Abstract

Several theoretical studies provide predictions on the relation between settlement likelihood and litigation stakes. Although models with generalizable settings argue in favor of a negative relation, certain specialized settings predict the opposite. In contrast to the theoretical literature, there is limited empirical analysis of the relation with only one study reporting evidence of a positive association. In this study, we infer how the stock market forms expectations regarding the relation between settlement likelihood and litigation stakes by analyzing stock returns around settlement announcement dates. We find that the market was more surprised when higher stakes lawsuits were settled, suggesting that higher stakes lawsuits were not expected to settle. We thus provide empirical support in favor of general theoretical models on conflict resolution that predict a positive relation between litigation stakes and settlement likelihood. Our results also have implications for studies of financial distress costs. Although we find evidence of the existence of financial distress costs, our results contradict a conclusion drawn in prior research—that the primary benefit of litigation settlements is the unexpected relief from financial distress costs.

1. Introduction

Corporate litigation has long been recognized as an important business phenomenon, and litigation outcomes can significantly impact the financial health and growth prospect of the firms involved. The litigation process begins with the filing of a lawsuit and ends with either judgment or private settlement between the warring parties. It is well known that litigations that go all the way to final judgment are costly. In contrast, settlements can be less expensive and less time consuming while giving both parties more flexibility and control over the final outcome (Schlicher, 2011). Despite this relatively uncontroversial rationale in favor of settlements, we observe a large number of lawsuits pursued all the way to trial. The ongoing Apple–Samsung patent imbroglio provides an example of a long drawn-out dispute that spans several jurisdictions. This phenomenon highlights the importance of studying the factors that determine the likelihood of litigation settlements, especially in light of the significant and growing amount of economic resources spent on corporate litigations.

The settlement-versus-trial decision has been extensively modeled in the economics literature. The early literature (e.g. Gould, 1973; Shavell, 1982) focuses on the incentives of the litigating parties and assumes that disputes will settle out of court when the cooperative surplus (i.e. the amount by which the utility gained from avoiding continued litigation exceeds the expected value of the trial outcome), as perceived by both litigating parties, is positive. This literature generally predicts that high-stakes lawsuits are more likely to settle. The literature subsequently evolved to explicitly model the bargaining process in a game theory setting in diverse ways, which has led to predictive and normative theories that are rivals to each other (Cooter and Rubinfeld, 1989).

One stream of this research generates definitive predictions by making restrictive assumptions about the scope of bargaining, the timing of offers, and the ability of parties to transmit information. For example, Bebchuk (1984) treats the settlement amount as endogenous, but assumes an information asymmetry between the plaintiff and the defendant. In such a setting, the probability of settlement will be lower for high-stakes litigations. In contrast, Nalebuff (1987) incorporates signaling in settlement bargaining and assumes a specific move order. To make the threat of going to trial credible, the plaintiff may strategically demand a larger settlement. Under Nalebuff’s specific structure and assumptions, the model predicts a positive relation between settlement likelihood and litigation stakes.

Due to the restrictive nature of the assumptions regarding the specific move order between the litigation parties, the models described above are not able to adequately address the problem of dividing the cooperative surplus between the defendant and plaintiff, which is at the heart of the strategic interaction between litigating parties (Cooter and Rubinfeld, 1989). As Cooter and Rubinfeld point out, this distribution problem can act as a source of instability that will result in bargaining breakdowns even when both litigating parties expect positive cooperative surplus if they settle. We note that the conflict theory in Hirshleifer (1991) explicitly models the implications of the distribution problem. The advantage of Hirshleifer’s setting is its generalizability, since no restrictive assumptions are made regarding the specific move order between the litigating parties. The model shows that higher stakes will prolong the conflict by exacerbating the distribution problem, as higher stakes give both parties more incentive to fight over how to divide the surplus from peace. Accordingly, conflict theory predicts a negative relation between settlement likelihood and stakes. This negative relation can be mitigated by the existence of complementarity (i.e. benefits derived from actively working together) that gives both parties more incentives to settle, although the presence of complementarity alone does not make settlement more likely as the existence of complementarity is often associated with higher stakes.

In contrast to the rich theoretical work on the economics of settlement behavior, there is very limited empirical evidence in support of these theoretical models. Fournier and Zuehlke (1989) provide the only empirical study in the corporate litigation setting that investigates the relation between litigation stakes and settlement likelihood. They document a positive relation between stakes and settlement likelihood, thus lending support to the restrictive structure models, such as Nalebuff (1987), over the more generalizable models, such as Hirshleifer (1991).

Note that the findings in Fournier and Zuehlke are based on a pooled sample of lawsuits of different types, and heterogeneity in lawsuit types is known to create problems for empirical studies on legal issues (Bizjak and Coles, 1995). In particular, pooling different types of lawsuits is likely to include lawsuit type as a potentially confounding variable in the empirical tests. For example, if antitrust lawsuits tend to have high stakes and also tend to be settled, pooling across lawsuits will lead to the result that high-stakes lawsuits tend to settle, even though within antitrust lawsuits the actual finding may be the opposite. Moreover, pooling across lawsuit type obscures the strategic aspects of settlement behavior, because the strategic importance of legal dispute varies considerably across different types of lawsuits. To empirically test the implications of theories that model the strategic interaction in corporate litigation, it is important to identify a setting where the litigating parties have a significant future interest other than the cash transfer between defendant and plaintiff that is tied to the litigation outcome. We do so in this study by focusing on economics of settlements for patent litigation. 1

Patent lawsuits provide an excellent window for examining the strategic interaction in corporate litigation, as firms extensively use patents as a strategic tool to establish entry barriers and to create and maintain competitive advantage (Rivette and Kline, 2000). Lanjouw and Schankerman (2001) identify two mechanisms through which patent litigation creates strategic value: (a) allowing firms to build a cumulative chain of products based on the technology in dispute and to appropriate rents from subsequent inventions, and (b) creating reputations that convey to competitors the willingness to aggressively defend intellectual property. Given these features of patent litigation, the strategic aspect of settlement behavior, as highlighted by Cooter and Rubinfeld (1989) and Hirshleifer (1991), is more likely to manifest in patent litigation than in other types of lawsuits.

A sample of patent lawsuits settled in the United States from 2002 to 2006 serves as the basis of analysis for this study. We exploit the stock market’s reactions to news of settlements under the maintained hypothesis of market efficiency to investigate the economics of settlement behavior. Two implications of the maintained hypothesis are critical to our empirical strategy. First, an efficient market reacts to settlement news only to the extent that the news is surprising (unexpected). Thus, the magnitude of the market reaction can be used to gauge the market’s expectation regarding the settlement likelihood prior to the arrival of settlement news. Second, in forming expectations, an efficient market incorporates all available information in an unbiased manner. Therefore, the expectation of the stock market provides a benchmark against which the implications of the theoretical models on settlement behavior can be empirically tested.

We note that stock market reactions to lawsuit-related news have been used as the empirical setting in prior literature, albeit with a different focus. In particular, the finance literature has exploited market reactions to litigation-related news to investigate the importance of financial distress costs independent of economic distress. Conceptually, economic distress arises from poor operating performance while financial distress arises from difficulty in obtaining sufficient cash flows to make obligatory payments. In practice, however, it is difficult to disentangle economic distress and financial distress, as they tend to co-vary (Gertner and Scharfstein, 1991).

As lawsuits can place firms in financial distress for reasons unrelated to their operating performance due to the possibility of having to pay large amounts of damages, the setting stimulates a line of empirical research that examines the determinants of stock returns around events of lawsuit filing and settlement (Bhagat et al., 1994; Bizjak and Coles, 1995; Cutler and Summers, 1988). Collectively, the evidence from these studies is consistent with the notion that lawsuit filings impose potential financial distress costs on defendants and thus trigger negative market reactions for defendants, while settlement events bring unexpected relief from the potential financial distress costs and thus result in positive market reactions.

By focusing on the role of financial distress in the litigation process, the research described above makes the implicit assumption that corporate litigation is mostly a financial matter with respect to the payment the defendant will have to pay the plaintiff. Although treating lawsuits as a financial matter may be less of a problem for certain types of lawsuits (e.g. contract liability), the assumption is clearly not applicable to the setting of patent litigation. In this study, we incorporate both the strategic and financial aspects of corporate litigation by examining how litigation stakes and financial distress jointly affect stock market reactions to patent litigation settlements.

Our results show that litigation settlements result in positive abnormal returns for both defendants and plaintiffs, indicating that litigations are costly for both parties and, thus, the resolution of litigation is considered good news by the market for both warring parties. Consistent with Hirshleifer (1991) and Bebchuk (1984), and in contrast to the empirical findings in Fournier and Zuehlke (1989), we find that the market does not expect high-stakes lawsuits to settle easily and, thus, their settlement produces more positive abnormal returns for both defendants and plaintiffs. Furthermore, consistent with the predictions in Hirshleifer (1991), our results show that complementarity interacts with litigation stakes to affect litigation outcomes, although no significant direct association exists between complementarity and settlement likelihood. Although we find some evidence of the existence of financial distress costs by showing that closeness to bankruptcy has explanatory power over market reactions to settlement news, our results contradict a conclusion drawn in prior research—that the primary benefit of litigation settlements is the unexpected relief from financial distress costs. Our results show that shareholders are more concerned with the strategic implications of patent litigation than with the threat of a monetary transfer brought about by the lawsuit. This finding is consistent with the growing focus on the strategic role of patents in the economics and industrial organization literature.

This study contributes to the literature on the economics of legal dispute resolution by providing new evidence in support of theoretical models that focus on the strategic aspects of corporate litigation. In contrast to findings from previous empirical research, our results lend support to the prediction of a negative relation between litigation stakes and settlement likelihood. This finding helps explain the existence of prolonged cases of strategically important high-stakes legal disputes, despite the seemingly uncontroversial rationale in favor of settlements. Moreover, this study makes an attempt to integrate the strategic and financial aspects of corporate litigation that so far have only been studied in separate lines of research in the literature. The findings suggest that the relative importance of the two aspects may vary considerably across different types of lawsuits, thus highlighting the importance of adequately considering the key features of the underlying setting for each type of lawsuit in empirical studies.

The paper is organized as follows. The next section provides a brief review of related literature and institutional background on patent and patent laws. Section 3 discusses our research hypotheses. Section 4 describes the sample and analysis methods used. Sections 5 and 6 discuss the empirical results and additional analyses. Section 7 concludes.

2. Literature review and institutional background

2.1. Trial vs. settlement decision

Several theoretical legal studies have examined the settle-out-of-court vs. go-to- trial decision in a variety of settings and identified common determinants (see, for example, Bebchuk, 1984; Gould, 1973; Nalebuff, 1987; Shavell, 1982, among others). Fournier and Zuehlke (1989) classify these determinants into four broad categories: (a) the amount of damages at stake in a trial; (b) the variance of the anticipated award distribution from trial; (c) the costs of litigating and rules determining who shall bear these costs; and, finally, (d) the presence of strongly skewed odds favoring one party or another. In this study, we focus on the first determinant – the litigation stakes.

The early literature (e.g. Gould, 1973; Shavell, 1982) focuses on the incentives of the litigating parties and assumes that disputes will settle out of court when the cooperative surplus (i.e. the amount by which the utility gained from avoiding continued litigation exceeds the expected value of the trial outcome), as perceived by both litigating parties, is positive. This literature generally predicts that high-stakes lawsuits are more likely to settle. The literature subsequently evolved to explicitly model the bargaining process in a game theory setting in diverse ways, which has led to predictive and normative theories that are rivals to each other (Cooter and Rubinfeld, 1989).

One stream of this research generates definitive predictions by making restrictive assumptions about the scope of bargaining, the timing of offers, and the ability of parties to transmit information. For example, Bebchuk (1984) treats the settlement amount as endogenous, but assumes an information asymmetry between the plaintiff and the defendant. In such a setting, the probability of settlement will be lower for high-stakes litigations. In contrast, Nalebuff (1987) incorporates signaling in settlement bargaining and assumes a specific move order. To make the threat of going to trial credible, the plaintiff may strategically demand a larger settlement. Under Nalebuff’s specific structure and assumptions, the model predicts a positive relation between settlement likelihood and litigation stakes.

Due to the restrictive nature of the assumptions regarding the specific move order between the litigation parties, the models described above are not able to adequately address the problem of dividing the cooperative surplus between the defendant and plaintiff, which is at the heart of the strategic interaction between litigating parties (Cooter and Rubinfeld, 1989). As Cooter and Rubinfeld point out, this distribution problem can act as a source of instability that will result in bargaining breakdowns even when both litigating parties expect positive cooperative surplus if they settle. Therefore, a general model that explicitly studies the implications of the distribution problem can shed more light on the dynamics of the settlement process.

Hirshleifer’s (1991) economic theory of conflict is an important theoretical study that models the implications of the distribution problem for conflict resolution. Although the focus of that study is on war, Hirshleifer himself identifies lawsuits as a setting where the model is potentially applicable. Parties in such a conflict would have to choose between productive effort and conflict (lawsuit). According to Hirshleifer, both parties involved in a war incur costs due to the following reasons: (a) attrition of the resources devoted to the conflict (e.g. military casualties); (b) forgone opportunities (e.g. the guns-and-butter tradeoff); and (c) collateral damage to productive resources (e.g. the potentially devastating consequences of nuclear war).

Parties involved in a patent lawsuit experience costs similar to those in the war setting. For example, attrition of resources can arise due to direct legal costs. Patent lawsuits can lead to forgone opportunities due to distraction to management or loss in productivity. There can be collateral damage when the uncertainties brought about by the lawsuit inhibit investment in the further development or productive use of the technology in dispute.

In Hirshleifer’s model, similar to the patent setting, the parties’ productive efforts can have complementarities. The model focuses on how outcomes are constrained by the technology of conflict and has two implications in the context of patent litigations: (a) peace (settlement) is less likely when the stakes are high; and (b) parties may continue to fight even in the presence of complementarity (i.e. when opportunities exist for the litigating parties to benefit from cooperative productive efforts), although the presence of complementarity can moderate the negative relation between stakes and settlement likelihood.

The first implication highlights the role of the distribution problem in continued conflicts. In anticipation of a “winner take all” outcome, both parties to a conflict invest more in fighting when there is more at stake. The second implication depends on the first. It is intuitively obvious that the presence of complementarity in productive efforts should favor settlement since both parties have incentives to take advantage of the complementarities. However, the less obvious implication arises because of the first implication: the presence of complementarity implies higher stakes, which make peace less likely. The two opposing effects of complementarity imply that the negative relation between litigation stakes and settlement likelihood will be mitigated by complementarity, although the presence of complementarity alone does not make peace more likely.

The implications of conflict theory regarding litigation stakes are also consistent with the predictions from the litigation settlement model in Bebchuk (1984), although the two models use different frameworks of analysis. Conflict theory examines the rational choice between fighting and productive efforts in general, whereas Bebchuk focuses on the implications of information asymmetry specific to lawsuit settings. In particular, the Bebchuk model demonstrates that information asymmetry deters settlement by making it difficult for the plaintiff to judge the actual type of defendant and, therefore, to propose a settlement amount that will be accepted by the defendant. In Bebchuk’s analysis, as the amount at stake in a trial increases, there is a corresponding increase in the probability that a dispute will end in a trial rather than an out-of-court settlement.

Unlike in the theoretical literature, settlement likelihood has rarely been studied empirically. Fournier and Zuehlke (1989) employ an empirical model of settlement choice to examine whether the variables prominent in the theoretical literature have statistically relevant implications for explaining the likelihood of settlement. They examine lawsuits spanning eighteen different kinds of disputes and find evidence that settlement likelihood increases with litigation stakes. We note, however, that it is likely that litigation stakes are tied to the nature of the dispute. For example, patent lawsuits typically have larger damages at stake than disputes over contracts. Thus, a finding that settlement likelihood increases with litigation stakes might be because patent lawsuits are more likely to settle.

2.2. Financial distress and stock market reactions to litigation-related news

The finance literature has exploited market reactions to litigation-related news to investigate the importance of financial distress costs independent of economic distress. There are competing views in the finance literature on the importance of financial distress costs. Based on the Coase theorem (Coase, 1960), studies like Haugen and Senbet (1978) argue that relatively costless informal reorganizations between equity and debt holders can preclude any drastic consequences of financial distress. Studies like Gertner and Scharfstein (1991) and Giammarino (1989), however, invoke factors such as information asymmetry and the free rider problem to argue that financial distress has significant consequences. In the literature, inter-firm lawsuits are considered useful settings to demonstrate the existence of financial distress costs because lawsuits are presumed to create a setting in which firms are placed in financial distress for reasons unrelated to their operational performance.

Cutler and Summers (1988) examined market reactions to a series of events in the high-profile Pennzoil vs. Texaco lawsuit and found that Pennzoil gained only a fraction of what Texaco lost in terms of dollar values. The authors attribute the asymmetric gain and loss to the indirect costs of financial distress. Following this study, Bhagat et al. (1994) used a large sample of inter-firm lawsuits to further investigate the importance of financial distress costs. They found significant negative abnormal returns for defendants and insignificant abnormal returns for plaintiffs around lawsuit filing dates. Part of the loss suffered by the defendants is recovered when lawsuit settlements are announced. The cross-sectional analyses in Bhagat et al. relate the negative returns around filing announcement dates and positive returns around lawsuit settlement dates directly to the level of financial distress for defendant firms, but they do not find a significant relation for plaintiff firms. Based on these findings, they attribute the positive market reaction for defendant firms upon settlement to the unexpected relief of financial distress induced by the lawsuit, thus providing support for the existence of costs imposed by financial distress.

In contrast, Bizjak and Coles (1995) find that the threat of a monetary transfer has little power to explain either wealth effects or the likelihood of settlement. They conjecture that the central concern of defendants is the lawsuit-induced uncertainty regarding whether or not they will be able to initiate or continue profitable business practices. Our study differs from the above two studies in that we focus on the event of settlement and explicitly consider market expectations regarding the litigation outcomes prior to the news of settlement. For example, in the ongoing Apple Inc.–Samsung Electronics Limited battle, several industry experts have written about their expectations regarding the outcome of the dispute. The stock prices of the two companies probably already reflect the market’s expectations regarding the likelihood and magnitude of the resolution of the conflict.

2.3. Institutional background: patent and patent laws

Firms extensively use patents as a strategic tool to establish entry barriers and to create and maintain competitive advantage, especially in technology-intensive industries (Chakrabarti et al., 1993; Porter, 1980; Rivette and Kline, 2000). Earl (2001) considers intellectual property protection through patents a significant part of knowledge management strategy. Similarly, Abril and Plant (2007) and Davenport et al. (1998) consider aggressive protection of “knowledge assets” as the main driving force behind a strategic approach to knowledge management.

Patent litigations entail significant direct and indirect costs. The direct costs involve payments to attorneys, experts, consultants, investigators, and anyone else who renders litigation support services. For instance, in defending itself against a patent infringement lawsuit, Research in Motion (manufacturer of Blackberry phones) is estimated to have incurred direct costs up to $22 million. 2

There are other costs (indirect) that a company bears when it enters litigation. These costs can include: (a) the lost time of company employees devoted to litigation instead of more productive activities; (b) the risk that a party’s technical or business information not known to the other party may be revealed and, contrary to protective orders, used by the other party in some adverse manner; and (c) the risk that an infringement defendant’s customers may stop or reduce purchases due to the mere existence of litigation and the threat it poses to the defendant’s continued ability to supply or to a customer’s perception of potential infringement liability as a product user (Schlicher, 2011). In a similar vein, there can be collateral damage because of other firms’ unwillingness to partner in joint projects because of the lawsuit. Schlicher argues that the indirect costs are likely to far exceed the direct costs. As a consequence, disputes regarding patents are of economic significance, both in terms of amounts at stake and costs of litigation, and both patent holders and law firms treat intellectual property (IP) litigation as a growth industry (Raghu et al., 2008).

The growing importance of patents and patent disputes has been accompanied by significant change in the legal landscape surrounding patent lawsuits over the last three decades. In particular, empirical legal studies have shown that the creation of the Federal Circuit in 1982 and the Markman decision 3 in 1997 are important changes in the patent regime in the United States. For example, Niles (1993) shows that since its inception in 1982, the Federal Circuit has become one of the most influential actors in the creation of licensing law.

Kesan and Ball (2006) show that there was a significant difference in duration and number of documents filed in cases resolved through summary judgment for the 1997 filed cases compared to the 1995 filed cases, a pattern consistent with the notion that more resources are allocated to the step of claim construction following the Markman decision, because Markman made claim construction a threshold legal issue in patent litigation. Kesan and Ball also assert that due to the increased uncertainty regarding how the court will handle the case, the claim construction procedure introduced by Markman would change how the parties involved in a patent lawsuit evaluate the probability of winning at trial and, in turn, the incentives to settle. In view of these significant changes in the patent regime, we chose a sample period well after the Markman ruling so that there would be no significant differences across the cases related to changes in the legal regime.

3. Hypothesis

We drew on the conflict theory model in Hirshleifer (1991) first to identify variables that potentially shaped market expectations and then to examine how these variables affected market reactions to settlements. We analyzed separately the effect on stock returns of defendants and plaintiffs. In addition, we examined the effect of the financial distress proxy used in Bhagat et al. (1994) and Bizjak and Coles (1995). To our knowledge, these two are the only studies that used a large sample to examine cross-sectional differences in abnormal returns around litigation settlements.

3.1. Litigation stakes

If the market formed expectations consistent with the theoretical predictions of Hirshleifer (1991) and Bebchuk (1984), it would expect lawsuits with higher stakes to be less likely to settle and thus to induce more “dead weight” loss due to litigation costs. As such, the market would be surprised by the settlement announcement of a high-stakes lawsuit, and the settling companies (both the defendant and the plaintiff) would experience more positive abnormal returns since, contrary to market expectations, they would not incur the costs of conflict going forward. In contrast, if the specialized settings in, say, Nalebuff (1987) dominated, we would see the opposite relation. Therefore, we hypothesize (in non-null form) that:

H1A: Abnormal returns for defendants around settlements will vary with litigation stakes.

H1B: Abnormal returns for plaintiffs around settlements will vary with litigation stakes.

3.2. Financial distress

If, as argued by Cutler and Summers (1988) and Bhagat et al. (1994), patent lawsuit settlements provide unexpected relief from financial distress for defendants, we would expect a positive relation between settlement announcement returns and proximity to financial distress. We note, however, that financial distress costs can affect return around settlement announcements in the opposite direction, if we consider the resources sacrificed by the defendants in agreeing to the settlement. Most settlements result in an exchange of cash from defendants to plaintiffs. For financially distressed defendants, this exchange can exacerbate the liquidity concern and, hence, further increase the cost of financial distress. Thus, the abnormal returns around settlement announcements for defendants will increase or decrease with the probability of bankruptcy, depending on which of the two effects dominates: the successful avoidance of bankruptcy hypothesized by Bhagat et al. or the liquidity effect discussed above. On the flip side, financially distressed plaintiffs should be able to benefit more than financially healthy plaintiffs from patent litigation settlements, because the immediate injection of cash from settlements helps to relieve the financial distress cost. Hence, we hypothesize (in non-null form) that:

H2A: Abnormal returns around settlements for defendants will vary with defendants’ probability of bankruptcy.

H2B: Abnormal returns around settlements for plaintiffs will vary with plaintiffs’ probability of bankruptcy.

3.3. Complementarity

Conflict theory discusses two opposing effects of complementarity on the likelihood of settlement: a positive direct effect and a negative effect through stakes. In our setting, complementarity comes into play when potential opportunities exist for the defendant and plaintiff to engage in cooperative productive efforts, which typically take the form of joint projects or cross-license agreements that can increase the market share of both parties. On the one hand, the presence of complementarity promotes settlements because the parties have economic incentives to work together (the direct effect). On the other hand, cooperative opportunities are more likely to exist when the technology in dispute is economically or strategically important, which usually implies high litigation stakes (the indirect effect). One empirical implication of this model is that the association between litigation stakes and the settlement likelihood (and, in turn, market reactions around settlements) can be confounded by the existence of complementarity. Specifically, we expect to observe the existence of complementarity to mitigate the effect of litigation stakes, because the market will be less surprised by the settlement of a high-stakes lawsuit when complementarity exists. As we expect a positive loading on litigation stakes in explaining market reactions, the loading on the interaction term of litigation stakes and complementarity should be negative. Thus, we hypothesize (in non-null form) that:

H3A: The association between litigation stakes and abnormal returns around settlements for defendants will be moderated by the presence of complementarity.

H3B: The association between litigation stakes and abnormal returns around settlements for plaintiffs will be moderated by the presence of complementarity.

4. Empirical analysis

4.1. Sample and data sources

Our sample was based on a settlement data set 4 provided by FTI Consulting, a firm specializing in strategic and litigation-related services. The FTI data set covered about 140 patent litigation cases settled in the United States from 2002 to 2006, most of which were filed after the Markman decision. For the purpose of this study, at least one party to the lawsuit needed to be publicly traded in the United States so that the market reaction could be observed. This restricted the sample to 82 defendants and 72 plaintiffs. For each settlement, the data set contained the identity of defendant and plaintiff, the settlement amount, the information source, the publication date of the source, and some additional information about the two parties or litigation history. The information sources included press releases, newswire services, and the business press. Since each settlement was usually reported multiple times, we verified the earliest date on which the market learned of the settlement by performing extensive searches around the source date in both Lexis-Nexis and company press releases, with the names of both parties as keywords. We excluded cases in which the same firm settled multiple lawsuits during a year. We further deleted cases that were settled after the jury reached a verdict, because such cases are not voluntary settlements.

Our final sample consisted of 75 defendants and 67 plaintiffs, with 46 paired cases in which both the defendant and plaintiff were publicly traded firms and thus were included in our defendant and plaintiff sample, respectively. The identification of these paired cases was critical to the empirical analysis on the effect of complementarity. The return data for the sample firms came from CRSP and financial statement data came from COMPUSTAT.

4.2. Research design

Following Bhagat et al. (1994), we ran cross-sectional regressions separately for defendants and plaintiffs, with abnormal returns around patent litigation settlements as the dependent variable.

4.2.1. Dependent variable

We used five-day cumulative abnormal return (day −2 through day 2) around settlement announcements as the dependent variable for regression analyses. We chose a slightly longer event window than Bhagat et al. (1994) (day −1 and day 0), because settlements are usually reported by multiple sources with slightly different publishing dates. Following Bhagat et al., we calculated abnormal returns using the market model and estimated beta based on daily returns from day −171 through day −22. We use the CRSP NYSE/AMEX/NASDAQ Value-Weighted Market Index as the proxy for the market return.

4.2.2. Independent variables

We measured litigation stakes using the reported settlement amount scaled by the market value of the firm at the end of the previous fiscal year, because this proxy allowed us to capture the importance of a lawsuit specific to each party.

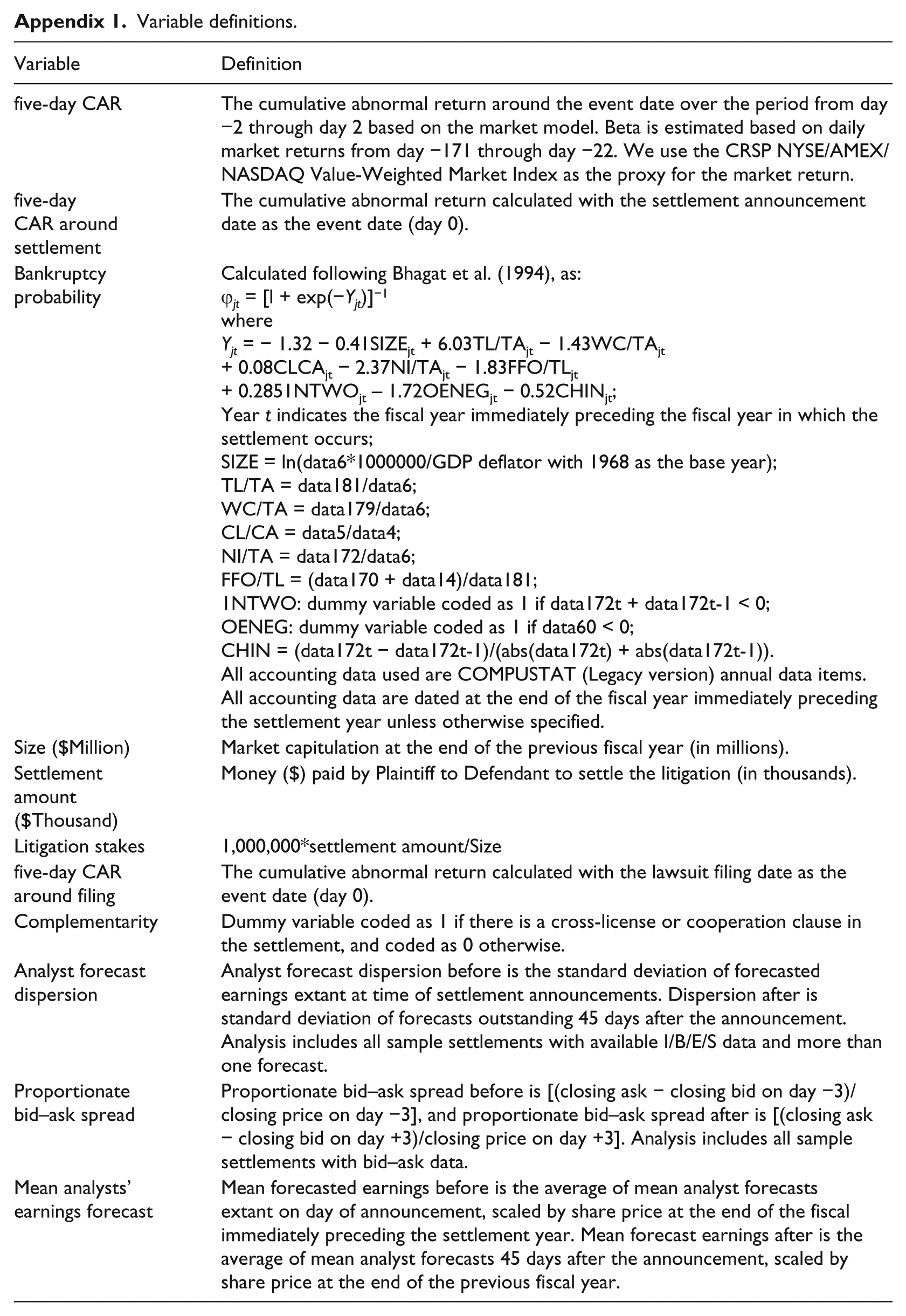

Probability of bankruptcy was calculated based on the parameter estimates in Ohlson (1980) and firm-specific accounting data at the end of the previous fiscal year. Following Bhagat et al. (1994), the probability is calculated as:

The variable Yjt has been constructed following Bhagat et al., in which:

Following Bhagat et al., Year t indicates the fiscal year immediately preceding the fiscal year in which the settlement occurred. Using accounting data from the preceding fiscal year helped to ensure that the effects of the settlement were not reflected in the control variables. SIZE = log(tota1 assets/GNP deflator); TL/TA = total liabilities/total assets; WC/TA = working capital/total assets; CL/CA = current liabilities/current assets; NI = net income; NI/TA = NI/total assets; FFO/TL = cash flow from operations (or funds provided by operations)/total liabilities; 1NTWO = 1 if net income was negative for the last two years and 0 otherwise; OENEG = 1 if total liabilities were greater than total assets and 0 otherwise; and CHIN is the most recent change in net income scaled by the sum of the absolute values of net incomes from the last two years.

We included market capitalization at the end of the previous fiscal year in all regressions as a control for size. Again, using accounting data from the preceding fiscal year helped to ensure that the effects of the settlement were not reflected in the control variables. We also used the logarithm of market capitalization as an alternative measure of size; the results did not change qualitatively.

We performed analysis using the paired sample to test the hypothesis regarding complementarity. The variable complementarity was coded as one if there were cross-licensing or cooperation clauses in the settlement agreement, and coded as zero otherwise.

For a subset of our sample cases (41 defendant firms and 39 plaintiff firms), we were able to identify the exact lawsuit filing date. 5 We used abnormal returns around filing dates as an additional control variable in the supplemental analysis. CAR around lawsuit filing dates was calculated in the same manner as CAR around settlement dates.

5. Discussion of results

5.1. Distribution of settlements

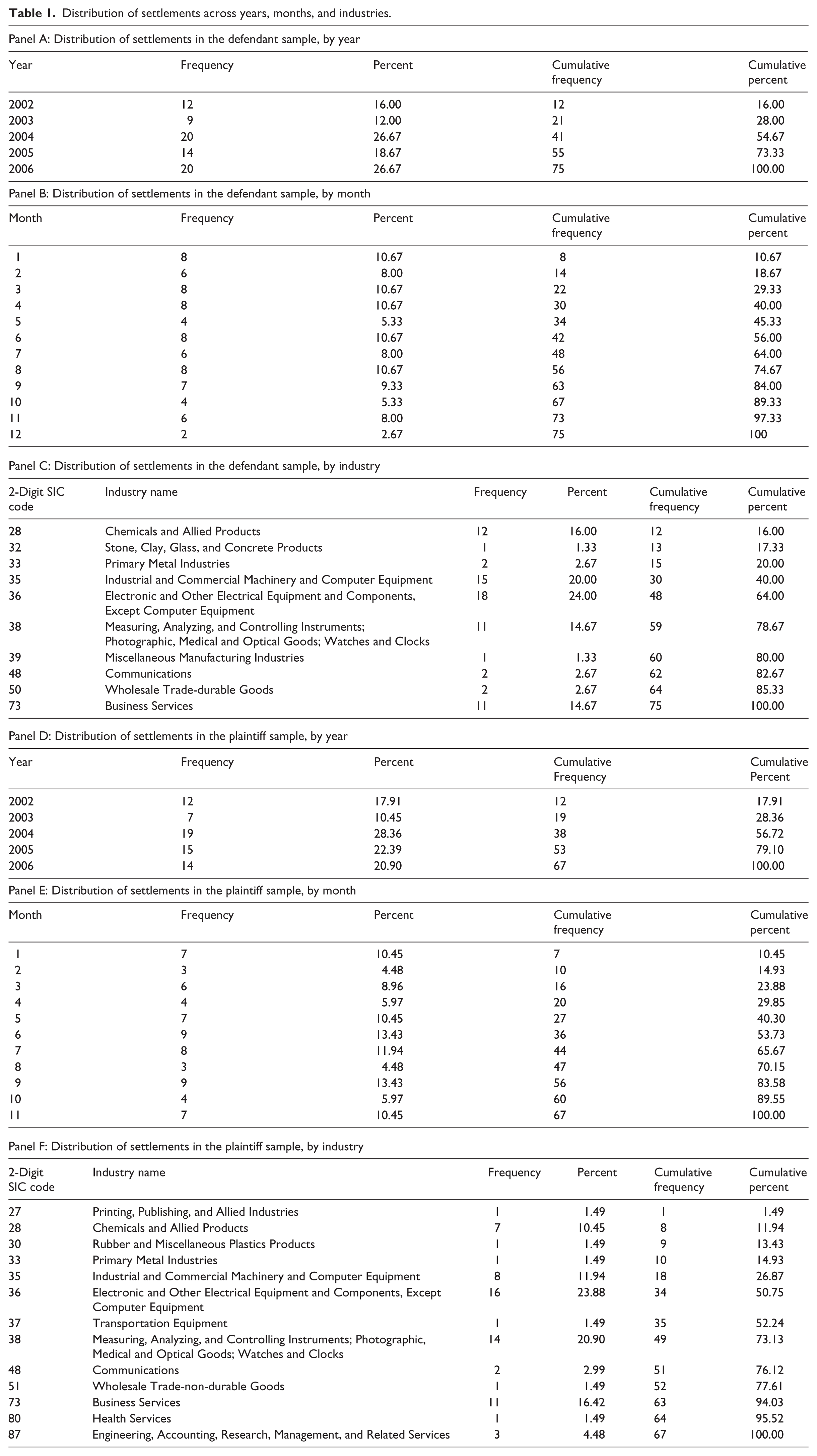

Table 1 presents the distribution of settlements by calendar year, calendar month, and industry separately for the defendants and plaintiffs in our sample. As indicated in Panels A, B, D, and E of Table 1, no calendar year had more than 29% of the settlements, and no calendar month had more than 14% of the settlements, in either the defendant or plaintiff sample, suggesting that the sample was well distributed across calendar years and months and was not clustered in event time. Consistent with our expectations regarding patent litigations, Panels C and F show that high-tech industries are heavily represented in both the defendant and plaintiff samples; this is particularly true for the electronics industry (SIC code: 36), the industrial/commercial and computer equipment industries (SIC code: 35), and the precision, medical and optical instruments industries (SIC code: 38).

Distribution of settlements across years, months, and industries.

5.2. Return patterns

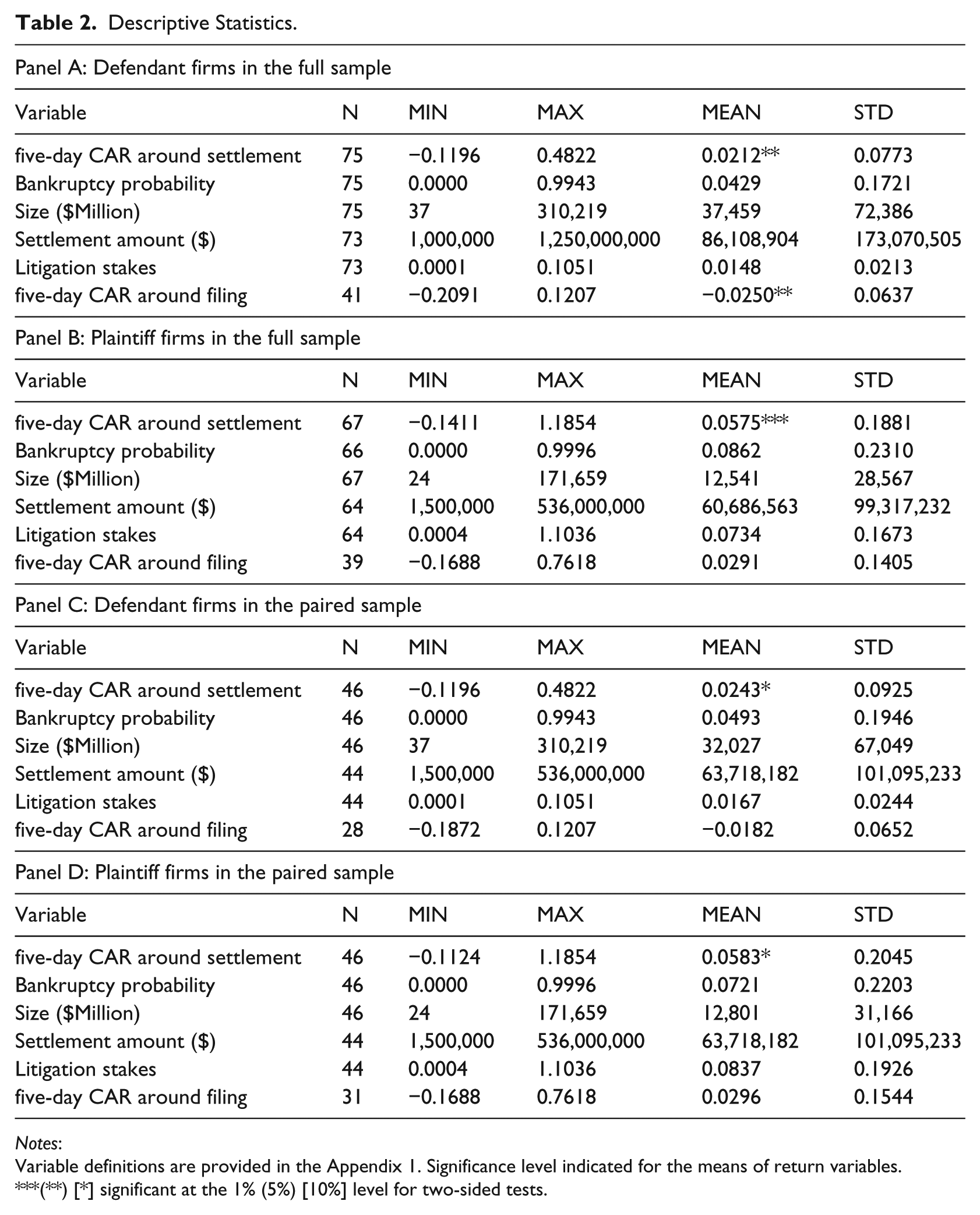

Abnormal returns around lawsuit settlements and filings are reported in Table 2. The average five-day cumulative abnormal return (CAR) around settlement announcements and lawsuit filings were 2.12% and −2.5%, respectively, for the defendant sample, both being significant at the 5% level. The return patterns were consistent with those reported in Bhagat et al. (1994), and they suggested that defendants suffered negative returns around filing dates and experienced positive returns around settlement announcements. This reversal implies that lawsuits are costly to defendants and that settlements are, in turn, considered good news.

Descriptive Statistics.

Notes:

Variable definitions are provided in the Appendix 1. Significance level indicated for the means of return variables.

(**) [*] significant at the 1% (5%) [10%] level for two-sided tests.

The average of the five-day CAR around settlement announcement was 5.75% for the plaintiff sample, being statistically significant at the 1% level. This is in contrast to the non-significant returns for plaintiffs found in Bhagat et al. (1994). Our results suggest that plaintiffs also benefited from settlements, although they did not experience wealth gain or loss when lawsuits were filed (since the five-day CAR around filing was insignificant for the plaintiff sample).

5.3. Litigation stakes (H1A & H1B)

As discussed earlier, several theoretical models in the literature have different implications regarding the relation between litigation stakes and settlement likelihood. According to Bebchuk (1984) and Hirshleifer (1991), lawsuits with higher stakes will be less likely to settle, which will result in a negative relation between settlement likelihood and litigation settlement. In contrast, Nalebuff (1987) predicts a positive relation. We empirically examined how the stock market formed expectations regarding a settlement by analyzing the stock returns around settlement announcements. Under our maintained hypothesis of market efficiency, the stock market would only react to the settlement news to the extent that the outcome was not expected. As a result, we could gauge how “surprised” the market was in response to the settlement news by examining abnormal returns around the settlement event.

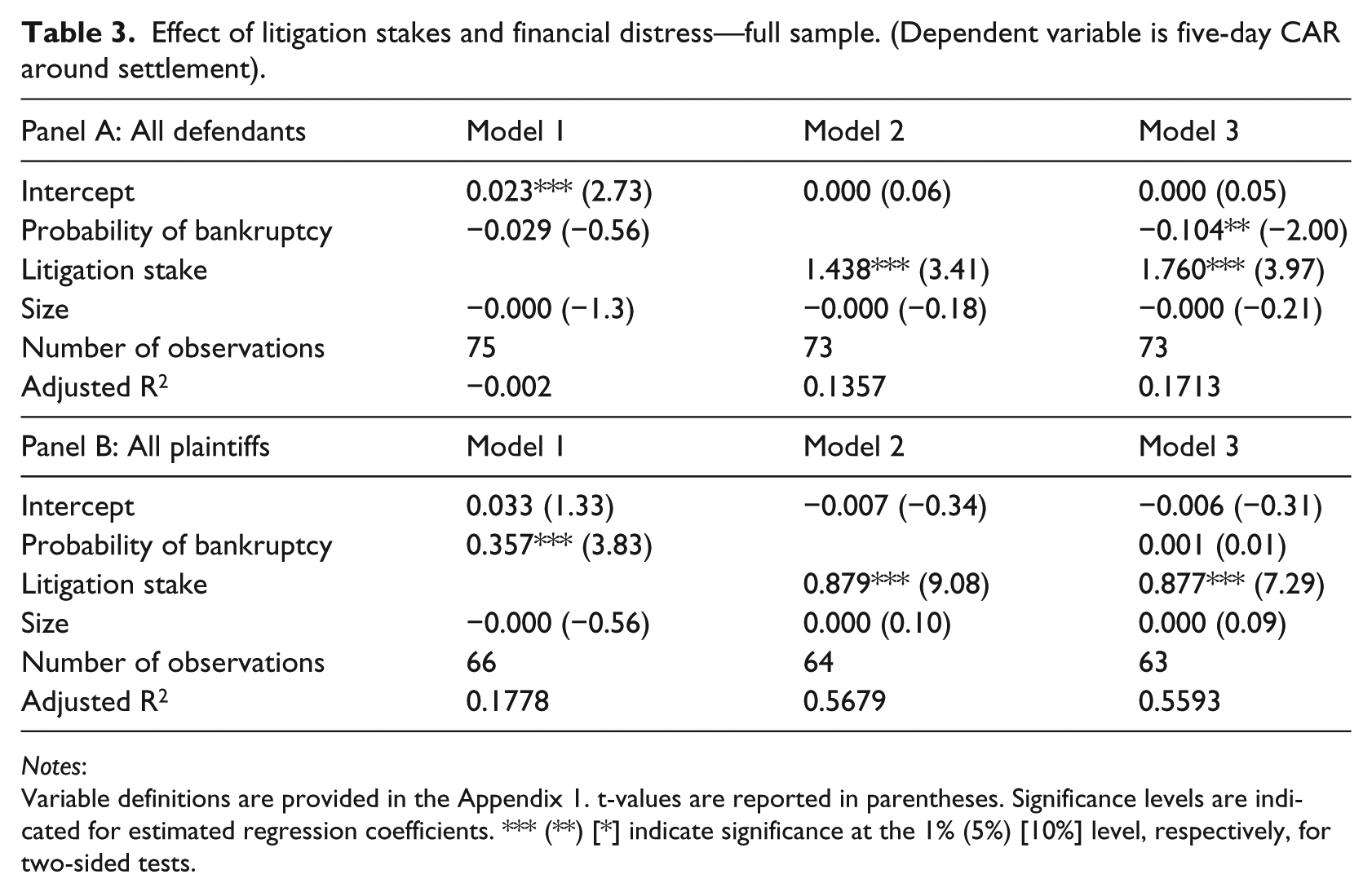

The coefficients on litigation stakes in Panels A and B in Table 3 demonstrate the results of the test H1A and H1B, respectively. Our findings on the test of H1A and H1B showed that the market expected a lower likelihood of settlement for a high-stakes lawsuit and, as a consequence, reacted more strongly when such a lawsuit was actually settled. Specifically, the coefficients on litigation stakes in Table 3 were consistently positive and significant for both defendant and plaintiff firms. Our results thus provide support to the conflict theory in Hirshleifer (1991) and the litigation settlement model in Bebchuk (1984) and, at a minimum, suggest caution in drawing conclusions regarding settlement likelihood based on the findings in Fournier and Zuehlke (1989). In addition, results reported in Table 3 showed that litigation stakes has significantly higher explanatory power than probability of bankruptcy, suggesting that litigation stakes is a more important determinant of settlement likelihood than financial distress, which is the focus of previous stock market studies on litigation settlements.

Effect of litigation stakes and financial distress—full sample. (Dependent variable is five-day CAR around settlement).

Notes:

Variable definitions are provided in the Appendix 1. t-values are reported in parentheses. Significance levels are indicated for estimated regression coefficients. *** (**) [*] indicate significance at the 1% (5%) [10%] level, respectively, for two-sided tests.

We note that a potential problem with our stakes measure is that it is highly correlated with another construct—settlement terms. In particular, a plaintiff should experience higher return upon the settlement when the settlement terms are more favorable (i.e. receiving a larger amount of cash from the defendant). Since our stakes measure is highly correlated with settlement amount, for plaintiffs, we cannot differentiate the effect of settlement terms from the effect of market expectations. On the other hand, the effect of settlement terms and the effect of market expectations should go in the opposite direction for the defendant, because a larger settlement amount means less favorable terms for the defendant. Therefore, the consistent positive association between defendants’ abnormal returns and our stakes measure gives us added confidence in attributing the results to settlement likelihood.

5.4. Financial distress (H2)

The coefficients on probability of bankruptcy in Panels A and B in Table 3 demonstrate the results of the test H2A and H12B, respectively. Model 1 in Table 3 is similar to the one used in Bhagat et al. (1994). The coefficient on probability of bankruptcy is insignificant for defendants, and positive and significant for plaintiffs. This result is in contrast to Bhagat et al., who find a significant positive coefficient on probability of bankruptcy for defendants and an insignificant coefficient for plaintiffs. After controlling for litigation stakes (Model 3), the coefficient on probability of bankruptcy becomes negative and significant for defendants, but probability of bankruptcy loses significance for plaintiffs. Overall, there is some support for the importance of financial distress costs, but our results suggest that unexpected relief from financial distress costs is unlikely to be the primary benefit of patent litigation settlements.

As discussed in the hypotheses development section, for defendants, settlements can have two opposing effects with respect to financial distress costs. Bhagat et al. (1994) argue that a settlement can convey to the market news of a successful avoidance of bankruptcy and relief from financial distress. However, a settlement also typically involves a transfer of cash from the defendant to the plaintiff, leading to increased liquidity concerns for the defendant. Our finding of a negative coefficient on the probability of bankruptcy suggests that the second effect dominates for patent litigations, a finding that is in direct contrast to the results found by Bhagat et al.

A possible explanation for this difference is the unique feature of patent litigations. In particular, Bhagat et al. (1994) make the implicit assumption of “no cash flow” settlements, that is, the amount of cash exchanged upon settlements is insignificant (at least, relative to the requested amount of damage). This does not appear to be the case for patent lawsuits. In our sample, the plaintiff typically asked for an unspecified amount of damage at filing, but the cash exchange upon settlement was significant. If a financially distressed defendant reaches a settlement and thus has to pay a large amount of cash to the plaintiff, it is not surprising that the market considers the settlement to be less good news. By the same token, financially distressed plaintiffs could benefit more from the immediate cash injection upon settlements than financially healthy plaintiffs. This could lead to the observed positive association between the probability of bankruptcy and plaintiffs’ abnormal returns upon settlements.

5.5. Complementarity (H3A & H3B)

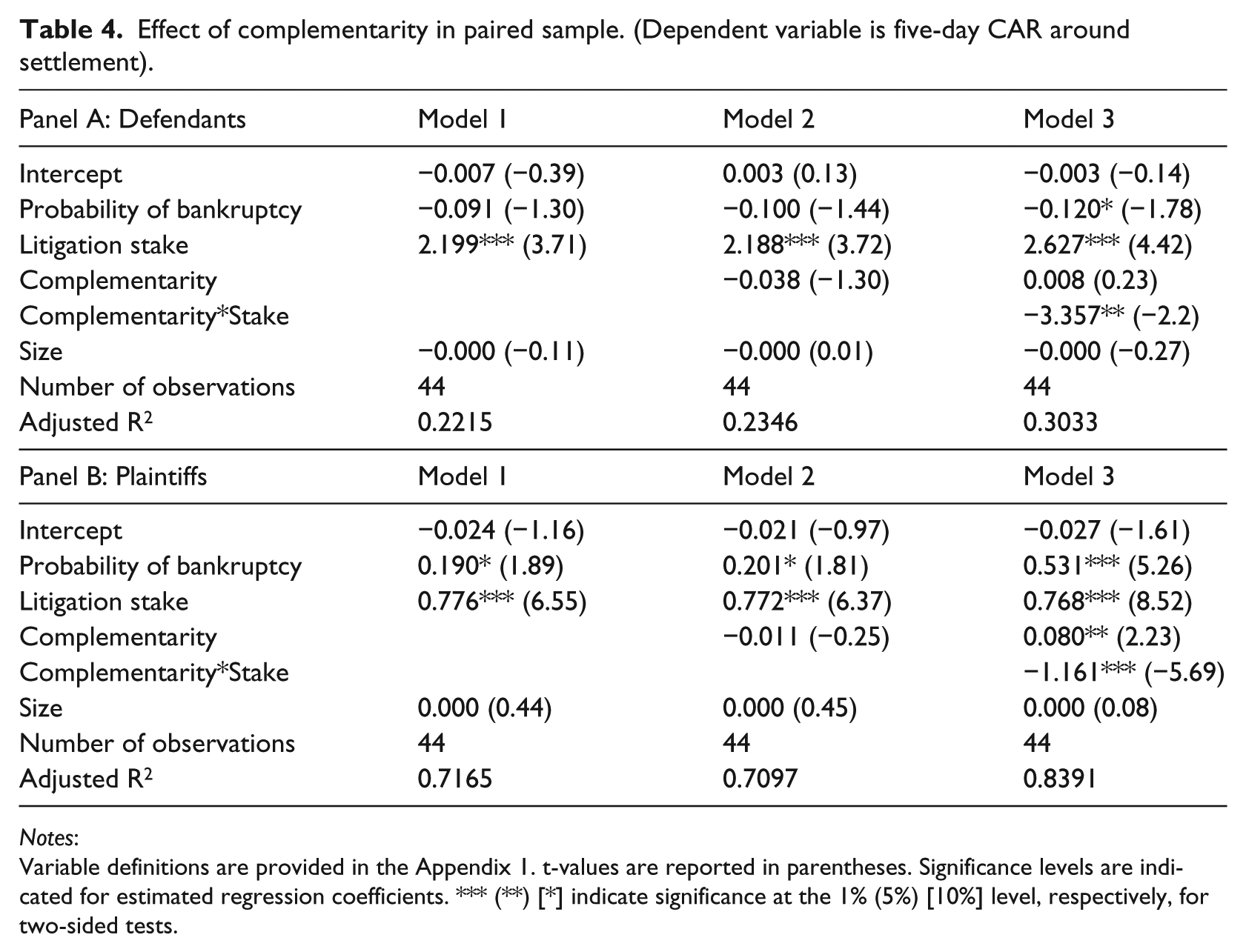

We examined the effect of complementarity using the paired sample. The results from Model 1 provided the baseline for the paired sample. Consistent with our expectation, the coefficients on complementarity in Model 2 were insignificant for both defendants and plaintiffs, indicating no direct association between market reactions and the existence of complementarity. However, as shown in Table 4, the coefficients on the interaction term of complementarity and litigation stakes in Model 3 are −3.357 and −1.161 for defendants (Panel A) and plaintiffs (Panel B), respectively; both were significant at a 5% level. These findings indicate that the positive association between litigation stakes and abnormal returns around settlements were stronger in absence of complementarity, thus providing support to H3A and H3B.

Effect of complementarity in paired sample. (Dependent variable is five-day CAR around settlement).

Notes:

Variable definitions are provided in the Appendix 1. t-values are reported in parentheses. Significance levels are indicated for estimated regression coefficients. *** (**) [*] indicate significance at the 1% (5%) [10%] level, respectively, for two-sided tests.

6. Additional analyses

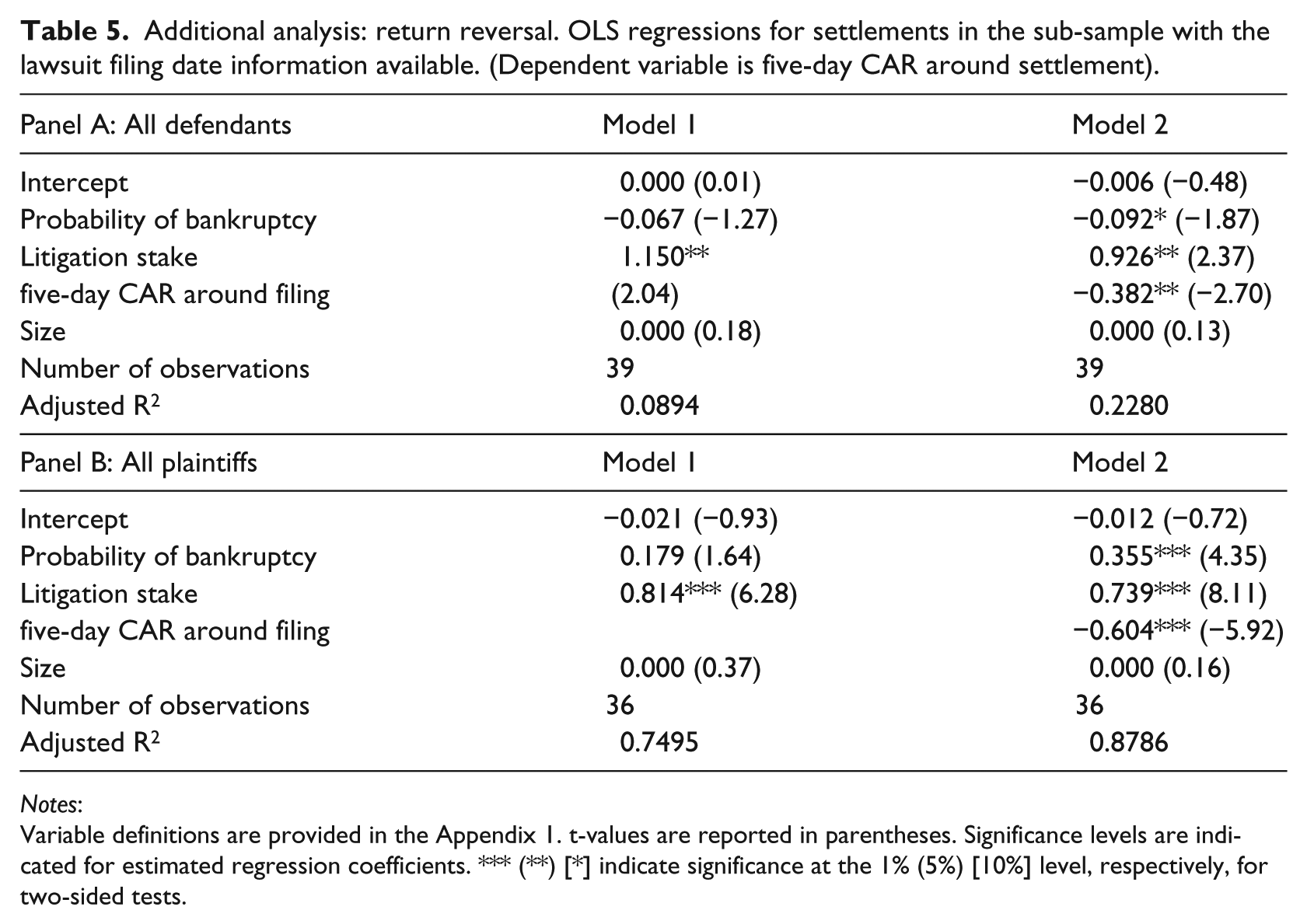

We performed additional analyses to check the robustness of our findings. First, we included the abnormal returns around lawsuit filings as an additional independent variable for the subsample, with the lawsuit filing dates available. We performed this test to control for the magnitude of benefits from settlements. That is, lawsuits were costly for the reasons we discussed earlier, and this cost varied across cases. Accordingly, the magnitude of the settlement’s benefit also varied across cases. It is possible that the relation observed between abnormal returns around settlements and litigation stakes was solely driven by that variation in the impact of settlements, rather than by the difference in the expected probability of settlements, as hypothesized.

Table 5 reports our additional analysis that helped to rule out that possibility. We used the abnormal returns around settlements as a proxy for the magnitude of lawsuit costs or settlement benefits. Specifically, we expected a negative association between returns around filings and returns around settlements, and examined whether the variables of interest were still significant after controlling for the reversal effect. Consistent with our expectations, the coefficients on filing announcement returns in Table 5 Panels A and B were negative and significant, indicating a reversal effect. After controlling for this effect, litigation stakes and probability of bankruptcy were still significant for both defendants and plaintiffs.

Additional analysis: return reversal. OLS regressions for settlements in the sub-sample with the lawsuit filing date information available. (Dependent variable is five-day CAR around settlement).

Notes:

Variable definitions are provided in the Appendix 1. t-values are reported in parentheses. Significance levels are indicated for estimated regression coefficients. *** (**) [*] indicate significance at the 1% (5%) [10%] level, respectively, for two-sided tests.

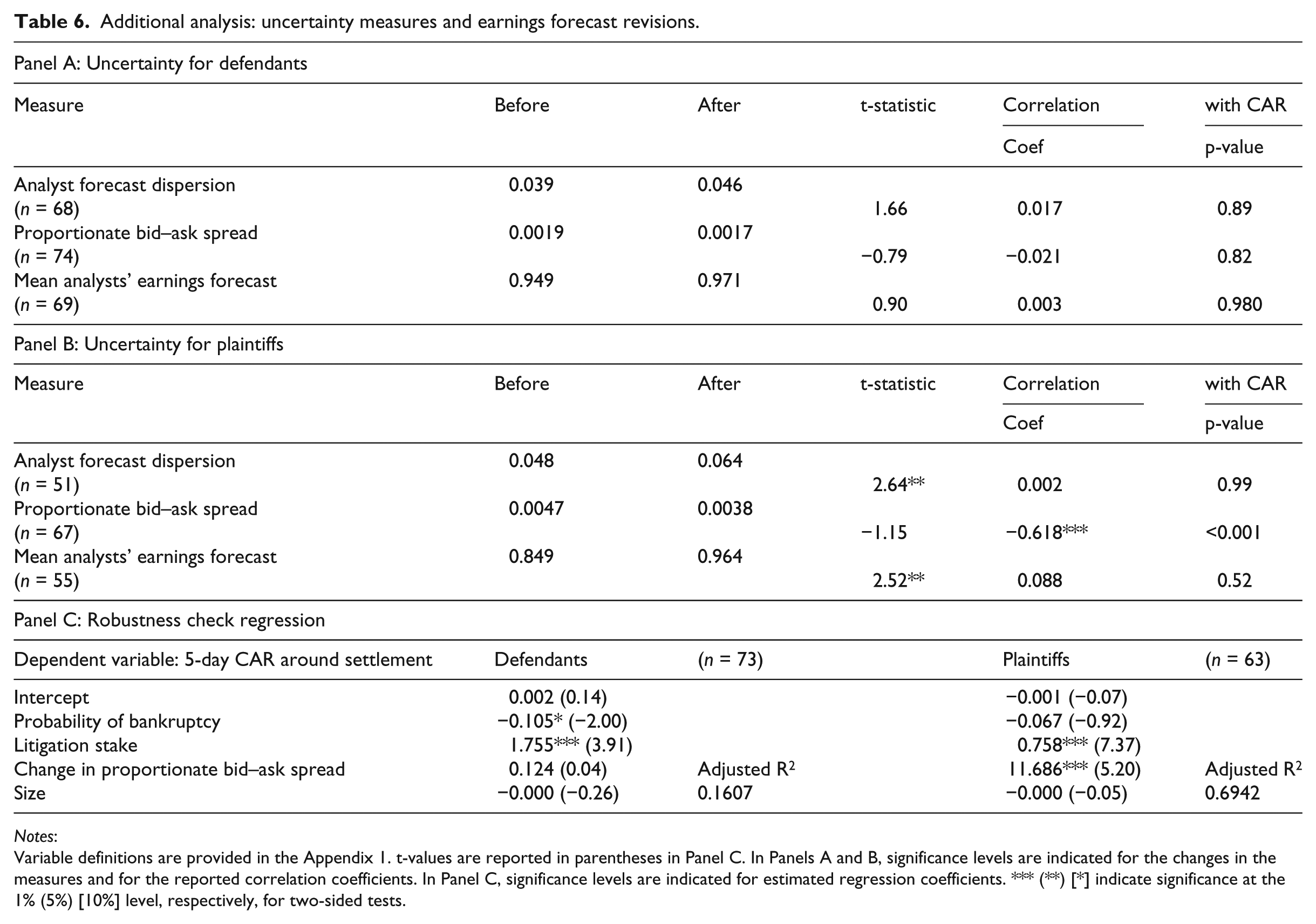

Our second robustness check was related to the effect of reduced risk. Since settlements represent resolution of uncertainty, it was possible that the positive returns around settlements were due to reduced risk. In other words, it could be a denominator effect. Our tests for the reduced risk possibility were similar to those used in Palmrose et al. (2004), who studied the market reactions to earnings restatement announcements. We tested the effect of reduced risk by examining the association of abnormal returns with two alternative measures of uncertainty: (changes in) analyst forecast dispersion and bid–ask spread. If reduced risk because of settlement was driving our results, we would expect both analyst forecast dispersion and bid–ask spread to decrease for both defendants and plaintiffs after the settlement announcement.

Table 6 Panel A covers the descriptive statistics for dispersion of analyst forecasts and the proportionate bid–ask spread. Following Palmrose et al. (2004), change in forecast dispersion was defined as the difference between the standard deviation of forecasted earnings extant at the time of settlement announcements and the standard deviation of forecasts outstanding 45 days after the announcement. Proportionate bid–ask spread was defined as the difference between the price-adjusted bid–ask spread on day −3 and the price-adjusted bid–ask spread on day 3. Defendants’ analyst forecast dispersion actually increased after settlement announcements (from 0.039 to 0.046), so it was unlikely to explain positive abnormal returns for defendants around settlement announcements. Plaintiffs’ analyst forecast dispersion also increased significantly (from 0.048 to 0.064). Again, being a positive change, it was unlikely to explain positive abnormal returns around the announcement. Moreover, the increase appeared to be driven primarily by a revision in analyst forecasts (from an EPS of 0.849 to 0.964). Correlation statistics reported in Panels A and B confirmed that there was no significant correlation between change in forecast dispersion and abnormal returns around settlement announcements.

Additional analysis: uncertainty measures and earnings forecast revisions.

Notes:

Variable definitions are provided in the Appendix 1. t-values are reported in parentheses in Panel C. In Panels A and B, significance levels are indicated for the changes in the measures and for the reported correlation coefficients. In Panel C, significance levels are indicated for estimated regression coefficients. *** (**) [*] indicate significance at the 1% (5%) [10%] level, respectively, for two-sided tests.

The proportionate bid–ask spread, however, decreased for both defendants in Panel A and plaintiffs in Panel B. The correlation statistics also indicated a strong negative correlation between changes in bid–ask spread and plaintiffs’ abnormal returns. The decrease of the bid–ask spread post-settlement announcement, along with the strong negative correlation with abnormal returns, indicated that a test with the change in bid–ask spreads as an additional control variable was necessary to check the robustness of the results.

Panel C of Table 6 reports the results of the robustness regression with the 5-day around settlement. We replicated Model 3 from Table 3 with the change in bid–ask spread as the additional control variable. We found that the coefficient on change in bid–ask spread was significant for plaintiffs. The other coefficients, however, were almost indistinguishable from Model 3 in Table 3, indicating that the conclusions drawn from the results in Table 3 were robust to including the change in bid–ask spread.

7. Conclusion

Corporate litigation has long been recognized as an important business phenomenon, and litigation outcomes can significantly impact the financial health and growth prospect of the firms involved. Despite the relatively uncontroversial rationale in favor of settlements in the litigation process, however, we observe a large number of lawsuits pursued all the way to trial. The significant and growing amount of economic resources spent on corporate litigation highlights the importance of investigating the factors that determine the likelihood of litigation settlements.

Several theoretical studies provide predictions on the relation between settlement likelihood and litigation stakes, producing predictive and normative theories that are rivals to each other. Although models with generalizable settings argue in favor of a negative relation, certain specialized settings predict the opposite. In contrast to the rich theoretical work, there is very limited empirical evidence in support of the relation predicted by these theoretical models. Fournier and Zuehlke (1989) provide the only empirical study in the corporate litigation setting that investigates the relation between settlement litigation and stakes. They document a positive relation between stakes and settlement likelihood, thus lending support to the nonstrategic bargaining models and to Nalebuff (1987) over Bebchuk (1984) and Hirshleifer (1991).

Note that the empirical analysis in Fournier and Zuehlke (1989) is based on a pooled sample of lawsuits of different types, and heterogeneity in lawsuit type can act as a potentially confounding variable in the empirical tests. Moreover, pooling different types of lawsuits is likely to obscure the strategic aspects of settlement behavior, because the strategic importance of legal dispute varies considerably across different types of lawsuits. In order to empirically test the implications of theories that model the strategic interaction in corporate litigation, it is important to identify a setting where the litigating parties have significant future interest other than the cash transfer between defendant and plaintiff that is tied to the litigation outcome.

This study provides empirical analysis of the theoretical predictions regarding settlement likelihood by focusing on patent litigations, as the strategic aspect of settlement behavior is more likely to manifest in patent litigation than in other types of lawsuits. We exploited the stock market reactions to news of settlements under the maintained hypothesis of market efficiency to investigate the economics of settlement behavior. Our empirical strategy allowed us to use the magnitude of the abnormal returns around the settlement news to examine the relation between litigation stakes and settlement likelihood. As the finance literature has exploited market reactions to litigation-related news to investigate the importance of financial distress costs independent of economic distress, we incorporated the key variables studied in this line of research in our empirical analysis to study how litigation stakes and financial distress jointly affected stock market reactions to patent litigation settlements.

This study contributes to the literature on the economics of legal dispute resolution by providing new evidence in support of theoretical models that focus on the strategic aspects of corporate litigation. In contrast to findings from previous empirical research, our results lend support to the prediction of a negative relation between litigation stakes and settlement likelihood. This finding helps explain the existence of prolonged cases of strategically important high-stakes legal disputes, despite the seemingly uncontroversial rationale in favor of settlements. Moreover, this study attempted to integrate the strategic and financial aspects of corporate litigation, which before had only been studied in separate lines of research in the literature. The findings suggest that the relative importance of the two aspects may vary considerably across different types of lawsuits, thus highlighting the importance of adequately considering the key features of the underlying setting for each type of lawsuit in empirical studies.

Our conclusions come with some caveats. In this study, we have analyzed only patent infringement lawsuits. In particular, the patent system is dynamic, with new legislation and landmark judgments significantly impacting the litigation landscape over time. For example, the passage of the America Invents Act in 2011 entailed a conversion to a first-to-file system. The US Circuit Court of Appeals for the Federal Circuits ruled that the widely used 25% rule is fundamentally flawed. 6 These events can completely change the patent litigation landscape. The implications for conflict resolution in patent litigations that we have documented in this study, however, are likely to remain relevant going forward.

Footnotes

Appendix

Variable definitions.

| Variable | Definition |

|---|---|

| five-day CAR | The cumulative abnormal return around the event date over the period from day −2 through day 2 based on the market model. Beta is estimated based on daily market returns from day −171 through day −22. We use the CRSP NYSE/AMEX/NASDAQ Value-Weighted Market Index as the proxy for the market return. |

| five-day CAR around settlement | The cumulative abnormal return calculated with the settlement announcement date as the event date (day 0). |

| Bankruptcy probability | Calculated following Bhagat et al. (1994), as:

φ jt = [l + exp(−Yjt)]−1 where Yjt = − 1.32 − 0.41SIZEjt + 6.03TL/TAjt − 1.43WC/TAjt + 0.08CLCAjt − 2.37NI/TAjt − 1.83FFO/TLjt + 0.2851NTWOjt – 1.72OENEGjt − 0.52CHINjt; Year t indicates the fiscal year immediately preceding the fiscal year in which the settlement occurs; SIZE = ln(data6*1000000/GDP deflator with 1968 as the base year); TL/TA = data181/data6; WC/TA = data179/data6; CL/CA = data5/data4; NI/TA = data172/data6; FFO/TL = (data170 + data14)/data181; 1NTWO: dummy variable coded as 1 if data172t + data172t-1 < 0; OENEG: dummy variable coded as 1 if data60 < 0; CHIN = (data172t − data172t-1)/(abs(data172t) + abs(data172t-1)). All accounting data used are COMPUSTAT (Legacy version) annual data items. All accounting data are dated at the end of the fiscal year immediately preceding the settlement year unless otherwise specified. |

| Size ($Million) | Market capitulation at the end of the previous fiscal year (in millions). |

| Settlement amount ($Thousand) | Money ($) paid by Plaintiff to Defendant to settle the litigation (in thousands). |

| Litigation stakes | 1,000,000*settlement amount/Size |

| five-day CAR around filing | The cumulative abnormal return calculated with the lawsuit filing date as the event date (day 0). |

| Complementarity | Dummy variable coded as 1 if there is a cross-license or cooperation clause in the settlement, and coded as 0 otherwise. |

| Analyst forecast dispersion | Analyst forecast dispersion before is the standard deviation of forecasted earnings extant at time of settlement announcements. Dispersion after is standard deviation of forecasts outstanding 45 days after the announcement. Analysis includes all sample settlements with available I/B/E/S data and more than one forecast. |

| Proportionate bid–ask spread | Proportionate bid–ask spread before is [(closing ask − closing bid on day −3)/closing price on day −3], and proportionate bid–ask spread after is [(closing ask − closing bid on day +3)/closing price on day +3]. Analysis includes all sample settlements with bid–ask data. |

| Mean analysts’ earnings forecast | Mean forecasted earnings before is the average of mean analyst forecasts extant on day of announcement, scaled by share price at the end of the fiscal immediately preceding the settlement year. Mean forecast earnings after is the average of mean analyst forecasts 45 days after the announcement, scaled by share price at the end of the previous fiscal year. |

Acknowledgements

We would like to acknowledge the helpful comments from Paul Beck, Christine Cuny, Rajib Doogar, Nuno Garoupa, Jay Kesan, Mark Peecher, Ram Ramakrishnan, Jonathan Rogers, and seminar participants at the 2011 American Accounting Association annual meeting, the University of Illinois at Chicago, and the University of Illinois at Urbana-Champaign. We also thank FTI Consulting for providing the data.

Final transcript accepted 4 August 2014 by Tom Smith (AE Finance).

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

1.

Despite focusing on only one type of lawsuit, our sample size was comparable to those of previous empirical studies based on multiple types of lawsuits.

2.

Estimate provided by Jay Kesan at the University of Illinois at Urbana-Champaign Law School.

3.

The US Supreme Court delivered a landmark decision in 1997 on the patent infringement case Markman v. Westview Instruments, Inc. Following this decision, patent claim interpretation is done in a separate hearing outside the presence of the jury.

4.

This data set is not proprietary and can be obtained for academic research, free of charge, from FTI Consulting. We do not have FTI data and lawsuit settlement dates after 2006.

5.

We collected this information through the litigating parties’ SEC filings (10-K and 8-K) and a Lexis-Nexis search.

6.

Uniloc USA Inc. et al. v. Microsoft Corp. et al., 2010-1035 (Fed. Cir. Jan 4, 2011).