Abstract

Are large corporations able to transcend individual self-interest in favor of a broad class interest, as suggested by class dominance theorists? Or, has the corporate elite become fractured? We address this ongoing debate through a unique case: the determinants of the breadth of corporate lobbying of the U.S. federal government. As predicted by the fracturing thesis, we find that financial companies no longer have a broader political interest than nonfinancial companies. However, we also find that mechanisms still exist that foster a broader class-wide interest. Specifically, a firm’s embeddedness in the interlocking directorate and policy-planning networks is associated with broader lobbying activities. Finally, we find support for the hypothesis that the interests of large corporations have become more globalized: firms with more global operations have greater breadth of lobbying activities. We therefore theorize that while banks no longer play the same role in diffusing a broadened interest through the capitalist class, alternative mechanisms continue to fulfill this role. Together, these findings demonstrate continued support for the class dominance thesis, even in the light of any fracturing of the corporate elite.

Introduction

Business interests disproportionately influence U.S. policy. While the level of business influence on government has long been a source of debate among pluralists, state-centered theorists, and Marxist/power elite theorists, a recent analysis examining the outcome of approximately 1,700 policy issues finds that the preferences of average Americans have no impact on policy outcomes, while the preferences of business groups and the wealthy 1 are consistently reflected in government policy (Gilens and Page 2014). Research has identified a number of avenues through which business interests take action to achieve this influence, ranging from campaign donations and lobbying to the threat of capital strikes to extract policy concessions. 2

While the empirical evidence of business influence on government policy is strong, the nature of the interests undergirding business political activity are not as well understood and thus are the subject of much debate. For instance, proponents of the biased pluralism perspective argue that although policy tends to reflect some set of corporate interests, those interests are divided by economic sector (Gilens and Page 2014; Hacker and Pierson 2010). However, proponents of a class dominance perspective argue that political actions of the leading edge of business are motivated by class-wide interests; such that on issues of collective interest, class-wide rationality prevails, and the individual benefits of a firm or sector are almost never secured at the expense of the class as a whole (Domhoff 2014, 2015; Dreiling and Darves 2016; Useem 1984; van Apeldoorn and de Graaf 2015).

At the core of this debate between biased pluralism and class dominance is the difference between the broad versus narrow interests of business. Understood as “what people have to gain or lose from an interaction, event, or relationship” (Roy and Parker-Gwin 1999:206), interest provides the conceptual foundation to assess the scope of business political action. Under biased pluralism, each firm has narrow individual interests that motivate its political activity. On any given issue, individual firms may have their narrow interests overlap, creating an interest group. On a different issue, however, the interests of those same firms may not overlap. In this way, narrow interests lead to collective action that is temporary and non-enduring (Mintz 1995). In contrast, the class dominance perspective contends that mechanisms exist that broaden the interests of the corporate elite, such that they develop a class-wide rationality (Domhoff 2014; Mizruchi 1992; Useem 1984). 3 Here, firms like Wal-Mart and Aetna may see beyond their narrow interest on a given policy, factoring instead how the policy will affect the class as a whole. Class-wide rationality, then, leads to a collective action that is long term and consistent over a range of issues.

Yet, surprisingly, there is little systematic empirical evidence regarding what factors are associated with class-wide interests. This is because it is quite difficult to measure class-wide rationality. Instead, much of the quantitative research focuses on measuring (1) political strategies assumed to represent class-wide rationality (e.g., Clawson and Neustadtl 1989; Murray 2014); (2) the effect of mechanisms assumed to be associated with class-wide rationality, such as interlocking directorates (Banerjee and Murray 2015; Mintz 1995); or (3) dyadic similarity as a measure of unity, as unity is the assumed result of class-wide rationality (Banerjee and Burroway 2015; Dreiling and Darves 2011; Mizruchi 1992; Murray 2017).

Moreover, long-term changes to some of the assumed mechanisms of class-wide rationality have given rise to the “fractured elite” thesis, which posits that the corporate elite no longer operate based on a class-wide rationality. Rather, each individual corporation takes actions to secure its own immediate benefit, often at the expense of the long-term interests of the class as a whole (Mizruchi 2013; Waterhouse 2014). The argument is twofold: first, that long-term processes (described below) have led to a decline in the institutional bases of collective action such that business has become increasingly fractured over time. The second is that, as a result of these processes, business today is sufficiently fractured to be unable to engage in meaningful collective action. In this paper, we test the latter, cross-sectional argument. We find that, despite the long-term structural changes described by fracturing theorists, business today still appears capable to engaging in class-based collective action, lending support to the class dominance perspective of business political influence (Domhoff 2015). We demonstrate the viability of our argument through analysis of the determinants of the scope of a firm’s interests in an as-yet-unseen political arena—the lobbying behavior of large corporations.

The Decline of Key Sources of Broad Interest

While finance capital was at the center of inter-corporate networks dating as far back as the 1870s, this began to change beginning in the 1980s (Mizruchi 2013:191–92). This is important to the development of a class-wide rationality because both banks and inter-corporate networks are theorized to have been important factors in broadening the interests of the corporate elite. Because banks lend capital to all sectors of the economy, their interests “transcend those of particular companies or industries” (Mizruchi 2013:112). Financial corporations’ broad interests also led to their central position in the interlock network to begin with. Banks sought out the CEOs of large corporations in diverse sectors of the economy as “sources of information and expertise both about sources of deposits and about investment opportunities in their industries,” while the said CEOs accepted the invitations to serve on the boards of financials as they were “eager to participate in decisions about capital flows” (Mintz and Schwartz 1985:151).

Starting in the 1980s, nonfinancial companies began diversifying into financial services, significantly increasing the share of their revenue that came from investments, securities, and personal financing (Waterhouse 2014:236). The consequence of this was that nonfinancial companies began lending each other money. This reduced the role of financial corporations in controlling capital flows through commercial loans, but it also took away some of their business as the primary source of investment for bank deposits (Mizruchi 2013:192–93). By the early-1990s, commercial banks responded to this change by moving into the realm of investment banking, becoming involved in fee-for-service activities such as currency swaps, securities underwriting, and derivatives (Davis and Mizruchi 1999:221; Mizruchi 2013:194).

This shift into investment banking activities also changed the rationality of banks from holding a broad interest in diverse sectors of the economy succeeding to a narrower interest. Commercial and personal loans are profitable for banks when they are paid back. These are long-term investments that depend on a healthy economy. In addition, individuals deposit more money in banks when employment is high and the economy is growing. This dependence on a strong economy was the source of banks’ former class-wide interest. Once they moved into investment banking, however, there arose a potential to profit from failure. That is, when a derivative such as futures, options, credit-default swaps, or collateralized debt obligations are bought and sold, one party is inevitably betting on the contract’s success, while the other is betting on failure. Thus, banks no longer solely profit from the success of the economy as a whole, but they begin to profit from failure and short-term speculation.

The consequence of this new, narrower interest motivating banks was a decline in the necessity of acquiring a “business scan” (Useem 1984), which came from having the CEOs of diverse sectors serve on corporate boards. Once banks began to shrink their boards of directors and reduce outside director invitations to nonfinancial corporate elites, financial corporations disappeared from the center of the inter-corporate network (Davis and Mizruchi 1999). Thus, theorists argue banks no longer serve the same role of diffusing the broad class interest that helps facilitate corporate political cohesion (Mizruchi 2013:197).

Although banks had shifted from the center of the intercorporate network by the mid-1990s, the general structure of the interlock network remained intact until about the year 2000 (Chu and Davis 2016). This is important because research shows the role of banks in diffusing information and broadening the cognitive range of the corporate elite may instead be filled by any type of firm as long as it is central in the network (Murray 2017). After 2000, however, the network began to become sparser, as companies stopped seeking out individuals who already directed multiple firms. This caused the “big linkers”—individuals who direct six or more companies—to decline significantly in number (Chu and Davis 2016).

This has two potential consequences. First, the interlock network may not function to generate a broad perspective; and second, the inner circle (directors who serve on two or more boards) may no longer be carriers of a broad class-wide perspective. 4 With banks and big linkers gone from the center of the interlock network, two important potential sources of broad interest disappeared with them. This led to the fractured elite thesis that the corporate elite today are incapable of transcending narrow firm-specific interests in favor of a broadened, class-based collective interest (Mizruchi 2013; Waterhouse 2014).

The Persistence of Alternative Sources of Broad Interest

In this paper, we contend that banks and big linkers are not the only potential sources of broad interest in the corporate community and that other mechanisms capable of generating a broad class-wide rationality persist. Specifically, we argue the fracturing thesis has overlooked three potential sources of broad interest. First, research has tended to focus on the overall thinning of interfirm networks and the decline of “big linkers” without fully theorizing the level of network connectivity sufficient to broaden a firm’s interests. Second, research has focused on the interlocking directorate network and left other interfirm networks—especially those formed through policy-planning organizations—understudied. Finally, research has emphasized domestic interests and undertheorized the ways in which a shift to global considerations also engenders broadened interests for firms.

How Interests Broaden: Big-linkers versus the Inner Circle

While evidence for a decline in the centrality of banks and the overall connectivity of the interlock network is incontrovertible, it is not clear what the interpretation of this should be. For instance, in 1982, Chase Manhattan bank was one of the most central firms and its directors were exposed to the views of 42 separate large corporations (Davis and Mizruchi 1999:217). After 30 years, the most central firm was a nonfinancial corporation (Boeing), whose directors sat on the boards of only 17 different firms.

In terms of developing a broad perspective, this raises a practical question: how many different firms and sectoral interests must firms be exposed to before their perspectives become class-wide? There is of course no clear-cut answer to this. If the threshold is 30 firms, then this decline is meaningful, but if it is five or three, then the decline is, needless to say, less impactful to developing class-wide interests. As Johan Chu and Gerald F. Davis (2016) demonstrate, the average number of steps between any two firms in the interlock network increased from 4.2 in 1999 to just below 5 in 2010. While this certainly suggests increased fragmentation in the network, it demands the question: does information diffuse at 4.2 steps but not at 5? In fact, Val Burris (2005) finds that political cohesion at the individual director level is associated with indirect interlocks as far away as six steps. Moreover, the decline in the number of a firm’s ties need not indicate a proportionate reduction in the diversity of interests it is exposed to. While the directors of Boeing formed linkages to under few than half the number of firms as Chase, the different industries these exposed the firms to stayed largely the same (Chase and Boeing directors united 13 and 11 different industries, respectively, through their board appointments). Thus, it may simply be that the decrease in network density is not extreme enough to eliminate it as a source of generating and diffusing a broad class interest.

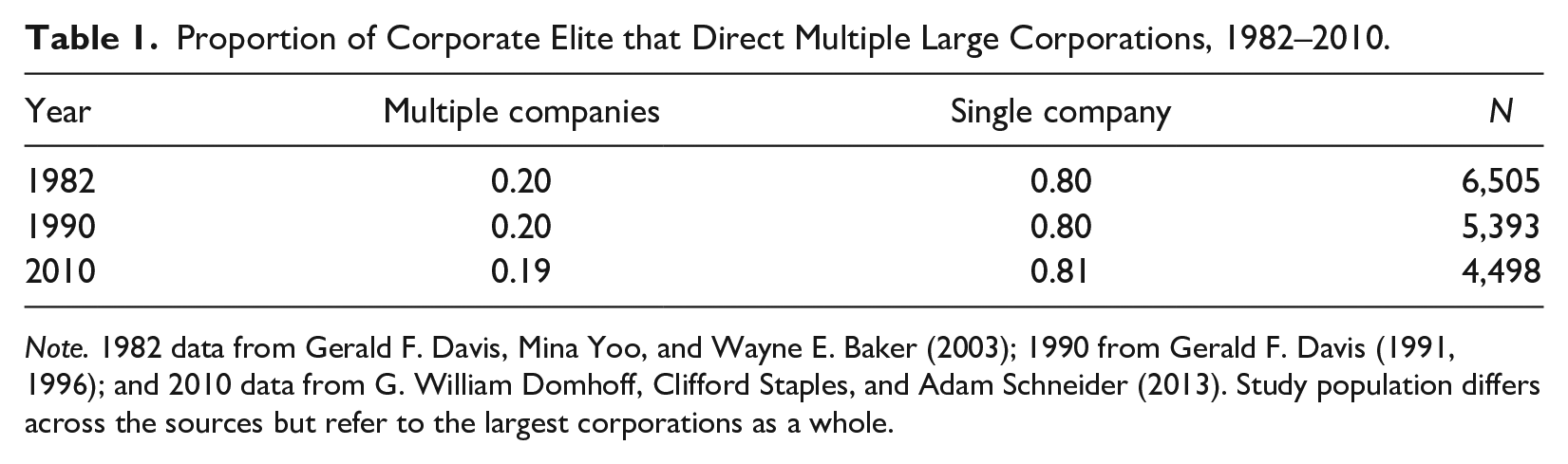

In addition, the interlock network’s role in generating class-wide rationality is not solely in diffusion, but also in the creation of an inner circle of business that has a broad perspective on business interests (Mizruchi 2013; Useem 1984:134–36). Beth Mintz and Michael Schwartz (1985:135) elaborate, “their interests—both directorate and investment—in several companies place them in a position to identify with the problems of diverse corporations and hence to generate policies reflecting a broad class interest.” Although the organizational network has declined in density as the number of big linkers has fallen, the number of inner circle members (i.e., those directing two or more firms) as a proportion of all directors has stayed remarkably constant (see Table 1).

Proportion of Corporate Elite that Direct Multiple Large Corporations, 1982–2010.

Note. 1982 data from Gerald F. Davis, Mina Yoo, and Wayne E. Baker (2003); 1990 from Gerald F. Davis (1991, 1996); and 2010 data from G. William Domhoff, Clifford Staples, and Adam Schneider (2013). Study population differs across the sources but refer to the largest corporations as a whole.

Chu and Davis (2016) place the big linkers as a unique group in terms of the diffusion of class-wide interest, yet the evidence from Michael Useem’s (1984) original study of the inner circle suggests the primary difference lies between individuals who direct a single company and individuals who direct two companies (inner circle periphery), rather than between directors of two companies (inner circle periphery) compared to the directors of three or more firms (the core of the inner circle as conceptualized by Useem). For instance, the inner circle periphery was 107 percent more likely than single-company directors to serve on U.S. federal advisory committee in 1975–1976. The core of the inner circle, however, was only 40 percent more likely than the inner circle periphery to serve (Useem 1984:78). This pattern of the behavioral difference between the non-inner circle and the periphery of the inner circle being greater than the difference between the core and the periphery of the inner circle holds in four out of the five business associations studied (Useem 1984:73) and in governance of nonprofit and philanthropic organizations (Useem 1984:82). This suggests that if inner circle members continue to develop a broad class-wide perspective, then their presence on a company’s board ought to result in that firm adopting policies reflecting a broader interest.

Networks beyond Interlocking Directorates

Most research has emphasized the role of interlocking directorates in shaping the interests of firms. Yet, research also finds that policy-planning groups provide an important alternative mechanism of influence. Where the interlocking directorate network is the unintended byproduct of individual firms seeking to manage the environment, policy groups exist for the express purpose of helping its members arrive at and diffuse certain political outlooks (Domhoff 2015:27; Judis 2001). These include groups such as the Business Roundtable, American Enterprise Institute, and the Council on Foreign Relations (CFR); whose interests collectively span a wide variety of economic and political issues in both domestic and global arenas.

Policy groups are important for two reasons. First, research finds that the policy network continues to shape the interests of affiliated firms and engenders greater similarity of behaviors between connected firms (e.g., Banerjee and Murray 2015; Burris 2005; Domhoff, Staples, and Schneider 2013; Dreiling and Darves 2011). Second, policy groups attract the very same members key to class-unity ascribed to the pre-fracturing period: inner circle directors. Useem’s (1984:73) classic study found that inner circle directors were 3.4 times more likely to be members of the Business Roundtable than single-company directors. Three decades later, this relationship still holds as 35 percent of the Business Roundtable is composed of inner circle directors, making inner circle members nearly three times as likely to take part in the policy discussions than individuals who direct a single Fortune 500 firm. 5 As with the director network, these groups bring business leaders from just about every sector of the economy together, ensuring a diversity of interests is represented. In this respect, we argue that policy groups have compensated for the decline of banks in the director network (and the resultant loss of the broadened view of the environment that they enabled). Thus, the inner circle may continue to diffuse a class-wide rationality developed in policy groups to the individual firms they direct, resulting in a broadening of member firm’s interests.

Globalization of Interests

Finally, theorists argue that globalization has shifted the center of class-wide rationality from the domestic to the transnational realm (Dreiling and Darves 2016; Heemskerk, et al. 2016; Heemskerk and Takes 2016; Murray 2017; Robinson 2004; Robinson and Harris 2000; Sklair 2001). While the extent to which global firms constitute a transnational capitalist class (TCC) is contested (Beckfield 2010:276; Mizruchi 2013; Pauly and Reich 1997:4–5), extant research suggests that global firms hold a broader set of interests than domestic firms. This goes back to G. William Domhoff’s (1967) classic study which identified international orientation as one determinant of the class-wide rationality associated with the corporate liberalism dominant in post-World War II U.S.: The business liberals, who usually come from the biggest, most internationally minded companies, speak through such organizations as the Council on Foreign Relations, the Business Advisory Council, the Committee for Economic Development, the Democratic Party, and the moderate wing of the Republican Party. (Quoted in Burris and Salt 1990)

However, it was not just that multinational corporations (MNCs) were relatively liberal. Rather, it was that their global operations provided a broadened awareness of the risks and possibilities that arose from foreign governments and international labor. One prominent example is the automobile industry, where automakers both expanded production to other countries to maximize profits and, in turn, gained a broader understanding of the ways in which global labor forces shaped their own long-term viability (Silver 2003). Another is seen in the movement toward corporate social responsibility (CSR), which was led primarily by MNCs who had a deeper awareness of the challenges facing business in the post-War era than domestic U.S. firms (Tsutsui and Lim 2015).

In more general terms, the increasing interconnectedness of global production and finance (Harris 2014) suggests that firms with global operations require a keener understanding of the various political environments of the countries they operate in. While research has not examined whether the international presence of U.S. corporations increases the scope of their domestic political interests, theorists argue that class-wide rationality for business today is embedded in a TCC (Murray 2017) that is qualitatively different from the internationalization of the mid-20th century (Sklair 2001:47–50). While the studies above are only suggestive on the particular question of a firm’s lobbying scope, a key claim of theorists who dispute the fracturing of U.S. business is that the domestic fracturing is countered by the rise of a new global business community (Murray 2017). Therefore, if processes around globalization do in fact function to broaden the interests of the corporate elite, this calls into question the thesis that financialization has fractured the U.S. corporate class. In the following section, we lay out several hypotheses regarding sources of broad interest based on the above discussion and test these on the lobbying behavior of U.S. Fortune 500 firms in 2012.

Hypotheses

Despite strong evidence of a decline in the overall connectivity of the interlock network (Chu and Davis 2016), we have argued there is evidence in support of the corporate network still underwriting a broad corporate interest, even if its impact may have declined. That is, the most central firms still have representation from a broad swath of economic sectors on their boards, the proportion of inner circle members sitting on boards is stable, and most firms in the network are still connected by fewer steps than previous research suggests is the maximum distance information diffuses in the corporate network. This would suggest the following hypothesis:

Major policy-planning organizations serve the explicit purpose of generating cohesion among the corporate elite around a set of policy prescriptions (Judis 2001). The fact that these groups also tend to draw their membership (1) from a wide sample of economic sectors and (2) from the inner circle means that the discussions that take place at the groups—and the policies that are formed out of those discussions—likely represent a broader class-wide rationality. Directors who are members of the policy-planning network may bring that class-based rationality back with them to their companies, thus broadening the interests reflected by corporate policy.

Next, internationalism has long been associated with broad class-wide interests. With globalization creating the potential for the rise of a TCC, broader class-wide interests may lie with the most globally oriented corporations.

While the above hypotheses suggest mechanisms that continue to broaden the interests of firms, as discussed previously, evidence for the movement of financial institutions away from the center of the director network is clear. The forces behind this suggest a change in the interests motivating financials and nonfinancials. Financial companies moved away from the center when they began drawing most of their profits from derivatives and other fee-for-service activities that depend not on a stable economy, but on banks outmaneuvering competitors. The result of this is to potentially narrow the interests of financial corporations. The driving force behind the banking industry’s movement into derivatives, however, was nonfinancials venturing into traditional commercial banking (providing commercial loans and even personal financing). This means that nonfinancial corporations have an increasing proportion of their profits tied to activities that depend on the health of the entire economy. In effect, as predicted by fracturing theorists, the unique position of financial firms may no longer apply.

In combination, the four hypotheses allow us to test the contention that mechanisms enabling a broader rationality for the corporate elite continue to persist in spite of the declining centrality of banks, the loss of the “big linkers,” and the resultant thinning of the overall director network.

Data and Methods

Study Population

To test our hypotheses on the sources of broad interest among the corporate elite, we examine the lobbying behavior of large corporations. This decision requires some explanation as it necessarily is also a decision not to study individual elites or other forms of political behavior. Before we detail our sample of firms, we lay out the logic behind operationalizing the corporate elite as organizations and why we examine lobbying behavior.

Operationalizing the corporate elite

The corporate elite may be conceptualized as either individuals affiliated with corporations or the corporate organizations themselves. In this paper, we focus on the behaviors of corporations because corporations represent the collective behavior of those that direct the corporation (Mizruchi 1992:59–64; Roy and Parker-Gwin 1999; Scott 1997). Corporations are also the basis on which the fractured elite thesis is based. Mark S. Mizruchi (2013) argues that the corporate elite pursue narrow sectoral and firm-level interests, not that they pursue their individual interests. Finally, organizations are the “real motors of business political motion” (Useem 1984:75). When it comes to lobbying, individual corporate elites do not hire lobbyists; their corporate organizations do.

Why lobbying

Most research on the collective political interests of business has focused on campaign finance, particularly through a firm’s political action committee (PAC) activities (e.g., Chu and Davis 2016; Dreiling and Darves 2011; Mizruchi 1992; Murray 2017; Walker and Rea 2014). 6 While these studies have helped elaborate upon the conditions under which firm interests are shaped through collective dynamics, we argue lobbying provides a better measure of a firm’s interest. This is for two reasons.

First, research finds campaign donations are beneficial to business not in providing influence over policy but in providing access to policymakers (Ansolabehere, Snyder, and Tripathi 2002; Clawson, Neustadtl, and Scott 1992; Victor and Koger 2016; Waterhouse 2014): while campaign finance is crucial for the outcomes of elections, its influence on policy is more limited (see Roscoe and Jenkins 2005). Instead, the access enabled through PAC donations is parlayed into specific policies by subsequently lobbying the now-presumed friendly elected officials (Kerr, Lincoln, and Mishra 2013; see also i Vidal et al. 2012). In line with this, research finds lobbying has a clear payoff for business: firms that lobby tend to receive increased profits, lower tax rates, and regulatory waivers, amongst other benefits (Baumgartner et al. 2009; Tomaskovic-Devey and Lin 2011). Consequently, firms spend even greater amounts on lobbying than contributing to elections (Milyo, Primo, and Groseclose 2000). In the 2012 presidential election cycle—the period of our study—business donated US$2.7 billion to campaigns, 7 but spent over US$3 billion on lobbying. 8 Therefore, we argue that an analysis of firm lobbying behavior provides a better measure of the interests of firms than campaign finance, which can better be thought of as the intermediary mechanism by which firms then receive access to realize their interests.

Second, lobbying provides a good measure of assessing the scope of a corporation’s interests. This is because the 1995 Lobbying Disclosure Act requires lobbyists to register and report the specific issues on which they engage in lobbying. 9 In contrast, with campaign finance, it remains unknown why a firm donates to a specific candidate—it may be out of narrow firm-centric interest, broad class interest, or out of social interest such as friendship or civic duty. That is, there is no clear way to measure the scope of interest behind campaign donations on a large scale. As the issues lobbied on are reported, however, we can look at the number of distinct issue areas a firm lobbies in as a measure of scope. As we elaborate upon in the following, this enables us to measure the ability of firm networks to broaden the scope of a firm’s interests (toward class-wide interests) or narrow them (toward firm-centric interests) in ways impossible with PAC data.

Final sample

A focus on lobbying requires a focus on corporate organizations, but given that we want to know about sources of broad interest among the corporate elite, we also focus on the largest corporations, rather than a representative sample of all corporations. Specifically, we take as our population the Fortune 500, the largest 500 firms by revenue. We do this because theories on the unity of business argue that the collective interests of business are generated and led by the largest, most influential corporations, rather than business as a whole (Domhoff 1967; Mintz and Schwartz 1985; Mizruchi 1992; Useem 1984). Focusing on the Fortune 500 is therefore standard in the research and allows us to relate our findings to prior studies (e.g., Banerjee and Murray 2015; Clawson and Neustadtl 1989; Dreiling and Darves 2011; Mizruchi 2013). Our final sample excludes a few firms which lacked complete board of director data, leaving a final sample at 488 corporations, all of which were among the largest 500 corporations in the United States in 2012.

Data Sources

Data on board of director membership come from LexisNexis Corporate Affiliations Database. The policy-planning membership lists used to determine company ties to policy groups are from 2010 and were generously shared with us by Val Burris. Data on the global orientation of firms (number of countries operating in), whether the company was a financial firm, and the industry breadth of its operations (number of industries operating in) also come from LexisNexis Corporate Affiliations. Data on firm revenue come from Fortune Magazine. 10 Finally, lobbying and PAC data originate from the Center for Responsive Politics. 11

Dependent Variable

Broad interest

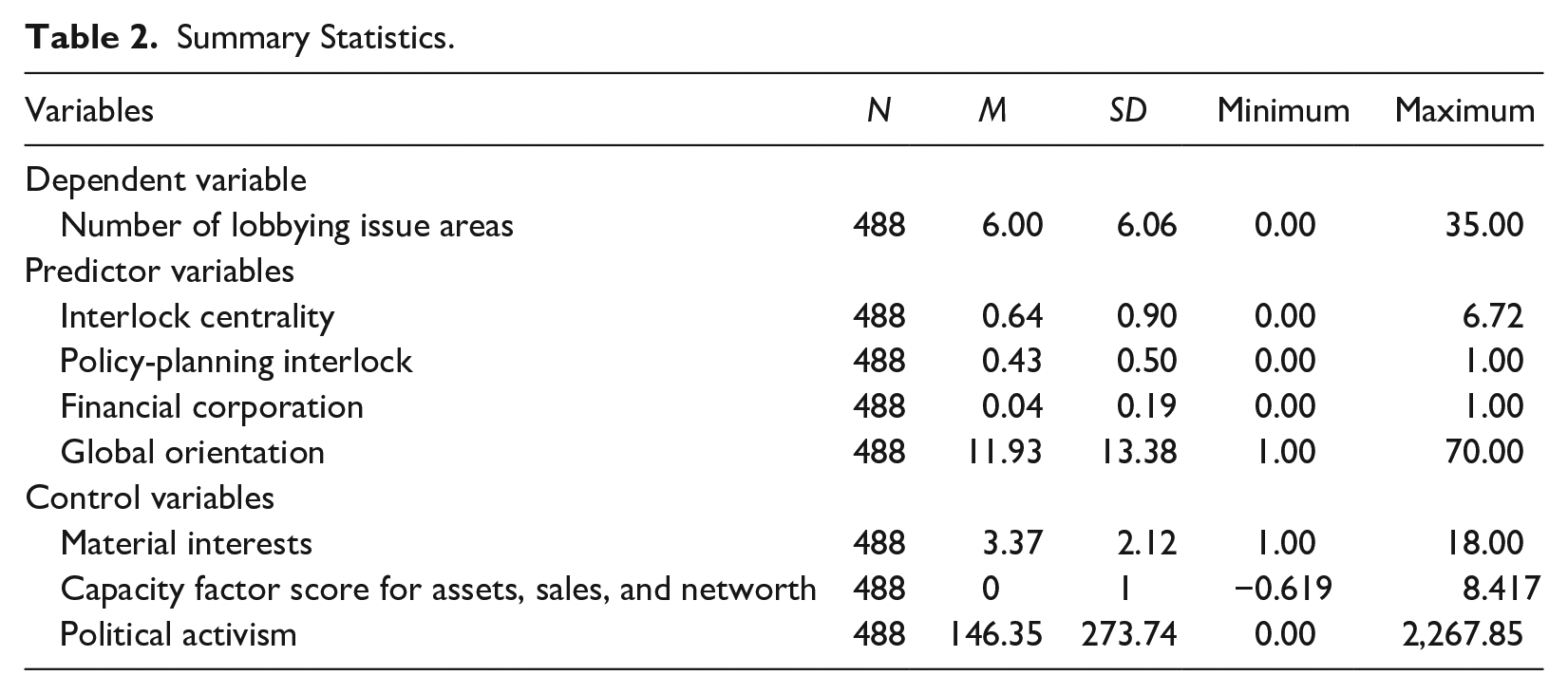

The Center for Responsive Politics uses the issues reported by lobbyists on government disclosure forms to identify 81 issue areas on which lobbying takes place. 12 These include general issue areas such as taxes, banking, defense, health issues, and immigration. Some issues, such as trade, are broader than other issues, like the food industry. Looking at individual issues makes it difficult to measure the scope of interest. Even so, it is also true that, in general, broader interests should be associated with lobbying on a wider array of issue areas. For example, if Firm A lobbies on 40 issues and Firm B lobbies on three, the likelihood is greater that Firm A has a broader interest. While less clear for smaller differences, this problem is ameliorated when we compare the sources of interest, rather than firms. That is, if firms associated with policy-planning groups consistently lobby on more issues than firms not involved in the policy network, we can be relatively confident that policy groups help broaden the interests of the corporate elite associated with them. Thus, we measure broad interest as a count of the number of issue areas in which a corporation engaged in lobbying activity in 2012 (Table 2).

Summary Statistics.

The broadening of a firm’s interest is key to how class-wide logics may be formed. That is, rather than some firms simply operating with predetermined class-wide interests while others follow firm-centric interests, theorists argue that class logics develop in a processual manner via a broadening of interests through relational processes with other firms. As Useem (1984) argues, “It is [a] sense of partial detachment from the narrow concerns of the individual firm and partial attachment to the broader concerns of the class-wide business community that centrally characterizes the inner circle’s outlook” (111, emphasis added). Therefore, by measuring the impact of our predictor variables on the scope of a firm’s lobbying, we can assess the degree to which mechanisms still exist that broaden the interests of firms. As we note, as a robustness check to minimize the noise generated from assessing the total number of issues, we also account for key issues where theorists argue fracturing is most visible (in taxation, healthcare, and finance).

Predictor Variables

Interlock centrality

We used director affiliation data to determine the interlocks between companies and each firm’s network centrality. A firm’s position in the network is measured by Bonacich centrality, which counts every interlock a firms has and weights it by the number of interlocks its neighbors in turn have (Bonacich 1972). Centrality scores, therefore, are associated with being connected to well-connected firms. We transform centrality values to their z-scores for ease of interpretation.

Policy-planning interlock

We operationalize this through a binary variable coded 1 if the corporation is represented in the membership of at least one of the following 12 major think tanks and policy groups: American Enterprise Institute, Brookings Institution, Business Council, Business Roundtable, Chamber of Commerce, Committee for Economic Development, Conference Board, CFR, Heritage Foundation, Hoover Institution, National Association of Manufacturers, and Trilateral Commission. These represent the most influential policy groups in this period and allow our study to be comparable to prior research (see Banerjee and Burroway 2015; Burris 2008; Judis 2001).

Global orientation

While part of the global orientation of firms is undoubtedly network based (i.e., through transnational interlocks and policy groups), scholars from the global capitalism school argue that the globalization of production is the foundation for the TCC (Harris 2014; Robinson and Harris 2000). We measure global orientation by the number of different countries a firm has operations in, standardized to z-scores.

Financial corporation

Here, our measure is a dichotomous variable coded 1 if a firm operates primarily in finance, that is, depository institutions, nondepository credit institutions, securities and commodities services, and holdings and investments (we operationalized that these are firms with Standard Industrial Classification [SIC] codes beginning with 60, 61, 62, or 67).

Control Variables

Material interests

A corporation’s immediate material interests are most shaped by the economic sectors it does business in. We therefore measure the breadth of a firm’s material interests as the number of different sectors a firm operates in, determined by first two digits of all a company’s different SIC codes, standardized to z-scores.

Capacity

One of the constraining factors in corporate political action is the financial capacity a firm has for such action. That is, regardless of the breadth of a firm’s interests, a company needs the capacity to direct resources toward lobbying. However, what constitutes a resource-rich firm varies by the sector the firm operates in. Consequently, we follow prior research (e.g., Dreiling and Darves 2011) and use principal factor analysis to extract a single variable for capacity that measures the company’s assets, sales, and number of employees, standardized to their z-scores.

Political activism

Another factor that may lead a firm to lobby on a variety of issues is if the corporation is simply more politically active. That is, even if the rationale motivating activity is not class based, a firm with a politically engaged CEO or senior leadership may attempt to influence a broad array of policy issues out of ideological motivation. Therefore, we measure the total amount of donations from the firm’s PAC, standardized to z-scores. As prior work suggests that interlocks and policy-planning ties also increase PAC donations (e.g., Murray 2014, 2017), this results in a conservative measure of the influence of our predictor variables on broad interest.

Descriptive Statistics

Analytic Strategy

The dependent variable, the number of issues lobbied on by a firm, is count data and over-dispersed, with a conditional variance that exceeds the mean. The over-dispersion of the data indicates a Poisson model is not as appropriate as a negative binomial regression (NBR) model. While NBR models have the same mean structure as Poisson, allowing the modeling of count data, they also include an additional parameter enabling the modeling of over-dispersion. Although 24 percent of firms did not engage in any lobbying, a Vuong test indicated this was not an excessive amount and a zero-inflated model was not appropriate.

While the above analytic technique is adequate for the data at hand, however, it does not eliminate the problem of homophily which arises when network variables are also predictor variables. That is, corporations may interlock with each other and the same policy groups due to some other form of deep (unmeasured) similarity, rather than those ties creating a similarity through the diffusion of class-wide rationality. As a robustness check on the causality of key network variables the NBR regression identifies as significant, we also conduct matched sample estimation, which controls for confounding factors and accounts for selection bias by comparing observations that have similar propensities of presence of a key predictor variable (Kim, Kogut, and Yang 2015; Rosenbaum and Rubin 1983). That is, we estimate the propensity that each firm has a key network connection (i.e., a direct interlock or a policy-planning interlock) based on all other independent and control variables. We then match each corporation that actually has the relevant network connection (the treated group) with a firm that does not have the connection (the untreated group) but has the most similar propensity score. Finally, we conduct a logistic regression on the matched sample to estimate the treatment effects on the breadth of issues lobbied on by the firm.

Findings and Discussion

Table 3 presents the results of a NBR model estimate of the number of issue areas a corporation lobbied on. As all nondichotomous variables are measured at the interval-ratio level, we transform these variables to their z-scores. Correspondingly, coefficient figures for these variables indicate the effect size on the outcome variable for a 1 standard deviation (SD) increase in the predictor variable. 13

Negative Binomial Regression Estimate of Breadth of Lobbying Interests.

Note. The first number is the unstandardized regression coefficient, the second number in parentheses is the Z statistic, and the third is the bootstrapped standard error. PAC = political action committee; VIF = variance inflation factor.

Variables standardized to their z-scores (coefficient interpreted as effect on outcome variable for 1 standard deviation increase in value of predictor variable).

p < .05. **p < .01. ***p < .001 for one-tailed probabilities.

We find that interlock centrality is a significant predictor of broadened interests (b = .105, p < .010). To illustrate, results indicate the most central firm (Boeing) broadens its interests by 156 percent based solely on network centrality when compared to an isolated firm. This supports H1: the more central a corporation is in the interlock network, the broader its interests. This also suggests that while a decline in network connectivity may have led to weakened network effects over time (our data do not speak to this), it has not been sufficient for the interlock network to no longer provide a broadened rationality to its members.

Being interlocked to a policy-planning organization is also positively and significantly associated with broader interests (b = .435, p < .001). Controlling for other sources of broad interest, including material interests and capacity, and having a director who is a member of a policy-planning organization increase the number of issue areas a firm lobbies on, providing support for H2.

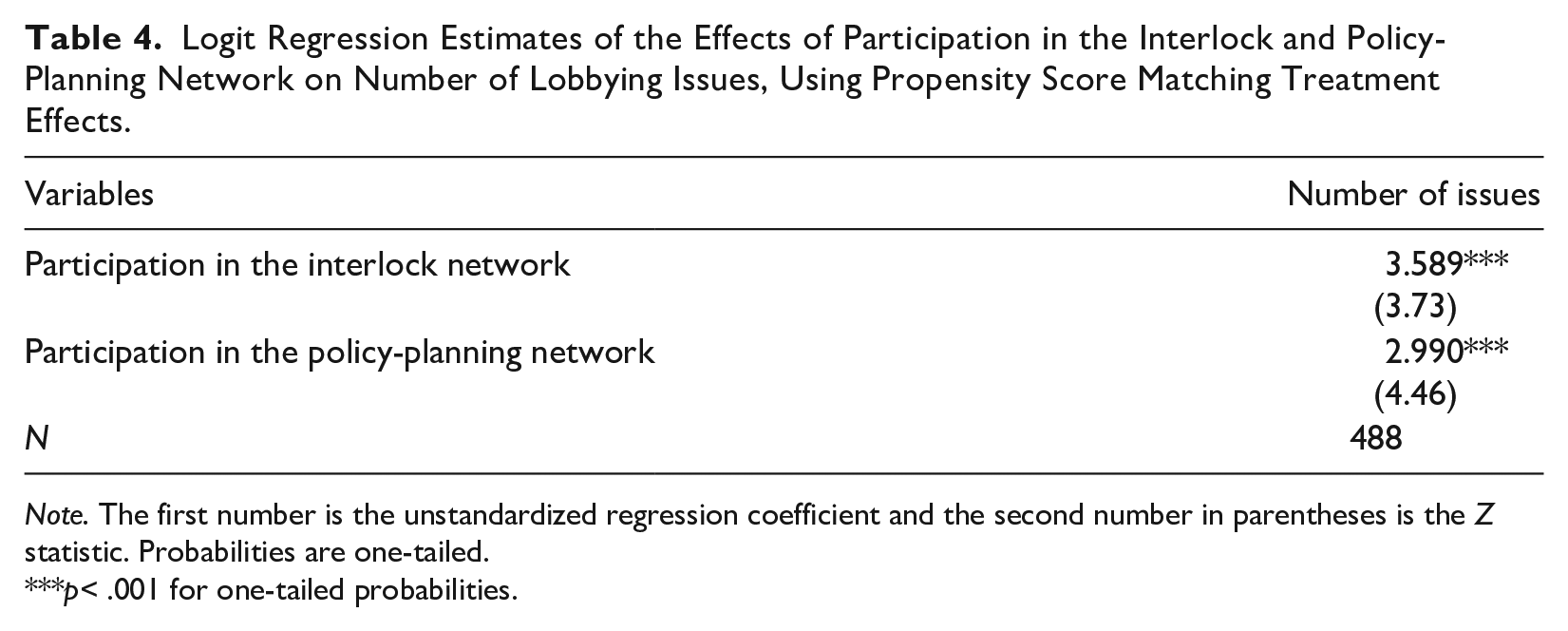

Policy-planning organizations and interlock centrality are distinct in these models, but are tied together in practice. For instance, 42.2 percent of the sample (206 of 488 corporations) participate in both networks. 14 This suggests that if these mechanisms are causal factors, then combined they hold the potential to considerably broaden the interests of the corporate elite. We explored this further in two additional ways. First, we include an interaction variable for firms involved in both networks and find that net of their individual impacts firms involved in both networks are even more likely to show broader interests (b = .061, p < .05). Second, we re-ran our original models, this time disaggregating firms that were involved in the policy network or isolated from it into two subsamples. We find that while centrality in the director network is associated with broader interests in both cases, the effect is approximately five times larger for firms isolated from the policy network (b = .317, p < .05) compared to those embedded it (b = .066, p < .05). This further suggests that while involvement in both networks further broadens the interests of firms, firms isolated from one network are more likely to then be influenced by the other. This lends support to an underlying contention of this paper. 15 As an additional, more robust test of causality of these network variables, Table 4 provides the results of a matched sample treatment effects analysis for each of the key network variables.

Logit Regression Estimates of the Effects of Participation in the Interlock and Policy-Planning Network on Number of Lobbying Issues, Using Propensity Score Matching Treatment Effects.

Note. The first number is the unstandardized regression coefficient and the second number in parentheses is the Z statistic. Probabilities are one-tailed.

p< .001 for one-tailed probabilities.

We see that participation in both the interlock network and the policy-planning networks is positive and significant. This suggests that for firms that are equally likely to have these network ties, the firms that actually have board interlocks and policy group ties lobby on a broader set of interests. In practice, this means firms tied to the director and policy networks lobby on approximately an additional 3.6 and 3 issues respectively, when compared to other similar firms. Given that firms lobbied on a mean number of six issues, this is a sizeable difference, constituting a 50 to 60 percent increase in the breadth of interests of these firms. 16

Given that our measure of broad interest is the number of issue areas on which firms lobby, it is possible the results have a democratizing bias on the substance of the issues under consideration. That is, it may be that embedded firms lobby on more issues simply because the issues they lobby on are themselves indicative of narrower, firm-centric interests. To assess this, we refer to the case studies explored by Mizruchi (2013). Mizruchi argues the breakdown of a class-wide consensus can be seen in the contemporary era through three main differences: (1) the unwillingness of the corporate elite to advocate for higher taxes even though research shows these are necessary for the long-term viability of the U.S. economy on which these firms depend; (2) the relative absence of corporate involvement in the Obama healthcare discussions (when compared to Clinton-era reforms) even though business recognized the rising costs to them from the existing system; and (3) a refusal to advocate for even minor regulations on financial instruments even though these result in recurring crashes to the United States and global economy.

While a detailed discussion of the policy proposals Mizruchi analyzes is beyond the scope of this paper, we tested whether lobbying in these three main issue areas impacted our results. In additional models, we controlled for whether firms lobbied on each of these issues and found effect sizes of our main predictor variables to be substantively equivalent in size and significance. Furthermore, we replicated our matched sample tests separately for whether firms lobbied on these specific issues. While we did find some variations in the magnitude of network effects, the substantive interpretation was the same: even in areas highlighted as exemplars of business disarray, a firm’s involvement in class-wide networks continues to motivate its involvement in the policy arena. 17

Next, H3 and TCC theory are supported by the results for the global scope of a firm’s operations (b = .063, p < .05). Although this appears small, the effect of globalization can be better appreciated by considering that the interests of the most globally oriented U.S. firm (operating in 70 countries) are broadened by 93 percent when compared to domestic-only firms. This suggests that the more globally oriented a firm is, the broader its interests.

While the above findings provide support for the class dominance thesis, the results for financial corporations support a key insight of the fracturing thesis: banks do not appear to have an especially broad interest in lobbying by virtue of their control over capital decisions. The coefficient for financial corporations is not significantly different from nonfinancials (Model 1: b = −.192, p > .05). This supports H4, suggesting that the shift to investment banking activity by commercial banks has narrowed their interests, while the move to commercial loans by nonfinancials has broadened their interests, resulting in similarly broad interests amongst banks and nonbanks. 18

This finding, in concert with the above results on network effects, is key to the larger argument of this paper. We theorize the fracturing thesis is likely correct that banks no longer have the same overarching interest as in decades past and thus do not play the same role in diffusing class-wide rationality as they used to. The fracturing thesis is likely incorrect, however, in assuming the absence of banks would leave the corporate community without the means to develop a broader political rationality. For instance, while 19 of the 20 firms, most central firms in the interlock network in our sample, are nonfinancials, we find this does not alter our main effects: firms tied to the director and policy networks tend to exhibit a broadened outlook regardless of the makeup of the sample.

The effect of these alternative sources of broad interest is, in fact, most visible when we consider financial companies. While operating as a financial company may not broaden a firm’s interests when compared to nonfinancials, financial corporations do, in fact, have slightly broader interests than nonfinancials. Specifically, financial corporations lobby, on average, in 6.7 issue areas, while nonfinancials lobby in 5.9. We find that this small difference is entirely due to the other sources of broad interest. Financial corporations are 45 percent more central in the interlock network and 3.5 times more likely to be members of a policy group.

Conclusion

It is certainly true that many of the longstanding sources of the diffusion of corporate class-wide rationality have declined over the last four decades. Large commercial banks, once at the center of the intercorporate network and unifying the corporate elite, have been replaced by a variety of different industries and sectors. The director network as a whole is also less dense and connected. Nevertheless, we find that key sources of broad class interest remain. Despite these major changes, the interlock network still diffuses a broader interest for firms that participate, with the most central having the broadest set of interests. In addition, participation in the policy-planning network also broadens a firm’s interests. While the nature of financial capital has changed significantly over recent decades, banks still participate in these key corporate networks at a higher rate than nonfinancials. Finally, the global nature of class-wide interests is reflected in the broadening effect of globalized operations.

These findings should be taken with some constraints in mind. First, our study is cross-sectional in nature and does not allow us to draw conclusions on longitudinal trends. Additional research is required to determine the effects of long-term changes in the institutional bases for corporate collective interests. Second, the results are limited to the behavior of domestic firms in the United States. Even so, we note that the fracturing thesis contains both a longitudinal and cross-sectional element. In finding that the interests of firms today are still broadened through their network affiliations, this challenges the conclusions of theorists who argue that the “established understandings of the effects of board interlocks on U.S. corporations, directors, and social elites no longer hold” (Chu and Davis 2016). Moreover, it is fracturing theorists specifically who emphasize the dissolution of the U.S. domestic network (Chu and Davis 2016; Mizruchi 2013). In contrast, we find that while globalization of interests broadens a firm’s interests—a key prediction of the TCC school—the impact of firm networks on domestic political behaviors remain.

Together, these findings are key to understanding modern corporate political action and the government policy that flows from this. For instance, the fractured elite perspective argues that the increase in individually based corporate action, such as lobbying, is a sign of fracturing and that fracturing is to blame for “the gridlock that now characterizes the American political system” (Mizruchi 2013:270–72). In fact, Mizruchi argues that much of the outcomes of neoliberalism, from a lack of universal health care to a failing public education system, are tied to the decline of the corporate elite. Our findings call into question the assumption that individual lobbying by corporations is not tied to class-wide interests. This then calls into question the broader contention that the current political context is a result of fracturing. What our study makes clear is the importance of looking at more than the domestic board interlock network when trying to understand corporate elite power. The interlock network is only one mechanism among multiple that helps to diffuse a broad political outlook that is key to a class-wide rationality. This class-wide approach is global in nature and is developed in corporate think tanks and discussed at policy group meetings, before diffusing through the interlock network (Dreiling and Darves 2011, 2016; Murray 2017; Robinson 2004; Robinson and Harris 2000; Sklair 2001).

Thus, rather than political polarization, neoliberalism, and imperial wars and regime changes being the result of a lack of corporate collective action, our findings suggest it is eminently plausible that these political policies remain the explicit result of corporate political action in service of transnational class-wide interests. In fact, these findings are consistent with recent research examining unity in political donations (Murray 2017).

What does this mean for us today? An approach that only focuses on the decline in density in the interlock network may, for example, interpret the rise of President Trump to the inability of a fractured elite to stop him. 19 Giving proper importance to the policy-planning network and global interests, however, provides a different interpretation. For instance, the President’s Strategic and Policy Forum—an advisory group formed to advise on economic issues—is filled with executives of the largest corporations, including the CEOs of financial firms and a variety of nonfinancial sectors ranging from manufacturing to retail, technology, media, and business consulting. 20 Of the 16 people appointed, 12 (75 percent) are affiliated with at least one policy-planning organization, while just under half (seven members) are affiliated with the Business Roundtable, with an equal number also being members of the CFR. While the CFR is traditionally seen as a globally oriented group, an additional four of the advisors are also members of the World Economic Forum. This suggests that a globally oriented corporate elite, united by broad class interests developed in the policy-planning network, are in positions of influence in the Trump administration. Crucial to our understanding, many of these same firms and industries were represented on advisory committees put forward by his predecessor, President Obama, often by the very same individuals (Young, Banerjee, and Schwartz 2018). What these tell us is that, instead of marking a retreat or disarray of the corporate elite, the Trump administration provides a continuation of many of the same mechanisms of business political action: senior executives linked through a variety of corporate networks.

Understanding the sources of class-wide rationality is key to an accurate interpretation of the corporate power structure and the current political climate. Our findings suggest that a greater emphasis should be placed on persistent mechanisms that unify the corporate elite, including unity engendered by central firms (regardless of whether they are financial firms), the policy-planning network, and finally, the transnational aspects of this elite. That is, even if the corporate elite do not always act as a monolithic bloc, the mechanisms that promote political unity still remain.

Footnotes

Authors’ Note

Tarun Banerjee is now affiliated with Department of Sociology, John Jay College, City University of New York.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.