Abstract

Over the past decade, governments have increasingly sought to mobilise private capital for expanding renewable sources of energy for the goals of decarbonisation and energy security. While existing research has focused on the financial and regulatory tools that states deploy to reduce investor perceptions of risk, scant attention has been paid to the role of knowledge infrastructures in energy finance. In this article, we address this gap by analysing how government energy models and scenarios are deployed to attract private sector investments for energy infrastructure projects. Using interview data and document analysis centred on a transnational expert network of energy modellers, we examine how government energy planning processes are reconfigured in response to new uncertainties and demands for risk mitigation from private finance. We develop the concept of epistemic derisking to capture how knowledge infrastructures are leveraged by states in efforts to mobilise private capital. Our findings show that energy models and scenarios are leveraged in efforts to reduce perceived risk less through their technical content than by what they signal about long-term stability in policy ‘vision’, consensus among energy systems stakeholders, and institutional capacity to manage change and uncertainty in energy systems. In addition, scenario outputs and project pipelines function as marketing devices within competitive financing landscapes. We explore how epistemic derisking operates within wider struggles over knowledge and authority in global energy governance. The article contributes to debates on green finance, energy futures and expertise, while raising critical questions about the limits of private finance-oriented decarbonisation strategies.

Introduction: Green State Capitalism and derisked decarbonisation

Over the past decade, the dominant approach pursued by governments to secure financing for expanding renewable sources of energy has been characterised by the use of public resources with the goal of reducing financial markets’ perceptions of various risks and uncertainties associated with investments in infrastructure projects. The energy crisis precipitated by the Russian invasion of Ukraine in 2022 brought renewed attention to this approach, particularly in Europe as it sought to strengthen regional energy security (Gabor, 2023; Ruck and Bieling, 2026). We understand this taken-for-granted logic of state-led but market- and security-oriented decarbonisation as a form of ‘Green State Capitalism’ (cf. Alami and Dixon, 2024). 1 A central objective of this approach is to mobilise capital and bank lending into energy infrastructure asset classes, which has been widely studied as tools and regimes of ‘derisking’ (Baker, 2022; Gabor, 2021; Hunt and Tilsted, 2025). Existing research has identified financial derisking tools and regulatory derisking tools as distinct types of policy instruments employed by states and otherwise promoted by multilateral development banks (MDBs) in their pursuits of decarbonisation. The former includes both monetary and fiscal instruments, such as loan guarantees, tax subsidies and power purchase agreements (PPAs), which guarantee stability of returns over time. The latter includes reforms to energy utilities markets and grid access guarantees to ensure security of transmission (Christophers, 2024; Gabor, 2021; Gabor and Braun, 2025). The assumption is that, in the absence of these efforts and investments by states and MDBs, renewable energy infrastructure developers would struggle to secure loans and investments from private sources, as they would remain relatively less profitable than alternative investments, including in carbon-intensive energy sources and forms of production (Christophers, 2024).

Researchers have long pointed to climate and energy governance as a knowledge-intensive process which involves and is shaped by complex socio-technical systems, calculative devices and specialised expert groups (Allan, 2017; Pendergrass, 2024). These knowledge infrastructures ‘comprise robust networks of people, artefacts and institutions that generate, share, and maintain specific knowledge about the human and natural worlds’ (Edwards, 2010: 17). In the context of energy system decarbonisation, relevant knowledge infrastructures include energy modelling, scenarios, transition plans, other planning frameworks and the people and agencies that produce them.

Researchers in economic geography, economic sociology and Science and Technology Studies (STS) have explored how economic models influence market structures (e.g. Braun, 2014; MacKenzie, 2008) and energy models influence energy policymaking (e.g. Aykut, 2019; Beck and Mahony, 2018; Midttun and Baumgartner, 1986). More recently, scholars have engaged with modelling practices in global environmental and energy governance, situating them within broader institutional contests over energy futures (Clift and Kuzemko, 2024; Eckhouse, 2025; Labban, 2012; Machen and Nost, 2021; Malm and Carton, 2024). However, so far the recent literature on derisking has not analysed how knowledge infrastructures in energy relate to the macrofinancial regimes within which states seek to mobilise capital for energy investment. In this article, we therefore ask: What role do government energy models and associated scenarios play in the government strategies to derisk private capital for energy system decarbonisation?

We use the term ‘energy models’ as a shorthand for the wide array of energy systems modelling families that have long been used by governments to inform energy systems planning. Energy models are used as inputs in energy scenarios, which can be understood as narrative tools that are ‘operationalised as quantified hypotheses for the evolution of key variables’ (Aykut, 2019: 17), such as changes in energy demand. Their temporal horizons can stretch from periods of years and decades, to half-centuries and centuries (Hedenus et al., 2013), and can aim at extrapolation of likely developments from existing trends (forecasting), or simulation of specific energy system changes or policy interventions (exploration), including in pursuit of specific policy objectives, such as carbon neutrality. Although our focus is on the use of energy models and domestic scenarios by governments, we note that they are also used by actors across the wider energy system and markets, including grid operators, utilities companies, consultancies, investors and NGOs for both business planning and influencing (Royston et al., 2023). Global energy models and scenarios, as well as Integrated Assessment Models (IAMs), are also developed and used by multilateral institutions such as the IPCC, the UNFCCC and the IEA, as well as fossil fuel companies that seek to shape energy markets (Clift and Kuzemko, 2024; Eckhouse, 2025; Labban, 2012; Malm and Carton, 2024; Zalik, 2010).

Using original interview data and document analysis centred on a formal transnational expert network of government energy modellers convened by the International Renewable Energy Agency (IRENA), we demonstrate how and why states wield energy systems modelling in efforts to derisk infrastructure investments. We find that governments are increasingly viewed as central to the mitigation of infrastructure investment risk, and energy modelling and scenarios are viewed as critical to this process. We term this ‘epistemic derisking’, which we define as the use of knowledge infrastructures to mobilise private capital into infrastructure asset classes. Epistemic derisking captures the strategy of leveraging authoritative knowledge to attract finance by managing risk perception. We find that the emergence of epistemic derisking as a function of energy modelling has transformed how government energy planning actors relate to economic and finance ministries, as well as to private finance. Energy models are perceived to influence the risk perceptions of investors – or perform markets – less through the technical details of the models than their capacity to signal long-term stability in policy ‘vision’, consensus among energy systems stakeholders, and institutional capacity to manage change and uncertainty in energy systems. Taken together, these dynamics demonstrate how energy modelling and planning have become embedded in Green State Capitalism. While we find some evidence from MDB and private sector actors indicating that knowledge infrastructures may have the intended derisking effect, we do not set out to systematically investigate whether epistemic derisking actually shifts investor behaviour and capital allocation. We understand it instead as a central but underexamined dimension of state strategies to mobilise private capital.

Any analysis that speaks to ‘performativity’ in economic structures must also account for ‘relations of power to perform, and the structural shaping of such relations’ (Christophers, 2014: 14). To this end, we argue that epistemic derisking is a critical but underrecognised dimension of contests over both knowledge in low-carbon transitions and ‘green’ finance – including ‘what counts as green’ (Leach, 2015) – as well as global energy futures, historically dominated by the fossil-centric imaginaries and conservative scenarios of institutions such as the IEA (Carrington and Stephenson, 2018; Eckhouse, 2025; Labban, 2012; Mohn, 2020). In foregrounding knowledge infrastructures as central to the negotiation of Green State Capitalism, our findings point to their potential for also pursuing more transformative visions of decarbonisation and finance.

The paper proceeds as follows. Credibility struggles in energy infrastructure financin section sets out how the political economy and economic geography of energy systems have been transformed through processes of liberalisation, financialisation and renewable energy integration, introducing new forms of risk and uncertainty. We explore the implications of these transformations in relation to changes in infrastructure financing, and how knowledge infrastructures become critical sites in the mediation and negotiation of risks. We then turn to research exploring how models make financial markets on the one hand, and on the role of energy models in energy policy on the other. Drawing on insights from these two literatures, we suggest that energy models and planning practices may be strategically wielded to manage perceptions of risk in energy infrastructure financing, introducing the concept of epistemic derisking. After describing our methods and data, we develop this concept through empirical research centred on IRENA’s Long-Term Energy Scenarios (LTES) Network of government energy modellers and technical partners. Then, we situate our findings in debates on the knowledge politics of energy transitions and green finance, state capacity for decarbonisation and the contestation of global energy futures. We conclude by summarising the article’s main contributions.

Credibility struggles in energy infrastructure financing

Energy systems have undergone significant political, economic and technological transformation over the past half century. In this section, we explore how changes in the structure of the energy sector, the ownership and geography of energy market actors, and the sources of energy, have rendered energy systems investments riskier and more uncertain over time. As the risk landscape changes and becomes more complex, knowledge infrastructures and expertise grow in importance. Turning to scholarship on the performativity of economic and energy models in markets and policymaking, we suggest that in the context of contemporary derisking efforts, states leverage energy models in efforts to reduce investor perceptions of risk and provide credibility of energy transition pathways.

New risks and uncertainties in energy systems

Energy governance has radically transformed through a sequence of changes beginning in the oil shocks of the 1970s. Political changes led to the retrenchment of state ownership and the disintegration and privatisation of many publicly-controlled and vertically integrated energy operators (Di Muzio, 2015). As state-owned enterprises were unbundled, market competition was introduced into energy supply chains, occurring in tandem with broader processes of financialisation in the global political economy (Christophers, 2024; Hanieh, 2024). The logic of energy governance shifted from long-term planning of fossil fuel extraction and utilisation for industrial and military purposes to short-term maximisation of shareholder value in privatised energy markets. This model of disintegrated and privatised energy market actors has largely endured until the present day, but recently it has been accompanied by the adoption of reforms to increase the share of ‘non-conventional’ renewable energy sources into the energy supply, as part of policies aiming at energy system decarbonisation and the strengthening of energy security (Baker, 2022; IRENA, 2023).

Efforts to integrate renewable sources of energy, such as solar, wind and hydropower, into energy systems present a host of new challenges and introduce new types of uncertainties into energy systems. Although the costs of accessing the energy source is negligible, capital outlays for renewable energy generation sites and production plants are often very high, and, unlike fossil fuel companies, their developers tend not to have access to cash flows to meet these investment demands (Christophers, 2024). Renewable energy production is, by its very nature, generally volatile and quite unpredictable. Electricity prices are, consequently, also characterised by high volatility. Electricity grids must also be updated to cope with both energy capacity expansion and the volatility of renewable power generation. It is primarily for these reasons that, as Christophers (2022, 2024) details, private sources of finance capital often perceive investments in renewable energy infrastructure projects as far riskier than many other types of investments, including in fossil fuel production.

These challenges are also compounded in low- and middle-income countries, where investors tend to perceive higher risks resulting from macroeconomic instability and associated energy demand fluctuations, as well as from what are perceived as weaker regulatory institutions and state capacity (Baker, 2022; Collington, 2025). Financial stability and business planning in energy systems are furthermore challenged by the growing awareness of the physical risks from climate change itself, as acute, extreme weather events and long-term ecosystem degradation exacerbate and introduce new pressures on energy infrastructure. In dealing with these physical risks, new uncertainties accrue from the costs and policy shifts of trying to prevent or adapt to climate change, which are known as transition risks (Semieniuk et al., 2021).

Renewable energy infrastructure projects rely on finance from both credit providers, such as commercial banks and multilateral development banks, and equity investors, such as institutional investors and asset managers. As Baker (2022) and Hunt and Tilsted (2025) describe, although these actors approach risk management differently, with a crude distinction being that credit providers engage more actively ex-ante to determine credit costs and equity investors engage throughout the investment lifecycle to maximise returns, the risk-return assessments of both types of investors must be compatible. Projects must first meet criteria to access loans, and this ‘bankability’ influences the costs of equity investment and, thus, overall ‘investability’ (Baker, 2022).

In this context, with efforts to integrate and expand renewable energy sources into energy systems, governments have increasingly adopted policies that aim at reducing investors’ perceptions of risk. These can include monetary and fiscal policy tools, such as the provision of public subsidies, loan guarantees and tax credits, as well as regulatory policies that create more favourable or stable market conditions, such as guaranteed electricity grid access (Christophers, 2024; Gabor, 2021; Gabor and Braun, 2025). Such derisking instruments underpin the approach we term Green State Capitalism, which has emerged as the dominant approach to pursuing green industrial strategy, and, more recently, energy security, promoted by both states across the Global North, as well as international financial institutions, such as the World Bank.

The multiplication of risks in energy systems decarbonisation and the concomitant demand to manage the risk perception of especially private investors (Hunt and Tilsted, 2025) renders knowledge infrastructures and expert actors central to efforts to understand and communicate a changing risk landscape. Knowledge infrastructures have long been critical to perceiving and governing climate change and energy systems (Edwards, 2017; Pendergrass, 2024). These infrastructures are themselves the sites of fraught contestation (Allan, 2017). For example, new financial instruments and frameworks for managing environmental and climate risks, such as impact investing or ESG (environmental, social and governance standards), have been the subject of jurisdictional struggles between different professional ecologies to establish and defend certain approaches over others (Bogner, 2024; Golka, 2024; Seabrooke and Stenström, 2023). Here, we are interested in how such knowledge infrastructures, once established, relate to the economic structures and market making endeavours of Green State Capitalism.

Despite their central role in government decarbonisation and energy systems planning, however, research has not yet explored the role of energy modelling and scenario planning in this contemporary political economic context of energy systems and infrastructure derisking. In broader terms, we view this as a crucial opportunity to reveal the ways that knowledge infrastructures are used by governments in the reproduction and negotiation of Green State Capitalism. In what follows, we demonstrate that energy modelling and planning have nonetheless been at the heart of energy systems policy and transformation historically, and posit that this suggests they likely play an important role in derisking.

Political economies of energy modelling and scenarios

To understand how energy models and scenario tools relate to derisking efforts under Green State Capitalism, we turn here to two strands of research on the role of modelling in market making and public policy. Both these literatures centre on the concept of ‘performativity’, which assumes that modelling and models are important because they actively shape social relations. Christophers (2017) distinguishes between ‘weaker’ and ‘stronger’ conceptualisations of performativity. In the case of the former, it denotes ‘generalized capacity for calculative devices and economic theories to enable certain forms of economic action to occur’ (p. 67). Stronger conceptualisations suggest that markets are themselves ‘artifacts of languages’ wherein statements by central bankers do not only describe the economy, but, in so doing, produce it (Holmes, 2013).

In general, STS scholarship on the role of energy models in policymaking has adopted a ‘stronger’ understanding of performativity. Early research explored the dynamics of energy model making, challenging the view that the variables and data used in energy models are simply technical questions and are instead ‘politically loaded when alternative possibilities are supported by conflicting interests’ (Midttun and Baumgartner, 1986: 222). Concerns about the ‘arbitrary’ choices of parameter values, such as the cost of carbon and technology cost curves, have also been a source of debate from within energy modelling communities themselves and NGOs involved in energy policy (Pindyck, 2017; Royston et al., 2023). Within this literature, the outputs of the models themselves directly influence policy design and decision-making practices by ‘bring[ing] into being the objects they describe, not just through the direct informing of policy decisions, but through the wider conditioning of the world according to authoritative scientific descriptions of it’ (Beck and Mahony, 2018: 2). In Beck and Mahony’s research, for example, negative emissions technologies are rendered plausible policy objectives through the representation of their possibilities in pathways developed by the IPCC. Others, adopting a slightly ‘weaker’ conceptualisation, explore how the authority of the models emerges by virtue of perceptions about the expertise of modelling communities, such as the Integrated Assessment Modeling Consortium, in the case of the IAMs used by the IPCC (Cointe et al., 2019).

Existing STS accounts of the performative function of energy models in policymaking nonetheless tend to abstract models from underlying economic structures and material constraints in which they operate (Mirowski and Nik-Khan, 2008). Following Christophers (2014, 2017), this points to the importance of analysing models’ performativity in the context of the (global) economic structures in which they operate. For example, the International Energy Agency (IEA) was established as a direct response to the transition from Anglo-American to OPEC dominance in energy markets ‘to remedy difficulties with how the future of energy was being performed’ (Eckhouse, 2025: 745), and its projections have continued to be a site of fraught contestation given their influence on energy market behaviour. Similarly, Zalik (2010) demonstrates how the energy scenarios produced by Shell not only reflect market dynamics, but entrench the company’s position by shaping expectations around oil scarcity and supply.

Indeed, as these latter papers also attest, energy modelling and scenario analysis are themselves not novel phenomena, and their role across space and time, and at different levels of governance historically, is indelibly related to transformations in (global) economic structures. Where scenario analysis in a broader sense has its roots in military strategic planning (Bradfield et al., 2005; Labban, 2012), the use of energy models in government energy planning dates to the 1950s, as growing energy demands under post-war processes of industrialisation spurred many states to adopt new forecasting tools. At this time, they were largely concerned with projecting rates of growth in the supply of electricity generation, which was used to inform investment decisions of state-owned energy enterprises (Aykut, 2019). Thus, in the 1970s the energy demand forecasts of France’s Commissariat général du Plan and the state-owned EDF would also form the basis of the state’s investment decisions (p. 18). Particularly following the 1970s oil crises, they came to be viewed by governments as indispensable for not only managing energy systems – as operational tools – but ensuring security of its supply as part of long-term energy planning processes. With growing interest in integrating and expanding the supply of renewable energy sources, energy models and scenarios have increasingly been used to inform domestic and EU decarbonisation plans, such as the European Green Deal and EU Climate Target Plan (Royston et al., 2023; Strachan and Li, 2021; Tsani and Kozlova, 2021).

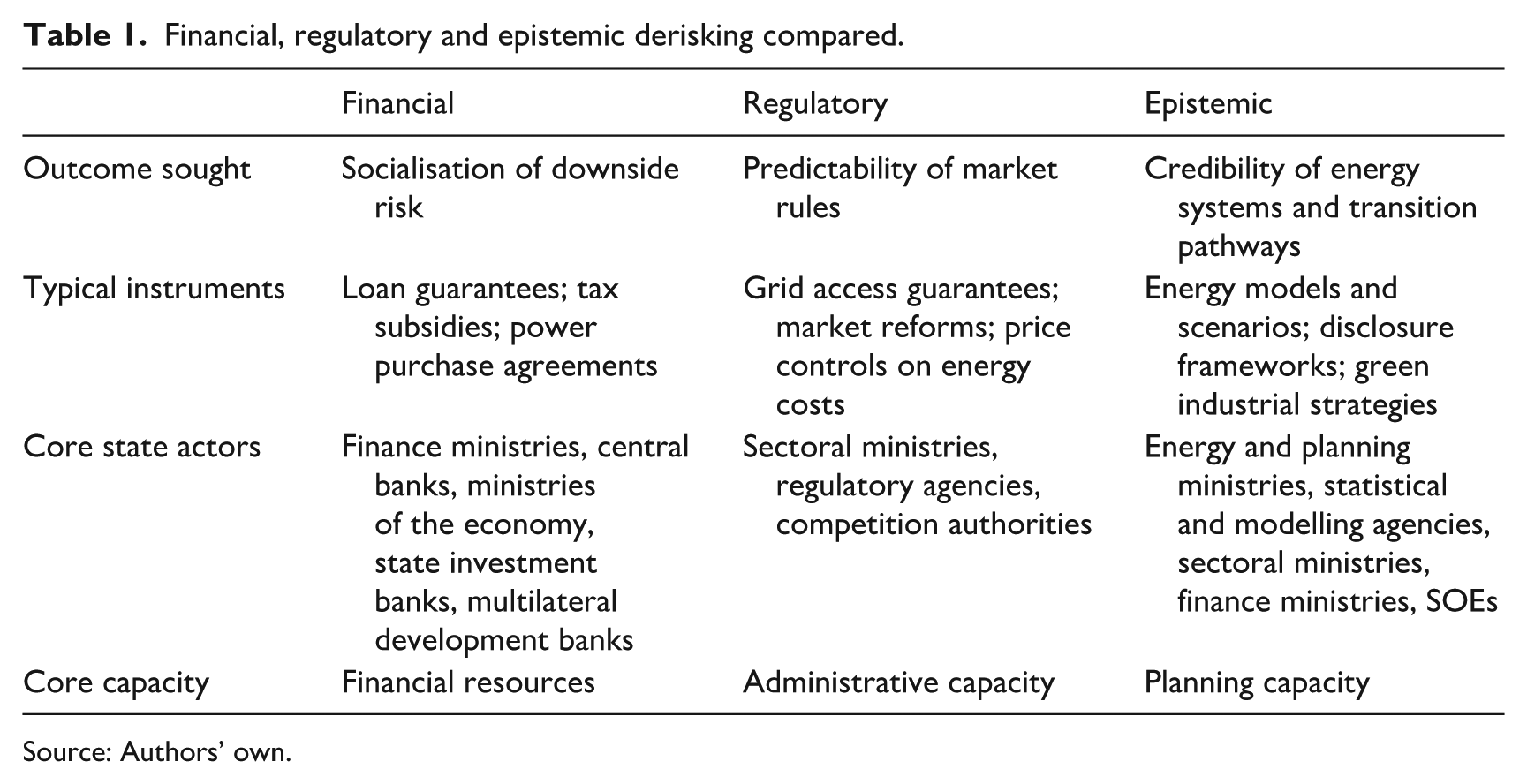

With the shift towards Green State Capitalism and contemporary attempts to derisk energy infrastructure financing, we are therefore interested in understanding how government energy models and scenarios intervene in investment decisions and energy infrastructure markets. In this way, we are also keen to unpack the ‘black box’ of performativity (Brisset, 2016): Do they perform? And if so, how? From the literature surveyed above, we theorise that, as knowledge infrastructures, they operate at the level of market expectations, coordination and credibility, and are used in efforts to reduce investor perceptions of risk. In this way, we suggest that they serve as part of the wider arsenal of ‘financial’ and ‘regulatory’ derisking tools, and we thus conceptualise the strategy of wielding energy models and their associated devices as a form of ‘epistemic derisking’. We use the term ‘epistemic’ here, because it captures the ways in which authoritative knowledge is leveraged by governments to stabilise expectations, render long-term plans credible, and, ultimately, coordinate actors across an investment chain (Cooiman, 2024). While we focus on energy models and scenarios here, we suggest that epistemic derisking tools also include other instruments, such as disclosure frameworks and green industrial strategies. Table 1 provides a summary of these forms of derisking in comparison, which will be further explored and substantiated in the coming analysis.

Financial, regulatory and epistemic derisking compared.

Source: Authors’ own.

Data and methods

Our empirical research combines in-person and online event observation, interviews and document analysis, with sampling centred on a formal transnational expert network of government energy modelling teams. Established in 2018, the Long-Term Energy Scenarios (LTES) Network is coordinated by the International Renewable Energy Agency (IRENA), and ‘provides a global platform to exchange knowledge and good practices in the use and development of model-based long-term energy scenarios to guide the clean energy transition’ (IRENA, 2025b). 2 Its members include government institutions responsible for energy modelling and the development of official national energy scenarios from 31 middle- and high-income countries, as well as 13 ‘technical partners’, which include actors involved in energy planning and financing also in lower-income settings, such as the World Bank and the Stockholm Environment Institute, the United Nations Framework Convention on Climate Change, the International Energy Agency, and 2 Chinese state agencies (IRENA, 2025b). The network organises workshops, events and webinars for members on themes and issues that members suggest are important through ongoing surveys, and also publishes reports documenting experiences of using scenarios and building institutional capacity in energy modelling for transition policy and planning.

Our engagement with the network began after one of us was invited to present previously published research at the network’s annual forum for members at IRENA’s headquarters in Bonn, Germany, and was able to observe the closed panel discussions of the 3-day event. Based on these observations, as well as informal conversations with members and network coordinators during the event, we then identified relevant experts to invite to participate in a series of semi-structured interviews. Rather than base our research solely on observations of these events, and to limit the potential bias that participation of a researcher can at times present, the analysis was primarily informed by interviews conducted by both researchers, as well as reports and webinars published by IRENA.

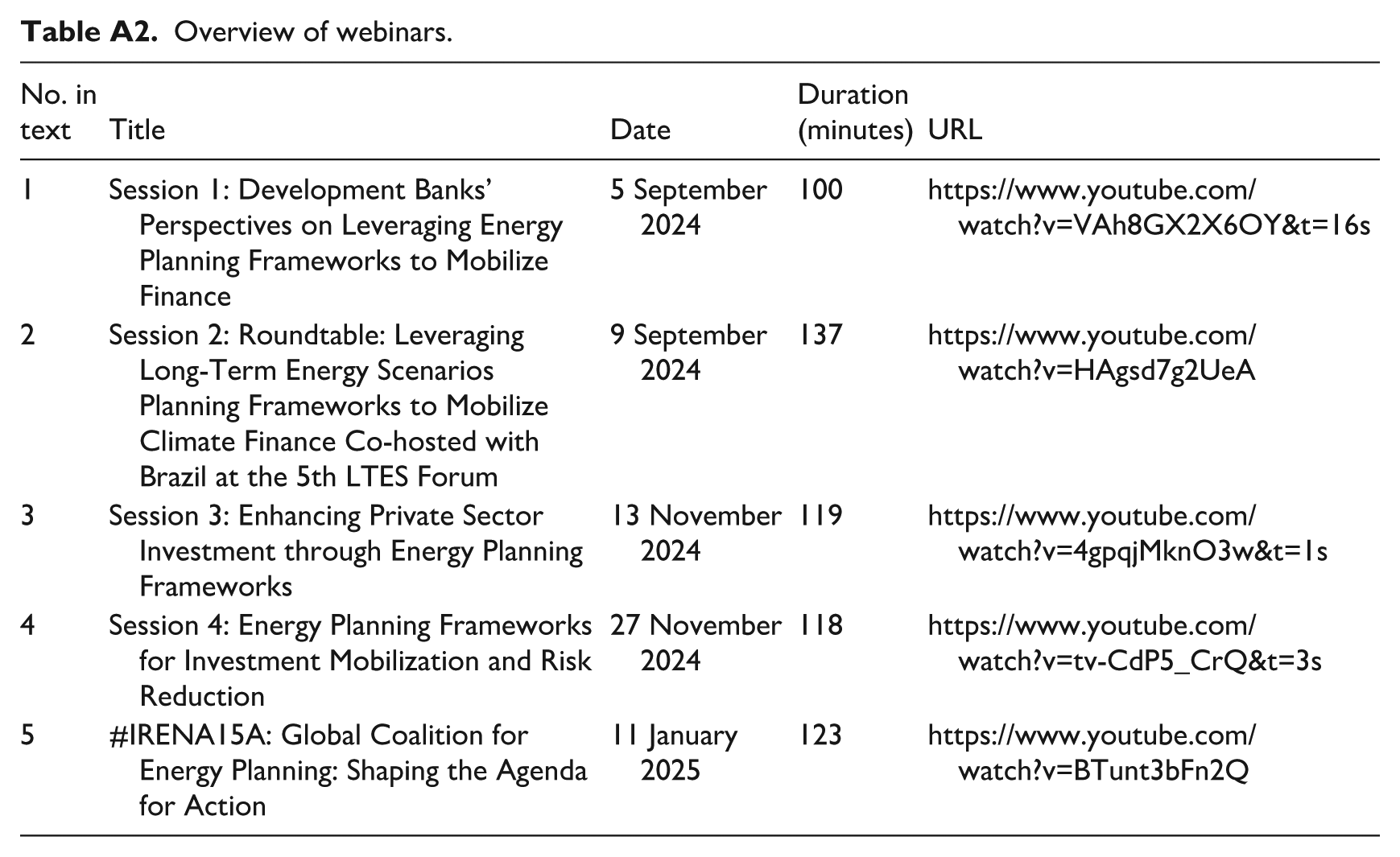

From our initial interviews, we were able to identify a further set of individuals including both government energy model developers and users, and individuals involved in the energy modelling and planning divisions of MDBs. In total, we interviewed 13 individuals across ten interviews. All interviews were conducted online via Microsoft Teams, and all participants provided informed consent. In addition to interviews, we analysed a total of twelve reports (676 pages) that were recommended by interview participants or that were identified as relevant through searches of IRENA’s publications platform. We also observed the four sessions of a publicly-available webinar series organised by IRENA on the theme of ‘Energy Planning Frameworks for Mobilizing Finance for the Energy Transition’ (IRENA, 2024), as well as a recording of a panel event to mark the launch of a new transnational advocacy network aiming to ‘promote energy planning as a tool to accelerate clean energy investments in developing countries’ (IRENA, 2025a). This Global Coalition for Energy Planning was launched by the outgoing G20 presidency in January 2025, and IRENA will serve as its secretariat. Panellists at sessions during both the 3-day forum and the online webinars also included individuals from private sector organisations involved in energy infrastructure financing processes.

All observation notes, interview and webinar transcripts, and reports were analysed in NVivo 14 using an iterative coding approach, beginning with an initial set of codes related to: (1) the organisational and technical details of how governments use energy models in relation to policy, planning and investment; (2) the functions of government energy modelling in relation to energy infrastructure investments, based on expectations from the existing literature discussion in the previous section; (3) comparisons with earlier uses of energy modelling in energy policy and planning; (4) examples of energy modelling being used in relation to energy infrastructure investments and derisking. An anonymised overview of interview participants and the time, date and duration of the interview is included in the Appendix A (Tables A1 and A2) to this paper.

Analysis

The literature explored in Section 2 points to the importance of situating the performativity of models in their broader economic and institutional context. Our analysis of how government energy models, as knowledge infrastructures, relate to the derisking of energy system decarbonisation therefore proceeds first by exploring to what extent energy models are being used towards these ends, and how that differs from extant applications. We also set out to understand how the government actors involved in energy modelling, planning and financing processes relate to each other and to infrastructure investors in this new economic context. Then, we move to an examination of why energy models are perceived to influence investor decisions, unpacking the black box of performativity and developing the concept of epistemic derisking.

The new economic and institutional context of energy modelling and scenarios

Our analysis indicates that energy modelling and scenario planning are characterised by new challenges related to the growing complexity of energy systems and the technical difficulties of integrating renewable sources. In this context, governments are increasingly viewed as central to the mitigation of infrastructure investment risk, with energy modelling and scenarios identified as critical to this process. The emergence of this new function for these tools is driven in part by demands from private sector investors, and has transformed how government energy modelling and planning actors relate to economic and finance ministries, as well as to private finance.

The creation of IRENA was itself framed as a response to the ways that ‘long-term energy and climate policy formulation and planning pose far more complex challenges than in the past’ (IRENA, 2020: 14). Our interviews and observation of online webinars gave deeper insights into the nature of this complexity: ‘. . . there is a growing level of uncertainty regarding the variables that need to be considered in the planning frameworks. Technology is changing, climate scenarios are changing, [things] are very different than what the history looks like and demand is also more uncertain’ (Arturo Alarcón, Webinar 1). While energy has always been a very ‘modelling intensive sector’, ‘in the past you could plan on the Excel, that was not such a stretch, it’s not the case anymore’ (Interviewee 6). The technical difficulties of integrating renewables is an important driver of modelling complexity, leading to a need for more sophisticated modelling tools and new skill sets for managing grid stability. One interviewee described this as a ‘change from one way of planning to another way of planning that requires more or different models that can take into account the stochastic nature of wind and solar’ (Interviewee 8), with another describing the need for ‘methodologies that can consider these type of uncertainties’ (Interviewee 7) – climate risks and technological change.

Interviewees described how, in this context, energy market actors increasingly looked to governments to mitigate risks. Governments were then turning to and adapting their existing knowledge infrastructures in the efforts to provide reassurance that energy infrastructure investment risks could be effectively managed. In other words, we found evidence of epistemic derisking. This was described as a ‘relatively new movement’ (Interviewee 4) and a ‘shift now that you’re detecting’ (Interviewee 8). As one interviewee put it, energy modelling was no longer ‘some cute science project in the corner’ (Interview 7), but was increasingly perceived as integral to the challenge of financing the energy transition. In some cases, this entailed adapting energy modelling and scenario analysis processes to directly incorporate financial information: I mean, before energy planning used to be just about that – just about energy planning, future scenarios for the power system. I think more and more what we’re seeing is countries actually getting into this space of backing their energy planning with a financial plan as well. (Justine Roche, World Economic Forum, Webinar 3)

For its part, IRENA has collated evidence of over 50 countries that have in recent years begun to integrate financial data into their energy and climate plans in efforts to attract financing (Asami Miketa, IRENA, Webinar 2). The development had not evolved evenly across governments; there were also countries that were described as having the potential to more actively use energy plans to leverage investments, but were still in the early days of acting on that ambition. For example, one interviewee described how, in Colombia, the scenarios from the national energy plan ‘are not being used enough to communicate about investment opportunities’, but it is a ‘work in progress’, with the government intending to scale up these efforts in coming years (Interviewee 2).

The shift towards epistemic derisking was described in terms of not only the growing complexity of energy systems, but also the shifting priorities of financial actors as they confront a changed investment landscape of new technologies and climate risks (Gustavo Naciff de Andrade, EPE, Webinar 2). Private sector investors described the growing importance of outputs in plans and scenarios in their investment decisions (Webinar 3). Models and scenarios could be used to technically demonstrate that there would be demand for renewable energy: ‘That provides assurance . . . [because] if it’s not needed and it’s not least cost and part of the plan, it is ultimately a risk for the financier in terms of repayment and so on’ (Interviewee 12). They were also being used by financial institutions to inform the structure of investments ‘as a way to help them assess the transition plans of their counterparties, and they’ve also started to integrate considerations from these scenarios into their credit risk ratings, which then also flow through and influence how they price their loans as well’ (Elizabeth Gillespie, Ernst & Young, Webinar 2).

Perhaps unsurprisingly, this transformation in the use of energy planning knowledge infrastructures was leading to shifts in how government actors involved in energy planning and finance relate to each other, as well as to private sector actors in energy systems and investors. Notwithstanding differences in the specific makeup of energy system bureaucracies, we offer below a generalised description of this changed institutional context.

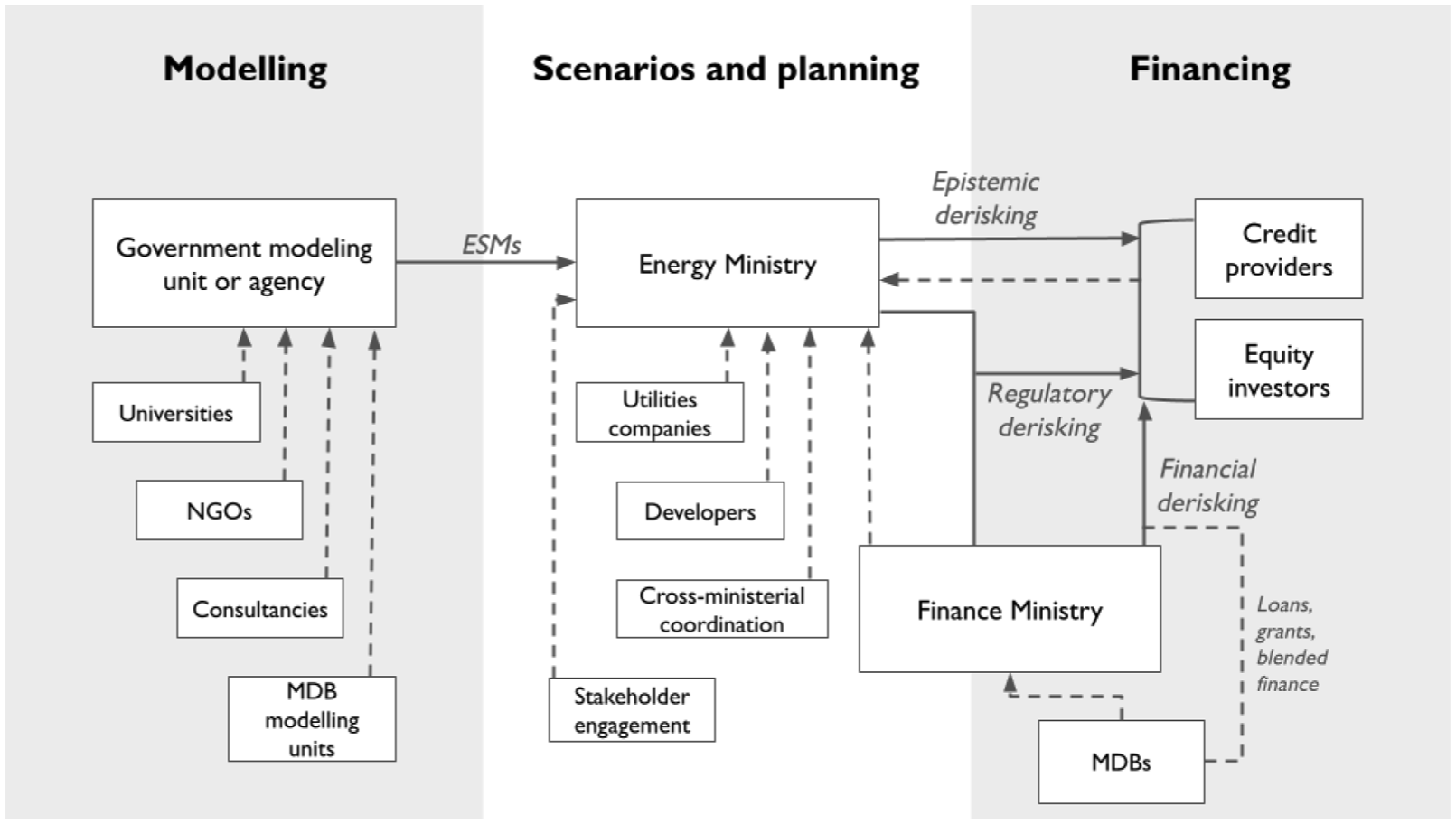

Formally, the management of modelling processes remains the responsibility of a government authority, such as an Energy Ministry or Planning Agency. In the case of most of the members of the LTES Network, the models are also developed by that authority, perhaps in collaboration with a university (Interviewee 5), though particularly in middle-income and lower-income settings, these processes also involve an NGO, such as the Stockholm Environmental Institute, a consultancy, or IRENA itself (Interviewees 5 and 7). As will be discussed in further detail in Discussion: Epistemic battlefields and the contestation of global energy future section, since 2020, the LTES has been engaged in various efforts to support the development of in-house modelling and planning capacity among its members (IRENA, 2020). A number of MDBs that provide energy infrastructure financing, such as the World Bank and the Inter-American Development Bank, also have in-house energy modelling teams, who are able to provide technical assistance to eligible countries to develop models and modelling capacity, but are not able to directly provide models or model outputs that inform domestic policy and infrastructure financing decisions (Interviewees 6 and 7).

The outputs of the energy modelling are then used to inform the development of energy scenarios. This stage of the pathway is typically the responsibility of the Energy Ministry, though the government’s Finance Ministry is increasingly involved and was described in interviews as often playing a determining role in the adoption of an energy plan. In the new context of derisking strategies, it is typically at this stage that the Energy Ministry and/or Finance Ministry first engage with potential commercial bank lenders and capital market investors and ‘dialogues on transition opportunities start’ (Tomohiro Ishikawa, Mitsubishi Financing Group, Webinar 3), with MDBs sometimes facilitating this process. In Brazil, the national development bank BNDES is typically very closely involved in scenario development and planning processes, ‘because energy planning can only be effective if the projects are developed, and the projects are only developed if they can find some financing solutions at the end of the day’ (Interviewee 5). A wider group of actors is also typically engaged through consultations and stakeholder engagement processes. These may include utilities companies and energy infrastructure developers, as well as actors and groups who may voice opposition to policy decisions, such as business associations and NGOs.

Depending on the context, these stakeholder processes may also receive both technical assistance from MDBs, NGOs and IGOs, and may also be contracted out to consultancies. At the policymaking stage, the energy plan, which typically includes a project ‘pipeline’, is developed and formally adopted. It is at this stage where the government formally commits to providing both financial instruments, such as loan guarantees and tax credits, and regulatory tools, such as grid access guarantees, to derisk investments and loans from private finance sources. If convinced by the pipeline and ‘due diligence’ of the project (Interviewee 12), the MDB will also commit to a financing mandate. Finally, at the implementation stage, if successful, equity and debt financing from capital markets and commercial banks is committed along with investments from state and MDB sources.

These relationships between the different actors and their relationship to financial and regulatory derisking are described in Figure 1. If governments are increasingly turning to knowledge infrastructures in efforts to derisk private sector investments in energy systems, why do states perceive it will work?

Relationships between government energy actors and infrastructure investors.

Opening the black box of epistemic derisking

Our analysis finds, in common with much of the existing literature surveyed above, that it was the outputs of energy modelling, and particularly their role in scenarios, rather than the technicalities of the models themselves, that were viewed as holding potential to influence private sector actors. Indeed, interviewees indicated that they don’t ‘think [private sector investors] are very interested in the details of the models and exercises, but more on the general outcomes’ (Interviewee 9). Investors ‘usually don’t care about the model, but the output of the model and what that tells them about their financial risk for that investment’ (Interviewee 8).

We were interested in gauging how, precisely, these outputs are perceived as being able to perform markets. We identified three ways in which energy models and scenarios are used to reduce private actor concerns about the risks associated with renewable energy infrastructure investments: (1) by providing a shared government vision to signal policy stability over long temporal horizons; (2) by demonstrating consensus across energy system stakeholders to signal coordination across the investment chain; (3) by signalling that the government has the planning capacity to manage energy systems change and respond to uncertainties. Beyond these three signalling effects, we also find that energy scenarios are used as marketing devices that enable governments to highlight clear investment opportunities in the context of a competitive project landscape.

Interviewees emphasised that scenarios and plans were important for articulating, in a broad sense, the government’s ‘shared view of the future and our ambition’ (Interviewee 4), ‘in general the path that the country is taking’ (Interviewee 9) and ‘what kind of long-term vision the government has, what kind of investment environment and what kind of development zones they’re looking into’ (Interviewee 10). Without this broad vision for the long-term, states would not succeed in attracting investments for specific projects within short- and medium-term plans: ‘If you don’t have that [long-term] plan, the country won’t be able to attract climate finance at all’ (Interviewee 9). Scenarios and plans are used to reduce investor concerns about political risks resulting from a change in government policy, which, as discussed earlier, are generally considered to be a source of higher capital costs for energy investments in lower- and middle-income settings (IRENA, 2024; World Bank, 2023).

In the context of the highly disintegrated structure of energy market actors, the existence of energy model outputs and scenarios were viewed as evidence of a planning process that signalled coordination across actors involved in the investment chain. Interviewees consistently stressed the importance of modelling and planning processes for attracting investment: ‘We always say that it’s not about energy plans; it’s about energy planning’ (Interviewee 4). Functionally, these processes enabled states to build consensus, align policies across government institutions and wider energy systems stakeholders (Interviewees 2, 4, 5 and 10; IRENA, 2020), and identify financial and regulatory ‘bottlenecks’, as well as derisking tools for responding to them (Interviewee 12). But most crucially, in so doing, they enable governments to demonstrate to investors that they have been able to coordinate energy market stakeholders across the public and private sectors. This was deemed central to the ability to ‘attract investments and reduce risks because there is consistency across these different institutions and they’re all involved in the plan from these institutions around the plan’ (Interviewee 11): I think the process aspect is definitely important in terms of giving the financier not just the assurance that it’s a least-cost project on the transition path, but also that there’s a certain ownership that this project is going to have some kind of broad-based political support and that also affects the risk or reduces the risk, I guess, of getting engaged with such a project. (Interviewee 12)

Beyond signalling consensus among stakeholders, energy model outputs and scenarios, as evidence of planning processes, also signalled that the government had the necessary capacity to respond to not only energy system changes, but also political, technological and economic uncertainties associated with their development. As one interviewee succinctly put it, capturing these performative effects of planning processes: ‘Planning can really also be a process for indicating that there’s planning’ (Interviewee 10): The process is the important thing, right? And showing an integrated, well aligned process is very important in that it reduces political risk . . . It makes the investment less risky – that’s the one thing we definitely agree on. (Interviewee 10)

Interviewees viewed that evidence of a ‘planning culture’ (Interviewee 6) within the responsible government agencies would help to signal the government’s ability to manage long-term energy systems changes. Although our research did not indicate directly that the epistemic authority of the modellers as an expert community was critical to investment decisions, we did find that how government energy institutions were perceived might be important. In general, agencies responsible for energy modelling needed to maintain a reputation for political independence and technical expertise (IRENA, 2020). One interviewee described, for example, how the reputation of the Mining and Energy Planning Unit as a ‘technical institution, an independent institution’ had proved pivotal in the government’s ability to demonstrate growing demand for renewable sources to the energy sector and financial markets, where previous attempts by the Environment Ministry had proven unsuccessful (Interviewee 2).

These signals, ultimately, are perceived to reduce investor concerns about risks of policy change, miscoordination between actors, and institutional capacity. Although not necessarily a form of epistemic derisking, we also identified a further important way that energy model outputs and scenarios influence markets more directly. Energy plans needed to include a clear ‘pipeline’ of specific energy projects to be considered for investment (Interviewee 12). This was not just important for the signalling effects described above, but because these pipelines serve more directly as ‘marketing’ devices that governments can use to promote specific projects to investors. Both MDBs and private sector investors emphasised the importance of this communicative performance in the context of a competitive project landscape for limited project financing: Whoever can make the clearest case and run the fastest is who wins. I mean that’s how allocation works. We don’t have perfect information to know what are the best projects and to hold out for giving concessionality where it’s the best place to put it. So, it is a first-come-first serve beauty pageant type of way, in that the most beautiful that comes the fastest, they get the money. And so you can imagine, from a country’s perspective, if they can become the most beautiful and move the most quickly, they will be able to take more of that concessionality pie. (Interviewee 7) What the private sector, what we are looking for, is not just the energy plan, but it’s more about marketing, right? So I hope those that are involved in energy planning will not just say, here’s energy planning and let’s wait whether the private sector wants to finance it or not, but you need to sell your story so that banks or asset managers will be excited with the opportunities . . . Without selling, there are so many opportunities out there and we may not be able to capture all of them. (Tomohiro Ishikawa, Mitsubishi Financing Group, Webinar 3)

In summary, our analysis demonstrates that government energy models and scenarios have been reconfigured within a new economic and institutional context in which states are increasingly expected to mitigate infrastructure investment risks and actively engage with financial actors. Within this context, these knowledge infrastructures operate as central instruments of epistemic derisking. Their intended effects rest less on the technical details of the models than on their capacity to signal long-term stability in policy ‘vision’, consensus among energy systems stakeholders, and institutional capacity to manage change and uncertainty in energy systems. In other words, it is hoped that they will stabilise investor expectations – not by reducing risk in any objective sense, but by helping to produce an appearance of coherence, planning capacity and strategic direction.

The term epistemic derisking implies that strategies that are ‘epistemic’ in the sense that they deploy knowledge infrastructures, and they ‘derisk’ because the overt goal is to mobilise private capital into infrastructure asset classes. At the same time, scenarios and project pipelines function as marketing devices that render investment opportunities visible and competitive within crowded financing landscapes. We suggest that it not only informs policy decisions, but likely accomplishes a ‘wider conditioning of the world’ through ‘authoritative scientific description’ (Beck and Mahony, 2018: 2). Taken together, these dynamics demonstrate how energy modelling and planning have become embedded and influential in Green State Capitalism, complementing financial and regulatory derisking tools by mobilising authoritative knowledge with the goal of facilitating the flow of private capital into renewable energy infrastructure. We propose that epistemic derisking efforts may also involve other knowledge infrastructures, such as geospatial tools, disclosure frameworks, industrial strategies, as well as modelling and scenario tools used to inform multi-sector Nationally Determined Contributions plans and green transition strategies. Our findings point to broader implications for how knowledge infrastructures become sites of political contestation, and how state planning capacity is mobilised in struggles over energy futures by global energy governance actors, which we now turn to in the following discussion.

Discussion: Epistemic battlefields and the contestation of global energy futures

Building on our analysis of epistemic derisking as a central mechanism in contemporary energy finance and governance, this section situates our findings within wider debates on knowledge politics, state capacity and the contestation of global energy futures.

Epistemic derisking speaks to scholarship that characterises low-carbon transitions as ‘epistemic battlefields’: sites of intense contests between knowledge forms and infrastructures, where transitions are viewed as deeply uncertain and risky endeavours and expert authority is a strategic asset. Epistemic battles in low-carbon transitions ultimately address the question of ‘what counts as green’ (Leach, 2015), which identifies that climate mitigation and adaptation goals and outcomes, as well as the processes that bring them about, are definitional concerns. While other political logics are certainly at play in transitions, including existential or distributional politics (Aklin and Mildenberger, 2020; Colgan et al., 2021), these knowledge conflicts are staged by a deeper-lying knowledge infrastructure that makes climate change and other environmental concerns politically legible in the first place, and are themselves a terrain for political engagement (Allan, 2017; Edwards, 2017). For example, climate change cannot be understood without a planetary apparatus for observation and modelling, but the scenarios and images produced by this apparatus can be tied to different political strategies (Pendergrass, 2024). Similarly, epistemic derisking cannot function without the knowledge infrastructures that make energy systems legible through models and scenarios, but whether and how these succeed in derisking private investment likely depends on how expertise is embedded in broader political strategies to build credible transition pathways connecting public and private actors.

Recent scholarship in political economy and economic geography has begun to study the epistemic battlefields of the green transition in various areas, building new insights on the crucial role of knowledge politics. As countries move from climate commitments to implementing industrial and energy system decarbonisation, expert authority shifts from transnational scientific bodies to domestic, hybrid expert networks, bringing new actors and knowledge forms into conflict (Frandsen and Hasselbalch, 2024). Private consultancies are increasingly moving into the provision of ‘climate services’ and sustainability consulting, which they have identified as a growing business area (Christensen and Collington, 2024). Green finance, too, is defined by struggles over expertise in developing and diffusing appropriate environmental standards (Seabrooke and Stenström, 2023; Sharma and Babić, 2025; Stenström, 2026), to the extent that some argue it is most productive to study the politics of green finance primarily as a contest over knowledge (Taeger et al., 2025). As climate change continues to worsen, we can only expect epistemic battles to intensify with growing societal demands for urgent mitigation and adaptation initiatives. Epistemic derisking contributes to this scholarship by theorising the connection between knowledge infrastructures, expert authority and private capital markets as a decisive parameter of Green State Capitalism and an important site for the study of expert coordination and conflict.

Although we have identified that MDB and private sector investors within IRENA’s orbit are using energy modelling outputs and scenarios in their investment decisions, this article has not attempted to systematically evaluate to what extent it changes investor behaviour. Government energy modellers and MDB staff, as well as private sector investors within IRENA’s orbit, were generally optimistic about the potential of using models in this way, but the empirical record of Green State Capitalism over the past decade arguably points to the need to be cautious about claims that such tools will succeed in closing the ever-widening global financing gap for the energy transition. Future research might set out to demonstrate more precisely the extent to which, and under what conditions, epistemic derisking influences investor decisions, perhaps through the development of process tracing case studies in countries that existing expert networks, including the one we focused on, identify as having relatively advanced modelling and planning capacity, such as Brazil.

Our findings do complicate the critique that by transferring risk to the state and outsourcing energy system development to markets, derisking necessarily renders states vulnerable to neocolonial extractivism through the hollowing out of public institutions (Gabor and Sylla, 2023: 1189–1190). Epistemic derisking is intensely capacity-hungry, requiring expert modelling units, interoperable databases, stakeholder engagement processes and the bureaucratic authority to convene them (Collington, 2026). Many governments, often with support from MDBs and NGOs, are rebuilding and in-sourcing rather than shedding technical expertise in their efforts to create credible energy system scenarios and multi-sectoral green transition strategies. Other governments outsource energy modelling and strategies to private consultancies, which can be seen, for example, in McKinsey’s involvement in Chile’s green hydrogen strategy (Collington, 2025). This raises an important distinction in epistemic derisking between cases where states own and develop their own knowledge infrastructure for energy systems modelling (strengthening state capacity) versus cases where this is privatised out (weakening state capacity). While both approaches are examples of epistemic derisking, we propose that particularly in higher income countries, state ownership of the energy planning system – including its knowledge infrastructure – likely sends stronger signals to investors, because state ownership is perceived as a marker of state capacity and, hence, lower risk. In lower income countries, conversely, outsourcing knowledge infrastructures to actors perceived by investors as credible sources of authority may function more effectively for epistemic derisking.

We suggest that in-house capacities could also be redeployed in pursuit of more transformative visions of decarbonisation and financing strategies. For example, if the ambition of the ‘Big Green State’ (Gabor and Braun, 2025) or ‘green economic planning’ (Ban and Hasselbalch, 2025) is to democratise and socialise investment and returns in the energy transition (and otherwise), modelling and planning could play a crucial role in both informing public and expert debate on energy policy decisions and enabling the state to pursue more genuine and equitable forms of decarbonisation. The very tools designed to reassure finance capital could strengthen the state’s ability to govern, coordinate and discipline energy markets and infrastructure finance, even as they fail in their current objectives to reduce investor concerns. Whether that potential is realised remains, of course, a political challenge.

We also argue that the promotion of epistemic derisking by IRENA must be situated within broader global contests over energy futures, currently dominated by IEA and OPEC, both of which have historically been overly pessimistic on renewables (Carrington and Stephenson, 2018; Eckhouse, 2025; Mohn, 2020). IRENA was founded in part as a response to the IEA’s longstanding pessimism towards renewable energy (Van de Graaf, 2013). Its own energy models, while certainly more optimistic about the potential of renewable energy expansion, nonetheless have relatively less political and institutional heft, limiting their influence on energy markets. In light of this, the LTES Network could be understood as a (counter-)strategy for building legitimacy for IRENA’s own vision of renewable energy expansion through state-led epistemic derisking of capital for energy infrastructure, building a coalition of government energy modelling agencies and seeking to strengthen their institutional capacity to achieve this. Such direct and practically oriented forms of ‘situated learning’ (Broome and Seabrooke, 2015: 956–957) might be viewed by IRENA as holding more promise and ability to move markets than trying to contest global energy projections head-on with their own models. In this way, solving practical challenges for member governments also helps IRENA gain legitimacy and higher standing with its stakeholders (Van de Graaf and Colgan, 2016).

Conclusion

Our article has explored how knowledge infrastructures in energy planning relate to the macrofinancial regimes within which states seek to mobilise capital for energy investment. Specifically, we asked how energy modelling and scenarios are deployed in the political economic context of energy systems and infrastructure derisking under Green State Capitalism. By combining insights across literature on the political economy of energy with the performativity of modelling, we theorise epistemic derisking as a distinct type of derisking which deploys knowledge infrastructures to attract private finance by managing risk perception across the investment chain. We empirically substantiate epistemic derisking through analysis of interviews, documents and webinars, centred on a network of government energy modellers. Our findings contribute not only to debates on the political economy of green finance and energy infrastructure, and the use of models in global energy and environmental governance), but also, we hope, to the emerging stream of scholarship on expert authority and conflict in Green State Capitalism, as well as more normative visions of equitable and transformative energy futures. Beyond exploring the effects of epistemic derisking on investor behaviour and state capacity, future research might also build on the emerging scholarship on green state planning to compare how modelling units interact and coordinate with other state agencies involved in green industrial policy across different geographies (Ban and Hasselbalch, 2025; Collington, 2026). By foregrounding knowledge infrastructures as a distinct lever in Green State Capitalism, the paper widens the analytical lens on how governments attempt – successfully or otherwise – to mobilise private finance for the energy transition and, increasingly, energy security. We hope that interrogating these dynamics also creates opportunities for asking the deeper political questions of who gets to plan, finance and govern the decarbonisation of our economies.

Footnotes

Appendix A

Overview of webinars.

| No. in text | Title | Date | Duration (minutes) | URL |

|---|---|---|---|---|

| 1 | Session 1: Development Banks’ Perspectives on Leveraging Energy Planning Frameworks to Mobilize Finance | 5 September 2024 | 100 | https://www.youtube.com/watch?v=VAh8GX2X6OY&t=16s |

| 2 | Session 2: Roundtable: Leveraging Long-Term Energy Scenarios Planning Frameworks to Mobilize Climate Finance Co-hosted with Brazil at the 5th LTES Forum | 9 September 2024 | 137 | https://www.youtube.com/watch?v=HAgsd7g2UeA |

| 3 | Session 3: Enhancing Private Sector Investment through Energy Planning Frameworks | 13 November 2024 | 119 | https://www.youtube.com/watch?v=4gpqjMknO3w&t=1s |

| 4 | Session 4: Energy Planning Frameworks for Investment Mobilization and Risk Reduction | 27 November 2024 | 118 | https://www.youtube.com/watch?v=tv-CdP5_CrQ&t=3s |

| 5 | #IRENA15A: Global Coalition for Energy Planning: Shaping the Agenda for Action | 11 January 2025 | 123 | https://www.youtube.com/watch?v=BTunt3bFn2Q |

Acknowledgements

We are grateful to the three anonymous reviewers for their constructive engagement with the manuscript. We would also like to thank our colleagues at the Organizations, Markets and Governance Research Group at Copenhagen Business School, in particular Cornel Ban, Søren Lund Frandsen and Eleni Tsingou, as well as participants in the STS Section Research Seminar at Danish Technical University and Finance and Society Conference 2025, for valuable feedback and discussion as we developed the paper.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Velux Foundation and Villum Foundation projects #37102 and #39017.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.