Abstract

Multinational enterprises (MNEs) take advantage of local differences in their global location of assets and activities. Scholarship in economic geography and international political economy associates value-producing entities organized in Global Value Chains (GVCs), and wealth-protecting entities in Global Wealth Chains (GWCs). At the aggregate level, these are often associated with different geographical manifestations, with GVCs centered around “production hubs” and GWCs around “offshore jurisdictions.” This indicates an asymmetrical geography between value and wealth with a low level of entanglement. This does not account, however, for the ways value and wealth are governed within MNEs. We investigate how the firm-territory nexus can be understood across scales and what this implies for the geographical overlap between GVCs and GWCs. While there is seemingly limited entanglement of GVC and GWC activities at the macro scale, at the meso scale there are overlaps and significant entanglement at the micro scale. This implies value and wealth are more geographically aligned than previously thought, and that initiatives aimed at regulating these chains needs to address practices within MNEs rather than targeting arbitrary geographies at the country level.

Introduction

Geographical fragmentation is one of the key characteristics of the global economy, in which multinational enterprises coordinate complex networks of legal ownership and economic relationships. Through Global Value Chains (GVC) and Global Wealth Chains (GWC), MNEs organize themselves to benefit from different economic and legal characteristics across countries, catering to their production and finance needs respectively (Gereffi et al., 2005; Seabrooke and Wigan, 2022). GVCs and GWCs serve a variety of needs, including outsourcing to jurisdictions with lower operational and labor costs, to handle exchange rate risks, to manage intellectual property, and ease intra-firm trade, among many other factors. This fragmentation also leads to specialization, as the firm-territory interaction impacts local economic geographies. Local geographies can be understood to serve different roles within the global economy, acting for example as production hubs (Coe et al., 2014; Criscuolo and Timmis, 2018) or as (offshore) financial centers (Garcia-Bernardo et al., 2017; Haberly and Wójcik, 2015, 2022). The intersection between these, and how value and wealth creation is entangled within the firm-territory nexus, is rarely investigated. This “yin and yang” picture of the global economy consisting of production and finance separately is often invoked implicitly or even explicitly (Seabrooke and Wigan, 2017: 22), and supported by the lack of integrated approaches to studying finance and production. We seek to locate the overlaps between GVCs and GWCs to find different views of how they may be “entangled” (this Special Issue theme).

Scholarship on production processes has focused on the development of Global Production Networks (GPNs) (Yeung and Coe, 2015) and GVCs (Gereffi et al., 2005). The GVC approach has been used to understand the unequal distribution of value and power across the fragmented production chain, often focusing on single industries or even single products (Sturgeon, 2019). Finance and law have been integrated as a factor in production processes (Coe et al., 2014; Cutler and Lark, 2022; Durand and Milberg, 2020; Faulconbridge, 2019; Milberg, 2008). The emphasis in these approaches has been to locate how credit money and financialization processes contribute to value creation in the production process (Morgan, 2014), with emphasis on the value creation process.

Other frameworks focus on financial relations as a primary rather than secondary focus. The first here is the Global Financial Networks (GFNs) approach, which focuses on how financial and business services, “world governments,” financial centers, and offshore jurisdictions come together to “manufacture the product of money in the world economy” (Haberly and Wójcik, 2022: 7). The second is the Global Wealth Chains (GWCs) framework, which deliberately mirrors the GVC typology to focus on how firms and professionals strategically plan across “multiple legal jurisdictions to control how assets are evaluated and governed” (Seabrooke and Wigan, 2022: 1), but does not include a focus on production processes.

The GVC and GWC typologies are frameworks that seek to explain the behavior of lead firms and lead suppliers in relation to others in the chain, allowing comparisons between types of cases based on assumptions about transaction complexity, the codability (opacity) of information, and supplier capabilities (Gereffi et al., 2005; Seabrooke and Wigan, 2017). In comparison to scholarship on GPNs and GFNs, which stress configurational complexity, the “chains” frameworks seek parsimony in facilitating case comparisons where the intent of the lead actors is important. We seek to disaggregate this intent into locatable configurations over scales, to locate where entanglement of GVCs and GWCs is likely and the implications of this entanglement for the international political economy.

As this Special Issue discusses, scholars have recently converged on trying to understand how GVCs and GWCs are entangled rather than simply noting their yin and yang relationship. What does this entanglement look like and mean for our understanding of contemporary capitalism? The thrust of existing scholarship on entanglements is that we should look beyond the behavior of lead firms in GVCs as concerned solely with production, and on wealth management as an additional activity that follows from value creation. The assumed linearity of value creation then wealth protection should be challenged, recognizing that MNEs entangle their chains based on the relative importance of intangible versus tangible assets, and the firm’s emphasis on value creation or wealth protection (Bair et al., 2023). This new work begs the question on how we may see chain entanglement geographically. In this paper we ask: how are MNEs’ GVCs and GWCs articulated geographically, and what does that imply for the entanglement of these modes of economic governance? We answer these questions by analyzing the geographical overlap between GVC and GWCs across micro, meso, and macro-scales. We hope that differentiating across scales can develop a better understanding of GVC-GWC entanglement.

We contribute to this general strand of scholarship by locating how MNEs locate production and financial activities across micro, meso, and macro-scales. This allows us to analytically separate the social organization of economic activities in the firm and the articulation of legal organization through the corporation (Robé, 2011, 2020). We argue that this distinction is important in viewing micro-positions in macro-structures, and the power asymmetries present at micro, meso, and macro scales that underpin how GVCs and GWCs are entangled in both form and practice. This requires assembling a range of data that reflects micro, meso, and macro activity in GVCs and GWCs. We assemble this data by drawing on country-based statistics, corporate reporting, and social media.

Our article proceeds as follows. First, we discuss the importance of distinguishing the firm and the corporation as a means to parse out relational and socio-legal views of economic activities that operate across scales. Second, we discuss the importance of territoriality and the firm-territory nexus for the global operation of GVCs and GWCs. We then correspond this thinking to macro, meso, and micro scales of economic activity and outline our search for data on entanglements between GVCs and GWCs across these scales. We present our empirical findings and conceptualize how these entanglements may be understood and connected. Finally, we discuss the broader implications GVC and GWC governance and entanglement and conclude on the ways in which different types of territoriality enables different types of economic relationships to emerge.

Geographies of value and wealth

Economic geography has a long-standing research agenda to differentiate the location of economic activities (Beaverstock et al., 1999; Lavoratori et al., 2020). Classically, Dunning and Norman’s (1983) ownership-location-internalization approach pointed to how the location of executive and professional staff was not especially linked to labor costs or specific geographies but more on staff availability as well as social and cultural factors (see also Faulconbridge et al., 2008: 212). Early theories contended that once a firm is of sufficient size the location of offices is driven by ease of communication to the “plant” and to allow managers to coordinate (Evans, 1973: 688). On GPNs, Yeung and Coe (2015) stress the importance of lead firms for location choices made in lower-tiers of suppliers. In the GVC literature location is also led by lead firms and relocation decisions are strongly informed by the capacity to upgrade parts of the chain (Verbeke and Asmussen, 2016).

In GVC research the location of production sites has been important for understanding uneven geographic development (Bair et al., 2021; Hess and Coe, 2006). Bernhardt and Pollak (2016) measure economic upgrading by the export value and export market share within an industry, identifying what countries upgrade in GVCs over time. In country-level analyses, the measurement of GVCs is focused on the level of integration of a country into GVCs as measured by trade in value added (OECD, 2021a). Such work shows that some countries over time experience increased or decreased economic and social downgrading by assessing value chain integration and up/downgrading via trade linkages (Criscuolo and Timmis, 2018; Johnson, 2018).

Location choices can also be driven by financial considerations, as has been explored in GWC and GFN literatures. In the research into GWCs, emphasis is usually put on jurisdictional differences and the opportunities for the structuring of corporate forms within them. Strategically placing asset ownership in low-tax jurisdictions has been a regular emphasis, especially tracing how firms and elites have developed strategies to exploit opportunities in particular jurisdictions like the British Virgin Islands (Robertson, 2021; Stausholm, 2022), Liechtenstein (Sharman, 2017), Luxembourg (Finér and Ylönen, 2017), Mauritius (Behuria, 2023), and others. Cross-country analyses of GWCs have mostly focused on identifying the features of financial secrecy (Cobham et al., 2015), or measuring the centrality of countries in ownership links within MNEs (Garcia-Bernardo et al., 2017). Such studies have identified how such jurisdictions attract financial inflows in a scale incommensurate with the size of the domestic economy (Tørsløv et al., 2018). Investigations have also shown how corporate ownership networks center around low-tax jurisdictions (Martins et al., 2019). Others have taken a more relational view, studying the role of tax professionals in this space and emphasizing the relationship between tax service suppliers and client location (Ajdacic et al., 2021; Elemes et al., 2021; Christensen and Seabrooke, 2022).

For the GFN literature, the location of activities is a mix of complementarities and opportunities provided by financial centers and offshore jurisdictions, with financial and business services and “world governments” (those with extraterritorial reach) enabling this activity (Haberly and Wójcik, 2022). While the GFN literature emphasizes the articulation of finance at the country level in terms of financial centers and OFCs, GWC literature has focused on the professional activity facilitating the networks of financial flows into and through these jurisdictions (Ajdacic et al., 2021; Arlen and Burelli, 2022). The location of activities is a mix of jurisdictional opportunity and professional enablement, such as the articulation of GWCs linked to London property investment (McKenzie and Atkinson, 2020; cf. Fernandez et al., 2016), private equity controlled German medical services (Bůžek and Scheuplein, 2022), or Mauritius’ self-entrapment in providing “low-value” financial services (Behuria, 2023). GWC and GFN scholarship generally distinguish between “offshore” and “regions of production” (Coe et al., 2014).

Corporations and firms

Some conceptual clarification is required for us to proceed our thinking on how GVC and GWCs are entangled, and how they can be measured. It is important not to see value and wealth as representing either “real” or “virtual” economic activity, respectively (Hall, 2013). In particular, the use of “offshore” strategies by firms has been characterized as “fictitious” (Clausing, 2009; Roberts, 1995), but such representations compound the gap between GVC and GWC research, and especially the implication that GWC represents pure legal maneuvering while GVC represents “real” economic activity. We draw upon Robé’s (2011, 2020) work and make a distinction between the “firm” and the “corporation.” Seeing the firm and the corporation as interchangeable is common, but analytically problematic. For Robé the firm is the organizational unit, the going concern, and the corporation is the legal framework created to protect managers and appease shareholders. The implication of this is that executive managers in the MNE control assets owned by entities in the corporate structure, which is divided and protected by the legal personality of the corporate entities. The core of the firm, the C-suite, orchestrates the corporate structure so that they can protect their operations across scale. Shareholders have claims on part of the corporate structure, those managed to satisfy them, but shareholders do not own the firm, nor are managers the agents of shareholders (Robé, 2011). Robé’s firm/corporation distinction has radical implications for those who view the corporation as a “legal fiction” (Jensen and Meckling, 1976), or follow an “agency theory,” investor/shareholder governance view of the firm. For economic geography and international political economy, the implication of the firm/corporation distinction is that we can provide nuance to the concept of virtual versus real parts of the economy by distinguishing activities within MNEs rather than at the aggregate level.

The social aspects of MNEs linked to the firm are from positional networks, in which professionals are able to organize, strategize, and foster and maintain social forms that affirm power asymmetries, including those related to class, gender, and race (Sheppard, 2002). The social aspect for territory is how the physical environment allows concentrated activity in world cities (Bassens and Van Meeteren, 2015; Beaverstock et al., 1999; Friedmann, 1986). On the legal aspects, we can see incorporation as the manifestation of MNEs’ strategy and sovereignty as the legal instantiation of territorial rule and means to (mis)recognize other polities (Epstein et al., 2018). As is well recognized, this sovereignty can be commercialized (Dörry, 2022; Wainwright, 2011). Those working in the “firm” can use the “corporations” as legal units that protect assets, for example through geographical arbitrage (Palan et al., 2023).

The production-led GVC side of a MNE consists of both firm and corporation components, in which agents, networks, and relationships organize and control value creation. The legal manifestation of GVCs is no less important than for GWCs, as the incorporation and contractual relationships between different legal units are imperative to GVC governance (Cutler, 2017). Similarly, GWCs have both a socio-organizational manifestation and a legal one. Contemporary MNEs rely on professional services to plan multinational corporate structures, especially for accountancy and financial management (Beaverstock, 1991, 1996; Boussebaa and Faulconbridge, 2019). Both GVC and GWC aspects of MNEs can be thought of in “firm” and “corporation” aspects, in which the legal strategies through corporations and the social organization of the firm are mutually reinforcing. We investigate the ways in which these aspects of GVC and GWC manifest differently geographically across scales.

Firms and territories

Economic geography and international political economy scholarship has well-established views of how MNEs relate to physical space. Most prominent among these is the “firm-territory nexus” from Dicken and Malmberg (2001), which is composed of firms, industrial systems, and territories. Firms are conceptualized as “the individual business organization” or a “system of similar and related firms” (Dicken and Malmberg, 2001: 345, italics in original), and territory is a “bounded segment of geographic space” (Dicken and Malmberg, 2001: 345). Industrial systems are the “particular constellation of processes and institutions in a specific segment of similar and related economic activity” (Dicken and Malmberg, 2001: 347). Firms develop governance systems in relation to the industrial system. Understanding firms involves: recognizing the nature of firms not only as legally bounded entities and owners of proprietary assets (both tangible and intangible) but also as institutions with permeable and highly blurred boundaries—in other words, conceptualizing them as “networks within networks” or “systems within systems” (Dicken and Malmberg, 2001: 346).

This view of the firm as fundamentally networked has had a great deal of influence on the literature (most recently Beaverstock et al., 2023), including the development of the GPNs and GFNs. The firm-territory nexus is replicated in thinking about GFNs, with territory bounded into “world cities,” “regions,” and offshore jurisdictions, and firms understood as global production networks and advanced business services. An “institutionally mediated interface” connects firms and territory (Coe et al., 2014: 764).

Investigating the firm-territory nexus requires thinking about the importance of different organizational roles. Fligstein (1990) noted long ago that managerial control within MNEs was being transformed by finance, empowering those “determined by a legal framework and a self-conscious vision of the world that make both old and new courses of action possible and desirable” (Fligstein, 1990: 4). Similarly, Zorn (2004) noted the rise of the CFO as a new organizational actor that was diffusing across American enterprises in response to regulatory pressures. Understanding and planning tax minimization requires the assistance of experts facilitating the connection between GVC and GWC entities (Clark and Monk, 2014; Wójcik, 2013). Tax professionals provide the tools needed for managers to make strategic decisions to use corporate forms to minimize taxation and provide those running the firm with greater flexibility (Ajdacic et al., 2021; Christensen et al., 2022). Even the top management of the firm may be unaware of the full extent of the legal devices used to optimize wealth protection (Robé, 2020: 266), meaning that GWC creation is a relationship established between the firm’s managers and external professionals, through blurred boundaries as conceptualized in Dicken and Malmberg (2001).

Research design

The key aspect of GVCs and GWCs is that they are geographically fragmented, in ways that enable MNEs to benefit from differences across legal and economic units. Similar to Dicken and Malmberg (2001) we reject the notions of “global” firms and chains as being placeless, but rather argue that their geographical configuration is essential. We do not argue that geographical overlap is the only way to study entanglement, but geographical configuration is one avenue to understand how different or similar value and wealth creation are within MNEs. The territoriality of firms happens at “a continuum of variable and overlapping scales” (Dicken and Malmberg, 2001: 355). We therefore organize our inquiry into the correlation between value and wealth across three scales of micro, meso, and macro.

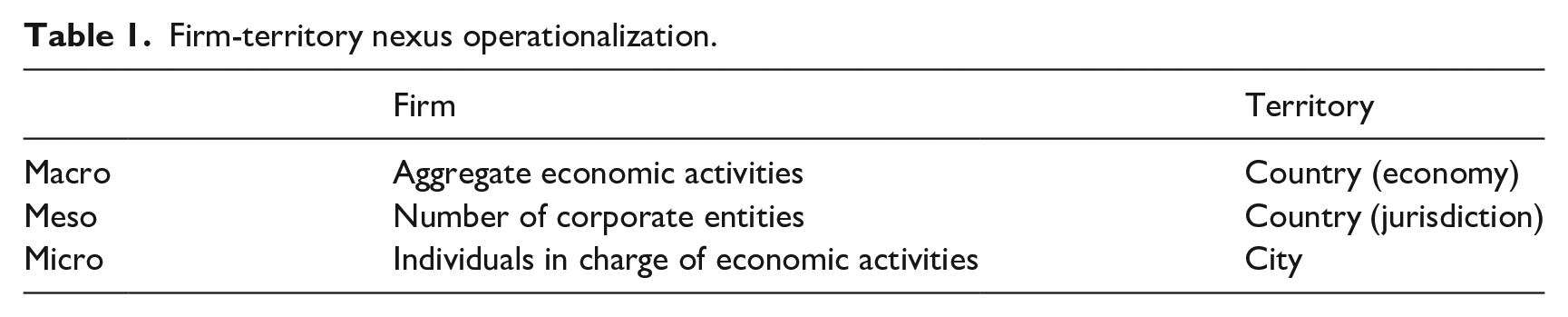

How do we map the firm-territory nexus? First, we need to operationalize the “firm” which at the macro level is aggregate economic activities in countries, at the meso level is the number of incorporated entities operating in each jurisdiction, and at the micro level consists of the individuals in charge of economic management. Then we need to operationalize the “territory” which at the macro and meso level is countries or jurisdictions, as that is the scale at which economic activities are recognized and the legal space within which corporations exist. At the micro level however, we are able to take into account the fact that individuals do not reside in abstract countries but are rather situated in concrete spaces (Sheppard, 2002). Here, we take larger cities as our unit of measure of “territory.” We do not mean to imply that either of these scales is a more “correct” measure of the firm-territory nexus, but rather seek to showcase how different economic interactions are likely to occur at different geographic scales.

The research on both GVCs and GWCs share the common characteristic that the literature—partially because of data restrictions—fluctuates between micro and macro studies (Sturgeon, 2019). We integrate them in our study. We expect different scales to present different opportunities for intersections between value and wealth, as legal and social manifestations of both value and wealth are likely to emerge at different scales. Table 1 above outlines how we study GVCs and GWCs across scales with different focus points. At the macro level, we can detect how aggregate economic activities, such as financial flows and trade relationships, occur differently across countries as an outcome of GVC and GWC structures. At the meso level, we identify for a range of corporate entities within MNEs and whether they fulfill a role mostly related to GVCs or GWCs, measuring to what extent each firm’s presence in each country tends toward value or wealth. At the micro level we study the location of managers responsible for the coordination of GVC and GWC. In terms of our distinction between the firm and the corporation (Robé, 2020), our study of GVC and GWC at the macro level is too aggregate to measure anything but outcomes of both social organization and legal maneuvering. The meso level, on the other hand, studies only the legal incorporation of entities within different jurisdictions, and therefore studies the “corporation” part of MNEs. The micro level looks purely at the social organization at the top level of the C-suite and professionals guiding the firm (see, most recently, Alvarez and Svejenova, 2022).

Firm-territory nexus operationalization.

A key factor for GVCs and GWCs is the differentiated geography in terms of institutions, in which countries provide different levels of protections for labor, environment, or other areas related to the total cost of production. For financial planning, too, GFN and GWC agree that “resulting legal–geographic fungibility is crucial to the logic of financial legal production” (Haberly and Wójcik, 2022: 49). This variation at the macro scale can be used by MNEs to plan the location of GVC and GWC entities, which are mapped onto sovereign territories according to conventional international statistical practices. Given that countries often specialize in production or finance, at this macro level we expect to see little overlap where GVC and GWC economic activity is highly concentrated in the same jurisdiction. Certainly, the standard international economic statistics, such as trade data and FDI and portfolio data, would identify jurisdictions as heavily skewed toward either GVC or GWC activities (Linsi and Mügge, 2019). Looking at the country level alone also risks falling into Agnew’s (1994) “territorial trap.” At worst such research can treat countries as empty nests and legal boxes, ignoring power relations across space and the social relations within space. Simply comparing countries makes it conceptually hard to discuss what possible dynamics exist between them (Bair et al., 2021). We look at the geography of incorporation within MNEs rather than aggregate economic activities.

The meso scale comprises of corporate entities, allowing a disaggregation of national level reporting into particular units, such as special purpose vehicles, holding companies, and other forms. This includes the creation of “in-betweener” rather than “stand-alone” corporate entities, especially for tax planning (Palan et al., 2023). The proliferation of corporate forms for financial and legal management—and wealth protection—has been noted in recent GWC-related literature, including growth in the intermediate holding companies and rearrangements of financing between high and low tax jurisdictions (Reurink and Garcia-Bernando, 2021: 1278–1279).

At the micro scale, managers in the firm coordinate with professionals to control GVCs and GWCs. While we do not map the explicit network between members of these communities, our approach is inspired by GFN and GPN literatures in terms of emphasizing the individual relationships behind global finance and production (Coe et al., 2008; Wójcik, 2013). Positionality is important for these relationships, as close physical placement, cohesive social networks, and racial and gender dynamics reinforce one another to amplify global power asymmetries (Sheppard, 2002: 318). Affinity can be important in allowing professionals to identify and learn from each other, as well as form networks of trust (Faulconbridge, 2014). Proximity is important in allowing professionals to meet regularly with clients and foster control of their activities through socialization (Beaverstock, 2004). It is at this micro-scale where legal affordances are defended, with reliance on a professional community to bolster interpretations of what is permissible and legitimate (Christensen et al., 2022; Cutler and Lark, 2022; Seabrooke and Wigan, 2022).

To study the geographical overlap, we first have to operationalize measures of both sides. This means we first need to define data points for concepts that are scarce in data (Sturgeon, 2019), as well as create ways to parse them out. There are very few standard ways to define how GVCs and GWCs can be measured geographically and our attempt here serves as a starting point to showcase different approaches to this problem.

A limitation to measuring overlap in such a data-scarce landscape is that, by design, this means we first have to parse out in different types of data what is either GVC or GWC activity. This means defining, for example, trade data to belong to GVC and financial flows to GWC, when in reality, some of these measurements are so aggregate that they likely reflect some of both (Ergen et al., 2023; Linsi and Mügge, 2019). This means that we may lose some intricacies of entanglement which cannot be measured, especially if the nature of entanglement is that it occurs through the same measurable event. Understanding entanglement more fully therefore depends also on qualitative studies (provided here in this Special Issue). Nevertheless, our operationalization provides a useful way to compare the two “sides” of MNE fragmentation and understand where and how it may intersect. We deal with the problem by measuring the relationship not just between two axes but also across scales. Accordingly, we rely on country-based statistics, corporate reporting tied to MNEs in a particular sector, and social media data on professionals from LinkedIn. Each data type has different limitations and advantages, and together therefore adds to a more complete picture than if focusing on one type of data alone. This also follows recent discussions in political economy on the need to “zoom in on concrete corporate practices and disaggregate compound statistics” (Ergen et al., 2023: 22) (Table 2).

Data overview.

Our specification of MNEs in the apparel manufacturing sector is required to reach a smaller subset of data points in accordance with the requirements of the data license from Orbis. Limiting to a smaller sample, we chose to focus on the apparel industry. This is first because things may look different for industries with substantially less production in their value chain (such as industries heavy on intellectual property). Apparel is not only well-known in the GVC literature (e.g. Barriento et al., 2016; Khan et al., 2020; Whitfield and Staritz, 2021), but also one of the most fragmented manufacturing industries (Bair and Mahutga, 2012). In the following, we present our findings in terms of the correlation between GVC and GWC measures at different scales of the firm-territory nexus.

Analysis and findings

Macro scale

Measuring GVCs and GWCs at the macro level means considering the fragmentation of the global economy in terms of value-adding production and wealth-protecting financial structures, respectively. The goal here is to show the aggregate economic activity that arises in specific locations in ways that reflect the differentiated status of countries within GVC and GWCs, and to determine to what extent these share a similar or dissimilar pattern. It could be the case that finance and trade integration are highly correlated, for example, if both are driven solely by growth or economy size. We know, however, that economies tend to specialize and that both economic and institutional features differ, not least because of legal variation across jurisdictions.

For GVCs, we locate where value-adding takes place on a quantifiable country level. Doing so has several data limitations, as is widely discussed in the GVC literature and is one of the reasons why many researchers opt for a qualitative approach (Sturgeon, 2019). One innovation for achieving such quantification has been the OECD Trade in Value Added database (Johnson, 2018; OECD, 2021a). We use data for 2015 for backwards and forwards linkages in GVCs in percent of GDP, taking the entire world as the trading partner for each country. Similar to Criscuolo and Timmis (2018), we take the average of forwards and backwards linkages to obtain a measure for each country of how central it is to global value chains.

For GWCs we measure the extent to which jurisdictions provide favorable institutional protections for finance using the Financial Secrecy Index (hereafter FSI, see Cobham et al., 2015). This index ranks economies based on their institutional capacity to act as havens for corporate or personal tax avoidance, coupled with their relative importance for cross-border financial services according to the volume of transactions. The FSI is important because it does not link financial secrecy to a list of “tax havens” declared by political entities (like the European Union, which excludes its own “tax havens”), but from the presence of regulations for secrecy and the amount of capital operating through these jurisdictions (Karhunen et al., 2022). The index consists of a combination of scoring legislation on a number of finance-related areas such as reporting requirements and then weighting each jurisdiction by its relative importance for global capital flows. Thereby it combines both the institutional features and the economic activities occurring. The index covers 112 countries and territories, but the overlap with the TiVA data (which has 64 countries) is unfortunately only 52 countries. Figure 1 maps the correlation between country values on both of these scales.

GVC-GWC entanglement at the macro scale.

Figure 1 illustrates the geographical correlation between GVCs and GWCs, using macro data at the country level. The lack of correlation shows that, in general, the countries where there is a high level of GVC integration are different from the countries that are important for providing financial GWC institutions. As can be seen, there is no correlation between these measures, and a regression using OLS yields a correlation coefficient that is not statistically significantly different from 0. The lack of overlap between international production and financial asset placement is not surprising. It can be seen as a stylized fact about the world economy (i.e. Criscuolo and Timmis, 2018), and corresponds well to the idea of “offshore” being different to “regions of production” (i.e. Coe et al., 2014). The firm-territory nexus here is then characterized by stark differentiation between GVCs and GWCs, though with notable outliers. Singapore and Luxembourg particularly stand out as having very high score on both GVC and GWC, a phenomenon referred to as “mid-shore,” when places combine on-shore characteristics with offshore services they are less likely to face the pressures that smaller, pure OFCs face (Coe et al., 2014; The Economist, 2013). These mid-shore jurisdictions may therefore act as important nodes of GVC-GWC entanglement in an otherwise fragmented economy.

Meso scale

In the next step of our analysis, we map how the firm-territory nexus looks between GVC and GWC at the meso level, looking at incorporated entities across different countries. Both GVC and GWC entities are governed with legal relationships in mind, including both ownership and contractual relations between lead firms and suppliers. These complex ownership networks are not a “legal fiction” but are deliberately designed to maximize value and wealth for lead firms (Robé, 2020). What we ask here is to what extent MNEs use different jurisdictions for GVC purposes than for GWC purposes, or if the same jurisdictions are used for different purposes, that is, a geographical overlap of GVC and GWC within MNE corporate structures.

Measuring the GVCs and GWCs at the level of the “corporation,” we use data from Orbis. We restrict our analysis to only the apparel sector to decrease the scope of the sample. We include subsidiaries for 18.343 companies in the apparel manufacturing sector with more than 100 employees and €750 million in turnover. The GWC side is defined as all subsidiaries that are financial categories within the North American Industry Classification System (NAICS), such as a holding company or a non-deposit credit institution. The GVC side is defined as all subsidiaries categorized within the non-financial categories of the NAICS system. This is a fine-grained measurement as we have data for most subsidiaries on their categorization. It measures the functional distinction, assuming financial subsidiaries are not likely to also undertake production. One limitation here is that non-financial subsidiaries may receive generous subsidies or tax incentives, which could impact GWC strategy. In such cases, our data cannot recognize parts of the MNE that look to be GVC but may also be key to GWC. Entanglement, or geographical overlap, may therefore be measured only as a lower bound in our approach.

Figure 2 shows the correlation between locations of GVC units and GWC units. Each dot represents a firm-country match, and its position on the chart is determined by the number of entities in each category. This means each country has multiple data points in the chart, as the configuration of GVC and GWC units within each country is different for each firm. If firms separate their GVC from GWC completely, then the figure would adopt an L-shape, with each firm-country match being close to the x and y axis. Indeed we do see many results along these lines, with some country-firm matches having several GVC units and 0 or few GWC units in a single jurisdiction, and vice versa. However, the findings indicate that most firms in most countries actually have a combination of both, with most of the dots in the middle of the diagram. Here, we see firms having both hundreds of non-financial and financial entities incorporated in the same locations. This indicates that there is indeed some more entanglement than indicated at the macro level. The correlation between GVC and GWC units is weakly positive, statistically significantly different from 0 at the 95% confidence level. We conclude that GVCs and GWCs are somewhat entangled geographically at the meso level, as many firms use the same jurisdictions for the incorporation of both financial and non-financial units.

GVC-GWC entanglement at the meso scale.

Micro scale

The firm-territory nexus includes the manifestation of firms within social spaces, where high-level managers and experts coordinate. MNEs’ complex networks are ultimately planned and managed through complex and open social relationships constituting the “firm” (Dicken and Malmberg, 2001; Robé, 2020). For GVCs, the firm-territory nexus consists of the spaces in which managers of MNEs are able to oversee the GVC from headquarters and use managers to coordinate relationships with suppler firms. For GWCs, the firm-territory nexus consists of the relations between the managers of the firm and the financial advisors and tax professionals who may act as consultants within or outside the firm (Christensen et al., 2022). Here, we emphasize geographical overlap and ask whether top managers in charge of GVC and GWC processes respectively co-locate. We focus the data on the level of individuals, and count their presence in world cities, where professionals interact.

The method for data collection is a novel way to retrieve data from an online professional social network, based on Garcia-Bernardo and Stausholm (2022). Publicly accessible LinkedIn data provides an opportunity to analyze professional characteristics. LinkedIn offers advertisers the possibility to target ads to certain professional demographics. By setting up an ad in the “campaign manager” we can cross boxes off for specific job titles, industries, educational background, or similar characteristics, which professionals usually make available on their profile. After specifying profile characteristics, the site identifies how many profiles fit the description (the potential audience, if we were to purchase the ad). By specifying geographic limitations in iterative searches, the site gives a number of profiles for each place. 1 We assume that the coverage for professions that are highly internationalized is not systematically skewed across countries, even if coverage is not at 100% anywhere. Garcia-Bernardo and Stausholm (2022) provides further details on how this search can be useful for studying the geography of professional groups.

Our use of LinkedIn data to locate professionals followed two steps. First, we obtained data on the GVC dimension, mapping where “CXO” (CEO, COO) executives are placed, using data from Garcia-Bernardo and Stausholm (2022). While the governance of the GVC is complex and there are many layers of decision makers, the strategic decisions are made at this level. The data is taken from LinkedIn and is available on the city level based on the reasoning that this is a more precise scale to study the location and positionality of managers. We combine the different managerial job titles to provide an overall assessment of CXO roles linked to GVC management.

Second, we want data on the GWC dimension. GWCs are characterized by needing professional expertise from tax professionals (Christensen et al., 2022; Hearson, 2018). Some of these professionals work within the firm (CFOs), whereas others are in global professional service firms and consultants (Ajdacic et al., 2020; Christensen and Seabrooke, 2022). Again, we use data from Garcia-Bernardo and Stausholm (2022), who identify a number of LinkedIn profiles with these titles by searching across cities in the Campaign Manager tool of LinkedIn. We use the absolute numbers, given that restricting to larger cities takes out some of the bias toward populated areas that would otherwise drive the results. This measure of tax professionals provides a new method to update earlier important work estimating the rise of professionals in offshore financial centers (Cobb, 1999).

Figure 3 shows our correlation of this management and tax advisors data. The X-axis shows the number of managers on LinkedIn with titles of CEO, COO, or CXO. The Y-axis shows the number of LinkedIn profiles working with wealth protection management, meaning tax advisors with titles such as Corporate Tax Director or Tax Advisor, as well as CFOs who manage the financial strategy of the firm including, but not limited to, tax issues. Each dot represents a city and the number of general and wealth protection managers that are located there, according to their LinkedIn profile. The figure illustrates a high degree of geographical overlap between the GVC dimension and the GWC dimension. Regression analysis yields a positive coefficient which is statistically significantly different from 0 at the 99% confidence level. This indicates there is a high degree of co-location between the general managers, who oversee the firm’s role in GVCs and its value-producing entities, with the managers and advisors in charge of creating the strategy and instruments tasked with optimizing the GWC. In Figure 3 the very top right corner includes cities where CXO and tax professional roles are highly concentrated, such as New York, London, Chicago, San Francisco, and Toronto. Agents in “local” networks position themselves toward each other, with these networks encouraging forms of brokerage and closure that give rewards to those recognized as powerful. This includes high-pay rewards to those in financial networks relative to managers of supply chains (Burt, 2010). We would expect to see coordination between C-suite managers and tax professionals to manage GVC-GWC entanglement. Such coordination is likely to be found in world cities (Bassens and Van Meeteren, 2015; Beaverstock et al., 1999). Our findings match well with research on how world cities, like New York, have attracted multinational enterprises to locate their headquarters in the city through favorable “governing law clauses” that benefit both GVC and GWC management (e.g. Potts, 2016), as well as through intense professional network maintenance (Kipping et al., 2019). It also conforms with research suggesting that corporate elites have become both more North American based and transnationalist (Beaverstock, 2005; Carroll, 2009), and how financialization has restructured MNEs (Morgan, 2014).

GVC-GWC entanglement at the micro scale.

Conceptualizing entanglement over scales

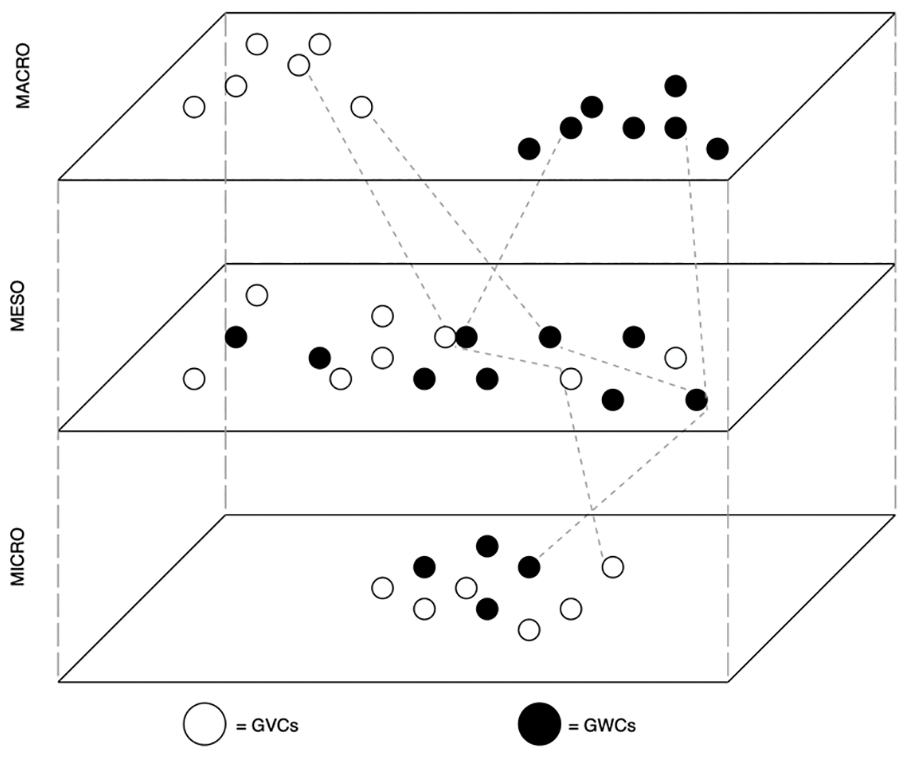

Our empirical findings show that the extent of entanglement between global value and wealth chains depends on the operationalization of the firm-territory nexus. As Dicken and Malmberg (2001) point out, territories are not boxes but rather continuums across which social and economic relations play out. In our analysis, we operationalize the firm-territory nexus across the micro, meso, and macro continuum, with these scales corresponding to different interpretations of the legal and social forms of MNEs (Robé, 2020). Our findings lead us to discuss the implications in terms of the configuration of GVCs and GWCs across scales. At the macro level, the placement of countries within hierarchies of value and wealth creation shows very limited overlap and a high degree of specialization. At the meso level, a complex network of ownership ties happens across countries in ways that are more likely to overlap. At the micro level, the individuals responsible for managing these chains are co-located in world cities. But how do these levels relate to each other?

Figure 4, below, illustrates our thinking of how the elements of GVCs and GWCs are located over macro-, meso-, and micro-scales. At the macro scale, our conceptualization of space combines the institutional features of countries with the statistical configuration of a country as a nest of aggregate reported economic activity. These may differ from how local communities experience the presence of MNE activities in important ways, but correspond to how the global activities of MNE’s can be measured and reported in comparable ways. Here, we see the specialization of countries within the hierarchies of value and wealth chains. At this meso scale, space is physical and legal, material and immaterial. The emphasis is on the mediation of productive and financial relationships according to what is legally afforded by a jurisdiction. This is the tie to the macro scales, as for example GWC units are more likely to be placed within certain jurisdictions—though not exclusively, as our results suggest. Orbis data on the apparel sector, reported above, shows a nest of GVC-GWC activity that suggested they are mixed within corporate networks.

Entanglements over scales.

At the micro scale, the figure illustrates the close proximity between managers as well as their ties to other scales, as corporations are established by the firm to exploit legal ambiguities, arbitrage, and absences for financial and legal management (Grasten et al., 2023), as well as to control production and employment relations (Khan et al., 2020). The micro level is a space where social networks benefit from propinquity, and where positionality can be asserted. Sheppard (2002) has discussed how the positionality of particular social groups can be replicated through “wormholes,” allowing professionals to connect between distant places with ease. The capacity for firm managers and tax professionals to oversee GVCs and GWCs from world cities comes from the maintenance of social networks that replicate power asymmetries. Such networks bolster selective interpretations of what firms can do with their corporate entities, allowing firms to leverage legal affordances from permissive jurisdictions with the knowledge that likeminded professionals and organizations, like the global accountancy firms, will support them (Grasten et al., 2023). Tracing how executive managers and professionals affirm their social networks and positionality is important for understanding GVC-GWC entanglements not only on production and finance, but also for labor and environmental issues. Such research builds on earlier findings pointing to how labor and production relations within MNEs are not simply dictated from the headquarters but managed through the corporate structure. Understanding how legal affordances are controlled by managers and articulated through corporate entities in different jurisdictions can shine a light on the contemporary management of environmental and labor issues in MNEs.

We have suggested that Robé’s (2011, 2020) distinction between the firm and the corporation, the former being the social organization and the latter the legal form, is important for locating how GVCs and GWCs are entangled. Distinguishing the firm rather than the corporate units has further implications for economic geography and international political economy research beyond understanding the overlap between GVCs and GWCs. The firm/corporation distinction is also useful in understanding the difference between transnational and cross-national analysis. Whereas the corporation exists as units within nations, firms act transnationally. This capacity to act and assert control comes from locations in which executive managers and tax professionals can interact at the micro scale and execute at the meso scale, which is informed by the opportunities provided by the macro scale.

Discussion and conclusion

Value and wealth both depend upon legal constructions and social organization, which tend to happen across different geographies and is best measured across a continuum of scales. We have suggested that applying the firm/corporation distinction to Dicken and Malmberg’s (2001) “firm-territory nexus” is a way to identify GVC-GWC entanglements and conduct a data search on how such entanglements may be identified. Our aim aligns with the common purpose of GVC and GWC scholarship, which is to establish who governs production and financial activities across multiple jurisdictions, and to establish the location of economic activities. For GVC literature this ambition has led to a focus on lead firms and then locating where value chain activity takes place, including distinctions between different service or production-based functions. At the macro scale, trade flow data provides data at the country level to identify how GVCs are established. For GWC literature the emphasis has been on lead suppliers of transnational financial and legal professional services, including differentiating why capital flows into what jurisdictions and for what likely purpose (tax minimization, secrecy, etc.). Data on financial secrecy, tax rates, and the scale of financial activities running through a country, provide estimates to identify how GWCs are composed at a macro scale. Seen “from above,” this national-based macro data tells us that GVCs and GWCs operate largely in separate sovereign territorial spaces.

But we know that GVCs and GWCs are intertwined, as stressed in scholarship on how their mix produces economic and social inequalities (Quentin and Campling, 2018). We have some clues on this entanglement from data at the meso scale, as given above in our example from MNEs in the apparel sector. At this scale we see “pure” GVC and GWC corporate entities—as assessed by their purpose and location—as well as a great deal of intermingling. At the meso level, corporate entities that are non-financial may benefit from favorable tax or other financial treatments. In other words, elements of GWCs are being built into GVCs. This is especially the case for financial and legal management, including for the manipulation of labor, environmental, and intellectual property issues. The financialization of MNEs does not only mean growth in the complexity and scale of GWCs (Haslam et al., 2022, and as also noted in the GFN literature, Haberly and Wójcik, 2022), but the integration of wealth protection schemes into the composition of GVCs (Morgan, 2014).

It is worth speculating whether this aligned GVC-GWC coordination is a new phenomenon, and whether it predates or has been diffused through the rise of corporate fragmentation into GVCs and GWCs. Our data does not allow us to study indicators of GVC-GWC entanglement over time. Jiang et al. (2018) have data over time, showing that “island” (tax haven) directors become more commonplace in US corporate boards. The use of tax professionals to coordinate and execute strategies for transfer pricing, is illustrative of a profession which governs GVC-GWC entanglements in practice (Christensen, 2022). We hope future work will explore further how relationships to tax expertise are copied and diffused across firms and sectors. The future of GVC-GWC entanglement is probably even more entangled across all scales. Given the changes to international tax governance, the pure GWC jurisdictions may die out while at the same time the “onshore” jurisdictions may become increasingly aggressive with respect to different types of tax incentives. This would create even more entanglement at the meso scale, requiring ever closer coordination at the micro scale and with a measurable impact at the macro scale in terms of location of economic activities.

Our tracing of data indicators of GVC-GWC entanglement over scales also has policy implications. Current European policy is to name and shame jurisdictions offering low taxes (European Council, 2021), identifying these sovereign territories at the macro scale. Examining the meso and micro scales complicates this view, showing how the location of professional practices is crucial to “offshore” behavior (Cobb, 1999; Garcia-Bernardo and Stausholm, 2022). At the macro scale, new international tax deals may minimize the differences between countries with respect to “offshore” finance (Christensen and Hearson, 2019; OECD, 2021b). GVC planning faces higher uncertainties regarding supply chains and higher frictions related to distance and transportation, which may bring production closer to end markets. At the meso level, GVC and GWC functions are likely to become even more integrated. Underpinning this activity is the micro scale, where the C-suite and professionals coordinate to run the firm by manipulating the corporation. MNE governance is, then, the establishment of micro-positions within macro-structures in which GVCs and GWCs are entangled by design. Viewing this entanglement first requires tractable data over scales. Future work can further theorization of how these scales are linked and how these linkages reflect and perpetuate power asymmetries in the international political economy.

At the macro level, the world may seem separated into regions of production and financial centers (Coe et al., 2014). If we look at the aggregate ways MNEs are structured, this separation is confirmed (Garcia-Bernardo et al., 2017), as locations of value and wealth activities follow different patterns on average. Taking a look within MNEs however, we see that the locations often overlap in practice, and ownership of subsidiaries are entangled across jurisdictions. These subsidiaries are, in turn, managed by the executive managers and tax professionals who co-locate in world cities. GVCs and GWCs are both expressions of how MNEs seek to locate and manage advantages across different geographies. Their geographic entanglement reflects how territorial scales give rise to different forms of economic organizing.

Footnotes

Acknowledgements

Our thanks to Javier Garcia-Bernardo for inspiration and collaboration. For vital feedback in the development of this paper we thank Adam Leaver, Daniel Mügge, Jean-Philippe Robé, and Crawford Spence.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Seabrooke acknowledges funding from the Independent Research Fund Denmark ‘TIME MIRROR’ project (#0217-00380B). Stausholm thanks support from the Fonnesbech Foundation.