Abstract

This study investigates the characteristics and attributes that private equity investors prefer when selecting target acquisitions. These characteristics are examined against a matched sample of firms subject to corporate acquisitions via tender/merger offer during 2000–2009, across seven countries: Australia, Canada, the United Kingdom, the USA, France, Germany and Sweden. We show that firm-specific characteristics are more influential in target selection than external or institutional variables. In particular, private equity targets exhibit lower stock volatility and long-term growth prospects, are larger, and have greater abnormal operating income relative to tender/merger offer target firms. Further, private equity bidders exhibit ‘home bias’, implying that familiarity motivates target selection. Institutional factors remain largely insignificant across all tests.

Keywords

1. Introduction

Private equity has grown into a valuable asset class in capital markets, and regulators acknowledge that such acquisitions ‘help to promote an efficient, dynamic and innovative business sector’ (Reserve Bank of Australia, 2007: 66). This paper investigates, across a sample of countries, the characteristics and attributes that private equity investors prefer when selecting target acquisitions. In particular, these include firm-specific characteristics such as financial and performance measures, as well as external or institutional determinants, such as jurisdiction. These characteristics are examined against a matched sample of firms subject to corporate acquisitions via tender/merger offer during 2000–2009, across seven countries: Australia, Canada, the United Kingdom, the USA, France, Germany and Sweden.

In addition, this paper investigates whether private equity bids exhibit home bias across countries, and within the United States. Equity home bias refers to the observed phenomenon that investors prefer local market securities, and has been labelled a ‘puzzle’ in prior literature (Warren, 2010). As private equity funds are sophisticated investors, and considering the findings of French and Poterba (1991), which showed that UK, Japanese and US investors heavily overweight their portfolios in their home market, a useful extension conducted in this study is an examination of whether such bias exists in the market targeted by private equity.

There is a broad literature considering target firm characteristics surrounding mergers and acquisitions (Alcade and Espitia, 2003; Chatterjee, 2000; Dietrich and Sorensen, 1984; Kuehn, 1975; Palepu, 1986; Singh, 1975; Siriopoulos et al., 2006); however, scant attention has been paid to target-firm characteristics of private equity bid target firms relative to other acquisition techniques (Chapple et al., 2010). Prior studies also present conflicting findings on the importance of target firm-specific characteristics in determining the probability of a merger or acquisition. Further, little prior research has investigates such characteristics in a cross-country setting, with such analyses instead being limited to one, or several countries’ markets. For example, Siriopoulos et al. (2006) and Chatterjee (2000) find that acquirers prefer larger, mature targets with high productivity in Greece and the United Kingdom. Singh (1975), Kuehn (1975), Palepu (1986) and Alcade and Espitia (2003) find that smaller firms with lower profitability and market to book ratios have a higher probability of a bid (relative to other potential target firms) in the United Kingdom, the United States and Spain.

This study contributes to the literature in three ways. First, little attention has been directed to the firm-specific characteristics of target firms subject to a private equity bid. While recent literature has considered the target firm-specific characteristics of private equity bids in an Australian context (Chapple et al., 2010), this study extends prior literature to consider these characteristics relative to tender/merger offers on an international basis across seven countries with a free and well-developed equity market listed on the FTSE Global Equity Index Series financial market list. These countries represent a sample covering both common and civil law legal systems. The difference between common law and civil law systems, as related to securities investment, is significantly related to, for example, the strength of investor protection (La Porta et al., 1998). Whether the strength of the investor protection provided in a market is a priority to sophisticated investors such as private equity investors is a useful distinction to make when investigating investor preferences.

Second, this study examines the effect of country-specific characteristics such as legal indices, interest rates and business cycles on financial markets in a private equity context. Foster et al. (2012) highlight the importance of country-specified variables in capital markets research. Their study examines equity valuation multiples in a global setting. It uses 22 variables intended to capture country-by-country differences according to four general categories: ‘economy related’, ‘capital market related’, ‘legal/political related’ and ‘financial reporting regime related’ factors. In our study, we have focused more on the legal/political related factors.

Finally, we examine the proximity of a bidder to its target, to isolate the existence of any home bias.

We find that targets chosen for acquisition by private equity firms exhibit lower stock volatility and lower ex-ante long-term growth prospects, are larger, and exhibit greater abnormal operating income relative to tender/merger offer target firms. After controlling for fixed effects and sensitivity to variable selection, the results are robust to alternate specifications. In addition, the results indicate that private equity firms exhibit equity home bias in their target selection. Although the results reveal the economic business cycle, interest rate and legal jurisdiction of the target firm country to be insignificant determinants of target firm choice, the pooled sample descriptive statistics indicate a greater number of bids/offers in common law jurisdictions and an increase in bids/offers during peak economic cycles resultant from lowered costs of borrowing.

The remainder of this paper is structured as follows. Section 2 describes the background, market and institutional framework for private equity acquisitions. Section 3 develops the theory suggesting the macro and firm level characteristics peculiar to private equity targets. Section 4 details the empirical design, followed by section 5, which covers the data. Section 6 presents the results, and Section 7 concludes.

2. Background

Private equity investment involves the acquisition of long-term growth potential target firms, with the aim of restructuring the firm to improve its value. The restructure involves both an injection of finance and stewardship (Black and Gilson, 1998). At the end of its investment horizon, the private equity investor aims to divest the firm at a higher value, concurrently generating wealth for the investors and employees of the restructured target firm. This makes private equity investment potentially advantageous not only for investors but also for the target firm, as it introduces skilled management to identify potential risks and enhance the efficiency and profitability of the acquired firm. Furthermore, post privatisation, management are able to focus on restructuring the organisation without the obligation to conform with transparency standards and reporting standards set by regulatory bodies such as the Securities and Exchange Commission (SEC) in the United States. Using US data, McKenzie and Janeway (2011) show that the public equity market substantially influences private equity returns on exit: in favourable conditions, an IPO is associated with a median internal rate of return of 76%.

The period 2006–2007 saw increased private equity investment within Australia and internationally, with private equity deals such as Publishing and Broadcasting Limited, Coles Myer, and the abandoned Qantas takeover prominent in the Australian press. The 2007 buyout industry exhibited conditions never before seen by investors, with fund sizes, returns and access to capital at all-time highs. 1 This increase in private equity dealings saw private equity account for 25% of global mergers and acquisitions deal value and 35% of the mergers and acquisitions deal value in the United States by July 2007, with private equity investment reaching a peak in 2007. However, the boom in private equity investment was short-lived, with the 2007 credit crunch, 2008 global financial crisis, and a reduction in market confidence sharply decreasing investment activity. Shareholders increased their risk aversion, and the global private equity market contracted by 40% to $190 billion in 2008. This decrease continued during the first half of 2009, which saw AUD $24 billion in private equity acquisitions – one-sixth the size of the activity a year earlier. The buyout industry has experienced renewed growth since the global financial crisis, raising expectations of a further private equity boom and bust cycle emerging. In light of this behaviour, private equity investment has drawn attention from regulators, for example in the UK and Australia, with regard to the role and impact of this style of acquisition on the capital markets. Hence it is timely, in this period of reduced activity, to investigate these types of deals and investor preferences. For this reason, we examine acquisitions during the period 2000–2009.

3. Theory and hypothesis development

The relation between private equity bid determinants at the firm and country levels compared to other merger and acquisition technique determinants remains a topical field of discussion amongst academics, practitioners and regulators. A recent study by Chapple et al. (2010) provides evidence of the link between private equity bids and accounting information within Australia. They find target-specific characteristics (e.g. larger size of the target firm, greater financial stability, greater free cash flows, lower growth) to be positively associated with the probability of a private equity bid relative to a benchmarked sample of merger/takeover targets. The findings within Chapple et al. (2010) are supported in a US context by Boone and Mulherin (2009) and Bargeron et al. (2008), and by Achleitner et al. (2010) and De Maeseneire and Brinkhuis (2012) for continental Europe. These studies find that in addition to the information relevance of reported financials such as size and leverage, other firm-specific characteristics such as corporate governance mechanisms and agency problems (represented by managerial ownership concentration, the presence of blockholders, bid competition and free cash flows) play a significant role in private equity bids and bid premiums. Further, Bargeron et al. (2008) draw on the increased media attention to private equity investments and justifications therein to provide systematic evidence on private equity acquisitions.

This paper extends upon the above studies to incorporate an international sample, in order to test the notion that private equity targets have greater financial slack, greater financial stability, greater free cash flows and lower measurable growth prospects compared to tender/merger offer target deals. Further, country level factors are likely to affect private equity activity and these factors are tested in the models used. The following sections provide the theoretical underpinning for these hypotheses.

3.1. Financial slack

Prior literature provides conflicting evidence on the financial slack of the acquirer and target firms at the bid date. Nevertheless, consensus exists that firms whose growth-resource imbalances are opposite to those of the acquirer will be targeted (Powell, 1997). For example, an acquirer with high liquidity and low leverage and growth prospects is more likely to target a firm with low liquidity and high leverage and growth prospects. Bruner (1988) finds that acquirers have greater financial slack ex ante. This supports the credence of Myers and Majluf (1984) that slack-rich acquirers with lower leverage target slack-poor firms with higher financial leverage and growth opportunities than comparative non-target firms. Smith and Kim (1994) negate prior studies by providing evidence that highly leveraged acquirers target firms with free cash flows which can be used to service the acquisition debt of the private equity acquirer. A similar line of argument may be used in the context of private equity investment, which by its nature, relies on relatively high levels of debt to finance the acquisition.

Based on prior literature (Achleitner et al., 2010; Weir et al., 2008; Chapple et al., 2010) and the weaker bargaining position of private equity target firms compared to tender/merger offer firms, the financial slack (leverage) of the target firm is predicted to be positively (negatively) correlated to the probability of a private equity bid. Hypothesis 1a is as follows:

H1a: Private equity bid targets have greater financial slack compared to tender/merger offer firms.

3.2. Stock volatility

Private equity funds are more likely to base their decision on privately acquired information compared to tender/merger offers, where the acquirer relies on publicly or semi-publicly available information. This distinction between the type of information supporting the decision to bid will have different implications on the level of public information in the market, the stock price, and hence the volatility of returns. Hutson and Kearney (2001) consider the daily price and volume data for 112 of the largest takeover targets in Australia between 1985 and 1993. They provide evidence on the conditional price volatility of Australian target firms subsequent to the takeover announcement, and find a decline in price volatility attributable to convergence of trader opinions with respect to target stock value. The leverage of the target firm will influence the stock returns and thus pre bid/offer stock volatility. It is thereby predicted that a negative relationship exists between stock volatility and the probability of a private equity bid. Hypothesis 1b is:

H1b: Private equity bid targets have lower stock volatility compared to tender/merger offer firms.

3.3. Free cash flow

Free cash flow measures the excess cash flow over cash required to fund all positive net present value projects discounted at the appropriate cost of capital and inclusive of optimal investment in slack (Jensen, 1986; Smith and Kim, 1994). Chapple et al. (2010) find free cash flows are positive and significantly related to the probability of a private equity bid relative to a corporate takeover for Australian target firms between 2001 and 2007 inclusive. Earlier studies, such as Lehn and Poulsen (1989), find undistributed cash flows to be a significant determinant of a firm’s decision to go private, while Opler and Titman (1993) and Weir and Wright (2006) find stable free cash flows to be a significant investment criterion sought after by private equity investment firms. Conversely, Weir et al. (2004) provide evidence that free cash flows are insignificant in relation to the probability of a UK firm going private.

While prior literature provides conflicting evidence on free cash flows as a determinant of a merger, acquisition or private equity bid, the majority of studies favour the perspective that firms with greater free cash flows will be subject to a private equity bid rather than a tender offer. Higher levels of free cash flows increase shareholder wealth where the private equity acquirer reduces the misalignment of resources, and thus agency costs, post-privatisation. It is hypothesised that a positive association exists between the free cash flows of the target firm and the probability of a private equity bid. Hypothesis H1c is:

H1c: Private equity targets have greater free cash flows compared to tender/merger offer firms.

3.4. Long-term growth prospects

As private equity funds focus on long-term investment horizons, the long-term growth prospects of the target firm are a major indicator of the probability of a private equity bid rather than a tender/merger offer. A target firm’s long-term growth prospects are commonly expressed as the market to book ratio, or Tobin’s q, indicative of the firm’s current and prospective performance. In addition, the long-term growth trends of the target firm are evidenced through abnormal return on assets around the bid announcement.

Morck et al. (1988, 1989) and Bargeron et al. (2008) provide empirical evidence suggesting the share price of firms subject to a bid increases between the announcement of the bid and the privatisation date, through the premise that inefficient management will be replaced with efficient management. In addition, Palepu (1986) finds that poorer stock market performance prior to a takeover bid increases the probability of bid occurrence. However, results of recent studies across different time frames and samples conflict with Palepu (1986) (for example Ambrose and Megginson, 1992). This is attributable to the market for corporate control hypothesis that inefficient firms are easy targets for acquisition by more efficient firms (Tremblay and Tremblay, 1988 and Dietrich and Sorensen, 1984).

Kumar (1984), Fowler and Schmidt (1988) and Yook (2004) provide evidence that managerial motives of growth and financial security increase the likelihood of mergers and acquisitions. Conversely, Chatterjee (2000), Weir and Laing (2003) and Siriopoulos et al. (2006) find that correcting managerial inefficiency is not an important motive for a takeover bid, but that financially strong and profitable companies make better targets. Brown and Da Silva Rosa (1997) and, Eddey and Taylor (1999) show that target firms underperform in the pre-bid period; subsequently, however, privatisation increases firm value through the realignment of management and shareholders’ interests. In relation to private equity acquisitions, Wang (2010) finds that the monitoring provided by private equity provides a solution to agency costs (as measured by improvement in discretionary accruals quality). Overall, where management are under-utilizing assets, privatisation can reallocate assets to managers who can better optimise the firm’s resources, thereby increasing the efficiency, firm, and thus shareholder value. It is hypothesised that:

H1d: Private equity bid targets have lower long-term growth prospects compared to tender/merger offer firms.

In addition to the firm level characteristics of private equity targets discussed above, country level factors such as legal origin, the cost of finance, and cyclical conditions likely impact the pattern of private equity activity. These characteristics are discussed next.

3.5. Legal origin

La Porta et al. (1997, 1998) and Lerner and Schoar (2005) examine the significance of international legal differences on debt and equity market development. They find that legal origin, being common versus civil law, plays an integral role in financial sector development. Legal origin influences corporate transactions due to the perceived higher investor protections, stronger enforcement of shareholder rights, and the enforcement of managerial fiduciary duties present in common law countries. Common law countries are believed to afford greater choice in action rights for investors, greater protection of minority shareholders and increased consumer confidence than civil law countries.

In a private equity context, Lerner and Schoar (2004) find that legal origin is significantly related to private equity contracts, indicated by larger transaction size in common law countries. Further, Djankov et al. (2003) find the time taken for dispute resolution arising from financial investment is strongly correlated with a country’s legal origin. Thus, private contractual arrangements only partially mitigate the effects of legal origin; further, legal origin is not the sole proxy indicative of legal regime influence on capital and equity markets investment. Given the greater investor protection afforded by common law jurisdictions, ceteris paribus, such countries should exhibit greater private equity activity.

H2a: Private equity bid target firms in common law (civil law) countries have a higher (lower) probability of a private equity bid compared to a tender/merger offer, ceteris paribus.

3.6. Cost of finance

In 2007 private equity professionals attributed the precipitous increase in private equity dealings to be the result of ‘private equity firms … bask[ing] in an era of cheap money and low interest rates’. 2 Echoing this notion is an Australian Senate inquiry into changing private equity investment levels, which investigated the acquisition debt profile of private equity investors. Negative correlation between the level of interest rates and private equity bids suggests that slack-poor acquirers take acquisition debt when interest rates are lower to acquire targets with financial slack that can subsequently be used to finance acquisition debt payments. It is therefore hypothesised that lower interest rates stimulate the economy, providing capital markets with increased funds for private equity investment.

H2b: Lower interest rates result in a higher probability of a private equity bid compared to tender/merger offer firms.

3.7. Cyclical conditions

Capital markets are closely associated with economic conditions, driving the growing number and increasing value of private equity investments. When returns on equity are higher there is greater incentive for firms to replace equity with debt and undertake otherwise foregone investment opportunities. It is anticipated that market conditions will be mirrored in private equity investment trends. That is, changes in interest rates will be correlated to a country’s business cycles, reflecting boom and bust cycles. This is suggested by the leveraged buyout boom resulting from the availability and low cost of debt exhibited in the economy.

The Australian private equity market lags behind those of the US and Europe by several years, suggesting a correlation with country-specific business cycles and economic conditions, with some firms diversifying investments by vintage over the business cycle to reduce risk. Hence, the business cycle is predicted to influence private equity investment dependent on the stage of the country’s boom and bust cycles. It is hypothesised that private equity bids exhibit greater occurrence during periods leading to a peak in economic activity, due to higher returns on equity and prospective investment opportunities. Hypothesis 2c is:

H2c: Private equity target firms in countries experiencing a peak (trough) have a higher (lower) probability of a private equity bid comparative to a tender/merger offer.

3.8. Equity home bias

As private equity markets are often characterised by information asymmetry and agency problems at the outset, the geographical proximity of the target firm to the acquirer is expected to exhibit an equity home bias, defined as the target firm being within the same country as the acquirer’s headquarters. To avoid overexposure to country-specific risks, private equity funds have the opportunity to diversify in target firms globally. Previous research in mergers and acquisitions shows that foreign bidders are attracted to larger targets, for which there is some technological synergy for the bidder (Harris and Ravenscraft, 1991). In relation to foreign bidders for Australian listed targets, Bugeja (2011) finds that foreign bidders acquire larger targets, with research intensity, for which they will pay a higher premium (more frequently in the resources sector). However, these characteristics do not appear to be the preferences of private equity acquisitions. Conversely, prior literature (such as Cumming and Dai, 2007; Lerner, 1995; Sorenson and Stuart, 2001 and Tian, 2007) focuses on the US venture capital market and finds such an investment bias to exist in the market across provinces in the US. This is consistent with the research of Coval and Moskowitz (1999, 2001), who find a geographically proximate preference within a 100-kilometre radius for investments in publicly traded firms. These findings are consistent with venture capital research by Lerner (1995) and Gompers and Lerner (1999), who provide evidence that venture capitalists exhibiting a closer proximity to the investee firm are more likely to serve on the firm’s board of directors post-acquisition, subsequently wielding greater influence on the operating and investment decisions of the target firm. Further, Fong et al. (2008) follow the provincial approach of Coval and Moskowitz (2001) using Australian data, and find an overweighting by Sydney and Melbourne fund managers in favour of Melbourne stocks.

This research considers whether private equity bids exhibit an equity home bias, and further, whether the firm and country specific characteristics of the target firm change based on the geographical proximity of the target firm’s country to the acquirer firm’s country: that is, whether foreign target firms exhibited different target characteristics to geographically proximate target firms between 2000 and 2009 inclusive. In light of the research results cited above, it is expected that an intraprovincial bias exists within the US, where US based private equity acquirers in one state target US based firms in a different state. Based on prior literature, hypothesis 3 is:

H3: Private equity bids exhibit home bias compared to tender/merger offer firms.

4. Empirical design

A binary logistic model is used to test the relationship between firm-specific and country-specific characteristics on the probability of a private equity bid compared to a tender/merger offer. The model by Chapple et al. (2010) is expanded to include target firm and country specific characteristics reflective of country level differences of target firms which are likely to influence the probability of a private equity bid. Additionally, firm specific characteristics, including annualised volatility and abnormal operating income, are included as indicators of pre bid/offer performance.

4.1. Firm specific variable data

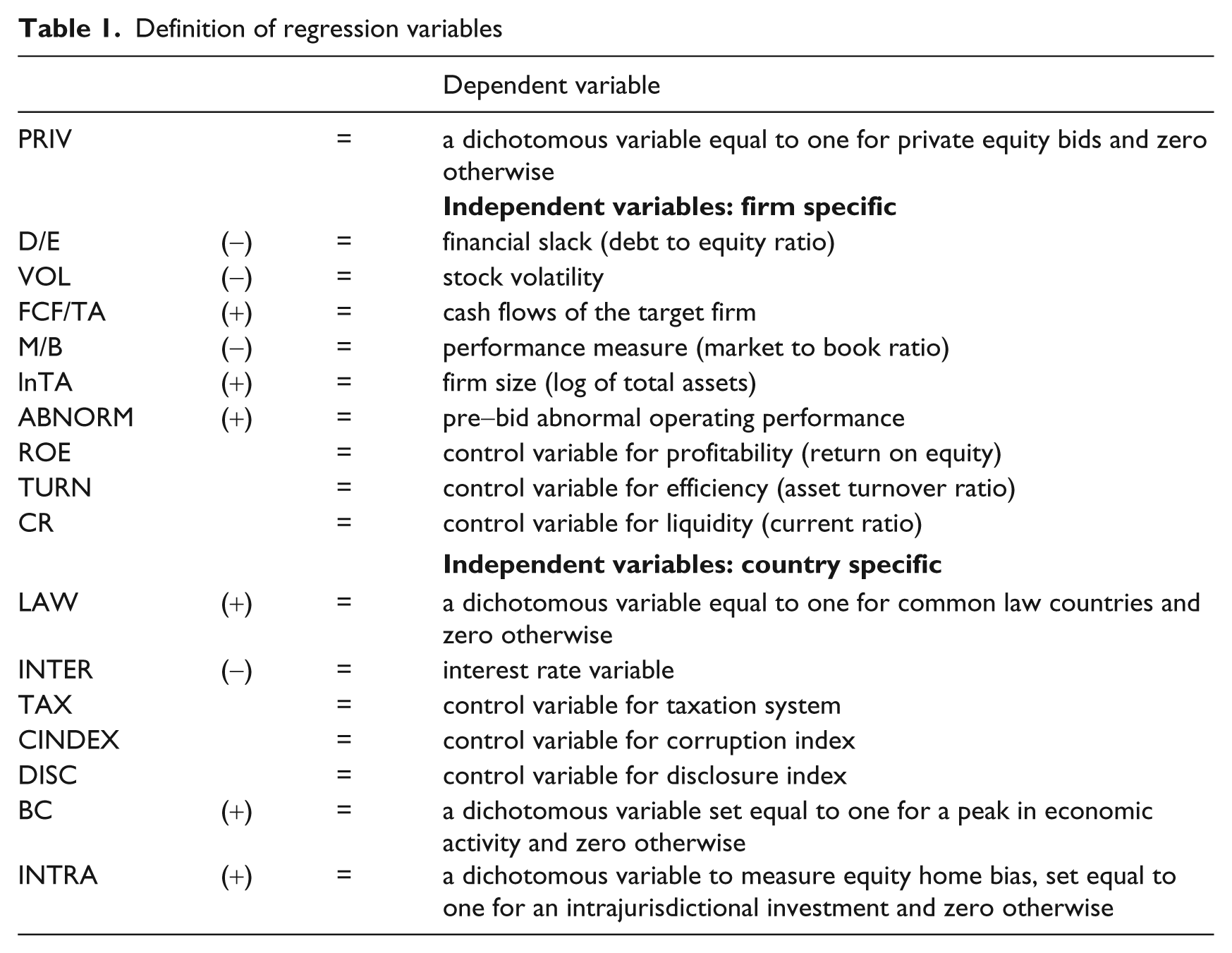

The variable of interest, PRIV, is a dichotomous variable set to ‘1’ for firms subject to a private equity bid and ‘0’ for a tender/merger offer. Each of the firm-specific characteristics of a private equity bid target firm, including size, leverage and profitability, are measured by size (lnTA), financial slack (D/E), free cash flows (FCF/TA), growth (M/B), stock volatility (VOL) and abnormal operating performance (ABNORM). A number of control variables for profitability (ROE), efficiency (TURN) and liquidity (CR) are used to account for the differences in the target firm’s internal characteristics.

4.2. Average total assets and market value of equity

Average total assets is calculated as the average between the bid-year total assets and those of the prior financial year. The market value of equity is determined by common shares outstanding multiplied by the price per share.

4.3. Stock volatility

Stock volatility is measured as the volatility of each firm’s stock returns over the 60 days prior to the bid/offer month, and is matched to the corresponding private equity bid or tender/merger offer by the bid/offer date and firm identifier. The volatility measure represents the daily logarithmic returns of stock (σd). Since this research considers stock volatility between private equity bid and tender/merger offer firms in conjunction with fiscal year data, the square root of time rule is used to annualise the daily volatility of stock returns. This is supported by the study firm’s demonstrating Brownian motion indicating that volatility increases with the square root of the unit of time. The daily volatility of stock returns is annualised (σa) by multiplying the daily volatility measure by the square root of 252, being the number of trading days in a given year where prices are subject to change. This yields an approximately correct annualized volatility measure as the daily volatility measure is calculated based upon simple returns.

4.4. Abnormal operating income

Prior studies such as Kaplan (1989), Mikkelson and Shah (1994) and Holthausen and Larcker (1994) use operating income before depreciation to determine abnormal operating income for management buyouts, initial public offerings and reverse leverage buyouts respectively. The use of operating income before depreciation does not take into consideration the comparison being made with fiscal year-end asset valuation post-depreciation. Hence, this study uses operating income after depreciation to calculate return on assets (ROA), as it represents the end of fiscal year operating income relative to the value of assets after accounting for asset usage over the fiscal year. Abnormal operating income is the firm’s operating income after depreciation divided by average total assets (ROA) minus the control operating income for each firm i, where i represents the private equity bid or tender/merger offer firm. 3

The pooled study sample, consisting of private equity bid and tender/merger offer target firms, is assigned a random number for each firm observation and is matched on country, fiscal year and GICS code to the abnormal operating performance (ROA) control sample, consisting of all firm observations from COMPUSTAT not previously matched to a private equity bid or tender/merger offer firm. 4 The control sample firm observations matched to a study firm observation are grouped according to the random number assigned to each study firm observation and the mean ROA calculated for each group. The mean is taken as the control operating income (ROA) for each firm.

4.5. Currency

All fiscal year accounting data is converted into United States dollars (USD) according to the exchange rate at the data date for the private equity bid and tender/merger offer study samples and the abnormal operating performance control sample. Daily currency exchange rates are from Worldscope and are matched to firm observations by the International Organisation for Standardisation (ISO) currency code. Where the conversion date falls on a weekend the preceding Friday’s exchange rate is used.

4.6. Country specific variable data

For the country specific determinants, LAW is a dichotomous variable set to ‘1’ for target firms in a common law country and ‘0’ if the target firm is in a civil law country. Further, an interest rate variable (INTER) is included to indicate the relationship between interest rates and private equity bid or tender/merger offer investment at the bid/offer date. A dichotomous variable (BC) is set to ‘1’ for a peak in the respective country’s economic activity in the year of the initial bid/offer and ‘0’ otherwise. 5 A dichotomous variable (INTRA) is included to provide analysis of the intrajurisdictional bias associated with private equity bids. Control variables for taxation (TAX), corruption (CINDEX) and disclosure (DISC) are used to account for extraneous factors in country-specific characteristics that may influence LAW, INTER and/or INTRA (La Porta et al., 1997).

4.7. Legal indices

Additional country specific variables, including the rule of law, judicial system, risk of expropriation, risk of contract repudiation, corruption index, disclosure index and the efficiency of the judicial system were obtained from La Porta et al. (1998). This research uses the judicial system, corruption and disclosure indices in the main regression. To check the robustness of the results the corruption index and disclosure index are substituted by the risk of contract repudiation and the efficiency of the judicial system respectively.

4.8. Equity home bias variables

Equity home bias is defined as ‘intrajurisdictional’, where the acquirer and target reside in the same country, and ‘intraprovincial’, where the acquirer and target reside in the same state (for US firms). An intrajurisdictional identifier is set to ‘1’ where the private equity bid or tender/merger offer is within the same country and ‘0’ otherwise. For the United States an identifier (ITRAUS) is set to ‘1’ for intraprovincial bids/offers where the target state is the same as the acquirer state and ‘0’ otherwise. Additionally, a variable (US) is set to ‘1’ for the United States and ‘0’ otherwise to test for robustness between the US and the remaining countries in the pooled sample.

4.9. Interest rates

Monthly United States federal funds target interest rates are obtained from WorldScope for 2000–2009. Once allowing for interest rate parity it is expected that interest rates remain the same across countries at a given point in time; therefore the US rate is used as a proxy for all countries in the sample.

4.10. Taxation

The taxation variable indicates whether the country has a classical or imputation taxation system. The corporate taxation rate is used to test for robustness, as the corporate tax rate may change significantly across time, whereas the taxation system may remain constant. The corporate tax rate for each sample year and country are obtained from KPMG’s Corporate and Indirect Tax Rate Survey 2009. 6 The corporate taxation rate is the country wide corporate rate; however a number of countries, for example the United States, use a combination of federal corporate income tax and state and local government taxes. Therefore, the United States corporate tax rate is the estimated average rate applied.

4.11. The model

Using the variables described above, this study tests the association between these factors relating to the bid and bid preferences and whether the bid was by a private equity acquirer. Table 1 specifies in full the regression variables. The logistic regression in this study is expressed as

where β1 through β9 pertain to the firm specific characteristics of a private equity bid compared to a tender/merger offer and β10 through β16 to country specific characteristics of a private equity bid compared to a tender/merger offer. The following section presents data collection for each of the variables necessary for the aforementioned regression.

Definition of regression variables

5. Data

5.1. Sample selection

The initial sample consists of firms subject to a private equity bid and a matched sample of tender/merger offer firms between 2000 and 2009, from the mergers and acquisitions database on Securities Data Corporation Platinum (SDC Platinum). The inclusion of private equity bid and tender/merger offer target firms allows for the identification of differences between the firm and country specific characteristics of firms subject to a private equity bid and the matched tender/merger offer firms.

The initial private equity target firm sample consists of firms categorised under the acquisition technique ‘leveraged buyout’ flag producing an initial sample of 13,883 target firms, and is exclusive of government and government controlled entities. The initial comparison tender/merger offer firm sample comprises 2986 target firms categorised under the acquisition technique ‘tender/merger’ flag for the initial 15 private equity bid countries with business cycle (peak and trough) data available through the Economic Cycle Research Institute. The tender/merger offer firms indicate a tender offer to acquire control of the target firm subsequently followed by a merger agreement. The initial sample includes firms from fifteen countries: Australia, Austria, Canada, France, Germany, India, Italy, Japan, New Zealand, South Korea, Spain, Sweden, Taiwan, the United Kingdom and the United States of America. The private equity sample is reduced to include only firms where the Acquirer’s Short Business Description characterises it as a private equity firm or fund, reducing the sample to 3436 target firm observations. The comparison tender/merger offer firm sample is reduced to include only firms not classified as a private equity acquirer, thus removing the possibility of duplication between the study and control target firm observations. This reduces the control group to 2959 tender/merger offer target firm observations.

Private equity bid and tender/merger offer firms without a CUSIP (Canada and United States) or SEDOL (Global) are excluded from the sample, reducing the private equity bid and tender/merger offer firms to 2056 and 2696 target firm observations, respectively. After omitting duplicate observations which may have resulted from the publicity of the first private equity bid or tender/merger offer, and observations with incomplete or insufficient data to meet the model requirements, the sample reduces to 227 and 1922 firms, respectively. A unique identifier for each firm observation in the private equity bid, tender/merger offer and abnormal operating performance control samples is created to reflect CUSIP for the Canada/United States firms and SEDOL elsewhere.

Financial data is for the fiscal year immediately preceding the private equity bid or tender/merger offer year, to reflect accounting information relevant to the decision to make a bid/offer on the target firm. The private equity bid target firm sample includes 146 firms, determined by the intersection of the private equity bid target firm sample and the availability of fiscal year data. The comparison tender/merger offer firm sample is 1195 firms, determined by the intersection of the tender/merger offer target firm sample and the availability of fiscal year data.

The private equity bid target firms are matched without replacement to the tender/merger offer target firms by country, bid/offer year and two-digit GICS code, resulting in a final study sample of 115 private equity bids and 380 tender/merger offers. These firms span seven countries with free and well-developed equity markets as outlined by the FTSE Group’s developed market list, including four common law countries (Australia, Canada, the United Kingdom and the United States) and three civil law countries (France, Germany and Sweden). The exclusion of emerging market countries prevents distortion of the importance of country specific determinants resultant from less economical integration with developed market countries. Country specific variables are matched to the private equity bid and tender/merger offer target firm observations by country, year and month.

6. Results

6.1. Descriptive statistics

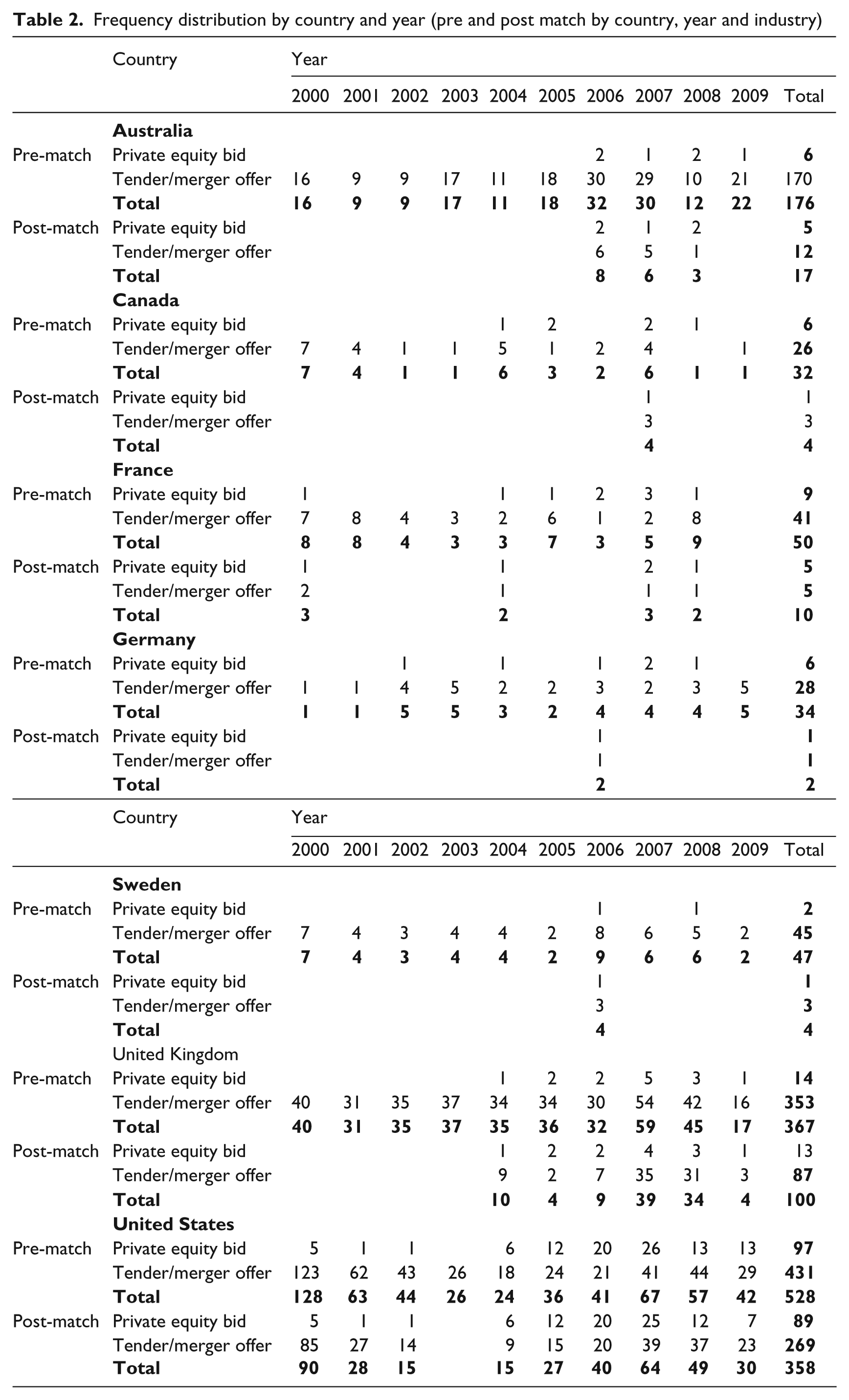

Table 2 presents the frequency distribution by country, year and pre and post-match private equity bid and tender/merger offer. The distribution highlights an increase in private equity bids over the period 2005–2007, with a decline in bids in 2008–2009. During the 2005–2007 period the proportion of private equity bids relative to tender/merger offers is higher. The distribution may be attributable to the favourable conditions for private equity investment, including lowered interest rates, in 2006–2007. 7

Frequency distribution by country and year (pre and post match by country, year and industry)

Table 3 presents the frequency distribution by industry pre and post-match. The consumer discretionary and information technology sectors exhibit the highest frequencies, with 38 and 32 post-match private equity bid target firm observations. The high number of information technology observations is unsurprising, with technological advances during the 2000–2009 period increasing consumer and investor confidence in this profitable, yet volatile, sector. The consumer discretionary sector represents favourable returns to investors, and thus increased marketable opportunities for investors within the sector due to increased consumer demand resulting from increased consumer wealth.

Frequency distribution by industry (pre and post match by country, year and industry)

Table 4 presents the descriptive statistics for the independent and control variables separately for the pooled sample, private equity bids and tender/merger offers. The pooled sample statistics indicate that volatility, free cash flows, market to book, firm size, abnormal operating income, current ratio, equity home investment, taxation system and disclosure index have means statistically different from zero. On average the standard deviation for firm-specific characteristics is higher for tender/merger offer target firms relative to private equity bid target firms. The direction of the mean of free cash flows for a private equity bid is positive (0.02070) whereas for free cash flows for tender/merger offers it is negative (-0.01427). This strengthens the argument that private equity bid target firms have greater free cash flows pre-bid than similar firms subject to tender/merger offers. The mean volatility suggests, on average, that tender/merger offer target firms experience greater volatility (0.68945) pre-offer than comparative private equity bid targets (0.45317). Abnormal operating income for private equity bid and tender/merger offer target firms have positive mean values; however, the private equity bid target firms’ are higher (1.05481) than the tender/merger offer target firms’ (0.47660). The country-specific characteristics are similar across private equity bid target firms and the control group.

Private equity bids and tender/merger offers descriptive statistics

Descriptive statistics for all firms subject to a private equity bid or tender/merger offer on SDC Platinum between 2000 and 2009 with financials data available on COMPUSTAT. The dichotomous variables (LAW, INTRA, BC and TAX) are included for completeness. The mean represents the proportion of target firms in common law countries, intrajurisdictional bids/offers, bids/offers in a peak economic state and target firms in countries with a classical taxation system respectively.

There are two methods for computing the systematic differences in the descriptive statistics over the study and control groups (standard error in the difference of the means (t-test Pr > |t|)). The method used is dependent on the variance of the study and control groups. Where the equality of variances significance probability is less than α=0.05 (Pr > F) it provides evidence that the variances of the private equity bid and tender/merger offer groups are different and the Satterthwaite method is used to test the difference between the means of the private equity bid and tender/merger offer groups. Where the equality of variances significance probability is greater than α=0.05 the pooled method is used. Where the probability is less than α=0.05 the difference in means is statistically significant from zero.

Table 5, Panels A and B provide Spearman correlation coefficients for the private equity and merger control samples respectively for all variables included in our regression model, including control variables. Notably, in Panel A, the annualised volatility of private equity bid targets is significantly negatively correlated with the business cycle variable BC (correlation coefficient of -0.41). While this is also the case for the control sample (Panel B), the magnitude of the correlation is far lower (correlation coefficient of -0.15), implying that the stock volatility observed for the private equity bid sample is more likely attributable to cyclical factors. In Panel B, the size variable LnTA is significant, and is negatively correlated with annualised volatility and positively correlated with free cash flow. These associations are insignificant for the private equity bid firms (Panel A), suggesting the absence of a size effect explaining these variables. Additionally, there are a number of correlations exceeding 50%, including return on equity and market to book (tender/merger control sample only), business cycle and interests rates, taxation system and corruption and disclosure indices. The correlation between interest rates and business cycle is expected, as changes in interest rates impact on national and global capital markets. With respect to the private equity bid correlation matrix, return on equity and market to book are no longer correlated and the home bias and tax system variables (INTRA and TAX respectively) are correlated, suggesting tax advantages may contribute to a foreign target choice.

Tables of cross correlations

6.2. Results discussion and analysis

The results from the binary logistic regression and fixed effects regressions are tabulated in Table 6. Fixed effects models are run on the premise that country specific variables are independent of firm specific variables; thus fixed effects regressions control for country and year fixed effects reducing the threat of omitted variable bias. The results provide the maximum likelihood estimates from the primary regression adjusted for serial correlation in the disturbance terms country and year. The logistic regression is double clustered by firm and country. The Pseudo R 2 for the main regression is 0.2297. After controlling for fixed effects by country and year, the Pseudo R2 is 0.2999.

Logistic regression results

This table presents the summary binary logistic regression results from the following model

where PRIV is a dichotomous variable set equal to PRIV=1 for private equity bids and PRIV=0 for tender/merger offer firms observations from SDC Platinum. D/E is long-term debt (total) divided by common/ordinary equity (total), VOL is stock volatility 60 days prior to the bid/offer date, FCF/TA is (operating activities net cash flow minus capital expenditures) divided by total assets, M/B is market value of equity divided by common/ordinary equity (total), lnTA is log of total assets, ABNORM is (operating income (after depreciation) divided by average total assets) minus control operating income, ROE is net income divided by common/ordinary equity (total), TURN is sales/turnover(net) divided by average total assets, CR is current assets (total) divided by current liabilities. LAW is a dichotomous variable set equal to ‘1’ for common law countries or ‘0’ for civil law countries (La Porta et al., 1998), INTER is the interest rate variable (Worldscope), TAX is a control variable for taxation system (KPMG’s Corporate and Indirect Tax Rate Survey 2009), CINDEX is the corruption index (La Porta et al., 1998), DISC is the disclosure index (La Porta et al., 1998), BC is a dichotomous variable set equal to ‘1’ for a peak in economic activity and ‘0’ otherwise (Economic Cycle Research Institute) and INTRA is a dichotomous variable set equal to ‘1’ for an intrajurisdictional investment and ‘0’ otherwise (SDC Platinum). All financials data is for the fiscal year preceding the private equity bid or tender/merger offer from COMPUSTAT. The comparative analysis between the probability of a private equity bid relative to a tender/merger offer given firm-specific and country-specific characteristics is calculated on a pooled sample of n=495, where n=115 private equity bids (PRIV = 1) and n=380 tender/merger offers (PRIV = 0) matched by country, year and 2-digit GICS code. The maximum likelihood estimates of a private equity bid are compared to a tender/merger offer with (2) and without (1) control variables. Fixed effects regressions are included to control for (3) year, (4) country, (5) country and year.

P-values are reported below the coefficient estimates in italics, and are corrected for heteroskedasticity and auto-correlation in the residuals.

,** and * denote a statistically significant difference at the 1%, 5% and 10% levels, respectively.

6.2.1. Firm-specific determinants

The results provide evidence that annualized volatility, market to book, firm size and abnormal operating income are all significant determinants of a private bid relative to a tender/merger offer. Annualised volatility is negative (-1.5832) and significantly associated with the probability of a private equity bid at the 1% level (0.0003), and at the 5% level when accounting for fixed effects by year (0.0279) and by country and year (0.0189). These results provide a strong argument for the market for corporate control hypothesis. Firms experiencing high volatility have a greater probability of a tender/merger offer to enhance shareholder value through efficient managerial practice relative to private equity target firms. Subsequent to the announcement of a merger attempt the target firm’s stock price increases in value; however, the greater the uncertainty surrounding the merger, the greater the volatility. Further, the acquirer’s managers know more about private equity target firms pre-bid compared to tender/merger offer target firms, where acquirers rely heavily on public information reflected in the stock price. Therefore, private equity bid target firms are more stable but experience managerial inefficiency, suggesting acquirers are more risk averse than tender/merger offer acquirers.

Results also show a significantly negative (-0.1085) association at the 10% level (0.0505) between a private equity bid and the target firm’s market to book ratio relative to a tender/merger offer. The lower market to book ratio attributable to private equity bids may be due to different acquisition techniques. Mergers are more likely to be between businesses in a similar sector or line of business; therefore post-merger changes to the target firm will be nominal. Private equity acquirers target firms irrespective of poorer operating performance relative to the market, are not constrained by synergistic ‘line of business’ targets and therefore are in a better position post-privatisation to make value enhancing operational changes. Firm size as measured by log of total assets is positively (0.2388) significant at the 1% level (0.0064), and after adjusting for fixed effects firm size is significant at the 5% level. These results indicate larger firms have a greater probability of a private equity bid relative to a tender/merger offer. One rationale is that private equity acquirers target large public companies they can take private, restructure and sell to another private equity investor or re-float. The payoff of these deals is significant for the private equity acquirer. Conversely, mergers are less concerned with target firm size and generally acquire firms with the view of monopolising or expanding their percentage hold over a particular industry or product line. In this respect, mergers exhibit a synergy whereby the acquirer and target firm cooperate advantageously to generate maximum profit after the merger.

Abnormal operating income is positively (0.1926) significant at the 5% level (0.0269); however, when controlling for fixed effects it is insignificant when year is included. Private equity bids therefore have a greater abnormal operating income relative to the tender/merger offer firms. This indicates that private equity acquirers prefer target firms that are better performers compared to similar merger firms in the same country, year and industry. Private equity acquirers therefore target firms requiring minimal operating restructure in terms of assets relative to operating performance.

Results also show that debt to equity (0.0546) and free cash flows (0.5094) are positively associated with, but insignificant determinants of, a private equity bid relative to a tender/merger offer. The control variables return on equity (-0.0937) and current ratio (-0.1406) are negatively correlated to a private equity bid. The current ratio is negatively significant at the 10% level (0.0749) and at the 5% level after accounting for fixed effects by country and year (0.0344).

Overall, the results support the hypotheses that private equity target firms exhibit lower stock volatility and long-term growth prospects, are larger and exhibit greater abnormal operating income relative to tender/merger offer target firms.

6.2.2. Country-specific determinants

The results indicate that legal origin is negatively (-1.0163) significant (0.0742) at the 10% level without the control variables included in the regression, and insignificant otherwise. This rejects the hypothesis that investors prefer common law over civil law countries.

The remaining country specific determinants are insignificant; however the results indicate association as hypothesised. There is a positive relationship between a peak in economic activity within a country and the probability of a private equity bid (0.0176). This is in conjunction with a negative correlation between interest rates and private equity investment (-0.0911). The relationship between business cycles and interest rates suggests business cycles are dependent on interest rate changes. The taxation system, corruption and disclosure indices are statistically insignificant.

6.2.3. Equity home bias

The results indicate that the choice between a local or foreign target is a positive (1.0140) and significant (0.0060) determinant of private equity bid probability relative to a tender/merger offer. As hypothesized, private equity acquirers target firms within the same country. Post-privatisation, it is intuitive that the acquirer prefers to be in close proximity to the target and in a position to restructure the board and managerial composition to achieve greater efficiency. There is also an incentive to target geographically proximate firms to reduce the cost base of restructuring post-privatisation, where specialised professionals are able to commute between the acquirer and the target firm during the restructuring. Mergers are more diversified across countries, especially where the acquirer seeks synergy to break into an international product market or achieve market monopolisation. Adjusting for fixed effects does not affect the significance of intrajurisdictional investment for private equity bids (0.0082).

6.3. Sensitivity analysis and robustness

Nine regressions are run for robustness to test for differences in the maximum likelihood estimates due to variable proxy selection and country undue influence. Table 7 presents the regression results for robustness and sensitivity to variable proxy choice. The results are consistent with the main regression, Table 6, with the exception of interjurisdictional investment (14). Regression 9 provides conflicting results, with debt to equity and interest rate significant at the 10% level and taxation system at the 5% level. The results controlling for United States and non-United States target firms provide consistent results for the United States but insignificant results for non-United States target firms, with the exception of firm size. This may be attributable to the small number of non-United States targets. Similar results are seen in regressions 9 and 10.

Robustness results

This table presents the summary binary logistic regression robustness results from the following model

where PRIV is a dichotomous variable set equal to PRIV=1 for private equity bids and PRIV=0 for tender/merger offer firms observations from SDC Platinum. D/E is long-term debt (total) divided by common/ordinary equity (total), VOL is stock volatility 60 days prior to the bid/offer date, FCF/TA is (operating activities net cash flow minus capital expenditures) divided by total assets, M/B is market value of equity divided by common/ordinary equity (total), lnTA is log of total assets, ABNORM is (operating income (after depreciation) divided by average total assets) minus control operating income, ROE is net income divided by common/ordinary equity (total), TURN is sales/turnover (net) divided by average total assets, CR is current assets (total) divided by current liabilities. LAW is a dichotomous variable set equal to ‘1’ for common law countries or ‘0’ for civil law countries (La Porta et al., 1998), INTER is the interest rate variable (Worldscope), TAX is a control variable for taxation system (KPMG’s Corporate and Indirect Tax Rate Survey 2009), CINDEX is the corruption index (La Porta et al., 1998), DISC is the disclosure index (La Porta et al., 1998), BC is a dichotomous variable set equal to one for a peak in economic activity and zero otherwise (Economic Cycle Research Institute) and INTRA is a dichotomous variable set equal to one for an intrajurisdictional investment and zero otherwise (SDC Platinum). All financials data is for the fiscal year preceding the private equity bid or tender/merger offer from COMPUSTAT. The maximum likelihood estimates of a private equity bid compared to a tender/merger offer: (6) US target firms, (7) non-US target firms, (8) intrajurisdictional investment, (9) interjurisdictional investment, (10) within US intraprovincial investment (INTRA = intraprovincial), (11) within US interprovincial investment (INTRA = interprovincial), (12) with repudiation of contracts as CINDEX and efficiency of judicial system as DISC, (13) with maximum corporate taxation rate as TAX and, (14) without business cycle variable.

P-values are reported below the coefficient estimates in italics, and are corrected for heteroskedasticity and auto-correlation in the residuals.

,** and * denote a statistically significant difference at the 1%, 5% and 10% levels, respectively.

The results indicate that intrajurisdictional investors consider the taxation system and corruption as significant determinants of private equity bids over tender/merger offers. The provincial investment results for the United States provide scant support for the hypothesised results, with the exception of annualised volatility for interprovincial investments. These results also provide evidence on the sensitivity of variable choice as proxies for the determinants of private equity bid target firm choice. Chapple et al. (2010) use alternative proxies for each of the target firm characteristics with robustness tests indicating the results are not sensitive to the choice of proxy for each attribute.

This study primarily used the country specific characteristics of legal origin, corruption and disclosure indices. Following La Porta et al. (1998), the corruption index (CINDEX) and disclosure index (DISC) are substituted by the risk of contract repudiation and the efficiency of the judicial system indices respectively, as shown in Regression 12. Regression 12 finds repudiation of contracts to be a negatively significant determinant of a private equity bid at the 5% level. This indicates that the higher the country’s contract repudiation, the lower the probability of a private equity bid relative to a tender/merger offer. Regression 13 replaces the dichotomous taxation system variable with the maximum corporate taxation rate by country and year for each firm observations bid/offer date. These results are consistent with the main regression. Regression 14 controls for the significant correlation between business cycles and interest rates by removing the business cycle variable from the regression. The business cycle variable is omitted as changes in interest rates influence country business cycles. The coefficients are similar to the main regression; however, the interest rate is less insignificant (0.1801).

Overall, the robustness and sensitivity results support the main regression and hypotheses that market to book and current ratio are significant at the 10% level, abnormal operating income is significant at the 5% level and volatility, firm size and intrajurisdictional investments are significant at the 1% level.

7. Conclusion

The results reveal that relative to tender/merger offer target firms, private equity bid target firms have lower stock volatility and long term growth prospects, but are larger in size and exhibit intra-provincial bias. These results indicate that private equity investors place greater reliance on firm specific characteristics (internal determinants) over country specific characteristics (external determinants). This can be explained through diversification of country specific risks by the acquirer. Strategically structured deals and low risk target firms mitigate country specific determinants such as corruption and disclosure indices. In this respect, the current regulatory avenues governing private equity investment internationally are adequate to support changes in economic conditions, as the results reveal that acquirers focus on firm specific characteristics by controlling for adverse country specific characteristics such as corruption and disclosure through investment contracts. Equity home bias is expected as private equity investors prefer a closer proximity to the target firm for ease of restructuring and corporate control. The results are thereby indicative of greater reliance on firm specific characteristics over country specific characteristics.

Specifically, this study proposed three sets of hypotheses regarding global private equity deals in comparison with tender offer/merger deals. First, regarding firm characteristics, we hypothesised that private equity bid targets have greater financial slack, lower stock volatility, greater free cash flows and lower long term growth (measured by market to book). The results support these predictions, except for the free cash flow hypothesis. Second, regarding private equity bid targets and country characteristics, we hypothesised that target firms in common law countries have a higher probability of a private equity bid, and that lower interest rates and a peak business cycle would result in a higher probability of a private equity bid. The results do not support these hypotheses. Finally, we hypothesised and found evidence that private equity bids exhibit home bias compared to tender/merger offer firms.

The hypothesised direction for business cycles, interest rates and jurisdiction are reflected in the composition of the pooled sample. A greater number of private equity bids and tender/merger offers occur in economies experiencing a peak relative to those experiencing a trough. The results support earlier studies that market to book, firm size and abnormal operating income are significant determinants of private equity bid likelihood. This study provides a unique perspective on private equity bid probability relative to a tender/merger offer. In contrast to prior research, this study draws direct inferences between the two acquisition techniques, rather than using a control sample of pooled acquisition techniques. Further, this study provides evidence that stock volatility is greater for tender/merger offer target firms relative to private equity bid target firm observations 60 days prior to the bid/offer.

Private equity investment has grown to be a valuable asset class in capital markets in the past decade. This paper provides empirical evidence on the internal and external determinants of private equity bids relative to a tender/merger offer. The results provide evidence that firm specific characteristics were relied upon to a greater extent than country specific characteristics in the seven developed countries included in this research for the study years 2000–2009, inclusive. The paper offers evidence that preconceived notions about private equity investment funds targeting underperforming firms are inaccurate, with stock volatility greater for tender/merger offer firms relative to private equity target firms that exhibit higher abnormal operating income and lower stock volatility pre-bid.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.