Abstract

This paper explores the impact of market discipline on bank risk taking. We examine a broad sample of financial institutions from the G7 nations over the period 1996–2010. We apply System Generalized Method of Moments estimation to control for endogeneity and other unobserved heterogeneity in a dynamic panel setting. Our analysis suggests that market discipline helps reduce bank risk (both equity and credit risk). Moreover, we find that this negative impact of market discipline is stronger: (a) in the presence of a risk-adjusted insurance premium; and (b) during the post-global financial crisis period. However, the disciplinary effect of market discipline is not enhanced in the presence of bank capital. We highlight the policy implications of these findings.

1. Introduction

Does market discipline impact bank risk in the way that regulators would hope? In this paper, we seek an answer to this question by developing and testing a conditional model of bank risk taking (both equity and credit) with the primary focus being on the role of market discipline, as captured by the degree of uninsured debt used by each bank. The core prediction is that market discipline will induce lower bank risk (Nier and Baumann, 2006).

The systemic problems in the finance sector that followed the global financial crisis (GFC) 2007/2008 provide a key impetus to improving our understanding of the determinants of bank risk. Evaluating bank risk is important to regulators/supervisors, borrowers, stock and bond holders. Regulators (including implicit and explicit safety net providers) and supervisors, who are responsible for maintaining financial stability, have a keen interest in bank risk taking due to the costs associated with bankruptcy, contagion and possible disruption in the allocation of credit.

In the banking sector, market discipline can be defined as a process in which private sector agents (stockholders, depositors or creditors at large) who face costs that increase as banks undertake risk, take countervailing action on the basis of these costs (Berger, 1991). For example, uninsured depositors such as subordinated debt holders, who are quite exposed to bank risk taking, might penalize riskier banks by requiring higher interest rates or by withdrawing their deposits (Martinez-Peria and Schmukler, 2001). Goldberg and Hudgins (2002) argue that any reduction in the level of uninsured liabilities corresponding with increasing bank risk will support the existence of market discipline. In this way, the banks are disciplined or penalized by the collective force of actions taken by market participants, aimed at protecting their interests. Moreover, the mere “threat” of such market discipline can plausibly inhibit or influence the decision making of banking firms toward more conservative/safer positions.

Theory suggests that for a given increase in bank risk, the resulting market discipline is likely to have a stronger cost impact the larger is the amount of uninsured funding. For example, Gropp and Vesala (2004) find that banks with a larger share of uninsured funding have incentives to take less risk. Similarly, Nier and Baumann (2006), provide evidence of effectiveness of uninsured funding as a measure of market discipline.

Further, there has been a number of proposals (e.g., Bank for International Settlement, 2003) supporting for increased use of subordinated debt, where banking activities are becoming more opaque. The use of market discipline for prudential purposes has also gained considerable importance in recent years as policymakers, increasingly attuned to its likely beneficial role, have incorporated it in their regulatory frameworks. This is best exemplified by the codification of market discipline as one of the three pillars in the supervisory architecture for internationally active banks (Basel II) (Stephanou, 2010). In particular, Pillar 3 recognizes that market discipline has the potential to reinforce capital regulation and other supervisory efforts to promote safety and soundness in banks and financial systems. Thus, market discipline can provide banks with an incentive to maintain a strong capital base as a cushion against potential future losses arising from their risk exposure.

Typically, interbank deposits are not covered by explicit deposit insurance schemes. In addition, banks are likely to be informed investors in the interbank market. A lending bank may be subject to the same kinds of shocks to risk and profitability as the borrowing bank (Nier and Baumann, 2006). As a result, interbank deposits are likely to be sensitive to the risk the borrowing bank is taking. Consistent with this argument, Ellis and Flannery (1992) find that interbank rates paid by large US money center banks include significant default risk premia. A number of studies (e.g., Flannery, 1998; Gropp and Vesala, 2004; Sironi, 2003) have shown that subordinated debt spreads reflect the risk profile of the bank. 1 Thus, we follow the work of Nier and Baumann (2006) and consider uninsured liabilities including interbank deposits and subordinated debt as a measure of market discipline. Our paper contributes to the existing strand of literature by analyzing the importance of market discipline during the GFC which, as yet, has not been scrutinized in any research on the determinants of bank equity risk. Our study also employs the dynamic panel data method to determine the impact of market discipline, and financial crisis on bank risk. In particular, we apply System Generalized Method of Moments (GMM) developed by Arellano and Bond (1991), then improved by Arellano and Bover (1995) and Blundell and Bond (1998). Further, following the theoretical work of Gorton and Santomero (1990), we contribute to the literature by, for the first time, empirically examining the possibility of a non-linear association between market discipline and bank risk. Finally, our sample of banks is drawn from a set of countries that were affected by the financial crisis to varying degrees. Thus, this gives us sufficient variability across the sample, which is important to detect any meaningful relationship between market discipline and bank risk.

Using bank balance sheet and market information for a sample of 288 financial institutions across seven developed nations (G7 countries: Canada, France, Germany, Italy, Japan, UK, USA) over the period 1996–2010, we document that bank risk is negatively related to market discipline. Our findings also show that the disciplinary effect of market discipline is not enhanced in the presence of bank capital (i.e., Tier 1 ratio). This finding is likely to disappoint regulatory bodies who strive to promote the complementary power of bank capital and market discipline to maintain financial stability. Further, we find that the impact of market discipline on bank risk is stronger in the presence of a risk-adjusted insurance premium. Finally, there is evidence that market discipline has a greater impact on bank risk in the post-GFC crisis period.

The remainder of the paper is structured as follows. Section 2 presents a literature review and provides a development of hypotheses. Section 3 discusses the data and research method. Section 4 documents and discusses our empirical results. Section 5 provides robustness tests. Finally, Section 6 concludes with policy implications.

2. Literature review and hypotheses development

The arguments supporting our focus on uninsured deposits, particularly subordinated debt, are two-fold. Firstly, the yield spreads of subordinated debt contain information about bank riskiness. Secondly, and more importantly, subordinated debt provides direct market discipline (Bliss and Flannery, 2001). Subordinated debt holders require a higher premium from riskier banks and thus risky banks face higher costs of debt financing. It is argued that this higher debt financing cost will encourage banks to maintain a lower level of risk (Blum, 2002; Nier and Baumann, 2006).

Prior literature (e.g., Gropp and Vesala, 2004; Nier and Baumann, 2006; Sironi, 2003) generally finds that subordinated debt investors, excluding government owned or guaranteed institutions, are sensitive to bank risk. However, Nier and Baumann (2006) use a number of market discipline variables including uninsured liabilities (i.e., the sum of subordinated debt and interbank deposits) and find that uninsured liabilities are positively related to bank capital ratios, which suggests an incentive for banks to limit their risk of insolvency by choosing a higher capital buffer for a given level of risk. 2 With regard to interbank deposits, Rochet and Tirole (1996) argue that there is a trade-off between the negative effect on bank risk due to peer monitoring and the positive effect on bank systematic risk due to increased interbank linkages. Further, Furfine (2001) concludes that interbank deposits provide the strongest disciplinary impact because this investor group is likely to be more sophisticated than the average. Moreover, their loans are expected to impose significant losses given the loan size and lack of collateral.

Further, Blum (2002) argues that if a bank is committed to a level of risk then the presence of subordinated debt can help to reduce bank risk, but if the bank is not committed to a specific level of risk, the issue of subordinated debt can flag higher risk than would be the case under a full deposit insurance regime. This is possible because in the case of default, the banks do not cover the full costs of default due to limited liability. More specifically, after having set a low interest rate corresponding to a low level of risk, a bank has some incentive to increase its risk. Rational creditors anticipate this behavior and demand a higher interest rate. This higher interest payment induces banks to take even higher risk because the “option to go bankrupt” becomes more valuable. Thus, if a bank can adjust its level of risk in response to changes in interest rates, subordinated debt can actually raise the level of bank riskiness (Blum, 2002). 3

Gorton and Santomero (1990) demonstrate that the spread–risk relationship should actually be non-linear, as the payoffs to subordinated debt effectively look like those to equity when leverage is high. This observation did little, however, to help uncover a relationship between debt prices and risk, casting serious doubts on the ability of subordinated debt to impose any market discipline on banks. Flannery and Sorescu (1996) conduct a further investigation on this association and propose that asset risk and leverage display a non-linear relation with subordinated debt rather than the linear linkage tested in previous studies (e.g., Avery et al., 1988; ; Gorton and Santomero, 1990). Further, they argue that there is little evidence of a relation between interest rate risk and subordinated debt.

Based on the above discussion, we empirically test the disciplinary role of uninsured deposits (H1) and further examine if there is a non-linear association between bank risk and market discipline (H2). Hence, our first two hypotheses are:

H1: Market discipline reduces bank risk (baseline hypothesis).

H2: There is a convex relationship between bank risk and market discipline.

A particular focus on bank risk stems from the moral hazard concern surrounding the principal–agent relationship between shareholders and debt holders in levered firms (Jensen and Meckling, 1976). This agency problem becomes even more complicated by the web of government financial support (implicit and explicit safety nets) implemented to protect the banking industry, particularly deposit insurance schemes. Deposit insurance curbs the incentives of insured depositors to monitor banks, as well as weakening their vigilance to demand correct prices relative to bank risk, and so banks are incentivized to switch funding sources to insured deposits.

Moral hazard can also stem from an incorrectly priced insurance premium (Merton, 1977). However, Pecchenino (1992) and Mishkin (2001) argue that a risk-based deposit insurance premium can reduce bank risk, since such insurance premiums are based on bank risk classifications regarding capital adequacy and supervisory ratings. The market can impose stronger discipline and reduce bank risk under a risk-adjusted insurance premium regime (Blum, 2002). It is likely that a risk-adjusted insurance premium scheme induces banks to be more prudent in their risk taking. Uninsured liabilities can provide useful information and improve bank supervisors’ assessment of bank risk profiles (Krainer and Lopez, 2008). Since risk-adjusted insurance premium criteria are based on supervisory ratings, improvement in the supervisory process can lead to an insurance premium imposed on banks that is better matched to their risk taking. Therefore, market discipline may assist a risk-adjusted premium scheme to monitor and reduce bank risk.

Accordingly, the third hypothesis is stated as follows:

H3: Market discipline more strongly reduces bank risk, in the presence of risk-based deposit insurance.

A bank capital effect on risk has long been argued by regulators and academics. In practice, the management of capital is the main way in which banks attempt to manage the risk of default (Nier and Baumann, 2006). However, in the presence of moral hazard resulting from deposit insurance, banks can increase shareholders’ wealth by choosing a riskier portfolio than they would in an unprotected environment. Thus, regulators require banks to maintain a higher capital buffer to absorb the increase in expected loss (Milne, 2002). This risk-based capital regulation sets an upper bound on the probability of insolvency. Kwan and Eisenbeis (1997) find that credit risk is negatively related to bank capital. Konishi and Yasuda (2004) find a similar result in Japan.

Black and Cox (1976) develop a model for subordinated debt pricing indicating that the spread can either decrease or increase asset risk, depending on firm leverage. Subordinated debt holders’ claims are senior to equity holders, but junior to those of non-subordinated debt holders. Therefore, when a firm is undercapitalized, subordinated debt holders behave like equity holders because taking more risk will increase their expected payoff. However, when firms are well-capitalized, subordinated debt holders resemble senior debt holders, and then increasing risk will reduce their expected payoff. Moreover, well-capitalized banks should be more prudent in their risk taking (Nier and Baumann, 2006). Therefore, if the bank is committed to a level of risk, market discipline is strengthened and this might reduce bank risk (Blum, 2002).

Therefore, the fourth hypothesis is:

H4: Market discipline exerts a stronger negative impact on bank risk as bank capital increases.

Furthermore, during times of economic expansion, the loss of short-term profit opportunities can outweigh risk-aversion and encourage bank risk taking (Knight, 2004). This can be accomplished by a series of credit expansions, increasing asset prices, taking on more leverage, or incurring more capital expenditure. Moreover, such activities can easily exceed sustainable levels. Thus, the market discipline assessment of risk will be dulled by this “system-wide” behavior during boom times.

On the other hand, during economic contractions banks tend to be weak and the probability of bank failure increases. Creditors and depositors will increase the level of monitoring and assessing bank risk accordingly. Moreover, during such difficult market times the safety nets have to absorb the loss from any banking failures, and this increases the chance that these mechanisms cannot fully shoulder banking system failure. 4 Hence, the fifth testable hypothesis is as follows:

H5: Market discipline is stronger in reducing bank risk, post-GFC.

3. Data and methodology

Our sample includes publicly listed banks from Canada, France, Germany, Italy, Japan, the UK and the US over the period 1996–2010. Bank-level information is extracted from the Bankscope and the Osiris databases. The final sample is an unbalanced panel of 288 banks giving a total number of observations of 2839 and 2775 for the analysis of equity risk and credit risk, respectively. Further, financial market data including individual bank weekly stock returns, Morgan Stanley Composite Index (MSCI) market index returns, 10-year government bond yields and dividend yields are collected from Datastream International.

3.1. Risk measures

The bank equity risk measures are total risk, systematic risk, interest rate risk and idiosyncratic risk. Total risk,

where

Bank credit risk is defined as

where

3.2. Bank-specific and country-specific variables

Market discipline is measured as the sum of subordinated debt and interbank deposits scaled by total liabilities (Nier and Baumann, 2006). As such, it is a measure of the scale of influence that uninsured liabilities have in total liabilities held by a bank. The Tier 1 capital ratio is used as a proxy for capital adequacy requirements. 5 Furthermore, although most countries have adopted international capital adequacy guidelines to manage their risk profile, there is considerable variation in equity across countries. The Tier 1 capital ratio can, therefore, reflect differences in capital management practice adopted across countries (Demigüç-Kunt and Huizinga, 2004).

Bank charter value represents the present value of future profits, if a bank continues to operate as a going concern. Bank charter value is the sum of the market value of equity and book value of liabilities divided by the book value of total assets (Keeley, 1990). Charter value plays a self-disciplinary role for banks to avoid excessive risk taking. However, there exists empirical evidence of a positive relationship between charter value and bank risk. One possible explanation is that charter value captures growth opportunities that originate from taking on more risky although positive net present value activities. If this is the case then both bank risk and charter value will tend to move together. In addition, Fonseca and González (2010) argue that the association between bank risk and charter values varies with the degree of competition. The increase in competition induces banks to undertake excessive risk, which in turn reduces the disciplinary effect of bank charter values. In fact, the G7 countries have been subject to various deregulations and financial integration that promote a higher level of competition. As a result, we do not expect a clear association between bank charter value and risk.

Off-balance sheet items constitute another important determinant of bank risk. Off-balance sheet activities are measured by the ratio of the total value of off-balance sheet items divided by total liabilities. It has been argued that off-balance sheet activities help to diversify the portfolio without altering capital structure (Angbazo, 1997). Banks with higher levels of off-balance sheet items are found to be more cost and profit efficient. However, due to the increasing occurrence of off-balance sheet activities and banking failures, there is a possibility of a positive relation between bank risk and off-balance sheet items. As a result, the relationship between off-balance sheet items and bank risk is ambiguous – it could be either positive or negative.

Another variable of interest is bank size. It is evident that the large banks are internally diversified, which has the effect of reducing bank idiosyncratic risk (Konishi and Yasuda, 2004). Furthermore, larger banks find it easier to access capital markets, and therefore they are in a better position to cope with liquidity shortfalls (Haq and Heaney, 2012). However, large banks differ from small banks in the composition of their asset portfolios. Large banks might be exposed to greater sensitivity due to general market movements, since they engage in a different mix of activities, lend to different sectors and hold less equity capital compared to smaller banks (Demsetz and Strahan, 1997; Nier and Baumann, 2006).

With regard to dividend yield, we expect a negative association between dividend yield and bank risk. Indeed, a low dividend yield reflects greater bank risk (Lee and Brewer, 1985). Dividend announcements are an effective and credible way of providing information to investors. Furthermore, if regulators force banks to change dividends, this will convey private information about a bank’s solvency status (Bessler and Nohel, 1996).

In theory, the combined cash flows from non-correlated revenue sources should be more stable than the individual sources. Further, diversification benefits exist, but the gains are offset by the increased exposure to non-interest activities, which are much more volatile, while not necessarily more profitable, than interest-generating activities (Stiroh and Rumble, 2006). In contrast, Baele et al. (2007) provide evidence that diversification decreases a bank’s idiosyncratic risk in Europe. In addition, Williams and Rajaguru (2013) argue that increases in Australian bank fee income (particularly income generated via insurance services) are used to supplement decreases in net interest margin, suggesting that banks are proactive in the process of disintermediation.

Following the work of Stiroh and Rumble (2006), we calculate a revenue diversification index (RDI). The RDI is estimated as

where

With regard to country-specific variables, we include the risk-adjusted deposit insurance premium, total stock market capitalization and real gross domestic product (GDP) growth rate. The risk-adjusted insurance premium variable is a dummy variable that takes the value of 1 if a country has the risk-based premium policy and 0 otherwise. The real GDP growth rate is used to capture macroeconomic activity that potentially affects bank risk (Hadad et al., 2011). Finally, to control for capital market competition in each country, we use stock market capitalization scaled by total GDP. The effect of macroeconomic conditions on bank risk is ambiguous, and thus no prediction is possible. The definitions of these variables are summarized in Appendix 1.

3.3. Research method

Our estimation technique is the GMM for dynamic panel data. 6 More specifically, we use the two-step estimation System GMM originally developed by Arellano and Bond (1991), then improved by Arellano and Bover (1995) and Blundell and Bond (1998). GMM is our preferred method for several reasons. Firstly, this approach takes into account the dynamic nature of bank risk by incorporating its lagged value as an explanatory variable. This dynamic issue is plausible because any past shock to bank risk can lead to banks shifting their behavior as well as affecting current risk. 7 As a consequence, estimators produced by static models are biased and inconsistent. Secondly, we are concerned about endogenous explanatory variables, including market discipline, bank capital and charter value. The System GMM addresses this concern. It is worth noting that potential endogeneity biases (particularly for the market discipline variable) need to be addressed by a suitable choice of estimation method (including the two-stage least squares procedure). However, due to a lack of economically motivated instruments (such as subordinated debt yield, monitoring by private parties) for our sample banks, we choose to apply the two-step system GMM estimation method.

Thirdly, the cross-sectional unobservable heterogeneity, which is time-invariant when presented in panel data, is purged out by first-differencing all the variables. Finally, in our model, since market discipline has total liabilities in the denominator and credit risk also has the same denominator, we face the “spurious ratio problem”. Specifically, misleading inferences can be drawn when standard statistical tests are applied to ordinary least squares regression models using ratio variables. System GMM overcomes the spurious ratio problem (Zhu, 2012, 2013).

We report diagnostics tests including Hansen J-statistics of over-identification, and the Arellano and Bond autoregressive tests AR(1), AR(2). The GMM model is well-specified and produces a consistent estimator if it satisfies two conditions. Firstly, the Hansen over-identification J-statistic needs to be statistically insignificant, indicating that the instrument variables are uncorrelated with the error terms. Secondly, the Arellano–Bond autocorrelation tests the serial correlation of the residuals in differences. Since AR(1) is negatively correlated by construction, we check for first-order correlation in levels by checking for second-order correlation in differences AR(2). Therefore, AR(2) should also be insignificant. The basic regression model is specified as

where

To examine whether market discipline is stronger in reducing bank risk in the presence of a risk-adjusted insurance premium (hypothesis H3), we interact the dummy variable

H3 predicts a negative sign for the coefficient

To investigate H4 focusing on the notion that banks with a higher capital ratio are more effective in facilitating a reduction in bank risk via the role of uninsured creditors, we interact Tier 1 bank capital

where

Given the 15-year span across our sample period, it is important to test for the possibility of structural change. For this purpose, the sample is split into two sub-samples, with 2007 chosen as the break point for the GFC. This facilitates tests for structural change between the pre-GFC (1996–2006) and the post-GFC (2007–2010). For this purpose we apply the following model:

where

3.4. Descriptive statistics and correlations

Panel A of Table 1 reports the descriptive statistics across all of our variables. The total risk measure has a mean of 33.40%. With regard to idiosyncratic risk, the mean value is 28.3%. The minimum and maximum value ranges from 3.8% to 179%. The mean systematic risk is 0.6. The minimum and maximum range is from –4.606 to 4.052. Interest rate exposure has a mean value of 0.026 with the minimum and maximum sample value of –1.367 and 1.99, respectively, while the mean value of credit risk is 0.005.

Descriptive statistics and correlation analysis.

This table presents descriptive statistics for various proxies of bank risk and explanatory variables. The study uses annual observations of bank-specific variables for listed bank stocks in G7 countries. The total number of observations across the sample with 288 different banks. There are four alternate equity-based risk measures: total risk (

Market discipline has a mean value of 0.29. Bank capital (Tier 1) ranges from –1.2% to 58.9%, with a mean of 10.3%. There are only two observations that have negative values. 8 Charter value ranges in value from 0.71 to 2.57. The mean and median are 1.031 and 1.012, respectively. Dividend yield has a mean of 2.1%, with a minimum value of 0% and maximum value of 3%. By construction, RDI has a distribution ranging from 0 to 0.5 – thus, a mean value of 0.324 indicates that our sample of banks have relatively diversified portfolios between non-interest and interest income. Off-balance sheet items show a mean value of 0.067, with a minimum–maximum range from 0 to 0.962. With respect to country variables, the GDP growth rate has a mean value 1.8%, ranging from –6.3% to 5.5%. This represents the volatility of a country’s economy during the recent financial crisis.

Pair-wise correlations are reported in Panel B of Table 1. Size has a relatively high correlation with market discipline (0.5), RDI (0.39) and off-balance sheet activities (0.56). In response to the potential problems these correlations might induce, as discussed above, we orthogonalize bank size against each of these variables to capture “pure size effects” (Baele et al., 2007; Haq and Heaney, 2012).

4. Empirical results

4.1. Market discipline and bank risk – baseline results

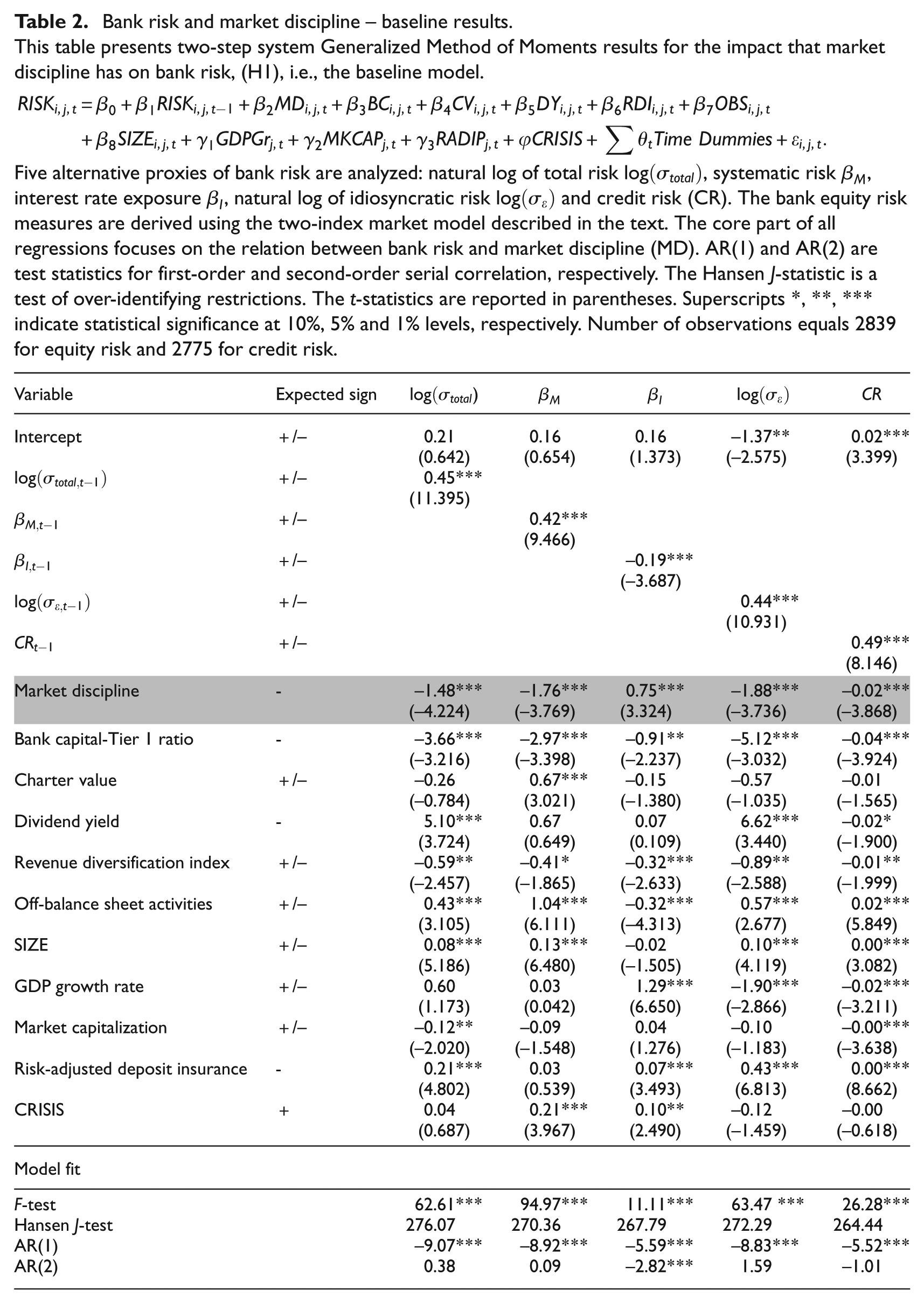

Table 2 provides the baseline regression results relating to the negative predicted linkage between bank risk and market discipline (H1). For four of the five bank risk measures, as predicted, the estimated coefficient on market discipline is negative and significant at the 1% level, indicating that market discipline reduces bank risk. This result is qualitatively similar across total risk, idiosyncratic risk, systematic risk and credit risk (columns 1, 2, 4 and 5, respectively) with the exception of interest rate risk (column 4). The findings show a positive association between market discipline and interest rate risk. A possible explanation for this could be that uninsured liabilities in banks can have various maturities (i.e., interbank deposits tend to be short term, whereas subordinated debt can be either long term or short term). Such a mix of maturities can potentially complicate the matching management practiced by banks, which then exposes them to a higher level of interest rate volatility.

Bank risk and market discipline – baseline results.

This table presents two-step system Generalized Method of Moments results for the impact that market discipline has on bank risk, (H1), i.e., the baseline model.

Five alternative proxies of bank risk are analyzed: natural log of total risk

The specification statistics in Table 2 show that the model is well fitted across most of the risk measures, with the exception of interest rate risk. Hansen J-statistics, which test over-identifying restrictions, indicate that our instruments are valid and that the moment conditions are met. Further, AR(2) are statistically insignificant for total risk, systematic risk, idiosyncratic risk and credit risk. In the case of interest rate exposure, the AR(2) test is statistically significant. In fact, across all of our tests pertaining to the interest rate risk measure, AR(2) statistics are highly significant. As a consequence, we conduct a robustness check in Section 5 to address this concern.

In addition to judging the statistical significance, the economic significance regarding the magnitude of these coefficients is very important. To assess the economic significance, we consider the impact of a hypothetical one standard deviation “shock” in the market discipline variable. With regard to total risk, all else being equal, a one standard deviation increase in market discipline (see Table 2) will see a reduction in total risk by 8.2% ((

In terms of systematic risk, well-diversified investors whose portfolio risk mostly depends on the level of market risk can benefit from a reduction of 0.102

The estimated coefficient on charter value is positive and statistically significant at the 1% significance level for systematic risk, suggesting that higher charter value might lead to higher systematic risk. This finding is in contrast to Konishi and Yasuda (2004) and González (2005). In addition, we do not find any statistically significant association between charter value with other risk measures, indicating that the increase in competition and changes in regulation during the sample period may have eroded the disciplining effect of bank charter value.

There is mixed evidence with regard to off-balance sheet activities and the measures of bank risk. While off-balance sheet activities decrease interest rate exposure, they increase other bank risk measures. The negative relationship is in line with the argument that off-balance sheet activities help diversify the portfolio without altering the capital structure of the bank (Angbazo, 1997), whereas the positive relation supports the argument that although banks can enjoy the diversification benefits, they are also exposed to more volatile income-generating activities (Esty, 1998; Stiroh, 2006).

Our findings show statistically negative association (with at least 10% significance) between bank diversification and all the bank risk measures. In contrast to prior literature (e.g., Baele et al., 2007), the significant and negative relationship supports the notion of diversification benefits.

Size has a positive and significant role for four of five risk measures, with the exception of interest rate risk being insignificant. This finding is consistent with the work of Demsetz and Strahan (1997) and Baele et al. (2007), suggesting that although large banks can benefit from diversification they use this advantage to operate at a lower capital ratio and pursue riskier activities.

With regard to the risk-adjusted deposit insurance premium, we find a positive and statistically significant association between the risk-adjusted insurance premium and bank risk (with the exception of systematic risk). Intuitively, the positive relationship is inconsistent with the expectation that the implementation of a more prudential insurance scheme would reduce the moral hazard problem. Thus, the moral hazard problem seems to be worse under the operation of risk-adjusted deposit insurance premium regime. Finally, we observe that the CRISIS dummy is positive and statistically significant for both systematic and interest rate risks.

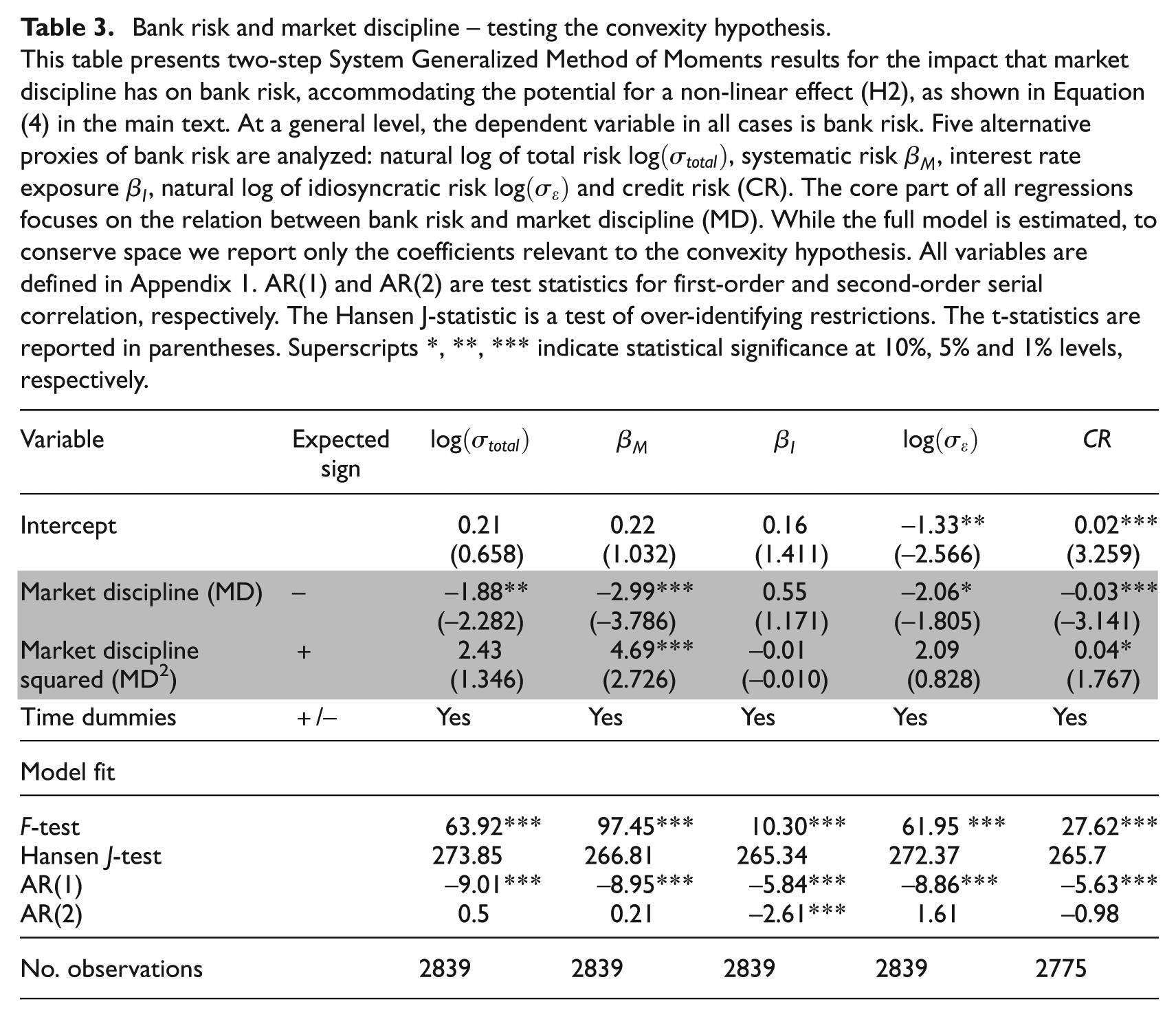

4.2. Convexity hypothesis – H2

Table 3 presents the regression results regarding the second hypothesis (H2) relating to whether the association between market discipline and bank risk is non-linear (and convex). There exists evidence supporting the convexity between bank uninsured liabilities and bank systematic risk and credit risk. This non-linear relationship potentially implies that if banks over-extend their use of uninsured liabilities as the funding source, banks risk might increase (beyond a certain inflection point). With regard to systematic risk, the shift in the relationship occurs once the share of uninsured liabilities to total liabilities exceeds 31% (see Equation (5)), indicating that beyond this point, bank systematic risk begins to increase. However, given that the mean value of uninsured funding in the sample is 2.9%, a value of 25% for market discipline is well into the right-hand tail of the empirical distribution – indeed, it represents the 95th sample percentile. We draw a similar conclusion for credit risk measure. 10 As such, the convexity lacks any real economic meaning.

Bank risk and market discipline – testing the convexity hypothesis.

This table presents two-step System Generalized Method of Moments results for the impact that market discipline has on bank risk, accommodating the potential for a non-linear effect (H2), as shown in Equation (4) in the main text. At a general level, the dependent variable in all cases is bank risk. Five alternative proxies of bank risk are analyzed: natural log of total risk

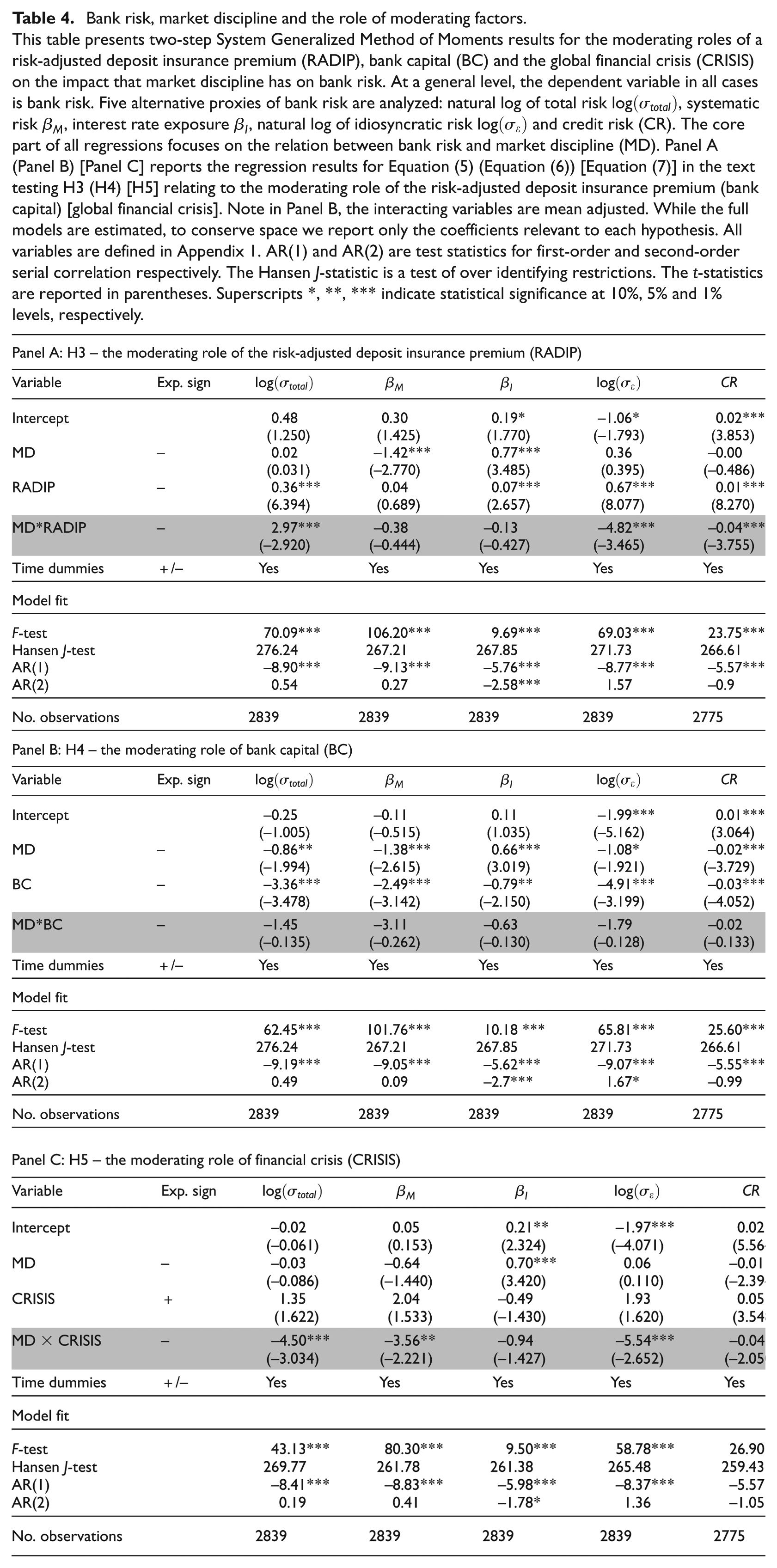

4.3. Market discipline effect moderated by the risk-adjusted deposit insurance premium – H3

Panel A of Table 4 contains the core results from the regression investigating the impact of market discipline on bank risk, in the presence of a risk-adjusted insurance premium. In three of the five regressions, the estimated coefficient on the interaction term (MD × RADIP) is negative and significant at the 1% level, consistent with H3, suggesting that market discipline imposes a stronger impact on bank risk (i.e., total risk, idiosyncratic risk and credit risk) in the presence of a risk-adjusted insurance premium. This finding is consistent with the work of Martinez-Peria and Schmukler (2001) on Latin American banks. However, there is no evidence that market discipline is stronger in reducing either bank systematic risk or interest rate exposure under a risk-adjusted insurance premium, suggesting that a deposit insurance system reduces the incentives of debt holders and creditors to monitor banks, diminishing the degree of market discipline.

Bank risk, market discipline and the role of moderating factors.

This table presents two-step System Generalized Method of Moments results for the moderating roles of a risk-adjusted deposit insurance premium (RADIP), bank capital (BC) and the global financial crisis (CRISIS) on the impact that market discipline has on bank risk. At a general level, the dependent variable in all cases is bank risk. Five alternative proxies of bank risk are analyzed: natural log of total risk

The estimated coefficient on the interaction term is insignificant in both these cases.

4.4. Market discipline effect moderated by bank capital – H4

Panel B of Table 4 presents the results from the test of whether market discipline reduces bank risk in the presence of a greater level bank capital, that is, H4. Our findings show that the bank capital ratio does not complement market discipline to curb bank risk. The interaction is insignificant for all risk measures. This evidence fails to support our H4. However, this finding has important policy implications for regulators and well-diversified investors. For example, regulators might like to rethink promoting the complementary effect of capital adequacy and market discipline through uninsured deposits, in particular subordinated debt.

4.5. Market discipline effect moderated by the crisis period – H5

Panel C of Table 4 reports the results with respect to the relative importance of market discipline on bank risk, pre-and-post the financial crisis (i.e., H5). The estimated coefficient on the interaction term is negative and statistically significant, suggesting that uninsured depositors impose stronger discipline during the post-crisis period across all risk measures. This is an encouraging sign to market discipline proponents. It appears that during and after the crisis, uninsured liabilities exert discipline in a manner that helps limit bank risk. This finding is consistent with Martinez-Peria and Schmukler (2001). However, it seems to contradict the work of Cubillas et al. (2012). It is possible that we observe this difference since our post-crisis period (2007–2010) coincides with the crisis period identified by Cubillas et al. (2012). The authors argue that the weakening of market discipline is due to the accommodative intervention policies. Nonetheless, during the crisis period the fear of loss might well offset government guarantee indulgence, which in turn induces investors to exert stricter discipline. After the crisis, the excessive government protection changes the market’s perception of bank risk, thus there is a decline in market discipline.

5. Robustness checks 11

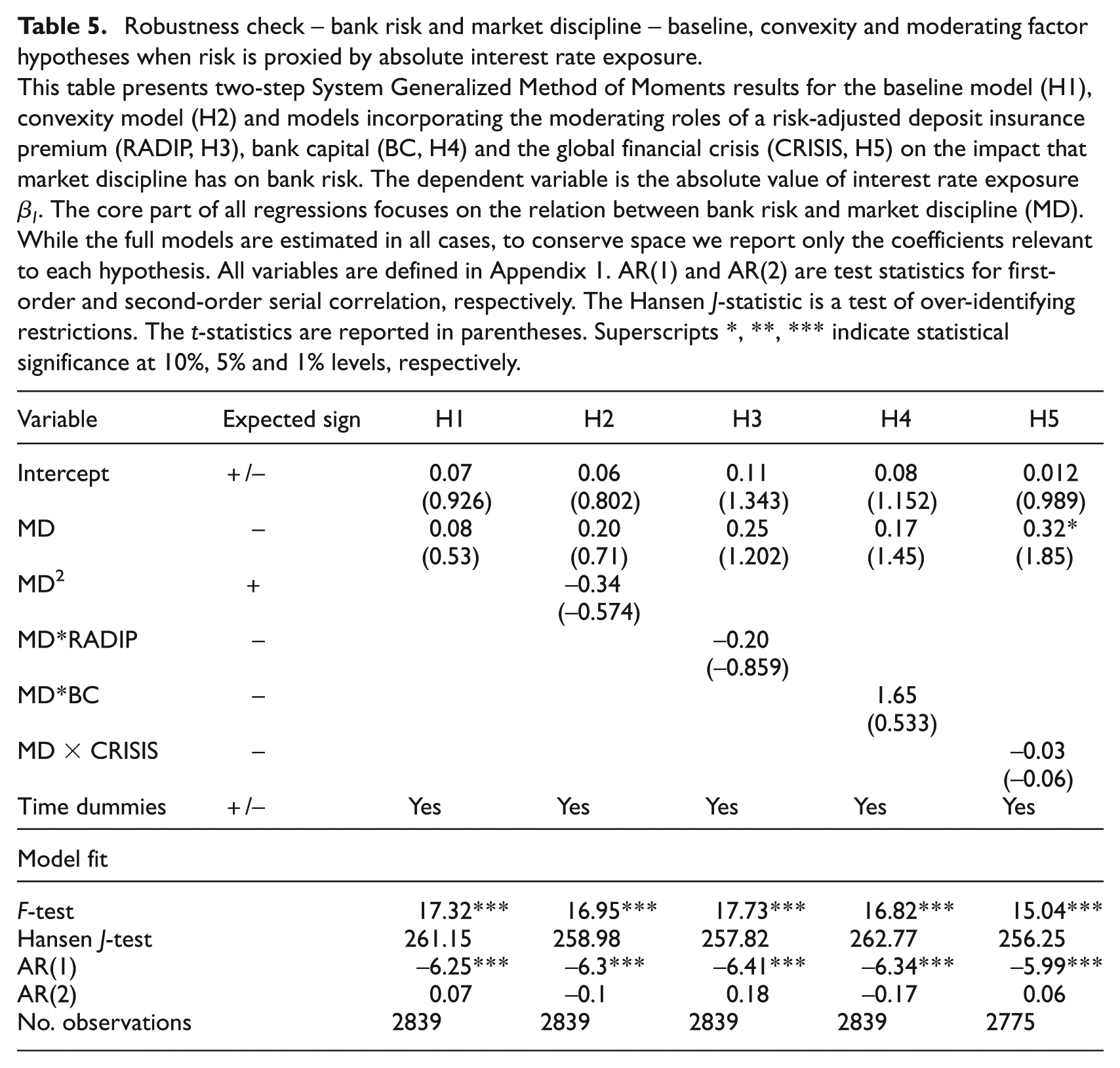

5.1. Alternative interest rate risk proxy

As discussed above, our model might not be well-specified in the case of interest rate risk reflected by AR(2) tests that are statistically significant. A simple solution might be to use the absolute value of interest rate exposure as an alternative proxy of interest risk. It can be argued that interest rate exposure is not a measure of risk per se. Since such exposure can take either a positive sign or a negative sign, a lower value does not necessarily reflect lower risk (i.e., lower sensitivity to interest rate changes) nor is it the case that only a higher value reflects higher risk. Rather, a value of interest rate exposure closer to zero represents lower interest rate risk, while values further from zero (whether positive or negative) reflect greater sensitivity to interest rate changes and, thus, higher interest rate risk. Indeed, previous studies have used the absolute value of such exposures as an alternative proxy for risk – for example, in the context of foreign exchange (FX) exposure/risk see Nguyen and Faff (2003). Accordingly, we re-estimate all models using the absolute value of interest rate exposure, |

Robustness check – bank risk and market discipline – baseline, convexity and moderating factor hypotheses when risk is proxied by absolute interest rate exposure.

This table presents two-step System Generalized Method of Moments results for the baseline model (H1), convexity model (H2) and models incorporating the moderating roles of a risk-adjusted deposit insurance premium (RADIP, H3), bank capital (BC, H4) and the global financial crisis (CRISIS, H5) on the impact that market discipline has on bank risk. The dependent variable is the absolute value of interest rate exposure

With the new risk proxy, AR(2) becomes statistically insignificant. This implies that the GMM estimator is consistent and unbiased. However, the coefficient on market discipline becomes statistically insignificant. This finding contrasts our main model results, which show a positive association of market discipline and interest rate exposure. In fact, the results against all hypotheses become insignificant. More specifically, we do not observe any evidence of a convex association, the interaction with risk-adjusted deposit insurance scheme and bank capital, thus rejecting H2, H3 and H4. Finally, there is no detectable evidence that market discipline imposes a stronger impact on bank interest rate risk in the post-crisis period, so rejecting H5. Overall, because the significant results using the raw interest rate proxy could be subject to the incorrect model specification, we conclude that there is no significant relationship between market discipline and interest rate risk.

5.2. Exclusion of Japanese banks

Japanese banks are among the world’s largest global financial intermediaries with widespread presence across several regions. Yet, Japan’s banking system has faced numerous, serious and long-term problems. 12 It is clear that the banking system in Japan is very different from other developed countries and thus it is possible that the findings are unduly affected. Accordingly, as a further robustness check we exclude Japanese commercial banks from the sample and re-estimate the models. The key results (un-tabulated) remain qualitatively unchanged. 13 However, with regard to H2, we detect significant quadratic terms in four of the five risk measures, with the exception of interest rate risk. Similar to the result reported in Section 4.2, although the non-linear term appears statistically significant, the inflection point lies in 95th percentile of the sample observations.

6. Conclusion

Using a sample of 288 listed banks drawn from the G7 countries over the period 1996–2010, we develop and test a model of bank risk taking with its primary focus being on the role of market discipline, as captured by the degree of uninsured debt used. The baseline prediction is that market discipline will induce a reduction in bank risk. Our model also tests for non-linearity in the effect of market discipline – a convexity hypothesis. In addition, we test the moderating roles of risk-adjusted deposit insurance premium, bank capital and the financial crisis on market discipline’s ability to reduce bank risk.

Our findings confirm that market discipline reduces bank equity risk (with the exception of interest rate risk) and credit risk. There is no meaningful evidence of any convexity in this relation. This result is broadly supportive of the recent policy initiatives that aim to strengthen financial stability by promoting the important role of market discipline. Our findings also suggest that in the presence of risk-adjusted deposit insurance, market discipline plays an effective role in reducing bank risk. Furthermore, our results provide insights particularly germane to regulators, with regard to the complementary role of market discipline and bank capital. Specifically, we find that in the presence of higher bank capital, market discipline does not impose stronger direct influence to limit bank risk. This finding is clearly a discouraging sign for bank regulators who endorse the symmetric and complementary role of the two Pillars (minimum capital adequacy as Pillar 1 and market discipline as Pillar 3) in protecting banking stability. Finally, there is evidence that market discipline has a greater impact on bank risk taking in the post-crisis period. Uninsured investors seem to discipline banks during and post the crisis in a manner that reduces bank equity risk and credit risk.

The results from our study should be of particular interest to policymakers, bank regulatory bodies and supervisory agencies that exercise regulatory authority over financial institutions, potential bank investors and creditors, as well as to academics. Regulators favor market discipline to promote the safety and soundness of the financial system. Basel Accord II focuses on encouraging banks across the world to put more emphasis on market discipline. Our evidence suggests that these efforts have had some success.

Footnotes

Appendix

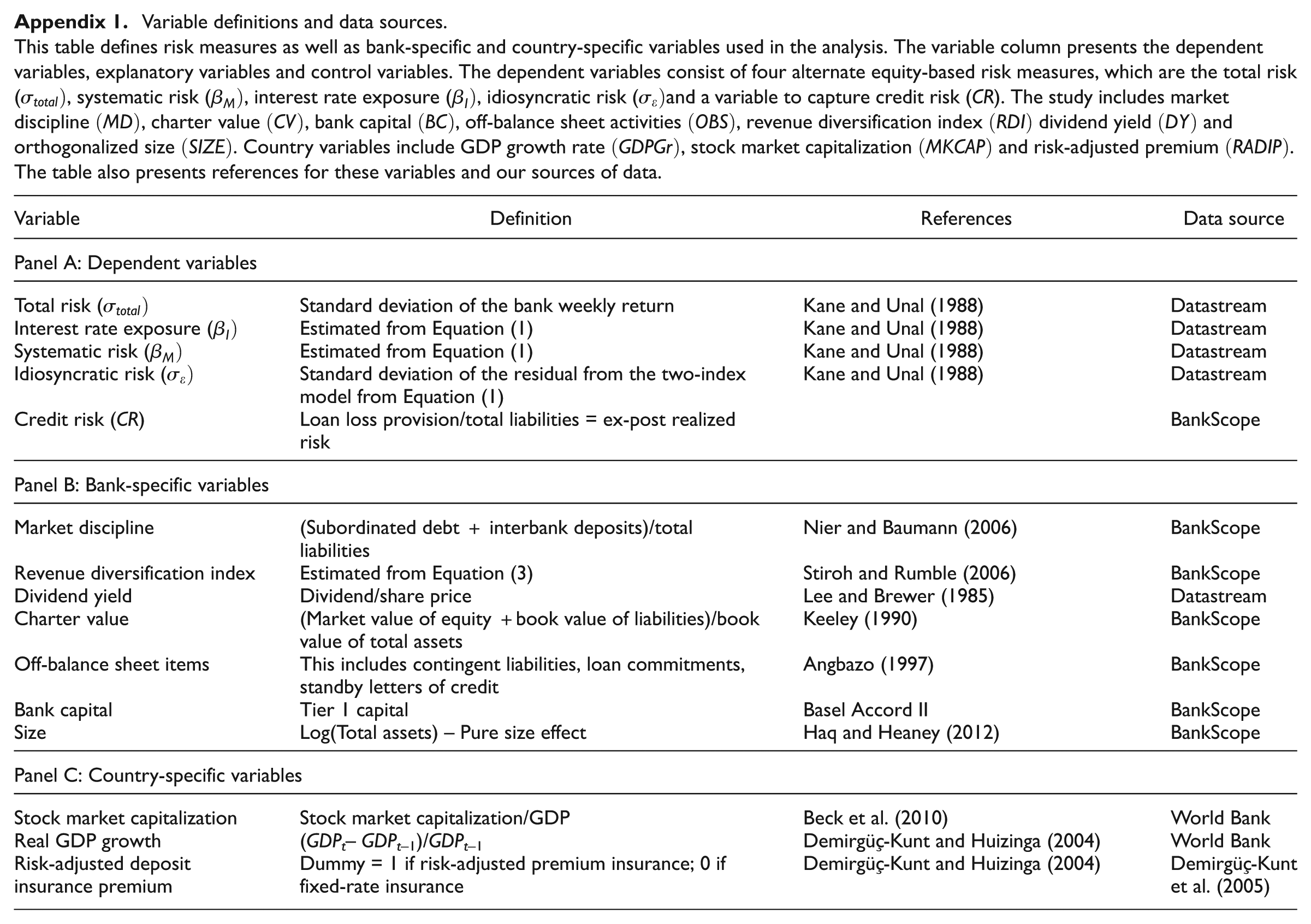

Variable definitions and data sources.

This table defines risk measures as well as bank-specific and country-specific variables used in the analysis. The variable column presents the dependent variables, explanatory variables and control variables. The dependent variables consist of four alternate equity-based risk measures, which are the total risk (

| Variable | Definition | References | Data source |

|---|---|---|---|

| Panel A: Dependent variables | |||

| Total risk ( | Standard deviation of the bank weekly return | Kane and Unal (1988) | Datastream |

| Interest rate exposure ( | Estimated from Equation (1) | Kane and Unal (1988) | Datastream |

| Systematic risk ( | Estimated from Equation (1) | Kane and Unal (1988) | Datastream |

| Idiosyncratic risk ( | Standard deviation of the residual from the two-index model from Equation (1) | Kane and Unal (1988) | Datastream |

| Credit risk ( ) | Loan loss provision/total liabilities = ex-post realized risk | BankScope | |

| Panel B: Bank-specific variables | |||

| Market discipline | (Subordinated debt + interbank deposits)/total liabilities | Nier and Baumann (2006) | BankScope |

| Revenue diversification index | Estimated from Equation (3) | Stiroh and Rumble (2006) | BankScope |

| Dividend yield | Dividend/share price | Lee and Brewer (1985) | Datastream |

| Charter value | (Market value of equity +book value of liabilities)/book value of total assets | Keeley (1990) | BankScope |

| Off-balance sheet items | This includes contingent liabilities, loan commitments, standby letters of credit | Angbazo (1997) | BankScope |

| Bank capital | Tier 1 capital | Basel Accord II | BankScope |

| Size | Log(Total assets) – Pure size effect | Haq and Heaney (2012) | BankScope |

| Panel C: Country-specific variables | |||

| Stock market capitalization | Stock market capitalization/GDP | Beck et al. (2010) | World Bank |

| Real GDP growth | (GDPt– GDPt–1)/GDPt–1 | Demirgüç-Kunt and Huizinga (2004) | World Bank |

| Risk-adjusted deposit insurance premium | Dummy = 1 if risk-adjusted premium insurance; 0 if fixed-rate insurance | Demirgüç-Kunt and Huizinga (2004) | Demirgüç-Kunt et al. (2005) |

Acknowledgements

The authors wish to thank Karen Alpert, Necmi Avkiran, Jiakai Chen, Tom Smith, Amine Tarazi, Barry Williams and participants at 25th Australasian Banking and Finance Conference 2012. The usual caveats apply.

Final transcript accepted 16 June 2013 by Tom Smith (AE Finance).

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.