Abstract

To understand a severe economic crisis such as that of 2008, it is not sufficient to analyze capitalism-in-general along with various economic policy decisions and contingent events. An adequate analysis requires taking account of the particular form of capitalism. This approach to crisis theory is illustrated by an examination of the roots of the economic crisis that broke out in 2008 in the United States.

That capitalism has inherent crisis tendencies is a central claim of Marxism. However, this does not mean that economic crises can be understood solely by analyzing capitalism-in-general. Some crisis analyses assume that, besides an analysis of capitalism-in-general, we are left only with consideration of state policies and contingent events. This article argues that, to utilize the potential power of Marxism for explaining capitalist crises, it is necessary to take account not just of three but of four different levels of abstraction at which one can analyze the capitalist system: 1) capitalism-in-general; 2) the particular form of capitalism at a given time and place; 3) state policies; 4) contingent events.

This article considers the role of the second level of analysis of capitalism in Marxist crisis theory, arguing that the prevailing form of capitalism should not be overlooked in the analysis of particular economic crises. By examining the economic crisis that emerged in 2008 in the United States, it shows how the second level of analysis can contribute to understanding a severe economic crisis. The last section offers concluding comments.

1. Economic Crisis and the Four Levels of Analysis of the Capitalist Economy

Marxists have traditionally defined an economic crisis as an interruption in the accumulation process. Two types of interruption, or crisis, occur in capitalist economies: short-run and long-run. A short-run crisis is a downturn in production, profit, and employment typically lasting 6 months to two years, which ends and gives way to normal accumulation through internal mechanisms of capitalism, although not before significant costs have been imposed on various segments of society. 1

However, our concern here is the analysis of long-run crises. A long-run crisis is an interruption in the accumulation process characterized by a long period of subnormal accumulation. Such a crisis cannot be resolved by internal mechanisms of capitalism but requires economic restructuring if normal accumulation is to resume. For that reason, a long-term crisis can alternatively be called a structural crisis.

The economic crisis that began in 2008 gives every indication of being a long-run, or structural, crisis. This is suggested by various indicators including the slow rate of recovery of GDP growth in the United States since the Great Recession ended in the third quarter of 2009, of 2.3 percent per year through the third quarter of 2014 (U.S. Bureau of Economic Analysis 2015: Table 1.1.6). Economic conditions have been even worse in a number of other developed economies. What kind of explanation can we provide for this type of crisis?

First we should consider the contradictions of capitalism-in-general that can give rise to economic crisis via the crisis tendencies of capitalism. However, while the fundamental crisis tendencies of capitalism-in-general represent the starting point for crisis analysis, an analysis at that level of abstraction cannot serve to explain why a particular crisis occurs in a particular place at a particular time. Which crisis tendency will cause a crisis? What determines whether a crisis will be of the short-run or long-run type?

To proceed any further, one must undertake a more concrete analysis than that of capitalism-in-general. However, this does not mean that the next step is to examine state policies and contingent events. There is another level of analysis that lies between that of capitalism-in-general and that of policy and contingent events. That is the level at which one identifies the particular form of capitalism in a given place at a given time.

Capitalism has existed for several centuries, yet, while always capitalism, it has taken a series of distinct forms over time and space. Such a particular form, once established, lasts for an extended period of time. A particular form of capitalism is defined by particular economic and political institutions, associated dominant ideas, and a particular form of the main class relations of capitalism, most importantly the capital-labor relation. Each form of capitalism is still capitalism: a system of generalized commodity production and the wage-labor relationship through which capital appropriates surplus value from labor.

The forms of capitalism have been given a variety of labels in the Marxist literature: stages, social structures of accumulation, or modes of regulation. A common depiction of the main forms is a sequence that starts with competitive capitalism, followed by monopoly or finance capitalism after around 1900, then state monopoly, or regulated, capitalism after World War II, and most recently neoliberal capitalism (or globalized or financialized capitalism in some accounts) since around 1980.

This level of analysis is different from the level of state policy. A state policy is narrow and in principle subject to change at any time. By contrast, a form of capitalism is a coherent entity with mutually reinforcing elements, which make it relatively stable for a significant period of time. A form of capitalism will give rise to certain kinds of state policies, which are constrained by the existing form of capitalism and hence have a stability and coherence that is not captured by the level of analysis that focuses just on individual state policies.

The prevailing form of capitalism is central to analyzing capitalist economic crisis because it is a major determinant of which crisis tendency inherent in capitalism will emerge and cause a crisis, as well as determining whether the emergent crisis will be a severe, long-term one. Individual state policies are likely to be involved in the origin of every crisis, big and small, as are contingent events. Hence, the third and fourth levels of analysis are also relevant to the analysis of every crisis.

2. The Current Crisis

The initial outbreak of a severe economic crisis in 2008 in the United States had two sides, a financial crisis and a real-sector crisis (the Great Recession). This structural crisis has causal factors at all four levels: capitalism-in-general, the prevailing form of capitalism, state policies, and contingent events.

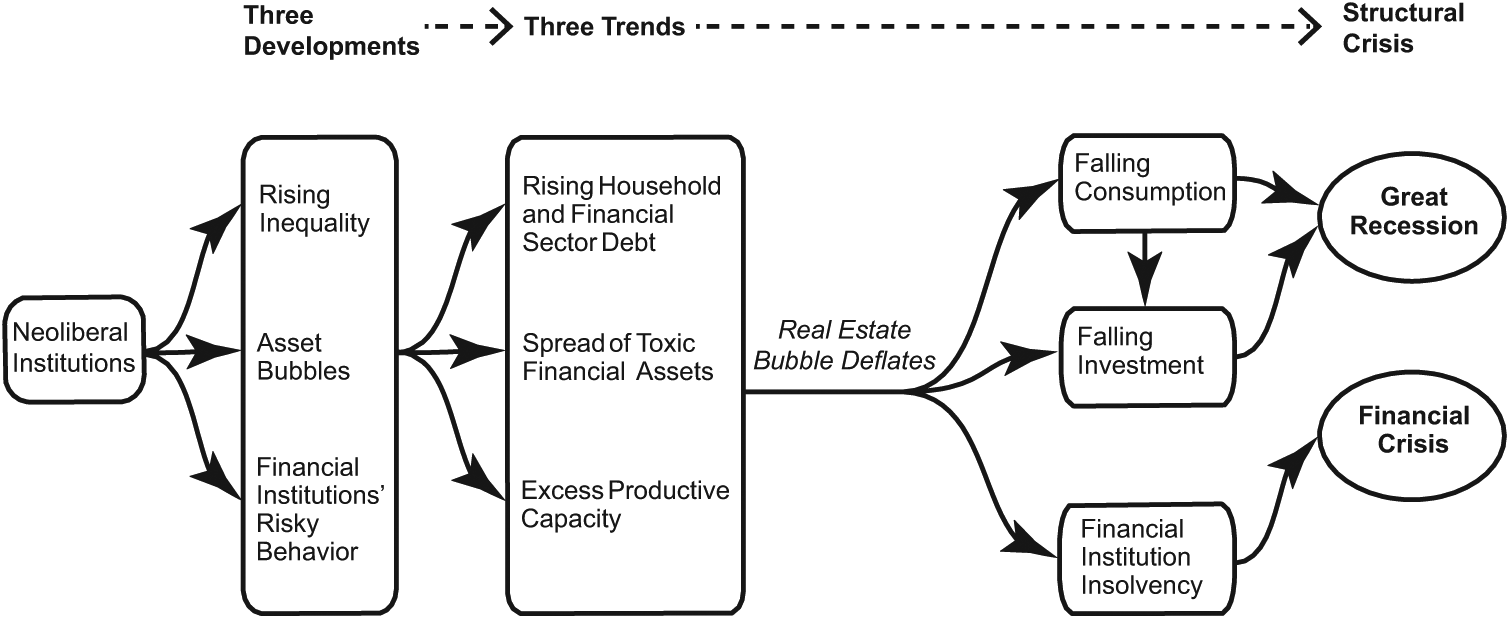

The analysis of the causes of the crisis in Kotz (2009) and in more detail in Kotz (2015: chapters 4-5) will be used here to show the role of the four levels of analysis. 2 Kotz (2009, 2015) offers the following argument. The period from 1979 to 2007 in the United States showed three important economic developments: 1) increasing inequality, in the form of a large and growing gap between profits and wages and rising inequality among households; 2) a series of large asset bubbles, with one in each decade; and 3) a shift in the practices of financial institutions toward speculative and highly risky activities.

Those three developments, interacting with one another, gave rise to three trends that were unsustainable over the long run. First, both household and financial sector debt relative to GDP rose from 1979 to 2007, with the former ratio doubling while the latter rose almost six-fold by the eve of the crisis (Kotz 2015: chapter 5, Figure 5.1). The rapid growth in household debt resulted from household borrowing to support consumer spending. By 2007 both sectors had so much debt that any drop in cash flow would be disastrous. Second, so-called “toxic” financial assets spread throughout the financial system. These included subprime and other unconventional mortgage-backed securities, collateralized debt obligations, and credit default swaps. They were toxic in that, far from reducing risk as their promoters claimed, these assets had values that could be sustained only if the housing bubble inflated forever.

The third long-term trend, of growing excess productive capacity, has not been widely noticed. Over time the share of industrial capacity in use trended downward. Figure 1 shows the capacity utilization rate in industry for selected business cycle peak years. The last three peak years since 1980 show a steadily declining rate of capacity utilization. By contrast, capacity utilization was higher and trended upward between the last two peak years through 1973 prior to the onset of an earlier long-run economic crisis. 3

Industrial Capacity Utilization Rate for Selected Business Cycle Peak Years

The spark that ignited the crisis, in both real and financial sectors, was the deflation of the housing bubble. In 2006 housing prices stopped rising, and in 2007 they began to fall. As a result, households could no longer borrow to support consumer spending and instead had to begin paying off loans, leading to a drop in consumer spending. The falling consumer spending, together with the effect of the housing bubble deflation on profit expectations, led to falling business investment. These two together turned expansion into contraction in the first quarter of 2008. Finally, the housing bubble deflation caused the market value of all those toxic securities to plummet, rendering most of the highly indebted big financial institutions insolvent and setting off a financial panic. The common belief that the financial crisis caused the Great Recession by cutting off funds for the real sector finds no support in the data, which show huge increases in cash in the hands both of financial institutions and nonfinancial corporations from the start of the crisis. However, the financial panic worsened profit expectations further, accelerating the decline in business investment and contributing to the severity of the recession.

Figure 2 illustrates this analysis of the causes of the current crisis. Three developments led to three unsustainable trends which, once the big asset bubble deflated, led to the real sector and financial sector crises. How can this analysis be interpreted in relation to the four levels of analysis of capitalism? Many Marxist analysts, as well as some non-Marxist ones, agree with some, or even all, of the causal links depicted in Figure 2 that go from the three developments to the three trends in the period 1979-2007 and to the resulting outbreak of the crisis in 2008. However, there is not wide agreement about how to interpret the cause of those three developments, which Figure 2 identifies as neoliberal institutions. How the causal relations in Figure 2 are interpreted in relation to the four levels of analysis of capitalism matters for our understanding of this crisis.

Causes of the Current Economic Crisis

3. The Form of Capitalism and the Current Crisis

The form of capitalism that emerged about 1980 is best characterized as neoliberal capitalism. 4 By examining the neoliberal form of capitalism, we can identify the specific features of the capital accumulation process in 1980-2007 and the contradictions in that accumulation process that led to the crisis in 2008. Important policy decisions that played a role in the crisis can be understood as flowing from the logic of the neoliberal form of capitalism.

Some analysts interpret the term “neoliberalism” as referring to a set of ideas (Foster 2007). Here neoliberalism is viewed as something broader, namely the form of capitalism that emerged after 1980. That form of capitalism is embodied in institutions, ideas, and the character of the main class relations of capitalism, particularly the capital-labor relation.

The institutions of neoliberal capitalism are located in the state relation to the economy, the labor market, the corporate sector, and the international arena. In the international arena neoliberalism is marked by free movement of goods and capital across national boundaries and a high degree of global integration of the production process. Institutions governing the state relation to the economy include deregulation of the financial sector and other previously regulated sectors, privatization of public enterprises and public services, renunciation of Keynesian aggregate demand management aimed at a low unemployment rate, cutbacks in social programs, and reduced taxes for business and the rich. 5 Other institutions include marginalization of collective bargaining, unrestrained competition among large corporations, and the penetration of market principles inside corporations (such as the hiring of CEOs from the outside rather than promotion from within).

The dominant ideas of neoliberal capitalism are a highly individualistic conception of society, the idealization of market relations, and a view of the state as an enemy of individual liberty, private property, and economic efficiency. The main class relation of neoliberal capitalism is a capital-labor class relation based on a high degree of domination of capital over labor, with capital able to set wages and working conditions with little effective resistance from labor. The extreme domination of capital over labor is the central feature of this form of capitalism, a relation that is enforced by the institutions and dominant ideas of neoliberal capitalism. 6

The neoliberal form of capitalism has suppressed some crisis tendencies while fostering others. Neoliberal capitalism undermines workers’ bargaining power, strengthening capital’s ability to raise the rate of exploitation over time. This tends to give rise to an upward trend in the rate of profit, although other factors could outweigh that effect. Basu and Vasudevan (2013) analyzed the movement of the rate of profit in the United States using a variety of measures, finding that almost every measure showed a long-term increase in the profit rate after the early 1980s rather than a decrease. Basu and Vasudevan also found that the long-term trend in the profit share was upward over this period, as one would expect given labor’s rapidly declining bargaining power. Thus, neither the tendency of the rate of profit to fall nor the reserve army/profit squeeze crisis tendency would be a strong candidate for explaining the crisis.

Since neoliberal capitalism gave rise to increasing inequality and a stagnating real wage for nonsupervisory workers after 1980 in the United States, it would seem to set the stage for a crisis of underconsumption. However, consumer spending trended upward, not downward, over the period 1979-2007, both relative to GDP and to disposable income, despite the rising inequality and a stagnating real wage (U.S. Bureau of Economic Analysis 2015: tables 1.1.5 and 2.1). Below I will argue that this suppression of the underconsumption crisis tendency resulted from the way the accumulation process proceeded under neoliberal capitalism.

The concept of neoliberal capitalism can explain the emergence of the three developments cited above that led eventually to the current crisis. The institutions and ideas of neoliberal capitalism fostered rising inequality, the shift in financial practices, and the series of large asset bubbles. Those three developments determined the form of capital accumulation in the neoliberal era, holding some of the fundamental crisis tendencies of capitalism at bay for several decades while limiting other crisis tendencies to the production of short-run crises only, and promoting a series of long economic expansions interrupted by relatively mild recessions that surprised many Marxist analysts. However, the contradictions embodied in those three developments led eventually to a structural crisis, in 2008.

Most of the institutions of neoliberal capitalism have directly promoted rising inequality, including the open world economy, renunciation of aggregate demand management (resulting in a higher average unemployment rate), deregulation of basic industries, privatization, cuts in social programs, tax cuts for business and the rich, marginalization of collective bargaining, and a market for corporate CEOs (which led to the skyrocketing of CEO pay).

The shift from traditional financial practices to pursuit of speculative and risky activities stemmed from several features of neoliberal capitalism. While deregulation of the financial sector was a central factor behind this shift, other factors were the intensification of competition in the economy, in the financial sector as well as the real sector; the expanding practice of hiring corporate CEOs from the outside; the shift from a long-term to a short-term time horizon for corporate decision makers; and the rise to dominance of free-market theories of finance. Furthermore, financial deregulation was not a lone government policy, but a part of the mutually reinforcing set of institutions, ideas, and class relations that compose the neoliberal form of capitalism.

Some regard asset bubbles as inherent in capitalism, in which everything is for sale. However, there were no big asset bubbles in the United States during 1948-80. The operation of the neoliberal form of capitalism can explain the series of large asset bubbles after 1980, as a consequence of the growing inequality and the transformed financial sector that in turn resulted from neoliberal capitalism. Rising inequality meant a growing flow of revenue into corporate profit and the incomes of rich households, which exceeded the available productive investment opportunities. Some of that flow found its way into an asset, which tends to start the asset price rising. The speculative, risk-seeking financial institutions of neoliberal capitalism enthusiastically supported speculation in assets, which enabled incipient asset bubbles to grow over time. 7

Thus, the neoliberal form of capitalism gave rise to increasing inequality, big asset bubbles, and a risk-seeking financial sector that together led eventually to the crisis in 2008. However, those three developments also explain the “successes” of neoliberal capitalism. Some Marxists intially doubted that neoliberal capitalism could bring a period of sustained capital accumulation since stagnating wages, along with the limited growth of state spending, would prevent the growing demand required to sustain accumulation. Yet the U.S. economy starting in the early 1980s produced three long economic expansions, in 1982-90, 1991-2000, and 2001-07.

The explanation for the long expansions is found in the same three developments. The imbalance between profit and wages meant a rising rate of profit which stimulated accumulation. The tendency for a shortage of demand to emerge was forestalled by debt-fueled consumer spending made possible by the other two developments, asset bubbles and risk-seeking financial institutions. The stock market bubble of the 1990s enabled upper income households to borrow against their inflating stock portfolios, causing an unusual lurch upward in consumer spending growth in the last three years of the 1990s that prolonged that expansion to become the longest one on record (Kotz 2003). In the 2000s an even bigger bubble in housing provided an appreciating asset against which a large swath of the population could borrow to support rising consumer spending despite stagnating real wages (Kotz 2009). The risk-seeking financial institutions found new ways to lend money even to low-income homeowners, which supported the growing debt-fueled consumer spending.

The mode of accumulation in neoliberal capitalism tells us which fundamental crisis tendency was operative in 2008. The debt-fueled consumer spending averted a crisis of underconsumption, but it did so by elevating consumer spending far above the trajectory that was sustainable based on ordinary household income. Firms invested in fixed capital to serve, and profit from, the rising sales due to debt-fueled consumer spending. This produced productive capacity that was required yet would become surplus once the asset bubble deflated and consumer spending returned to a normal relation to disposable income. That is, the crisis tendency of over-accumulation of fixed capital, one of the crisis tendencies of capitalism-in-general, was fostered by the neoliberal form of capitalism and was the operative crisis tendency in 2008. 8 By June 2009, after debt-fueled consumer spending had evaporated, the industrial capacity utilization rate fell to 66.9 percent, by far the lowest rate in the postwar period. 9

Individual policy decisions played a role in the process that led to the crisis. In 1998 the head of a regulatory agency, the Commodity Futures Trading Commission, called for regulation of financial derivatives. This led to a political battle that was won by Treasury Secretary Lawrence Summers, who was able to first postpone the proposed regulation and then insert a ban on any regulation of derivatives into the last financial deregulation act of that era, the Commodity Futures Modernization Act of 2000. This was followed by the very rapid spread of toxic financial derivatives in the United States and global financial system, which played a central role in the financial panic of 2008. Another example was the 2004 decision by the Securities and Exchange Commission to grant an exemption for the five biggest investment banks to the Commission’s rule regulating the maximum permissible level of debt leverage, on the grounds that giant investment banks were sophisticated enough to handle additional leverage. Over the following years the leverage ratio of four of the five rose to thirty to one. After 2007 all five teetered on the edge of bankruptcy, contributing to the financial crisis (Kotz 2015: 129). 10 While these two policy decisions contributed to the severity of the financial crisis of 2008, they were not isolated events but occurred in the context of the dominance of neoliberalism which strongly favored such policy decisions.

Contingent events also played a role in 2008. The failure of the big investment bank Lehman Brothers contributed to the financial panic in September 2008. If Lehman had been more cautious in the preceding years, it might not have failed. If the Fed had bailed Lehman out, the effect would have been lessened. However, neither alternative history would have forestalled the structural crisis.

4. Concluding Comments

The prevailing form of capitalism played an important role in the origin of the current crisis. An analysis that ignores the form of capitalism is left only with tendencies emerging from capitalism-in-general on the one hand and individual state policies and contingent events on the other. Since an analysis at the level of capitalism-in-general cannot determine which crisis tendency is operative in a given time and place, the analyst is stuck with either a highly abstract account that cannot be persuasive or an account that gives policies and/or contingent events a bigger role than they deserve. 11 The particular form of capitalism is a systematic entity, one that emerges from the contradictions of capitalist development. By including the form of capitalism in crisis analysis, we can show how a crisis emerges from the concrete form of capitalism rather than just policies and contingent events.

Every past severe structural crisis of capitalism has been followed by major institutional restructuring, and there is no reason to expect that the current crisis will be an exception, despite the current tenacity of neoliberalism. An advantage of the framework presented here for analyzing the current crisis is that it sheds light on the possible future directions of restructuring, which is helpful for developing political strategy for the socialist movement. This framework can be used to develop an analysis of the possible future directions of economic change, as in Kotz (2015: chapters 6 and 7), which argues that both theory and history suggest that one of three alternative directions of restructuring is likely to emerge in coming years: a right-wing nationalist and statist form of capitalism, a social-democratic form of capitalism, or a transition to socialism. Such an analysis can provide the forces that favor a transition to socialism with arguments in favor of that direction of change.

Footnotes

Author’s Note

This is a revised and shortened version of a paper that was presented at a session on “Marxist Perspectives on the Causes of the Crisis of 2008” sponsored by the Union for Radical Political Economics, at the Allied Social Science Associations convention in Boston, January 5, 2015. The original title was “Roots of the Current Economic Crisis: Capitalism, Forms of Capitalism, Policies, and Contingent Events.”

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

1

Marxist theory argues that a short-run crisis creates conditions that tend to eventually resolve the crisis and lead to the resumption of accumulation. However, it is argued below that in a long-run crisis that tendency is blocked.

2

Kotz (2009) and ![]() do not address the issue of concern here: the role of the four levels of abstraction in analyzing economic crisis.

do not address the issue of concern here: the role of the four levels of abstraction in analyzing economic crisis.

3

4

Some analysts argue that financialization is a better overall conception of post-1980 capitalism (Lapavitsas 2013), and others view globalization as the best way of framing post-1980 capitalism (Bowles et al. 2005). For a comparison of these three ways of understanding contemporary capitalism, see ![]() : ch. 2).

: ch. 2).

5

When the crisis broke out in the fall of 2008, the resulting panic led some of these institutions to shift temporarily. For example, the United States and the other major capitalist states introduced large fiscal stimulus programs. However, by 2010 the panic subsided and neoliberalism returned with an austerity policy.

6

7

Big asset bubbles can arise in other socioeconomic forms besides neoliberal capitalism. A huge real estate bubble has arisen in the cities of China recently although China’s economy is heavily state-regulated.

9

In addition to the excess productive capacity that was revealed only after debt-fueled consumer spending evaporated, ![]() showed that the capacity utilization rate in industry was lower in each successive business cycle peak in the neoliberal era through 2007 despite the debt-fueled consumer spending at the last two cyclical peaks. This suggests a tendency of over-accumulation of fixed capital even apart from the effect of asset bubbles on consumer spending. The observed over-accumulation of fixed capital likely results from the sense of euphoria among investors induced by big asset bubbles, leading to exaggerated expectations of future profits from investment in fixed capital.

showed that the capacity utilization rate in industry was lower in each successive business cycle peak in the neoliberal era through 2007 despite the debt-fueled consumer spending at the last two cyclical peaks. This suggests a tendency of over-accumulation of fixed capital even apart from the effect of asset bubbles on consumer spending. The observed over-accumulation of fixed capital likely results from the sense of euphoria among investors induced by big asset bubbles, leading to exaggerated expectations of future profits from investment in fixed capital.

10

Of the five biggest investment banks, one went bankrupt, two had to be acquired by larger institutions, and two were bailed out by the government.

11

An analysis of crisis tendencies in capitalism-in-general can be combined with a study of the empirical data to seek to find out which crisis tendency operates in a given period. ![]() followed that approach. While that approach can yield useful information, it cannot explain why one particular crisis tendency was the operative one in a particular time and place.

followed that approach. While that approach can yield useful information, it cannot explain why one particular crisis tendency was the operative one in a particular time and place.