Abstract

The concept of ‘finance’ or the ‘financial system’ can be confusing. The assumption is that the financial system consists of related markets trading in a variety of financial instruments that are ultimately of a similar nature. In the late-19th century, however, financial assets have bifurcated into broadly two classes of property titles: incorporeal assets and intangible assets. This article argues that interrelations between the two classes of assets have generated pro-cyclical trends that are not dealt with by current regulation. It argues that these pro-cyclical trends can be even more confusing in the age of globalisation.

Introduction

Analyses of the current and ongoing crisis in the world can be divided broadly into two groups. The first group considers the crisis to be essentially a financial crisis. The causes, and hence the solutions, of the crisis are traceable largely to lack of financial oversight, wrong incentives, problems of governance and fraud, and so on. The second group seeks to understand the crisis in structural terms as either the crisis of neoliberal capitalism or the crisis of global capitalism, or possibly a geopolitical crisis that manifests itself, like the one experienced during the 1930s, first as a financial crisis, then as an a structural economic crisis, but also as a hegemonic crisis (Nesvetailova 2010, Shiller 2008).

Proponents of the second set of theories present structural interpretations of the crisis. They have tended to emphasis growing inequality in the world, both between and within countries, as a major cause of the crisis (Crotty 2008; Wade 2008). The argument is that the slowing growth rate of real wages in the USA and Europe is the core structural cause for the crisis. As wage growth stalled from about the 1980s in the USA and from the 1990s in the European area, effective demands stalled as well. For reasons that are better understood today, the financial system was able to bridge the growing gap between supply and effective demand by generating ever more sophisticated and obscure credit instruments. But as these credit instruments were largely built upon each other, the system had to collapse eventually like a house of cards. The sub-prime market in the USA triggered the collapse for two related reasons. First, by the year 2007 the first tranche of ‘teaser’ sub-prime mortgages were transformed into their long-term full rates of interests. Many borrowers were unable, as was known from the start, to pay back the full rate of interest, let alone the capital, on those subprime mortgages. Second, the situation was exacerbated as the USA began to raise federal interest rates in 2007. What unfolded, then, was not a simple contagion effect, but rather the collapse of a gigantic Ponzi that was erected through ever more obscure derivative instruments erected on an original Ponzi in the subprime market. Once one card was pulled from underneath, the entire building collapsed. As Bryan and Rafferty (2006) argue, derivatives are perfect instruments of ‘market hoping’, and they can bring down two apparently entirely separate markets with one financial instrument. Hence, they proved perfect instruments of contagion.

I agree with the above thesis. I would like to link the causes of the crisis, however, to another deep structural development that emerged even earlier in the 20th century: the rise of intangible assets, and particularly what is known in legal and accounting jargon as ‘goodwill’. My argument at this point is conceptual, and suggestive. My thesis is that there are inherent pro-cyclical qualities to a capitalist economy that is founded on what John R. Commons called futurity, which renders modern capitalism inherently speculative. Furthermore, the pro-cyclical qualities were exacerbated under the conditions of globalisation. Third, and related to this, the policy debate is founded on implicit and sometime explicit assumptions that policy-making processes are based on scenario planning: once a future scenario is agreed upon, it is up to the policy-making apparatus to be courageous enough to opt for the right policy. I would tend to assume that future scenarios are produced largely as linear projections of past. Certain groups that have managed to wrest some power, such as economists in this case, will tend to dominate ideas about the future based on projections of theoretical frameworks. But most crucially, the state will tend to pursue certain policies not because they are considered to be the right policies, but because they are relatively easier to pursue than others. I tend to view what we call neoliberal policies, which dominated the agenda from the early 1980s to the turn of the century, as one type of such policy choices. They were chosen less because of the tremendous power of some unified global elites or a transnational ruling classes, joined together by a powerful but erroneous ideology, than because in conditions of sovereignty and sovereign equality, they were relatively easier to pursue than the more difficult, collective-action nightmare that would be required in order to achieve global synchronous policies between demand and supply.

This is a good opportunity to make a link with the theorising of modern capitalism that regulation approaches have developed. Finance plays a key role in the regulationists’ interpretation of the Fordist and post-Fordist eras. As Aglietta indicated, the financial system and government monetary policies were ‘a second line of defence to guarantee the durability of growth’ during the ‘golden era’ of Fordism (quoted in Dunford 2013: 147). The neoliberal era is associated, in contrast, with the erosion of the capacity of the nation-states to ensure social cohesion and the failure to put in place new mediation mechanisms. The rising power of financiers and rentiers, and their ability to take precedence over manufacturing capital, is key to this understanding. The neoliberal era is inherently crisis prone. The regulationist critique centres on the breakdown of the virtuous forms of national regulation and the rise of ‘Strict financial criteria compelled them to maximise short-term equity values and to bear down on terms and conditions of employment and wages’ (Dunford 2013: 148).

I have no problem with this assessment. But I have serious doubts about the idea of some ‘golden era’ in which finance was harnessed to social needs, in contrast with the bad era of neoliberalism which was really, the liberalisation of finance from the production needs of society. It is a good normative argument, based on the Marxist distinction between different spheres of capital – productive, commercial and finance. The evolutionary institutionalism of Veblen, Commons and Minsky never subscribed to such a distinction. They thought, in Gary Dimsky’s words, that ‘the capitalist economy has a financial aspect at its root’ (Dymski 1991: 2). In other words, productive or commercial capital is not less interested in the pecuniary value of capital than is ‘financial capital’; indeed, they all treat their assets as financial. That meant that in practice, ‘ownership rights in productive assets are embodied in long-lived, alienable nominal contracts or claims. So any individual’s wealth is more properly measured by the market value of her net assets than by the value of the “real assets” to which those paper assets correspond’ (Dymski 1991: 2). It also means that accumulation, if this is the right word, ‘takes the form of maximizing the value of nominal assets’ ownership entities’ (1991: 2). A key aspect of modern capitalism is the various techniques and the manipulation that are aimed at maximising the value of nominal assets’ ownership entities. The evolutionary story is how the nominal values of intangible assets increasingly shaped the dynamics of modern capitalism.

The article begins by presenting a brief history of goodwill accounting. I follow with a section that describes the link between Jan Toporowski’s theory of capital asset inflation and pro-cyclicality. I conclude with an argument that pro-cyclicality has been exacerbated during the era we call ‘globalisation’.

Incorporeal and intangible assets

The concept of ‘finance’ or the ‘financial system’ can be confusing. The common assumption is that the financial system consists of related markets trading in a variety of financial instruments that are ultimately of similar nature. In the late-19th century, however, financial assets have bifurcated into broadly two classes of property titles: incorporeal assets, such as credit and debt instruments that were traded in markets and were recognised as a distinct class of property titles by economists from about the mid-19th century, and intangible assets that reflected very broadly any other possible income that could not be accounted for either by tangible assets (e.g. machinery, etc.) or incorporeal assets. Now, some economists still think of both categories as being one incorporeal category in the sense that both are indeed not corporeal. But to its merit, US law, for instance, distinguishes between two sets of assets: incorporeal, which can be thought of as strictly financial assets, and intangible, which, as we will see below, refers to individual or corporate entities’ ‘goodwill’ value.

The concept of intangible property and goodwill has a long, venerable history in common-law countries. The concept can be traced back to the court rulings of late-16th century England. Modern economic historians have demonstrated that, oddly perhaps, In the English context a credit economy arose prior to a monetary economy (Muldrew 1998). British courts recognised early on that one’s access to credit was closely linked with one’s ‘good name’ in society (Allan 1889). If a person tarnishes the good name of another person unjustifiably, that person may be denied access to credit. The injured party may have monetary recourse to compensate for such damage. Similarly, in early rulings, it was not unusual for, say, a pub owner who felt aggrieved at being falsely accused of serving bad beer to use the courts to recover some of the losses.

British courts accepted, therefore, the important philosophical idea that individuals possessed some intangible qualities that they ‘owned’, and furthermore, that such qualities had monetary value. The courts described good-name assets as ‘good will’ and placed monetary value on goodwill – although to the best of my knowledge, they never developed a systemic technique for evaluation of the monetary value of goodwill. Libel laws were developed in this context as well. The number of cases that involved goodwill rose steadily during the intervening centuries.

By the late-19th century, businessman and the courts in the USA and the UK increasingly recognised that companies may have created a reciprocal ‘goodwill’ value among prospective clients by impressing upon them the quality of their products. The law of trademarks and trade-names was developed initially as an attempt to protect the consumer against the ‘passing off’ of inferior goods under misleading labels. Increasingly, writes Felix Cohen in the appropriately entitled article, ‘Metaphysical nonsense and the functional approach’, the courts have departed from any such theory and have come to view this branch of law as a protection of property rights in diverse economically valuable sales devices (Cohen 1935: 814). It was also recognised that companies could signal quality or other ‘attachment’ of consumers to certain products such as brand name recognition, trade mark and logos (Hopkins 1900).

The law was brought to bear, in such cases, to protect intangible values that companies worked so hard to build. US courts, in particular, were prepared to recognise as well that management skills, organisational skills and so on were ‘goodwill’ assets, held by individuals and companies. The US courts also accepted the proposition that state laws and regulations may have impacted on the current and future profit-earning capacity of businesses. For instance, the interstate railway regulations could impose upper-sealing on cost of freight, which in the monopolistic conditions of the late-19th-century US railway system might lead to income reduction by the railway company (Commons 1919). The courts would therefore adjudicate the cost and penalties new state regulation would impose on such companies, and provide compensation to the injured parties. The injured parties might be the railway company or indeed, the public – an idea that paved the way for subsequent anti-trust rulings. The courts’ decisions were based on the principle of fairness, liberty and so on. But in doing this, the courts recognised that companies as well as their clients ‘owned’ something that they did not strictly possess: future profits.

Intangible assets and goodwill were given monetary value on three occasions: first, value was placed on intangible assets by the courts in their rulings on cases such as the one described above – for example, in disputes between railway companies and states. In such rulings, the courts would seek to calculate the impact of regulation on businesses as ‘going concerns’, and would include future profits in the equation (Commons 1961).

Second, goodwill and intangible value were introduced in the many mergers, trusts and combinations that have proliferated in the late-19th-century USA. It was recognised that the different parties to a merger or ‘trust’ brought into the combined enterprises something more than the physical assets they owned: they also brought their ‘goodwill’, and expected to be compensated for it. For instance, in the case of the merger of the United States Leather Company in 1883, the largest company by capitalisation at that time (larger even than Standard Oil), the new merged company was capitalised at US$131,000,000, which was estimated to have been roughly 1 per cent of US GNP that year (Dewing 1930). Of that figure, exactly half was capitalised goodwill, or half of 1 per cent of US GNP in 1883. In the case of the formation of the US Steel Trust of 1901, the new trust was capitalised at US$1.4 billion, of which half again, or US$700 million, was capitalised goodwill. Nominal US GNP in 1901 is calculated as having been US$21.47 billion (Balke & Gordon 1986), and hence, according to these calculations, the US Steel Trust was capitalised at 6.5 per cent of US GNP in 1901, of which goodwill amounted to 3.2 per cent of US GNP. These are serious figures.

The practice from the 1880s to around the 1920s was to differentiate between two classes of shares: first, ‘preferred shares’, which would normally represent the replacement value of the assets that were brought into the merged business. They represented, in other words, more or less the assumed corporeal value of the enterprise. ‘Common shares’, in contrast, represented what was called at the time, the ‘entrepreneurial value’ of an owner’s contribution to the enterprise, or ‘goodwill’. Preferred shares would normally have a guaranteed dividend value of 7 per cent per annum (Kemper 1921), which was accumulative (although in the case of United States Tanners, it was 8 per cent per annum). 1 The new industrial preferred stocks constituted, therefore, a definite class of financial instruments (Kemper 1921: 55). Preferred shares were seen (and were treated at the time), therefore, like bonds (see Dewing 1930, Kemper 1921 for discussion). The United States Leather Company preferred shares were trading at much higher value than its common shares. Initially, they were traded at $60 per share, declining swiftly to $40, whereas the common shares traded initially at $5 a share. But for a brief period in 1899, the value of the common share of the United States Leather Company rose briefly to above $40. In that very brief moment, most of the common shares were disposed of by their original owners.

I am presenting the examples of the United States Leather Company, but all the large mergers in the USA from 1880 onwards had a large goodwill component. Kemper Simpson calculates that on average, the goodwill value in such mergers amounted to 40 per cent of the capitalisation of US companies (Kemper 1921). I estimate the amount of goodwill generated in such mergers in the USA around the turn of the century as being about 3 to 4 per cent of US GNP per annum. Clearly, these are very rough figures, since the value of common shares oscillated during these years.

A third venue for the generation of goodwill was the capitalisation of companies as ‘on-going’ concerns, placing a value on future profits. Hence, companies were traded at a price-to-earnings ratio (P/E ratio) of their current earnings. Today, we take this for granted, since it was established more or less empirically in the early 20th century, when there were attempts to find some law of ratio. Of course there is no such law: it is all based on future market expectations, and that component became, in time, the largest (Kaner 1937).

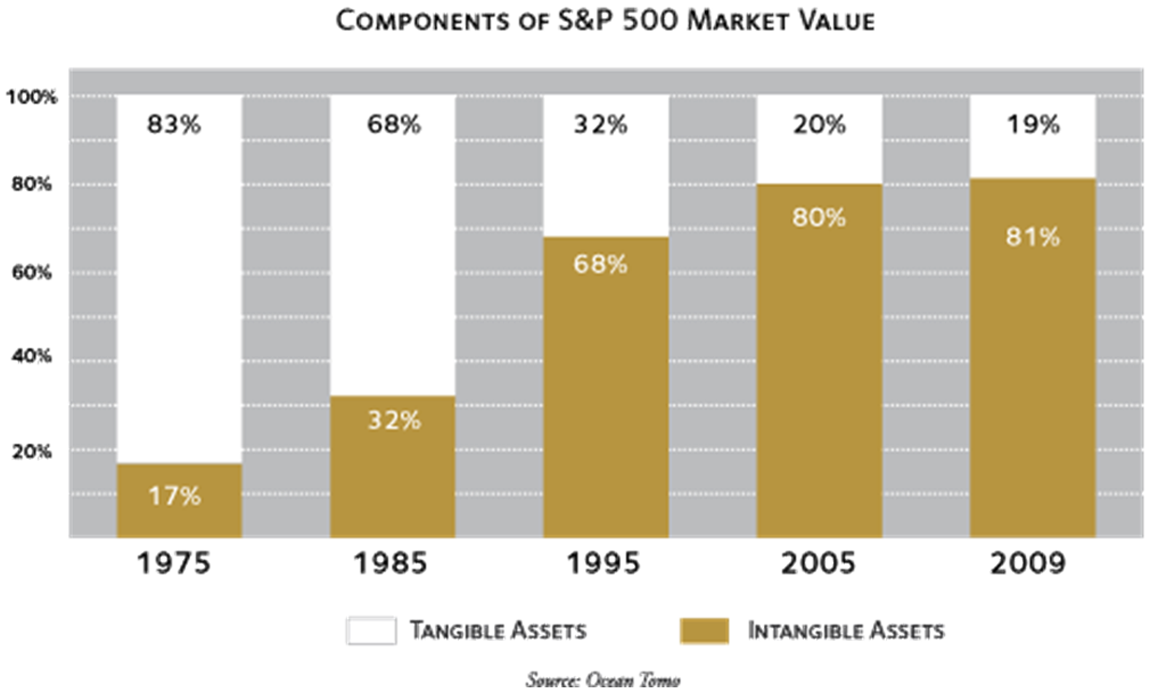

Today according to some estimates, the goodwill value of the Standard & Poor’s 500 amounts to about 80 per cent of their value. The graph below (Figure 1) is by a consulting firm, Ocean Tomo. Ocean Tomo’s equivalent figures for the year 2009 for the EU were 70 per cent, 35.8 per cent for Japan, and 73.5 per cent for China (Ocean Tomo 2009). Wealth in modern economies is largely denominated goodwill.

John Commons refers to the acceptance and incorporation of the concept of intangible property, specifically, goodwill, into law and calculations of value and justice by the US court system in the late-19th century. Businesses were considered ‘going concerns’, and valued on the basis of anticipated future earnings discounted against current rate of interests. Keynes also wrote about this: ‘when a man buys an investment or capital-asset, he purchases the right to the series of prospective returns, which he expects to obtain from selling its output, after deducting the running expenses of obtaining that output, during the life of the asset’ (Keynes 1936: 135).

To the best of my knowledge, neither Veblen, Commons nor Keynes followed up this notion by identifying the pro-cyclical dynamics that result in such conditions. The theory finds echoes, however, in Jan Toporowski’s notion of capital asset inflation, to which I now turn.

Pro-cyclicality of the financial system goes global

As the value of companies rose dramatically in the late-19th century, not least due to the increased value ‘released’ as goodwill, it led to two related dynamics, and specifically, to what Jan Toporowski calls capital asset inflation.

Orthodox finance theory draws largely on Walras’s theory of the markets for loanable funds: savings are brought into equilibrium with investment in the market for loanable funds. Capital market arbitrage is supposed to occur perfectly and instantaneously, rather than as a process over time. In such a perfect market, problems arise out of temporary disequilibrium. Toporowski argues, in contrast, that ‘the actual value of the capital market, by which is meant the market for long-term securities, is determined by the inflow of funds into that market’ (Toporowski 1999: 2). This leads to a situation whereby:

The net excess inflow into the capital market determines stock prices: When this inflow increases, brokers faced with rising purchase orders raise prices to induce stockholders to sell and maintain brokers’ stock balances. In this situation, turnover and prices rise in the market. Extended over a longer period of time, a growing net excess inflow gives rise to a process of capital market inflation. (1999: 2)

Today, most of that inflow is taken out by the issue of government and corporate bonds. But as companies were beginning to be valued against future profits, they could use these future profits now embedded in their rising share value as collateral to borrow money. In fact, in many cases, a new development was witnessed towards the late-19th century, whereby companies and individuals began to borrow heavily against what was seen at the time as ‘inflated value’ (or ‘water’) in order to bid for stocks and shares in theirs and other companies. This led to further capital asset inflation.

I suspect that what was going on here was a early privatised form of what today we call quantitative easing (QE), or the injection of broad money instruments into the system. As a recent Bank of England report makes clear,

There are a number of ways through which injections of money into the economy via asset purchases funded by reserves might be expected to affect nominal spending growth. But one important route is through higher asset prices, which should reduce the cost of obtaining funding and increase the wealth of asset holders, thus boosting spending and increasing nominal demand. (Joyce et al. 2010: 3)

The introduction of goodwill accounting in the late-19th century short-circuited the process. Companies now valued their assets much higher than before, once goodwill was factored in. As long as they were able to capitalise their higher valuations – and all the evidence suggests that they could – they effectively increased the wealth of asset holders, probably reducing the cost of obtaining funding (although this is an empirical question that needs to be validated through empirical research). Indeed, the period from about the 1880s onward saw a dramatic decrease in the interest paid on US Treasury bonds – an outcome that is associated with QEs (although again, the question of whether low US Treasury guilds were partly affected by rising intangible value clearly needs to be researched further). Thus, they were able to boost overall spending and increase nominal demand.

Collateralised assets could be also used to generate credit that could be used to bid for other assets: say, real estate. Higher real estate prices could be used, in turn, as collateral for further debt, which could be ploughed back into the real-estate or into other assets, and so on.

On the face of it, there are no clear internal market mechanisms to stop or slow down these reinforcing trends. Different assets can enter into a whirlpool of asset bubble inflation, and at least in theory, the process can go on forever. The result is that in the society of futurity, it is no longer possible to have a clear indication of the ‘real’ value of any assets. The very concept of real as opposed to nominal or fictional value is an anachronism – useful, no doubt for political or rhetorical purposes, but little more. The nominal value of assets, which is the only value in which owners are interested, is based on projected future earnings, which represent, by and large, optimism or pessimism about the future. The problem is compounded because the only measure of ‘real’ value is other financial assets; but all assets are directly or indirectly valued in the same process. Valuations tend, therefore, to reinforce each other’s valuations in a pro-cyclical manner. So while there is justifiable concern over speculation, in practice it is not possible to tell when value becomes speculative, or whether a Ponzi is developing or not (unless a complete fraud is perpetrated). At best, therefore, the notion of bubbles or Ponzis are based on historical evidence or sheer intuition. For instance, historical ratios of average wages against the value of housing tend to serve as a guide for reasonable valuations of the housing markets. But clever economists can always claim, as some have done during ‘boom times’, that we are now in a ‘new economy’ – the implication usually being, let’s forget historical ratios and push for a bit more futurity.

Financial regulations were never designed to deal with the pro-cyclical tendencies of the capitalist system in the age of futurity. This is partly due, surprisingly, to the very fact that the theory of futurity was never incorporated into financial theory.

At the same time, these reinforcing mechanisms can go into reverse, as they did during the ongoing financial crises, as one class of asset drags another class down in a never-ending downward spiral. At its height, about $50 trillion of ‘wealth’ was wiped from the books during this current crisis, manifesting as an expression of the deep crisis. Still, the crisis was not as catastrophic as the $50 trillion figure might suggest. Indeed, at the time of writing, the world economy had ‘recovered’ about $30 trillion.

The analysis suggests that the problems in the financial markets were not simply of speculation and financial de-regulation – these are undoubtedly exacerbating trends, but at the more profound level, the entire capitalist system in the age of futurity is profoundly ‘speculative’. Valuations are based on the future; investment strategies are based on future projection; and the financial system is a bridge not simply between savers and borrowers, but between future and present. It issues credit in the faint hope that income streams will be sufficient in the future to pay it back. It often gets things wrong.

My argument, in other words, is about the profundity of the ‘speculative’ nature of modern capitalism. The system relies ultimately on emotions such as ‘trust’ or ‘confidence’ not because these are ‘transaction cost’ reducing strategies, but because like paper money itself, the entire edifice of value is fundamentally a fiction that can work only as long as everyone is prepared to uphold that fiction

Globalisation exacerbates, however, both the problem of pro-cyclicality and its links with household demand. On the one hand, a Ponzi develops largely because of huge asset inflation through the pro-cyclicality described above. Each class of assets, when seen individually – say stock market valuation of the energy sector, or the housing market, and so on – may appear sometimes out of kilter with historical ratios.

But when states are embedded in larger systems, internal valuations of various class of assets are determined by large-scale processes beyond the control of governments. So to take a case in point, while the Spanish banking system was highly regulated before the onslaught of the crisis, and Spanish banks appeared initially robust and strong, the Spanish real-estate market was integrated into a European wide real-estate market, and increasingly reflected a European-wide valuation of properties. The highly regulated Spanish banks would advance credit to construction companies on the basis of a‘solid’ valuation of their property portfolio, but as the portfolio valuation was based on a market that was much larger than the Spanish market; the market was brought down like a house of cards once that larger market suffered a collapse. This is an aspect of globalisation that was not appreciated before the crisis; that globalisation integrates not only production, but most importantly, in conditions of heightened capital mobility, complex processes of asset price integration sometimes work in mysterious ways.

The London housing market, meanwhile, is partly integrated into a worldwide economy of ‘Richistan’ – not least because of the historical oddity of the system of taxation on non-domiciled individuals. A rule inherited from the times of the Napoleonic wars has created an effective loophole in British taxation whereby people who were born in other countries, and their children, can avoid paying tax on their non-British holdings. The central London housing market, therefore, only partially responds to the UK economy’s situation.

It was difficult to know before the crisis that the Spanish real estate market was so ‘inflated’, or whether the London housing market is inflated or not, because ultimately all these measures are relative. The best indicators we have are based on the concept of a national economy. But the very concept of the national economy is a relatively recent fiction that emerged in statistical work from around the 1920s onward.

Not only were financial regulations never designed to handle the pro-cyclical nature of an economy of futurity; but they are designed around the fiction of a ‘national’ economy, whereas the world economy is, on the one hand, highly integrated, and on the other, consists of so many geographical economies.

Pro-cyclicality and demand cycles

This is linked to the problem of inequality and democracy. The economic argument for equality is largely theoretical and based on the observation that the success of the ‘golden age’ of the Atlantic economy was achieved because of a political system that ensured a degree of synchrony of demand and supply, by linking various mechanisms of productivity growth with wage growth. The argument is supported by certain statistics that suggest that from the 1920s to the 1970s, the bulk of productivity growth in the USA and Western Europe was translated into higher average wages, and only a relatively small portion went to capital.

The argument here supports that theory, although from a slightly different angle. The reason is that if valuations are ‘fiction’ in the age of futurity, then the fictional consumer must be sustained as well. Otherwise, the system does not clear. The problem, however, is that the fictional consumer was not maintained. Income and wealth inequality is the observable side of the built-up lack of demand. The increase in wage inequality in the USA is well documented. A recent report by the Congressional Budget Office shows that between 1979 and 2007:

The share of after-tax household income for the top 1 per cent of the population more than doubled, rising to 17 per cent in 2007, from 8 per cent in 1979.

The most affluent fifth of the population received 53 per cent of after-tax income in 2007, up from 43 per cent in 1979.

The lowest fifth of the population received about 5 per cent of after-tax income in 2007, down from 7 per cent in 1979.

The remaining three-fifths of the population – the broad middle class – suffered a loss in their income share, from 50 per cent to 42 per cent, and each of the three quintile groups suffered an income loss ranging between 2 and 3 percentage points.

The real increase in inequality has been greater than the above, argues Khan. ‘The decline in the income shares of the low and middle income groups took place despite a sharp increase in the number of earners, principally female, per household, rising debt per household and the loss of much of pension benefits’ (Khan 2012: 5). Similar trends are seen in Asia and Europe (Allen 2005).

Valuations of future income streams are based on some idea of future sales of a product or a service, and they, in turn, are based ultimately on available demand. What we have learned from the financial crisis is that the fictional consumer can be maintained either through increased household income – which was what the period of Fordism was about; or through rising effective income through lower costs of wide-consumption goods like those produced by China; or through household income plus debt, which was what the period that is now called ‘neoliberalism’ was about. For a while, it did not matter which was which. Now it does.

Progressive critiques, including that by Strange, were that the third route is profoundly mistaken. I agree. I have questions, however, as to the degree to which the third route was chosen, and by whom.

The picture is of an integrated global system of – let’s call it ‘value assessment’, which combines economies of different geographies and size. At the same time, an inherited ‘Westfailure system’, in Susan Strange’s words (Strange 1999), works by supposedly controlling territorial chunks, most of which were carved in a process that, at least as far as an economy is concerned, is almost entirely arbitrary. Some of these governments oversee very large chunks of territories, some very small territories, and some medium-sized territories. Who controls what is largely a matter of historical accident. The majority of these states have inherited another set of conditions: they have joined together in a system that was meant to transnationalise their economies. In other words, they actively worked together, more or less since the 1860s, on a project that was aimed to reduce their ability to control what takes place inside their territories. It appears to me that the very logic of the project implies that as it progressed, their ability to make genuine choices diminished.

Strange’s own work exemplifies these contradictions. She identified the rise of what had become known as the ‘competition state’ theory; the idea that in the new conditions of mobile capital, states were increasingly engaged in competition over market share. I have made the argument, with Jason Abbott (Palan and Abbott 1999), that in such a competitive situation, the type of chunks of real-estate that you end up controlling determines to a large extent the kind of strategy that you are likely to pursue. I have since written specifically about the clubs of Liliputians of this world – tax havens, which combined have managed to pin some serious Gullivers to the ground (Palan 2003, 2010).

In such conditions, the policy that Margaret Thatcher called ‘there is no alternative’, although undoubtedly self-serving in her case, is to some extent a reality. There is an alternative, of course, but the alternative requires a great degree of cooperation among the key states. It is easier, under such conditions, to adopt what are often described as neoliberal policies: pro-market policies that are aimed at outwardly producing the impression of success within the territorial chunks that states happen to control, leaving aside the bigger problems of demand cycles.

Conclusion

Modern capitalism is founded on the principles of futurity. Hence, modern capitalism is inherently speculative. This should not be a problem, as long as the ‘fiction’ of valuation is carried to its logical conclusions. It is not enough that asset price inflation is maintained in the financial system, leading to the pro-cyclical trends describe above. Ultimately, the fiction can be maintained only if the interest payment on the debt that sustains the entire system is maintained as well. Interest payments can be sustained if the system clears – if consumers also have a sufficient amount of ‘fictional’ income as well. The political systems and ideologies that have prevailed in the past three decades forgot this small matter of clearing. They have produced, therefore, a crisis-ridden system.

Footnotes

Acknowledgements

This is a revised version of a paper that was presented at the 2012 annual conference of the British International Studies Association (Edinburgh, Scotland, 20-22 June). In revising this paper, I have had the benefit of comments from Charlie Dannreuther, Pascal Petit and Anastasia Nesvetailova. The paper also draws on work and discussions I have had with Yuval Milo.