Abstract

By examining digital labor platforms that connect customers with gig workers, we attempt to solve the puzzle concerning why these labor platforms, such as ride-hailing companies and food delivery companies, continue to suffer weak profitability even though they promise a more efficient way to mobilize and utilize the platform’s labor force. Stylized facts on the profitability of the top ten global labor platforms and a descriptive analysis of their cost structures are presented. We further argue that the modes of production and competition inherent in digital labor platforms are critical to this profitability puzzle because they determine the upper limit of surplus value extraction in production and the heavy financial burden of profit generation for labor platforms.

1. Introduction

The platform economy—and its rapid growth since 2012—has gained much attention from academia, regulators, and the general public. It is an economic form and a set of business models in which producers and consumers produce, transact, and distribute under the organization and coordination of digital platforms. The application of digital technologies, the proliferation of the internet, and the widespread diffusion of mobile devices have brought about many transformative life experiences. Nevertheless, the widely claimed potential of the platform economy cannot be simply justified by technological innovation. The platform economy relies on platform companies to operate; like traditional capitalist companies, platform companies depend on profits to survive and grow. In addition, without focusing on the bottom line, platform companies are likely to encounter declining interest from existing and future investors. Therefore, to understand the behaviors and dynamics of the platform economy, it is necessary to investigate the profitability of the platform companies.

This research focuses on a particular type of platform company that connects customers with gig workers who perform discrete tasks or provide labor-intense services. Labor platforms are ubiquitous and transform how people move around (Didi, Lyft, Uber), deliver and receive food (DoorDash, Grubhub, Meituan), and complete other everyday tasks (Taskrabbit, Amazon, Mechanical Turk). The past decade has seen a fivefold increase globally in the number of digital labor platforms (International Labour Organization 2021), which have contributed on a massive global scale to an ever more intimate connection between the virtual and real economy. Moreover, after the Great Recession, labor platforms are also treated by policymakers in many economies as crucial job creators.

More importantly, digital labor platforms are recognizably transforming the world of work. Acting as intermediaries that connect service/product providers and customers, platform companies can largely avoid employers’ traditional obligations by outsourcing and pursuing lean production “in heightened form” (Srnicek 2017: 90; Zwick 2018). They are highly capable of mobilizing and utilizing their labor force thanks to flexibility, regulatory arbitrage, and algorithmic management. Living in the age of high unemployment and underemployment, workers are increasingly subject to precarious working conditions shadowed by flexibility, while platform companies take advantage of gaps in labor regulations. Digital platforms adopt algorithmic management in allocating jobs and monitoring and controlling the labor process, leading to the intensification of work and the deteriorating job experience (Rosenblat and Stark 2016). Because working through digital labor platforms is typically individualized and segmented, workers face significant impediments when trying to organize for collective bargaining, which further prevents them from better compensation and protection (Lei 2021). These technological, institutional, and organizational changes work predominantly in favor of platform companies and should therefore expectedly contribute to a high profitability potential.

In reality, however, this expectedly high potential does not materialize as actual high profitability, nor does this highly extractive labor practice produce a successful platform business model with high profitability that can reproduce and sustain itself. These expected results are, in fact, far from the truth based on our detailed analysis of the financial statements of the leading labor platform companies. 1 Herein, we propose that a profitability puzzle exists in the dominant business model of labor platforms: Why do the labor platforms we use today fail to generate significant profits despite their highly extractive labor practices? In section 2, we present the stylized facts about the profitability of major labor platforms and provide a descriptive analysis of the cost structure. In section 3, we dive deep into two critical aspects of the labor platforms—the mode of production and the mode of competition—to make sense of the profitability puzzle. Section 4 discusses the implications and concludes the article.

2. Stylized Facts

We use the financial data from the ten largest global labor-based platform companies by gross transaction value (GTV) and market capitalization. They operate online food ordering and delivery or ride-hailing platform businesses in North America, Europe, East and Southeast Asia, and Latin America. By the end of 2022, these companies as a whole were valued at $264 billion. This aggregated number, nevertheless, is even smaller than the market capitalization of the smallest company (Meta) among big tech giants, suggesting that these labor platform companies are only medium or small players in the overall platform economy. However, labor platforms play a crucial role in employment. Although it is debatable whether they have created new jobs or just replaced old jobs on their platforms, today these companies organize and coordinate millions of drivers, couriers, and other gig workers across the globe.

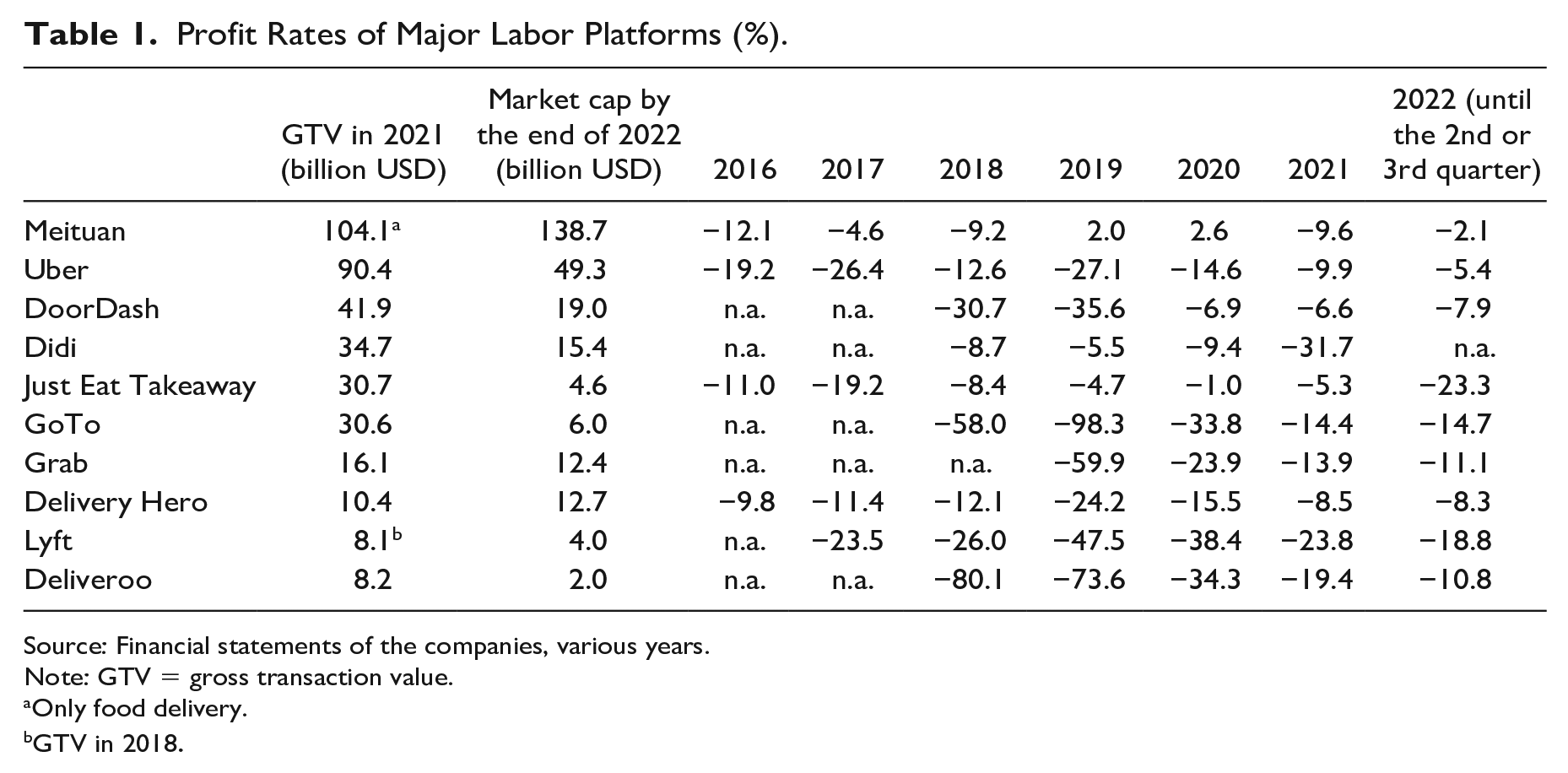

Profitability herein is measured as a ratio between profits (losses) from operations and total assets in order to focus on the primary businesses of platform companies and exclude the impacts of financial investments and income taxes on profitability. Table 1 reveals the profitability of these 10 labor platform companies ranked by their GTV. All of them have suffered weak profitability or, in fact, significant losses over the years except for Meituan in 2019 and 2020 only. The simple average of all the profit rates in table 1 is −20.7 percent. Companies such as GoTo, Grab, and Deliveroo endured extreme losses, with profit rates even lower than −50 percent. During 2016–2022, although almost all the companies suffered losses, large-scale (measured by GTV) companies on average were more profitable than smaller ones. This positive correlation between scale and profitability reflects the fact that platforms may gain more monopoly power through the economies of scale and network effect if they successfully expand their scale relative to their competitors.

Profit Rates of Major Labor Platforms (%).

Source: Financial statements of the companies, various years.

Note: GTV = gross transaction value.

Only food delivery.

GTV in 2018.

Most labor platforms in table 1 experience a generally declining trend in loss. Figure 1 presents the average profit rates for a balanced sample of the four companies that have data over the period of 2016–2022 (Meituan, Uber, Just Eat Takeaway, and Delivery Hero) and an unbalanced sample of all 10 companies. For each sample and each year, a simple average and an asset-weighted average are both presented. It is interesting to note the divergence between the unweighted and weighted averages of the unbalanced sample. The unweighted average exhibits a significantly larger decline in 2018 and 2019 than the weighted average, which is driven by the largest asset-heavy companies, particularly Meituan and Uber. This divergence reflects the fact that smaller companies, as new entrants into the platform economy, are more aggressive than their asset-heavier counterparts and chase operational scale by paying massive subsidies to attract and retain gig workers and customers. Such practices have recognizably become an alarming fashion in platform competition, leading to high costs of operation and low profitability (Li and Qi 2022).

Profit rates of major labor platforms.

As figure 1 shows, average profits by all four measures improved from 2019 to 2022. One should be cautious in interpreting this trend as a permanent recovery in profitability because this trend overlaps with the COVID-19 pandemic, which has significantly stimulated contactless services that labor platforms provide. The spike in unemployment and underemployment as well as the suppressed real wage also contributed to the rapid growth of these platforms. Despite the impacts of the pandemic, most labor platform companies still accrued heavy losses, which only highlights the inherent constraints of labor platforms.

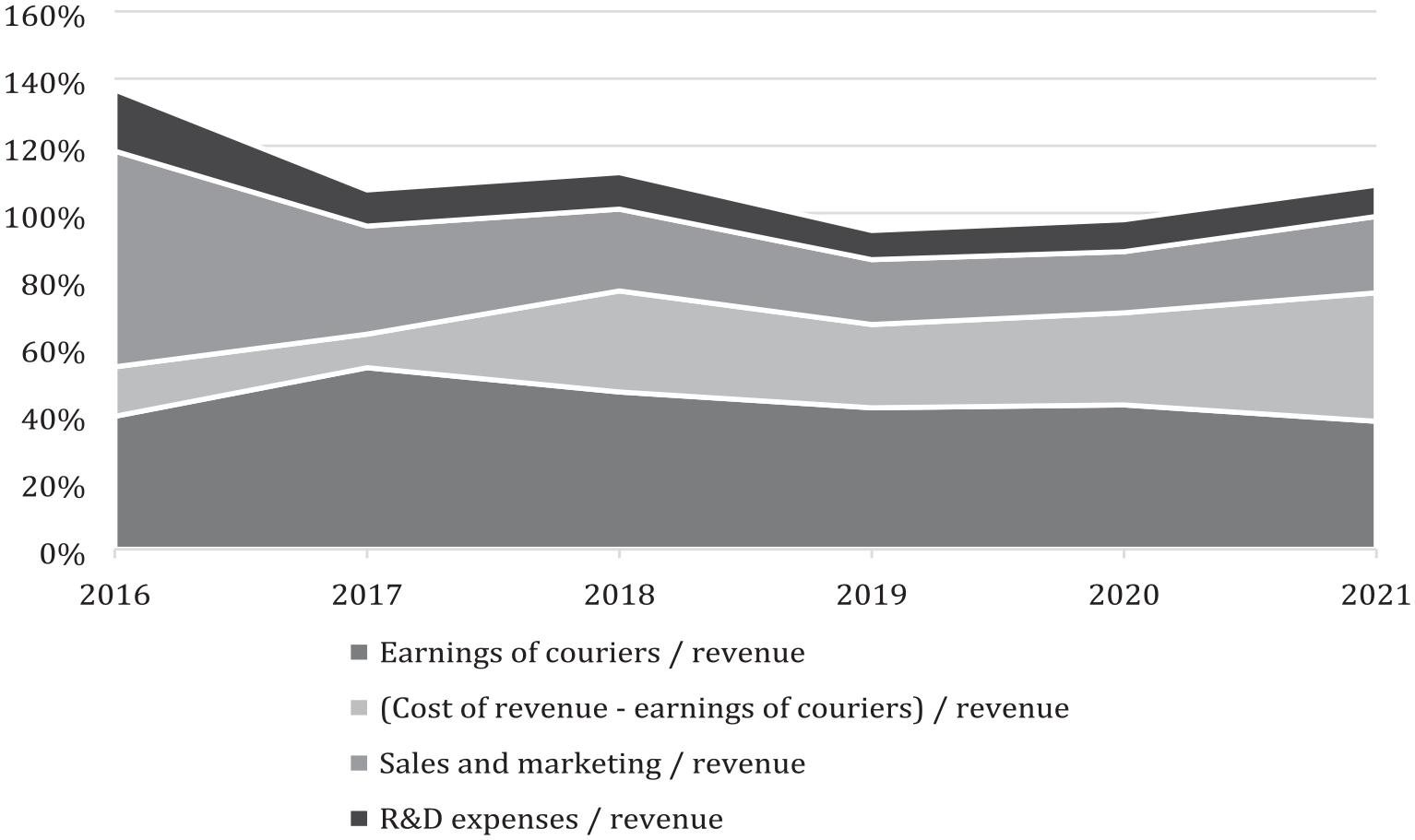

Consequently, a descriptive analysis of the cost structures of labor platforms is needed to further explore the connections between the major costs they incur and the business strategies they adopt. We focus on the top two labor platform companies—Meituan and Uber—that have so far released detailed data about their costs, especially the costs related to platform labor. 2

Figure 2 presents the major costs of Meituan. The earnings of couriers category has the highest ratio over revenue, an average of 44 percent from 2016 to 2021. Earnings of couriers represent the platform labor costs that Meituan bears in food delivery, the core business of the company. Earnings of couriers is on average equivalent to 81 percent of food delivery revenue, thereby limiting the room for profits and other costs of the core business. 3 Nevertheless, Meituan has adopted a strategy of building a platform ecosystem on the basis of food delivery by developing a variety of other services—such as retailing, restaurant logistics, hotel and restaurant booking, travel, bike sharing, and so on. The contribution of food delivery in revenue declined to 54 percent by 2021. If the strategy is successfully implemented, it will enhance the utilization rate of the time of couriers by dispatching more kinds of delivery orders to them; it will also increase user stickiness or loyalty and the platform’s monopoly power, which in turn will allow the platform to charge restaurants, grocers, hotels, and other sellers more commission and advertising fees.

Major costs of Meituan.

However, the implementation of the ecosystem strategy demands massive investments in advertising and customer incentives. This requirement, in fact, explains why sales and marketing is the second largest cost, equivalent to 30 percent of revenue. Cost of revenue (excluding earnings of couriers) is, on average, equivalent to 24 percent of revenue, which is largely related to the expansion of its retail business, a crucial step in Meituan’s ecosystem building. These three cost categories add up to 98 percent of revenue, leaving only 2 percent of revenue to break even before covering research and development (R&D) expenses, administrative expenses, and other costs. However, when R&D expenses take on average 11 percent of revenue—and given other costs in the business operation—a heavy loss can be easily anticipated.

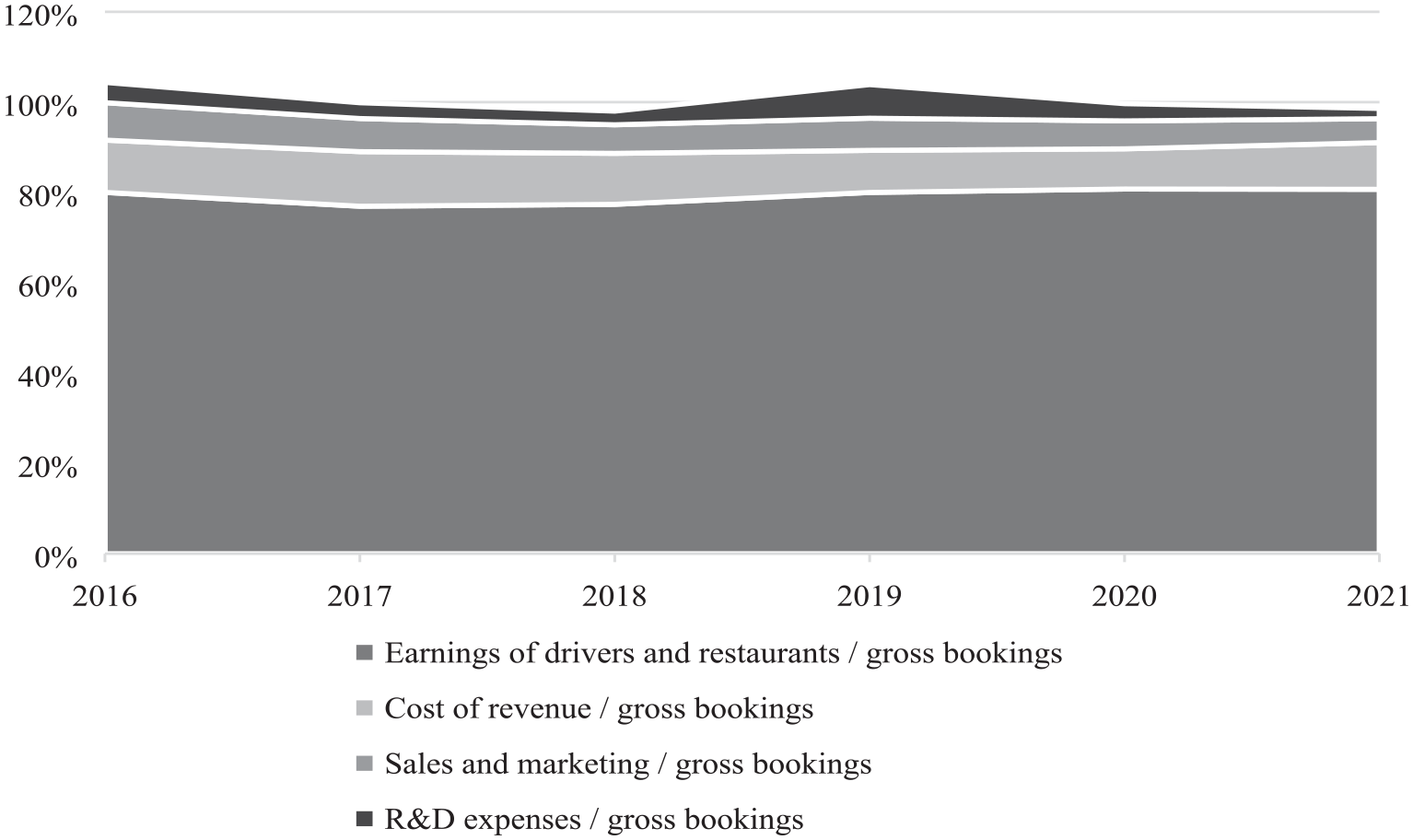

Figure 3 presents the cost structure of Uber, which runs both a ride-hailing platform and a food delivery platform. Earnings of drivers and restaurants 4 on average is about 79 percent of the gross bookings (i.e., GTV) on Uber platforms from 2016 to 2021. The size of this cost relative to gross bookings has been stable despite significant growth in gross bookings. The second largest cost is cost of revenue, amounting to 11 percent of gross bookings. As defined in Uber’s financial statements, cost of revenue primarily consists of insurance costs, credit card processing fees, bank fees, data center and networking expenses, mobile device and service costs, and so forth. Another 7 percent of gross bookings are used to cover sales and marketing costs, indicating that Uber must constantly invest in advertising and provide customers incentives to maintain and strengthen its market power. All three parts add up to 97 percent of gross bookings. Because R&D expenses take another 4 percent of gross bookings, there is no room for Uber to achieve positive profits.

Major costs of Uber.

Although the empirical analysis above presents the weak profitability of labor platforms—ubiquitous across geographical locations and persistent over years—it seems to contradict many academic findings and public concerns that gig workers on these labor platforms are largely undercompensated and overworked (Montalban, Frigant, and Jullien 2019; Qi and Li 2020). In order to reconcile and make sense of the contradiction between the extractive labor practice and the low actual profitability of labor platform companies, we argue in the following section that the profitability puzzle can be explained by the modes of production and competition, two critical components underlying digital labor platforms.

3. Explaining the Puzzle from the Modes of Production and Competition

3.1. Mode of production

Digital labor platforms such as Uber and Didi do not perform well in controlling costs related to platform labor. Meituan can reduce the proportion of labor costs only by expanding aggressively into non-labor-based industries. The incompetence in controlling labor costs is a necessary consequence of the way labor platforms shape and configure the technological and organizational dimensions of the production process.

Digital labor platforms utilize information technologies to match customers on the demand side to gig workers and merchants on the supply side. Platforms facilitate transactions by automatically collecting and analyzing data from both sides and dispatching tasks to specific workers based on certain standards (e.g., the distance between the worker and the customer). With artificial intelligence (AI)–based algorithms, platforms can not only match current demand and supply but also make precise predictions on future demand and provide guidance for the temporal and geographical allocation of production capacity. Platforms can extract and process data to personalize marketing based on up-to-date customer information and behaviors, thus shaping customer preferences and creating demand. Data and information technologies are critical resources in the platform economy. When platforms monopolize these resources, they control the market access of workers to customers. Therefore, the income of platforms can be viewed as a form of rent arising from owning data assets as well as the technologies that enable platforms to utilize the data (Durand and Milberg 2020; Foley 2013; Rotta 2022). Platforms reproduce their positions as digital landlords by constantly collecting data, transforming data into assets, and upgrading their technologies. The amount of rent that a platform can receive largely depends on how exclusive its control is over data and leading information technologies.

Despite the similarities between platforms and traditional landlords, there is a substantial difference. Rent can be consistently extracted only after value and surplus value is produced; in contrast to traditional landlords, platforms actively engage in the production process in which the sources of rent are located. Information technologies are used by platforms to monitor and discipline gig workers. Platforms collect multidimensional data about the labor process of workers with apps, GPS, payment records, cameras, and customer evaluations. Algorithmic management utilizes data such as working time, work schedule, service quality, transactions, earnings, and job history to customize incentives to targeted workers and control the labor process (Kellogg, Valentine, and Christin 2020; van Doorn and Badger 2021). These algorithms, along with non-algorithm rules, place geographically dispersed workers under intensive supervision. This disciplinary system on labor platforms is particularly effective in lengthening the working day and enhancing workers’ responsiveness when they lack alternative job options and must rely exclusively on platform-mediated jobs.

In this sense, platforms shape the technologies of the production process in a way that primarily enhances the utilization of labor time and imposes algorithmic management over the labor process. A gig worker receives more orders on the platform than in the traditional mode of production. Algorithmic management disciplines workers to provide adequate and qualified services. Nevertheless, it is crucial to note that the technologies barely affect the production process in the narrow sense (i.e., the process in which workers perform labor to finish each task). For instance, a ride-hailing driver picks up customers and drives the car to the destination in the same way as a taxi driver provides services. A delivery worker in the platform economy finishes an order in the same way as the task is done in the traditional offline economy. The technologies adopted by the platform have changed how workers receive information about the job, how workers allocate labor time, and how workers get disciplined, but not how workers perform labor and finish tasks. The latter remains largely unchanged relative to the traditional form before the platforms appeared.

The technological transformation of the production process is associated with the organization of labor. It is widely recognized that platforms organize gig workers without establishing a formal employment relationship, which helps platform companies evade legal responsibilities associated with formal employment and makes the supply of labor more flexible (Schor and Attwood-Charles 2017). A crucial result of this organizational arrangement is that platforms connect millions of gig workers without changing the technologies with which gig workers finish tasks. In most cases, gig workers purchase key means of production used for their platform jobs, which saves platform companies from massive fixed investments; nevertheless, it also means that workers on the platform tend to use the same means of production as self-employed workers use in the traditional economy. For instance, vehicles in the ride-hailing industry have no significant technological differences from taxis and cabs in terms of gas efficiency, service life, or safety. Gig workers on the platform are not technologically more competent than self-employed workers in the traditional economy in finishing tasks.

To illustrate the impact of the mode of production on profitability, we express the total profits of a labor-based platform using a simplified equation:

where:

In the case of ride-hailing or food delivery,

The rest of the three parameters

The technologies used for supply-demand matching and algorithmic management can effectively extend working time

3.2. Mode of competition

The upper limit of total effective labor effort (

We adopt a theoretical framework in which production and competition, as well as their interactions, shape firms’ strategies, the result of which is profitability. Regarding production and competition, Marx, discussing his theories on the absolute and relative surplus value, set a good example. For Marx (1976), production has a fundamental role in the economy; the mode of production in capitalist firms affects and is also affected by the competition among capitalists. The production of absolute surplus value involves a vicious cycle between intense exploitation (extended work hours, increased labor intensity, etc.) and mutually harmful competition among capitalists, whereas the production of relative surplus value implies constant work hours (in most cases) and mutually beneficial competition among capitalists. Similarly, Crotty’s (1993) theorization of competition regimes also involves the transition in the modes of accumulation (production) from capital widening and capital deepening.

These insights shed light on the understanding of the relationship between production and competition in the platform economy. Labor platforms not only, as elaborated above, have limited capacity to control labor costs (relative to revenue) but also face low barriers to entry, exposing incumbent platforms to the persistent challenges of new entrants. The key set of information technology used by labor platforms is widely recognized as soft; it is not difficult for new entrants to overcome the technological barriers. In fact, it is a common practice for platform companies to rent important infrastructure (cloud computing, payment instruments, etc.) from big tech companies, thereby further lowering technological barriers to entry. More importantly, labor platforms connect gig workers without offering a formal employment contract, thus changing the way these workers finish tasks or providing them with means of production. All these features of production allow new entrants to achieve an explosive expansion that rapidly erodes incumbents’ market shares, especially when the new entrants invest massively in customer and worker incentives.

The incompetence in controlling labor costs and the low barriers to entry jointly put labor platforms in coercive competition (Crotty 1993) or an expand-or-die situation. Competition from new entrants and internal labor-cost pressures lead to cutthroat competition in which platforms engage in price wars to maintain market shares. These wars can be major events in the market; they can also happen on small scales in daily competition among platforms. The labor cost associated with price or subsidy wars becomes a crucial factor that leads to losses. It is noteworthy that financial capital (venture capital, private equity, sovereign wealth funds, etc.) plays a critical role in supporting platforms in the fierce competition (Li and Qi 2022). Financial capital tends to maximize the market capitalization of platform companies by assisting or compelling them to expand and achieve market monopoly. The financial value imperative prioritizes expansion and monopolization over profitability, leading to massive and persistent losses.

Expansion and monopolization through price or subsidy wars are costly and unsustainable. We can consider this strategy a low-road strategy in platform rivalry. It is implemented only when platforms are cornered in an expand-or-die situation and are coerced by each other to expand. Along with the low-road strategy, platforms in practice also adopt three high-road strategies to avoid price wars and seize more economic power, all of which have implications on profitability. 5

First, the platform may implement a strategy to improve labor extraction and maximize the difference between the effective labor effort of gig workers and their earnings. Using equation (1), this strategy corresponds to an increase in

Second, platforms may also adopt labor-replacing technologies. A typical example is ride-hailing platforms’ exploration of self-driving car technologies, aiming to reduce the costs of drivers to zero. However, these novel technologies demand massive and continuous R&D investment, which suppresses platform profitability by increasing

Last, platforms may pursue a monopolization strategy in which the platform engages in both labor- and non-labor-based services (particularly e-commerce) to build up a platform ecosystem and more monopoly power. The labor-based services play an infrastructural role in forming a massive customer base. This base becomes a critical resource (Li and Qi 2022) that generates platform power, so more advertising and commission fees can be charged on the platform. This monopolization strategy demands platforms expand and permeate into other aspects of customers’ daily lives; it usually involves the development of super apps that require more attention and time from users. However, these investments are costly in terms of advertising expenses and customer incentives. Some unprofitable investments are made only for the purpose of increasing user stickiness or loyalty in a highly competitive environment. Thus, many platforms usually incur heavy losses implementing this strategy.

Therefore, the mode of competition inherent in labor platforms compels them to engage in cutthroat price wars, further extract worker efforts, and heavily invest in R&D and other ecosystem-building efforts. Although some strategies cannot be pushed without limits, others inevitably increase the financial fragility of digital platforms.

4. Conclusion

This study addresses the weak profitability puzzle of digital labor platforms and investigates the modes of production and competition in an attempt to solve this puzzle. Although certain technological efficiency in the platform economy is undeniable, we call for a closer examination of how platform technologies shape and configure certain aspects of the production process while leaving others untouched. It is argued that those technologies are primarily related to market matching and labor discipline rather than the way workers perform labor and finish tasks, which have imposed limits on the potential of profitability. These limits and the fierce competition among platforms tend to corner them in an expand-or-die situation. Both low-road and high-road strategies for competition have inevitably generated a heavy financial burden and significantly jeopardized platform profitability.

Our analysis also sheds light on how to build a more cooperative and viable platform economy as an alternative. Both high labor precarity and low platform profitability challenge the sustainability of the current platform model. Although it is often pointed out how imperative it is to reform the current organizational and distributional aspects of labor platforms, our findings emphasize the crucial importance of a profound transformation in the direct production process of the platform economy, particularly the technological aspect. The prevailing labor platforms are designed by platform capital to utilize millions of cheap workers conveniently and flexibly, which results in millions of precarious jobs. A new form of labor platform should utilize technology in a way that creates high-quality jobs that can integrate workers’ skills and technologies in the production process. This direction may help businesses imagine and develop a better alternative with platform technologies that fosters a cooperative platform intent on improving labor conditions rather than capitalizing on labor extraction.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

1

During our revision of this article, Silicon Valley Bank, the bank that had been deeply interwoven to the tech sector, including the platform economy, collapsed on March 10, 2023, further revealing and adding to the vulnerability of these digital platform companies.

2

The cost structures of Didi and DoorDash are not presented here because of the word limit but are available upon request.

3

4

Because of data availability, the earnings of restaurants cannot be excluded from the category, but we assume its proportion is stable over years.

5

These strategies—which in no way guarantee sustainable profits—should be viewed as platforms’ attempts to tackle the problem of labor costs rather than interpreted as recommendations from the authors on how to build a sustainable and inclusive economy.