Abstract

In this article, we meta-analyse 69 empirical studies assessing the association between corporate voluntary disclosure and ownership concentration and types, and how institutional characteristics and research design moderate these relationships. Our overall analyses show that state, foreign and institutional ownerships have a positive effect but managerial ownership and ownership concentration have a negative effect on voluntary disclosure. Since the overall effect may conceal the underlying factors that cause heterogeneity in the effect size distribution, we select two important institutional factors: country-level investor protection and the equity market development, and research design and journal quality, to explain the mixed and conflicting findings. Our results emphasise the need to consider legal and institutional characteristics, and researcher induced-artefacts, in understanding the role of ownership structure and identity in corporate voluntary disclosure.

1. Introduction

Corporate voluntary disclosure is an important means for management to communicate firm performance and governance to outsider stakeholders and has remained an important field of empirical and theoretical studies since the 1970s. According to the Financial Accounting Standards Board (FASB, 2001), the term voluntary disclosure describes disclosures, primarily outside the financial statements, that are not explicitly required by generally accepted accounting principles (GAAP) or specific country rules (García-Meca and Sánchez-Ballesta, 2010). When a firm makes the decision to disclose information voluntarily, it assumes that benefits will outweigh costs. Such benefits may come in the form of reduced cost of financing investment opportunities (e.g. cost of equity), lower transactions costs for investors by reducing information asymmetry between the contracting parties and more efficient functioning of capital markets (Healy and Palepu, 2001; Leuz and Verrecchia, 2000).

The literature on voluntary corporate disclosure over the last 40 years has predominantly focused on examining how firms’ specific characteristics are associated with the extent of corporate voluntary disclosures. 1 In recent years, corporate voluntary disclosure studies have shifted towards understanding the role of governance structure in voluntary disclosure primarily using contracting costs and signalling theories (García-Meca and Sánchez-Ballesta, 2010). It has been argued that superior governance structure ensures better monitoring of managers, reduces agency conflicts between contracting parties and improves financial reporting transparency (Fama and Jensen, 1983; Jensen and Meckling, 1976; Watts and Zimmerman, 1990). Other researchers have employed legitimacy theory, political economy theory, stakeholder theory and proprietary cost theory to explain why firms disclose certain types of information voluntarily (Birt et al., 2006; Henderson et al., 2004).

Corporate ownership structure, as part of the governance mechanism, has received increasing attention in recent years (Connelly et al., 2010; Hope, 2013). Ang et al. (2000) and Armstrong et al. (2010) highlight the agency conflicts existing between different groups of equity ownership and their impact on the demand for accounting information. They suggest that the expected relations between the demand for quality accounting information and ownership structure are driven primarily by economic incentives, and that such demand varies cross-sectionally with ownership structure. This finding is due to the emerging insight that different categories of owners may have different preferences and priorities with respect to corporate risk, stability, growth and performance (Douma et al., 2006; Gedajlovic et al., 2005).

Most prior studies document a positive relation between higher quality governance mechanisms and voluntary disclosure (e.g. Ajinkya et al., 2005; Karamanou and Vafeas, 2005; Laksmana, 2008), but with regard to the effect of ownership structure on voluntary disclosure, the empirical results are mixed and, in some cases, conflicting (Arcay and Vazquez, 2005; Armstrong et al. 2010; Brown et al., 2011; García-Meca and Sánchez-Ballesta, 2010; Luo et al., 2006). In their reviews, Artiach and Clarkson (2011) and Brown et al. (2011) attribute the mixed evidence across studies to the variations in the number of disclosure items, the mode and nature of disclosure (e.g. from total voluntary disclosures, to specific issues such as earnings forecasts and corporate social and environmental information), the type of disclosure required by owners and the research setting being examined. The conflicting results could also be due to treating ownership as a homogeneous group by ignoring the identity of the owners, who have different motivations affecting corporate decision-making (Hautz et al., 2013; Heugens et al., 2009).

In recent years, there have been calls for better understanding of the important role of corporate ownership structure, given its strong influence on governance and monitoring globally (Judge, 2011, 2012). In the accounting discipline, García-Meca and Sánchez-Ballesta (2010: 622) undertook a review of 19 studies that examined the relationship between corporate voluntary disclosure and ownership concentration and found a negative association between the two variables. 2 However, although they did not consider other types of ownership structure, they suggested that further research into other forms of ownership would be very desirable to provide more insights into the ownership and voluntary disclosure relationship.

Following the suggestions outlined above from the literature, in this article, we address this gap in the literature by presenting a review of studies that have examined the relation between corporate ownership concentration and types (namely, institutional, foreign, state and managerial ownerships) and voluntary disclosure and assess the underlying factors that give rise to such divergence in results. We do this by employing meta-analysis techniques, because such procedures are effective ways of drawing valid inferences from a diverse evidence base that has produced mixed findings, since narrative reviews may not capture the underlying reasons for differences in results (Stanley and Doucouliagos, 2012). In particular, we assess the role of institutional characteristics, such as country-specific investor protection levels and capital market development, in the relationship between ownership types and voluntary disclosure. Prior studies suggest that legal and institutional attributes affect financial reporting behaviour (e.g. Bushman and Piotroski, 2006; La Porta et al., 2000; Leuz et al., 2003). To control for the simultaneous effect of investor protection and market development, along with other moderating variables, namely, journal quality, index construction and substantial/family ownership (FO), we employed a more advanced multivariate meta-regression methodology (meta-analytic regression analysis (MARA)), which has not been utilised in prior meta-analysis papers in accounting.

Based on 69 studies, our analyses show that voluntary disclosure, on average, is lower in countries with more concentrated ownership, which is consistent with Leuz et al. (2003) and García-Meca and Sánchez-Ballesta (2010). However, this negative relationship between ownership concentration and voluntary disclosure is not affected by the level of investor protection and other moderating factors, but it is greater in countries with lower capital market development. These results suggest that concentrated owners are in a more entrenched position to expropriate minority shareholders in countries where the equity market is not well developed. Regarding ownership types, we find that institutional owners have a beneficial effect on the extent of voluntary disclosure, as is evident from a significant positive association between the two constructs. The positive effect is more evident in countries where the level of investor protection is low and the capital market is less developed, suggesting that institutional investors demand more public information from firms operating in low investor protection and low capital market development countries, and thus play an effective monitoring role. We also find foreign investors and state ownership are positively associated, but managerial ownership is negatively associated, with voluntary disclosure.

Our study contributes to the debate on the relationship between voluntary disclosure and ownership attributes by offering a quantitative generalisation drawn from a large sample of empirical studies dealing with this topic. We provide evidence that ownership type is not homogeneous, due to different investment objectives and horizons, and as a result, such relationships between voluntary disclosure and ownership structure are affected, both in direction and strength. It is, therefore, important for investors and policymakers to understand the role of ownership identity as a monitoring mechanism in corporate voluntary disclosure policy, rather than focusing on ownership concentration only. Our study also shows that jurisdictional differences (particularly, investor protection level and equity market development), research design and construct measurement are important factors to consider. The in-depth analyses of a large number of studies facilitate theory development and provide guidance to future researchers in conducting empirical studies on this issue.

The remainder of the article is organised as follows: the next section develops the hypotheses. Section 3 explains the research methods employed in this study, including the procedures adopted in collecting the data and their main characteristics. Section 4 presents the results and Section 5 concludes the article.

2. Hypotheses development

Owners differ in terms of power, wealth, competence and non-ownership ties to the firm. These differences affect their objectives and the way they exercise their ownership rights and, therefore, have important consequences for management behaviour with respect to corporate reporting policy (Connelly et al., 2010; Pedersen and Thomsen, 2003). This section reviews the theoretical foundations for the association between ownership concentration and four ownership types (institutional, foreign, state and managerial ownerships) and voluntary disclosure.

2.1. Ownership concentration

Theoretical justifications for information disclosure and ownership concentration derive from two perspectives. Morck (2000), using agency theory, argues that when a firm has widely dispersed ownership, a ‘free rider problem’ will emerge because dispersed owners lack both the means and motives to address managerial agency problems. When information asymmetry and interest misalignment between the owner/principal and the manager/agent are present, problems associated with managerial opportunism will be greater, causing agency costs to rise (Fama and Jensen, 1983; Jensen and Meckling, 1976). To reduce such costs, firms disclose additional information (García-Meca and Sánchez-Ballesta, 2010).

On the one hand, controlling shareholders are typically assumed to have fewer agency conflicts with managers and boards of directors compared with widely owned firms. This is due to there being little separation between ownership and control, hand-selection of directors and managers and more intense monitoring of managers (Armstrong et al., 2010). However, high ownership concentration may increase agency conflicts between majority and minority shareholders if controlling shareholders’ interests converge with management objectives (Fama and Jensen, 1983; Ghazali and Weetman, 2006; Pound, 1988). As such, the demand for high-quality public disclosures and financial reporting to monitor management appears less important for firms with controlling shareholders than for firms with dispersed ownership that rely more heavily on outside directors to monitor management. This situation increases the potential for expropriation of minority shareholders and subsequent withdrawal of relevant information.

Proprietary cost theory has also been employed to explain the relationship between various types of voluntary information and ownership concentration. Proprietary costs arise when private information, if released, may harm the firm’s competitive position. For instance, large investors may prefer to limit disclosure-related costs, such as competitive and preparation costs (Verrecchia, 1983), to increase short-term profitability. However, proprietary costs vary depending on the level of competition and entry barriers within the market that affect voluntary disclosure (Birt et al., 2006; Clarkson et al., 1994).

Based on the above theoretical predictions, the following hypothesis is proposed in this research:

H1. There is a negative association between ownership concentration and corporate voluntary disclosure.

2.2. Institutional ownership

The corporate governance literature suggests that institutional investors play an active role in the monitoring and control of firms that benefit the company by reducing agency costs and information asymmetry (Donnelly and Mulcahy, 2008). Generally, large institutional investors enjoy greater voting power, allowing them to undertake corrective actions when deemed necessary, because they possess financial know-how and are better able to determine their information needs and expect firms to meet their expectations (Donnelly and Mulcahy, 2008; Hope, 2013). Ajinkya et al. (2005) argue that institutional investors desire and demand more voluntary disclosures, and that such disclosures, especially earnings forecasts, are closely watched by market participants. They further suggest that these institutions, as outsiders, might not be able to directly oversee the activities of managers, but could elicit greater transparency by demanding more information from the firm, given their decision-oriented focus. Analytical studies such as that by Diamond and Verrecchia (1991) demonstrate that substantial shareholdings of institutional investors also encourage more dissemination of private information to reduce information asymmetry. Laidroo (2009), in contrast, suggests that when the ownership of institutional investors is high, such investors can negotiate with firms to have direct access to private information, which reduces the companies’ need for dissemination of voluntary information to the general public. From a supply perspective, firms increase voluntary disclosure as a signalling mechanism to potential investors in the stock market prior to raising new or additional funds, and institutions prefer to buy stocks in firms that have sustained disclosure enhancements (Bushee and Noe, 2000; Firth, 1980).

Thus, the following hypothesis is tested in this research:

H2. There is a positive association between institutional ownership and corporate voluntary disclosure.

2.3. Foreign ownership

The corporate governance literature commonly distinguishes between foreign and domestic owners (e.g. Douma et al., 2006). Mangena and Tauringana (2007) argue that foreign investors incur more information and agency costs when investing in a foreign country. In a similar vein, Huafang and Jianguo (2007) suggest that due to geographical separation, local accounting standards, language barriers between shareholders and management and the lack of knowledge of local operating environments, foreign investors face high levels of information asymmetry compared to domestic investors. This phenomenon is commonly known in accounting and finance literature as ‘home bias’. Furthermore, Khanna et al. (2004) provide evidence that foreign investors from countries with better disclosure standards demand greater disclosure to reduce information asymmetry. Accordingly, management may increase voluntary disclosure to reduce home bias among foreign investors. However, it has been argued that if foreign owners become substantial shareholders, firms will have less need for equity finance from the local market since funds are acquired from foreign sources. Therefore, the demand for public information may decline due to the ability of foreign investors to extract such information privately from local owners (Laidroo, 2009).

Using legitimacy theory, Haniffa and Cooke (2005) suggest that the presence of foreign investors may result in a higher legitimacy gap. Therefore, management uses voluntary social and environmental disclosure as a proactive legitimacy strategy to encourage foreign flows of capital and satisfy foreign ethical investors.

Thus, the following hypothesis is tested in this research:

H3. There is a positive association between foreign ownership and corporate voluntary disclosure.

2.4. State ownership

There is no consensus concerning theoretical predictions about the association between state ownership and voluntary disclosure. The resource dependence theory suggests that the presence of the state as a major shareholder reduces a firm’s external dependencies, and thus the firm has less incentive to make voluntary disclosures beyond those required by law (Wang et al. 2008). Bushman et al. (2004) find that state ownership and financial transparency are negatively related, a result consistent with the suppression of information transparency by state-owned firms (because of expropriation activities) or information transparency not being required (because of direct governance over firm management). Similarly, using property rights theory, Hope (2013) suggests that managers in state-owned companies lack incentives to increase corporate profitability and improve corporate reporting policy, since the government owns a large proportion of such companies’ shares.

On the other hand, Williams (1999), using Bourgeois theory of political economy, suggests that government plays an important role in reducing the adverse effects of imperfect competition and externalities by establishing an adequate corporate reporting policy. This theory suggests that when the state has shareholdings in the company, the socio-political and economic system of a nation interacts to shape the perceptions of organisations on the need to release social and environmental information that meet stakeholders’ social expectations. Similarly, Naser et al. (2006), using legitimacy and stakeholder theories, argue that government may put pressure on firms (via government-appointed board members) to disclose more social and environmental information, rather than only financial information, in order to improve social perceptions of firms in which it has significant ownership.

We thus propose the following hypothesis in this research:

H4. There is an association between state ownership and corporate voluntary disclosure.

2.5. Managerial ownership

Managerial ownership (i.e. ownership by executive directors and chief executive officer ownership) also affects a firm’s disclosure policy. Jensen and Meckling (1976) suggest that if directors have shareholdings in the company, their interests will be more in line with those of other shareholders. Therefore, they will have long-term interests in the company and less incentive to expropriate minority shareholders. Accordingly, it is expected that managerial ownership will have a positive effect on voluntary disclosure.

However, beyond a certain limit of managerial ownership, the entrenchment effect takes place (Jensen and Ruback, 1983). Shleifer and Vishny (1997) suggest that when a large portion of the company’s shares are owned by managers, they have incentives to reduce corporate transparency in order to preserve their strong voting power and serve their own interests. For instance, block manager owners have direct access to information and may control a firm’s operating and financial policies by taking executive roles on the board of directors, a strategy that reduces their incentives to disseminate information voluntarily (Chau and Gray, 2010). When the proportion of insider ownership becomes greater, the monitoring capacity of outsiders is reduced, which results in less voluntary disclosure by firms.

Thus, the following hypothesis is proposed in this research:

H5. There is an association between managerial ownership and corporate voluntary disclosure.

3. Methods

3.1. Studies included in meta-analysis

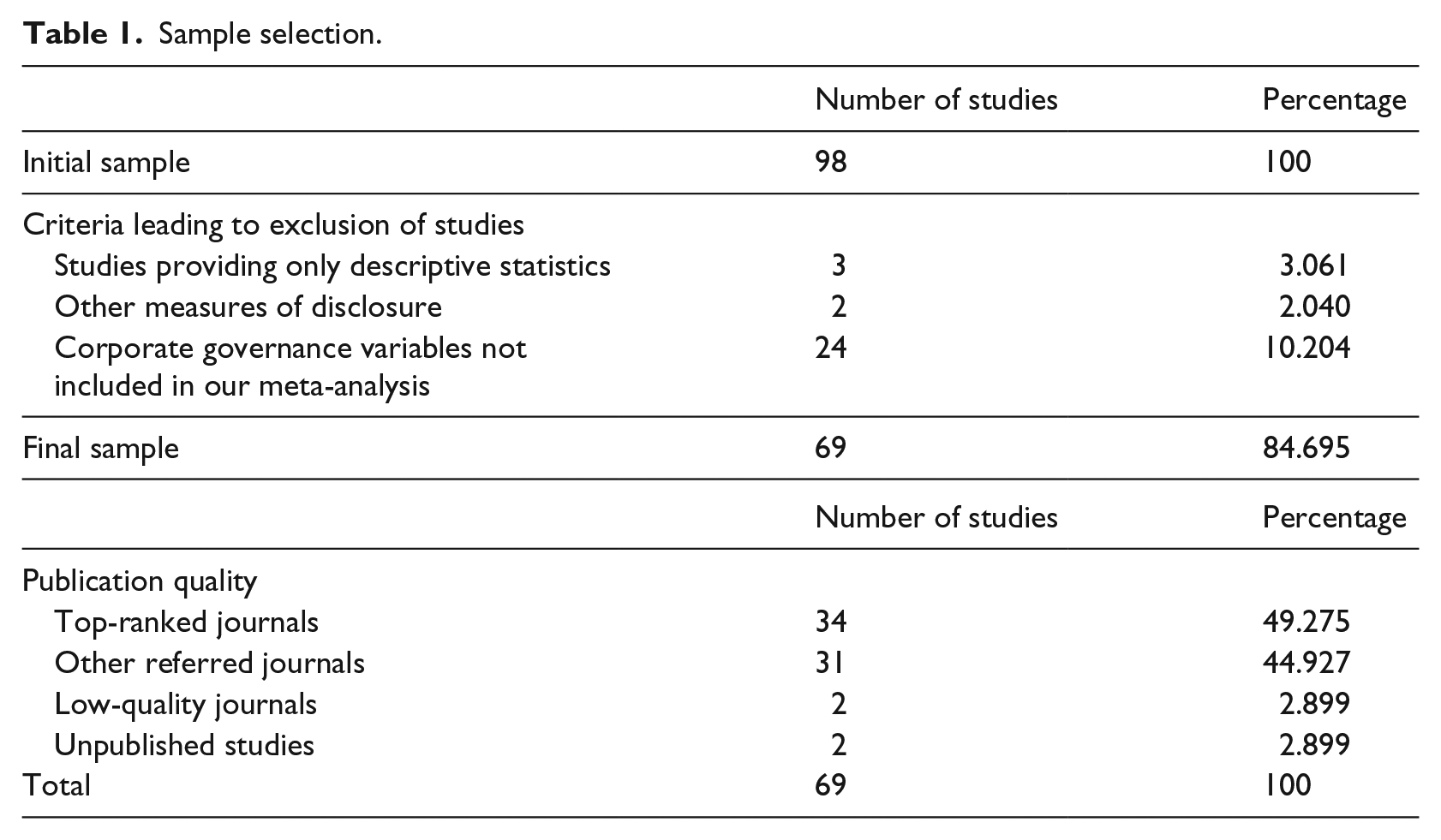

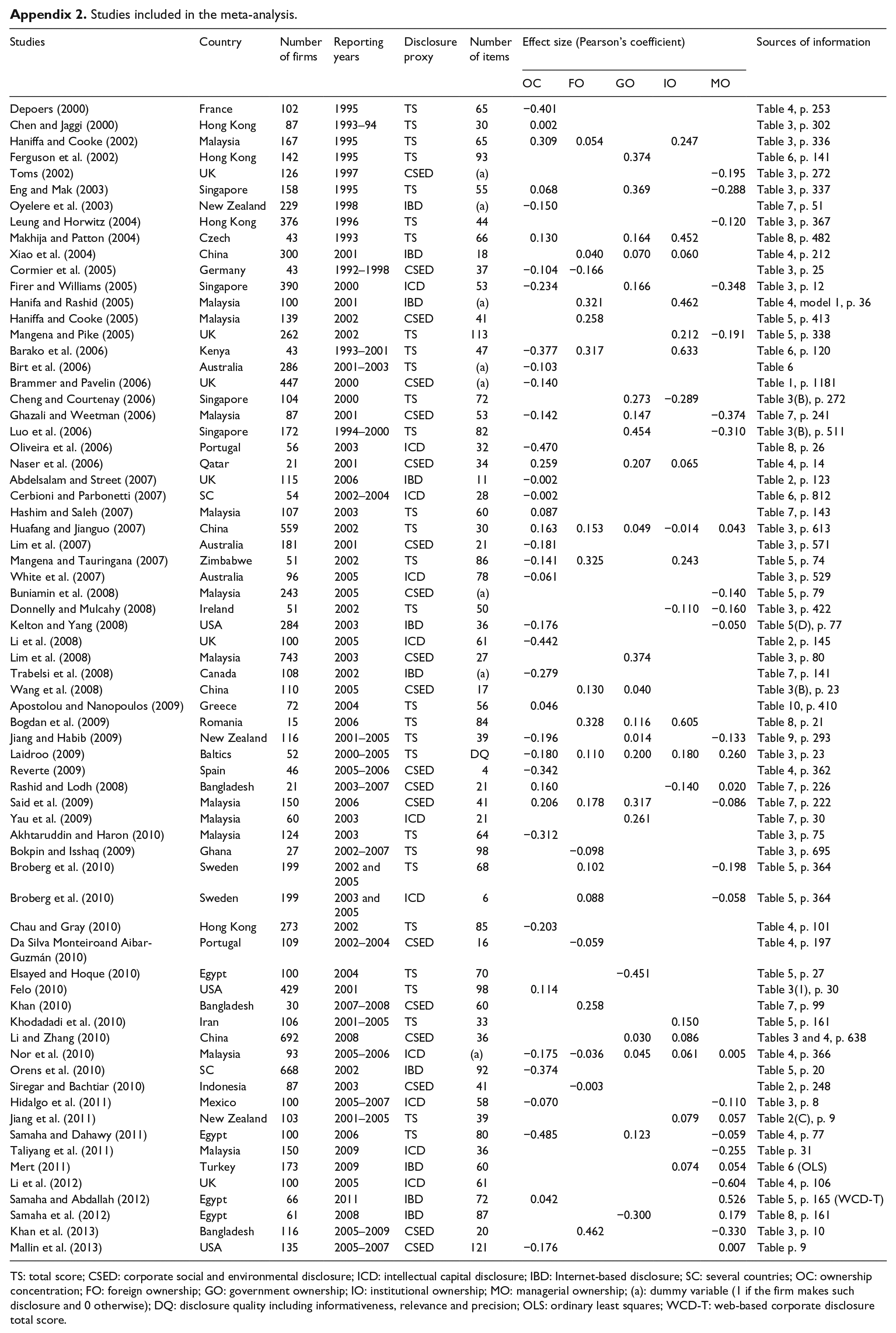

In order to obtain relevant meta-analytic papers, we searched several accounting and finance journals, including search of databases such as ScienceDirect, EJS (EBSCO), Blackwell, Springer, Sage, Emerald, Inderscience, Macmillan, ABI Inform and Social Science Research Network (SSRN). The keywords used include voluntary disclosure, ownership concentration, ownership structure and terms such as managerial, institutional, state and foreign ownerships. We also consulted accounting and corporate finance journals that typically publish studies dealing with corporate governance, corporate ownership and voluntary disclosure. After excluding 29 studies for not meeting the criteria 3 required for meta-analysis, the final sample comprised 69 studies. A total of 34 papers were published in ranked journals (A* and A), 4 31 empirical studies appeared in other refereed journals (B and C), 2 studies were published in low or un-ranked journals and only 2 papers are unpublished. Table 1 shows the sample selection process. Appendix 1 shows the journal ranking and Appendix 2 summarises the results of the 69 studies by year of publication, country setting, number of companies sampled, reporting years and the effect size measure (r) for each ownership attribute: ownership concentration, institutional, foreign, state and managerial ownerships.

Sample selection.

3.2. Meta-analysis procedures

We approached our study in two ways. First, we used meta-analysis techniques developed by Hunter and Schmidt (1990), Rosenthal (1991) and Hunter and Schmidt (2000) to compute effect size. This meta-analysis approach reports findings in terms of bivariate effect sizes. Second, to assess the association between the effect size and moderating variables, we performed meta-analytic regression analysis, popularly known as MARA (see Lipsey and Wilson, 2001). The advantage of meta-analytic regression is that it allows us to assess whether jurisdiction-level moderating effects on the associational strength of the focal relationship still hold in the presence of plausible control variables. Miller and Cardinal (1994) suggest that analysing (moderator) variables simultaneously in a multiple regression format allows proper assessment of the relative explanatory power of each variable. This is because these variables directly compete against one another in the same statistical analyses.

3.2.1. Effect size computation

The meta-analysis technique requires computing the effect size 5 to measure the standardised magnitude of the association between the dependent and independent variables. The effect size is an index used to represent and standardise the findings of the included studies (Lipsey and Wilson, 2001). It provides information about the magnitude of the association between the five ownership forms (ownership concentration, foreign investors, institutional shareholders, state ownership and managerial ownership) and voluntary disclosure level for each study included in the meta-analysis.

In computing the effect size from the reported statistics, a range of procedures were used. When a study reports Pearson’s r coefficient, such a statistic was used to calculate the effect size between the voluntary disclosure score and explanatory variable. Whenever other statistics are reported, such as Student’s t and Z value, we transformed them into r following Rosenthal (1991).

6

We then implemented three steps as suggested by Hunter and Schmidt (2000): (1) the mean correlation

3.2.2. Variables intervening in the association between ownership attributes and voluntary disclosure

The literature documents inconsistency in findings concerning the relationship between different types of ownership and voluntary disclosure. Various factors espoused in the literature could contribute to the results’ heterogeneity, such as legal and institutional characteristics, level of investor protection and market development, among others. Using meta-analysis, it is possible to quantitatively determine if these factors, referred to as moderating factors, have influenced the relationship between ownership forms and voluntary disclosure. In our study, we employed two country-specific moderating factors, investor protection and the level of market development, as well as other researcher-induced factors, to investigate whether the conflicting results between ownership concentration, ownership types and voluntary disclosure could be explained by these factors, or whether the results are just random errors. These two characteristics have generally been used in the literature for explaining differences in voluntary disclosure among countries (Jaggi and Low, 2000; La Porta et al., 2000). We outline how these two factors would act as moderating variables in the association between ownership concentration, ownership types and voluntary disclosure.

Ownership concentration determines the power and incentives of large owners to enforce their objectives. In jurisdictions where markets are underdeveloped, concentrated ownership gives such owners power to get involved in governance and in determining strategies. This power and the incentives will be less under high legal enforcement and high market development settings, since minority investors will be more protected by law and market forces (Pedersen and Thomsen, 1997). For instance, Leuz et al. (2003) suggest that the level of outside investor protection determines the extent of financial information reported to outsiders, noting that weak legal protection appears to result in lower disclosure levels. In addition, a strong equity market is generally characterised by low ownership concentration and high volume of transactions, implying better disclosure and production of information (Salter, 1998). This implies that ownership concentration will have a negative effect on voluntary disclosure in low investor protection and low market development settings.

Different types of owners have different preferences and objectives, and it has been suggested that legal characteristics and market forces affect manager–owner behaviour with respect to disclosure strategy (Beyer et al., 2010). First, institutional investors generally tend to have multiple ties with the firm in which they own shares, since they will also act as creditors with the same firm (Heugens et al., 2009). Large institutional investors enjoy greater voting power and are better able to determine the investors’ information needs (Donnelly and Mulcahy, 2008). In a low disclosure environment, institutional owners would play an important role in improving reporting quality, because investor protection regulations and market forces are less able to control management discretion over corporate reporting policy.

Second, as the primary objective of foreign investors is to protect their investments by realising higher performance, they generally demand more information compared to their domestic counterparts due to information asymmetry (home bias). However, if they find a favourable legal environment that protects their financial interests, they may put pressure on management to go beyond the higher profitability objective to improve corporate reporting policy. Furthermore, foreign investors in a less developed market encourage management to improve corporate reporting policy, since they bring good governance experience from their home markets to ensure that managers operate in line with their expectations (Chibber and Majumdar, 1999; Heugens et al., 2009). Therefore, we expect foreign investors will have a stronger association with voluntary disclosure in a weak legal setting.

Third, the association between state ownership and voluntary disclosure is expected to be affected by the level of investor protection and capital market development in a country. If the prevailing rules and institutions influencing corporate transparency are weak, managers may be less inclined to disclose information beyond mandatory requirements because private investors (who generally demand more information) will have less influence on management dominated by state enterprises. In contrast, in a developed capital market, where there is already a high level of corporate disclosure (due to strong lobbying and competition), firms with substantial state ownership have an incentive to match their private shareholder-dominated counterparts in mitigating reputational loss.

Finally, managerial investors are viewed as insider owners, who combine a substantial equity stake with direct managerial control over the firm (Heugens et al., 2009). They generally invest a part of their wealth in the firms they manage; therefore, they will be more risk-averse than more diversified investors (Fama and Jensen, 1983). This risk aversion may be higher under stringent legal rules (e.g. strong investor protection, high market development), given the increased level of litigation risk that may arise.

Other researcher-induced factors considered in this study are measurement of disclosure index construction, publication quality and measurement of the explanatory variables. The first of these addresses how disclosure construction 11 affects the ownership structure and voluntary disclosure relationship. According to Artiach and Clarkson (2011), ‘different disclosure indices often develop within different studies that address relatively similar issues because there is no agreed upon theory to guide the choice or number of items to include within the index’ (p. 26). Accordingly, disclosure index construction is expected to moderate the relationship between ownership structure and types and voluntary disclosure. Publication quality may also moderate the examined relationships, since quality journals conduct a more thorough and rigorous review process (Moller and Jennions, 2001). Finally, meta-analytic accounting literature posits that the measurement of explanatory variables may also affect the examined relationship (Ahmed and Courtis, 1999; García-Meca and Sánchez-Ballesta, 2010).

3.2.3. Measuring moderating factors, additional tests and file drawer problem

For investor protection level, our classification is based on the ranking provided by the World Bank 12 and World Governance Index. High investor protection countries are those which have an investor protection rank lower than the median rank within the sample. Similarly, countries classified as part of the high (low) market development group are those possessing a market development ratio 13 higher (lower) than the median ratio.

The moderating effect of disclosure index construction was examined by dividing our sample into two groups: (1) low number of items group (disclosure index including a number of items lower than the median) and (2) high number of items group (disclosure index higher than the median). For journal quality, we divided our overall sample into two groups: high-quality journal papers and low-quality journal papers. The first group includes all published papers that appear in A*- and A-ranked journals in the Australian Business Deans Council (ABDC) list (2013), while the second group includes all studies identified in SSRN and published in other journals. 14 Finally, ownership concentration was sub-grouped into percentage of shares owned by substantial shareholders (state ownership) and FO groups. It should be noted here that managerial, government, foreign and institutional ownerships were measured using the percentage of shares owned by managers, government, foreign shareholders and institutions, respectively, so no further grouping was considered necessary.

As published studies may remain undetected even after a thorough search, the reliability of the results could be questioned. Rosenthal (1979) refers to this problem as the ‘file drawer problem’. To determine whether the conclusions drawn from our meta-analysis are likely to be influenced by any such publication bias, we applied Orwin’s (1983) method, which in turn is modified and based on Rosenthal’s (1979) approach. This method requires the estimation of the fail-safe 15 N. The fail-safe N is calculated when significant associations are reported for the meta-analysis.

3.2.4. MARA

Meta-regression represents an extension of sub-group meta-analysis. However, instead of taking into account only one moderator at a time, it tests for all moderators (Higgins and Green, 2011). In meta-regression, the dependent variable is the weighted effect size of an examined relationship, and the explanatory variables can be continuous variables or dummy variables depending on the study characteristics (Hedges and Olkin, 1985). MARA represents a special meta-analytic approach using weighted least squares (WLS) regression analysis in order to assess the association between the effect size and the moderating variables, in an attempt to model and explore the heterogeneity in the effect size distribution (Lipsey and Wilson, 2001).

Therefore, the MARA model in our meta-analytic review is specified as follows

where

4. Results

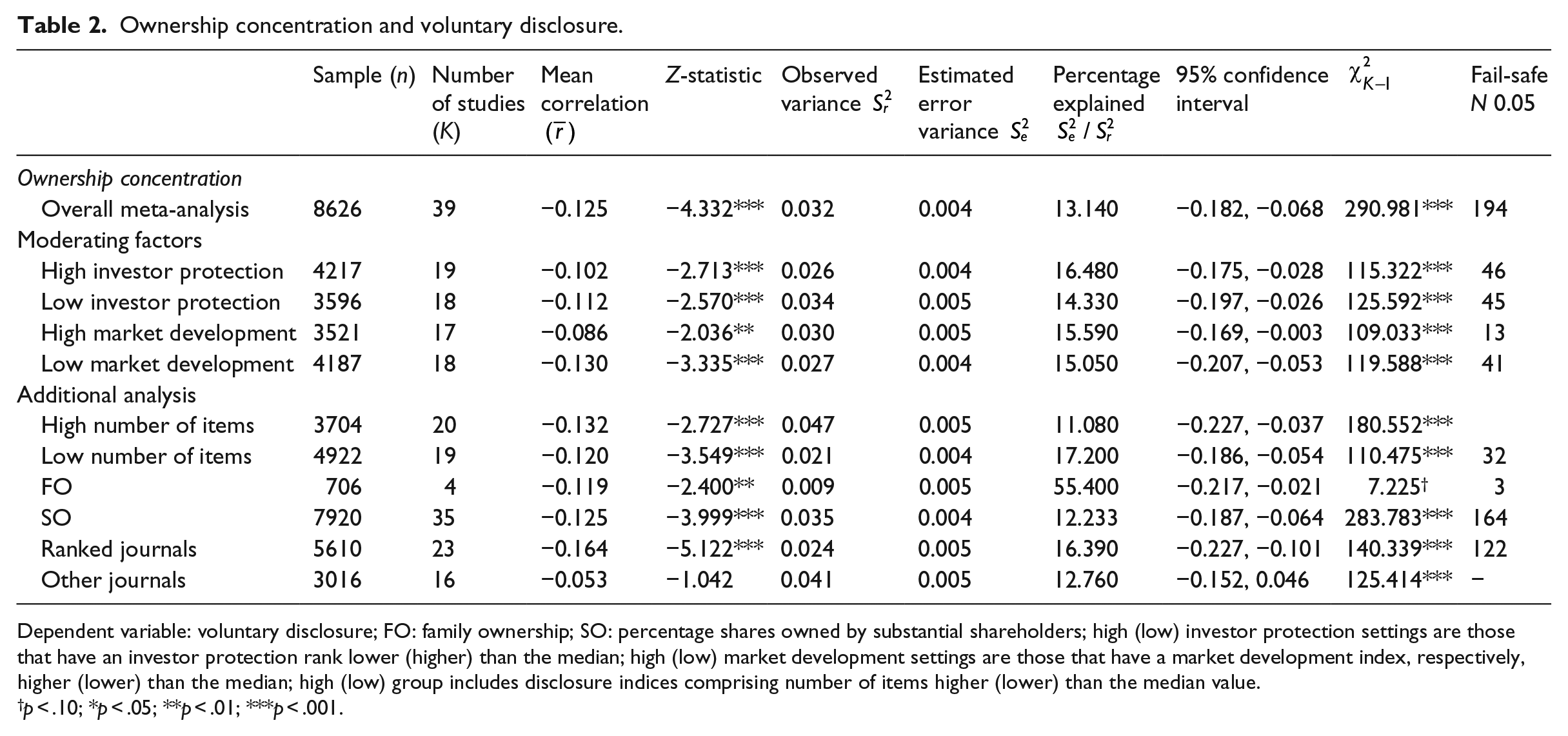

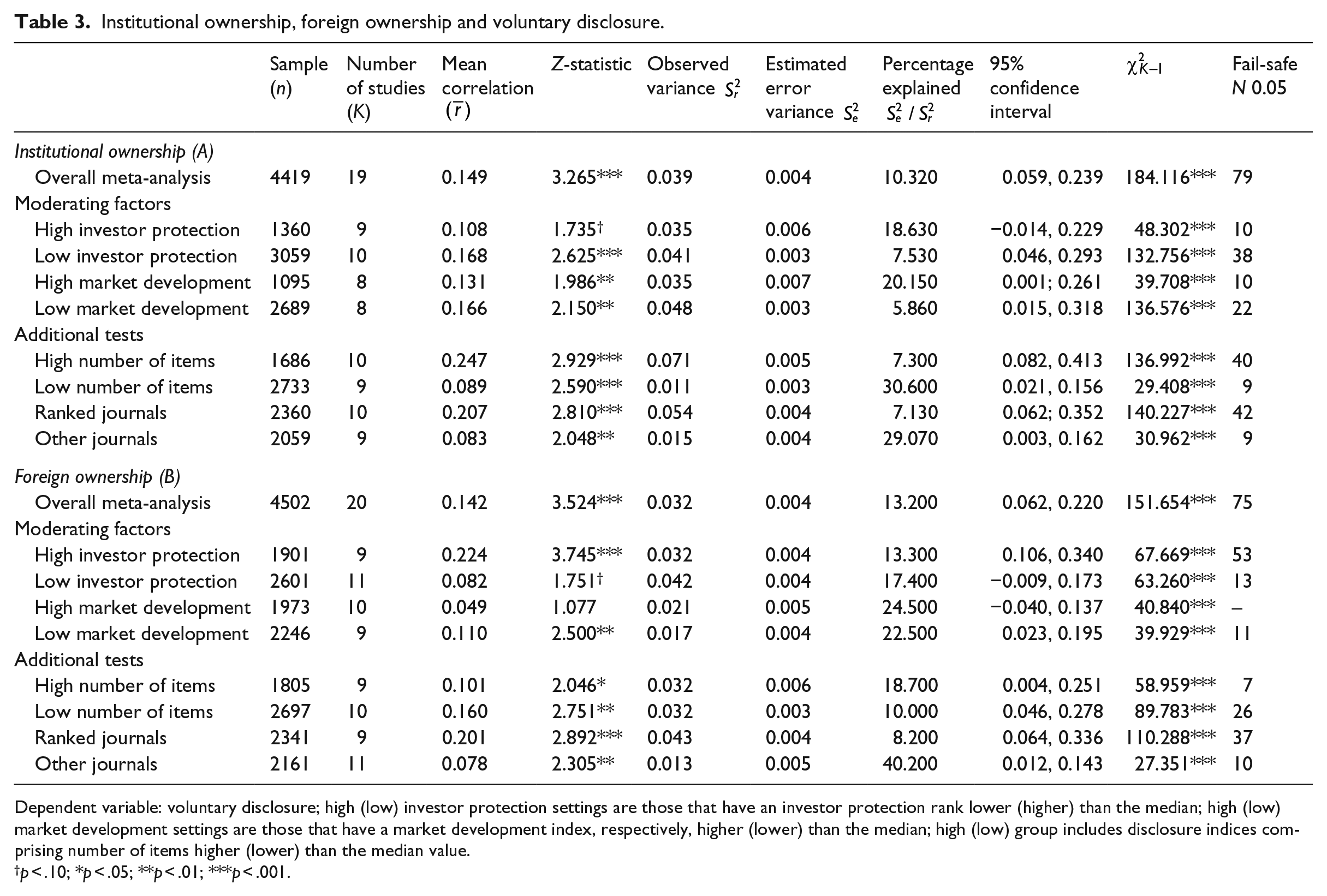

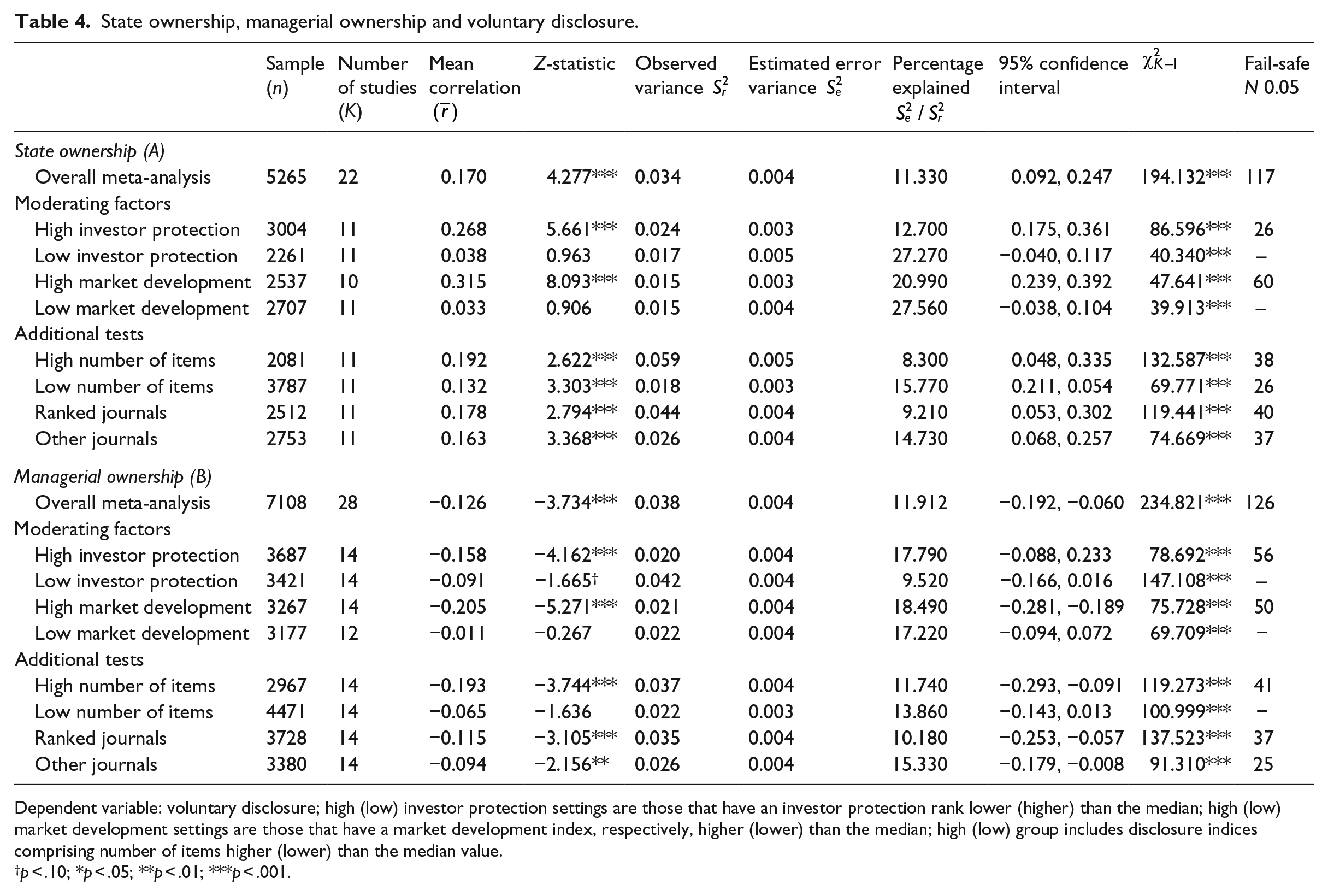

The univariate meta-analysis results are presented in Tables 2 to 4. We first present the overall results, and if the homogeneity test is rejected, we present further analyses according to moderating variables explained earlier. In Table 5, we present the MARA results.

Ownership concentration and voluntary disclosure.

Dependent variable: voluntary disclosure; FO: family ownership; SO: percentage shares owned by substantial shareholders; high (low) investor protection settings are those that have an investor protection rank lower (higher) than the median; high (low) market development settings are those that have a market development index, respectively, higher (lower) than the median; high (low) group includes disclosure indices comprising number of items higher (lower) than the median value.

p < .10; *p < .05; **p < .01; ***p < .001.

Institutional ownership, foreign ownership and voluntary disclosure.

Dependent variable: voluntary disclosure; high (low) investor protection settings are those that have an investor protection rank lower (higher) than the median; high (low) market development settings are those that have a market development index, respectively, higher (lower) than the median; high (low) group includes disclosure indices comprising number of items higher (lower) than the median value.

p < .10; *p < .05; **p < .01; ***p < .001.

State ownership, managerial ownership and voluntary disclosure.

Dependent variable: voluntary disclosure; high (low) investor protection settings are those that have an investor protection rank lower (higher) than the median; high (low) market development settings are those that have a market development index, respectively, higher (lower) than the median; high (low) group includes disclosure indices comprising number of items higher (lower) than the median value.

p < .10; *p < .05; **p < .01; ***p < .001.

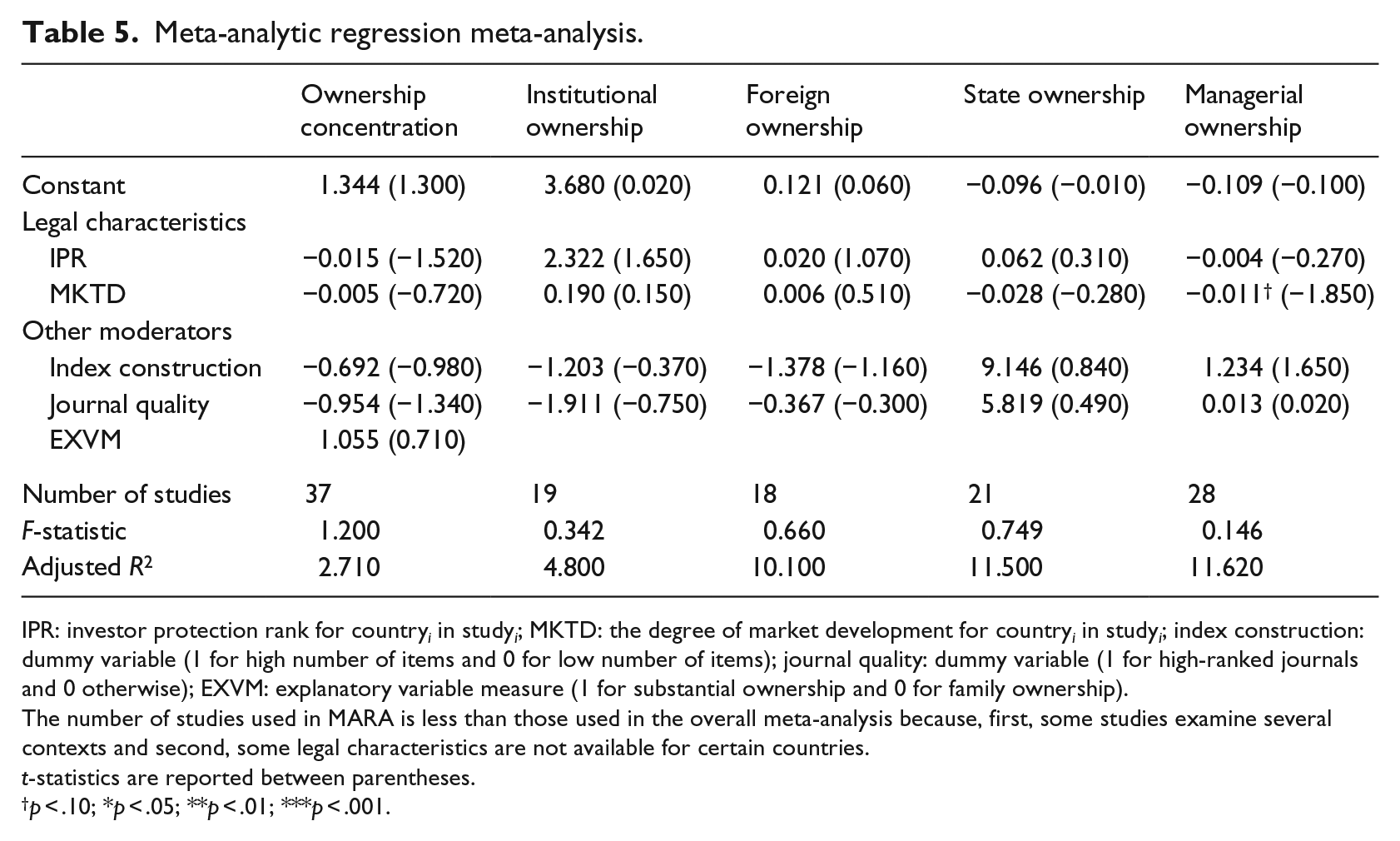

Meta-analytic regression meta-analysis.

IPR: investor protection rank for country i in study i ; MKTD: the degree of market development for country i in study i ; index construction: dummy variable (1 for high number of items and 0 for low number of items); journal quality: dummy variable (1 for high-ranked journals and 0 otherwise); EXVM: explanatory variable measure (1 for substantial ownership and 0 for family ownership).

The number of studies used in MARA is less than those used in the overall meta-analysis because, first, some studies examine several contexts and second, some legal characteristics are not available for certain countries.

t-statistics are reported between parentheses.

p < .10; *p < .05; **p < .01; ***p < .001.

4.1. Ownership concentration

The relationship between ownership concentration and voluntary disclosure in 39 studies (n = 8626) is shown in Table 2. The overall meta-analysis shows that ownership concentration is significantly negatively associated with voluntary disclosure, with a mean effect size

4.2. Institutional ownership

The relationship between institutional ownership and voluntary disclosure is significantly positive, with a mean effect size

4.3. Foreign ownership

Table 3(B) shows a significant effect size

The level of investor protection has a moderating effect on the relationship, with a mean correlation

4.4. State ownership

The relationship between state ownership and voluntary disclosure in 22 studies (n = 5265) shows a significant association, with a

Consistent with our expectation, the positive association between voluntary disclosure levels and state ownership is greater in high investor protection and high market development countries. As stated earlier, firms with substantial state ownership tend to disclose more social and environment items, and the demand for such disclosure tends to be higher where the capital market is developed and legal enforcement is better. This could be seen as state ownership having a complementary role in voluntary disclosure.

4.5. Managerial ownership

Managerial ownership is negatively associated (

4.6. Additional tests and file drawer problem

Additional tests examined whether disclosure index construction and publication quality moderate the above associations. With respect to the construction of disclosure index, we find that this factor moderates the association between institutional, foreign, state and managerial ownerships and voluntary disclosure. We also find that the quality of journals moderates all the associations considered in univariate tests.

To test for the stability of the results, we computed the fail-safe N for each significant association. The number of unreported needed studies with insignificant results required to reduce the mean effect size to a specified criterion is generally high. It ranges from 3 to 194 studies, indicating that our meta-analytic findings have not been compromised by the file drawer problem.

4.7. Meta-regression (MARA)

In Table 5, we report the MARA results for each ownership form after controlling for all moderating variables. For managerial ownership, the degree of market development negatively moderates the relationship between management ownership and voluntary disclosure, with a coefficient of −0.011 (t-statistic = −1.850). For the remaining regressions, the moderating variables do not affect the overall relationships between ownership concentration and forms (institutional, foreign and state ownerships) and voluntary disclosure. It should be noted that the MARA methodology controls for underlying correlations among the independent variables. While we find a high level of correlation among the moderating variables, raising concerns about multicollinearity, the variance inflation factor (VIF) statistics are generally lower than the well-accepted cut-off point of 10 (Neter et al., 1989). Furthermore, the difference in the results could also be due to the use of different weightings for the effect size in MARA (Heugens et al., 2009).

5. Discussion and conclusion

Many studies have addressed the effect of ownership structure on voluntary disclosure over the last decade. They have, however, at best produced mixed empirical evidence. The conflicting results could be due to treating ownership as a homogeneous group by ignoring the identity of the owners, who have different motivations affecting corporate decision-making (Hautz et al., 2013). As such, there have been calls to better understand the role of ownership attributes in corporate reporting policy (Armstrong et al., 2010; Brown et al., 2011; García-Meca and Sánchez-Ballesta, 2010). To contribute to the ongoing debate on the role of ownership on disclosure policy, we investigated, using well-accepted meta-analysis techniques, the association between voluntary disclosure and ownership concentration and different ownership types: state, institutional, managerial and foreign ownerships. Furthermore, we tested the moderating effects of the levels of investor protection, market development and a number of other variables, on these associations.

Based on 69 empirical studies undertaken over the last 13 years, our primary analysis shows that ownership concentration and managerial ownership are negatively associated with voluntary disclosures, while state, institutional and foreign ownership types are positively related to voluntary disclosures. Testing for the moderating effects, we document that the negative association between voluntary disclosure and concentrated ownership is greater in low market development settings. In low capital market development settings, concentrated owners become more entrenched and extract information from management for private benefit, thus reducing voluntary information disclosure.

The negative relationship between managerial ownership and disclosures is more evident in countries with strong legal enforcement mechanisms (investor protection and market development). In high investor protection settings, managerial incentives to voluntarily disclose information could be constrained by the potential for litigation and managerial reputation loss, implying that shareholder litigation risk and corporate governance mechanisms are important determinants of voluntary disclosure strategies (Beyer et al., 2010).

The higher level of correlations between voluntary disclosure, and institutional and foreign ownership in weak legal enforcement settings and less developed markets, suggests that these investor categories act as effective monitors and play a substitution role for weak legal enforcement. Finally, state ownership is associated with more voluntary disclosures in high investor protection and high market development settings. This is consistent with arguments that most firms with substantial state owners disclose more social and environment items, and investors’ demand for such disclosure tends to be higher where the capital market is developed and legal enforcement is better.

Overall, our meta-analysis provides cross-country evidence that ownership identity, and legal and institutional characteristics, are important in understanding the relationship between voluntary disclosure and ownership types. One important implication of our meta-analytic findings is that since potential owners differ in terms of wealth constraints, competence, preferences and non-ownership ties to the firm, these differences affect the way owners exercise their ownership rights, which therefore has important consequences for corporate reporting policy. Another important implication is that there is no universal association between ownership structure and voluntary disclosure, since such a relationship depends on the interplay between country- and firm-level governance mechanisms.

Footnotes

Appendix

Studies included in the meta-analysis.

| Studies | Country | Number of firms | Reporting years | Disclosure proxy | Number of items | Effect size (Pearson’s coefficient) |

Sources of information | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| OC | FO | GO | IO | MO | |||||||

| Depoers (2000) | France | 102 | 1995 | TS | 65 | −0.401 | Table 4, p. 253 | ||||

| Chen and Jaggi (2000) | Hong Kong | 87 | 1993–94 | TS | 30 | 0.002 | Table 3, p. 302 | ||||

| Haniffa and Cooke (2002) | Malaysia | 167 | 1995 | TS | 65 | 0.309 | 0.054 | 0.247 | Table 3, p. 336 | ||

| Ferguson et al. (2002) | Hong Kong | 142 | 1995 | TS | 93 | 0.374 | Table 6, p. 141 | ||||

| Toms (2002) | UK | 126 | 1997 | CSED | (a) | −0.195 | Table 3, p. 272 | ||||

| Eng and Mak (2003) | Singapore | 158 | 1995 | TS | 55 | 0.068 | 0.369 | −0.288 | Table 3, p. 337 | ||

| Oyelere et al. (2003) | New Zealand | 229 | 1998 | IBD | (a) | −0.150 | Table 7, p. 51 | ||||

| Leung and Horwitz (2004) | Hong Kong | 376 | 1996 | TS | 44 | −0.120 | Table 3, p. 367 | ||||

| Makhija and Patton (2004) | Czech | 43 | 1993 | TS | 66 | 0.130 | 0.164 | 0.452 | Table 8, p. 482 | ||

| Xiao et al. (2004) | China | 300 | 2001 | IBD | 18 | 0.040 | 0.070 | 0.060 | Table 4, p. 212 | ||

| Cormier et al. (2005) | Germany | 43 | 1992–1998 | CSED | 37 | −0.104 | −0.166 | Table 3, p. 25 | |||

| Firer and Williams (2005) | Singapore | 390 | 2000 | ICD | 53 | −0.234 | 0.166 | −0.348 | Table 3, p. 12 | ||

| Hanifa and Rashid (2005) | Malaysia | 100 | 2001 | IBD | (a) | 0.321 | 0.462 | Table 4, model 1, p. 36 | |||

| Haniffa and Cooke (2005) | Malaysia | 139 | 2002 | CSED | 41 | 0.258 | Table 5, p. 413 | ||||

| Mangena and Pike (2005) | UK | 262 | 2002 | TS | 113 | 0.212 | −0.191 | Table 5, p. 338 | |||

| Barako et al. (2006) | Kenya | 43 | 1993–2001 | TS | 47 | −0.377 | 0.317 | 0.633 | Table 6, p. 120 | ||

| Birt et al. (2006) | Australia | 286 | 2001–2003 | TS | (a) | −0.103 | Table 6 | ||||

| Brammer and Pavelin (2006) | UK | 447 | 2000 | CSED | (a) | −0.140 | Table 1, p. 1181 | ||||

| Cheng and Courtenay (2006) | Singapore | 104 | 2000 | TS | 72 | 0.273 | −0.289 | Table 3(B), p. 272 | |||

| Ghazali and Weetman (2006) | Malaysia | 87 | 2001 | CSED | 53 | −0.142 | 0.147 | −0.374 | Table 7, p. 241 | ||

| Luo et al. (2006) | Singapore | 172 | 1994–2000 | TS | 82 | 0.454 | −0.310 | Table 3(B), p. 511 | |||

| Oliveira et al. (2006) | Portugal | 56 | 2003 | ICD | 32 | −0.470 | Table 8, p. 26 | ||||

| Naser et al. (2006) | Qatar | 21 | 2001 | CSED | 34 | 0.259 | 0.207 | 0.065 | Table 4, p. 14 | ||

| Abdelsalam and Street (2007) | UK | 115 | 2006 | IBD | 11 | −0.002 | Table 2, p. 123 | ||||

| Cerbioni and Parbonetti (2007) | SC | 54 | 2002–2004 | ICD | 28 | −0.002 | Table 6, p. 812 | ||||

| Hashim and Saleh (2007) | Malaysia | 107 | 2003 | TS | 60 | 0.087 | Table 7, p. 143 | ||||

| Huafang and Jianguo (2007) | China | 559 | 2002 | TS | 30 | 0.163 | 0.153 | 0.049 | −0.014 | 0.043 | Table 3, p. 613 |

| Lim et al. (2007) | Australia | 181 | 2001 | CSED | 21 | −0.181 | Table 3, p. 571 | ||||

| Mangena and Tauringana (2007) | Zimbabwe | 51 | 2002 | TS | 86 | −0.141 | 0.325 | 0.243 | Table 5, p. 74 | ||

| White et al. (2007) | Australia | 96 | 2005 | ICD | 78 | −0.061 | Table 3, p. 529 | ||||

| Buniamin et al. (2008) | Malaysia | 243 | 2005 | CSED | (a) | −0.140 | Table 5, p. 79 | ||||

| Donnelly and Mulcahy (2008) | Ireland | 51 | 2002 | TS | 50 | −0.110 | −0.160 | Table 3, p. 422 | |||

| Kelton and Yang (2008) | USA | 284 | 2003 | IBD | 36 | −0.176 | −0.050 | Table 5(D), p. 77 | |||

| Li et al. (2008) | UK | 100 | 2005 | ICD | 61 | −0.442 | Table 2, p. 145 | ||||

| Lim et al. (2008) | Malaysia | 743 | 2003 | CSED | 27 | 0.374 | Table 3, p. 80 | ||||

| Trabelsi et al. (2008) | Canada | 108 | 2002 | IBD | (a) | −0.279 | Table 7, p. 141 | ||||

| Wang et al. (2008) | China | 110 | 2005 | CSED | 17 | 0.130 | 0.040 | Table 3(B), p. 23 | |||

| Apostolou and Nanopoulos (2009) | Greece | 72 | 2004 | TS | 56 | 0.046 | Table 10, p. 410 | ||||

| Bogdan et al. (2009) | Romania | 15 | 2006 | TS | 84 | 0.328 | 0.116 | 0.605 | Table 8, p. 21 | ||

| Jiang and Habib (2009) | New Zealand | 116 | 2001–2005 | TS | 39 | −0.196 | 0.014 | −0.133 | Table 9, p. 293 | ||

| Laidroo (2009) | Baltics | 52 | 2000–2005 | TS | DQ | −0.180 | 0.110 | 0.200 | 0.180 | 0.260 | Table 3, p. 23 |

| Reverte (2009) | Spain | 46 | 2005–2006 | CSED | 4 | −0.342 | Table 4, p. 362 | ||||

| Rashid and Lodh (2008) | Bangladesh | 21 | 2003–2007 | CSED | 21 | 0.160 | −0.140 | 0.020 | Table 7, p. 226 | ||

| Said et al. (2009) | Malaysia | 150 | 2006 | CSED | 41 | 0.206 | 0.178 | 0.317 | −0.086 | Table 7, p. 222 | |

| Yau et al. (2009) | Malaysia | 60 | 2003 | ICD | 21 | 0.261 | Table 7, p. 30 | ||||

| Akhtaruddin and Haron (2010) | Malaysia | 124 | 2003 | TS | 64 | −0.312 | Table 3, p. 75 | ||||

| Bokpin and Isshaq (2009) | Ghana | 27 | 2002–2007 | TS | 98 | −0.098 | Table 3, p. 695 | ||||

| Broberg et al. (2010) | Sweden | 199 | 2002 and 2005 | TS | 68 | 0.102 | −0.198 | Table 5, p. 364 | |||

| Broberg et al. (2010) | Sweden | 199 | 2003 and 2005 | ICD | 6 | 0.088 | −0.058 | Table 5, p. 364 | |||

| Chau and Gray (2010) | Hong Kong | 273 | 2002 | TS | 85 | −0.203 | Table 4, p. 101 | ||||

| Da Silva Monteiroand Aibar-Guzmán (2010) | Portugal | 109 | 2002–2004 | CSED | 16 | −0.059 | Table 4, p. 197 | ||||

| Elsayed and Hoque (2010) | Egypt | 100 | 2004 | TS | 70 | −0.451 | Table 5, p. 27 | ||||

| Felo (2010) | USA | 429 | 2001 | TS | 98 | 0.114 | Table 3(1), p. 30 | ||||

| Khan (2010) | Bangladesh | 30 | 2007–2008 | CSED | 60 | 0.258 | Table 7, p. 99 | ||||

| Khodadadi et al. (2010) | Iran | 106 | 2001–2005 | TS | 33 | 0.150 | Table 5, p. 161 | ||||

| Li and Zhang (2010) | China | 692 | 2008 | CSED | 36 | 0.030 | 0.086 | Tables 3 and 4, p. 638 | |||

| Nor et al. (2010) | Malaysia | 93 | 2005–2006 | ICD | (a) | −0.175 | −0.036 | 0.045 | 0.061 | 0.005 | Table 4, p. 366 |

| Orens et al. (2010) | SC | 668 | 2002 | IBD | 92 | −0.374 | Table 5, p. 20 | ||||

| Siregar and Bachtiar (2010) | Indonesia | 87 | 2003 | CSED | 41 | −0.003 | Table 2, p. 248 | ||||

| Hidalgo et al. (2011) | Mexico | 100 | 2005–2007 | ICD | 58 | −0.070 | −0.110 | Table 3, p. 8 | |||

| Jiang et al. (2011) | New Zealand | 103 | 2001–2005 | TS | 39 | 0.079 | 0.057 | Table 2(C), p. 9 | |||

| Samaha and Dahawy (2011) | Egypt | 100 | 2006 | TS | 80 | −0.485 | 0.123 | −0.059 | Table 4, p. 77 | ||

| Taliyang et al. (2011) | Malaysia | 150 | 2009 | ICD | 36 | −0.255 | Table p. 31 | ||||

| Mert (2011) | Turkey | 173 | 2009 | IBD | 60 | 0.074 | 0.054 | Table 6 (OLS) | |||

| Li et al. (2012) | UK | 100 | 2005 | ICD | 61 | −0.604 | Table 4, p. 106 | ||||

| Samaha and Abdallah (2012) | Egypt | 66 | 2011 | IBD | 72 | 0.042 | 0.526 | Table 5, p. 165 (WCD-T) | |||

| Samaha et al. (2012) | Egypt | 61 | 2008 | IBD | 87 | −0.300 | 0.179 | Table 8, p. 161 | |||

| Khan et al. (2013) | Bangladesh | 116 | 2005–2009 | CSED | 20 | 0.462 | −0.330 | Table 3, p. 10 | |||

| Mallin et al. (2013) | USA | 135 | 2005–2007 | CSED | 121 | −0.176 | 0.007 | Table p. 9 | |||

TS: total score; CSED: corporate social and environmental disclosure; ICD: intellectual capital disclosure; IBD: Internet-based disclosure; SC: several countries; OC: ownership concentration; FO: foreign ownership; GO: government ownership; IO: institutional ownership; MO: managerial ownership; (a): dummy variable (1 if the firm makes such disclosure and 0 otherwise); DQ: disclosure quality including informativeness, relevance and precision; OLS: ordinary least squares; WCD-T: web-based corporate disclosure total score.

Acknowledgements

The authors gratefully acknowledge the constructive comments and suggestions from Darren Henry, Paul Kim, Robert Rosenthal, seminar participants at La Trobe University, two anonymous referees and editors of this journal, Peter Clarkson and Baljit Sidhu.

Final transcript accepted 25 February 2016 by Peter Clarkson (AE Accounting).

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

1.

Marston and Shrives (1991) and ![]() provide reviews of these studies. Ahmed and Courtis (1999), using meta-analytic techniques, find that firm-specific attributes such as firm size, leverage and international cross-listing are positively associated with corporate disclosures (voluntary and aggregate).

provide reviews of these studies. Ahmed and Courtis (1999), using meta-analytic techniques, find that firm-specific attributes such as firm size, leverage and international cross-listing are positively associated with corporate disclosures (voluntary and aggregate).

2.

Although they examined 27 studies, there were 19 studies on ownership concentration and voluntary disclosure (p. 620). They also examined the association between board independence and voluntary disclosure using 19 prior studies and find a positive association between the variables. ![]() , who focus on the distribution of ownership shares (ownership concentration) and voluntary disclosure, have examined two forms of ownership concentration (insiders vs outsiders) with only seven studies.

, who focus on the distribution of ownership shares (ownership concentration) and voluntary disclosure, have examined two forms of ownership concentration (insiders vs outsiders) with only seven studies.

3.

The criteria considered for the inclusion of studies are as follows: (1) the study should deal with voluntary disclosure with at least one of the above ownership types examined as an explanatory variable and (2) sufficient data are provided in the empirical paper included in the meta-analysis to compute the effect size (e.g. Pearson’s coefficient, t-statistic, Z-statistic, p-value). ![]() provides some examples of papers excluded for not meeting these criteria.

provides some examples of papers excluded for not meeting these criteria.

4.

For the purpose of ranking, we used the Australian Business Deans Council (ABDC) list of journals (2013), in order to avoid confusion due to the availability of several university-specific and commercial journal rankings.

5.

6.

Ahmed and Courtis (1999); Ahmed et al. (2013) and Trotman and Wood (1991) followed the same procedures in prior meta-analysis in accounting and auditing ![]() , cf. Chapter 3), if the regression coefficient is negative, it is necessary to keep the negative sign.

, cf. Chapter 3), if the regression coefficient is negative, it is necessary to keep the negative sign.

7.

For

8.

The observed variance

9.

10.

11.

Empirical disclosure literature focuses on the assessment of the level of voluntary disclosure, either in annual reports (total score, intellectual capital information or social and environmental disclosure) or on firms’ websites (Internet-based disclosure). The total score refers to those studies using a mix of information dealing with financial, social and environmental and intellectual capital information.

13.

14.

We have taken appropriate measures not to double count the same paper (published with a different name).

15.

The fail-safe N is calculated using equation (5):

16.

Hedges (1982) and ![]() show that the optimal weight to be used in MARA is the inverse variance weight, which is calculated as follows:

show that the optimal weight to be used in MARA is the inverse variance weight, which is calculated as follows:

17.

We calculated mean difference and t-statistics for all moderating variables but not reported.