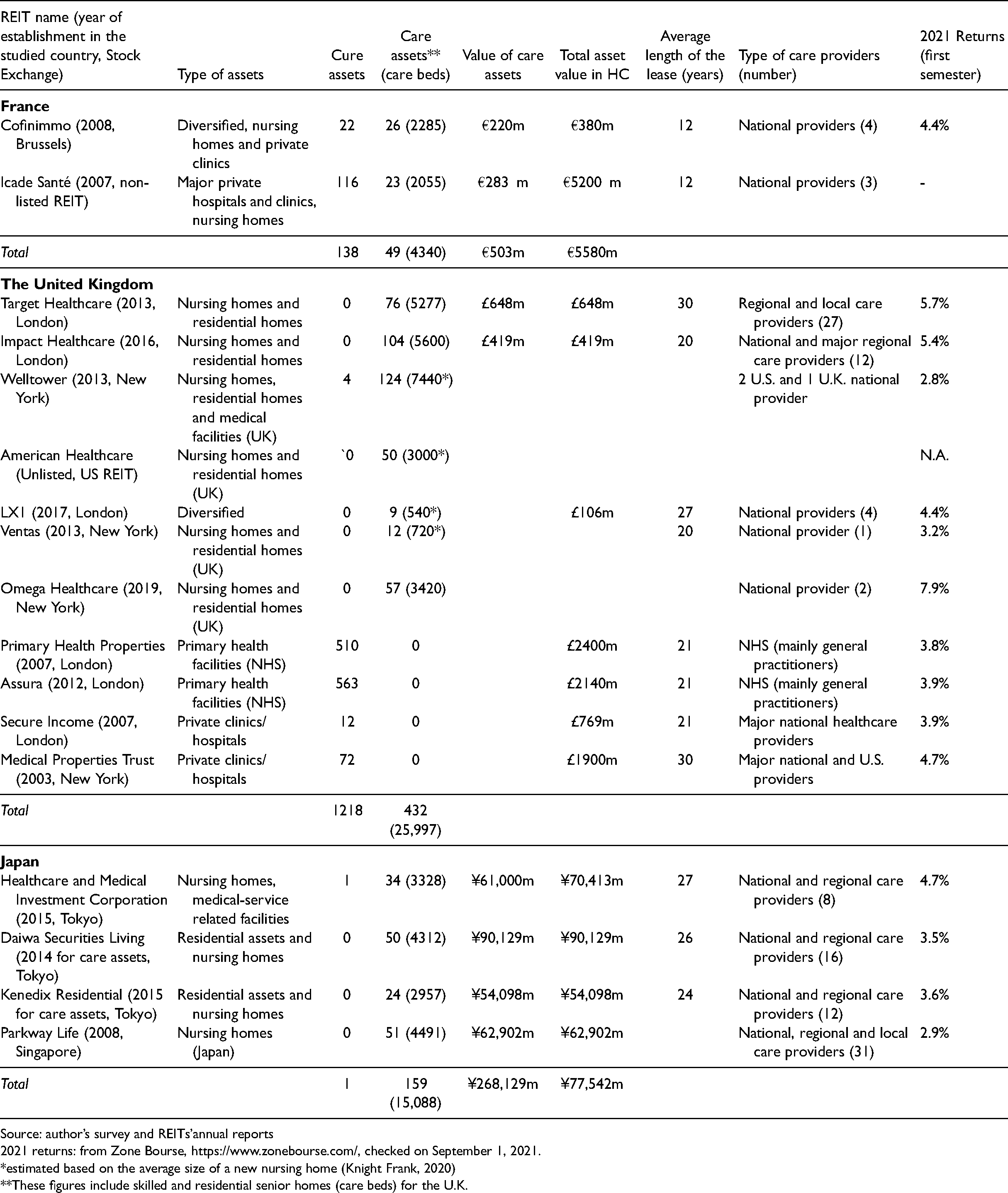

Indeed, the French HC-REIT market became active shortly after its launch in 2007. Within 5 years, three diversified HC-REITs started to operate in the care sector (i.e. the Belgian REIT Cofinimmo, Gecina and Foncière des Murs). In 2012, Cofinimmo established a REIT with the care provider Orpea (Cofinea) with the aim to reach an investment volume of €500 million in EHPAD properties. Yet, in the mid-2010s, REITs interest in the care sector declined sharply. Gecina and Foncière des Murs found they needed far greater knowledge of the healthcare sector to operate effectively and decided to withdraw from the industry, selling their portfolio with handsome capital gains to an unlisted healthcare fund (interview 01, 2016). For its part, the Cofinea REIT did not witness any development. Today, only two HC-REITs operate in the French care sector: Cofinnimo, with a residual portfolio of EHPAD properties whose leases have not been renewed, and Icade Santé, an unlisted REIT with a majority ownership (58.6%) by Icade, the real estate arm of the public financial group Caisse des Dépôts et de Consignation (CDC). Icade Santé has become a major landlord of private clinics. Although it started diversifying in the European nursing home market in 2018, it has so far managed to acquire twenty EHPAD facilities in France. However, with a total supply of 4340 care beds, the two REITs operating in France control less than 2% of private EHPADs nationwide (Table 2).

Characteristics of the Health Care (HC-REIT) markets in the three countries (as of December 2020).

Source: author’s survey and REITs’annual reports

2021 returns: from Zone Bourse, https://www.zonebourse.com/, checked on September 1, 2021.

*estimated based on the average size of a new nursing home (Knight Frank, 2020)

**These figures include skilled and residential senior homes (care beds) for the U.K.

List of interviews.

The slow development of the French HC-REIT sector is due to the difficulty in building portfolios that meet a critical threshold of properties under management. One major obstacle is the limitation in authorizing new EHPAD operations. Since 2010, local authorities are responsible for these authorizations, which they grant through public tender. But to limit the cost of care assistance, only two to three EHPAD tenders are made each year (interview 16, 2021). To circumvent these restrictions, the supply of new care beds is expanded by either converting residential care homes without nursing into an EHPAD facility, or by transferring the authorization of an existing site to another within the same jurisdiction where a larger structure can be built (interview 03, 2016).

Another barrier to the growth of HC-REITs has been due to competition with individual investors in the financing of for-profit EHPAD facilities. The government incentivizes small investors to acquire residential units in senior care homes (with or without nursing) through a tax relief system known as ‘Censi Bouvard’. Because the expected returns from these individual investors are one or two points lower than those of REITs, some care providers that are considering selling their properties are tempted to choose these small investors as landlords, even if it requires interacting with many at once 3 (interview 02, 2019).

More generally, French for-profit providers also consider the physical real estate dimension of a nursing home as part of their operational activity, in addition to its profit-generating component; they, therefore, tend to sell properties only when they are short on liquidity (interview 08, 2017). A notable exception is the Korian group, the largest care provider in Europe. To achieve rapid growth, the French group divested most of its properties to REITs or unlisted funds. In 2020, Korian signed an agreement with Icade Santé, in order to allow the former to have the option to become the tenant of some of its newly (re)developed EHPAD facilities managed. However, while this agreement was underway Korian also started to move from an ‘asset light’ to an ‘asset smart’ business model, which prioritized renting or owning according to the occupancy cost of each nursing home facility. To retain control of its asset portfolio, the group established its own unlisted fund in 2019 for which it is the majority shareholder.

Finally, it is worth noting that one French REIT seriously considered acquiring public EHPAD properties in the early 2010s to access the well-subsidized market of large-scale facilities (80 beds on average). However, the REIT faced strong reluctance from local authorities and representatives on the boards of the respective EHPADs, as well as other regulatory constraints governing the legal status of the facilities as state properties (interview 01, 2016). Given these conditions, it is unlikely that the securitization of EHPAD facilities will undergo significant progress without going through a process of ‘privatized financialization’ (Aalbers, 2016).

A friendly environment for financial investment in the UK’s nursing homes

The UK has a similar population size and ageing pattern to France, but only has 212,000 care beds in the so-called ‘skilled nursing homes,’ which are mostly located in the for-profit sector (Table 1). The industry estimates that at least 75,000 additional care beds will be needed by 2030 (Grant Thornton, 2018).

As a liberal welfare state, the UK has developed DC schemes to compensate for the erosion of defined benefits (Table 1), but nearly half of UK retirees are not joining the private option (FCA, 2018) but instead rely on the low income provided by mandatory state pensions (Table 1). This puts enormous pressure on local councils, who are responsible for financing long-term institutional care. Therefore, the state has adopted an asset-based approach to welfare to make housing equity a substitute for retirement benefits (Elsinga and Hoekstra, 2015). The Care Act 2014 introduced expense co-payments in care homes based on an occupants’ housing wealth (Wood et al., 2020). Under this system, social care and accommodation costs are bundled together into one co-contribution by occupants; individuals with savings and assets – including owner-occupied homes in many cases 4 – valued at more than £23,250 must be self-funded. Recent industry figures show that 45% of care home residents are self-funded, 35% are entirely supported by the state, while 11% are partially funded (Kay, 2021). For those who cannot afford care costs, the usual route is to sell their home. However, other solutions can involve loans secured by the ownership of the home whose pay-out is deferred until death, such as through ‘deferred payment schemes’. 5

With public and not-for-profit care homes accounting for only 16% of care bed supply, local councils must turn to for-profit providers to place elderly recipients. Rates are typically negotiated at 10% below the market, which means that providers charge self-funded residents about 40% more than benefit recipients in the same nursing home (House of Commons, 2017: 28). This, in turn, pushes fund managers to bear the risks of further erosion of public care funding.

The securitization of care homes in the UK started in 2013. American REITs seeking to diversify their portfolios in Europe were drawn to the shared language and similar business-friendly environment afforded by the UK – in contrast to France where US REITs’ master leases are considered abusive by care providers as they can impose automatic rent increases on the tenant 6 (interview 17, 2021). The penetration of American REITs in the UK was further boosted by the abovementioned private equity debacle of Southern Cross and Four Seasons Healthcare (Horton, 2021). Today, there are four US HC-REITs 7 operating in the UK, with Welltower being by far the largest (Table 2). The US trusts operating in the UK share a similar business model to their domestic counterparts, which comprise: (i) the establishment of master leases with a handful of large-scale US and UK care providers; (ii) a focus on the UK's South England and Greater London regions where household wealth and housing price inflation are the highest; and (iii) a focus on care homes with a quasi-exclusive clientele of self-funded residents. The US trusts are currently moving towards residential care homes (without nursing), notably for patients suffering from dementia (Knight Frank, 2019). Because of their high credit rating, they benefit from lower capital borrowing costs, which allow US HC-REITS to achieve economies of scale by building large-size facilities (i.e. with more than 60 beds) and assisting in renovations. Nevertheless, American trusts provide investors with lower returns than their UK counterparts, with the notable exception of Omega Healthcare (Table 2).

Unlike their American peers, British HC-REITs has developed a significant share of state-funded residents (40%), which provide their portfolios with greater spatial diversification (interview 06, 2017). The two main UK trusts, Target Healthcare and Impact Healthcare, have assets spread across the country, except in the poorest regions (e.g. Wales and the North East). Both limit their exposure to the Greater London market where competition with pension funds and foreign investors puts downward pressure on returns (interview 07, 2017). However, the two trusts also have important differences. Impact Healthcare has a business strategy more similar to that of US REITs, which focuses on the balance sheet of a small number of major national providers. In contrast, Target Healthcare focuses on partnerships with a variety of medium- and small-scale providers. To offset the long-term risk (30 years) associated with small operators, the trust prioritizes the quality and location of the care facilities it invests in, so as to make it easier to convert the properties to other uses in case of provider failure. Regardless of these approaches, both UK REITs had yields exceeding 5% in the first semester of 2021 – despite the wider impact of the COVID-19 pandemic – and whose returns primarily went to UK investment and wealth management firms.

HC-REITS operating in the UK has been developing at a rapid pace over the past 5 years, and now account for 5%–6% of the estimated supply of care homes in the country 8 . Yet, asset managers still face challenges in developing their portfolios. Available land for new care home development is scarce, and a significant proportion of the existing stock does not meet the HC-REIT investment criteria, in terms of asset size, location and regulatory compliance. This implies that HC-REITs must incur significant costs to build new homes, to refurbish or expand existing ones or to grant loans to their tenants. Another obstacle is the high fragmentation of the care industry (the vast majority of the 5500 providers only run a single facility), which increases the perceived risk regarding a tenant’s financial resilience, even though small family homes are said to provide better quality care than large national providers (Horton, 2020).

Despite their rapid growth, HC-REITs that run nursing homes are dwarfed by the three powerful trusts involved in cure (clinics, hospital) facilities, and whose respective assets are valued at £2 billion each (Table 2). Cure HC-REITs hold spatially diversified medical facilities that offer investors stable and secure income streams. The two largest REITs in cure assets, PHP and Assura, have been entrusted with the management of long-term leases of public primary health facilities backed by the NHS. These trusts posted lower returns than UK care REITs in 2021 (3.8–3.9%), but were still attractive considering that rents are primarily paid by tax revenues. Their robust performance compared to other investment vehicles has benefitted British investment funds, and even more so global investment firms based in Australia, Norway or the United States (including Vanguard and Blackrock groups).

Japan's intermediate pathway to securitization

Unlike their British and French counterparts, Japanese HC-REITs have not been able to penetrate the cure market to date, because medical corporations are often owned by a single doctor who benefits from the facility's tax-exempt status 9 (interview 14, 2018). The care market, on the other hand, is considered to have great prospects. With nearly one in 10 individuals over the age of 80 years, and a ratio expected to reach 13% by 2030 (Table 1), Japan seems to be an ideal market for the nursing home industry.

Long-term care of the elderly has long been provided by families in Japan, but changes in living conditions and the growing involvement of women in the workforce have shifted care responsibility towards institutional facilities (Hirayama, 2010). In 2000, a public long-term care insurance system known as kaigo hoken was introduced to provide universal access to care services for people aged 65 years and older. Half of the funding is supported by compulsory premiums paid by a citizen over the age of 40 years, in addition to tax revenues. Social care and accommodation are bundled together, with nursing home residents initially charged a flat fee regardless of income. However, as ageing progresses, the co-payment has increased from 10% to 20% or 30% for those with moderate (¥2.8–3.4 million) and high incomes (¥3.4 million or more) (Yamada and Arai, 2020).

The state has shown its determination to encourage private initiatives in long-term care (Saito, 2014). Between 2000 and 2018, care beds in for-profit nursing homes increased from 36,900 to 514,000 (Ministry of Health, Labour and Welfare, 2019). As a result, the for-profit sector, which accounted for only 5% of care beds in 2000, now controls half of the total supply (Table 2) – and this has occurred amid a constant increase in the number of public nursing homes.

The kaigo hoken system has largely benefited middle- and high-income households, who were no longer obliged to bear the full cost of care (Izuhara, 2007). Yet most Japanese retirees do not enjoy generous pension benefits. Japan's pension regime combines a PAYG approach with modest state expenditure and voluntary private schemes. The traditional DB plan used by Japanese employers has shifted to DC plans since 2001, but more than half of elderly households rely exclusively on public pension benefits (Olivares-Tirado and Tamiya, 2013). This puts the average monthly pension at ¥150,000–200,000 (US$1350–1800) for full-carrier earners. Therefore, some for-profit providers have designed a system by which older residents pay monthly fees out of their pension and are charged an additional ‘upfront fee’ 10 (nyukyokin) varying across regions – on average ¥5 million (US$45,500) and up to ¥70 million (US$ 410,000–630,000) in Tokyo special districts (Lifull, 2021). To pay this fee, nursing home residents often draw on their deposits and financial assets, which for many is a home equity that they must sell to meet the costs of long-term institutional care.

In its effort to encourage for-profit providers to develop their core business activity, the state placed its hopes on the mobilization of financial investment in care facilities. To this end, three HC-REIT structures were created in 2015 after a 13-year effort by the state to set up a new investment channel in the sector (interview 12, 2018). However, two of these trusts were not able to develop portfolios of a critical size to be financially viable and had to be absorbed by the overarching REIT of the same sponsor group (Kenedix Residential NEXT Investment, and Daiwa Securities Living Investment Corporation). This has left Healthcare & Medical Investment Corporation (HCM) as the only REIT specialized in healthcare listed on the Tokyo Stock Exchange.

The three Japanese trusts pursued similar investment and management policies, characterized by long-term leases (23–27 years), with a preference for large national, publicly listed providers and with regional companies of strong operational and financial track record. Rents are in principle not subject to increase, although revisions are permitted in the event of significant changes in macroeconomic environment. The trusts also seek economies of scale by purchasing large facilities (exceeding 100 beds) in many cases provided by unlisted funds as an exit strategy – typically located in peripheral areas of Japan's three major metropolitan regions (i.e. Tokyo, Osaka, Nagoya). Nevertheless, the Japanese nursing home industry is made up of mostly small, inexperienced and, in many cases, unreliable providers. According to one of my informants, only 500 of the 5000 providers would be ‘REIT-able’ in terms of quality of care and revenue strength (interview 10, 2018). Furthermore, the majority of these facilities have less than 50 beds, well below the economies of scale sought by REIT managers. In some cases, the properties are owned by individual homeowners who are encouraged by tax incentives to build a nursing home on their vacant land and to entrust its operation to a care provider (interview 14, 2018).

Japanese REITs do not lack the financial capacity to acquire real estate assets because they are backed by large financial groups. However, Japan's REIT regime does not allow these trusts to engage in real estate development or renovation, nor in lending to providers (PWC, 2019). Tokyo-listed HC-REITs are thus severely limited in generating the economies of scale necessary to make their portfolios profitable. Nevertheless, their small capitalization does not prevent them from performing well: in the first half of 2021, Japanese HC-REITs provided returns of 3.4%–4.5% to their shareholders, mainly trust banks and asset management firms affiliated with large Japanese conglomerates. The upfront fees charged by some providers are part of this rental income, and represent between US$10,000 and $70,000 (interview 15, 2021).

The long-term care market in Japan has also attracted a Singapore-based HC-REIT, Parkway Life, which began operations as early as 2008. Initially focusing investment in the Southern regions of Honshu, it has since spread across the whole country while carefully avoiding competing with Japanese HC-REITs. With a portfolio of 51 facilities, Parkway Life has managed to capture nearly a third of the HC-REIT market in care beds in Japan. This is partly because Singapore's REIT regulations are less stringent than those in Japan. There, trusts are allowed to undertake property development activities as long as they intend to retain the property upon its completion (PWC, 2019). Parkway Life also operates on a different business model than its Japanese counterparts. Its investments target relatively well-located properties and show a less risk-averse strategy by partnering with a large array of providers – both national and local, listed and unlisted (31) – whose properties they redevelop and expand through Asset Enhancement Initiatives (interview 11, 2021). To this end, Parkway Life established a wholly owned subsidiary that provides the flexibility to tap into different capital markets and their products. Although Parkway Life has managed to extract greater real estate value than its Japanese peers through the Asset Enhancement Initiatives, its performance is in line with American HC-REITs (2.9% in the first half of 2021), whose shareholders are more or less the same groups (e.g. US-based international investment firms, Blackrock and Vanguard groups). The Singaporean trust faces the same constraints as its peers in partnering with reliable care providers, although it demonstrates a less risk-averse strategy by engaging with small companies. Its portfolio of nursing homes, almost exclusively based in Japan (half in the Southern regions of Honshu), is therefore growing at a relatively slow pace.

As a result, although the potential of the for-profit nursing home market has become significant in Japan, the four HC-REITs operating in the country currently control only 2.5% of the existing stock of private care beds.

Conclusion

This article has highlighted the uneven outcomes of nursing home securitization across national welfare regimes and landlord–tenant relationships in the care sector, while also pointing out the effects of differentiated REIT regimes within a single national context.

France and the UK present contrasting cases in the degree of financialization occurring in their respective welfare regimes and in the securitization of their nursing homes. The French retirement system is (so far) weekly financialized, with strong state control in the management of affordable EHPAD facilities and in the strict regulation permits to run new nursing homes – all of which considerably reduces the investment scope of HC-REITs. The UK, however, has one of the most financialized pension systems in Europe, with an overwhelming proportion of for-profit nursing homes that have been targeted by financial players, most notably HC-REITs. In this liberal welfare state, the balance of power between landlords and tenants is clearly in favour of the former, who subject care providers to systematic rent increases. As a result, care costs have steadily risen, which has depleted the resources of local councils and imposed a substantial financial burden on a growing population of self-funders.

The case of Japan shows, however, that the linkages between pension schemes, long-term care policy and the financialization of nursing homes are not so straightforward. Japan has a fairly financialized pension system, combined with a long-term care policy that encourages the development of for-profit facilities and REIT investment in long-term care structures. Nevertheless, the securitization of nursing homes has not lived up to the government's expectations. The defensive regulation of domestic REIT activity may explain some of the difficulties trusts encountered in increasing their asset portfolios, but the operations of the Singapore-based REIT, Park Life, shows that a more flexible REIT regime does not fundamentally remove barriers for property acquisitions in the sector. Rather, other determining factors include the late emergence of the long-term care sector itself, and the contradictory measures the state has undertaken in regard to senior living accommodation.

Indeed, there are contradictions in Japan's national policies promoting an ‘asset-light’ business model in long-term institutional care. One example has been the disconnection between measures encouraging sale-leaseback arrangements in favour of REITs, and tax rebates inciting individual landowners to retain ownership of their nursing homes facilities. Similar issues exist in France, where the early establishment of HC-REIT channels in 2007 was soon followed by stringent limitations on the issuance of new EHPAD permits that resulted from cuts in state transfers to local authorities. The French case further reveals the blurring of state and market relations with regard to the role of the public bank CDC. By creating Icade Santé as the healthcare channel of its real estate arm (the ICADE group), the CDC ended up establishing a ‘financial vehicle within the state’ (Wijburg, 2019: 6) for self-financing.

The limited growth of HC-REITs managing care assets in France and Japan should not lead to the conclusion that the financialization of nursing homes is bound to remain weak. Unlisted investment funds also operate in this sector, sharing portfolio income between a handful of institutional investors, and supplying HC-REITs with investable properties. Large-scale providers have also created their own listed funds to further extract value generated from their real estate assets. The emergence of ‘asset-smart’ business models such as that developed by the French group Korian, suggests that these large providers may well strengthen their position vis-à-vis financial landlords.

As national populations age, it is clear that welfare systems will not be able to cope with the needs of their elderly dependents, whether in terms of meeting pensions obligations, the cost of social care/accommodation, and the provision of affordable nursing homes. But as can be seen in the UK and Japan, where the pension financialization is more advanced, residents of nursing homes increasingly compensate for the erosion of their benefits by de-stocking the value of their homes. While the spread of this asset-based welfare approach offers REIT managers good prospects for maintaining high risk-adjusted returns despite the weakening of state welfare regimes, it has also widened the income gap between elderly populations in different regions, which severely undermines intergenerational solidarity.

Because of these differentials, REIT asset managers and other financial players are likely to be increasingly selective in their selection of care facilities, both in terms of location and customer base, thereby leaving whole areas within national territories underdeveloped. Despite the challenge of finding suitable ‘pipelines’ for long-term care facilities, they are determined to increase their exposure to niche markets such as healthcare as the progressive financialization of pensions increases the need for investment opportunities. These actors are counting on the fact that both public and small private providers will not have the willingness or capacity to adapt their facilities to changing care needs and standards.

Therefore, if we want to avoid reproducing the growing problems of nursing home supply that exist in liberal welfare states, it is imperative that the state retains ownership of public nursing homes and provides strong support to the not-for-profit sector. The state should maintain its commitment to pension and social care funding so that the home equity built up over a working life is passed on to future generations, rather than being sold off to financial investors. This paper has pointed to new areas where financialization has sought to transform established practices of social welfare and well-being. By shedding light on the interlinkages between social properties and welfare policies, it brings a new perspective to the current debates on the political economy of real estate financialization. Further research is nevertheless needed to explore the co-evolution of pension policies, the tenure of long-term care facilities and social inequalities in these and other welfare settings give rise to.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Agence Nationale de la Recherche [ODESSA project: Optimising care DElivery modelS to Support Ageing-in-place: towards autonomy, affordability and financial sustainability] (grant number ANR-14-ORAR-0006).