Abstract

This article uses a survey of Australian corporate treasurers to shed light on the gap between the theory and practice of corporate finance in Australia. Seven areas are examined: capital structure, payout policy, cash holdings, initial public offerings, seasoned equity offering, mergers and acquisitions, and corporate governance. We also exploit the global financial crisis (GFC) to examine the effect of liquidity shocks on a firm’s capital structure choices. We then compare our Australian survey results with results from a comprehensive US survey conducted by Graham and Harvey. Our survey shows that the board of directors plays the most important role in determining capital structure decisions and that corporate treasurers play the most important role in cash holding decisions. This contrasts with the academic literature that has typically focused on the role of chief executive officer (CEO) in both capital structure and cash holding decisions. In addition, our respondents do not view the tax advantage of interest deductibility to be of first order of importance for debt issuance choices, which contrasts with most of the US empirical studies. Finally, we juxtapose the theory–practice perspective, with a review of the most recent 5 years (2011–2015) of corporate finance research published in the leading Asia Pacific Basin finance journals.

1. Introduction

Our paper answers the recent call from Dempsey (2014),

1

who states,

… rather than continue to build elaborate theoretical models with limited success to explain the actions of financial advisers, finance academics should leave their offices and go and talk with them.

We answer Dempsey’s (2014) call in two steps. In the first step, we design survey questions to elucidate whether corporate treasurers 2 make their decisions according to the main corporate finance theories. In designing our survey, conscious to achieve the best possible response rate, we choose a narrow focus mainly relating to capital structure questions. 3 Our approach is to focus on the factors and considerations that are identified by corporate treasurers themselves. To do this, we ask corporate treasurers who are responsible for the capital structure policies of their firms about the factors that they consider. This approach provides an alternative, important perspective that supplements the empirical and theoretical literatures.

In the second step, we review the past 5 years (2011–2015) of corporate finance research in the Asia Pacific Basin. Specifically, we review seven areas of corporate finance in the four leading Asia Pacific journals, namely Accounting and Finance, Australian Journal of Management, International Review of Finance and the Pacific-Basin Finance Journal. 4 The seven areas are as follows: (a) capital structure, (b) payout policy, (c) cash holdings, (d) initial public offerings (IPOs), (e) seasoned equity offerings (SEOs), (f) mergers and acquisitions, and (g) corporate governance.

Our survey of Australian corporate treasurers contributes to the literature in the following three ways. First, much of the previous research on firms’ capital structure choices takes an analytical approach that is tested empirically. 5 However, the results are often inconclusive due to econometric challenges. We illustrate with two examples here. The first example is in the test of the determinants of capital structure. Welch (2012) is critical of most empirical regression models in the capital structure literature that have never been held to research test standards, such as using quasi-experimental settings to resolve the endogeneity problem (see Gippel et al., 2015). The second example is in the test of the speed of debt adjustment to the target leverage. Flannery and Hankins (2013) show that the presence of lagged dependent variables combined with firm fixed effects in a regression can introduce serious econometric bias. This bias occurs if the dependent variable is clustered or censored, and/or the independent variables are missing, correlated with another variable, or endogenous. Using a survey method, we aim to bridge this gap between theory and practice, as surveys provide an opportunity to ask qualitative questions about what corporate treasurers actually consider when making capital structure choices – questions that an analytical approach and economic modelling cannot readily answer.

Second, the surveys that have been conducted in the field to date focus mainly on the financial behaviour of US firms, with only limited investigation of other countries, and very little consideration of the Australian practice, especially after the most recent global financial crisis (GFC). 6 So far, international surveys do not always find consistency across responses by chief financial officers (CFOs) to capital structure decisions across countries. For example, on one hand, in a European survey study, Brounen et al. (2004) find support for the landmark US survey finding of Graham and Harvey (2001) that most of their CFO respondents identify ‘financial flexibility’ to be the most important factor in determining their debt level. But these results are in direct contrast to those results reported by a UK survey by Beattie et al. (2006), who find that ‘ensuring the long-term survivability of the company’ is the most important determinant of debt level. Beattie et al. (2006) attribute their results to the stricter creditor rights enforced in the UK bankruptcy laws. Therefore, UK CFOs may adopt a more defensive capital structure strategy. These studies highlight that differences in financial market conditions and regulatory environments across countries can play an important role in determining target debt levels.

Financial market settings in Australia are different to those encountered in the aforementioned international survey studies. Australian investors can reduce their personal tax payments via a franking credit that is generated by equity issuance under the Australian tax system (Ainsworth et al., 2015). Franking credit rebates might then reduce firms’ weighted average costs of capital (WACC) through a decrease in costs of equity financing (with part of the return required by equity holders potentially being made up of franking credits provided by the government). 7 A lower cost of equity financing would induce relatively greater reliance on equity in Australia (Pattenden, 2006). This would pose a challenge to the trade-off theory that suggests firms only trade-off interest tax deduction benefits with financial distress costs when making debt borrowing decisions. Our survey is not only able to ask corporate treasurers whether they follow trade-off theory, but also whether (and how) the imputation tax credit system in Australia has affected their debt financing decisions.

Third, this survey is a timely opportunity to ask corporate treasurers how Australian firms finance their capital needs in response to the GFC. 8 Existing capital structure theories are silent as to how the GFC will affect financing decisions. 9 Therefore, there is no doubt that the GFC will challenge academics to refine or modify their existing capital structure theories. For example, during times of crisis, firms will face difficulty in rolling over their shorter-term debt. The survey results will shed some light on how major liquidity shock events (like the GFC) affect Australian corporate treasurers’ financing choices.

Our findings are beneficial for practitioners, as they provide insights on not only how corporate treasurers generally meet their financial needs in response to the GFC, but also how capital structure theories can help them understand drivers of their firm value. For academic researchers, this study highlights the current and future directions of capital structure that academics should focus on. For example, what proxies should we consider using for financial leverage and debt maturity? Which stakeholders are the main drivers of capital structure decisions? For regulators, this study can provide a better understanding of how the Australian financial settings might affect capital structure decisions of Australian firms. Therefore, regulators may be able to improve Australian financial settings to improve firm value. For finance educators, the results of this survey indicate how Australian corporate treasurers perceive existing capital structure theories and what factors directly affect their final decisions.

The remainder of the article is organised as follows. Section 2 describes the design and administration of our survey. Section 3 reconciles or highlights the gap between our survey results with the three main areas of capital structure theories, namely financial leverage, debt maturity, and credit ratings and credit spread. Section 4 reviews several areas of corporate finance research in the leading journals in the Asia Pacific Basin. Section 5 concludes the article with suggestions for future research.

2. Survey design and administration

We designed the survey for this study together with the Finance and Treasury Association (FTA) of Australia. The FTA is a professional association for executives working across all aspects of treasury and financial risk management. 10 We have used a mixture of question forms including yes/no questions, ranking of alternative options, some open-ended questions and mostly closed responses taking on a 5-point Likert scale to facilitate quantitative analysis of the responses. 11

The FTA distributed the online survey link with a cover letter in September 2014 to all of its members across organisations in Australia, representing 754 unique companies including 17 government agencies. The FTA sent a follow-up email to their members in October 2014. In its cover letter, the FTA reminds potential respondents that it seeks one response per corporate, preferably from one of the senior Treasury Professionals within the organisation. We ensure that there are no duplicate responses in our final sample. Our sample consists of 94 respondents, representing a 12.5% response rate. Our response rate is higher than two recent similar surveys conducted in the United States (Graham and Harvey, 2001, 9%) and in Europe (Brounen et al., 2004, 5%). The majority (70%) of respondents were either treasurer or treasury managers, followed by other financial management positions (23%) such as funding analyst or treasury accountant, while a relatively small percentage (7%) identified as the CFO.

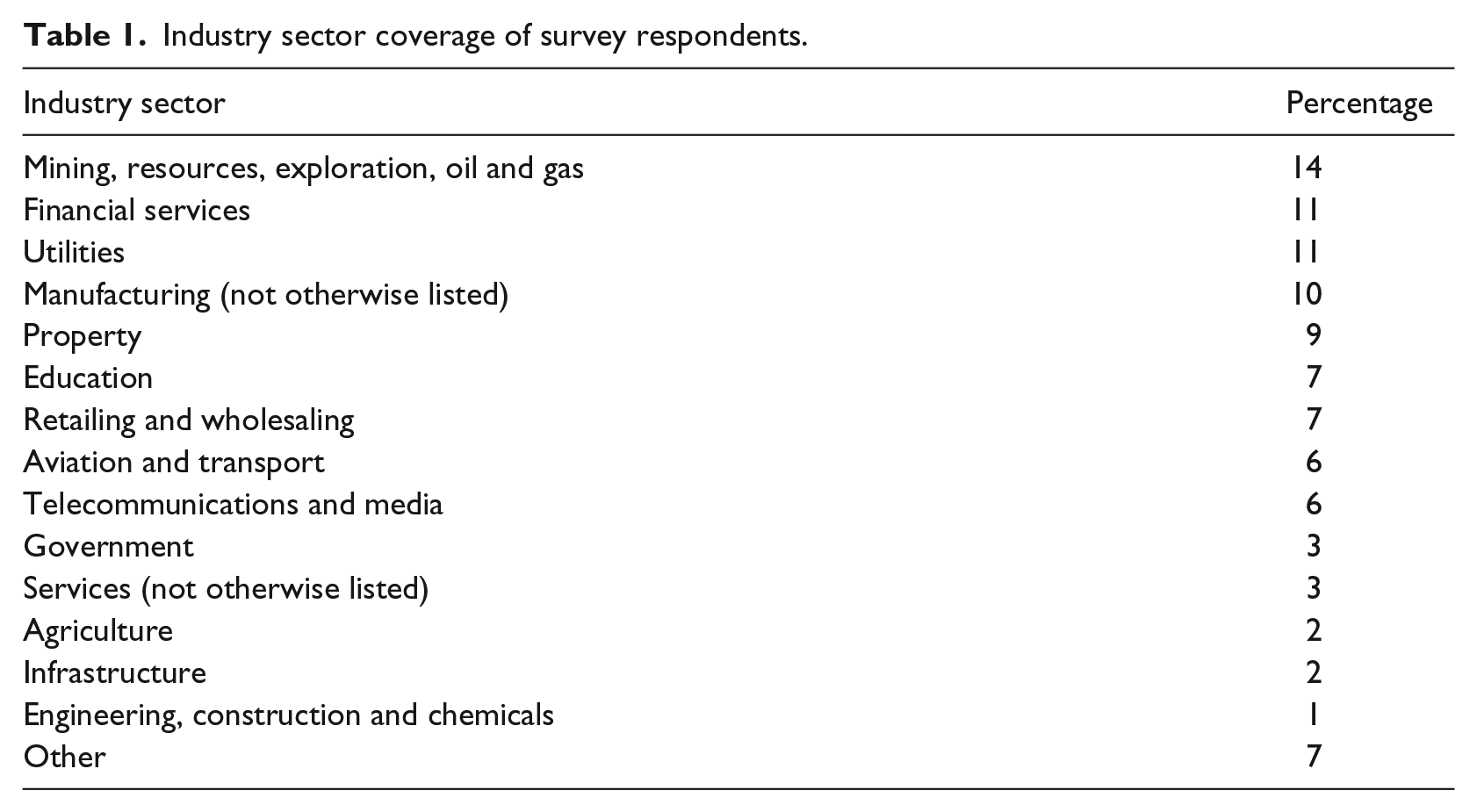

The survey results capture a diverse range of industry sectors, shown in Table 1. Most of the business conducted by the respondent firms takes place in the Asia Pacific region (85%) and 86% of the respondent firms are listed in the Australian Stock Exchange. The size of the companies varies considerably, with 54% generating annual revenue of more than AUD $1 billion and 12% generating annual revenue of less than AUD $50 million.

Industry sector coverage of survey respondents.

3. Survey results

3.1. Financial leverage

3.1.1. Who decides the capital structure for the organisation?

The survey results indicate that the board of directors (92%) plays the most important role in determining capital structure decisions, followed by management (CFO 52%, chief executive officer (CEO) 42% and treasurer 37%). 12 In contrast, much of the capital structure literature focuses more on managerial influences such as compensation packages and managerial entrenchment. For example, Friend and Lang (1988) find that managers with a particular type of compensation package (such as higher equity ownership) are more likely to maintain a lower debt ratio in the firm, as this defensive strategy is likely to reduce their human capital risk exposure. 13 Furthermore, Berger et al. (1997), and Agha (2013) show that entrenched CEOs seek to avoid debt when CEOs are not properly incentivised. Our results are inconsistent with the literature that considers managers aligning capital structure in their own interest.

Second, our survey indicates that labour unions and external parties such as employees, debt holders and bankers play an insignificant role in determining financial leverage decisions. This is in contrast to academic work that considers the relationship between union power and capital structure decisions. For example, Matsa (2010) documents that firms increase financial leverage in response to the increase in power of labour unions, whereas Woods et al. (2015) find that stronger labour union power leads to the firm being able to sustain relatively less external debt.

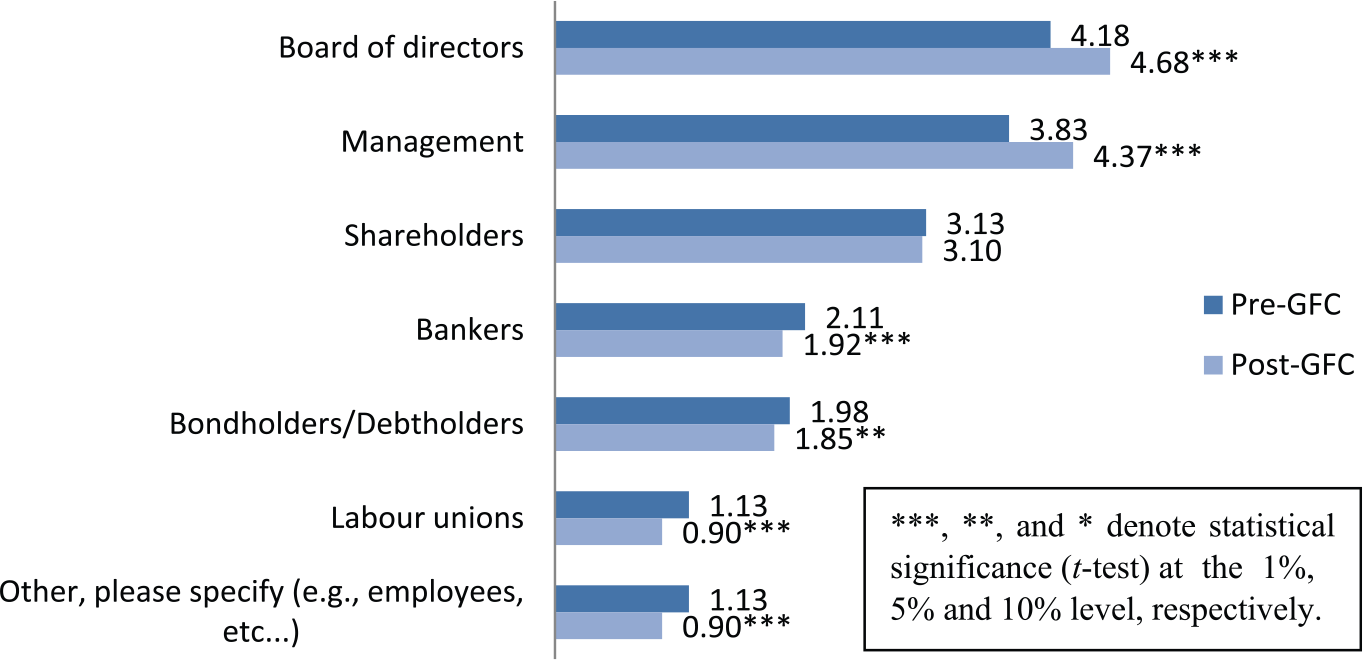

We further explore whether the GFC has changed the relative importance of stakeholder groups when determining the firm’s capital structure. 14 The results are illustrated in Figure 1. We also test whether each group is statistically more important or less important after the GFC using a t-test.

Importance of decision-makers in determining firm’s capital structure decisions (1 = less important, 5 = very important).

Figure 1 shows that groups (such as the board of directors and management) with an important influence on capital structure decisions prior to the GFC have even greater influence after the GFC, at the 1% significance level. In contrast, those external parties (labour unions, bondholders and bankers) with a less important influence on capital structure decisions have an even lower influence after the GFC. Interestingly, the GFC seems to have resonated the pre-GFC results further, in the sense that stakeholder groups that were reasonably important pre-GFC have become even more important post-GFC.

Also, respondents indicate that they do not often engage with external parties to determine desired leverage; 39% do not seek external advice at all, 54% have some engagement with external advisors and only 7% of respondents engage extensively with external parties. Those who do seek advice from external parties mainly engage with key investors and lenders (77%), market analysts (40%) and less often with regulators (17%) or other parties (14%).

3.1.2. How to measure financial leverage in practice?

About half (52%) of respondents indicate that their organisation measures their target leverage rate as debt/(debt + equity). This is consistent with Welch’s (2011) advice to avoid using debt/assets as a proxy for financial leverage, as assets include non-financial interest-bearing liabilities that should not be considered as either debt or equity.

To measure equity, book value of equity is used more frequently, by 71% of respondents, than is the market value of equity (29%). This result informs future empirical research to focus more on the book value of financial leverage rather than the market value of financial leverage in Australia.

3.1.3. Do firms target financial leverage or interest coverage ratio?

There has been a long debate in the literature as to whether there is conclusive evidence in supporting one of the following two competing capital structure theories: (a) static trade-off theory and (b) pecking order theory. The main difference from static trade-off theory is that there is no optimal corporate debt ratio for firms under pecking order theory.

The static trade-off theory explains that when determining an optimum debt level, firms need to trade-off the tax deductibility of debt (marginal debt benefit) with bankruptcy costs of debt (marginal debt costs) for the following two reasons. First, Modigliani and Miller (1963) show that firm value increases proportionally with the level of debt borrowing due to the interest tax deductibility savings on their debt borrowing. Second, however, high leverage will also be more likely to attract a higher probability of bankruptcy. Therefore, the static trade-off theory will prescribe an optimal level of target leverage.

In contrast to the static trade-off theory, the pecking order theory proposes that financial leverage is path dependent rather than having an optimal target. Specifically, the pecking order theory proposes that firms prefer internal financing to external financing and prefer debt to equity if the firm issues securities due to different transaction costs driven by asymmetric information between insiders and outsiders (Myers and Majluf, 1984).

Chang and Dasgupta (2009) conclude that a number of existing econometric tests of target behaviour have no power to distinguish between the two competing theories. Since then, Chang and Dasgupta (2011) and Elsas and Florysiak (2011) make some improvements in this line of research using Monte Carlo simulations and dynamic panel fractional (DPF) dependent variable estimator. However, we turn to survey research which is a more direct approach by asking the capital structure decision-makers.

Our respondents indicate that their target ranges for debt ratios are usually somewhat tight (55%), sometimes flexible (33%), but seldom strict (13%). The target gearing ratio is almost symmetrically distributed among organisations. For example, 74% of organisations aimed their gearing ratio between 21% and 40% or 41% and 60% (42% and 32%, respectively). Only 13% had a target of <20% and 13% had a target of >60%. Therefore, our survey results are more consistent with the trade-off theory, rather than the pecking order theory. Our survey results are also consistent with the most recent empirical study by Khoo et al. (2015) who find Australian firms do have specific leverage targets.

Our survey also asks whether firms have a target interest coverage ratio. Exactly half of respondents have a target minimum interest coverage ratio in place. Those respondents with this target in place, generally perceive it as important (average of 4.24 out of 5, 5 = most important) and use earnings before interest, tax, depreciation and amortization (EBITDA) to measure it (62%). For 74% of respondents, the target lies between 1.0 and 3.0.

3.1.4. What are the determinants of financial leverage prior to or after the GFC?

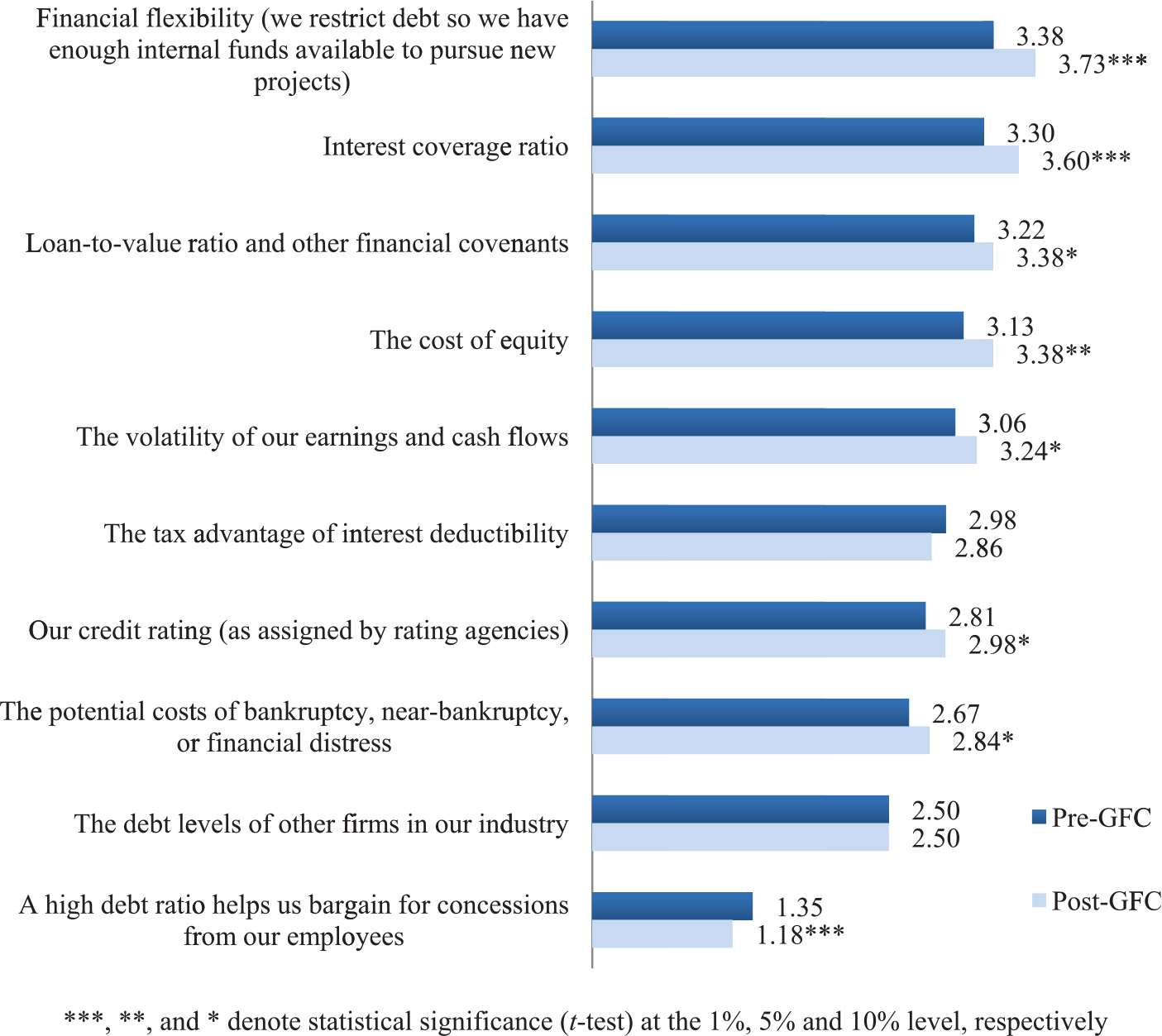

Setting the appropriate level of debt is complex and usually depends on several factors. Figure 2 presents the results for the determinants of financial leverage prior to or after the GFC. Maintaining financial flexibility (using internal funds first) is consistently ranked as the most important determinant of financial leverage in Australia prior to and after the GFC, suggesting that Australian firms follow the pecking order theory. Our survey results present an interesting practical backdrop to the mixed empirical results 15 for the pecking order theory in Australia.

Factors affecting the level of debt (1 = less important, 5 = very important).

In Figure 2, respondents generally indicate that before the GFC, ‘internal’ factors such as financial flexibility, interest coverage ratio and loan-to-value ratio are regarded as more important than ‘external’ factors (e.g. credit ratings, potential costs of bankruptcy and debt levels of other firms in their industry.) Unsurprisingly, these external factors have become more important after the GFC, because the GFC would have significantly changed the external market conditions.

One possible reason for these internal determinants of financial leverage to be so important prior to the GFC is because such factors are frequently included in borrowing agreements. For example, our survey results show that (a) debt service or coverage ratio (47%), (b) times interest earned (43%) and (c) debt-to-equity ratio (38%) are all the basis of financial covenants that are regularly included in the treasurers’ borrowing agreements (respondents are allowed to select more than one). Our survey results also lend support to Cotter’s (1998) finding that most Australian firms attach debt covenants to their debt issues. Only 16% of the survey respondents indicate that they had no covenants. Other less common debt covenants (31%) were also mentioned, such as loan-to-value ratio, debt-to-asset ratio and letter of comfort.

Interestingly, Figure 2 also shows that our respondents do not view the tax advantage of interest deductibility to be first order of importance as suggested by the most recent US empirical study by Heider and Ljungqvist (2015). However, this is consistent with our expectation that there might be a lower cost of equity financing in Australia (Melia et al., 2015). That is because Australian investors can reduce their personal tax payments on dividends via franking credit that is generated by equity issuance under the Australian imputation tax credit system.

Furthermore, our respondents indicate that ‘the debt levels of other firms in our industry’ are relatively unimportant in the Australian market. These results are in contrast to the US empirical studies, such as Zhang (2012), which consistently find support for the role of industry leverage in determining an individual firm’s leverage. Our respondents also indicate that setting capital structure is often dependent on multiple criteria, such as funding costs (80%), funding source access (78%), risk appetite (57%) and credit rating objectives (43%) (Figure 3).

Other factors also affecting the level of debt.

3.1.5. How is debt structured and sourced? 16

In contrast to Cotter’s (1999) finding that Australian firms heavily rely on bank debt, our survey shows that most treasurers actually diversify their debt structure (although bank debt is still the main component of the debt portfolio). Only 36% use solely bank debt for debt funding. In addition, the majority (83%) of respondents who use sources other than bank debt, do so for >50% of total debt funding. Sources being used include bank debt (80%), bonds (46%) and other debt (30%) including government debt, term loans and trade finance.

Moreover, only 34% of firms exclusively use domestic sources for raising their debt. Respondents also indicate that the main reason for offshore funding is for diversification purposes (71%), followed by less important reasons such as lack of domestic funding capacity (41%), other factors (mainly price and tenor) (32%), asset matching (17%) and revenue matching (17%).

Overall, our results indicate that most Australian treasurers diversify both in terms of type and regional sources of debt. These findings differ from those in the US study by Graham and Harvey (2001) in two main ways. First, in our study, 66% of respondents use foreign debt, whereas Graham and Harvey’s survey indicates only 31% seriously consider issuing foreign debt. This difference could be due to the traditionally smaller debt market in Australia compared to the United States (Alcock et al., 2012). Second, in contrast to our results, Graham and Harvey (2001) find that the most popular reason for using foreign debt is providing a natural hedge 17 for foreign revenues, followed by keeping the source of the funds close to the use of the funds, and tax incentives.

3.2. Debt maturity

3.2.1. What is the weighted average debt maturity and how is maturity measured?

Most respondents (60%) indicate a current weighted average maturity of their debt portfolio of 3–5 years, followed by 0–2 years (23%), 6–8 years (12%) and > 9 years (5%). However, the number of years of borrowing is a less common measure of debt maturity compared to duration (52%), and then debt maturing in more than 1 year (45%). Notably, debt maturity in more than 1 year is commonly available from annual reports and can be easily ascertained. This is the reason why this measure has been used in the most recent Australian debt maturity study by Tan (2011).

3.2.2. Do firms have a target debt maturity?

Most Australian company treasurers (64%) have a target range for the average maturity of debt. Specifically, 16% have a strict target maturity range, 18% have a slightly strict target and 39% have a flexible target range.

3.2.3. What are the determinants of debt maturity prior to or after the GFC?

We ask treasurers which factors were important in debt funding decisions pre-GFC, and whether these factors have become more or less important after the GFC. The results are presented in Figure 4. The two most important factors pre-GFC were as follows: (a) Myers’ (1977) maturity matching between debt and asset life (consistent with empirical findings of Graham and Harvey (2001)) and (b) issuing long-term debt as a risk-mitigation tool for ‘bad times’.

Consideration factors short-term versus long-term debt, for Pre-GFC (1 = less important, 5 = very important).

In contrast, the least important factor is taking on short-term debt to reduce risk taking as predicted by Myers (1977), indicating that the term of debt is not often used as a control mechanism for the overinvestment problem. Moreover, Flannery (1986) and Kale and Noe (1990) predict that if firms expect their credit rating to improve, they prefer to issue short-term debt to capture a lower interest rate in the future. Our survey finds limited evidence for Flannery’s (1986) theory, which is similar to the findings of Graham and Harvey (2001). Interestingly, the GFC seems to have functioned as an amplifier in the sense that factors that are important pre-GFC have now become even more important.

With regard to the question whether the GFC has changed the importance of factors affecting debt maturity decisions, one notable result is that firms choose to issue longer-term debt to minimise the risk of having to refinance in ‘bad times’. This reaction to the GFC event is consistent with our expectation that the financial crisis reduces the liquidity of funding in the market.

3.3. Credit ratings and credit spread

Alali et al. (2012) find that US firms with good corporate governance have a significantly higher credit rating. However, Aldamen and Duncan (2012) find that having good corporate governance only reduces the cost of debt for non-intermediated debt but not for intermediated or private debt, as private lenders already have greater access to private information.

3.3.1. Credit ratings agencies and current credit ratings

Among those respondents who have a credit rating (42%), S&P and Moody’s agency ratings are most popular. Often both agencies are used; S&P is used by 89% of rated respondents compared to 70% using Moody’s, while Fitch is used by only 15%. In terms of credit ratings, respondents of the survey generally have upper or medium investment-grade debt for long-term debt.

3.3.2. Do firms have target credit ratings?

Our survey results indicate that most respondent firms do not have a target rating. Only 35% of respondents indicate that they have a target credit rating in place. Of these firms, 45% indicated that this target credit rating is very important. Our survey results are inconsistent with the indirect results from two empirical studies relating to credit ratings. For example, Dang and Partington (2014) find that the historical credit rating plays a more important role in predicting the next rating change than current rating, and Wang et al. (2014) find that the movement in credit rating events contains value-relevant information in Australia. Both of these findings suggest that firm credit ratings are important.

Respondents were also asked to identify their current target credit rating and the results are reported in Figure 5. It can be highlighted that:

14% of respondents have a target rating of A−/A3;

41% of respondents have a target credit rating of BBB+/Baa1;

23% of respondents have a target credit rating of BBB/Baa2;

Overall, 69% of the respondents have a target of investment credit rating (BBB+/Baa1 and above).

Target credit rating.

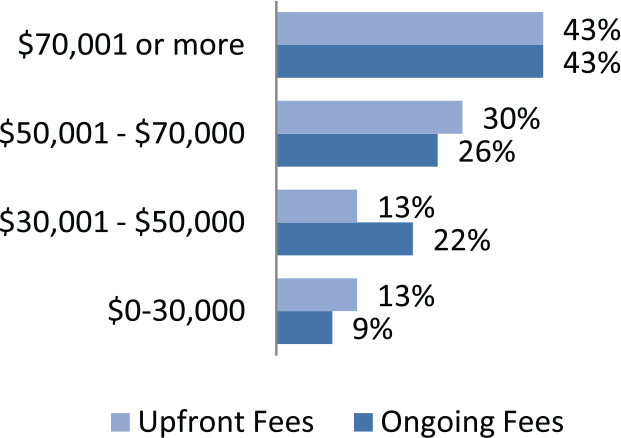

3.3.3. Fees for credit ratings

The upfront and on-going fees are displayed in Figure 6. Most respondents pay over AUD$70,000 for both upfront and on-going fees.

Credit rating fees.

3.3.4. Credit spread of debt

Figure 7 shows the credit spread of debt over the benchmark rate for our respondents. Our results show that surveyed firms display a relatively wide cross-section spread of debt over the benchmark rate, ranging from 0 to >201 bps. However, most firms have an average spread of 101–150 bps.

Spread of debt over benchmark rate.

In the last few years, researchers have found new determinants of the cost of debt. For example, the cost of bank loans can be reduced if (a) the loans are made by more competitive and skilled banks (Ongena and Roscovan, 2013); (b) the likelihood of earnings management on credit ratings is low (Shen and Huang, 2013); (c) the firm has higher bond liquidity (Darwin et al., 2012) and (d) the firm has higher discretionary accruals (Aldamen and Duncan, 2013). 18

4. Review of six areas of corporate finance research

After comparing our main capital structure survey results with academic theories and empirical evidence, we now consider how our other survey results correspond to the literature in leading Asia Pacific journals.

4.1. Payout policy

In terms of the corporate payout policy, firms can either pay dividends or repurchase shares. If there is no obvious tax advantage to either strategy, then share repurchases can be a substitute for dividends, and this dividend substitution effect has been supported in many countries. However, the dividend substitution effect is not supported in Australian off-market repurchases. These results are unsurprising because Australian off-market repurchases offer more tax advantages to investors who receive franking credits (Au Yong et al., 2014; Brown et al., 2015). 19

The following survey results show that Australian firms have more incentive to use dividends to manage their capital, consistent with the empirical findings by Melia et al. (2015). 20 For example, respondents who are responsible for capital management (62%) mainly use dividends as a tool to manage capital (85%). Dividend reinvestment (55%), debt buybacks (55%) and share buybacks (45%) are also used as tools to manage capital. The most commonly used criteria in assessing which approach will be used to manage capital by our respondents are liquidity constraints (82%), market conditions (68%) and corporate tax consequences (59%).

4.2. Cash holdings, financially constraint and liquidity

Our survey results indicate that the management of liquidity and funding risk has maintained its status as the most important risk management function, being a key function for 98% of respondents. Our results also show that a vast majority of organisations have a formal liquidity policy in place (77%). These formal liquidity policies include counterparty limits (73%), maturity limits (58%) and minimum liquidity reserves (71%). In total, 85% of respondents indicated that they review and update these liquidity policies annually. Our survey results suggest that liquidity management plays a big role in corporate finance.

For the academic literature in the areas of cash, financial constraints and liquidity management, there are three main research questions. First, what are the determinants of cash holdings? Second, what is the value of excess cash holdings? Third, what is the interpretation of the investment-cash flow sensitivity? 21 However, the first question has received relatively less attention in recent years. For example, Steijvers and Niskanen (2013) show that descendant CEOs have greater incentive to hold cash, because they face higher external financing costs than founder CEOs.

To answer the second question, two recent Australian studies focus on the determinants of marginal cash holdings. First, Lee and Powell (2011) show that Australian equity holders place less value on firms that hold excess cash for long-term rather than short-term periods. This is because long-term excess cash holdings are more likely to be associated with agency costs rather than precautionary purposes. 22 Second, Chan et al. (2013) partition firms into financially constrained and non-financially constrained firms, and find that equity holders place more value on financially constrained firms.

The third question mainly focuses on the controversial interpretation of the investment-cash flow sensitivity in the literature. On one hand, Fazzari et al. (1988) argue that we can interpret a firm’s investment-cash flow sensitivity as its financial constraint problems. This is because the investment made by a more financially constrained firm would be more sensitive to the next available unit of cash. The interpretation of Fazzari et al. (1988) has been challenged by Kaplan and Zingales (1997, 2000). Kaplan and Zingales (2000) conjecture that the sensitivities are at least partially caused by excessive managerial conservatism, that is, managers who are reluctant to rely on external financing will amplify the investment-cash flow sensitivity.

Both interpretations have been applied in two recent studies. First, Tam (2014) finds a lower investment-cash flow sensitivity for subsidiaries of listed parents. Tam (2014) interprets his results, in the spirit of Fazzari et al. (1988), as the parent’s listing status helping to mitigate the subsidiary’s financial constraint. 23 Han and Pan (2015) show a higher investment-cash flow sensitivity for CEOs with higher inside debt holdings. They interpret their results, in the spirit of Kaplan and Zingales (2000), as CEOs with higher inside debt holding acting in a risk-averse manner by avoiding external financing, hence amplifying the investment-cash sensitivity. 24

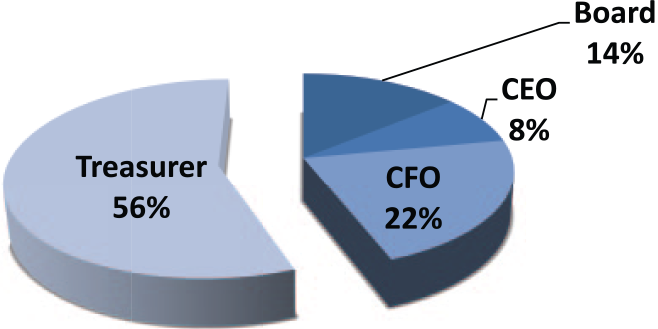

4.2.1. Who decides the cash holdings for the organisation?

Our survey asked respondents to categorise different decision-makers according to their importance in determining the organisation’s cash holding level (Figure 8). In all, 56% of respondents indicated that the treasurer is very important in determining the organisation’s cash holding level, followed by the CFO (22%). Alternatively, 14% of respondents identified the CEO as less important in determining cash level. By contrast, much of the cash holding literature focuses more on how cash holdings are influenced by the CEO’s compensation package including the CEO’s inside debt holdings (Han and Pan, 2015) and the CEO’s options holdings (Liu and Mauer, 2011).

Importance of decision-makers in determining cash holding level.

In unreported results, the data indicated that the percentage of respondents who classified the board’s role in determining cash holding level as ‘less important’ was equal to the percentage classifying the board’s role as ‘very important’. Comparing these results, it can be inferred that the board’s role in this regard is perhaps more idiosyncratic than other decision-makers, having various degrees of control depending on the particular organisation and that organisation’s respective policies.

4.3. IPOs

Prior to an IPO, private firms should have the incentive to increase their offer price to maximise the IPO proceeds. For example, Liu et al. (2014a) show that issuing firms have a strong incentive to manage their IPO earnings to obtain a higher offer price before the abolition of the fixed-price offering system in China. This is because, under the fixed-price offering system, the offering price is determined by the product of the firm’s earnings and a regulated price-to-earnings ratio. However, underpricing, defined as the difference between offer price and the first day trading price, is a common phenomenon around the world. This naturally prompts researchers to investigate the reasons for IPO underpricing.

So far, the most plausible explanation given by the Asia Pacific Journals is asymmetric information between issuing firms, underwriter/investment banks and new investors. To entice new investors to reveal their true price, O’ Connor Keefe (2014) shows that underwriters do not fully impound all elicited ‘positive’ information from investors on offer price; thus, the offer price is under-priced. This effect is more pronounced when there is a hot IPO market in which investors are more challenged to differentiate bad quality firms from good quality firms.

To mitigate IPO underpricing from information asymmetry, there are at least three possible strategies IPO firms can follow. First, IPO firms can get venture capitalists involved in their IPOs, because venture capitalists are experts who help certify the R&D information reported in the IPO prospectus (Cho and Lee, 2013). Second, similarly, firms should disclose having a relationship (if any) with high credit quality banks, which may help certify the financial health of the IPO firms (Hao et al., 2014). Third, firms should go public in jurisdictions where legal protection is stronger, because strong legal protection can alleviate information asymmetry (such as property rights protection), hence reducing underpricing (Liu et al., 2014b).

However, disclosing more information does not necessarily reduce IPO underpricing, as the type of information matters. For example, the market penalises those IPO firms that report the use of proceeds for growth activities, because growth activities are associated with greater uncertainty (Wyatt, 2014).

4.4. SEOs

Similar to the above-mentioned IPO literature, when firms issue seasoned equity, the SEOs tend to be under-priced. Recent SEO studies in the Asia Pacific Journals focus on how to reduce underpricing in the following three ways in China. First, Chinese firms with a credit rating (regardless of investment vs non-investment grade) benefit from less underpricing (Poon et al., 2013). Second, SEO firms with large governmental block holding are less likely to be under-priced because they enjoy an implicit loan guarantee (Chen, 2015; Cheung et al., 2012). Third, SEO firms that issue SEOs with warrants (vs cash) enjoy a positive return in the short-run (Bae et al., 2013). This is because underwriters will only enter into an agreement to buy back at a predetermined price that is lower than future stock price; hence, there is a certification effect. However, this certification effect does not materialise into a higher long-run stock return.

4.5. Mergers and acquisitions

The main discussion on mergers and acquisitions has been around the following question: Do diversified firms enjoy a diversification premium or suffer a value discount? Two relevant Australian studies provide conflicting results. 25 On one hand, Fleming et al. (2003) find that diversified firms suffer a diversification discount between 1988 and 1998. On the other hand, Choe et al. (2014) show that Australian diversified firms enjoy a diversification premium (2004–2008).

It would be interesting for future research to use the five measures of diversification in Choe et al. (2014) to re-examine the findings by Fleming et al. (2003). Furthermore, future research can examine whether the following two channels in other countries can explain the diversification premium found in Australia: (a) through lower probability of default for the smallest and least focused firms in the United States (Grass, 2012) and (b) through adopting good corporate governance policies in New Zealand and the United States (Al-Maskati et al., 2015; Starks and Wei, 2013).

4.6. Corporate governance

In the area of corporate governance, most recent studies focus on when the corporate directors add or destroy firm value. 26 For example, directors can create higher firm value in the following situations: (a) when directors have more prior director experience (Gray and Nowland, 2013); (b) if director expertise is business related, such as lawyers, accountants, consultants, bankers and outside CEOs (Gray and Nowland, 2015); (c) when female directors moderate excessive firm risk (Hutchinson et al., 2015); (d) when firms have high advising needs and external financing needs (Lee and Lee, 2014) and (e) when directors curb excessive managerial compensation at low levels of managerial ownership (Cheng et al., 2012).

In contrast, directors have also been found to destroy firm value. For example, Griffin et al. (2014) and Zhu and Gippel (2015) find that directors (and other insiders) profit from their trades on their private information about debt covenant violations. 27 Therefore, it would be interesting for future research to find the net impact of corporate directors on firm value.

5. Conclusion and future directions

This article reviews the most recent 5 years (2011–2015) of corporate finance research published in the four leading Asia Pacific Basin Journals, namely Accounting and Finance, Australian Journal of Management, International Review of Finance and the Pacific-Basic Finance Journal. 28 The key focus is on capital structure research in Section 5.1. The other six aspects presented in Section 5.2 are as follows: payout policy, cash holdings, IPOs, SEOs, mergers and acquisitions, and corporate governance.

5.1. Conclusion and future directions for capital structure research

This article further explores the differences in capital structure theory and practice, the effect of the GFC on capital structure decisions and the evaluation of Australian corporate treasurers’ practices compared to international survey results. As such, this article serves as a bridge between academic theories and practice in Australia. Our survey also reshapes and perhaps challenges researchers’ thinking with regard to how Australian firms design their future corporate financing issues in the following six ways.

First, academic literature has relied on the assumption that CEOs are the most important decision-makers in capital structure and cash holding decisions. However, our survey results challenge this assumption. We show that the board of directors (treasurers/CFOs) plays the most important role in determining capital structure decisions (cash holding decisions). Therefore, we encourage future empirical research that examines (a) board-related issues with capital structure decisions and (b) treasurer/CFO-related issues with cash holding decisions.

Second, most Australian firms have a target financial leverage and interest coverage ratio. The most important determinants of financial leverage for Australian firms are financial flexibility and interest coverage ratios, which are required to be maintained by their borrowing agreements. However, tax deductibility of interest expense is not of first order of importance in Australia. The likely explanation is that the rebates of franking credits (tax deductibility of dividends) are likely to reduce the tax benefits of issuing debt, so there is not much benefit in issuing debt over equity. We encourage future research to design a direct test to examine the franking credits explanation in Australia.

Third, most respondents indicate that they diversify their debt sources across debt instruments and borders for diversification purposes. With the availability of debt structure data in the Capital IQ database over recent years, we encourage more future research to investigate the diversity of debt structure, rather than debt–equity choices.

Fourth, most Australian firms have a weighted average maturity of 3–5 years and pursue a target debt maturity range. The most important determinant of debt maturity is consistent with the most commonly prescribed debt maturity theory, that is, the matching principle, which matches the maturity of debt to the maturity of assets. However, after the GFC, firms responded by borrowing longer-term debt to minimise the risk of having to refinance in ‘bad times’. Therefore, it would be interesting for future researchers to find out (a) how should the bond market respond to this high demand of long-term debt? and (b) whether more long-term debt (i.e. frequently associated with less frequent monitoring) will destroy firm value.

Fifth, a majority (two-thirds) of the survey respondents do not have a target credit rating, which is thereby inconsistent with the indirect empirical results showing firms have target credit ratings. We urge future research in this area to address this puzzle.

Sixth, most studies conducted in capital structure assume that managers are fully ‘rational’ and objective but the recent ‘behavioural’ literature shows that managers are more likely to be overconfident (Huang et al., 2016). However, their sample only covers the industrials. Therefore, it would be interesting for future research to investigate how overconfident managers would make their corporate financing decisions, especially with respect to Real Estate Investment Trusts. 29

5.2. Other areas of corporate finance and future directions

Other key aspects of corporate finance research published in four leading Asia Pacific journals between 2011 and 2015 are presented below. In terms of payout policy, our survey results indicate that firms mainly use dividends to manage their capital. However, the most recent empirical results show that Australian firms use off-market repurchase offers rather than paying more dividends. It would be fruitful for future research to reconcile the conflicting survey results with empirical results.

In terms of the cash holding literature, there have been debates on whether investment-cash flow sensitivity should be interpreted as financial constraints or managerial conservatism. More importantly, we show that the most recent two studies published in Asia Pacific journals still arbitrarily use each of these two interpretations. Maybe, instead of debating the interpretation of investment-cash flow sensitivity, it might be more fruitful for future research to find out what really determines a firm’s investment-cash flow sensitivity.

In the literature of both IPOs and SEOs, most papers published in Asia Pacific Journals show that there is underpricing. These papers also propose some mechanisms to reduce underpricing. For example, IPO papers propose certification by venture capitalists and banks to reduce underpricing. SEO papers propose that SEO firms should have a credit rating, a higher government holding or a warrant compensation offer. However, the proposed SEO mechanisms in these papers have only been examined in China. It would be interesting to ask whether our Australian managers follow these prescribed strategies (or other strategies), and why.

In the mergers and acquisitions literature, there has been mixed evidence in diversification premium or discount in Australia. We urge new research to further explore the reasons or channels in which the diversification premium or discount arises.

Finally, in the corporate governance literature, corporate directors have been found to enhance and destroy firm value. It would be interesting for researchers to devise quasi-natural experiments built on exogenous events, such as the sudden death of directors, to determine the net impact of corporate directors on firm value.

Footnotes

Appendix 1

Acknowledgements

The authors would like to thank the members of the Finance and Treasury Association (FTA) of Australia for completing the survey. Especially, the authors gratefully acknowledge the contribution of the FTA’s CEO (David Michell), FTA’s National Technical Committee (Fulvio Barbuio and Joanna Wakefield) in providing their valuable comments on our survey questionnaire and early drafts of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Final transcript accepted 18 January 2016 by Kathleen Walsh (AE Finance).