Abstract

Most scholars interpret Marx’s prices of production as those which achieve simple reproduction assuming profit rates are equal and all capitals turn over completely each year. The dynamics of equalization, as circulation intertwines with production over the business cycle, is absent. The traditional ‘Marxist’ equation for the profit rate likewise considers only simple reproduction. This leaves a gap in our understanding of Marx, particularly regarding the impact of turnover time on the profit rate, one of Ricardo’s original problems which Marx claimed to solve. Starting from a critique of Veronese Passarella’s and Baron’s attempt to extend the traditional equation to expanded reproduction, I develop a more general equation showing how changes in turnover times, rate of surplus value and accumulation affect the equalization process, the formation of the general profit rate and hence of prices of production. Finally, considering Moseley’s introduction to the recently published translation of a 27-page excerpt from Marx’s Economic Manuscript of 1867–1868, I suggest an equation for decomposing the profit adjustment during equalization.

JEL Classification: B24, B51, E11.

Keywords

Since the beginning of the 1820s, this phenomenon [turnover time] has led to the complete destruction of the Ricardian school.

Introduction

Marx’s analysis of the formation of prices of production has been replaced, in most of the literature, by an interpretation due to Von Bortkiewicz (1949 [1907]). This interpretation subordinates the formation of prices of production to the definition of the necessary and sufficient conditions for the simple physical reproduction of inputs, assuming equal turnover times, equal rates of surplus value, constant labour productivity, constant prices and fully equalized rates of profit (Freeman 2007, 2023). This paradigmatic shift transforms the equalization process into a process-free equilibrium. 1 The process that forms prices of production, along with the general rate of profit, disappears together with the social relationship between wage workers and capitalists.

From the beginning of the 1980s, scholars began arguing that, because of this and other lacunae, the faults alleged to arise within Marx’s own theory are unsubstantiated. Marx did not fail to transform inputs because this is not necessary, and his theory of prices of production, along with the profit rate, is logically consistent. 2 However, though these authors show that traditional criticisms of Marx’s theory of value are inadequate, they fall short of a full dynamic description of price formation. To correct this, I reconsider the intertwined relation between the process of production and the process of circulation. I therefore exhibit the effect of turnover time on Marx’s equation for the rate of profit under expanded reproduction, and conclude by showing how changes in turnover times, rates of surplus value and rates of accumulation affect each other. I also show that a further decomposition is necessary to distinguish those forces that exert their influence during the equalization process throughout the business cycle. 3

After introducing the reader to turnover time and its centrality for Marx’s thought, I focus on the equation for the rate of profit under expanded reproduction provided by Veronese Passarella and Baron (2015). I thereby show that the inner connection between the processes of circulation and production unveiled by Marx requires a profound reconceptualization of the so-called transformation problem.

Turnover time

The turnover time of the money-capital which a capitalist advances is the average time period in which this money-capital completes its circuit. It represents a major part of Marx’s analysis in the second volume of Capital (henceforth KV2), but its importance is underestimated, with serious consequences for our understanding of his theory of value, above all the formation of the general rate of profit and consequently prices of production. The passage through which ‘the transformation of surplus-value into profit proceeds from the concrete unity of both [circulation and production] processes’ (Marx 2015 [1864–1865]: 92) disappears (henceforth I will use MMV3 for Marx’s Economic Manuscript of 1864–1865, used by Engels for his edition of the third volume of Capital).

The restrictive habit of assuming equal and constant turnover times is due to Von Bortkiewicz (1949 [1907]) who derived it from Tugan-Baranowsky and justified it as follows (Von Bortkiewicz 1949 [1907]: 200): ‘In so far as it is a question of demonstrating Marx’s errors it is quite unobjectionable to work with limiting assumptions of this kind, since what does not hold in the special case cannot claim general validity’ (emphasis added).

This criterion is unexceptionable in itself but is applicable only when the general theoretical formulation to be proved false has been correctly identified. Bortkiewicz did not do this, as shown by Moseley (2016), Kliman (2000, 2007) and other scholars (Freeman & Carchedi 1995). However, these scholars do not discuss the use of the ‘special case’ of equal turnover time, focusing on Bortkiewicz’s simultaneist and physicalist assumptions (because his simple reproduction is, first of all, a physical reproduction of goods). Only a few early authors (Murray 1998; Foley 1982, 1986; Kotz 1991; Moseley 1991; Rosdolsky 1977 [1968]; Tombazos 2013 [1994]) emphasize the role of turnover.

In recent years, two important books have addressed this issue, namely, Bryer (2017) and Jones (2021). 4 In their 2015 article, Veronese Passarella and Hervé Baron summarize the sparse previous literature and address the relationship between capital in production and in circulation, focusing on the influence of financial capital on the general rate of profit and thus recovering Marx’s analysis of turnover time. This leads them to suggest an equation for the rate of profit in the case of expanded reproduction. The importance of turnover time is also acknowledged in Moseley (2019). Jefferies (2022) provides estimates of the turnover of US circulating capital and the profit rate of private corporations from 1964 to 2017 and discusses the neoclassical and Marxist literature on the statistical measures currently used.

In notebooks V and VI of the Grundrisse, Marx (1973 [1857–1858]: 516–549, 618–743) sketches an analysis of turnover time. In the 1861–1863 manuscript, he distinguishes different forms of capital (MECW, Volume 31: 401), sums up Ricardo’s clumsy analysis of the effects of different forms of circulation on commodity values (MECW, Volume 31: 404–405) and considers the various forms assumed by capital in the sphere of circulation: interest-bearing capital [Zinstragendes] as well as money-dealing capital [Geldhandlungskapital] and commercial capital [Warenhandlungskapital] as opposed to productive (industrial) capital (MECW, Volume 33: 9–68; Volume 32: 464–70). Unfortunately, space does not allow me to discuss the evolution of Marx’s criticisms of classical economists on the various forms assumed by capital in relation to its circulation process.

In fact, Marx fully develops his analysis of turnover only in the manuscripts which became chapters 7–17 of KV2 edited by Engels, who mainly used Manuscript II, written between late 1868 and mid-1870. Here Marx makes precise suggestions on how turnover time influences the rate of profit, which he contrasts with the economists of his time.

Let us briefly reconsider the circuit of industrial capital (KV2: 135–136, 229), in KV2 (Engels’s edition chapters 1–6). Industrial capital is opposed to capital of circulation [Cirkulationskapital] 5 (KV2: 271; Hecker 2009: 22), which Marx understands as an independent kind of capital. Marx distinguishes, within the capital of circulation, between interest-bearing or financial capital (owned by capitalists specialized in lending money to industrial and commercial capitalists) and the different forms of merchant’s capital [Handelskapital]: commodity-dealing or commercial capital and money-dealing capital. Commercial capital conducts the purchase and sale of commodities necessary to provide industrial capital with its means of production (and therefore to undertake production itself), and to sell the commodities subsequently produced on the market; money-dealing capital conducts the technical operations connected with monetary payments and receipts. These particular forms of capital are analysed in Chapters four and five of MMV3 (Parts four and five of KV3); until then Marx’s analysis of industrial capital, developed at a higher level of abstraction, assumes the functions of circulation are not carried out by independent forms of capitals. Thus, the general concept of industrial capital includes commodity capital, money-capital and productive capital (KV2: 133); only later are the functions of commodity and money capital treated as the domain of independent forms of capital. The analysis still assumes the absence of credit, so money is the only means of purchase and all commodities produced are sold.

In KV2, to adequately analyse the turnover time of industrial capital, Marx examines the different forms taken by productive capital, fixed capital and circulating capital, which his contemporaries badly defined and misunderstood. Two chapters– 10 and 11– specifically criticize Adam Smith’s and David Ricardo’s failed attempt to understand the difference between them. For example, on Smith Marx says (KV2: 282) that one of the errors that follow from his conception was that of taking fixed and circulating capital as characteristics attributable to things (. . .) however, in enumerating the things which fixed and circulating capital consist of, it becomes evident that Smith lumps together the distinction between fixed and fluid components, which is only valid, and only has any meaning, in relation to productive capital (capital in its productive form), with the distinction between productive capital and the forms pertaining to capital in its circulation process: commodity capital and money capital.

Where referring to Ricardo, Marx emphasizes (KV2: 303) the fetishism peculiar to bourgeois economics, which transforms the social, economic character that things are stamped with in the process of social production into a natural character arising from the material nature of these things. Means of labour, for instance, are fixed capital – a scholastic definition which leads to contradictions and confusion.

Stuck in an approach focused on the material elements of capital, both Smith and Ricardo neglected the value process. In contrast, Marx (KV2: 262–263) abstracts from the heterogeneous material composition of the components of productive capital in the

where C ′–M ′ apex indicates an increase, expressing capital as a process of self-expanding value (KV2: 185): Capital, as self-valorising value, does not just comprise class relations, a definite social character that depends on the existence of labour as wage-labour. It is a movement, a circulatory process through different stages, which itself in turn includes three different forms of the circulatory process. Hence it can only be grasped as a movement, and not as a static thing.

Capital value passes through the different forms of money-capital, productive capital and commodity capital; a periodical reproduction that in its duration is typically ‘different in the different spheres of investment’ (KV2: 235–236): The circuit of capital, when this is taken not as an isolated act but as a periodic process, is called its turnover. The duration of this turnover is given by the sum of its production time and its circulation time. This period of time forms the capital’s turnover time. It thus measures the interval between one cyclical period of the total capital value and the next; the periodicity in the capital’s life process, or, if you like, the time required for the renewal and repetition of the valorisation and production process of the same capital value. If we disregard the individual occurrences that may accelerate or shorten the turnover time of individual capital, the turnover times of capitals differ according to their different spheres of investment [my emphasis].

Though the importance of this circuit is widely recognized, most Marx scholars have not fully appreciated the consequences Marx drew from it; they have stuck with the accountancy convention that capital is fixed if it participates in production for more than one year, a choice that blurs fundamental differences between fixed and circulating capital. Thus, for Napoleoni (1972: 133–134) To have an objective criterion for judging this durability, we reason as follows . . . : a certain capital is called fixed if its duration is greater than one year; . . . ; vice versa, it is called circulating if its duration is equal to or less than one year.

Another typical misunderstanding leads to dismissing the analysis of turnover. The argument, used by Lapavitsas (2000) and criticized by Jefferies (2022: 13), concerns a point Marx was well aware of: that the continuous reproduction of industrial capital requires circulation and production, though they proceed temporally, to be under way at the same time (KV2: 183): The real circuit of industrial capital in its continuity is therefore not only a unified process of circulation and production, but also a unity of all its three circuits. But it can only be such a unity in so far as each different part of the capital runs in succession through the successive phases of the circuit, can pass over from one phase and one functional form into the other; hence industrial capital, as the whole of these parts, exists simultaneously in its various phases and functions, and thus describes all three circuits at once.

Industrial capital does not pass through its various phases all at once, but is deployed to make production continuous. At any given time, a part in money is set aside to purchase inputs, other parts are tied up in inventory (of inputs awaiting production, undergoing production or awaiting sale) and a part in unallocated receipts from sales.

6

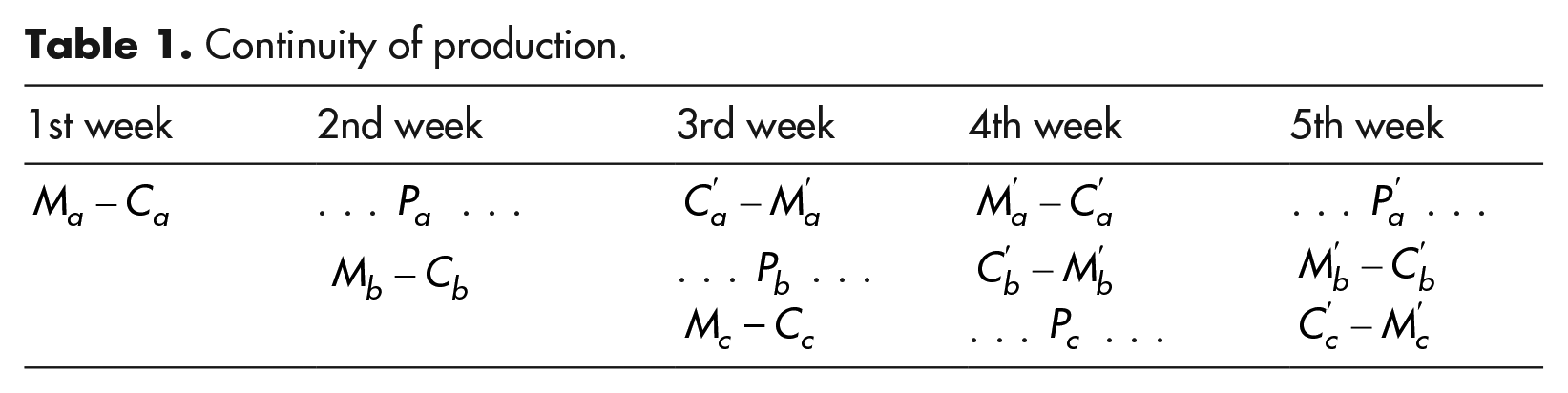

Moreover, portions of each such part pass through the circuit at different rates. These portions are hence invested at the same time in different phases of the circuit, so that once one is ready to pass to its next phase, another can substitute for it. Table 1 illustrates this point schematically for three portions

Continuity of production.

For simplicity, Table 1 assumes all realized values are reinvested and that the period of sales and purchases is the same length as that of production. Starting from the third week, one portion of total individual capital will always be passing through each phase of the circuit. Looking at the diagonals (from left to right) we see that the capital advanced decomposes into three temporally distinct portions, facilitating the continuity of each phase. For example, the succession of The coexistence which determines the continuity of production (. . .) exists only through the movement in which the portions of capital successively describe the various stages. The coexistence is itself only the result of the succession.

On the same page, Marx emphasizes the dependence between the coexistence and the succession of the different stages: Every delay in the succession brings the coexistence into disarray, every delay in one stage causes a greater or lesser delay in the entire circuit, not only that of the portion of the capital that is delayed, but also that of the entire individual capital.

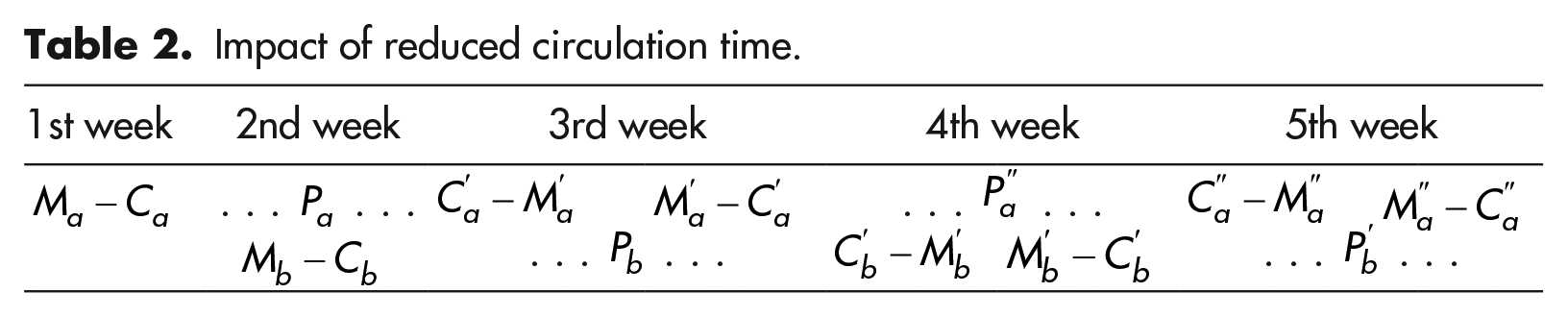

Table 1 shows that any interruption in this succession disrupts the continuity of production. Table 2 shows the effect of shortening the circulation phase. For example, if it is halved, the total of both phases (purchase and sale) is only 1 week, the total turnover time and capital advanced are reduced by one-third, and this will still guarantee the continuity of an even greater volume of production.

Impact of reduced circulation time.

This increases the number of turnovers of variable capital and creates additional value insofar as the total variable capital applied in the period increases. It is easy to verify that in both cases the total surplus value produced in a year would be the same if there were simple reproduction (even though in Table 2 the capital advanced is reduced by one-third), however, the annual rate of surplus value and, therefore, ceteris paribus also the rate of profit, would be greater in the second case.

Marx’s equation of the rate of profit

The stages of circulation cannot modify the amount of value produced in the production phase, but they do not limit themselves to changing owners. As we will see, they can help create the conditions for subsequent greater creation of value. Clearly, reductions in overall circulation time have historically occurred mainly in the production phase, but the above example is particularly important because it highlights an aspect of social reproduction that has often been ignored. For Marx, the only part of capital turnover which is significant for the creation of surplus value is that relating to the industrial variable capital, as is clear from the manuscripts used by Engels for KV3 (MMV3: 264):

7

the differing proportions of circulating and fixed capital, of which constant capital is composed, in the different branches of industry, do not have any bearing in themselves on the rate of profit; what is decisive is the ratio between the variable capital and the constant, while the value of the constant capital, and thus its relative magnitude in relation to the variable, is absolutely independent of the fixed or circulating character of its components.

This is not to say that the turnover time of fixed capital plays no role in equalizing the profit rate. On the contrary, Marx regarded it as one of the main bases of the business cycle, and hence, the formation of prices of production (KV2: 264). Here, however, the point is the role that it plays in determining the annual surplus value created by the variable capital advanced.

Marx (KV3: 335; KV2: 369) determines the number

If v is the initial variable capital advanced

8

and

This is of course an average; accidental differences being levelled out between the various circuits of money-capital in the period considered; n therefore represents the number of times the same initial variable capital v repeats its circuit in the period considered. Following Marx, we can write

where S is the total surplus value produced in a year and

where

The annual rate of surplus-value, given by the ratio S/v and the real rate of surplus-value

Marx often considers the real rate to be constant, but this does not change the fact that the annual rate may increase (decrease) if capital accumulation involves a shortened (lengthened) period of production and/or circulation with, therefore, an increase (decrease) in the number of turnovers. In fact, he also considered the changes in the real rate arising from an increase in productivity. On this, see in KV1 the chapter on ‘The General Law of Capitalist Accumulation’, and especially section 3 on the industrial reserve army (KV1: 771–772, 782–783, 790), with more on this point below.

Turnover and expanded reproduction

Equation (2) applies only to simple reproduction; it does not account for any change in surplus-value arising from accumulation. Veronese Passarella and Baron (2015: 1438) rightly argue that neither the equation provided by Marx in KV3 nor the equation ‘provided by Engels in Chapter 4 of the same volume can be regarded as the general equation of the annual rate of profit’. They suggest an alternative equation for a simplified two-sector economy containing a productive sector (‘manufacturing industry’) and an unproductive sector (‘banking and finance industry’), whose investment is deducted from the surplus-value of the productive sector. They assume that a share β of surplus-value produced by productive capital is retained and re-invested in variable capital in that sector, and modify the numerator of the profit rate by changing total surplus-value

Designating by

where

Since Veronese Passarella and Baron are interested in the relationship between these two sectors, they employ simplifying assumptions (no fixed capital, equal turnover times, constant rate of accumulation in variable capital, constant rate of exploitation and no capitalist consumption), justified for this specific purpose. They rightly emphasize the decisive place of circulation time in capitalist dynamics. In their words (Veronese Passarella and Baron 2015: 1431–1435) the annual general rate of profit depends on the ratio between the time of circulation and the time of production, which they call the temporal composition of capital (Proposition 4, p. 1432).

From Equation (5), it is clear that unproductive capital can have two opposite effects: the capital invested in this sector appears in the denominator and reduces the rate of profit, while any reduction of circulation time affects the number of turnovers of variable capital in the productive sector and increases the rate of profit. Which effect prevails is not predetermined and can change over the course of the business cycle (Fichtenbaum 1988; Jefferies 2022; Jones 2017).

Admittedly, Veronese Passarella’s and Baron’s proposed equation does not consider changes in the real rate of surplus-value or in the number of turnovers of variable capital arising either from innovations that shorten production time such as new organizations of the labour process, higher capacity utilization, or from more effective costs of circulation. In their equation the real rate of surplus-value is given, as is the number of turnovers

The general rate of profit in expanded reproduction

Veronese Passarella and Baron point out that Marx’s equation for the rate of profit is appropriate only for simple reproduction and suggest an alternative. I agree with their criticisms of Marx’s formulation but their equation should be modified to take into account the effect of accumulation on the denominator and changes in

Changes in turnover time of industrial variable capital

In simple reproduction we can determine

Now, to highlight how

If instead of considering the overall change of turnover time from time t to time

Changes in circulation time and production time

A further development of Equation (7) could decompose the turnover time of industrial variable capital by enquiring how circulation and production time affect it. The impact of circulation time can be distinguished from that of production time as follows:

If the average time of production is equal to 10 days, the average time of circulation is equal to 8 days, and the reference time unit for the number of turnovers is 360 days (the commercial year), then the number of turnovers will be given by 360 / (10 + 8) = 20. Considering the rates of change

We have:

From Equation (7):

Substituting in Equation (7) gives:

We can then replace Equation (7) with Equation (7a). The two rates of change,

As Marx emphasizes, ‘the division between mercantile and productive capital, involves a concentration of mercantile costs and a consequent reduction in them’ (MMV3: 400). Labour productivity clearly plays a major part also in the sphere of circulation. New technologies had a tremendous impact, for example, computerization, which transformed the retail industry from the early 1950s onwards. Engels underpins that the ‘main means of cutting circulation time has been improved communications. And the last fifty years have brought a revolution in this respect that is comparable only with the industrial revolution of the second half of the last century’ (KV3: 164). As Marx writes on the role played by commercial capital, its absolute size is in an inverse ratio with the number of its turnovers. All the [c]ircumstances that shorten the average turnover of commercial capital, such as the development of means of transport, for example, reduce the absolute magnitude of this commercial capital > (all other circumstances remaining the same) < and hence raise the general rate of profit. And vice versa. (MMV3: 376)

The rate of profit of commercial capital is determined by ‘its quantitative proportion to the total capital, to the sum of the capital advanced in the processes of production and circulation’ (MMV3: 416; see also 418–20). Of course, it is always important to distinguish the sphere of circulation in the strict sense from the productive role of industrial capital within this sphere (KV2: 214, 229; MMV3: 376).

Finally, we could distinguish between changes in the number of turnovers arising from the difference between the working period and the period of production. This last includes the time during which ‘the object of labour is subjected to natural processes of shorter or longer duration, and has to undergo physical, chemical or physiological changes while the labour process is either completely or partially suspended’ (KV2: 316; see also Tombazos 2013 [1994]: 193–196). Accumulation may affect the working period without affecting the period of production, making it possible to raise productivity without changing the number of turnovers. Vice versa, the number of turnovers can change without any change in productivity (e.g. if it shortens circulation time or a different length of the production process) (KV2: 310; KV3: 163–164). Marx devoted two chapters (12 and 13) of KV2 to the above distinction (see pp. 316–317 for some clear examples).

Changes in industrial variable capital

We can express the rate at which variable capital advanced accumulates, during period t, in terms of the average variable capital advanced during period t – 1. If

Finally, from Equations (6), (7) and (10):

Of course,

To distinguish the change in the flow of variable capital due to the new investment (disinvestment) in variable capital from that due to a change in the average number of turnovers

The fourth term of (11a) gives the combined effect of the change in variable capital and the change in the number of turnovers on the flow of variable capital applied during the period. The third term gives the effect of accumulation on variable capital, the second the effect of the change of the number of turnovers and the first specifies the flow of variable capital if

Of course, the number of turnovers could decrease (with

Since accumulation as such does not necessarily imply that surplus-value is invested into additional variable capital, we may want to consider a reduction in variable capital advanced coupled with an increased number of turnovers. Three such cases deserve attention:

A more efficient organization of the productive process;

Accumulation of constant capital introducing a new or improved technology;

An increased share of surplus-value devoted to investments in circulation costs, which shorten the time of circulation.

Clearly, the increase or decrease in the number of turnovers may over- or under-compensate for the reduction in variable capital applied in each turnover.

Changes in the real rate of surplus-value

Marx analyses the effect of changes in the real rate of surplus-value in parts 3–5 of KV1 and Chapter 25 on the general law of accumulation of capital. The four main factors that increase the real rate of surplus-value (KV1: 655) are:

Lengthening the working day or Absolute Surplus Value (KV1: 293–306,340–416). Important in early capitalism, it is still present where the bargaining power of the work force is weak;

Reducing the value of the means of subsistence through increased productivity or Relative Surplus Value (KV1, Chapter 12), which increases the surplus value obtained in a given working day;

Increasing the intensity of labour (KV1: 660–661);

Changing the wage rate (relaxing Marx’s provisional assumption that the ‘labour-power occasionally rises above its value, but never sinks below it’ (KV1: 655)).

is the real rate of surplus-value and

Using Equations (11)–(13):

Productivity plays the main role in capitalist development (KV1: 431–432). It plays a part in all branches of production, because those individual capitalists who introduce productivity enhancements appropriate extra surplus-value. They can sell their products ‘above their individual but below their social value’ because they ‘can only command a more extensive market if their prices are reduced’ (KV1: 434). However, even though ‘the capitalist who applies the improved method of production’ manages to appropriate an extra surplus, ‘as the new method of production is generalized, . . . the difference between the individual value of the cheapened commodity and its social value vanishes’, in fact, the same conditions that forces him ‘to sell his goods under their social value . . . forces his competitors to adopt the new method’ (KV1: 436).

However, a rise in productivity affects the general real rate of surplus-value, the economy-wide real rate, only when it reduces the value of labour-power: ‘only when the increase in the productivity of labour has seized upon those branches of production and cheapened those commodities that contribute towards the necessary means of subsistence, and are therefore elements of the value of labour-power’ (KV1: 436, 645–647).

A further important indirect effect of increased productivity is the possibility to support more unproductive labour in the sphere of circulation, with a positive effect on the turnover time of capital.

Marx devotes Section 3 of Chapter 25 of KV1 to the industrial reserve army (the ‘Progressive Production of a Relative Surplus Population’): ‘a surplus population of workers is a necessary product of accumulation’ and at the same time ‘it becomes a condition for the existence of the capitalist mode of production’ (KV1: 784). He situates accumulation in the context of the decennial cyclical path of modern industry (KV1: 790) which, though interrupted by smaller oscillations, constitutes the actual process (even though in other contexts he refers to cycles of different length (KV1: 786)). The industrial reserve army is both the condition and the result of this path, along with the accompanying changing relation between paid and unpaid labour-time, that is, surplus-value. Indeed, different real rates of surplus-value are associated with different stages of the cycle and different spheres of production.

Accumulation affects the variable component of capital in several ways. While in a given sphere of production growth can generate ‘an absolute diminution in its variable component’, in spheres where it proceeds on the existing technical basis it ‘attracts additional labour-power’ (KV1: 782). The labour market is thus under pressure in some spheres where it attracts more workers, whereas in others a part of the work force becomes superfluous.

Changes in the destination of surplus value

We can decompose Equation (13) to highlight the share

The two shares,

An alternative decomposition of

Defining

After some algebraic manipulations, we get:

In what follows, I use Equation (13) for the sake of simplicity; however, it will be always possible to substitute Equation (13) with Equation (13a) or (13 bis).

Changes in capital advanced

In expanded reproduction in general, total capital advanced normally includes an increase in the average capital advanced. Veronese Passarella and Baron take a different approach; they only use the capital advanced at the start of the period in the denominator of the equation of the annual rate of profit. This would overestimate the rate since accumulation also affects the amount of capital advanced.

I suggest the denominator include the capital advanced due to accumulation. If

where

In the case of circulation costs equal to zero (the initial assumption followed by Marx), using Equation (14) for the numerator, Equations (10) and (17) for the denominator of Equation (3), the rate of profit is:

Relaxing the provisional assumption on zero circulation costs, as Marx does, the same reasoning followed for industrial capital can be used to include merchant’s capital advanced in the sphere of circulation, and thus, the denominator of the previous expression becomes:

The symbols the average profit is now . . . determined by the total profit that the total productive capital produces; but it is not calculated just on this total productive capital alone, . . . ; it is calculated, rather, on the total productive and commercial capital together.

Clearly, for Marx, money-dealing capital (not to be confused with interest-bearing capital) plays the same role as commodity-dealing capital in determining the average rate of profit (MMV3: 421): Just as in the case of commodity-dealing capital, a part of the productive capital present in the circulation process in the form of money capital separates off and performs these operations [the purely technical movements of money payments and receipts] of the reproduction process for the whole of the remaining capital. The movements of this money capital are thus simply movements of a now independent part of productive capital in the course of its reproduction process.

Therefore, commodity-dealing and money-dealing capital affect circulation time and participate in the determination of the general rate of profit with the related equalization process (MMV3: 444) (even though they do not create value directly (MMV3: 388)), whereas interest-bearing capital does not (MMV3: 469–470).

Capital invested in the circulation sphere typically affects the general rate of profit in five ways:

By reducing the surplus-value available for accumulation because a part of surplus value is spent as revenue for circulation costs;

By increasing the denominator of the rate of profit;

By reducing circulation time, therefore increasing the number of turnovers that productive capital can make, especially that of variable capital;

By reducing the industrial capital that must be advanced for a given or larger volume of production;

By increasing the capacity utilization of industrial fixed capital, therefore reducing unit costs.

Overall, as Marx makes clear, the role played by the merchant’s capital is only apparently negative as regards the rate of profit of productive capital (MMV3: 405): The profit of the productive capitalist is therefore reduced [by the circulation costs]. But because of the concentration and economy that results from the division of labour, this reduction is less than it would be if he had to advance the capital [of circulation] himself. The reduction in the rate of profit is less, because the amount of capital advanced in this way is smaller.

Turnover times, accumulation and prices of production

In addressing the so-called transformation problem, most scholars leave aside Marx’s dynamic approach by considering only, and at that very partially, the tables used in Chapter 9 of KV3. It is true that to examine the differences in organic compositions of capital when he sketched out a solution to the transformation problem addressing one of the limits of Ricardo’s theory of labour value Marx had initially considered only the average rates of profit of five spheres of production, with their capital compositions expressed in terms of percentages, and a single period of reproduction, even assuming equal turnover time and equal rates of surplus-value for all spheres of production. However, this observation has to be qualified.

In this respect, Jefferies (2021: 20–23) and Meek (1977: 99–101) recall passages from the Grundrisse (Marx 1973 [1857–1858]: 435–36). Meek also mentions a letter written by Marx to Engels on 2 August 1862 (MECW, Volume 41: 394–398); other passages can be found in the MECW (Volume 31: 263–264, 296–303, 415–416 and Volume 32: 23–28). This cannot justify the indifference shown on this matter, above all by Marx scholars. In general, whenever Marx makes provisional assumptions, he subsequently discusses the consequences of removing them. This was also his intention in the case of the transformation of values into prices of production. Not taking this into account would imply a serious methodological error.

Already in Section 3 of Chapter 2 of MMV3 (Chapter 9 of KV3), Marx mentions the need to reconsider ‘the laws governing the rise and fall of the rate of profit, developed in Chapter One’ and states that ‘the general rate of profit is determined not only by the average rate of profit in each sphere, but also by the distribution of the total capital [my emphasis] between the various particular spheres’ and ‘this distribution is constantly changing’ so that we have again a constant source of change in the general rate of profit, [even if w]ithin each sphere there is room for shorter or longer periods in which the profit rate in that sphere, rises, falls, and rises again, etc. before this movement is consolidated (MMV3: 281).

Therefore, here Marx has already begun analysing the dynamic nature of the formation of the general profit rate.

A few pages later, Marx clarifies it was necessary to understand the formation of the general profit rate during equalization and raises the key question (MMV3: 285): how does equalization take place? The very fact that this appears in Section 4 of Chapter 2 of MMV3 (Chapter 10 of KV3) shows that he did not consider the mere fluctuation of market prices a sufficient mechanism for realizing equalization (see also MMV3: 470).

Individual value, social value and average productivity

Chapter 10 of KV3 was dedicated to a first account of the equalization process in line with the distinction between individual value and social value that Marx subsequently used in KV1. Even this transformation from individual value to social value, and the related development of the category of socially necessary labour, is usually removed from the traditional analysis of the formation of the profit rate.

The category of socially necessary labour-time is often badly ‘translated’ as if Marx intended to refer to the most efficient technology available, which then becomes the only technology worthy of analysis. This is not Marx’s approach to competition. While it is true that competition diffuses the most efficient technology, differences between the individual values of commodities produced with different technologies will persist for as long as it takes for this most efficient technology to be adopted. Besides, if they adopted the new technology, some capitalists could go bankrupt on their old fixed capital investment. This process is constantly being renewed. Innovation, with its consequent increase in the productivity of labour, is not a process that ever reaches a point of final rest; while new technology is spreading socially by modifying the previous amount of socially necessary labour required to produce a commodity, new technologies are being introduced by later capitalists who seek to improve yet further on existing methods including those that, at the time, are still the most efficient.

More importantly, it is inconceivable that all the spheres of production suddenly reach a point of rest at the same time, with all the capitalists adopting the best available technology. Yet this assumption is made by most economists including most Marx scholars. Analysing the process of equalization, these scholars additionally assume that innovations in one sphere of production will not affect others: the assumption is thus that in all the spheres of production all capitalists at the same time adopt the best available technology, leading to a kind of end of history within the given period chosen as reference. In fact, even in the case of constant productivity, though with different levels within each sphere of production, average productivity will necessarily change due to market price fluctuations and/or to the transfer of individual capitals from less to more remunerative spheres of production, or to more advanced technology available within the same sphere, and this will affect the industries’ average rate of profit (De Marco 2021).

The general rate of profit is not just an overall statistical average of the industries’ average rates of profit: it is the resulting moving centre towards which the industries’ average rates of profit tend due to the centripetal force determined by the law of competition between capitals with different rates of profit within the same sphere of production and across the other spheres of production. At the same time, it is a moving centre as a consequence of the changing distribution of capital between the various industries (MMV3: 281), as well as a consequence of the centrifugal force determined by the drive towards the best possible rate of profit that is characteristic of the process of accumulation of capital ( ‘the unceasing movement of profit making’ (KV1: 254)).

The timespan of the tendency towards equalization

In the traditional equilibrium approach, the timespan of the period taken into consideration has only a kind of ‘logical’ temporal dimension in sharp contrast with Marx (MECW, Volume 32: 459) who instead is very explicit about the timespan for the formation of the ‘ideal’ average rate of profit The real profit deviates from the ideal average level, which is established only by a continuous process, a reaction, and this only takes place during long periods of circulation of capital. The rate of profit is in certain spheres higher for some years, while it is lower in succeeding years. Taking the years together, or taking a SERIES of such EVOLUTIONS, one will in general obtain the AVERAGE PROFIT. Thus it never appears as something directly given, but only as the average result of contradictory oscillations.

In KV3 Marx qualifies the equalization between different industries’ average rates of profit by referring to the tendency to equalization (KV3: 273) or the (temporal) process of equalization (KV3: 274, 304). He repeats the same reasoning in Chapter five of MMV3 (Part five of KV3): ‘The general rate of profit, on the other hand, only ever exists as a tendency, as a movement of equalisation between particular rates of profit’ (MMV3: 469; KV3: 488). This process takes time and, in fact, Marx refers to the prices of production as the long run condition of supply (MMV3: 307–308; KV3: 300; see also MECW, Volume 32: 459–460).

Equalization can only be achieved by chance or approximated over a long period (the cycle of fat and lean years suggested by Marx (MMV3: 313–314) because the divergences between the average annual profit rates of the various spheres of production are the normal condition of reproduction (MMV3: 470), the annual rate of profit changes over the lifespan of the fixed capital advanced in the unfolding of the accumulation process (Shaikh 2008: 168–169, 2016: 104–106).

If, during the process of its formation, the general rate of profit represents the ideal centre for the average rates of profit of the various spheres of production, this does not imply that the general rate is always reached or that capitalists can simply apply it to their money-capital advanced; moreover, the overall measure of the general rate of profit can be really determined only backward, at the end of the business cycle of industrial capital.

The turnovers of fixed capitals overlap and never coincide in their lifespan; some major industries may happen to have a similar average lifespan but the temporal distribution of capital is not predetermined and cannot be predicted. Of course, capitalists can look at the past and current general rate as a reference to measure their success and decide how to accumulate. But they can only have a rough idea of the general rate of profit that will prevail over the life of their fixed capital in the face of changing productivity. Furthermore, as Marx notes in a passage that has often gone unnoticed, the general average itself is just an ideal point of reference between spheres with different average rates of profit (MMV3: 284): Between those spheres that approximate more or less to the social average there is again a tendency to equalisation, which seeks [my emphasis] a possibly ideal mean position, i.e., a mean position which does not exist in reality [my emphasis]. In other words, it tends to shape itself around this ideal as a norm.

If we do not pretend to live in a fantasy world, then we should agree with Marx: ‘One can only speak of an average rate of profit when the rates of profit in the different branches of production of capital are different, not when they are the same’ (MECW, Volume 33: 94), otherwise the whole equalization process would make no sense. See also MECW (Volume 32: 273).

The accumulation process and the redistribution of capital

Marx emphasizes the role of accumulation in the dynamics of equalization. He attributes an even more important role to new capital invested than the migration of already existing capitals (MECW, Volume 32: 460–461): it is the inflow of new, ADDITIONAL capital, even more than the redistribution of capital already invested, that equalises the distribution of capital in the different spheres. The SURPLUS PROFIT in the different spheres, on the other hand, is discernible only by comparison of the market prices with cost prices [prices of production]. As soon as any difference becomes apparent in one way or another, then an outflow or inflow of capital from or to the particular spheres [begins]. Apart from the fact that this act of equalisation requires time [my emphasis], the average profit in each sphere becomes evident only in the average profit rates obtained, for example, over a cycle of 7 years [my emphasis], etc., according to the nature of the capital. Mere fluctuations – below and above – if they do not exceed the average extent and do not assume extraordinary forms, are therefore not sufficient [my emphasis] to bring about a TRANSFER OF CAPITAL, and in addition the TRANSFER of fixed capital presents certain difficulties. Momentary booms can only have a limited effect, and are more likely to attract or repel ADDITIONAL CAPITAL than to bring about a REDISTRIBUTION of the capital invested in the different spheres. One can see that all this involves a very complex movement . . . within each individual sphere, and, on the other hand, competition among the capitalists in the different spheres, play a part, and, in addition, the speed of the equalisation process, whether it is quicker or slower, depends on the particular organic composition of the different capitals (more fixed or circulating capital [my emphasis], for example) and on the particular nature of their commodities, that is, whether their nature as use values facilitates rapid withdrawal from the market and the diminution or increase of supply, in accordance with the level of the market prices.

The distribution of total surplus-value is not realized at the end but throughout the entire period of reproduction considered; furthermore, during the processes of distribution intertwined with processes of production, circulation time is affected by the migration of capitals, ‘by the continual transfer of capital from one sphere to another, where profit stands above the average for the time being’ (KV3: 310), even though this transfer mainly concerns additional capital and hence accumulation, because it is difficult to liquidate fixed capital already operating (here it is crucial to refer to the equation of the rate of profit under expanded reproduction). 11 Of course, even under a regime of simple reproduction, this recognition rules out by definition any possibility of considering the redistribution of total surplus value only at the end of the time period chosen as reference, as instead it is usually assumed in the Marxist literature, the so-called pooling-and-redistribute process (Laibman 2018: 32).

This redistribution will affect the key components into which profit rates can be decomposed, namely the turnover time, the composition of capital, and the real rate of surplus-value (MMV3: 281; see also De Marco 2021). Indeed, if equalization is not just a pure reverie, how is it possible that during this real process these key components are unaffected by changes in the distribution of capital and vice versa?

Why the assumption of equal turnover times should be removed

The category of turnover time has always been considered as if it were only a further ‘complication’ or another minor source of unequal profit rates. Indeed, Marx placed the differences in turnover times and in the organic composition of capitals on the same level of abstraction, because they both affect the process of formation of the profit rate. He develops the exam of the effect of turnover times in the manuscripts drafted after the second chapter of the main manuscript for KV3 (second part of KV3) devoted to the ‘The Transformation of Profit into Average Profit’. 12

He explicitly states that turnover is as important as the organic composition of capital

13

(KV3: 243; MMV3: 252): We have now to investigate: (1) differences in the organic composition of capitals; (2) differences in their turnover time.

He repeats this point a few pages later (KV3: 250; MMV3: 260–261): Besides the differing organic composition of capital . . . there is a further source of inequality between rates of profit: the variation in the length of capital turnover in the different spheres of production.

He reiterates the importance of turnover time in his analysis of mercantile capital (MMV3: 415): As far as productive [industrial] capital is concerned, its turnover expresses on the one hand the periodicity of reproduction and therefore depends on the amount of commodities put on the market over a certain period of time. On the other hand, the circulation time also forms a limit, even if one capable of extension, which may have a more or less constricting effect on the formation of value and surplus-value, because it has an impact on the scale of the production process. Thus, the turnover exerts its determining function [emphasis added] on the mass of surplus-value annually produced and therefore on the formation of the general rate of profit.

There is therefore no doubt that Marx considered both turnover times and organic composition decisive in determining differences between industrial profit rates. Why did he not pursue the intention to investigate the effect of turnover time on the rate of profit? Actually, he is very clear in explaining why he will not examine the impact of circulation time (MMV3: 261): The extent to which circulation time has an impact on the rate of profit is a question we do not wish to examine here in detail (since Book Two, which is devoted to discussing this, has not yet been written).

A few pages later he adds that this will in fact be ignored (MMV3: 266; KV3: 254): we shall ignore for the time being the differences that may be produced here by variation in circulation times. (We shall return to this point later.)

Unfortunately, he did not ‘return to this point later’, but he did not change his mind about its importance, as the following passage shows (KV2: 294): When the social surplus-value is distributed between the capitals invested in different branches of industry, differences in the various times for which the capital is advanced (for example, varying lifespan in the case of fixed capital) and different organic compositions of capital (thus also the different circulations of constant and variable capital) have similar effects in the equalisation of the general rate of profit and the transformation of values into prices of production [my emphasis].

However, as I discuss below, Marx did try to deal, at least in part, with the effects of turnover times on the equalization process as discussed in Moseley (2019).

Changes in turnover times

What happens when a higher-than-average profit rate draws capitals from one to another sphere of production, or when accumulation modifies the proportion in which capitals are invested in the different spheres of production? What happens when turnover times change as a result of innovations in either production or circulation, introduced before and after changes in market prices, or due to the change in the distribution of capital?

Here I can only outline an answer. My book under review (De Marco 2023b)contains a more detailed discussion of the effects of turnover on the transformation of values into prices of production.

First of all, when capital moves from spheres with a lower average profit rate to those with a higher rate, especially when new capital is redistributed, it reduces the time of circulation of money-capital advanced in the former, increasing the number of turnovers, and raises it in the latter, decreasing the number of turnovers. The effect of the redistribution of capitals on turnover time will precede changes in market prices. When commodities sell faster (increasing turnover time), this signals to the capitalists that demand is growing and consequently market prices rise (MMV3: 303–304). Conversely, when commodities take longer to sell (reducing turnover time), this signals to the capitalists that demand is shrinking. If this slowdown proves persistent, competition forces the market price down (MMV3: 298). These processes will be reinforced by the reduced (increased) accumulation rates that will further reduce (increase) supply in the spheres that originate (receive) the outflow (inflow) of capitals. Moreover, the capacity utilization of fixed capital rises (decreases), lowering (increasing) unit costs and hence both the individual and social value of commodities.

The number of turnovers for each individual capital in a given sphere will generally continue to be different. In the spheres where the inflow of capital occurs the evolution of turnover times will hinge upon the technologies adopted by the new capitals. It is also possible that some capitalists with lower productivity will be pushed out of the market by going bankrupt (KV1: 777).

On the other hand, the capitalists’ drive to secure the highest possible individual profit rate can produce another chain of effects. Instead of migrating to a more profitable branch of production, capitalists with lower rates can try to shorten the time of production and/or circulation of their capitals by introducing new production processes, re-organizing the labour process and increasing the intensity of labour, as Marx spells out in KV1and KV2 (see, for example, the chapter on the reduction of the turnover-time of fixed capital in Mandel (1975 [1972]: 223–247)). The chain of changes can become more complex especially considering the evolution of business cycle.

Decomposition of the profit-adjustment in expanded reproduction

Moseley (2019) shows that Marx was trying to distinguish the influence of turnover time on the formation of prices of production from that of the composition of capital. Below, I decompose the profit-adjustment under expanded reproduction, following a reasoning similar to Marx (2019 [1867–1868]). De Marco (20023a) discusses some important differences.

Designating by

Considering Equation (18), assuming no circulation costs, and dividing by

where

Now we can compare the general rate of profit r with the value rate of profit

Therefore, since the costs of production are the same for Pti and Wti:

Assuming no circulation costs, the capital advanced

From Equation (20) the total profit-adjustment becomes: 14

Assuming

Defining

Equation (25) breaks down as follows:

The first product in the square bracket refers to the deviation due to the difference between number of turnovers, the second to that due to the difference between organic compositions and the third to their combined effect (see also De Marco 2023a).A further adjustment due to unequal real rates of surplus-value can easily be formulated.

As noted, the general rate of profit is not just an overall average but also the ever-changing result of the ‘constant equalisation of ever-renewed inequalities’ (MMV3: 305; KV3: 298). Equation (30) exhibits the differences between the general rate of profit and the industries’ profit rates that are not yet equalized or, as traditionally formulated, in a ‘non-equilibrium’ state. 16

These are the resultant of conflicting forces: the centripetal force of competition and the centrifugal force of the drive for the best possible profit rate (MMV3: 471); over the cycle of industrial capital, one or the other can prevail alternately depending on the sphere of production (KV1: 782–783).

A slightly more complex expression for

and

where

So that (18a) becomes:

Defining

The decomposition of Equation (25) becomes:

where

Now, Equation (30a) tells us that the equalization process involves the circulation capital and its impact can be easily analysed.

Conclusion

In the traditional literature on Marx’s profit rate, the notion of equilibrium invariably presupposes that industry average rates are fully equalized and prices, turnover times, rate of surplus value, remain constant during the period considered. This turns the equalization process into a pure reverie supposedly sprung from Marx’s mind. The very special (and ideal) condition of equilibrium is assumed to be already reached, so that the process through which this might be attained is ignored as being of no consequence. Following Marx, my own stance is: (1) it is much more interesting to understand how the forces that push towards the equalization exert their influence, (2) other forces push to disrupt the equalization and (3) the formation of prices of production has to be considered over the business cycle of industrial capital.

The transformation of values into prices of production should be discussed on the basis of Marx’s dynamic approach, as noted by the TSSI school (Freeman and Carchedi 1995; Kliman 2007) and other scholars (for example, Fineschi 2001, Mazzetti 2004).

The traditional equilibrium interpretation is not adequate to describe the process of equalization because it relies on simplifying assumptions which rob the analysis of the intertwined character of the processes of production and circulation of capital. The length of the periodical reproduction of advanced capital (turnover time) has been set aside, or indeed, completely misunderstood, removing the dynamic of these processes from the analysis. The use of money-capital circuit is the conditio sine qua non for understanding how the various forms of productive capital (fixed and circulating) transfer their value during valorization and circulation.

However, most scholars who do recognize the importance of this circuit stop halfway, without taking into account Marx’s subsequent analysis of the turnover time of capital as developed in KV2. Correcting this weakness highlights the crucial distinction between the annual and real rates of surplus-value in the transformation of values into prices of production, and paves the way to the recovery of the role played by the various forms of capital within the process of circulation, namely, money-dealing capital and commercial capital.

Reconsidering the temporal dimension of capital reproduction also requires a deeper analysis of Marx’s equation for the profit rate, taking into account the changes that affect it over the business cycle. These concern firstly, the number of turnovers of variable capital; secondly, the capital advanced on average in the period (arising from the investment (disinvestment) of constant and variable capital); thirdly, the real rate of surplus-value and fourthly, the amount of capital invested in the sphere of circulation.

Following Marx, I suggest the general profit rate should be understood as a moving average of industries’ average profit rates, which change over the business cycle and are influenced by the continuous transfer of capital between industries, by changes in turnover times, changes in labour productivity, changes in real rates of surplus value, accumulation rates and by investment of capital in the sphere of circulation.

Finally, I suggest that the total profit-adjustment should be broken down so as to highlight the forces moving each individual industry towards equalization in terms of the rates of change in the real rates of surplus value, in the organic compositions of capital, in turnover times and in the processes of accumulation.

Footnotes

Acknowledgements

I am very much indebted to Alan Freeman, Giovanni Mazzetti, José Tapia, and my friends from ARELA (Association for the Redistribution of Labour), Gabriele Serafini and Mauro Parretti. I am also grateful to two anonymous reviewers and to Aldo Balardini, Stefano Lucarelli, Marco Veronese Passarella, Hervé Baron, for their helpful comments on an early version of this article. I am thankful and greatly appreciated the patience, as well as the valuable and thorough editing by Dr. Anitha Babu. All errors are my own.