Abstract

This paper examined the impact of financial integration on economic growth in Southern African Development Community (SADC) and Economic Community of West African States (ECOWAS) countries over the period 1993–2013. Using the Panel ARDL PMG Model developed by Pesaran and Shin, other control variables (trade openness, inflation, government expenditure, and institutional quality) were captured in the model. It was found that there is a significant and positive impact of financial integration on economic growth in the ECOWAS region in the long run. Whereas, even after controlling for necessary variables, financial integration exacerbates negative and insignificant effects in determining economic growth in the SADC region, both in the short run and long run. The insignificant and negative impact of financial integration on the region’s economic growth was attributed to several possible factors, including the low level of financial development in the SADC region, which is unconnected with the poor level of governance, unstable and fragile financial stability, or low creditworthiness, that are prevalent in developing countries like those in SADC countries. The findings suggest, amongst others, that increasing financial integration could improve the productive capacity of the economy, including more investments and the efficient allocation of capital, thus enhancing economic growth in these regions. This paper sheds new insights on a better evaluation of the past and present theorizing on the subjects of financial integration and economic growth, especially in comparing the separate effects on the economies of the SADC and ECOWAS countries.

Keywords

Introduction

The consequences of financial globalization on growth have long been a source of discussion among academic economists and practitioners. The elimination of restrictions on international capital transactions has been hailed as a source of growth in some cases and condemned for causing financial instability and crises in others. This argument has left the findings in the finance–growth nexus literature contradictory.

When it became clear that the lack of well-developed financial systems was impeding progress in most developing countries in the early 1980s, financial development and integration became the most important reform strategies for most developing countries. As a result, cross-border capital flows have exploded in the last three decades. The Southern African Development Community (SADC) and the Economic Community of West African States (ECOWAS) regions are no exception to this phenomenon and have worked to promote regional financial integration in all spheres among member countries since its inception. For instance, as of 2015, the regional bloc had signed 26 protocols covering a broad range of topics, including commerce, finance, and investment, energy, transportation, and communication, amongst others (Mlambo, 2015).

International capital transactions between countries have since increased from roughly 5% of global GDP to over 20% during that time. The intensification of the financial globalization (FG) process has inevitably drawn economists' and policymakers' attention to the actual macroeconomic consequences of unrestricted capital flows. Their true benefits, particularly for long-term economic growth, are hotly debated. Although receiving countries benefit from capital flows because they get access to lower-cost finance, the history of international financial integration (IFI) has not always been smooth or risk-free. Surges in capital inflows, particularly in emerging nations, can create serious problems such as significant currency appreciation pressures, asset price bubbles, and rapid loan growth, all of which can cause financial system fragility. The Latin American and Southeast Asian financial crises of the 1980s and 1990s exemplified the destabilizing implications of huge changes in capital flows. More recently, the financial upheaval that industrialized countries have experienced has prompted economists to take a more cautious approach to financial globalization. The difference this time was that the crisis began in the developed financial systems of affluent economies, which had previously been seen to be relatively resilient, and highlighted the worldwide monetary and financial system’s vulnerabilities as a whole. It does not appear to matter how capital moves, Rodrik and Subramanian (2008) observe. The fact that capital travels in significant amounts across borders—the famed feature of financial globalization—appears to augur disaster, “they noted, recommending that international capital flows be curtailed”. In light of this, the International Monetary Fund recently approved capital controls as a legitimate policy tool to assist countries in managing significant capital inflows. Although the organization remains a strong proponent of international finance’s positive role in fostering global economic efficiency, it is increasingly aware that if left unchecked, the process of financial globalization could have negative consequences.

These arguments and deliberations give rise to the following questions: Do economies that are financially more open grow faster than those that are closed, precisely because of their openness to financial markets? Are policies that promote boosting international financial integration, and hence financial globalization, sensible? Does financial integration impact differently on the economies of ECOWAS and SADC countries? These questions raise important issues from both a theoretical and a policy perspective. As a result, it is not surprising that the number of views on the subject is high and growing. Therefore, this paper represents the first attempt to consider the comparative analysis of the impact of financial integration on the economic growth of the ECOWAS and SADC regions.

After this introduction, the paper is divided into five parts. The section Literature Review presents the literature review. Stylized facts are given in the section Stylized Facts. The variables, data, and methodology are discussed in the section Variables, Data, and Methodology. The empirical findings are presented in the section Empirical Results and Analysis. The sixth section concludes.

Literature Review

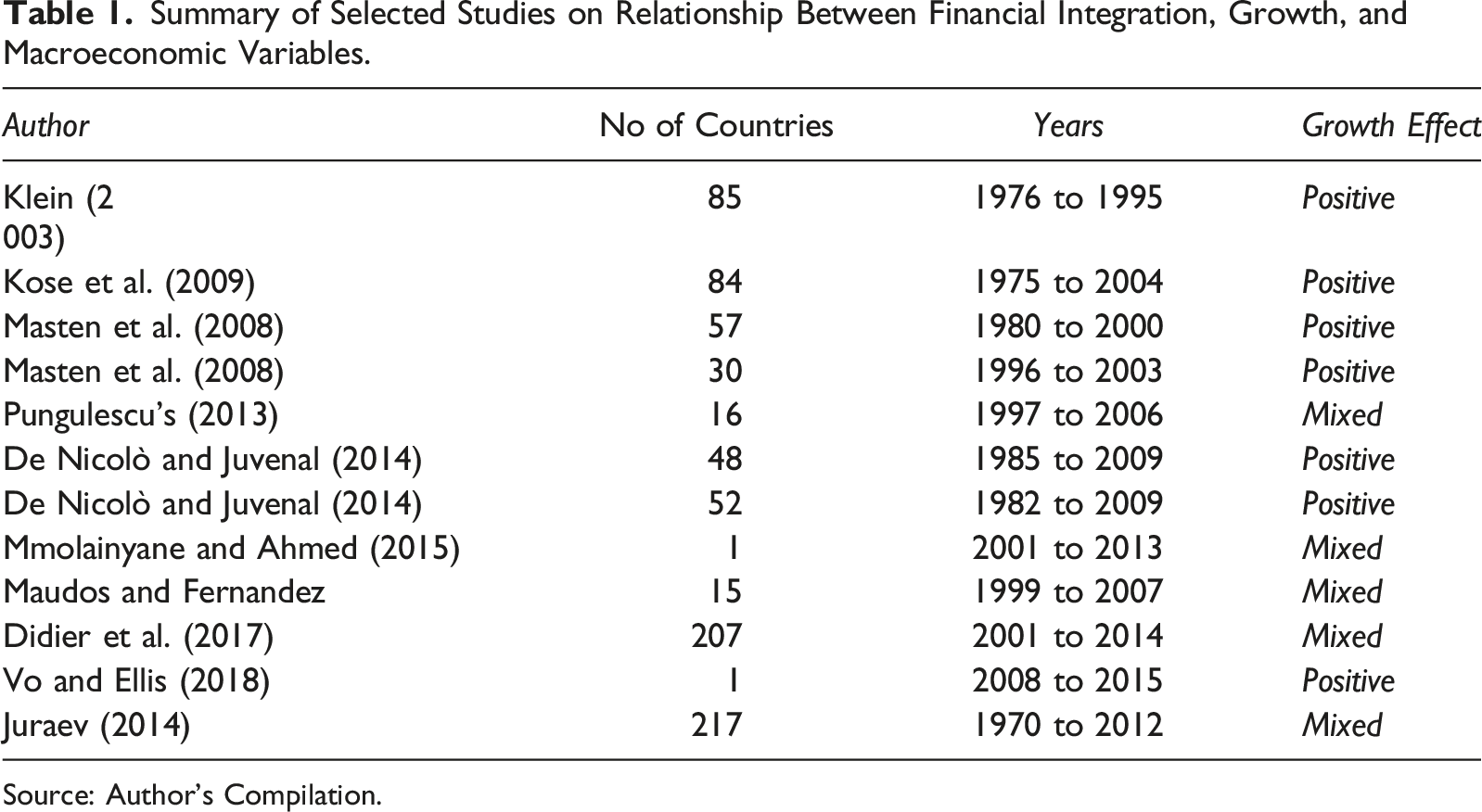

This section examines the literature related to financial integration and economic growth. Previous empirical studies on the impact of financial integration have not yet been widely discussed and are scarce in the ECOWAS and SADC regions. For example, the significance of financial integration on growth is rather mixed (Juraev, 2014).

Theoretically, financial integration is to the degree that economies are fully integrated and without any forms of cross-border restrictions (Baele et al., 2004); barriers pertaining to international investments and capital mobility are removed (Karpoff et al., 2017). According to Hajilee and Al Nasser (2017), the financial market is an important channel affecting economic growth. Theoretical studies provide inconclusive evidence of the nexus between financial integration and economic growth.

According to the standard one-sector neoclassical growth model, the typical theoretical channel via which financial integration influences economic growth is the augmentation of capital. In other words, mainstream theory predicts that financial integration will result in capital flows from capital-rich economies to capital-poor economies, as the latter should have greater returns on capital. In theory, these financial flows should supplement limited domestic savings in capital-poor nations and allow for more investment by lowering capital costs. Even in the fundamental neoclassical model, Henry et al., 2007 argues that the finance channel should represent only a temporary, rather than permanent, boost in growth from financial integration. However, it is unclear how important this distinction is going to be in studies that look at growth over just two or three decades. Certain forms of financial flows may also result in technology spillovers and act as a conduit for absorbing managerial and other forms of organizational skills from more advanced economies.

Newer studies stress the relevance of indirect channels, stating that it is the collateral advantages of these flows, not simply the direct financial flows, that generate the growth benefits of financial globalization (see Kose et al., 2006). Improvements in institutions (defined generally to encompass governance, the rule of law, and so on) and better macroeconomic policies are two of these indirect pathways. The impact of financial integration on the development of the financial sector is discussed by Levine (2005) and Mishkin (2008). Stulz (2005) examines institutional quality and suggests that globalization lowers certain agency problems by lowering the cost of outside financing, generating incentives for enterprises to employ more external finance to strengthen their governance. According to Gourinchas and Jeanne (2006), financial integration can impose macroeconomic policy discipline by increasing the benefits of good policies and catalyzing political support for reforms, whereas Bartolini and Drazen (1997) argue that exposing a country to such costs through increased financial openness can signal a country’s commitment to better macroeconomic policies.

Despite these optimistic viewpoints, pessimistic studies suggest that financial integration hinders growth because nations with less developed institutions are more vulnerable to economic shocks (Boyd & Smith, 1992). Given the abundance of cross-country studies, many have looked at the direct and indirect effects of financial integration on economic growth. For example, Bekaert et al. (2005), for example, look at the direct influence of the financial-growth nexus and show that financial integration boosts economic growth across a range of variables. Indirect impacts have also been studied in a number of studies. For example, Mmolainyane and Ahmed (2015) look at the direct and indirect effects of financial integration and expansion. They discover that integration has a direct and positive impact on growth, while their indirect observations show that integration has a positive impact on growth through increased financial accessibility. In a similar context, Masten et al. (2008) argue that financial integration has a positive influence on growth after a certain level of financial development. According to Edison et al. (2002), factors including GDP per capita, banking sector development, and low levels of corruption influence the integration-growth nexus. Past empirical studies on the effects of financial integration on economic growth have produced ambiguous conclusions. Previous empirical studies on the integration-growth nexus have focused on the effects of capital controls on economic growth. These studies imply that financial integration has no significant impact on growth. According to Klein (2003), capital account openness benefits 85 middle-income nations, but it has little effect on high-income or least-developed countries. Kose et al. (2009) investigate the impact of financial integration in developed and developing nations, finding that financial integration boosts consumption in various developing countries. In this vein, De Nicolò and Juvenal (2014) provide evidence of a positive relationship between financial integration and macroeconomic stability. It is worth noting that studies like Pungulescu’s (2013) show that pre-crisis financial integration was higher; but, during the post-crisis period, both new and old EU member states experienced significant integration reversal. In a similar study, Maudos and Fernandez (2015) examined how the global financial crisis, which began in 2007, has impacted integration and growth. Their findings show that until the crisis, advances in integration contributed a considerable portion of financial development, with a positive contribution of roughly 0.04 percentage points to GDP growth in the EU-15 nations from 1999 to 2007. During the crisis, however, the reduction in integration had a severe influence on financial development and economic growth. The financial-growth nexus is ambiguous, according to Coeurdacier et al. (2020), with the efficiency of financial integration varying depending on parameters such as country size, risk levels, and capital insufficiencies. The integration-growth nexus in developing countries is found to be indeterminate (Eichengreen, 2002; Saafi et al., 2016). Despite the meager research done in the region, studies on the financial integration process have accelerated in Asia, the Middle East, and Latin America.

Despite divergent viewpoints, countries have begun to prioritize financial system integration. In the 1990s, for example, East Asian, South Asian, and African countries eased their capital markets and interest rates, resulting in a number of liberalization regimes (Juraev, 2014). The financial integration process in East Asia and the Pacific is documented by Didier et al. (2017). Their findings imply that the region has been financially connected even during the 1990s, when East Asian countries accounted for the majority of intraregional and outbound investments, rather than South Asian countries. In East Asia, full liberalization is connected with negative growth outcomes, whereas partial liberalization is associated with positive growth outcomes (Ben Gamra, 2009). Capannelli and Filippini (2009) analyze ASEAN+3 and EU integration activities and conclude that financial integration activities are more spread across ASEAN+3 nations. Given the diversity of ASEAN countries, it is critical that governments coordinate their integration plans, beginning with detecting and resolving negative imbalances (Morales & Estrada, 2010). According to recent research by Vo and Ellis (2018), financial integration linkages strengthen in the Vietnamese context during and after a global financial crisis.

This study attempts to fill the research gap in the current literature by analyzing the effect of financial integration on economic growth in the SADC and ECOWAS regions of Africa. Against the backdrop of mixed empirical findings, this study comparatively examined the effect of financial integration on growth in the SADC and ECOWAS regions.

Stylized Facts

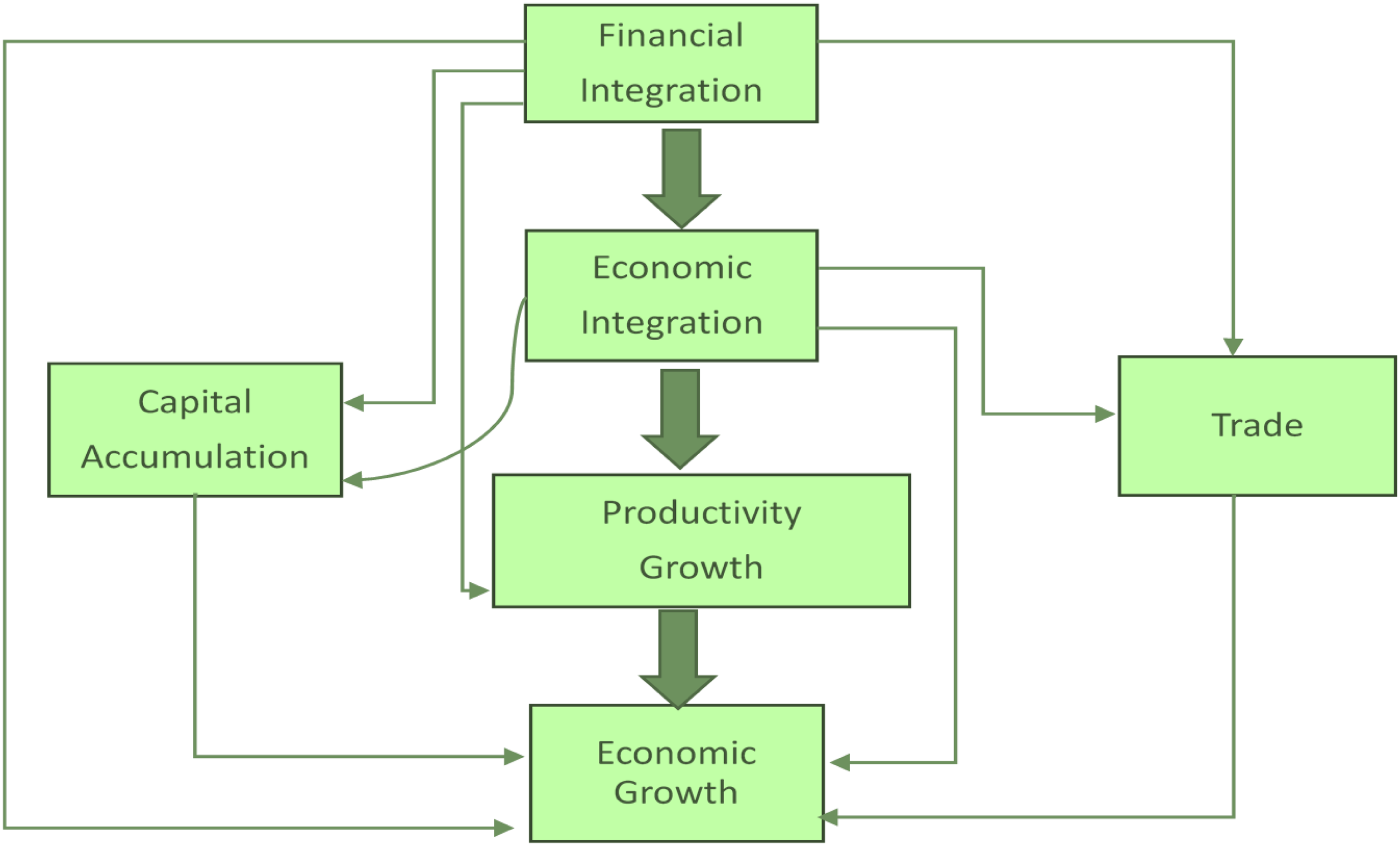

The conceptual framework of the relationship between financial integration and economic growth

Overview of the Financial Sector Developments

Southern African Development Community

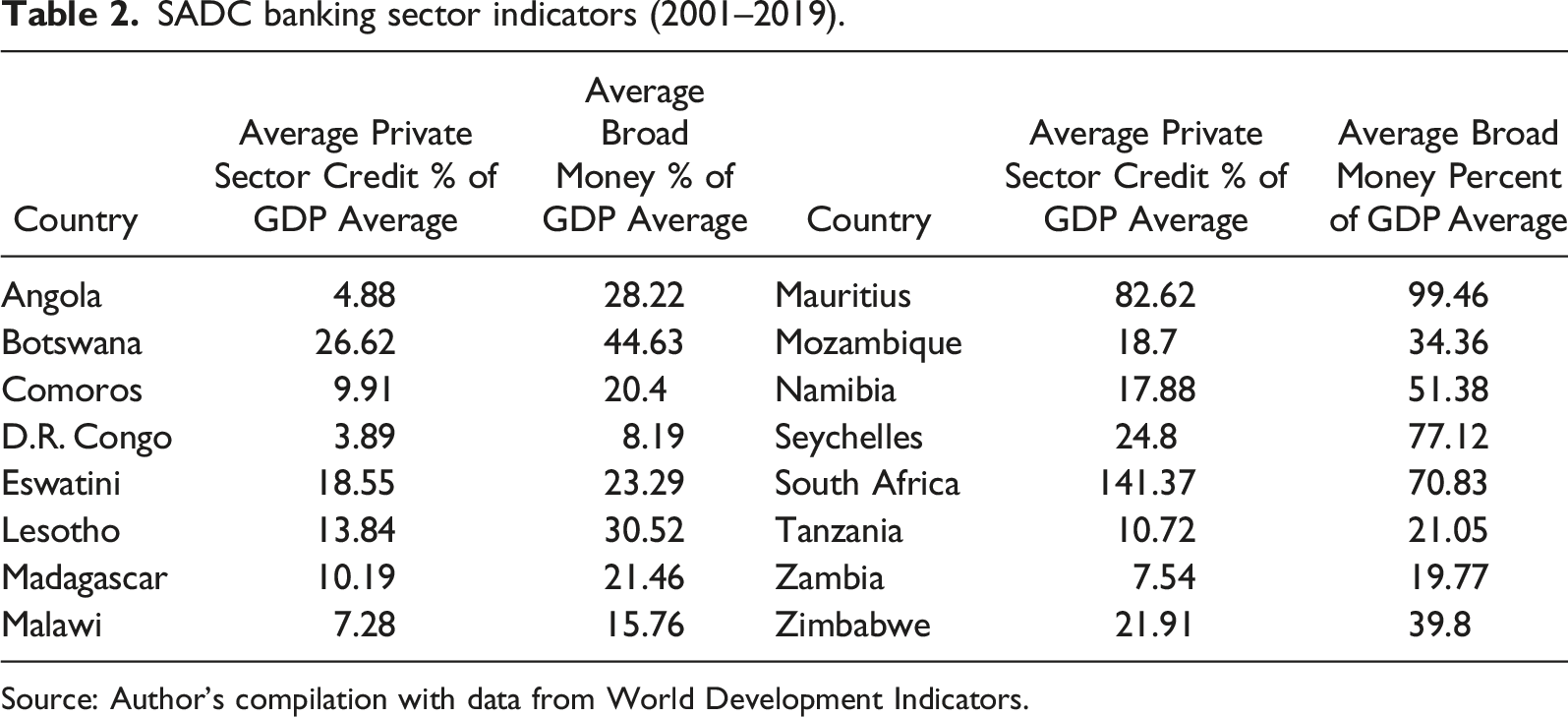

The Southern African Development Community (SADC) is a 16-member regional economic community in Southern Africa. The Southern African (Figure 1) Development Community (SADC) was established in 1992 to facilitate the integration of southern African markets. Both economic and political factors have affected this to date. The SADC Industrialization Strategy and Roadmap (SISR) were introduced in 2017 as a sign of the SADC’s efforts to encourage industrial growth and improve regional relations. One of the most promising areas for development on the African continent is the financial sector. The successful expansion of financial services to include the continent’s lower-income and “unbanked” population has the potential to create jobs, create safety networks, and eventually contribute to poverty reduction (ibid, 2013). To achieve the aforementioned, the SADC community has advocated for liberalized financial markets in order to create a market-driven regional financial services industry. South Africa has one of the most developed markets in the region, with a highly sophisticated stock exchange and a sizable bond market (Mahawiya, 2015). As a result, South Africa’s financial sector often dominates the region more than the financial sectors of other regional countries (ibid, 2015, p.7) (Table 1). The conceptual framework of the relationship between financial integration and economic growth. Summary of Selected Studies on Relationship Between Financial Integration, Growth, and Macroeconomic Variables. Source: Author’s Compilation.

SADC banking sector indicators (2001–2019).

Source: Author’s compilation with data from World Development Indicators.

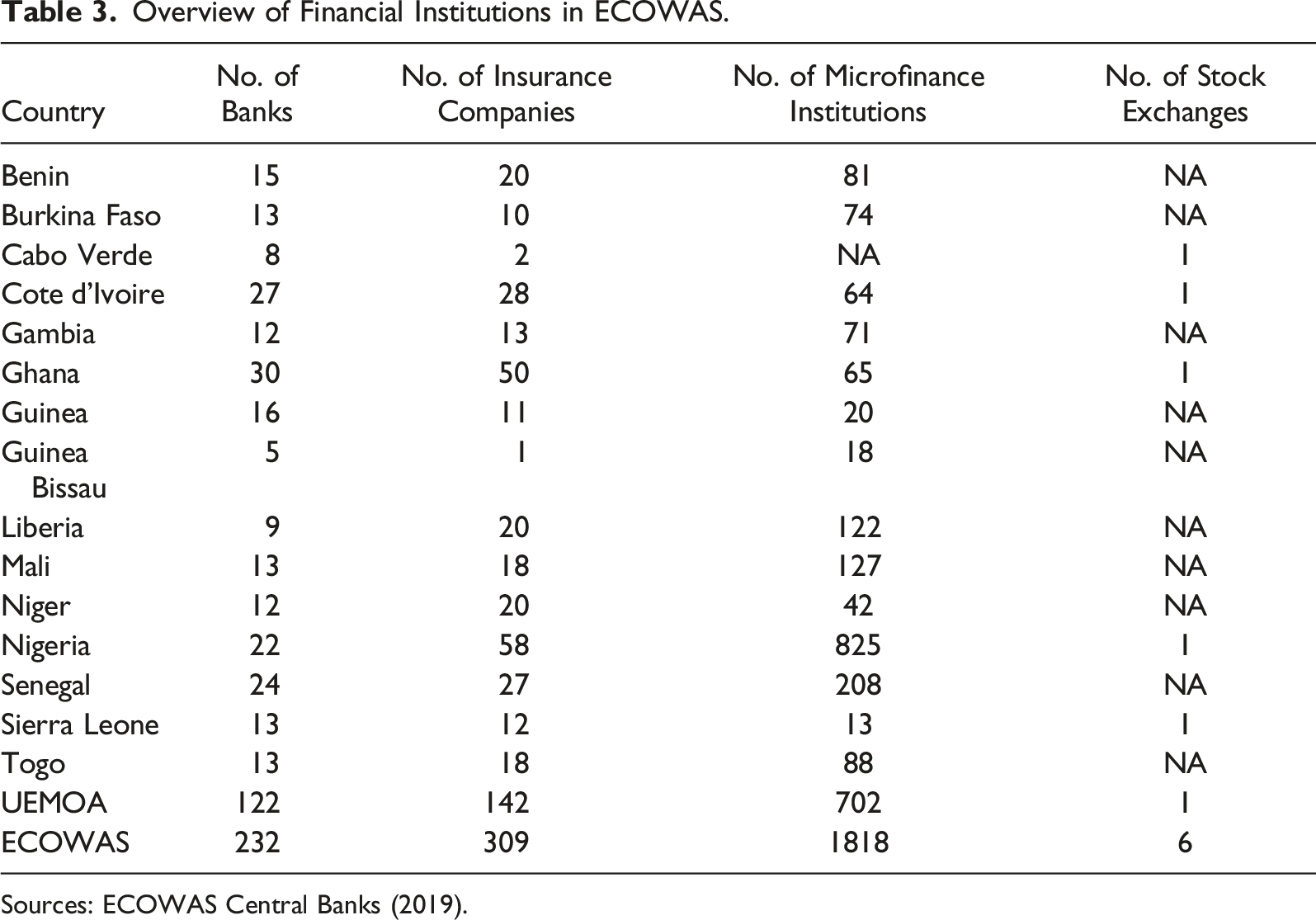

Economic Community of West African States

Overview of Financial Institutions in ECOWAS.

Sources: ECOWAS Central Banks (2019).

Variables, Data, and Methodology

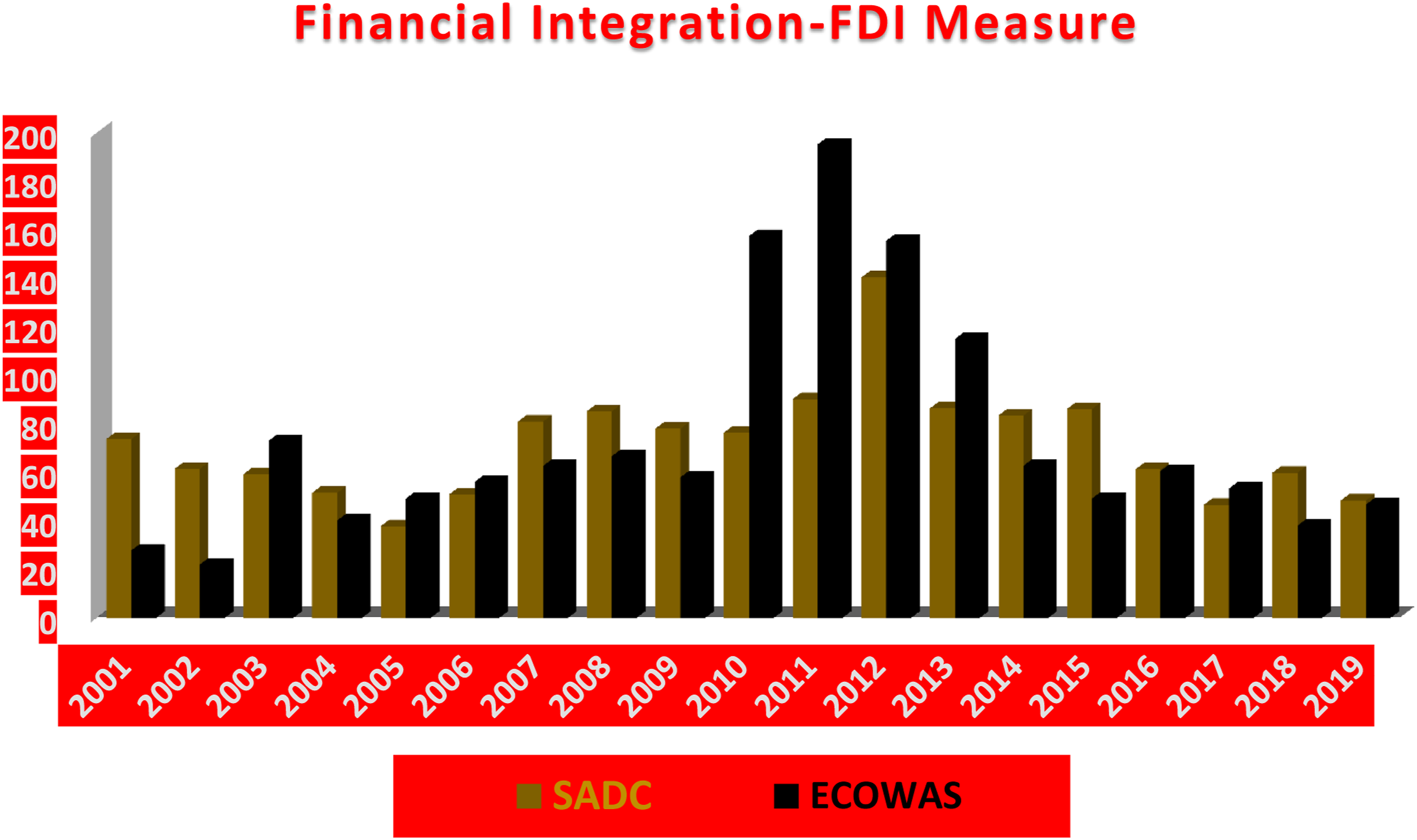

For the financial integration study, foreign direct investment (FDI) as a percentage of GDP was used as a proxy. FDI is generally regarded as the most reliable source of capital inflows. According to strong theoretical discussions and several pieces of empirical evidence, many of the indirect benefits of financial integration are produced primarily by FDI flows. FDI, portfolio investments, and other types of financial transactions are measured by stock, or flow, ratios of assets and liabilities, or the sum of the two (Gehringer, 2013). Quinn (1997), Rodrik (1998), Quinn and Toyoda (2008), Lee et al. (2017), and others have used these measures to investigate the implications of financial integration. The degree of trade openness (the sum of import and export) and the impact of FI on growth can be influenced by the degree of trade openness in a country. On the other hand, Aizenman (2008) argues that due to public finance linkage, trade opening will eventually lead to financial opening, government spending, and the level of institutional quality, as measured by the control of corruption index, where larger values signify better institutions, that is, less corruption, and inflation are also used as control variables. This is to account for external factors such as public opinion. External factors, government activities, and macroeconomic stability are all taken into account. The data was sourced from these databases: The World Development Indicators and the Worldwide Governance Indicators. It covered the period from 2001 through 2019 (Figure 2). Financial Integration-FDI Measure. Source: Author’s computation, with data from WDI.

This section also describes the econometric method that is used to assess the relationship between financial integration and economic growth in the ECOWAS and SADC regions. In order to capture both the long-run and short-run relationships between dependent and explanatory variables, the panel autoregressive distributed lag (ARDL) model was used. According to Pesaran et al. (1999), panel ARDL can be used to estimate models containing I(0), I(1), or both I(0) and I(1) variables. Because the model incorporates lags of both dependent and independent variables, the coefficients of the ARDL estimate are deemed consistent even if there is an endogeneity concern. The panels consist of data for a maximum of 16 SADC countries and 15 ECOWAS countries over the period 2001–2019. Consequently, two models are estimated. The following is a representation of the Panel ARDL model

To estimate the panel ARDL model, Pesaran et al. (1999) proposed the pooled mean group technique. For large numbers of time observations and groups, the pooled mean group (PMG) estimator of dynamic panels is highly efficient. Long-run coefficients are not allowed to differ among countries in PMG estimation, although short-run coefficients and error variances are. A maximum likelihood estimate is used to calculate long-run coefficients and group-specific error-correction coefficients.

Empirical Results and Analysis

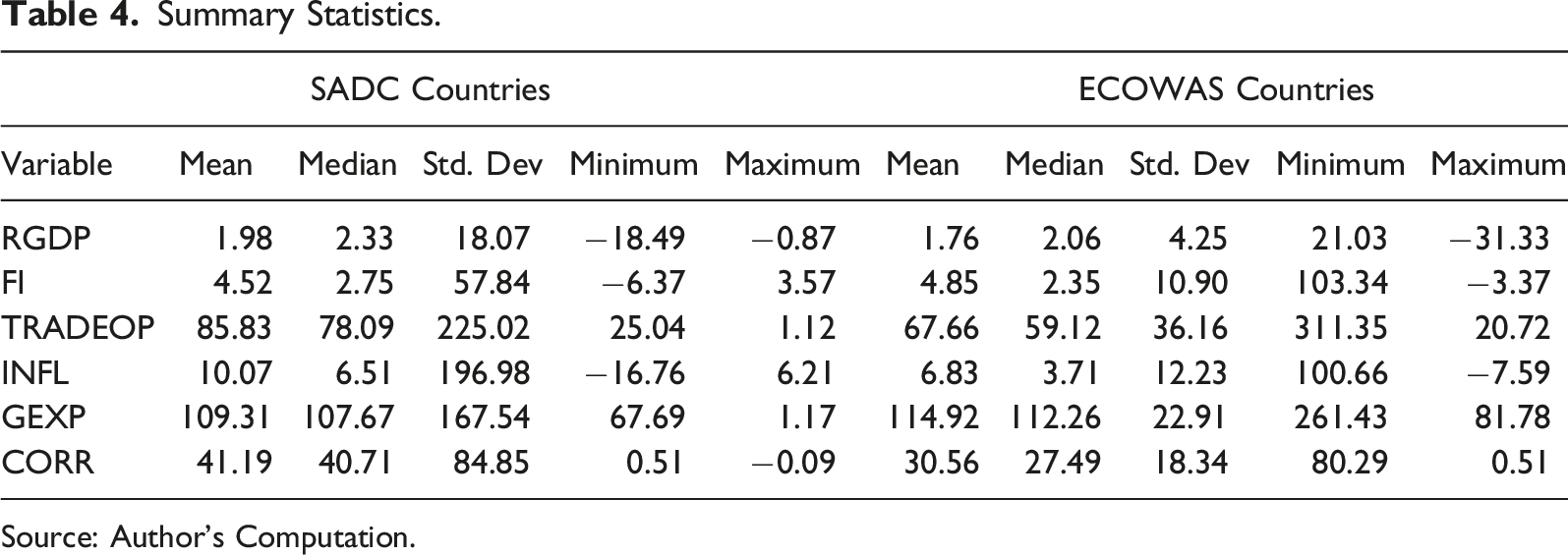

Summary Statistics.

Source: Author’s Computation.

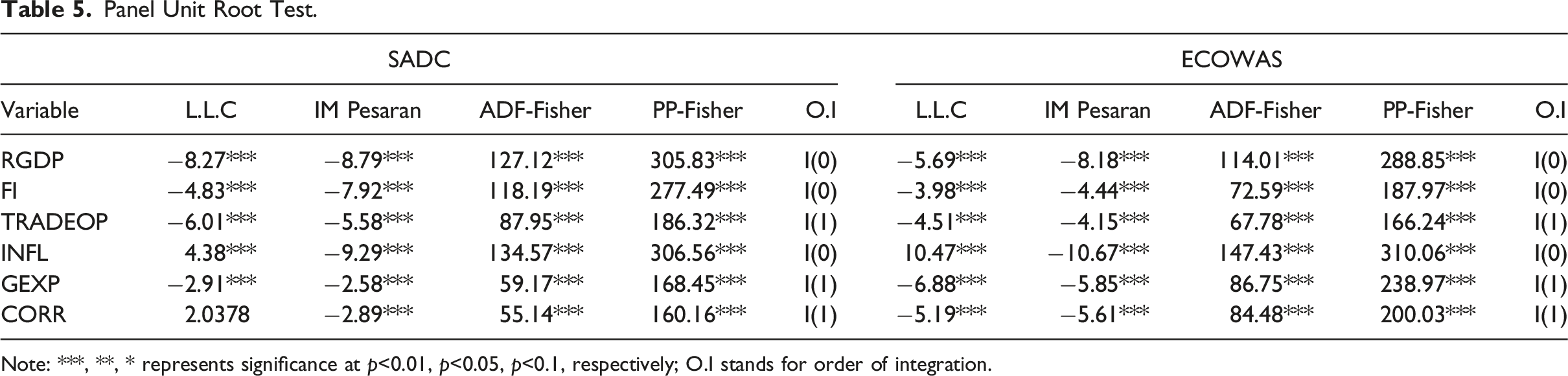

Panel Unit Root Test.

Note: ***, **, * represents significance at p<0.01, p<0.05, p<0.1, respectively; O.I stands for order of integration.

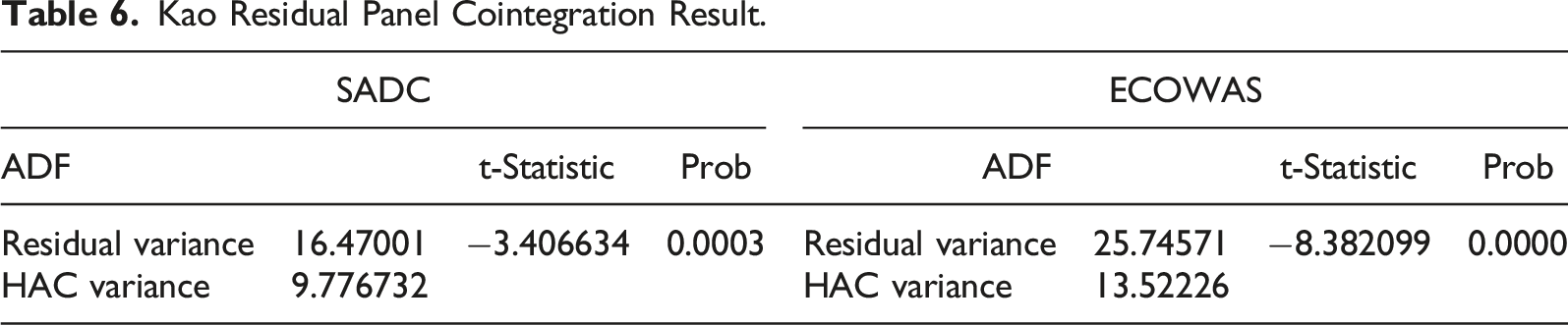

Kao Residual Panel Cointegration Result.

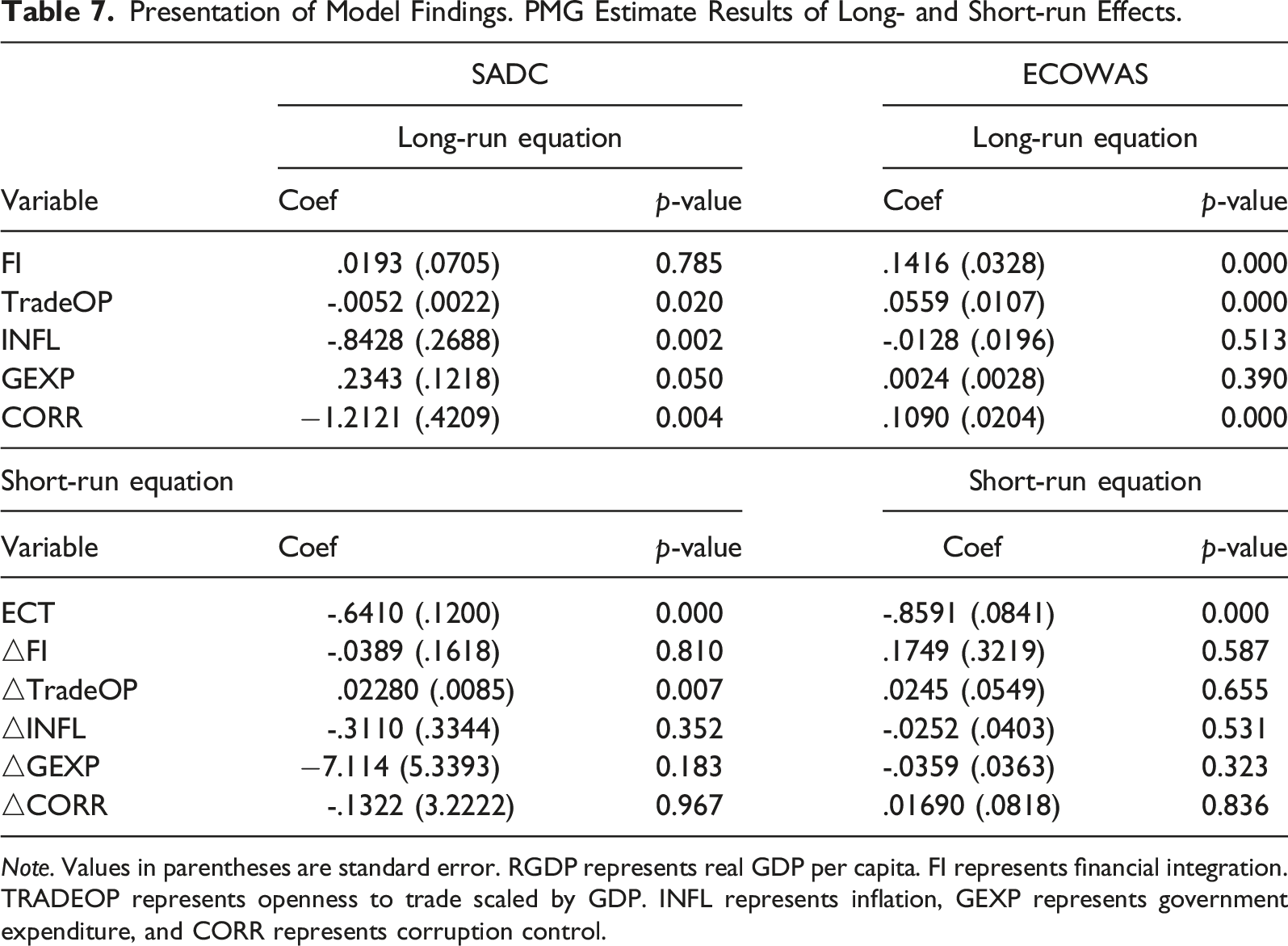

Presentation of Model Findings. PMG Estimate Results of Long- and Short-run Effects.

Note. Values in parentheses are standard error. RGDP represents real GDP per capita. FI represents financial integration. TRADEOP represents openness to trade scaled by GDP. INFL represents inflation, GEXP represents government expenditure, and CORR represents corruption control.

Conversely, the long-run financial integration variable estimate (.0193) for the SADC model is positive but insignificant to growth in the region within the period of study. This finding justifies the stylized facts given in Section Two of this Study (Table 2) that the SADC financial sector is still experiencing low stages of growth. Ahmed (2011) evaluated the influence of international and regional financial integration on the real economies of 25 developing countries and got the same result. According to the study, there was no conclusive evidence connecting financial integration to economic growth. According to the study, higher human capital levels, a stable macroeconomic environment, and good institutions can reduce the negative and insignificant effects of international financial integration. Similarly, Hye and Wizarat (2013) used the ARDL method to show that financial integration has no significant long-term influence on Pakistani economic growth. For both models, only trade openness is found to be a significant variable for economic growth in the short run. Other variables are not significant. For the SADC region’s model, all the control variables (trade openness, inflation rate, government expenditure, and corruption index) became statistically significant in determining the region’s economic growth in the long run. This is slightly different from the ECOWAS result, as inflation and government expenditure are found to be insignificant. This is not similar to the finding of Hope (1972). However, as expected, the inflation rate has a negative influence on the region’s economic growth. Despite some inconsistent results, the parameters are similar to the empirical findings of King and Levine (1993) and Osada and Saito (2010).

Conclusion and Policy Recommendation

Financial integration is thought to stimulate economic growth as a result of its effects on broadening and deepening financial interrelationships within a region or among countries. Against this backdrop, the study carried out an empirical analysis of the possible impact of financial integration on economic performance in African countries, focusing on the SADC and ECOWAS regions for the period 2001–2019. Data sourced from WDI and WGI was analyzed using the Panel ARDL PMG Model. The following findings were made: There is a significant and positive impact of financial integration on economic growth in the ECOWAS region. Whereas, even after controlling for necessary variables, financial integration exacerbates negative and insignificant effects in determining economic growth in the SADC region, both in the short run and long run. The negative and insignificant impact of financial integration on the region’s economic growth is attributed to several possible factors, including the low level of financial development in the SADC region, which is unconnected with the poor level of governance, unstable and fragile financial stability, or low creditworthiness, that are prevalent in developing countries like the SADC countries. Furthermore, financial integration is imperfect due to country-specific characteristics and can trigger economic instability.

Policy Recommendations

The majority of studies on the economic impact of financial integration focused on emerging economies, shifting away from low-income countries, especially those in Africa. Therefore, it is imperative to extend the research on the financial integration-growth nexus to low-income countries. Therefore, the study recommends as follows: Firstly, for African countries, especially those in the SADC and ECOWAS regions, to satisfactorily benefit from financial integration gains and achieve the desired levels of economic performance, relevant policies must be introduced and implemented quickly. However, without considering the necessary pre-requisites needed for financial integration, hasty financial liberalization will cause more harm than benefits since the significant effects of financial integration for a country are dependent on the existing development of third economic and social characteristics. Secondly, the regulation of financial development and trade openness should be a part of policies aimed at enhancing financial integration. Fundamentally sound financial institutions and financial structures pave the way for financial openness and its benefits. Without good macroeconomic policy, an economy cannot integrate financially and, as a result, cannot function positively in economic growth. Thirdly, in order to improve financial integration and economic development, the results indicate that the government should work to eliminate corruption and maintain macroeconomic stability. Furthermore, in order to allow technology diffusion and cross-border capital flows, SADC and ECOWAS countries should put in place and develop governance institutions (security of property rights, transparency of the legal system, and investor-friendly regulations) as well as human capital formation.

However, these findings and conclusions cannot be easily transplanted to other countries in Africa, whereby further research in this area that will focus on other African countries is equally suggested.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.