Abstract

Marxist views of the relationship between financial and real cycles suffer from three major weaknesses: (a) financial developments are almost always reactions to real sector developments; (b) financial crises can trigger but not cause real sector crises; and (c) the 2008 financial crash played only a triggering, not causal, role in the ensuing Great Recession. I would argue, by contrast, that (a) in the era of big finance, finance capital does not necessarily shadow or merely react to industrial capital, it also behaves independently; (b) financial sector crises can be transmitted (through debt deflation) to the real sector; and (c) the 2008 financial crash played not only a triggering but also a causal role in the ensuing Great Recession.

1. Introduction

Mainstream neoclassical economic theory tends to regrettably trivialize the role of credit and/or finance: its parasitic expansion, its systematic draining of the real sector, and its destabilizing impact on the economy are either left out of this theory altogether, or discussed only in passing. Money supply and/or credit creation is treated in this model as confined or limited by the production capacity of the real sector: production or output determines national income, national income determines national savings, national savings determine (through financial intermediaries) financial resources for investment, investment determines production, and so on. This circular relationship is illustrated in the model by what is called the “circular flow” diagram.

The financial sector in this model thus plays essentially an intermediary role: it consolidates the numerous nationwide savings and funnels them toward the industrialists for productive investment. While this may have been true in the earlier stages of capitalist development, when banks played an essentially intermediary role between savers and investors, it is certainly not the case in the era of big finance where “finance mostly finances finance,” as Professor Jan Toporowski (2010) put it.

Unsurprisingly, major financial bubbles and bursts have no place in mainstream economic theory. For, according to theory’s near-barter general equilibrium and/or “circular flow” model, monetary or financial deviations from the underlying real values would be only temporary as such deviations would soon be reverted back (either by market mechanism or by government intervention) to their initial positions of equilibrium.

In a similar fashion, many contemporary Marxist economists also tend to give short shrift to monetary/financial categories in their explanations of the Great Recession that followed the 2008 market crash (Brenner 2009; Kotz 2011a, 2011b; Kliman 2011; Bellamy Foster and Magdoff 2010). Just as neoclassical economists seem incapable of extricating themselves from the elegant but abstract “circular flow” model, so too many Marxist economists seem reluctant to look beyond the “circuit of capital” model, which is discussed largely in volumes one and two of Marx’s Capital, and which like the neoclassical “circular flow” model is fashioned primarily on real, not financial, sector developments.

This regrettably flawed treatment of finance capital by a great number of today’s Marxist scholars represents not only an obvious departure from earlier views of Marxist scholars like Hilferding (1981), Hobson (1965), and Lenin (1916), but also from Marx’s own treatment of finance capital (1967: 476-519). A careful reading of his work on “fictitious capital” reveals keen insights into a better understanding of the instabilities of today’s financial markets. His work on “money capital and real capital” shows that he did, indeed, envision market scenarios where part of the real-sector profits (which he called surplus capital, and which are nowadays called “retained earnings”) may permanently abandon or leak out of the production/reproduction circuit in pursuit of speculative gains through buying and selling of assets (ibid.).

It is true that Marx’s discussion of fictitious capital remained brief and fragmented. Nonetheless, what he wrote (in broad outlines) about market scenarios where finance capital can and does sometimes expand outside or independent of the real sector of the economy is clearly at odds with the views of many contemporary Marxist economists who seem to perceive financial developments as mere reflections of or reactions to some supposedly undercurrent real developments.

By thus neglecting or trivializing the crucially important role of financial factors as sources of instability and crisis in today’s advanced market economies, these economists tend to either dismiss as “only monetary,” or provide woefully insufficient explanations for either the 2008 financial crash or the Great Recession that followed the crash. Yet, an understanding of market cycles of boom and bust of the past several decades, as well as of the on-going chronic Great Recession, “requires us,” as Professor Peter Gowan puts it, “to transcend the commonsense idea that changes in the so-called real economy drive outcomes in a supposed financial superstructure” (2010: 47).

A distinct advantage of Marxist theories of capitalist crisis is that, contrary to mainstream theories, which tend to blame the recurring crises of capitalism largely on “external” factors, they focus on the structural dynamics of the market mechanism that tend to periodically erode capitalist profitability from within the system itself. While rival Marxist theories have almost always disagreed on factors that precipitate a fall in profitability, they all have agreed that those factors operate within the sphere of production, or the real sector. A declining trend in profitability, which precedes and/or drives a crisis, could thus be occasioned by factors such as insufficient aggregate demand, overcapacity, profit “squeeze,” or a too high capital–labor ratio, which is more or less the same as Marx’s too large of an “organic composition of capital” (Shaikh 1978).

Prior to the rise of finance capital to the stage of independent parasitic expansion (from industrial capital), Marxist proponents of these theories of crisis could safely disregard the role of the financial sector in the articulation of their theories. For, under such market conditions, finance capital moved more or less in tandem with industrial capital, as it was used or invested largely for commercial and manufacturing purposes. Thus, for example, Marxist theories of the 1970s recession could, as they actually did, justifiably discount or disregard the role of the financial sector and focus mainly on the role of the real sector developments in their explanations of that recession (ibid.).

Under market conditions of extensive financialization, however, the role of financial bubbles and bursts in bringing about economy-wide crises can no longer be ignored, or trivialized. For, under these conditions, finance capital often finds more lucrative investment opportunities in the financial sector than the real sector. Larger and larger shares of credit creation are increasingly devoted to financial rather than real investment. Greatly facilitated by extensive deregulations of recent decades, these developments have in recent years led to a number of destabilizing financial bubbles, whose bursts have constituted the driving forces behind the ensuing recessions: recessions or crises of debt deflation.

These developments have posed serious challenges to contemporary Marxist theories of crisis. For, grounded in the sphere of production, they seem to fall short of providing satisfactory explanations for either the financial bubble that burst in 2008, or the Great Recession that followed the collapse of the bubble. With few exceptions (Gowan 2010; Mohun 2010; Dumenil and Levy 2011), most Marxist scholars argue that (a) the inflation of the bubble was a reaction to low or insufficient profitability in the real sector, and (b) the impact of the bursting of the bubble on the ensuing long recession was a “triggering,” not a causal effect. To make this argument plausible, that is to build a theoretical foundation that the “crisis-prone” conditions that escalated into the Great Recession by the financial collapse were already present in the real sector, a number of these scholars insist that the U.S. economy never really recovered from the 1970s’ contractionary cycle (Kliman 2011; Bellamy Foster and Magdoff 2010; Brenner 2009; Kotz 2011a, 2011b).

2. Instances of Misdiagnosis

Radical proponents of the underconsumption theory of economic stagnation, for example, tend to attribute every crisis in the financial sector to a crisis of profitability in the real sector. Thus, John Bellamy Foster and Fred Magdoff, two of the leading advocates of this theory, write, “Our argument in a nutshell is that both the financial explosion in recent decades and the [2008] financial implosion now taking place are to be explained mainly in reference to stagnation tendencies within the underlying [real] economy” (2010: 81). Acknowledging and then rejecting alternative explanations of the crash, they further write, “the root problem went much deeper, and was to be found in a real economy experiencing slower growth, giving rise to financial explosion as capital sought to ‘leverage’ its way out of the problem by expanding debt and gaining speculative profits” (ibid.: 82). It follows that, as Bellamy Foster and Magdoff conclude, financial implosions and crises are also ultimately caused by crises of profitability in the real sector. “Since financialization can be viewed as the response of capital to the stagnation tendency in the real economy, a crisis of financialization inevitably means a resurfacing of the underlying stagnation endemic to the advanced capitalist economy” (ibid.: 90).

Bellamy Foster and Magdoff’s stagnation argument that the 2008 market crash in the United States was preceded by nearly four decades of economic inertia, that is the argument that the U.S. economy never really recovered from the 1970s’ fatigue, is based on the theory of monopoly-finance capitalism, expounded by Kalecki (1997), Steindl (1952), and Baran and Sweezy (1966). According to this theory, at higher stages of capitalist development, monopolistic/oligopolistic market structures tend to gradually replace competitive market structures. As this change in market structure erodes price competition, it also reduces the dynamic impetus to investment on new innovations. At the same time, monopoly capitalism also reduces purchasing power and consumer demand as it further aggravates poverty and inequality. Reduced demand for both capital and consumer goods means narrowed opportunities for profitable investment in manufacturing, that is stagnation in the real sector of the economy. It also means a steady outflow of capital from the sphere of production to the sphere of speculation. Thus, not only the financial bubble and its burst (in 2008) but also the ensuing Great Recession all had their roots in capitalist tendencies to monopoly and stagnation.

Robert Brenner, another radical scholar, likewise explains the credit expansion and financialization of recent years as a reaction to the “declining profitability” and the resulting stagnation in the real sector. However, contrary to the Monthly Review theory of underconsumption, which attributes the problems of insufficient demand and stagnation to “monopoly capitalism,” Brenner attributes these problems to the systemic tendency to overcapacity: to constantly produce/supply more than it can consume/demand.

In the 1970s, when the Japanese and European economies were doing well while the U.S. economy was grappling with the crisis of “stagflation,” Brenner argued that the suffering of the U.S. economy at the time was because by the late 1960s and early 1970s it had lost considerable share of its global markets to Japan and Europe. Now that stagnation has also engulfed Japan and Europe, Brenner argues that the problem of insufficient demand has become global: it is both systemic and global. “The long term weakening of capital accumulation and of aggregate demand has been rooted in a profound system-wide decline and failure to recover the rate of return on capital, resulting largely . . . from a persistent tendency to over-capacity, i.e. oversupply, in global manufacturing industries” (2009: 3).

A major response of manufacturers to “overcapacity” and weak demand, according to Brenner, was reflected in the easy monetary policies of credit expansion and indebtedness, designed to offset the declining demand in the real sector through debt and asset price inflation. However, the intractable structural weakness continued to hound the economy, until it eventually collapsed in 2008. “From the start of the long downturn in 1973, economic authorities staved off the kind of crises that had historically plagued the capitalist system by resort to ever greater borrowing. . . . But they secured a modicum of stability only at the cost of deepening stagnation. . . “ (ibid.).

Just as Brenner denies independent developments of the financial sector from the real sector, so he rejects the view (and the evidence) that a declining financial cycle can precipitate and/or lead a declining real cycle. To the extent that a financial crisis can or does affect the real sector it would have only a triggering effect on the already anemic or stagnant economy ready to collapse: “What suddenly turned the specter of a severe cyclical downturn or worse into the reality of catastrophic systemic crisis was a development in the financial sector of which few were aware” (ibid.: 4).

David Kotz, another radical economist, likewise rejects the view that the long chronic recession that followed the 2008 financial collapse was transmitted from, or driven by, the financial sector: “One common view is that the severity of the real sector crisis is a result of the financial sector crisis. . . . This paper argues that the real sector crisis that began in 2008—the so-called “Great Recession”—is not primarily a result of the banking collapse” (2011b: 1). Instead, “It is argued that the current crisis can be understood as a particular kind of over-investment crisis” (2011a: 2). Specifically, Kotz argues that the easy credit and the strong, asset-bubble-induced demand that preceded the 2008 crash led manufacturers to invest and expand production capacity. Once the bubble burst and the bubble-induced demand faded, however, producers found themselves saddled with “overcapacity” and falling profits, which he calls the “crisis of over-investment.”

The glaring inconsistency here seems to be lost on Professor Kotz: debt or asset-price inflation, boosting demand, drives an expanding cycle, such as the one that preceded the 2008 market crash; but debt or asset-price deflation, dampening demand and producing or leading to overcapacity/overinvestment, does not cause a declining cycle, it only triggers it. In other words, the so-called “wealth effect” on demand, and therefore on the economy as a whole, works only in one direction!

Andrew Kliman, another radical economist, is even more dismissive of the contributory role of the 2008 financial collapse in the Great Recession that followed the collapse, save for a “triggering” effect. He is also dismissive of the views and evidence that, starting with 1983, the U.S. economy did, indeed, recover from the long stagnation that lasted from the early 1970s to early 1980s:

I will argue that the economy never fully recovered from the recessions of the mid-1970s and early 1980s. . . . I will argue that the persistently frail condition of capitalist production was among the causes of the financial crisis. And, most importantly, I will argue that it set the stage for the Great Recession. . . . In light of the frailty of capitalist production, the recession and its consequences were waiting to happen. (2011)

Kliman adamantly insists that the real-sector rate of profit (which he defines “as a percentage of the amount of money invested”) in the U.S. economy has been either stagnant or in decline for the past forty years. The following is the proffered explanation for this alleged four-decade-long stagnation/contraction.

Prior to government intervention in market developments, that is before the Great Depression and WW II, periodic crises of capitalism were left to run their course, which meant widespread bankruptcies and extensive value or capital destruction. While brutal, those earlier crises also had salutary, “market-cleansing” effects as they wiped out inefficiencies and excess capacities and paved the way for fresh beginnings and robust profitability. However, as interventionist government policies since the Great Depression and WW II have prevented “value destruction” and/or “market-cleansing,” they have also led to anemic recoveries, or chronic stagnations.

During the global economic slumps of the mid-1970s and early 1980s, however, much less capital value was destroyed than had been destroyed during the [Great] Depression and the following World War. . . . But since so much less capital value was destroyed during the 1970s and early 1980s than was destroyed in the 1930s and early 1940s, the decline in the rate of profit was not reversed. And because it was not reversed, profitability remained at too low a level to sustain a new boom. (ibid.)

It is true that government demand-management policies since the Great Depression have made market fluctuations less severe than those before the depression. It does not follow, however, that “since so much less capital value was destroyed during the 1970s and early 1980s . . .,” the U.S. economy did not, therefore, recover from the 1970s’ slump, as Kliman claims. Although he backs up his claim by his own unique calculations of the rate of profit, those calculations are highly questionable. Not surprisingly, the outcome of his calculations, that is his measure of the rate of profit, displaying a constantly declining trend for the entire post-WW II period, flies in the face of reality; it is at odds not only with the official rates of profit, but also with those of many independent scholars, including a number of radical/Marxists (Shaikh 2010; Mohun 2010; Dumenil and Levy 2011).

3. Concluding Remarks

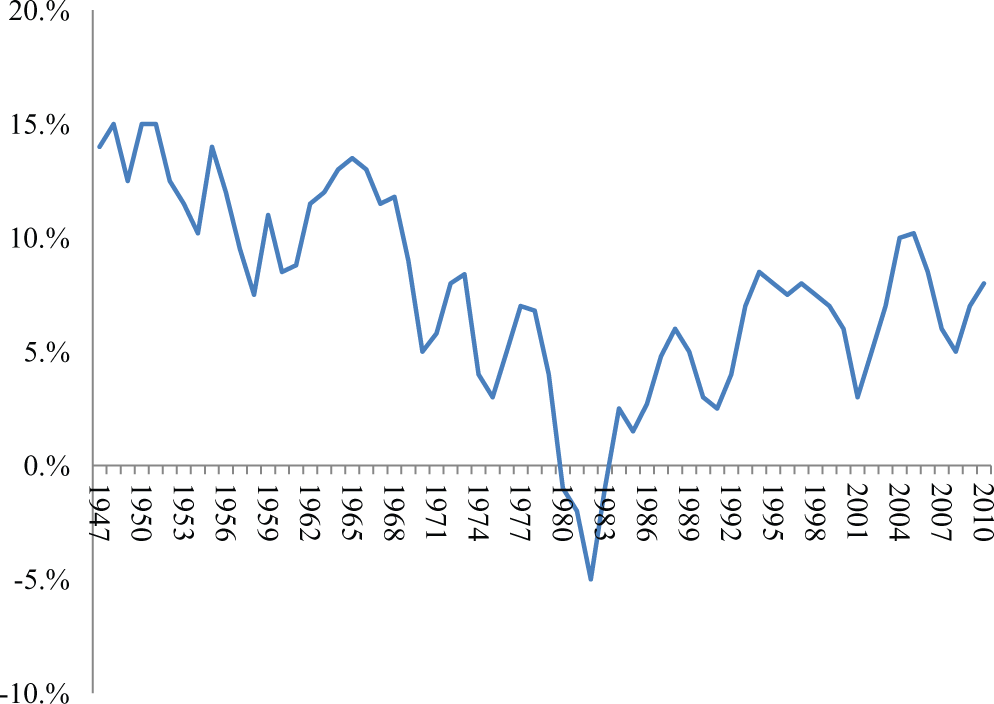

A detailed evaluation of these economists’ views of the Great Recession is beyond the purview of this discussion; nor is such a thorough assessment essential to the discussion. Suffice it to say that their main claim that the recession was not caused by the 2008 financial collapse and the ensuing debt deflation; and that it was, instead, precipitated by a “long period of chronic stagnation and a falling trend in profitability” is not supported by facts. Evidence shows that, contrary to such claims, the 2008 financial collapse and the ensuing Great Recession were not preceded by a pattern of declining profits in the real sector of the economy. Empirical data indicate that the declining profitability trend that had started in the late 1960s and early 1970s was reversed in 1983-84. Since then the real sector profit rate on a macro level went through a number of zigzags, but the overall profit trajectory from 1983 to 2008 displayed a rising trend. The most noteworthy of those zigzags were two relatively short-term declining cycles of the early 1990s and the early 2000s, on the one hand; and three longer term rising cycles of the 1983-87, 1993-2000, and 2002-2008, on the other (Figure 1). As Basu and Vasudevan point out:

The main conclusion that we can derive from inspecting the time-series plots of various measures of the rate of profit for the U.S. economy (Figures 1–12) is that, other than one case, all the measures display similar trends: there is a break in the declining trend of profitability in the early 1980s; the subsequent period is marked by either a trendless or a slowly rising trend in profitability. . . . The weight of evidence thus suggests clearly that the current crisis was not preceded by a prolonged period of declining profitability. (2013: 83, especially Figure 21)

Rate of Profit, U.S. Non-financial Corporations (1947-2010).

These findings confirm those of the renowned Marxist economist Anwar Shaikh who has, likewise, demonstrated empirically that the relatively long cycle of stagnation that had started in the late 1960s and early 1970s turned into a new cycle of expansion in 1983-84 that, with the exception of a few short downturns along the long expanding cycle, continued until it was turned into the Great Recession by the 2008 financial crash. Shaikh highlights a number of contributing factors to that expansion: drop in wages and other labor costs, drop in interest rates, extensive deregulations, and asset price/debt-driven strong demand (2010, especially figures 1 and 6).

One would hope that in light of this evidence those Marxist economists who have so far tended to give short shrift to the role of finance capital in precipitating economic crises would now be willing to expand their traditional theories of crisis, and acknowledge the fact that, in the era of finance capital, financial cycles can and do sometimes lead real cycles. Alas, in a regrettably rigid and ahistorical fashion, these economists continue to insist that the role of finance capital is essentially secondary or incidental to that of industrial capital.

It is true that a number of these economists have written extensively on the so-called financialization of most of the advanced market economies, and the havoc that parasitic finance capital has inflicted on these economies. Nonetheless, they tend to explain every development in the financial sector by a reaction to changes in the profitability imperatives in the non-financial sector, as if financial factors cannot affect profitability imperatives in the non-financial sector. It is one thing to say that the expansion of fictitious finance capital in an economy is ultimately bound by the aggregate magnitude of the real values that are produced in that economy; it is quite another, however, to view finance capital as largely shadowing industrial capital, as these economists tend to do.

It is not clear why these radical scholars seem to think that the “wealth effect” on demand, and therefore on the entire economy, works only in one direction: debt and/or asset-price inflation can boost demand and cause or magnify an expanding real cycle; but debt and/or asset-price deflation cannot cause a real-sector recession!

Of course, the dampening effects of debt deflation on demand would be manifested in a number of ways: underconsumption, overcapacity/overinvestment, or falling rate of profit. This allows Robert Brenner and David Kotz, for example, to argue that the Great Recession has been a crisis of overcapacity or overinvestment; it also allows the proponents of underconsumption theory to claim that it has been a crisis of underconsumption; and it further allows Andrew Kliman and his co-thinkers to argue that the crisis validated the theory of “the tendency of the rate of profit to fall.” But all these problems (insufficient demand, overcapacity/overproduction, and falling profits) were and/or are largely symptoms or effects of the crisis of debt deflation, not its causes: they were driven primarily by the 2008 financial implosion and the ensuing debt deflation. This means that not only was the Great Recession triggered by the financial collapse, but that it was also driven largely by the resulting debt deflation.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.