Abstract

We study the relationship between stock price synchronicity and information disclosure of firms listed in the Chinese stock market, using hand-collected data on firms’ official microblogging content in Sina Weibo, a popular microblogging service in China. We find that after controlling for the impact of traditional media, the number of Weibo tweets is related negatively to stock price synchronicity, indicating that stock prices incorporate firm-specific information disclosed in the firm’s official Weibo. Number of microblogging fans can strengthen this negative relationship. Our result is robust to alternative measures of stock price synchronicity, microblogging information disclosure, and to endogeneity issues.

JEL Classification:

1. Introduction

Traditional media such as newswires, broadcasts, financial websites, and newspapers, provide information that can be accessed by investors on a restricted time and resources basis only. Users/investors are now no longer satisfied with the one-way dissemination of information via traditional media. They are seeking a channel that enables them to interact directly with management. In addition, the traditional media are biased toward the coverage of high-visibility firms due to the high informational demand on these firms (Miller, 2006). Thus, if low-visibility firms disseminate news only through an ineffective channel, there will be a high chance that investors may not receive information in a timely manner. Drake et al. (2012) suggest that investors’ demand for information presses firms to seek an effective channel to disseminate firm-specific information.

The emergence of microblogging, such as Sina Weibo (hereafter Weibo) 1 in China, facilitates multiple-party dialog and interactions. The contents posted on Weibo are small messages, such as short sentences, 2 images, videos or web page links (Kaplan and Haenlein, 2011), allowing other users to add comments correspondingly and thus forming a live conversation stream. Weibo can circumvent the limitations of traditional media in a number of ways. 3 For example, unlike websites and newspapers, which usually do not provide any access restriction, Weibo allows users to control who can read their Weibo messages. In particular, only registered users can access the information. Furthermore, thanks to the affordability of portable consumer electronic devices and the advancement of information technology, the short nature of Weibo messages also allows users to post information quickly and reach their target audience in seconds. This makes Weibo a highly effective and efficient way of transmitting information to the targeted audience over traditional media. In fact, Weibo has experienced a boom, both in user numbers and information sharing activities in China in recent years. To make the best use of the wide popularity of Weibo, many firms and government organizations have set up an official Weibo account to stay connected with the investment community.

In principle, Weibo can improve the information environment via two mechanisms. First, firms may disclose new information on Weibo rather than on traditional media channels. In other words, the disclosure contains incremental information that is not available from other traditional channels. Second, disclosure via Weibo may disseminate information more broadly. Information diffusion is expected to be quicker with Weibo. Unlike in the United States where the U.S. Securities and Exchange Commission allows firms to use Twitter, Facebook, and other social media to disseminate important information, it is however illegal for firms in China to disclose new information on Weibo earlier than on the traditional channels. This is because, regardless of whether the traditional channels or Weibo are used, the China Securities Regulatory Commission (CSRC) requires that any disclosure via Weibo cannot be made earlier than the corresponding disclosure via the designated outlets and that the Weibo disclosure should not contain more information than those on the traditional channels. 4 In addition, CSRC also requires that disclosure cannot be done in a preferential or selective manner so that some market participants (such as security analysts and fund managers) can obtain information in advance. 5 It is noteworthy that though a firm may put up a news item via all possible media channels at the same time, it does not mean that investors will receive the news at the same pace. The fact that Weibo allows the news item to reach the targeted audience in seconds puts Weibo in a much better position over traditional media in information transmission, thus creating a strong incentive for investors, security analysts, and fund managers, and so on, to use Weibo to access the information quickly and effectively. This also means that even though the setting of China does not allow us to examine the first mechanism, it is still of great importance and interest to understand the role of the second mechanism, which our article aims to examine. 6

The stock market in China provides an interesting venue to understand the impacts of microblogging disclosure on the capital market. 7 First, it is well-known that unlike well-developed stock markets in the United States and United Kingdom where institutional investors play a dominant role in security trading, the Chinese stock market is dominated by retail or small investors (Ng and Wu, 2007). Retail or small investors are informationally disadvantaged, as they have limited access to information channels. Second, empirical studies also show that the role of security analysts in reducing the information asymmetry between firms and investors is quite weak in China (Feng and Li, 2011; Zhu et al., 2007). Third, since 2005, China’s split-share-structure reform has abolished the trading restrictions on shares mainly owned by state shareholders, making previously non-tradable shares owned by state shareholders legally tradable. As a result, these state shareholders have incentives to strengthen corporate governance and reduce the information asymmetry between the firm and investors as their wealth is now more sensitive to stock price movements (Hou et al., 2012). Putting a good corporate governance system in place can reduce agency costs, while information disclosure can provide investors with more relevant information to value a stock; both of them enhance firm value. One way to reduce information asymmetry is to transmit firm-specific news in a timely and effective manner. Bringing these factors together, it is not difficult to understand that on one hand, small investors are eager to find cost-effective way(s) to quickly access valuable information, while security analysts cannot satisfactorily fulfill their role; on the other hand, listed firms have incentives to reduce the information asymmetry problem by finding effective ways of information disclosure to small investors. Weibo seems to serve this purpose well.

As more and more listed firms set up their official Weibo account and use it as a disclosure channel in China, we are motivated to investigate whether the messages posted on the Weibo platform can improve the information environment in terms of the dissemination of firm-specific information, and whether the incremental information is useful for investors’ decision-making. To this end, stock price synchronicity (SYN) can be a good measure, as it measures how much firm-specific information is impounded into stock price. It is also interesting to differentiate the impacts of different types of Weibo information disclosure on SYN and to determine whether investors can benefit from them.

We hand-collect all the Weibo messages (i.e. tweets) published officially by the listed firms between 2011 and 2013. We examine the impacts of the amount of disclosures on SYN and find that synchronicity tends to be lower as firm-related disclosure increases. The relationship does not hold for disclosures that are unrelated to the firm. Furthermore, our results suggest that the number of Weibo fans intensifies the negative relationship between the number of firms’ Weibo tweets and SYN.

Our studies differs from three related previous studies. He et al. (2014) investigate the impact of firms’ launch of Weibo on their SYN and find that the establishment of an official Weibo account and the intensity of microblogging (i.e. number of tweets) help firms reduce SYN. Hu et al. (2016) show in the context of analysts’ earnings forecast in China that after a firm uses Weibo for information disclosure, analysts’ forecast revision becomes more frequent, average forecast errors become smaller, and stock price becomes more responsive to analysts’ forecasts. Hu et al. (2016) examine the role of Weibo in affecting analyst decision, but we extend their analysis by considering the mediating role of analysts in affecting SYN. In addition, we consider the role of Weibo fans as well. The focus of He et al. (2014) is whether firms with a Weibo account and the number of tweets affects SYN, we also examine whether different types of tweets (original tweets vs forwarded tweets, and whether or not tweets are firm-related) affect SYN. He et al. (2016) examine what determines the intensity of microblogging and find that corporate governance is an important determinant. In our study, we examine not only whether Weibo affects SYN but also how Weibo affects SYN.

We make the following three contributions. First, we extend studies on microblogging to examine its relationship with SYN. Previous studies focus on stock index price movement (Bollen et al., 2011), corporate profitability (Luo et al., 2013), stock price (Yu et al., 2013), and stock price liquidity (Blankespoor et al., 2014). Our results complement the literature on the effectiveness of Weibo by investigating how Weibo influences SYN. Second, we show that even in China where it is illegal for firms to disclose new information on Weibo earlier than on the traditional media channels, the information diffusion role of Weibo is still significant in determining SYN. Finally, we provide new evidence on firms’ voluntary disclosure in terms of microblogging. As an innovative channel to disseminate information, microblogging is relatively new to many users who are interested in direct communication with firms. Our research adds to the existing literature on voluntary disclosure and sheds light on the usefulness of microblogging in the stock market.

The remainder of the article is organized as follows. Section “Literature review” reviews the relevant literature, and section “Hypothesis development” develops our research hypotheses. Section “Methodology and data” describes our study design, sample, data source, and models. Section “Empirical results” discusses our empirical results, while section “Concluding remarks” concludes.

2. Literature review

2.1. Research on microblogging

Weibo, namely microblogging in Chinese, is a user-relationship-based platform for information sharing, communication, and access to the platform. Weibo users can set up individual communities through WEB, WAP, and a variety of clientele servers (Lee, 2011; Sun and Zhang, 2008). The general public can connect to the global knowledge network through the media by microblogging, providing information and sharing their own routes of transmission (Bowman and Willis, 2003). Weibo users are free to publish information in various forms, including text (140 characters), images, audio, video, and other short content. Any message published in Weibo is brief but can contain a large amount of information, and its release is faster than traditional paper/online media.

With the rapid growth of microblogging users, microblogging has become an important platform for firms wishing to disclose information. For example, Moe and Trusov (2011) find that firms can spread their brand quickly through the microblogging platform, allowing timely release of the latest information on their products, and significantly increasing their chance of communicating directly with consumers. As a result, information dissemination would be expected to be effective.

In recent years, research has started to examine the impact of microblogging information disclosure on firms and the capital markets. Traditional information disclosure often affects only a small section of investors, resulting in information asymmetry among different types of investors and lower market liquidity (Blankespoor et al., 2014). Compared to firms’ official announcements through newspapers and other traditional media, microblogging provides powerful interactivity, allowing firms to deliver timely information to more investors, thus reducing information asymmetry and bid-ask spreads of stock prices (Blankespoor et al., 2014). Bollen et al. (2011) found that microblogging sentiments (or emotions) can better predict the trend of the Dow Jones Industrial Average Index. The wider the microblogging audience coverage, the higher the frequency of customer access to microblogging and thus the higher the chance for them to buy the firm’s products, thereby increasing profitability (Luo et al., 2013) and enhancing the stock value of the firm (Yu et al., 2013).

There are two main approaches of understanding the relationship between microblogging tweets and stock market in the literature. The first one is to look at how stock market reacts to the arrival of tweets in terms of volume (or its variants) because increases in volume may indicate arrival of new information or aggregate information in the market. For example, Mao et al. (2012) found that the daily number of tweets that mention S&P 500 stocks is significantly correlated with S&P 500 daily closing price, price change, and daily absolute price change. Sprenger et al. (2014b) also found that tweet volume predicts trading volume. The second approach uses textual analysis to extract from tweets sentiments or information, which is found to be able to explain stock prices (Sprenger et al., 2014a).

2.2. Research on SYN

SYN measures the extent to which individual stock prices move with the stock market. Higher SYN indicates that stock price, on average, contains more market-wide information and thus less firm-specific information (Tang et al., 2011). Generally speaking, the more firm-specific the information disseminated by firms, the lower is their SYN (Durnev et al., 2003; Hutton et al., 2009; Jin and Myers, 2006; Morck et al., 2000). Early literature focuses on the impact of major legal systems on SYN. For example, Morck et al. (2000), using the country-level R2 statistic, found that the lower SYN in emerging markets is due to a lack of investor protection. Jin and Myers (2006), using the data of more than 40 countries, further validate the impact of investor protection in the institutional environment on stock price behavior. Chan and Hameed (2006) also found that the cost of information gathering is larger in emerging capital markets, where the law enforcement is not strong, information transparency of listed firms is poor, and there are a large number of family-owned firms. As a result, the stock price volatilities of both individual firms and the market have become similar.

Following Morck et al. (2000), many studies use firm’s SYN to measure the information content of the firm’s stock price. Li (2005) and Gul et al. (2010) examine the impact of corporate governance structure on SYN in the Chinese market. They found that, with increasing concentration of ownership, the tunneling behavior of large shareholders becomes more serious, thus leading to an increase in SYN. However, when the ownership concentration is above a certain threshold, the interests of large and small shareholders will converge, which will force firms to release more information in order to reduce information asymmetry, thus leading to a decline in SYN. You et al. (2006) found that the synchronization of stock price tends to weaken when the security systems gradually improve and the legal protection of investors strengthens. Tang et al. (2011) studied the relationship between SYN and political connections and found that political connections reduce firms’ incentive to disclose specific information, thus resulting in significantly higher SYN. They also find that the positive association between political ties and SYN exists only in regions where the degree of market development is low, government intervention is high, and the legal environment is poor. Piotroski and Roulstone (2004) found that insider trading improves the firm-specific information content of a stock price, as insider traders, who possess and trade on superior inside information about the firm, reveal this information to the market via their trading activities. Institutional investors may use their professional skills and social networks to collect private information on the firm and, therefore, institutional investors’ trading in the firm’s stocks may reveal firm-specific information and thus improve market efficiency (Hou and Ye, 2008). Zhu et al. (2007) found that analysts, using their expertise in information gathering and information processing, can make a stock price more informative about the firm’s fundamentals and thus improve its information content, resulting in the reduction of SYN. However, Feng and Li (2011) argue that security analysts in China often report less firm-specific information and more market-level information. They found that analyst coverage has a positive relationship with SYN. In short, the level of SYN depends mainly on the firm-specific information content of the stock price. If a firm has a high level of information opacity, its stock prices contain less individual information content, and thus, we would expect SYN to rise (Wang et al., 2009).

3. Hypothesis development

Information disclosure helps reduce information asymmetry (Beyer et al., 2010). In China, however, the information disclosure of publicly listed firms until recently was limited to traditional transmission outlets, which are specialty newspapers designated by the CSRC, such as “China Securities News,” “Shanghai Securities News,” and “Securities Times.” In recent years, this information disclosure monopoly has incurred criticisms that traditional paper media, due to the constraints of layout, printing time, and other factors, is likely to cause information asymmetry among different investors (Blankespoor et al., 2014). Furthermore, if investors question the content of the disclosed information, they cannot communicate with the firms in a timely manner due to the lack of interactivity of the traditional media.

With the rapid development of communication technologies, especially the popularity of online communications, the communication between firms and investors has reached a new level. The emergence of microblogging provides an additional interactive channel for information dissemination, which allows firms to, on top of the traditional media and other information intermediaries, communicate with investors directly and frequently in real time. Microblogging has several distinctive advantages over other information channels. First, firms have verified accounts, so users can trust the information in tweets from such sources. Second, microblogging allows each user to decide whom to follow, resulting in a self-moderation on the content. This creates a strong incentive for firms, for the purpose of investor relations, to publish valuable information to maintain or increase mentions, the rate of retweets, and their followership (Chang et al., 2008). Third, compared to traditional media, which can only publish news articles at distinct point in time, everyone can create and disseminate information on microblogs at any time (Sprenger et al., 2014b). Fourth, only current information is available from microblogging, making users exposed to the most recent information only. Fifth, tweets-forwarding (or retweet) function can help increase the audience of original tweets significantly and quickly. On the one hand, this function allows interaction among users which induces trading from “side-lined” investors when they learn that other users share a similar signal (Cao et al., 2002). On the other hand, even when there is a disagreement about the signal or information content, Das et al. (2005) suggest that this disagreement leads to extensive debate/discussion and the release of more information. This is because users can add information by generating entirely new content or interpreting existing content. Finally, Yang and Counts (2010) show that as tweets allow inclusion of a hyperlink to another website, it enhances greater information propagation. This set of distinctive features of microblogging addresses the deficiency of the long time gap between a firm’s official announcements and enriches the content of information disclosure. Potentially, it can expand the breadth of information disclosure, thereby improving the transparency level of the firm’s information. Information transparency, consequently, can reduce information asymmetry among investors and thus improve the quality of their evaluations of the firm. Information transparency is therefore expected to improve the firm-specific information content of stock prices, making stock prices more (less) responsive to the firm-related (market-wide) information and, therefore, resulting in a reduction in SYN (Hutton et al., 2009; Jin and Myers, 2006; Morck et al., 2000). Based on the above analysis, we develop our first research hypothesis.

H1. Information disclosure by listed firms through Weibo increases the firm-specific information content of stock price, thus lowering SYN.

As discussed earlier, users of microblogging are no longer just passive information receivers as in the traditional media. They become actively involved in information selection and dissemination because their search, action, and sharing activities on microblogging present a positive interaction, which, in turn, helps them learn, solve problems, or make decisions. For example, microblogging fans not only receive information about an object of interest through microblogging, but also disseminate relevant information through the microblogging’s forward functions. These forward functions, without the active involvement of the fans, cannot facilitate the transmission of information broadly and effectively. In other words, it is the active involvement of the fans that helps improve the information dissemination. Thus, given the fact that these forward functions are always available on Weibo, it is not unreasonable to expect that the higher the number of fans of a listed firm’s official microblogging, the more extensive the coverage of its firm-level information disclosure, and the more firm-specific information its share price will incorporate, thus reducing SYN. Based on the above analysis, we formulate our second research hypothesis.

H2. Increasing the number of fans following a firms’ official Weibo strengthens the negative association between Weibo information disclosure and SYN.

Security analysts, as an intermediary in the information markets, have a wide range of information-gathering and dissemination channels, as well as a wealth of financial and other professional knowledge, and they use this knowledge to participate actively in the transfer and adoption of the information of listed firms. They collect a range of information through comprehensive consolidations, evaluations and analyses, report earnings forecasts, and recommend stocks, as well as expressing their views publicly on television, newspapers, and other media, so that the information can be transmitted more rapidly and extensively to investors. Despite Lepone et al. (2012) show that investors’ access to analyst reports is far from even, analyst coverage is considered by listed firms as a way to disclose information on the magnifying glass (Knyazeva, 2007). The intermediary role played by analysts helps improve the speed and breadth of information transfer for listed firms, enabling investors with poor information-gathering ability to obtain timely information on listed firms. Therefore, the more the analyst coverage, the faster the dissemination of information and the greater the relevance of the information investors can gather to make informed investment decisions, thus increasing the chance that this information will be reflected in share prices.

Hu et al. (2016) show in the context of analysts’ earnings forecast in China that after a firm uses Weibo for information disclosure, analysts’ forecast revision becomes more frequent, average forecast errors become smaller and stock price becomes more responsive to analysts’ forecasts. This evidence is consistent with the view that analysts may gather useful information from firms’ official Weibo. By comparing the official announcements disclosed through microblogging and information from other sources, analysts can filter and pass on relevant information to investors, so that information can be better disseminated in the market and thus better reflected in stock prices. Based on the above analysis, we develop the third research hypothesis.

H3. Increasing analyst coverage strengthens the negative association between information disclosure by listed firms through Weibo and SYN.

4. Methodology and data

4.1. Measure of SYN

Following Roll (1988), we use the market model to decompose firms’ total return variations into two components: those related to common (market-wide and/or industry-wide) factors and those related to firm-specific factors. SYN is simply measured as the ratio of the common factor variation to the total return variation. To construct SYN at monthly level, we first estimate the following market model for each firm in each day

where RETid is the stock return of firm i (A-share traded on either the Shanghai Exchange or Shenzhen Exchange) on day d; MKTRETd and MKTRETd–1 (INDRETd and INDRETjd–1) are the value-weighted A-share market return (daily return of the industry firm i) on dth and d–1th days, respectively,

8

and

Our definition of SYN is based on R2 for the market model used. To circumvent the bounded nature of R2 within [0, 1], we use a logistic transformation of R2

SYNid is the synchronicity index of firm i’s share price on day d. To compute the monthly SYN, we take a weighted average of daily SYN where the weighting

4.2. Regression models and variable definition

To test for the effects on SYN of information disclosure on Weibo, financial analyst coverage and fans of Weibo, we estimate the following regressions

where the key variable of interest is Blog which refers to the number of tweets on a listed firm’s official Weibo. To minimize the concern of large discrepancies of the number of tweets across sample firms and also to distinguish whether a sample firm has set up a Weibo account, we use ln(1 + the number of tweets) instead. Given the popularity of the forward functions of microblogging, many listed firms’ Weibo may contain forwarded tweets that have not much substantial original content therein. It is noteworthy that the microblogging content of firms varies widely. Some firms’ official Weibo accounts often just release irrelevant information such as “Chicken Soup for the Soul” or “Weather Forecasting.” For example, the People’s Daily in 2013 issued 16,689 Weibo tweets but, after a closer check, we found that only 19 tweets, or 0.11%, are related to the firm itself. Therefore, simply using the number of Weibo tweets may pose a potential research bias, as investors value only those Weibo tweets that contain firm-related news. If a tweet has nothing to do with the firm, whether it is an original tweet or a forwarded one, it has no incremental value to investors and thus no impact on SYN. To solve this issue, we also use ln(1 + the number of firm’s original tweets) and ln(1 + the number of firm’s forwarded tweets) to serve as alternative measures of information disclosure with Weibo. If the firm’s Weibo can play the role of information disclosure, we then expect the coefficient on

In Equations (or) Models (4) to (6), we also include a control variable called media coverage (Media), defined as the number of news items published in the important newspapers during the day. We use this variable to control for the impact of traditional media channels on SYN. We collect the data from Infobank, a popular newspaper database in China. To control for unobserved heterogeneity and time effects, we also include firm-fixed effects

To test H1, we specify Model (3); we also specify Models (5) and (6) to test for H2 and H3, respectively. The statistical significance of the interaction variable provides direct evidence to support H2 or H3. In Model (5), analyst coverage (Analyst) is measured as the natural logarithm of one plus the number of financial analysts following the firm’s Weibo. In Model (6), “Fans” refers to the number of fans following a firm’s official Weibo, which is measured as ln(1 + number of fans).

4.3. Data source

The number of microblogging tweets per month is hand-collected from Sina Weibo. To enhance the validity of our measure of official microblogging information disclosure, we collect only from the official microblogging of listed firms, which have been authenticated by Sina Weibo as V-plus registered users. Neither do we include the microblogging of controlling shareholders, subsidiaries or affiliates of listed firms, or individuals who assume a managerial role in the firm.

Our sample covers the period 2011–2013. Sina Weibo started its service in August 2009, and only a few listed firms had an official Weibo account before 2011. Through reading Weibo contents, we hand-collect firm-related tweets, that is, those tweets related to the firm’s business, finance, R&D, reputation, and so on. Some firms, for example Fuxing Pharmaceutical, though having registered a Weibo account, have never released any information on Weibo. We simply delete these firms from our sample. The final number of listed firms in our sample includes 610 firms with 5057 firm-month observations with tweet news, and 5651 firms with 71,048 firm-month observations without tweet news.

For financial data, we use the CSMAR database and the WIND database. We apply the following sampling filters: (1) we exclude financial and insurance firms; (2) we exclude firms with less than a 1-year post-IPO age; (3) we exclude firms with missing financial data. Monthly data are used. After applying the filters, we end up with 2351 firms with 76,105 firm-month observations. To mitigate the potential impact of extreme values on our findings, we winsorize at the 1% level on both sides for all the variables.

5. Empirical results

5.1. Descriptive statistics

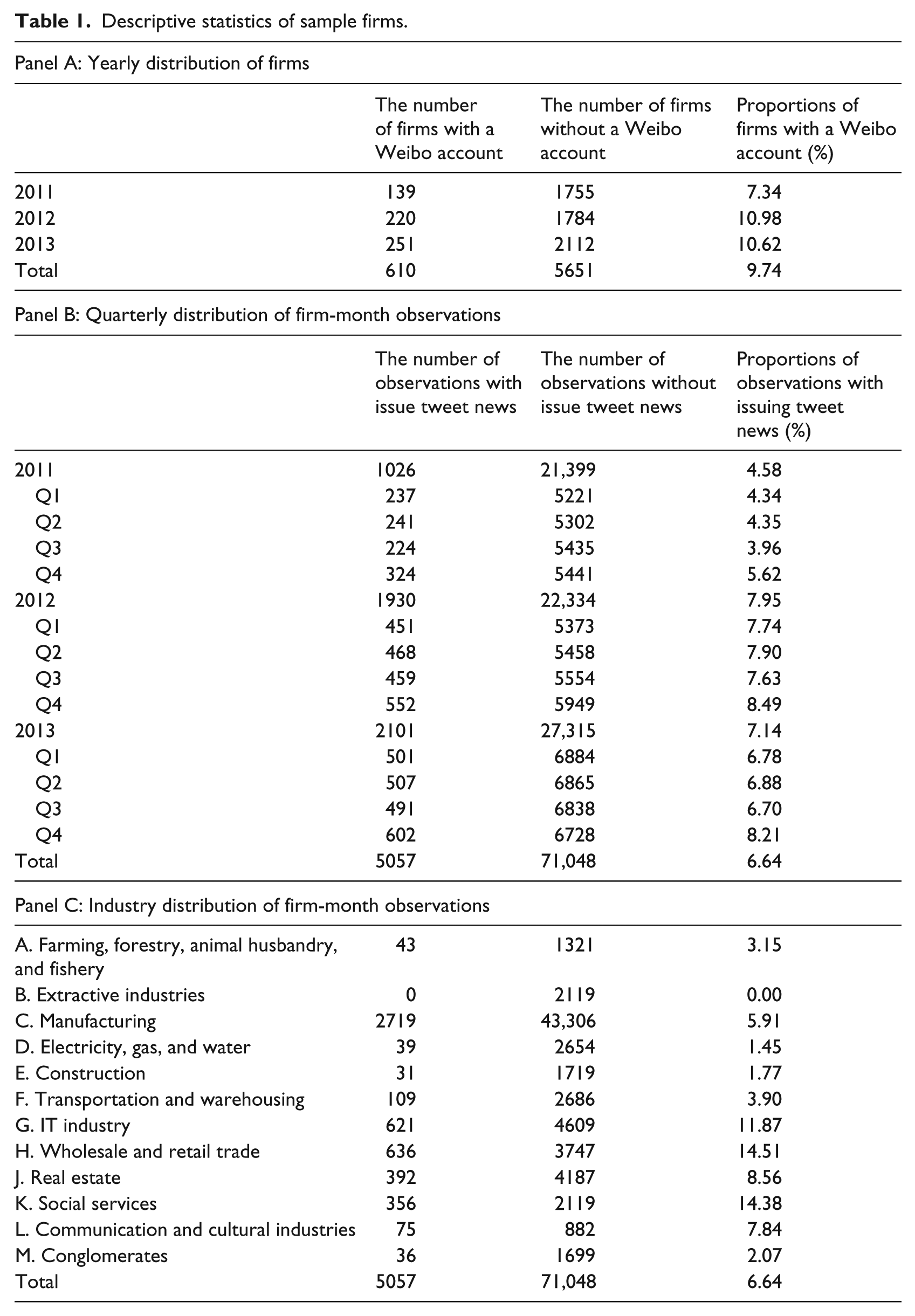

Table 1 provides descriptive statistics for the sample firms. Panel A reports a summary of the firms with/without a Weibo account for each year in the sample period 2011–2013. In 2011, there are 139 listed firms that have registered a Weibo account, representing 7.34% of the total sample, while in 2013, there are 251 listed firms having a Weibo account, accounting for 10.62% of the whole population of listed firms. Overall, the number of listed firms in China that have a Weibo account is still small (i.e. 9.74%). In Panel B, we report a summary of the firm observations for firms with/without a Weibo account in each quarter in 2011–2013. It shows that the distributions of the number of firms in all the quarters are similar for each year. Panel C reports the industry distribution of the firm observations for those firms that have a Weibo account. While the manufacturing sector accounts for the lion’s share (2719 firm-month observations), it is only 5.91% of all the firm-month observations in this sector. In contrast, the observations associated with the firms with a Weibo account in the wholesale and retail trade sector represent 14.51%, while no firm from the extractive sector has an official Weibo account.

Descriptive statistics of sample firms.

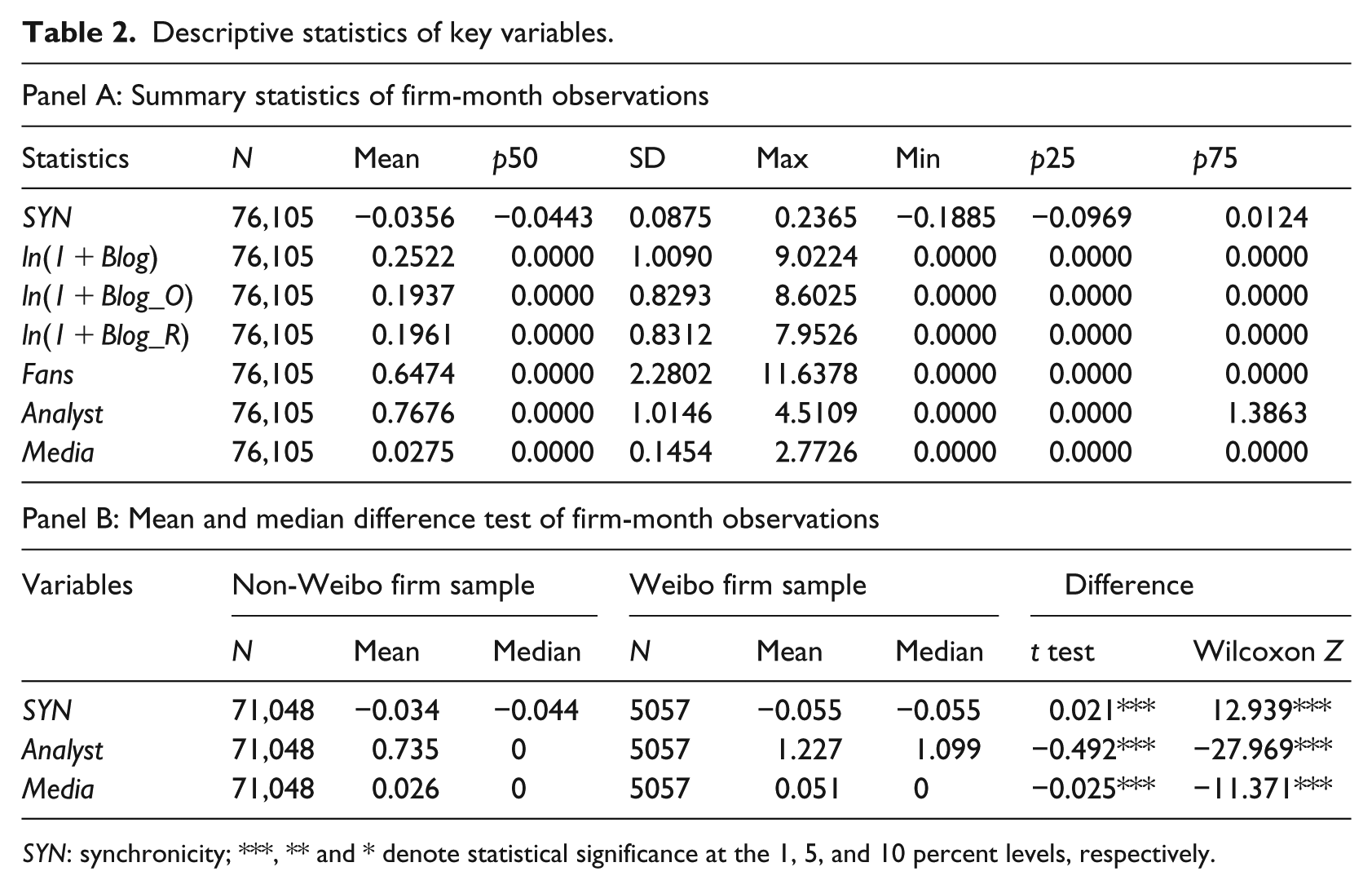

Table 2 reports descriptive statistics for the key variables used in our study. Panel A of Table 2 shows that SYN has a mean of −0.0356 and a median of −0.0443, respectively, and this suggests that the distribution of SYN is not quite symmetric. The average number of tweets per month is 1.2969 (= exp(0.0124)), while the maximum number is 8286.64 per month. With regard to the three Weibo information release measures (i.e. ln(1 + Blog), ln(1 + Blog_O), and ln(1 + Blog_R)), they have averages of 0.2522, 0.1937, and 0.1961 and standard deviations of 1.0090, 0.8293, and 0.8312, respectively, revealing that these three measures can capture different aspects of firms’ information dissemination via Weibo. Media coverage (Media) is over-dispersed, as its average coverage and standard deviation are 0.0275 and 0.1454, respectively. For the number of the fans of a firm’s official Weibo, the monthly mean and standard deviation are 0.6474 and 2.2802, suggesting that some firms have very few fans while others have a very large number. For analyst coverage (Analyst), the daily mean is 0.7676, indicating that the number of times the firm is followed by different security analysts in a month is 2.15 times. These figures indicate that some of the sampled firms are not well followed, while others are always catching the eyes of security analysts.

Descriptive statistics of key variables.

SYN: synchronicity; ***, ** and * denote statistical significance at the 1, 5, and 10 percent levels, respectively.

Panel B of Table 2 reveals that there is a significant difference in the mean (or median) of SYN, analyst coverage and media coverage between firms with a Weibo account and those without a Weibo account. More specifically, the former tends to have a lower SYN but a higher analyst coverage and media coverage than the latter.

Table 3 shows the correlations between the main variables. As is consistent with our research hypotheses, Table 3 clearly demonstrates that the number of tweets (ln(1 + Blog)), the number of original tweets (ln(1 + Blog_O)) and the number of forwarded tweets (ln(1 + Blog_R)) are significantly negatively related to SYN. This is consistent with the view that when firms use a Weibo account, investors can obtain broader and/or more in-depth firm-specific information, which results in a stock price containing more firm-specific information, and thus a lower SYN. Similarly, the number of microblogging fans (Fans) is also correlated significantly negatively with SYN, suggesting that, with a larger number of fans, firms can more quickly disseminate firm-specific information, thus lowering SYN. The variable Media is also negatively correlated with SYN. In fact, Fan has the strongest correlation with SYN among the main variables.

Correlation matrix.

***, ** and * denote the correlations that are significant at the 1%, 5%, 10% levels, respectively.

5.2. Main regression results

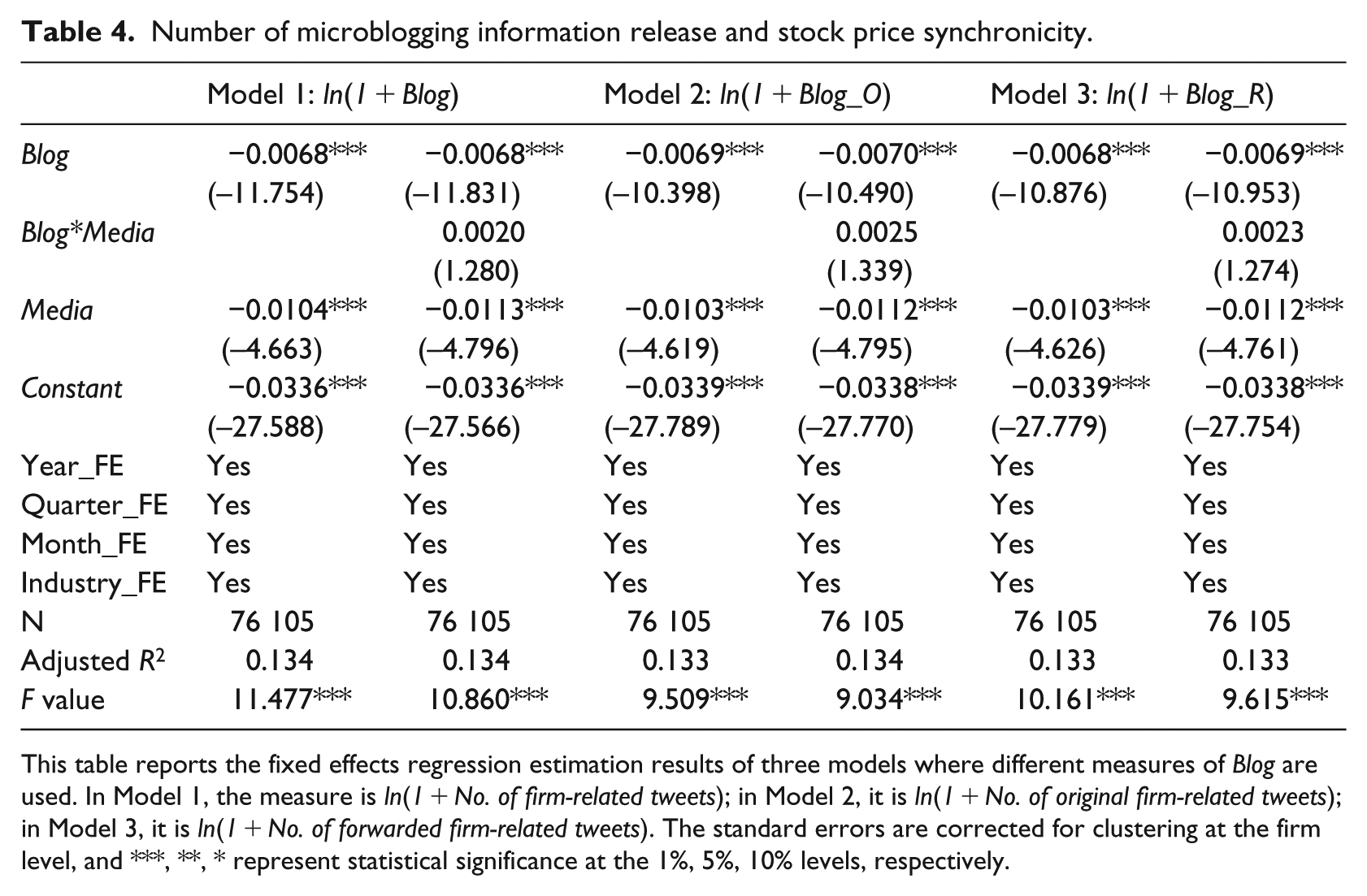

We specify a baseline regression where the three different measures of Blog are used. They are ln(1 + number of firm-related tweets), ln(1 + number of original firm-related tweets), and ln(1 + number of forwarded firm-related tweets) which are labeled as ln(1 + Blog), ln(1 + Blog_O) and ln(1 + Blog_R) in Models 1, 2 and 3, respectively. The baseline results are presented in Table 4.

Number of microblogging information release and stock price synchronicity.

This table reports the fixed effects regression estimation results of three models where different measures of Blog are used. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

Table 4 shows a significantly negative association between firms’ official Weibo tweet number and SYN, which is stable across all regressions; all regression coefficients keep their statistical significance and there are no changes of sign regardless of the measure of tweet number used. In particular, the coefficient on Blog in Model 1 is −0.0068 and statistically significant at the 1% level. This indicates that the breadth of a firm’s official Weibo is beneficial for the dissemination of information. We find that the higher the number of original Weibo tweets, the better is the information that the stock price carries and thus the lower will be the SYN. The coefficient on Blog is even slightly larger if Blog is measured as original tweets; the coefficient is now −0.0069. In other words, tweets that are high in information content, such as those original tweets, can lower SYN further. This result is consistent with the view that investors are more concerned about those Weibo tweets and forwarded tweets that are firm-related, probably because investors can use such information to make better investment decisions which, in turn, results in the incorporation of more firm-specific information into the firm’s stock price and thus a lower SYN.

The impact of Media is also statistically significant and negative; furthermore, the size of the coefficient on Media is larger than that of Blog, suggesting that traditional media plays an even more important role in determining SYN than Blog. As both Blog and Media are negatively related to SYN, this suggests that the number of tweets released via Weibo or news items published in major newspapers both contribute to the reduction in SYN.

To investigate whether Weibo can provide a channel in addition to the traditional one (i.e. the designated newspapers), we include an interaction term Blog*Media in the regressions. The results, also reported in Table 4, show that the interaction term is not statistically significant at the 10% level for all three Blog measures. This suggests that information released via Weibo has an additional but independent effect beyond the traditional newspaper outlet; that is, more tweets with firm-related information further reduce SYN.

Table 5 shows the regression results for Blog’s interaction with Fans. After including the variable Fans and the interaction term Fans*Blog, both the coefficients on Blog and Media are still statistically significant at the 1% significance level, but the coefficient on Blog*Media remains statistically insignificant. The coefficient on Fans is not significantly different from zero, but the coefficient on the interaction term Fans*Blog is significantly negative, which indicates that an increase in the number of fans can reinforce the negative relationship between the number of Weibo tweets and SYN. The higher the number of fans, the more likely the forwarding function will be used, so that more Weibo users will receive the relevant information, thus leading to higher breadth of the spread. If more firm-level information is disseminated widely to investors, the stock price will contain more firm-level price information, resulting in a lower SYN. Similarly, the regression results for Models 2 and 3 also show that an increase in the number of fans is conducive to a strengthening of the negative relationship between the number of Weibo tweets and SYN. We also include the interaction term Blog*Media into the regressions, but the coefficient on this interaction term is not statistically significant. The evidence that the coefficient on Blog*Fans is statistically significant while that of Blog*Media is not, is intuitive—it is Fans rather than Media that is the channel through which Blog influences SYN as Fans alone does not affect SYN if Blog is not available.

The impact of fans on the relationship between Blog and SYN.

This table reports the fixed effects regression estimation results of three models where different measures of Blog are used. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); and in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

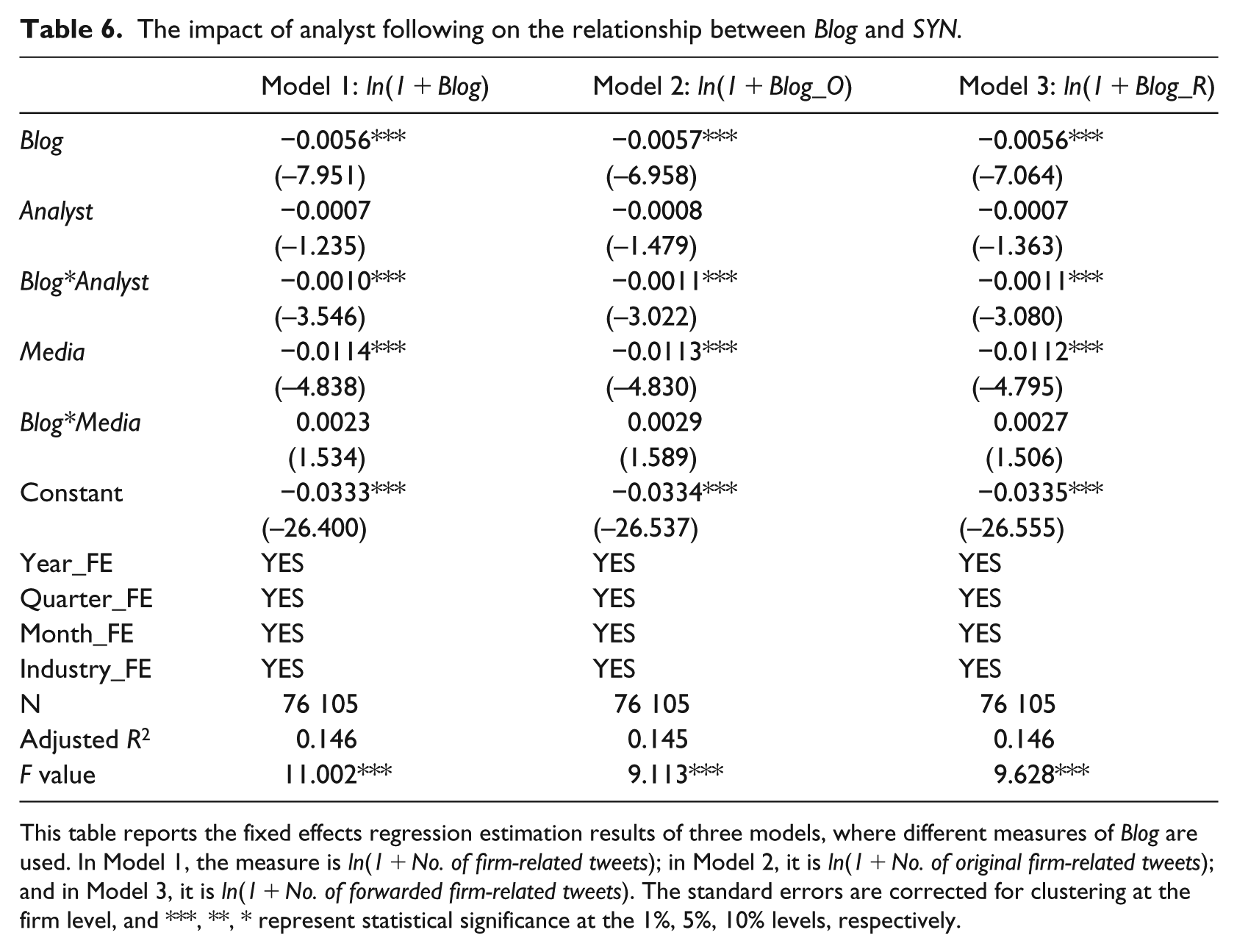

Table 6 shows the regression results for Blog’s interaction with the number of analysts following (Analyst). First, there is no statistically significant relationship between Analyst and SYN, suggesting that analyst coverage does not influence SYN. Second, analyst coverage (Analyst) can strengthen the relationship between Blog and SYN. For example, in Model 1, the coefficient on the interaction term Analyst*Blog is statistically significantly negative (–0.0010). This implies that when the size of the analyst following is zero (or equivalently, when Analyst takes the value of one), the actual relationship between the number of Weibo tweets and SYN is negative (i.e. –0.0056). However, when the size of the analyst following is large (say, 4.5109 or its max value), the relationship can change from −0.0010 to −0.0101 (= −0.0056 + (–0.0010 × 4.5109)). This suggests that analyst coverage and interpretation of relevant information enhance the incorporation of firm-specific information into stock prices and thus strengthen the negative association between the number of Weibo tweets and SYN. Similarly, Models 2 and 3, where the original tweet number and forwarded tweet number are used, yield similar results. In particular, the coefficient on Blog*Analyst here is still negative and statistically significant.

The impact of analyst following on the relationship between Blog and SYN.

This table reports the fixed effects regression estimation results of three models, where different measures of Blog are used. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); and in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

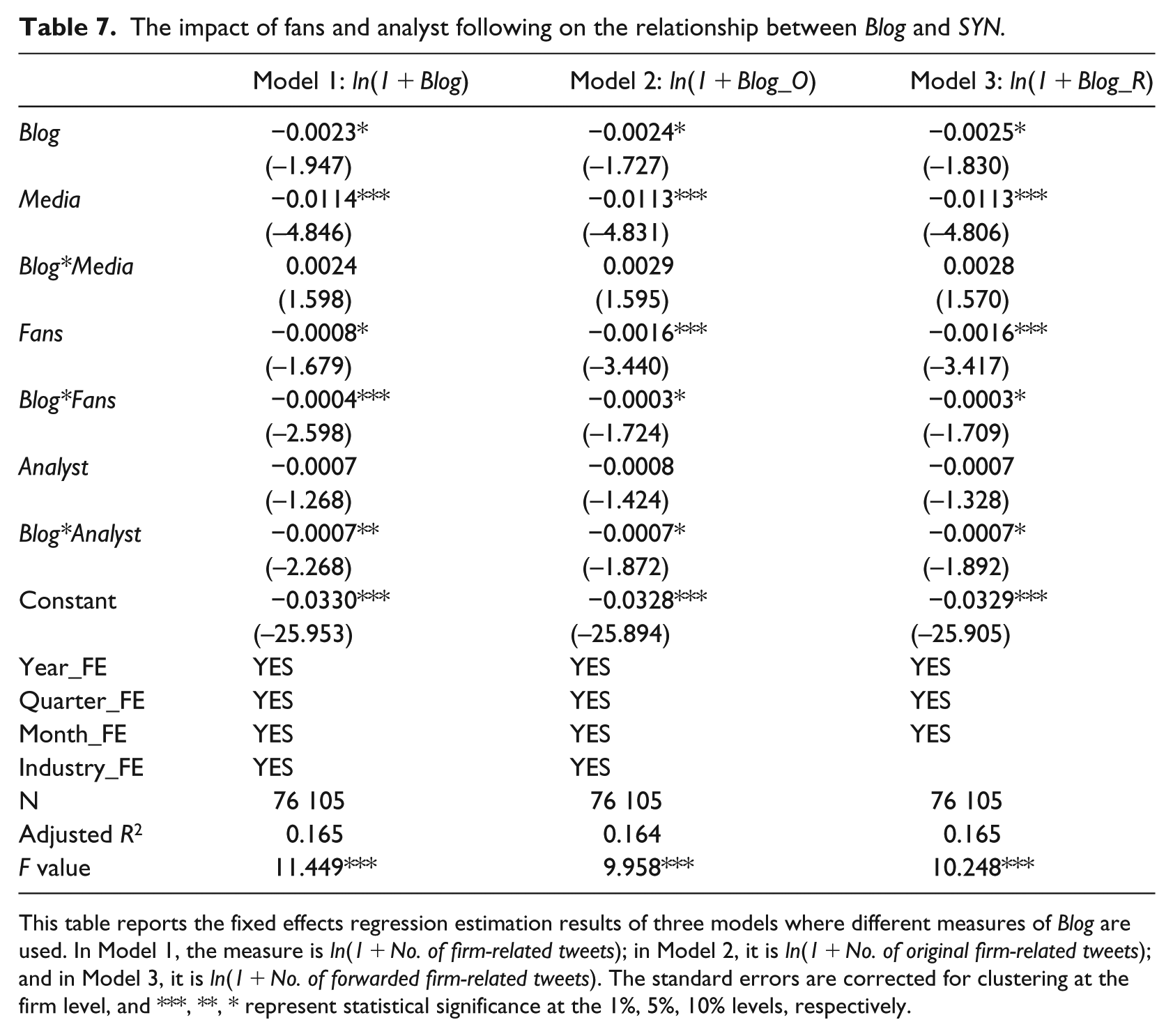

As both Fans and Analyst serve a similar role of enhancing the incorporation of firm-specific information into stock prices by utilizing information from Weibo tweets, it is interesting to understand whether their role is complementary or substitutive. Table 7 reports the regression results for the interactions of Blog with Fans and with Analyst. Similar to the results reported in previous tables, the main effect of Blog, Fans, and Media are negative and statistically significant, while that of Analyst is not. In addition, the interaction variable between Blog and Media is still not statistically significant, but the coefficient on Blog*Analyst and Blog*Fans are still significant. This evidence seems to suggest that even though Fans and Analyst may serve the similar role of enhancing information diffusion, the role of Fans seems to be substitutive for that of Analyst because the role of Analyst is no longer significant in the presence of Fans. However, there is a relatively more important role for Analyst to play in the presence of Blog. This is because the coefficient on the interaction variable Blog*Analyst is always larger than that on Blog*Fans, no matter what Blog measures are used. This implies that the role of Analyst is more important when compared to that of Fans.

The impact of fans and analyst following on the relationship between Blog and SYN.

This table reports the fixed effects regression estimation results of three models where different measures of Blog are used. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); and in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

5.3. Robustness checks

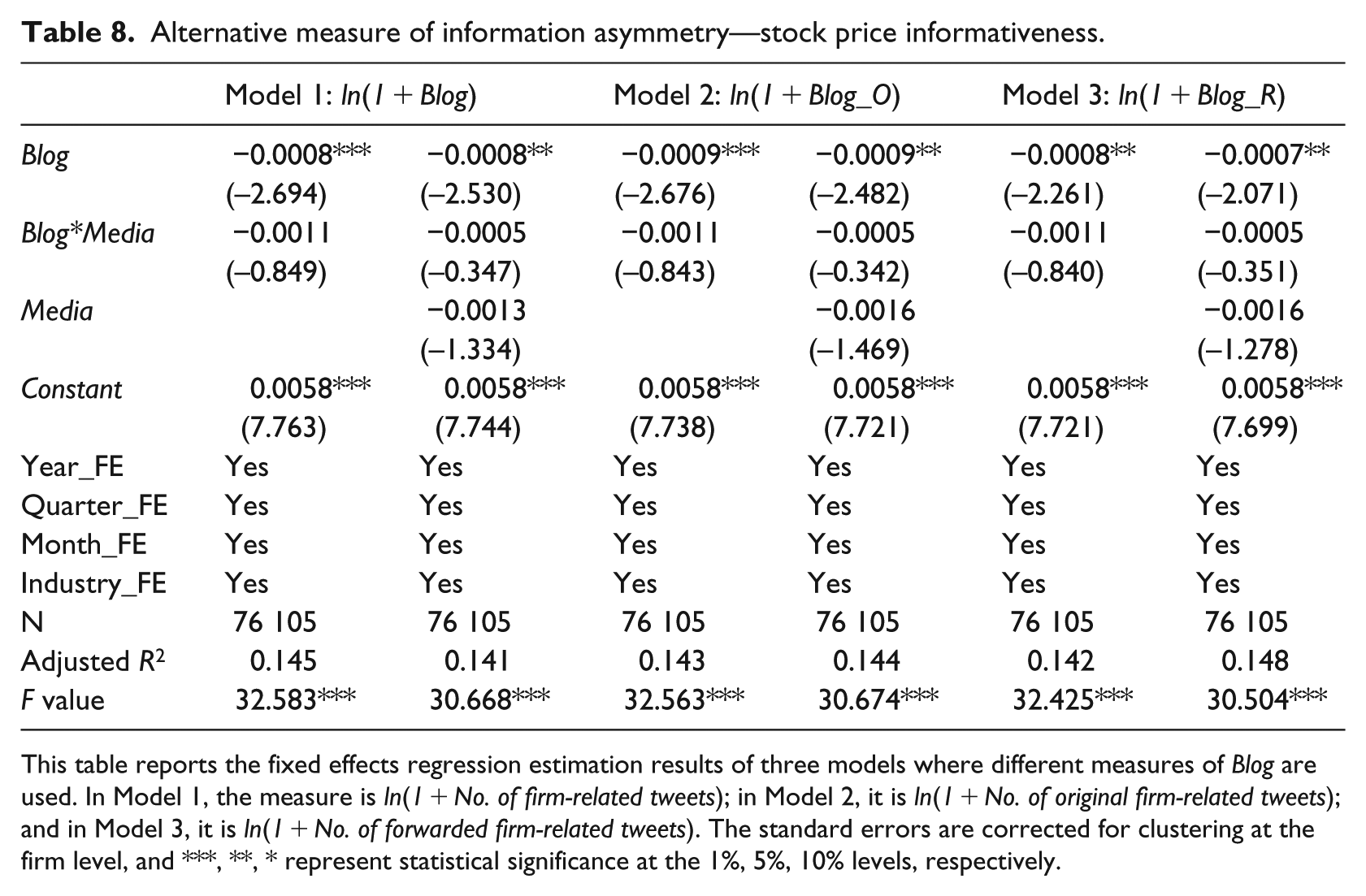

5.3.1. Alternative measure of SYN—stock price informativeness

One may argue that lower R2 actually means “less informative stocks” (Devos et al., 2015; Li et al., 2014). To circumvent this issue, we use a measure of “stock price informativeness” as the main variable to test the results, as Chan and Chan (2014) show that stock price is more informative when stock return synchronicity is higher. To construct this measure at monthly level, we first use daily returns and trading volume to analyze the impact of information asymmetry on the dynamic volume-return relation based on (Llorente et al., 2002) approach

According to (Llorente et al., 2002)

We use daily turnover as a measure of trading volume

Similarly,

The results, shown in Table 8, indicate that the coefficient on Blog is statistically significant and negative with information asymmetry in all of the three models. Thus, those additional analyses provide further evidence that Weibo disclosure increases the information transparency of those firms, resulting in the decrease (increase) in information asymmetry (stock price informativeness). However, the coefficients on Media and its interaction with Blog, Blog*Media, are not significant.

Alternative measure of information asymmetry—stock price informativeness.

This table reports the fixed effects regression estimation results of three models where different measures of Blog are used. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); and in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

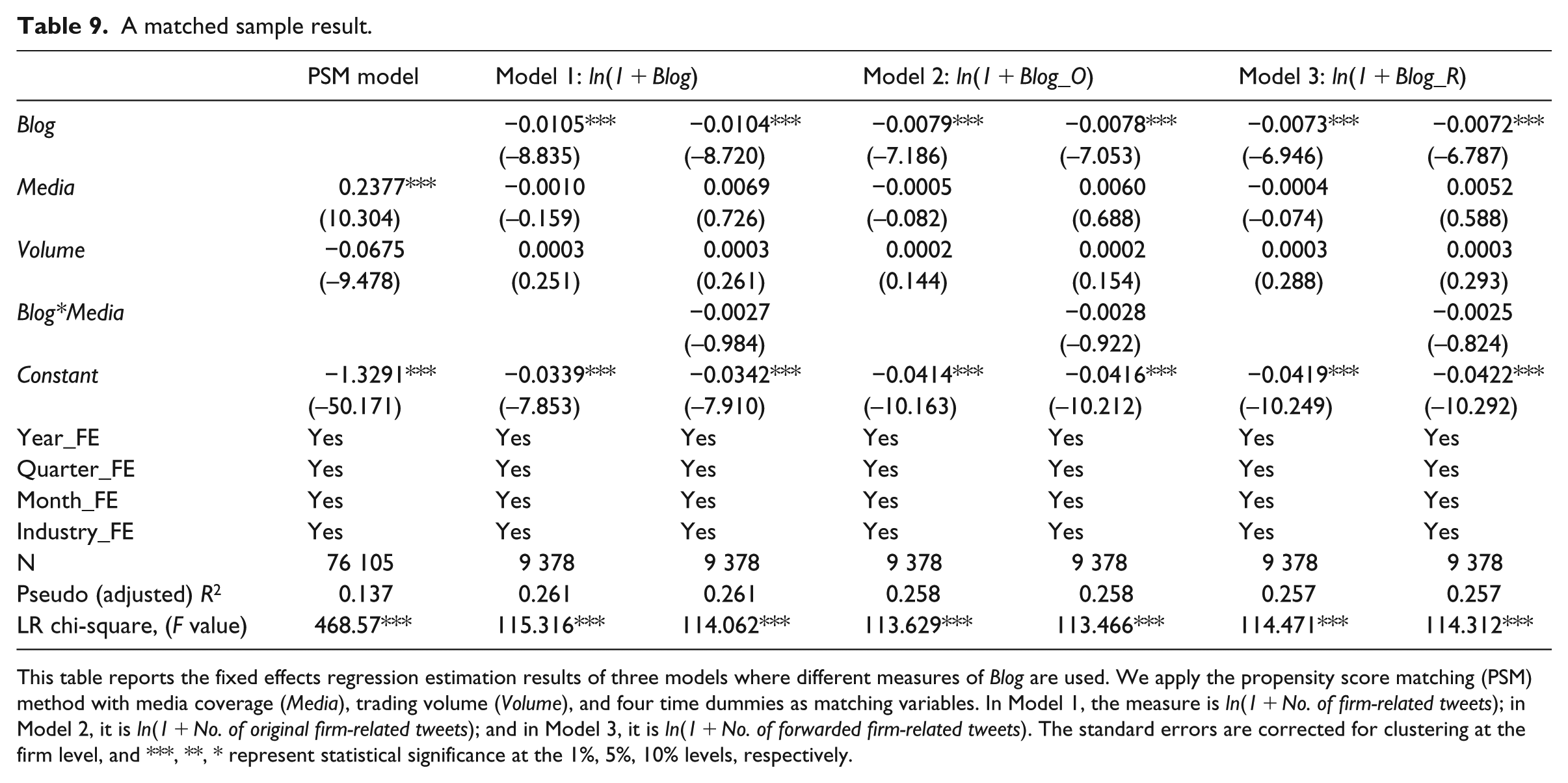

5.3.2. Matched sample analysis

As the full sample contains only those observations with Weibo information disclosure, accounting for only 6.64% of all firms, there is an imbalance between the number of firms with Weibo and the number of those without Weibo, which gives rise to reasonable doubt as to the representativeness of the sample. To mitigate this concern, we use a matching sample technique called propensity scores method (PSM) to choose 71,048 non-Weibo observations, as the matched sample based on media coverage, trading volume, and time dummies, including year, quarter, and month effects. Table 9 reports the fixed effects regression results for the matched sample for different measures of Blog. No matter what measure of Blog is used, Table 9 shows that the number of tweets is still negatively related to SYN, confirming the previous findings. In other words, using Weibo helps expand the breadth and depth of information disclosure, resulting in the firm’s stock price incorporating more firm-specific information and thus leading to a decline in SYN. The coefficient on Media is positive and statistically significant only in the case where Blog is absent; it is not significant in other cases, and neither are the coefficients on the interaction term Blog*Media. The results are consistent with Table 4. Furthermore, we conducted the Average treatment effect among treated (ATT) test of PSM and found that the average value of SYN in the treated group is −0.0879, while the average value of SYN in the control group is −0.0631; the treated group has a value of 0.0248 lower than the one in the control group and this difference is statistically significant (t-statistic = –3.70).

A matched sample result.

This table reports the fixed effects regression estimation results of three models where different measures of Blog are used. We apply the propensity score matching (PSM) method with media coverage (Media), trading volume (Volume), and four time dummies as matching variables. In Model 1, the measure is ln(1 + No. of firm-related tweets); in Model 2, it is ln(1 + No. of original firm-related tweets); and in Model 3, it is ln(1 + No. of forwarded firm-related tweets). The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively.

5.3.3. Controlling for endogeneity

The finding of a negative association between the number of microblogging tweets and SYN might be driven by some unobserved common factors that affect both firm decisions to use Weibo and SYN (He et al., 2016). To address this potential endogeneity issue, we use a two-stage least squares (2SLS) method.

We use the number of tweets of previous month as an instrument. Due to the random arrival nature of news, this variable is expected to directly affect Weibo information release only, but not SYN, and consequently it can serve as a good instrumental variable (IV) to solve the endogenous issue that may affect the relationship between Weibo information disclosure and SYN.

We first run a regression as per the specification of Equation (8), where the impact of Media and the IV on the number of Weibo tweets (Blog) is estimated. We then obtain and use the predicted Blog

Table 10 reports regression results for the impact of Weibo information release on SYN after controlling for the endogeneity problem. Columns 1, 5, and 9, respectively report the results of the first-stage regression to check whether the instrument is relevant and does not suffer from any weak-instrument problem. In accord with our expectation, the first-stage regression results show that the firm’s Weibo information release is related to its Weibo information release in previous month; the coefficient on

2SLS results.

This table reports the 2SLS estimation results for three models where different measures of Blog are used. In Model 1, the measure is ln(1 + Blog); in Model 2, it is ln(1 + Blog_O); and In Model 3, it is ln(1 + Blog_R). Blog refers to the number of tweets, while Blog_O and Blog_R stand for the number of original tweets and the number of forwarded firm-related tweets, respectively. The instrument is Blog in previous month. The standard errors are corrected for clustering at the firm level, and ***, **, * represent statistical significance at the 1%, 5%, 10% levels, respectively. KP (CD) stands for Kleibergen-Paap, (Cragg-Donald) and the number in bracket for these two tests refer to the Stock–Yogo critical values at 10%.

Columns 2, 6, and 10 report the second-stage regression results (i.e. the impact of Weibo information disclosure on SYN after controlling for the endogeneity problem). The results show that the number of Weibo tweets (Blog) is still associated with SYN negatively. Firms’ publishing of relevant information through Weibo can improve the breadth and depth of information disclosure, resulting in more firm-level information reflected in the firm’s stock price and thus a decline in SYN. The coefficient on Media is still negative and statistically significant, while the interaction term, Blog*Media, is not significant in any of the second-stage regressions. This result further corroborates our earlier findings. 9

6. Concluding remarks

No longer passive recipients of information statutorily disclosed by listed firm, investors are increasingly wishing to engage in active and effective dialog with firms. The emergence of microblogging (e.g. Weibo) provides a platform for communication between firms and investors, allowing firms to deliver timely information to a broad base of investors in an effective way.

Using hand-collected data on the microblogging contents of firms’ official Sina Weibo accounts for the period 2011–2013, we analyze the relationship between the magnitude of official microblogging disclosure and SYN in China. After controlling for the impact of traditional media, we find that the number of tweets on listed firms’ official Weibo is negatively associated with SYN, suggesting that the firm-level information from Weibo tweets is incorporated into stock prices. There is no evidence that information disclosure via Weibo interacts with the one via traditional media. Taken together, the results are consistent with the view that Weibo provides an additional channel other than traditional media firms may use to publicize information to investors. We further find that the number of Weibo fans can strengthen the negative association between the magnitude of microblogging disclosure and SYN. This lends support to our Hypothesis 2 but not to Hypothesis 3. These findings are robust to alternative measures of SYN and microblogging disclosure as well as to the endogeneity problem.

Our study has an important policy implication. Consistent with Chang et al. (2008), our finding suggests that microblogging disclosure of official information content can reduce information asymmetry between investors and firms because firms can establish an effective investor relation program by disclosing more firm-relevant information via official microblogging. Meanwhile, the regulators may wish to revise relevant provisions to encourage listed firms to use microblogging and other social media to disseminate information, thereby helping increase the breadth of information disclosure, reduce SYN, and enhance the efficiency of capital markets.

Our research is based on the information view that Blog enhances investor’s decision by reducing information asymmetry (Solomon et al., 2014). But there is another view called the salience view that Blog merely shifts investor attention across securities, causing a transitory increase in investor demands for stocks in the news (Daniel et al., 1998; Hong and Stein, 1999). Our measure of tweets is volume-based and does not allow us to examine this alternative view adequately. Future research might consider using textual analysis to extract sentiments or information content from tweets and examine how they affect SYN and whether there is a transitory increase in investor demands in China.

Footnotes

Final transcript accepted 25 July 2018 by Kathleen Walsh (AE Finance).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Zhou acknowledges the financial support provided through the Fund of the National Natural Science Foundation of China (No. 71462012; 71462011).