Abstract

Iwi, the tribal entities of the Māori people of Aotearoa New Zealand, now manage billions of dollars, a task requiring increasing sophistication in their investment strategies. Asset classes of Iwi have evolved from the properties, fisheries quotas, and cash they received through Aotearoa New Zealand’s Treaty settlement process to now include major investments in private equity, infrastructure, and other financial assets. The literature has, however, been largely silent on Iwi investments. Performance discussions tend to emphasize a western approach focusing on traditional financial performance measures. Using Waikato-Tainui operated Tainui Group Holdings (TGH) as an example, we analyze a sample of corporate disclosure documents. We find the intent of tribal (Iwi) investment firms may not be adequately captured through traditional investment frameworks and classic performance metrics. Drawing parallels between Iwi investment firms and impact investing widens the scope for financial managers to think differently about how we quantify Indigenous investment performance.

1. Introduction

The total value of the Māori asset base in 2013 was estimated to be NZ$42.6 billion (BERL, 2013). 1 With a total of 75 Treaty settlements 2 completed since 1992 and more to come from ongoing settlement negotiations between Iwi 3 and the New Zealand government, the Māori asset base is expected to continue growing. Treaty settlements to date are worth NZ$2.3 billion and have grown to an estimated NZ$9.2 billion (Smellie, 2018; TDB Advisory, 2019). While the settlements represent a fraction of total assets under management for Iwi (tribe), they have contributed to the growing economic power of Māori. These settlements require investment and management, and they will continue to shape the future of Iwi, and demand sophistication in the investment approach.

In the 28 years since the first Iwi received their Treaty settlement, significant assets have been returned to Māori, enabling them to become significant players in New Zealand’s financial industry. However, the literature around Iwi investments remains sparse. Māori assets, specifically, land, fisheries, forests, and other treasures are collectively held and managed by each Iwi 4 (Lashley, 2000). Studies have focused primarily on how the land and fisheries assets have been utilized (Awatere et al., 2014; Clarke-Nathan, 2016; Edwards, 2010; Findlay, 2000; Mataira, 2000; Sullivan and Margaritis, 2000). The bulk of the literature has, however, been on the topic of Māori entrepreneurship and the larger question of Māori economic development, understandably so, given the historical grievances which resulted in limited Māori economic activity.

The increasing economic importance of Iwi investment entities, referred to hereafter as Māori Asset Holding Institutions (MAHI), has not gone unnoticed by the business and investment community in New Zealand. There has been increased media discussion and industry publications which seek to compare these investments to those made by traditional investment managers (see ANZ, 2017; BNZ, 2012; Chapman Tripp, 2018; NZIER, 2005; PWC, 2012; TDB Advisory, 2017, 2018, 2019). Comparison has involved the use of western frameworks which rely primarily on financial metrics such as return on investment, profit, diversification, total debt to assets, and other financial ratios. It is the contention of this article that while these classical financial concepts can and should be applied to Iwi investments, they do not tell the full story. Specifically, a narrow focus on financial performance neglects the influence that Indigenous values, culture, and history, which inform Iwi investment philosophy and approach, have on Iwi investment decision-making.

Our theory follows recent work by Craig et al. (2013), which utilizes the concept of accountability reporting, as opposed to financial reporting, as a platform for using Indigenous perspectives to assess Indigenous organizations and provide lessons for non-Indigenous organizations. We also take our impetus from developments within industry regarding non-financial information (NFI) reporting, particularly climate-related disclosures (Task Force on Climate Related Financial Disclosures, 2017). In like manner, this article seeks to take a deeper look at the investment framework which guides Iwi in their investment management function and raises the question of whether western reporting is appropriate as a performance measurement tool for MAHI. Through a case study of the investment arm of the Waikato-Tainui Iwi, Tainui Group Holdings (TGH), New Zealand’s most populous Iwi, we highlight deficiencies in the ability of western reporting to fully reflect the multidimensional nature of Indigenous investments.

From the literature, we know that the motivating factors for Indigenous self-employment include, but are not limited to, the profit motive that tends to dominate western corporates (Haar and Delaney, 2009). In addition to financial performance, Indigenous values informed by tikanga and mātauranga Māori are also important (Merrill, 1954; Mrabure, 2019; Perry et al., 2003; Reihana et al., 2007; Te Aho, 2005; Scrimgeour and Iremonger, 2011). Tikanga is defined as Māori customs, values, and practices that have developed, and can be thought of as the Māori way of doing things. Mātauranga Māori refers to Māori knowledge including Māori views and perspectives. For the purposes of this case study, tikanga and mātauranga Māori are used to characterize Māori beliefs, philosophies, values, and custom. We show how these extend to and inform the investment behavior of MAHI. To tease out the tikanga and mātauranga Māori factors driving the investment thinking of MAHI, we conduct an analysis of a sample of TGH’s corporate documents and report on the prevalence of tikanga and mātauranga Māori elements. We then compare these with the prevalence of western financial metrics present in the documents.

An example of one such factor is the Māori cultural value of kaitiakitanga, which would prohibit Iwi investment entities from making any investments that may result in environmental damage. This investment constraint has meant MAHI essentially engage in only green investments irrespective of any potential financial penalty. Incorporating strong cultural values as it relates to caring for the wellbeing of the Iwi and the environment implies Māori investment strategies are akin to those of impact investors.

The idea of pursuing both financial and social goals, widely referenced in the literature on impact investing (see Bugg-Levine and Emerson, 2011), is also inherent in the investment mandate and operations of MAHI. MAHI are informed by an Indigenous worldview which emphasizes improved outcomes for social wellbeing, and the environment. In this respect, there appears to be a similarity between the environmental, social, and governance (ESG) factors that characterize impact investing and the equivalent Māori concepts informing Māori financial decision-making and business conduct. These Māori concepts include kaitiakitanga, that is, guardianship and care of the environment; whanaungatanga, that is, social relationships/family connections; and, mana/rangatiratanga, that is, governance, leadership, and respect (Craig et al., 2018; Love, 2017).

By investigating how the Māori worldview of investments is reflected in TGH’s statements of investment strategy and their disclosures of performance, we argue that application of a purely western and traditional financial performance assessment is inappropriate. By considering Iwi investments as a portfolio of intergenerational wealth containing social, cultural, and environmental assets (Wood and Mika, 2018), we draw parallels between endowment funds and Indigenous investment funds. However, the Māori worldview informs the investment—and diversification—strategy, requiring a framework like that being developed for impact investors, to be applied to Indigenous finance.

2. Background: Investment philosophy of the Māori of Aotearoa New Zealand

Indigenous groups have sought to advance their economic development through entrepreneurial initiatives which exhibit distinctive Indigenous characteristics (Hindle and Moraz, 2010). For Māori, the Indigenous people of New Zealand, this has been exhibited through heritage entrepreneurship, tribal entrepreneurship, and Indigenous self-employment. Heritage entrepreneurship has involved the actions of various Iwi (tribes) to reclaim significant assets from the state through the Treaty settlement process, tribal entrepreneurship has encompassed the management and expansion of the tribal asset base through collectively owned enterprises and/or joint ventures while Indigenous self-employment has been characterized by small- and medium-sized enterprises owned and operated by Māori (De Bruin and Mataira, 2003). It is worth noting Māori rapidly embraced entrepreneurial concepts like trade and exporting following the first contact with Europeans, and before becoming a part of the British Commonwealth (Henry, 2007). As a result, Māori have a long history of entrepreneurship but were disadvantaged by the loss of their economic base due to colonization. While the literature on heritage entrepreneurship and Indigenous self-employment continues to grow into a significant body of work within the field of Indigenous entrepreneurship (Hindle and Moraz, 2010), there remains a dearth of research on tribal entrepreneurship. 5

As emphasized in the framework and schematic view of tribal entrepreneurship presented by Mataira (2000), tribal entrepreneurship, as practiced by some Iwi, has risen out the economic disenfranchisement of Iwi following colonization. Waikato-Tainui was seriously impacted due to the confiscation of more than 1.2 million acres by the crown during the Land Wars of the 19th century, virtually all the Iwi’s land. For Māori, who were agrarian traders, this left Waikato-Tainui without an economic base (De Bruin and Mataira, 2003). The desire to reclaim land as historical redress serves two purposes. First, relinking Māori with their historical lands fulfills cultural and spiritual goals, as connection to ancestors and ancestral lands is an extremely important part of Māori culture, and second, increases the asset base that supports tribal entrepreneurship. It is therefore one of the driving forces of Māori enterprise. In addition, the loss of language, culture, and tribal autonomy are also key driving factors (Mika, 2018).

Māori social and cultural values are steeped in cosmogony, cosmology, mythology, religion, and anthropology (Harmsworth and Awatere, 2013). A matrix of these beliefs which informs tikanga and mātauranga Māori was developed by Henare (1998) and has now become known as the koru 6 of Māori ethics model. The model identified kotahitanga (unity), wairuatanga (spirituality), manaakitanga (the ethic of care for all things), whanaungatanga (relationship and kinship), and kaitiakitanga (guardianship) as the main elements of Māori ethical values. These are the core characteristics which distinguish Māori enterprise and have been the subject of several studies; see Mrabure (2019), Haar and Delaney (2009), Scrimgeour and Iremonger (2011) and Mika (2018).

These values, or some variation thereof, are abundant in the literature on the motivations driving Māori entrepreneurship and economic development and are also reflected in the models of Māori entrepreneurship mentioned above. The Māori worldview not only influences the entrepreneurial orientation of MAHI but also underpins business behavior, commercial, and investment decisions (Mrabure et al., 2018). The Māori approach to business, as expressed through tikanga and mātauranga, encompasses practices of collectivism, intergenerationality, social and cultural preservation, and environmental sustainability (Wood and Mika, 2018). Embedded in the Māori perspective is a deviation from the profit and wealth maximization motive. Māori are indeed concerned with profit, but it is not the main driving force in investments and commercial pursuits (Mika et al., 2017). This type of investment thinking would perhaps best be characterized in financial theory as impact investing and is similar to the Aboriginal Financial Institutions (AFI) in Canada which have been described as model impact investors in the literature (UBC Sauder Centre for Social Innovation & Impact Investing, 2018). Locating Māori, as an Indigenous group, in the impact investing space may indeed be appropriate given their investment philosophy aims to create positive social and environmental impact beyond financial return (see O’Donohoe et al., 2010 for a definition of, and theoretical framework for, impact investing).

Within the organizational structure of Iwi, tribal entrepreneurship is executed by the commercial and investment arm of the Iwi through what can be described as an Indigenous impact investment business model. Within this model, certain restrictions are imposed on investment decision-making to ensure investments are consistent with tikanga and conform to the cultural and spiritual needs of the tribe. For instance, Waikato-Tainui tend to place restrictions on selling land-based investments irrespective of financial returns. The responsibility for pursuing social, economic, and cultural wellbeing goals largely sits with the social arm which implement social programs using proceeds from the investments made by the investment arm. Within this structure, the two arms, social and investment, are interlinked in the pursuit of the goal of advancing the social and economic wellbeing of Iwi members. The hurdle rates and financial targets required by the investment arm are set to provide the projected cashflows the social arm will need to continue its social and environmental programs (Scrimgeour and Iremonger, 2011), while the priorities of the social arm are directed by the Iwi within a collectivistic framework whereby all members have a direct say in the Iwi’s direction and decisions (Kawharu, 2016).

It is therefore clear the investment operations of Iwi have a high degree of correlation with the definition of impact investing promulgated by the Global Impact Investing Network (GIIN). The Network defines impact investing as “an investment made into companies, organizations, and funds, with the intention to generate social and environmental impacts, alongside financial returns.” The three types of investment vehicles utilized by impact investors are direct investments, comingled funds, and funds-of-funds (Johnson and Lee, 2013). From the description of the major investment activities of Iwi, direct investments and joint ventures in regionally based Māori operated enterprises or infrastructure projects are the preferred vehicles through which Iwi engage in impact investment. Through a direct investment vehicle, Iwi create employment for tribal members and in doing so address the significant social problem of Māori unemployment (Kawharu, 2016). Increasing the employment of tribal members has become a defining factor in how Iwi measure their social impact and is a practice parallel with the concept of impact measurement used in the impact investment literature (Social Impact Investment Taskforce, 2014).

3. Methodology

Our analysis takes its impetus from Bowman’s (1984) seminal paper, which analyzed annual reports for corporate strategy and risk. A similar methodology is used to analyze social and environmental reporting (Guthrie and Mathews, 1985; Guthrie and Parker, 1990) and intellectual capital disclosures (April et al., 2003; Abeysekera and Guthrie, 2004a, 2004b, 2005; Beattie et al., 2006; Bontis, 2003; Bozzolan et al., 2003; Brennan, 2001; Olsson, 2001; Petty and Guthrie, 2000). Adopting the analysis approach for annual reports suggested by Beattie et al. (2004), we provide a comparative synthesis of TGH’s Statement of Investment Purpose and Objectives (SIPO), Constitution, 2017 and 2018 Annual Reports, Investment Committee Terms of Reference (TOR) and Investment Strategy Statement. These documents were selected as they are public disclosures of TGH’s investment framework, and relevant to external stakeholders from a regulatory perspective.

3.1. Development of codes

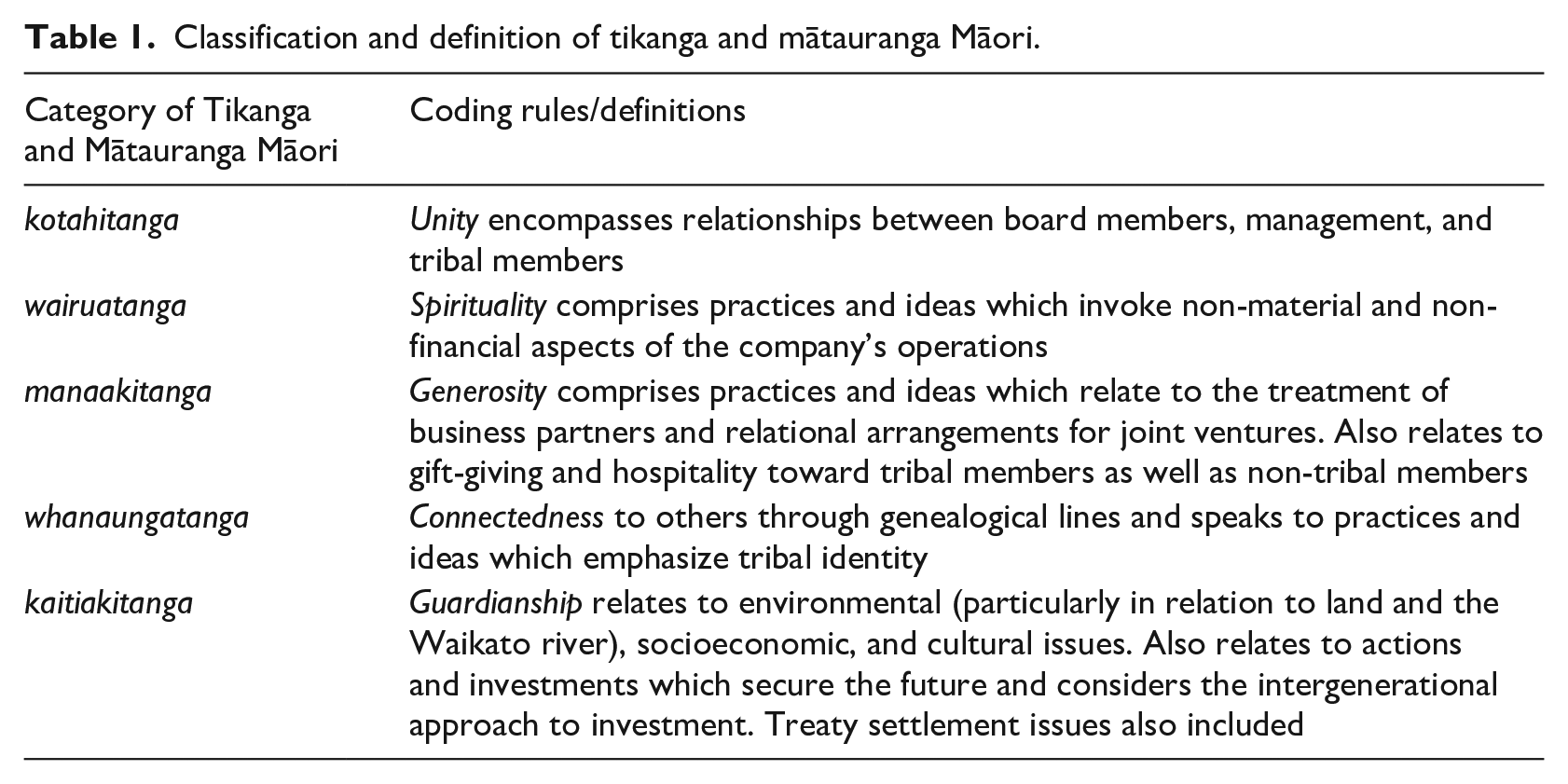

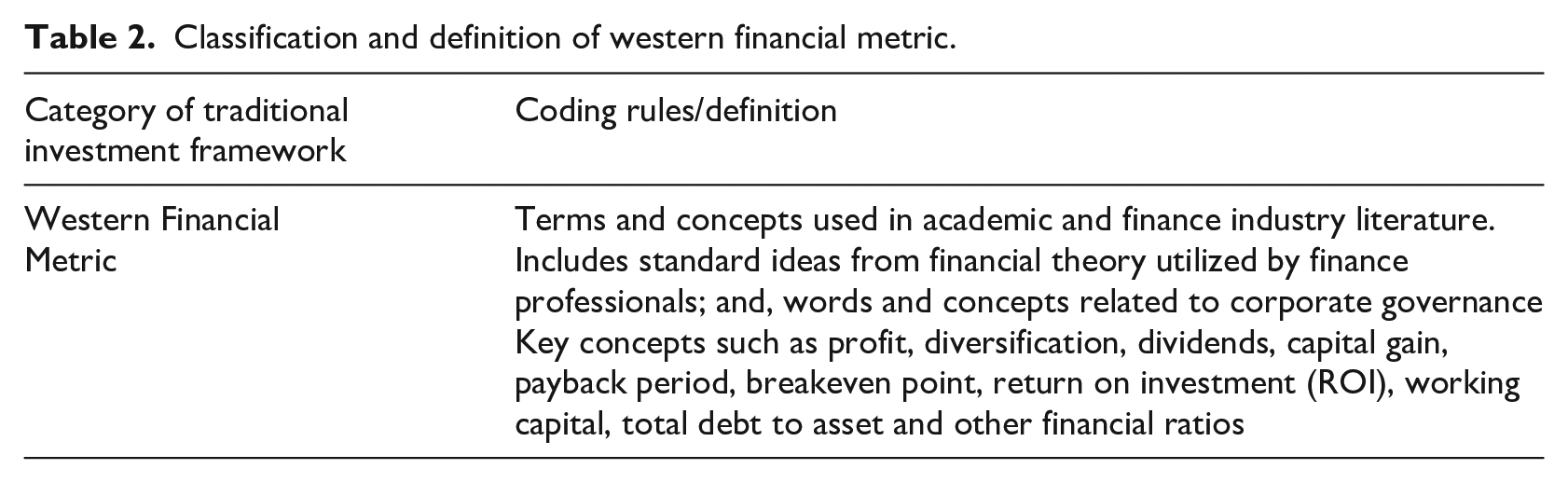

The sample documents were read in their entirety and coded according to the main elements of Māori ethical values described in the previous section. That is, we use the Henare (1998) model and apply the codes listed in Table 1. These are widely considered to be the core distinguishing features of Māori enterprise and are in line with related literature (see Best and Love, 2010; Haar and Delaney, 2009; Harmsworth and Awatere, 2013; Henwood and Henwood, 2011; Kawharu, 2016; Mika, 2018; Mika et al., 2017; Mrabure, 2019; Scrimgeour and Iremonger, 2011). We define traditional western financial metrics as the key terms and concepts used by financial professionals and in academic and finance industry literature (Table 2).

Classification and definition of tikanga and mātauranga Māori.

Classification and definition of western financial metric.

Reading of the documents supported the use of predefined codes as a starting point for the analysis (Nielsen, 2008). The unit of analysis and the unit of measurement selected was the phrase/sentence. For the purposes of coding TGH’s Constitution, the western financial metrics sub-category also related to issues of corporate governance. These rules served as the coding instrument.

The computer software package used to code the documents was the QDA Miner developed by Provalis Research. 7 Codes are organized in a code book, displayed as a tree structure with codes associated with each category or theme delimited as sub-nodes. Coding is performed by assigning a code from the code book to a selected body of text. An intuitive coding process is made possible by the tree structure and is complemented by the ease of making comments and attaching memos to coded segments. The software provides inbuilt frequency analysis tools which presents results in tabular and graphical formats. The coding was performed by a single coder and was re-coded a second time to ensure consistency and reliability with the original coding.

The documents were sourced from TGH’s website, uploaded in PDF format to the QDA Miner and converted to plain text within the package. The documents did not have to scanned or manipulated in anyway due to this conversion ability within the software program, eliminating editing or reformatting of the text and preserving the contents of the original files. The coding proceeded in two steps, following Weber (1990), with main categories coded in the first instance and sub-categories in the second.

4. Comparison and synthesis

We identified two themes as the main factors informing the investment framework of Tainui Group Holdings Limited, as an example of MAHI more generally:

Balancing current and future distributions;

Land ownership.

In this section, we discuss each theme, before turning to an overarching difficulty for MAHI in measuring and communicating non-financial goals.

4.1. Balancing current and future distribution

In the same way that Haar and Delaney (2009) characterized whanaungatanga as the main distinguishing tikanga value for Māori entrepreneurial enterprises, our results indicate that kaitiakitanga distinguishes MAHI from more traditional impact investors. The notion of intergenerational wealth transfer is one that is important to Māori and is encompassed in the concept of taonga (treasure). Taonga covers natural and cultural resources such as land, waterways, forests, and the Māori language (Te Reo). Under a Māori worldview, a taonga must be handed to the next generation in a better state than it was received and plays into the ideal of kaitiakitanga, which speaks to the idea of guardianship and emphasizes the need to protect and preserve resources, natural and otherwise, for the next generation.

Viewed through the lens of kaitiakitanga, intergenerationality becomes a much broader and unique concept when applied to the investment framework of Iwi. For instance, in believing that taonga should be handed to the next generation in a better condition than they are currently, kaitiakitanga also places a strong emphasis on the environmental, socioeconomic, cultural, and tribal responsibilities the current generation has. This results in Iwi being more than “just” investors with a long-term horizon and the discipline to maintain assets for long periods of time. Unlike other long-term investors, such as Warren Buffet or the New Zealand Super Fund, Iwi investments must meet the criteria of being environmentally friendly, reflective of Māori culture and values, and able to meet the future needs of the next generation in terms of employment and social needs. Perhaps most importantly, Iwi investments are rooted in the narrative of cultural and historical preservation as expressed through the Treaty settlement process.

The importance to Tainui of kaitiakitanga can be seen throughout the documents we analyze, as it is the most frequent tikanga and mātauranga Māori value in half of our sample documents (36.2% in SIPO, 42.6% in 2017 Annual Report and 47.3% in 2018 Annual Report). A key aspect of the intergenerational approach is the efforts by TGH to balance its current and future distributions. TGH, like other MAHI, face the challenge of needing to provide funding to meet the cultural and socioeconomic needs of tribal members. Māori are overrepresented negatively across many social statistics within New Zealand including life expectancy, 8 home ownership, 9 unemployment, 10 and Māori incarnation rates, 11 among others. This highlights a particular challenge for MAHI, like TGH, to meet the needs of and support the current generation, which conflicts with the need to grow the Iwi’s strength for future generations. The conflict of internal distribution was highlighted in the literature as one of the key criticisms of TGH (Van Meijl, 2003).

The concept of intergenerationality, that is, funding activities into perpetuity, is evident in the management of university endowment funds. However, there exist key differences between MAHI and the traditionally managed endowments that become clear when comparing the two. Merton (1993) argues that endowment funds should follow a policy of diversifying their endowment and capitalized non-endowment income, as well as hedging it against future downturns. Merton explains that in practical terms if the university endowment fund is in a region where economic activity is dominated by a given industry, the (university-based) fund should diversify its research and teaching activities away from the local industry. Going further, the endowment fund should short the stock of firms within the locale of the university, as a hedge against loss of income and wealth. Given Iwi, in this case TGH, aim to provide for future generations, the endowment fund model suggested by Merton (1993) implies the optimal investment strategy would diversify away from their local region and industry. Specifically, away from the Waikato Region and its main economic activity of primary/dairy production. Going further, TGH would short sell the shares of Fonterra, the largest publicly listed firm in the region. While modeling the theoretical strategy is beyond the scope of this article, such an exercise would be markedly different from the current strategy pursued by TGH.

It is a comparison such as this where the case for an Indigenous investment framework applicable to Iwi is strongest. Even though TGH, and Iwi in general, could be classified as traditional investment firms with an intergenerational view, as university endowment funds are, their diversification strategy is one which sees them investing even more aggressively in the Waikato Region. In its 2018 annual report, the company indicated its highest investment priority was an increased investment for the completion of Ruakura Estate, a legacy project which will develop tribal lands into a state-of-the-art inland port and logistics hub. Other investments being made into the region include the construction of an additional 40 rooms to its Novotel Tainui Hamilton hotel and of housing units in its Rotokauri Rise joint venture project. The Waikato Region holds significant historical and socio-cultural significance for TGH as highlighted in the literature on the Waikato-Tainui Iwi. Divesting away from its rohe (tribal area) would prove difficult given the Waikato-Tainui Iwi’s cultural and historical sensibilities in respect of the region and its tribal lands. TGH illustrates how the investment decisions of Iwi are shaped by non-financial goals underpinned by tikanga and mātauranga Māori values. It is these values and worldview, along with the need to redress historical grievances, which inform the investment framework of Iwi and sets them apart from traditional investors.

When viewed through the lens of investing funds into perpetuity and the model considered optimal by Merton (1993), TGH’s investments are sub-optimal, undiversified, and thus not mean–variance efficient (a foundational finance concept, underpinning modern financial theory). However, when viewed through the lens of tikanga and mātauranga, they enhance the value of kaitiakitanga, therefore meeting the requirement of TGH’s key investment philosophy.

4.2. Land ownership

Rebuilding the tribal estate, through the maintenance and acquisition of land in the Waikato region, is one of the main drivers of investment decisions for TGH. The core business of the company is reflective of this. The prominence of land and property for the Waikato-Tainui Iwi is driven by the loss of land which the Iwi suffered during the Land Wars. Land, as a feature of the TGH narrative, was encapsulated in kaitiakitanga again, reflecting the expansiveness of the coding rules associated with this tikanga category. Throughout the documents analyzed, TGH consistently emphasized the primacy of land as an asset class and has noted one of its objectives is to maintain and increase its land holdings (Tainui Group Holdings, 2012). The Land Wars of the 19th century resulted in the confiscation of large tracts of lands by the crown, leaving Iwi, who were agrarian traders and tangata whenua,

12

without an economic base (De Bruin and Mataira, 2003). Waikato-Tainui was one of the worst affected Iwi. The company’s CEO, Chris Joblin, in discussing TGH’s land assets has said,

It is about the future generation. 1.2 million acres of our land was confiscated in 1863 and we waited 100 plus years to get that back. In our context, land is very important because of that loss. So, for us, we have been blessed with an endowment that is land based. It’s all about looking for opportunities to maximise that. (quoted in Jennings, 2018)

The MAHI’s sentimental and historical attachment to land as an asset class has, in some respects, served to constrain its growth potential due to the restrictions on the use of tribal land (Sautet, 2008). These restrictions have resulted in several acres of unproductive land being registered in TGH’s asset base. When viewed through a traditional investment framework, the maintenance of unproductive land within the investment portfolio has resulted in the company forgoing higher returns and limiting its potential to maximize wealth for the Iwi. From a tikanga and mātauranga perspective, however, the importance of land ownership for Waikato-Tainui cannot be overemphasized.

The diversification thrust which has seen TGH invest in equity and directly in local companies has served to reduce its appetite for land acquisition. An argument could, however, be made that the company has yet to fully maximize the benefits of diversification because at 67% (2015), 51% (2016), and 53% (2017) of the total asset base, land and property remain the main asset class in its portfolio mix (TDB Advisory, 2017). Based on the principle of kaitiakitanga and the historical antecedents highlighted in the literature, it remains doubtful as to whether TGH will be able to, or should, fully diversify away from land and property in the Waikato region. This presents a conundrum for TGH in that their inter-regional investment in Waikato land and property will hamper their ability to support the Iwi should the economy of the Waikato region be affected by some adverse event. The present realities and future risk of climate change, its impact on land and property, highlights the issue of environmental management as important for TGH. On one hand, TGH is upholding kaitiakitanga by being invested in its tribal lands, whereas, on the other hand, kaitiakitanga defined as an obligation to the next generation is potentially being stifled by a lack of diversification.

The dilemma raised by the attachment to land and property assets domiciled in the Waikato region is easily resolved under a traditional investment framework. Not so under a tikanga and mātauranga framework, where whanaungatanga, characterized as tribal connectedness and identity, has driven TGH to deepen its investment activity in the region. Whanaungatanga exhibited a 17.9% prevalence in the SIPO, a 9.4% prevalence in the 2017 annual report, and a 9.6% prevalence in the 2018 annual report. That this tikanga principle shows up the most in the SIPO gives an indication of its impact on asset allocation decisions made by TGH. Even when the company sought to diversify under what was considered a traditional investment framework, it could not diversify optimally in the manner proposed by Merton (1993) and maintain its identity as a MAHI. Diversifying away from its rohe (tribal area) would compromise TGH’s mission to maintain and expand the tribal land and assets of the Iwi. The company has, therefore, sought to diversify through what we will classify as an “inbound” (that is, internal) diversification strategy. The inbound diversification, here defined as inter-regional investments in the Waikato-Tainui tribal area, indicates the company has recognized the dangers of being heavily invested in a single asset class and has sought to address the limitations of their geographical constraints, while maintaining the tikanga principle of whanaungatanga.

4.3. Measuring and communicating social goals and outcomes

As noted above, MAHI’s need to incorporate tikanga and mātauranga concepts such as kaitiakitanga and whanaungatanga into their investing framework makes applying traditional investment frameworks difficult, if not inappropriate. An additional complication is measuring and communicating social goals, especially in documents that are more focused on traditional finance measures. Two concepts referenced throughout TGH’s documents are kaitiakitanga (guardianship) and wairuatanga (spirituality). As described above, kaitiakitanga encompasses a wide range of objectives and goals, not least safeguarding the wealth and assets of the tribe for future generations, while promoting and caring for the wellbeing of the tribe today. It is important to note here that wellbeing in the sense of kaitiakitanga is of the people—housing, education, employment—and of their environment, including guardianship of the natural landscape. Wairuatanga, or spirituality, promotes the non-financial, spiritual needs of the tribe. For Waikato-Tainui, the acquisition of land confiscated during the land wars and their ancestral connection to the land lends a spiritual aspect to any land investments made. For Māori, genealogy is important, and identity is interwoven with the land. 13

While both kaitiakitanga and wairuatanga are key goals expressed within the analyzed disclosures, there is a disconnect present, illustrative of the tension between Māori principles and expressing investment performance using a western financial framework. This tension between the traditional and Indigenous investment frameworks was reflected in the prevalence of western financial metrics between documents: 8.3% in TGH’s SIPO, 98.4% in the constitution, 90.9% in the Investment Strategy, and a 55.8% prevalence in the Investment Committee TOR. Western financial metrics were also the second most coded item in the 2017 and 2018 annual reports. TGH has objectives that go beyond maximizing financial return and it is these that dominate its SIPO. In contrast, the Investment Strategy appears to have little relation to the investment philosophy outlined in its SIPO. We suggest that the reasoning is twofold.

First, we propose the objectives of the documents are different. The SIPO and TOR are more likely to be aspirational in nature, a statement of intent and values. The Annual Reports and Investment Strategy, however, exist to provide investors and stakeholders disclosure of TGH’s progress to date and a strategic outline of how they will meet their goals. The nature of a document with a reporting function may be biased toward a more financially orientated discussion of performance, as performance needs to be quantified. Annual reports are designed within a western regulatory framework, presenting a financial snapshot of the success and progress of a financial entity, in almost exclusively financial terms. When commercial or investment goals are not solely financial however, the usefulness of the disclosure may break down, and the tension between Indigenous values and western performance measures is exacerbated. This raises the question of whether documents like the Annual Report are the correct avenue through which to try and communicate ongoing achievement of tikanga and mātauranga goals.

Second, the investment philosophy of the company is informed by non-financial concepts expressed by tikanga and mātauranga, concepts which are difficult to reflect in an investment strategy document. The high prevalence of tikanga and mātauranga values coded in the SIPO indicates that an Indigenous investment framework is a key driver of TGH’s investment process. Achieving greater alignment between its SIPO and other corporate documents will require TGH, and Iwi in general, to think about returns and performance in non-financial terms. As it stands, however, the language and framework around such thinking is in its infancy. Consensus on the metrics of social, cultural, environmental, and spiritual capital is yet to be achieved, and as such western financial metrics continue to dominate investment practice (Emerson, 2003).

The last 20–30 years has seen a growing acceptance by financial managers of the need to incorporate both financial and non-financial goals into annual reports, efforts made more explicit in the impact investing and socially responsible investment (SRI) fields. 14 The tikanga and mātauranga principles which underpin Māori commercial pursuits are congruent with the social and environmental concerns which impact investing and ethical investing seek to address (Scrimgeour and Iremonger, 2011). Efforts made within these areas to quantify and measure achievement of both financial and non-financial goals may prove useful; however, there are unique challenges in incorporating tikanga and mātauranga Māori in these frameworks. For instance, the quadruple bottom line reporting framework, which adds spiritual and cultural dimensions to the more common triple bottom line, may prove useful for Māori enterprises and MAHI. 15 Requiring quantification of what may prove to be ultimately unquantifiable values, raises questions of whether inherently western disclosure frameworks are best placed to report on the success of investment decisions made with more than financial performance in mind. An example in Tainui’s context is the benefits from rebuilding the Iwi’s property portfolio. The confiscations of Tainui land resulting from the Land Wars in the 1860s have left an indelible scar on the Iwi. Acquiring more land, irrespective of its productive value, can therefore lead to an improvement in the spiritual wellbeing of the tribe, wairuatanga. The difficulty comes through in how you quantify the spiritual improvement, and as often becomes necessary within an investing framework, compare that against the benefits of other investments, such as education scholarships, or investment in new businesses employing Iwi members.

Another framework that has gained in popularity is social return on investment (SROI), which is designed to allow for performance measurement of socially orientated projects and is applied in a wide range of contexts. 16 However, the issue of quantifying the benefit of an investment project in monetary and financial return terms remains a significant roadblock to its implementation in the context of Iwi and MAHI investment reporting. Spiritual wellbeing, and its restoration, is again an example of a potentially unquantifiable goal. Ultimately, what is measured is managed: when an aspect of an investment decision is inherently hard to quantify, including its payoffs, how does a manager compare and decide between projects? Additional thinking is needed within this space.

Turning to kaitiakitanga, guardianship, in a SROI framework also proves to be potentially problematic for multi-generational investments. When discounting future benefits (i.e. cashflows), SROI applies fundamental finance principles. Even for a small discount rate, longer-term payoffs are disadvantaged compared to those occurring sooner. There is, therefore, a possibility that the investment decisions recommended under SROI would conflict with tikanga and mātauranga concepts like kaitiakitanga.

Despite the issues raised here, the recent growth in impact investing should give Iwi more confidence in exerting tikanga and mātauranga as a dominant investment framework. Given impact investing is underpinned by similar social and environmental issues addressed by tikanga and mātauranga, Iwi could easily develop considerable expertise in this area. Indeed, many elements of social impact measures such as The Impact and Reporting Investment Standards (IRIS) and The Global Reporting Initiative (GRI) are already incorporated in the TGH’s annual reports.

5. Conclusion

As one of the first Iwi to receive a Treaty settlement from the New Zealand Crown, the Waikato-Tainui Iwi is a useful and informative example of how Indigenous groups manage and invest their financial resources for the benefit of their tribal members. The key question we have sought to examine is whether the way in which Indigenous groups, such as Waikato-Tainui, approach investment and financial affairs is adequately captured by western financial frameworks. The extant literature is clear that a framework of tikanga and mātauranga values underpins the Māori approach to finance and business in general (Haar and Delaney 2009; Mika, 2018; Mika et al., 2017; Mrabure, 2019; Mrabure et al., 2018; Scrimgeour and Iremonger, 2011; Wood and Mika, 2018). Analysis of a select sample of the corporate documents of TGH, the investment arm of the Waikato-Tainui Iwi, confirms the existence of a tikanga and mātauranga framework as a distinct feature of Māori investment outfits.

We document two key themes following the content analysis: the need for TGH to balance current and future distribution and the importance of land as an asset class. We then discuss the challenge of measuring and communicating non-financial goals and outcomes. Kaitiakitanga proved to be the most prevalent tikanga value, reflecting the intergenerational and long-term approach TGH takes toward its investments. We draw parallels between Iwi and impact investors, regarding the value placed on environmental and social responsibility. At the fund level, we suggest there are similarities between university endowment funds and TGH as perpetual asset managers, however, we differentiate the two in terms of the Māori worldview’s impact on wider investment goals.

A significant challenge TGH faces is simultaneously delivering financial and social returns. This dual role was also identified as a distinct feature of the investment firm and Iwi commercial arms in general. As Iwi seek to fulfill their dual roles, language and metrics which speak to more than “just” financial returns will have to be developed so Iwi can pursue commercial initiatives without sacrificing their tikanga and mātauranga values. The advent of impact and socially responsible investing, as well as the introduction of a wellbeing budget and the living standards framework in Aotearoa New Zealand, provides an opportunity for Iwi to develop specialized expertise. By engaging in the impact investing space and adopting appropriate performance frameworks, there is potential for traditional investment and finance professionals to learn from Iwi about how best to incorporate the social, cultural, spiritual and environmental values of tikanga and mātauranga Māori (and Indigenous peoples more generally) in modern investment practice.

Footnotes

Appendix 1

Acknowledgements

The authors would like to thank Ella Henry, Pare Keiha, Agnes Naera, the editors, an anonymous referee, and participants at a Finance Department Brown Bag Seminar, for their helpful comments and feedback. All errors remain the authors.

Final transcript accepted 29 May 2020 by Barry Oliver (AE Finance).

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.