Abstract

Natural dye-based textile production is increasingly promoted as an environmentally sustainable alternative to synthetic dyeing. However, its economic sustainability and livelihood implications remain underexplored, particularly in place-specific contexts. This study examines the financial performance, operating risk, and efficiency of artisan-managed natural textile dyeing enterprises in Assam, India—a region characterized by rich biodiversity, long-standing dyeing traditions, and rural livelihood dependence on small-scale production systems. Drawing on primary enterprise-level data from lac and indigo (rom) dyeing units, the study employs an integrated analytical framework combining cost–volume–profit (CVP) analysis, regression modelling, and Data Envelopment Analysis (DEA). The study is based on primary data collected from 150 enterprises, and econometric estimations were conducted using Stata 17. The results show that natural dyeing enterprises are economically viable, exhibiting high gross profit and contribution margins, low break-even sales, and substantial margins of safety, indicating limited operating risk. Regression analysis reveals that profitability is driven by contribution margin, scale of operation, and technology type, while labour cost intensity negatively affects financial performance. DEA results indicate higher technical and scale efficiency among indigo dyeing enterprises, whereas inefficiency among lac dyeing enterprises is largely attributable to sub-optimal scale. A positive relationship between technical efficiency and profitability further highlights the role of efficient resource use in strengthening enterprise resilience. By integrating financial performance, efficiency, and risk analysis within a place-based empirical framework, the study contributes to debates in economic geography and socio-environmental sustainability. The findings demonstrate how environmentally benign, traditional production systems can support resilient rural livelihoods when embedded within appropriate efficiency-, scale-, and productivity-enhancing strategies.

Keywords

Introduction

The textile dyeing industry is a major contributor to global manufacturing and employment, yet it is widely acknowledged as one of the most environmentally polluting segments of the textile value chain.1,2 The large-scale use of synthetic dyes has led to severe water pollution, chemical waste, and occupational health hazards, particularly in developing countries where environmental regulations and effluent treatment facilities are inadequate.3–5 Research in Tiruppur, India, and Dhaka, Bangladesh, shows that untreated effluents from textile dyeing have degraded river systems such as the Noyyal and Buriganga, making them unsuitable for irrigation and aquatic life due to intense colouration, elevated chemical oxygen demand (COD), and heavy metal accumulation.6,7 Around 10–15% of dyes used in textile processing fail to adhere to fabrics and are discharged directly into wastewater. 8 These effluents often contain toxic, carcinogenic, and non-biodegradable compounds that persist in ecosystems and pose serious risks to human health.9,10 As concerns over environmental degradation, climate change, and public health intensify, the textile sector faces mounting pressure to adopt cleaner and more sustainable production systems.11,12

Recent reports from Assam’s leading newspapers have underscored the harmful effects of synthetic dyes in the state’s textile sector. The Sentinel Assam 13 reported that two textile factories in Guwahati were sealed for releasing untreated dye effluents into the Mora Bharalu river, highlighting the ecological risks posed by synthetic wastewater discharge. Similarly, another Sentinel Assam 14 editorial emphasized the adulteration of Muga silk with synthetic dyes, warning of both environmental hazards and threats to Assam’s cultural heritage. The Assam Tribune 15 has long reported on the health impacts of synthetic dyes, noting cases of skin allergies among children wearing chemically dyed clothes and promoting natural alternatives. The same outlet 16 stressed the importance and relevance of natural dyes for sustainable textile practices. Collectively, these accounts provide a strong rationale for exploring natural dye alternatives to safeguard Assam’s environment, public health, and traditional weaving industries.

Within the sustainability discourse, natural dyes have re-emerged as environmentally benign alternatives to synthetic dyes. 17 Derived from plants, insects, and minerals, they are biodegradable, renewable, and generally safer for ecosystems and human health.11,18 The use of colourants dates back to the Stone Age, when minerals served as pigments, and expanded with weaving across ancient civilizations such as the Phoenicians, Indians, Romans, Egyptians, and Africans.11,17,19 Until the mid-nineteenth century, natural dyes dominated textile colouration. 20 Synthetic dyes later gained prominence due to lower costs, ease of application, and superior colour fastness.4,21,22 Today, thousands of synthetic dyes are manufactured, with textiles as their primary application. 23 In contrast, natural dyes account for less than 1% of global dye consumption, constrained by limited extraction yields, high production costs, and weak fabric affinity. 24 Despite these limitations, the environmental and health risks of synthetic dyes have led to bans in several countries, prompting renewed interest in natural alternatives. 25 Natural dyes are relatively simple to apply, eco-friendly, biodegradable, renewable, safe, and non-allergenic, with minimal risk of harmful chemical reactions.26–28 Recent studies confirm that, with appropriate mordants and techniques, natural dyes can achieve acceptable colour strength and fastness, reaffirming their technical feasibility in modern textile production.17,26,29–34 Beyond environmental benefits, natural dyeing practices are closely tied to traditional knowledge and artisanal production. 18 In developing economies, particularly rural and resource-rich regions, traditional textile enterprises generate employment, preserve cultural heritage, and support inclusive development. 35 Handloom and artisanal sectors are vital livelihood sources where industrial opportunities are scarce. 36 Consequently, natural dye-based enterprises are increasingly recognized as eco-friendly units and instruments of sustainable rural entrepreneurship.25,33,36

India has a long tradition of natural dyeing 37 with the North-East particularly significant due to its biodiversity and indigenous dye-yielding plants. 38 Over 240 dye plants have been identified in the region, many in Assam.39,40 Assam’s ethnic groups—including the Bodo, Mishing, Ahom, Garo, Dimasa, and Assamese communities—maintain distinctive attire often coloured with indigenous dyes. 41 This cultural richness makes Assam a hub for natural dyeing techniques, though much expertise remains confined to rural artisans unaware of commercial opportunities. 42 Assam’s association with natural dyes dates back to the medieval period, exemplified by the Brindabani Bastra created under Srimanta Sankardeva using plant-based colours. 43 Today, lac and indigo (rom) dyeing continue in artisan-managed enterprises, typically small-scale, family-run, and embedded in local socio-economic systems. 38 While small industries in India are renowned for indigenous fabrics and designs, 44 global competition, reliance on outdated methods, and grassroots inefficiencies pose challenges, threatening both artisan livelihoods and the long-term sustainability of Assam’s textile industries. 45

Despite growing interest in natural dyes from environmental, cultural, and technological perspectives, the economic and financial viability of natural dye-based textile enterprises remains underexplored. Existing studies emphasize dye extraction, application techniques, and fastness properties.17,27,29–31,33,34,42 Research on Assam’s textile industries often highlights livelihoods and cultural significance,35,41,45 or adopts technical lenses.38,42,46 Yet, rigorous empirical work on enterprise-level profitability, cost efficiency, operating risk, and technical efficiency is scarce. Integrated quantitative analyses combining financial performance with efficiency measurement are notably absent, leaving unanswered whether natural dyeing enterprises can sustain themselves under market constraints.

This gap is critical because environmental sustainability alone does not ensure the long-term survival of small and artisan-managed enterprises. For natural dyeing units to scale up, compete in niche and mainstream markets, and provide stable livelihoods, they must demonstrate economic viability, efficient resource use, and resilience to fluctuations in demand and costs. Evidence from small enterprises and informal production systems suggests that profitability, cost structure, and efficiency are decisive for survival and growth.47,48 Without empirical insights into these dimensions, policy initiatives promoting natural dyes risk remaining normative rather than evidence-based.

Against this backdrop, the present study evaluates the financial performance and economic viability of natural textile dyeing enterprises in Assam, focusing on lac and indigo dyeing industries. Using primary data from artisan-managed enterprises, it employs an integrated framework combining cost–volume–profit (CVP) analysis, regression modelling, and Data Envelopment Analysis (DEA). CVP analysis assesses profitability, break-even performance, and operating risk; regression identifies determinants of profitability and resilience, controlling for scale and cost intensity; DEA measures technical and scale efficiency, quantifying input savings and productivity improvements.

The study pursues three objectives: to evaluate financial performance using CVP indicators such as gross profit ratio, contribution margin, break-even sales, and margin of safety; to identify key factors influencing profitability and operating risk through regression analysis; and to assess technical and scale efficiency using DEA, examining its relationship with financial performance. By integrating these approaches, the study provides a multidimensional assessment that moves beyond descriptive or single-method analyses. Empirically, it offers rare quantitative evidence on artisan-based enterprises; methodologically, it advances research by unifying CVP, regression, and DEA; and from a policy perspective, it delivers evidence-based insights into efficiency improvement, scale optimization, and cost management. Overall, the study strengthens the economic rationale for promoting natural dye-based enterprises as sustainable and resilient components of rural and green industrial development. Building on these, this study advances existing literature by providing an integrated empirical assessment of enterprise performance in natural dye-based textile production. Whereas prior research has typically examined profitability, cost structures, or efficiency in isolation, this study unifies these dimensions within a single analytical framework. By combining cost–volume–profit (CVP) analysis, regression modelling, and Data Envelopment Analysis (DEA), it demonstrates how cost structure, operating risk, efficiency, and profitability are jointly determined in artisan-managed enterprises. Applied to Assam’s context, this integration offers rare empirical evidence on how environmentally sustainable production systems perform under real-world economic conditions, thereby extending both sustainability and small enterprise scholarship.

Theoretical grounding

This study is guided by two complementary theoretical stances that help the interpretation of enterprise performance in the context of natural dye-based production systems.

First, the sustainable livelihoods approach offers a conceptual lens to understand how resource-based, small-scale enterprises contribute to income generation and resilience in rural economies.49,50 This view emphasizes how locally available natural resources, household labour, and traditional knowledge systems influence the shaping of livelihood outcomes. In the context of natural dyeing enterprises in Assam, this framework is particularly relevant, as production is closely embedded in local ecological and socio-economic conditions.

Second, the study draws on firm-level performance theory, which highlights the importance of cost structure, efficiency, and scale in determining profitability.51,52 Within this perspective, financial outcomes depend on how effectively enterprises manage variable costs, control fixed costs, and utilize available resources. The cost–volume–profit (CVP) framework captures the role of cost structure and operating risk,53,54 while Data Envelopment Analysis (DEA) provides a measure of technical and scale efficiency.47,55

By combining these perspectives, the study adopts an integrated framework that links livelihood-based production systems with firm-level performance dynamics. This approach provides a basis for understanding how profitability, efficiency, and operating risk are jointly determined in small, artisan-managed enterprises, and helps anchor the empirical analysis within both sustainability and economic theory.

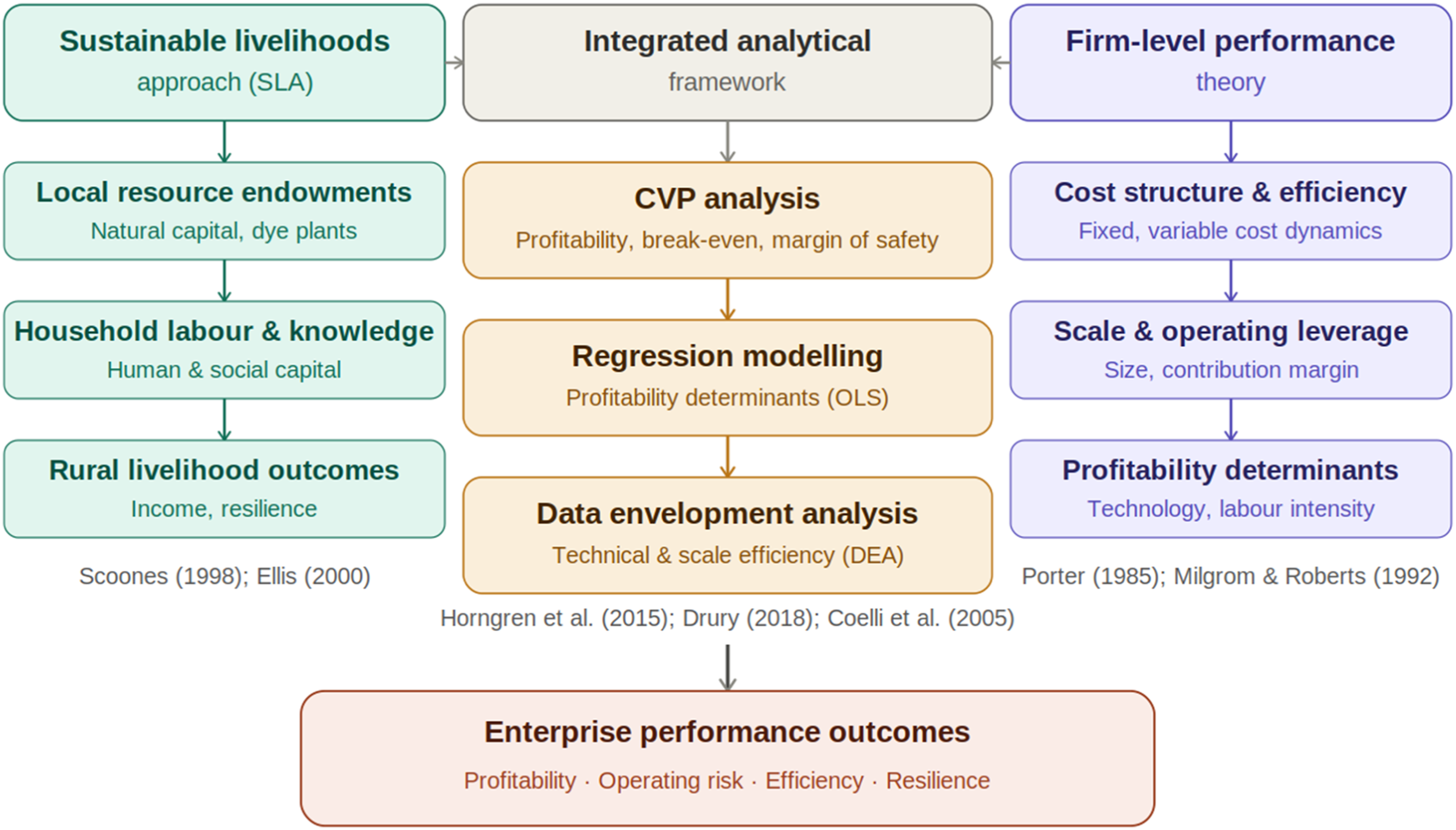

The framework presented in Figure 1 rests on two complementary theoretical pillars. The Sustainable Livelihoods Approach (left) situates production within local ecological and socio-economic conditions, tracing how natural resource endowments, household labour, and traditional knowledge translate into rural livelihood outcomes. Firm-level performance theory (right) focuses on the internal economics of the enterprise, linking cost structure, scale, and operating leverage to profitability determinants. Together, these two pillars form an integrated analytical framework (centre) that is operationalized through three empirical tools: Data Envelopment Analysis (DEA), which measures technical and scale efficiency; regression modelling, which uses OLS estimation to identify the factors that determine profitability; and cost–volume–profit (CVP) analysis, which evaluates profitability, break-even performance, and operating risk. When combined, these methods provide a multifaceted evaluation of artisan-managed lac and indigo dying businesses in Assam, India, based on a set of enterprise performance outcomes, including profitability, operating risk, efficiency, and resilience. Integrated conceptual framework for enterprise performance in natural dye-based production systems. Source: Authors’ creation.

Data and methodology

Study area and sampling design

The study is based on primary data collected from natural textile dyeing enterprises in Assam, India, during 2024–25. Assam has a long tradition of natural dyeing, with artisan-managed enterprises continuing to operate. More than 240 natural dye-yielding plants have been identified in the North-East, most of them in Assam. 39 Chakravarty and Kataky 56 documented that active dyeing units are relatively limited and spatially concentrated, with Boko in Kamrup district and Titabor in Jorhat district serving as principal centres of commercial and technological viability. Building on this evidence, the present study focuses on these two locations: Titabor, dominated by lac-based dyeing enterprises, and Boko, representing indigo (rom) dyeing enterprises. Their selection reflects both historical association and contemporary relevance as clusters with the highest concentration of active units. Focusing on these centres allows meaningful variation in technology, cost structure, and performance while ensuring the sample reflects significant practices in Assam.

Within the study areas, random sampling was used to select enterprises. The unit of analysis is the artisan-managed natural dyeing enterprise, typically household or micro-enterprise level. A total of 150 enterprises were surveyed, representing both lac and indigo units. The sample size was determined by population availability, analytical requirements, and field feasibility. Pre-survey reconnaissance confirmed a finite and well-defined population of active enterprises. A sample of 150 was adequate for descriptive analysis, multiple regression estimation, and Data Envelopment Analysis (DEA). For regression, the sample exceeds rules of thumb relating observations to explanatory variables, ensuring reliable inference. For DEA, the number of decision-making units far exceeds minimum requirements, allowing meaningful efficiency measurement. These considerations justify the chosen sample size as analytically sufficient and practically feasible. All econometric analyses were done using Stata 17, while the DEA computations were conducted using DEAP 2.1.

Data collection involved face-to-face interviews with enterprise owners or primary operators familiar with production and financial details. Each interview lasted 35–45 min, depending on enterprise size and complexity. Follow-up questions were asked where necessary to cross-check responses and improve reliability. Informed consent was obtained from all respondents, and confidentiality of enterprise information was assured.

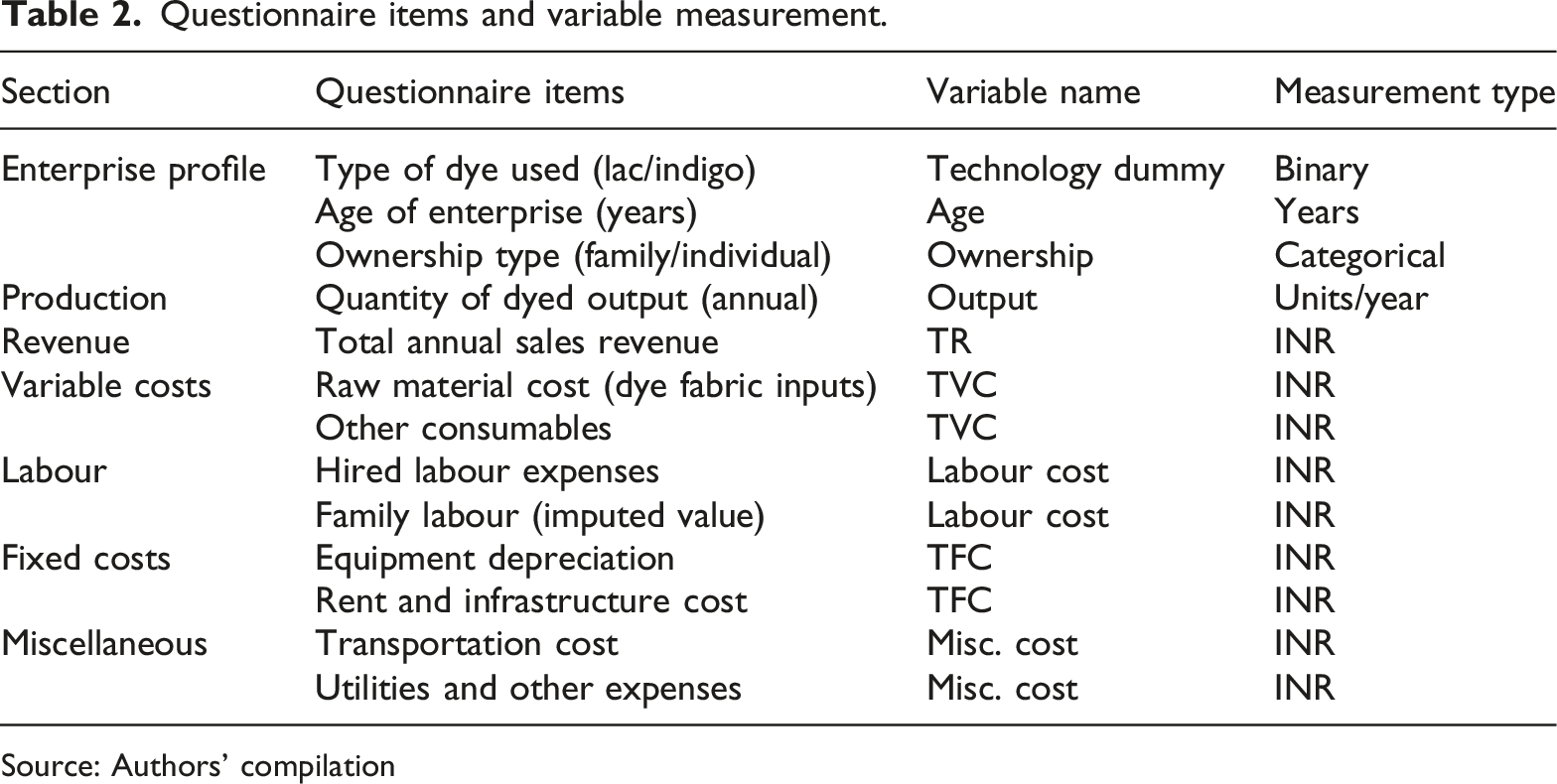

Data collection and variable construction

Key variables used for the study.

Source: Authors’ compilation

Questionnaire items and variable measurement.

Source: Authors’ compilation

The questionnaire items were designed to directly correspond with the variables used in CVP analysis, regression models and DEA estimation, ensuring internal consistency between data collection and empirical analysis. Cost intensity variables such as labour expense ratio and miscellaneous expense ratio are expressed as proportions of total sales. A binary technology dummy variable is constructed to distinguish indigo dyeing enterprises from lac dyeing enterprises. Scale of operation is proxied by average sales revenue.

As the study relies on self-reported financial data, there is potential for measurement error arising from recall bias or reporting inaccuracies. To mitigate this, responses were cross-verified during interviews wherever possible. Nevertheless, some degree of measurement error cannot be entirely ruled out.

Methodology

Accounting ratios and cost–volume–profit (CVP) indicators

To assess financial performance and operating risk, the study employs a set of accounting ratios and CVP indicators derived from the enterprise profit identity. These indicators include gross profit ratio, contribution margin ratio (profit–volume ratio), labour expense ratio, miscellaneous expense ratio, break-even sales, and margin of safety.

Rather than treating these indicators as isolated descriptive measures, the study uses them as structural indicators of cost behaviour and operating leverage. Industry-wise averages of these indicators are computed to facilitate comparison between lac and indigo dyeing enterprises.

Enterprise profit function

The enterprise profit function expresses a firm’s objective in microeconomic terms: profit (π) equals total revenue minus total cost, modelled as a function of output and input prices. 57 It links observable outcomes—revenues, costs, profits—to technology, scale, and price effects, forming the basis for cost–volume–profit (CVP) diagnostics and econometric models. 53 Empirically, profit regressions identify determinants of performance in small enterprises and agriculture, while efficiency tools such as DEA complement profit analysis by benchmarking input use.47,58 Together, CVP, regression, and DEA decompose profitability into price, scale, and cost components, connecting them to managerial and policy variables.

At the enterprise level, a natural dyeing unit is modelled as a production entity that transforms labour and material inputs into dyed textile output under given technological and market conditions. The profit of enterprise i is defined as:

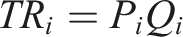

Total revenue is expressed as:

Total cost is decomposed into variable and fixed components:

Substituting, enterprise profit can be written as:

This expression highlights the central role of contribution margin

Cost–volume–profit (CVP) framework

Cost–volume–profit (CVP) analysis is employed to examine the relationship between output volume, cost structure, and profitability, with particular emphasis on contribution margin, break-even point, and margin of safety. The CVP framework is widely used in managerial and applied economic analysis to evaluate operating leverage and financial risk by decomposing profits into fixed and variable cost components.53,54 By explicitly linking sales volume to cost behaviour and profit outcomes, CVP analysis provides a simple yet powerful tool for assessing enterprise viability and sensitivity to demand fluctuations, especially in small and micro-enterprise settings.

The contribution margin (CM) for enterprise i is defined as:

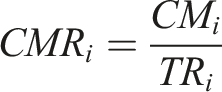

The contribution margin ratio (CMR) is given by:

The CMR measures the proportion of sales revenue available to cover fixed costs and generate profit and is widely used as a key indicator of cost efficiency in cost–volume–profit analysis.53,54

Break-even analysis and operation risk

The break-even point (BEP) represents the level of output or sales at which total revenue equals total cost and profit is zero. That is,

Solving for output at the break-even point:

In value terms, break-even sales are expressed as:

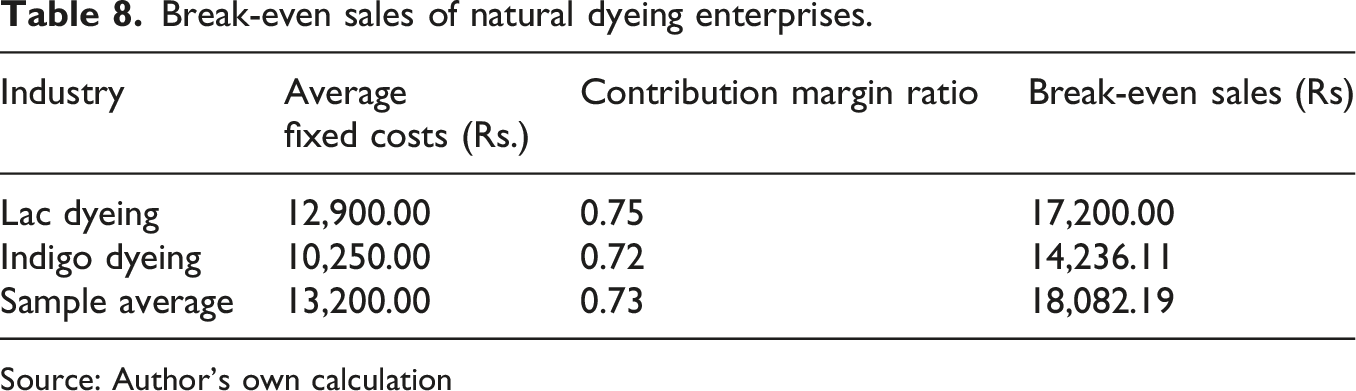

Enterprises with lower break-even sales levels face lower operating risk, as they require a smaller volume of sales to avoid losses. Accordingly, break-even analysis provides a direct measure of financial vulnerability under fluctuating market conditions, particularly in small and micro-enterprises where fixed costs amplify operating leverage.53,54,59,60

Margin of safety and financial resilience

While break-even analysis identifies the minimum sales required for viability, the margin of safety (MOS) measures the extent to which actual sales exceed this threshold:

The margin of safety ratio (MoSR) is defined as:

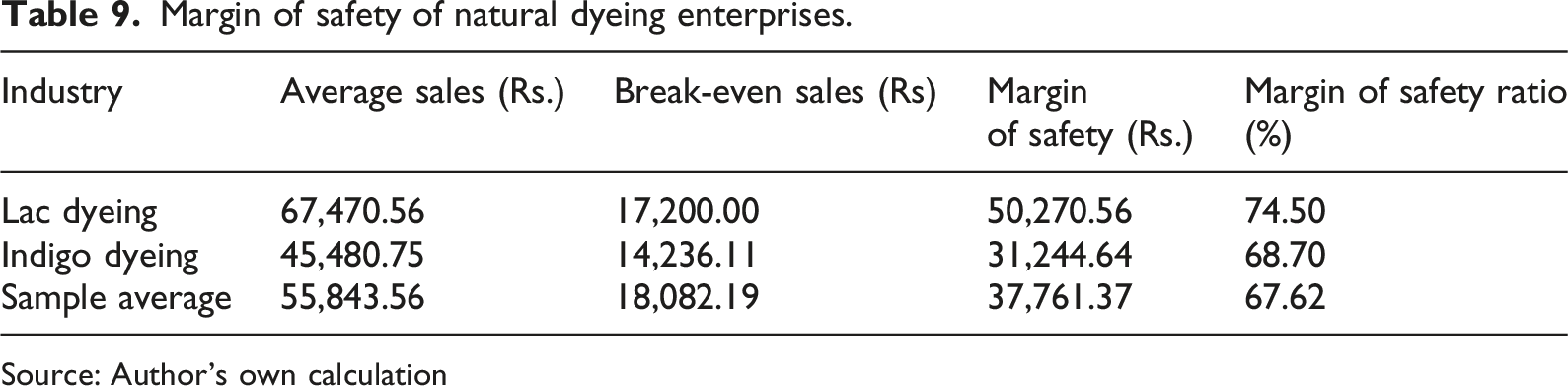

A higher margin of safety indicates greater financial resilience and the ability to withstand adverse shocks such as demand contraction or cost escalation, as it reflects the extent to which actual sales can decline before losses occur. Together, break-even point (BEP) and margin of safety (MOS) capture the risk dimension of enterprise performance by quantifying exposure to fluctuations in sales and costs.53,54,59,60

Regression model specification and estimation strategy

While CVP analysis provides structural insights into profitability and risk, it does not explain why enterprises differ in performance. To address this, the study employs regression analysis to model profitability, cost efficiency, and operating risk as functions of enterprise characteristics, estimating a series of cross-sectional enterprise-level regression models to identify their key determinants. Ordinary Least Squares (OLS) estimation is employed, with heteroskedasticity-robust standard errors to account for scale-related variance in enterprise outcomes. A potential concern in the empirical specification is endogeneity between efficiency and profitability, as more efficient enterprises may achieve higher profits, while higher profitability may also enable efficiency-enhancing investments. Given the cross-sectional nature of the data and the absence of suitable instruments, the analysis does not attempt to establish causal relationships. Instead, the regression results are interpreted as identifying associations between variables. Future research using panel data or instrumental variable approaches could address this issue more rigorously.

Profitability models

The enterprise profitability model forms the core econometric specification of the study. Profit is modelled in reduced form as a function of technology type, scale, and cost structure, consistent with firm-level performance analysis where profitability outcomes are linked to observable characteristics rather than derived from optimization models.61,62 Reduced-form regressions are widely applied to small enterprises. 58 A technology dummy captures process differences, while logarithmic scale accounts for non-linear size effects. Cost structure is represented by labour and expense ratios. 63 Contribution margin ratio, central to CVP analysis, measures operating leverage.53,54

Enterprise profitability is modelled in reduced form as:

Ratio-based and risk models

Absolute profit levels indicate financial performance but are scale-sensitive and may obscure efficiency across firms. To address this, ratio-based and risk-oriented models are estimated. Gross profit ratio normalizes outcomes for comparison across heterogeneous enterprises.58,61 Operating risk is assessed using break-even sales and margin of safety, core CVP tools for evaluating vulnerability and leverage.53,54 Break-even identifies the minimum sales to avoid losses, while the margin of safety measures resilience to demand shocks. 60 Incorporating these CVP indicators into regressions extends accounting diagnostics into econometric analysis.

To control for scale bias, additional models are estimated with ratio-based dependent variables:

Operating risk is examined using break-even scales and margin of safety ratios:

These models explicitly link cost structure and scale to financial vulnerability.

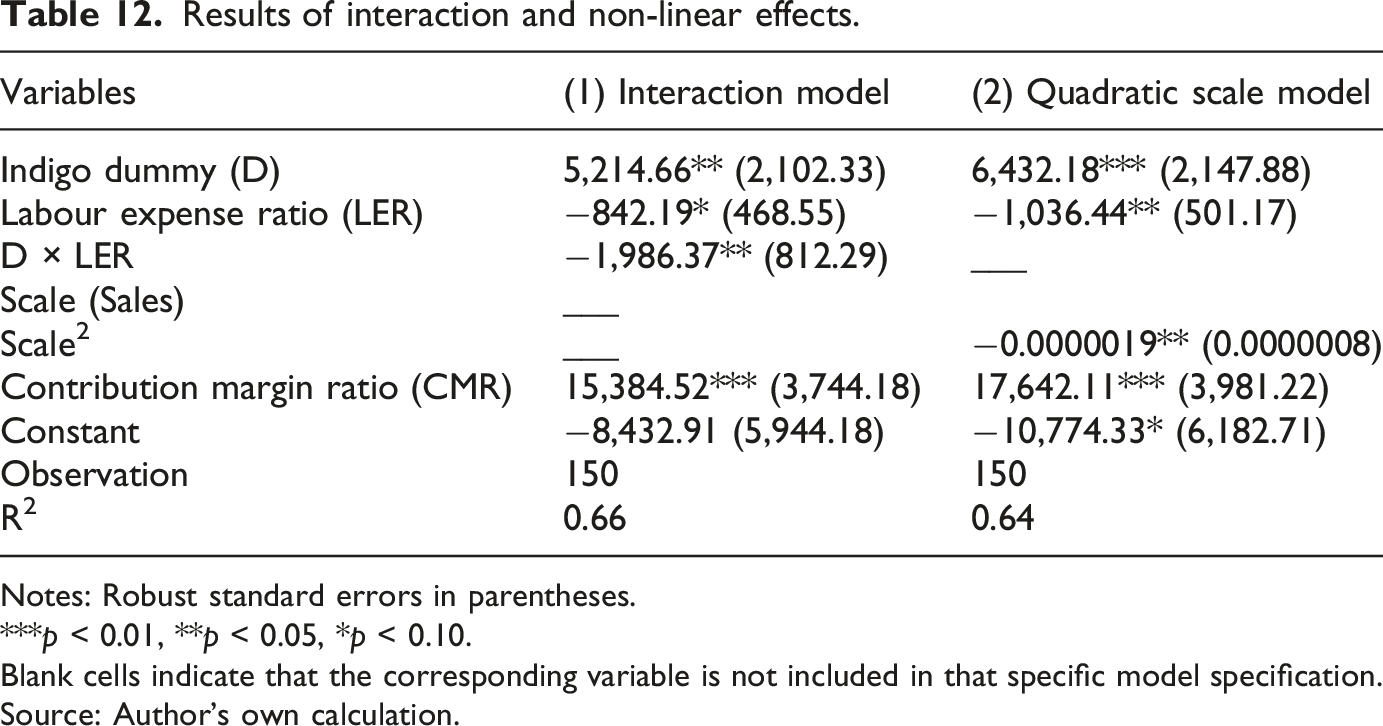

Interaction and non-linear effects

To refine interpretation of baseline profitability results, interaction and non-linear specifications are estimated as robustness checks. Interaction terms between technology type and labour expense ratio test whether labour cost intensity affects profitability differently across production technologies, a common approach in applied econometrics to capture heterogeneous responses. 62 Quadratic scale terms assess non-linear returns to scale and optimal enterprise size, reflecting diminishing returns often observed in micro-enterprises due to coordination costs or rising overheads.47,61 These models validate and deepen the core profitability analysis by explicitly testing heterogeneity and non-linearity.

To capture technology-specific cost sensitivity, interaction terms are introduced:

In addition, quadratic scale terms are used to test for diminishing returns:

Diagnostic test.

Notes: Breusch–Pagan and White tests reject the null hypothesis of homoskedasticity at the 1% level.

All models are estimated using OLS with heteroskedasticity-robust standard errors.

Source: Author’s own calculation.

adenotes significance at the 1% level.

In addition to the reported diagnostic tests, alternative model specifications were estimated to assess the robustness of the results. These included variations in variable definitions and model specifications. The core findings remained qualitatively consistent across these specifications, reinforcing confidence in the stability of the estimated relationships.

Data Envelopment Analysis (DEA) method

Financial indicators alone cannot capture how efficiently enterprises transform inputs into outputs; hence the study incorporates Data Envelopment Analysis (DEA), a non-parametric frontier technique widely applied to measure relative technical and scale efficiency with multiple inputs and outputs.55,64 DEA constructs an empirical efficiency frontier against which each unit is benchmarked, identifying those that convert resources most effectively without assuming a functional form.65,66 Each enterprise is treated as a Decision-Making Unit (DMU) using labour, variable, and fixed costs to generate gross profit. An input-oriented DEA model is adopted, with Constant and Variable Returns to Scale specifications estimated to distinguish technical from scale efficiency. Efficiency scores are then incorporated into regressions to examine the efficiency–profitability nexus. The choice of inputs and output is guided by both theoretical considerations and data availability. The selected inputs—labour expenses, variable costs, and fixed costs—represent the primary resources utilized in production. Gross profit is used as the output variable as it captures value addition net of intermediate costs and aligns with the study’s focus on economic viability. This specification is consistent with standard applications of DEA in enterprise performance analysis, where cost-based inputs and profit-related outputs are used to evaluate resource-use efficiency. 47

Definition of decision-making units (DMUs)

Each artisan-managed natural dyeing enterprise surveyed in the study is treated as a Decision-Making Unit (DMU). Let there be

Input–output specification

Based on data availability and relevance to production decisions, the DEA model employs the following input–output structure:

Inputs

(i) (ii) (iii)

Output

Gross profit is selected as the output variable as it reflects productive performance net of intermediate costs and aligns with the study’s objective of assessing economic viability.

Input-oriented DEA model

An input-oriented DEA model is adopted, reflecting the fact that enterprises have greater control over input usage than output prices or market demand. The objective is to determine the proportion by which inputs can be reduced without reducing output.

Constant returns to scale (CRS) model

The CRS DEA model assumes proportional changes in output with changes in inputs. For each DMU

A DMU is considered technically efficient if

Variable returns to scale (VRS) model

To account for scale heterogeneity, the VRS DEA model introduces a convexity constraint:

Scale efficiency and returns to scale

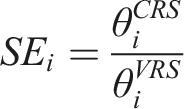

Scale efficiency (SE) is calculated as:

Returns to scale are classified as: (i) Increasing Returns to Scale (IRS) if scaling up inputs leads to more than proportional output increase (ii) Constant Returns to Scale (CRS) if outputs change proportionally (iii) Decreasing Returns to Scale (DRS) if outputs increase less than proportionally

This classification helps identify whether inefficiency arises from sub-optimal scale or technical factors.

DEA efficiency scores indicate the proportion by which inputs can be reduced while maintaining the same level of output. For example, a score of

Results

This section presents the empirical findings of the study in a structured manner. Results are first reported for accounting ratios and cost–volume–profit indicators, followed by regression estimates and Data Envelopment Analysis (DEA) results. Each set of results is subsequently discussed in relation to enterprise performance, efficiency, and operating risk.

Financial performance of natural dyeing enterprises

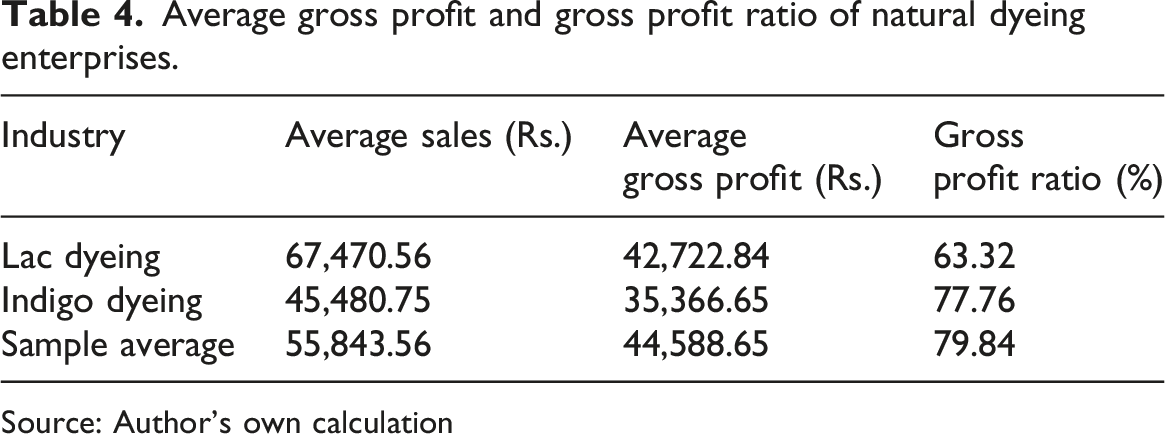

Average gross profit and gross profit ratio of natural dyeing enterprises.

Source: Author’s own calculation

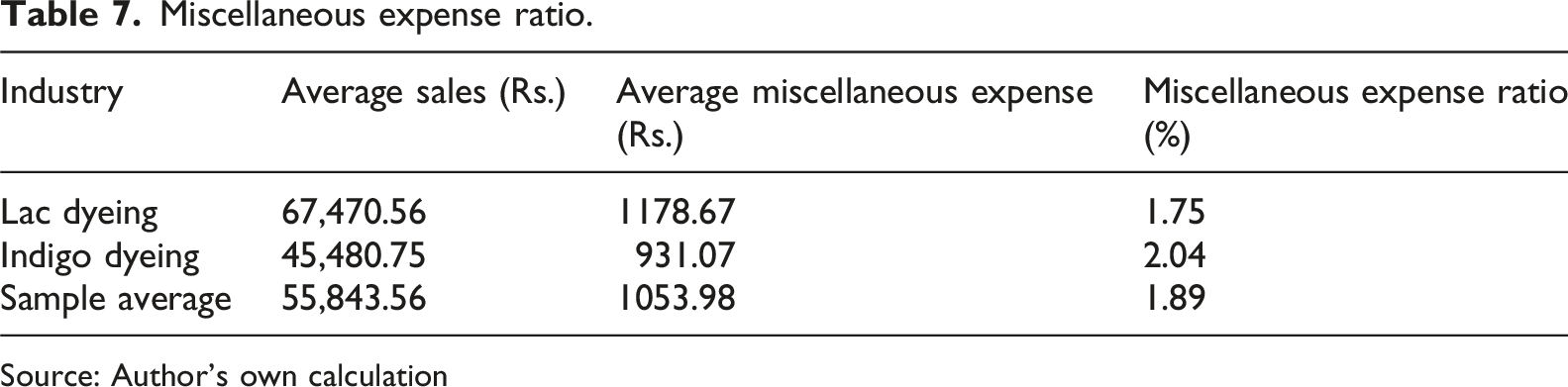

The relatively high gross profit ratios observed in the sample require contextual interpretation. These values primarily reflect the cost structure of artisan-managed enterprises rather than unusually high absolute profits. In particular, the low variable cost base, driven by the use of locally available raw materials and limited reliance on purchased inputs, results in a large share of revenue being retained as gross profit. In addition, labour costs are partly understated in accounting terms due to the use of family labour, which is either unpaid or imputed at below-market rates.

On the revenue side, natural dye-based textiles often cater to niche and culturally embedded markets, where products may command price premiums relative to mass-produced alternatives. At the same time, the small scale of operations implies that absolute profit levels remain modest despite high profit ratios. Accordingly, the reported figures should be interpreted as indicators of cost efficiency and pricing structure rather than as evidence of unusually high-income levels.

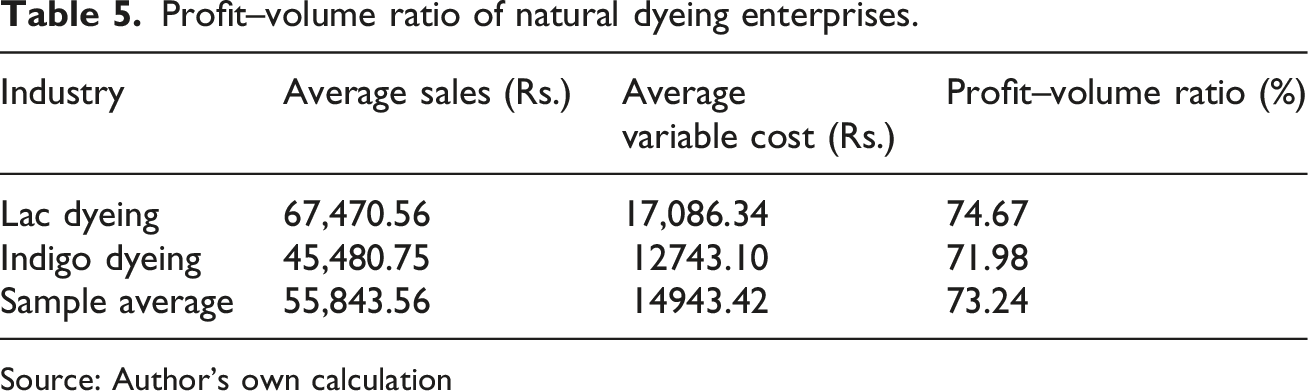

Profit–volume ratio of natural dyeing enterprises.

Source: Author’s own calculation

Expense structure of natural dyeing enterprises

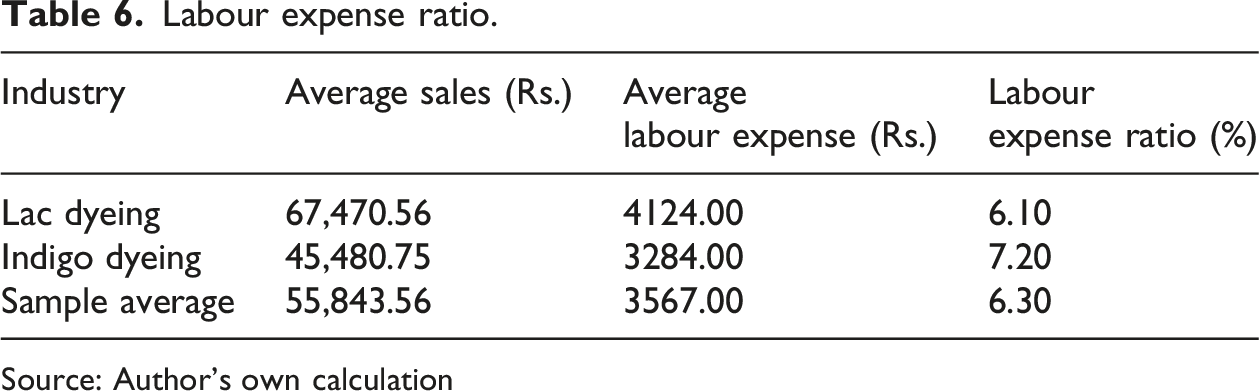

Labour expense ratio.

Source: Author’s own calculation

Miscellaneous expense ratio.

Source: Author’s own calculation

Cost–volume–profit (CVP) analysis

Break-even sales of natural dyeing enterprises.

Source: Author’s own calculation

Margin of safety of natural dyeing enterprises.

Source: Author’s own calculation

Determinants of profitability and risk

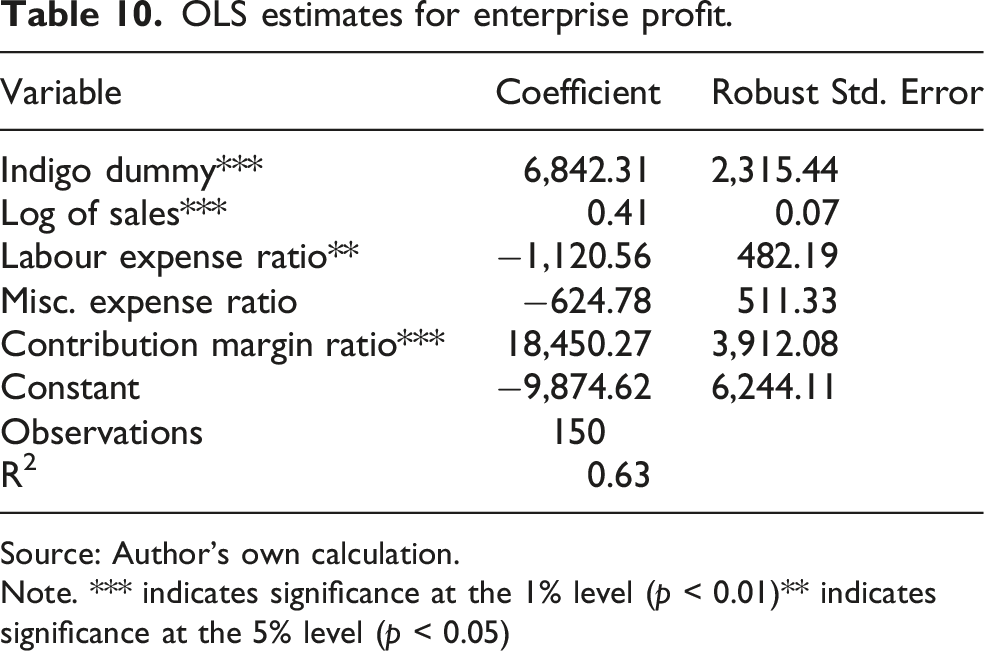

OLS estimates for enterprise profit.

Source: Author’s own calculation.

Note. *** indicates significance at the 1% level (p < 0.01)** indicates significance at the 5% level (p < 0.05)

Although heteroskedasticity is detected, OLS coefficient estimates remain unbiased and consistent; the use of heteroskedasticity-robust standard errors ensures valid statistical inference. The model demonstrates strong explanatory power, with an R2 of 0.63, indicating that nearly two-thirds of the variation in enterprise profits is accounted for by the included variables. The indigo dyeing dummy is positive and statistically significant, showing that indigo enterprises earn higher profits than lac enterprises, even after controlling for scale and cost intensity. The coefficient on log sales is positive and highly significant, confirming the presence of scale economies. The labour expense ratio exerts a negative and significant effect, suggesting that higher labour cost intensity reduces profitability. The contribution margin ratio emerges as the most influential determinant, with a large positive coefficient significant at the 1% level, underscoring the central role of variable cost efficiency in shaping enterprise profitability.

To control for scale bias, additional models are estimated with ratio-based dependent variables.

Each column reports results from a separate regression, estimated using the same sample but different dependent variables.

Results of ratio-based profitability and operating risk models.

Source: Author’s own calculation.

Notes: Robust standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.10.

GPR: Gross Profit Ratio; BEP: Break-Even Sales; MOSR: Margin of Safety Ratio.

In the table:

(1) = Regression Model 1: Dependent variable: Gross Profit Ratio (GPR)

(2) = Regression Model 2: Dependent variable: Break-Even Point (BEP).

(3) = Regression Model 3: Dependent variable: Margin of Safety Ratio (MOSR).

Interaction and Non-linear Effects models test mechanism heterogeneity and diminishing returns, so they are best shown as one compact table with two specifications.

Results of interaction and non-linear effects.

Notes: Robust standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.10.

Blank cells indicate that the corresponding variable is not included in that specific model specification.

Source: Author’s own calculation.

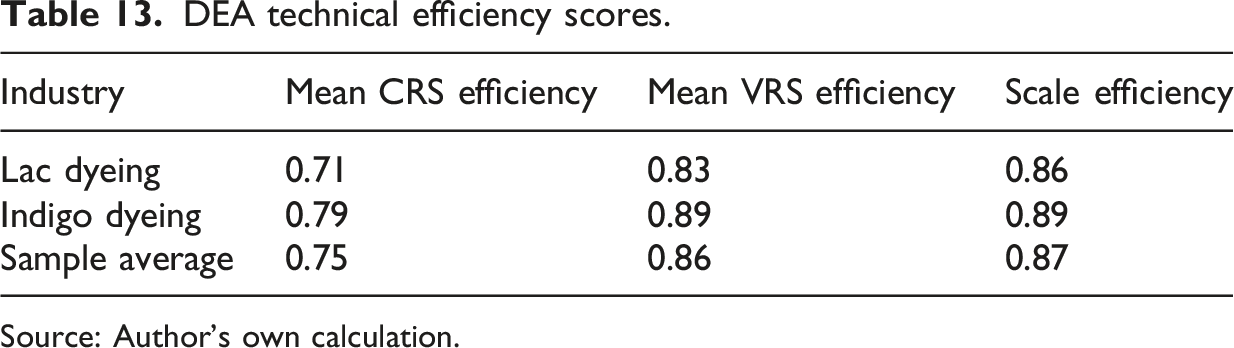

Technical and scale efficiency

DEA technical efficiency scores.

Source: Author’s own calculation.

The efficiency analysis indicates that indigo dyeing enterprises perform better than lac dyeing units under both constant and variable returns to scale, reflecting stronger technical efficiency and more effective utilization of resources. Scale efficiency is also comparatively higher for indigo enterprises, suggesting that they operate closer to the optimal scale of production. At the aggregate level, the sample shows moderate efficiency overall, with room for improvement in both technical and scale dimensions, particularly among lac dyeing enterprises.

Discussion

The combined evidence from regression and efficiency analyses offers a comprehensive perspective on the profitability dynamics of natural dyeing enterprises in Assam. OLS results highlight structural determinants of profitability, while DEA findings illuminate the efficiency with which enterprises deploy resources. This dual approach clarifies how technology, scale, and cost structures interact to shape performance. The convergence of results across profitability, risk-based, and interaction regressions strengthens confidence in the conclusions. Technology choice, contribution margin, and labour cost intensity consistently drive performance, while non-linear scale effects emphasize the importance of optimal enterprise size rather than unbounded expansion.

A key finding is the superior profitability of indigo dyeing enterprises compared to lac units. The positive and significant coefficient on the indigo dummy variable, reinforced by DEA results, shows that indigo units operate with higher technical and scale efficiency. This resonates with broader literature, where indigo has historically been associated with standardized processes, lower raw material costs, and stronger market demand. Chen and Chen, 67 for instance, demonstrated through a three-stage DEA analysis of Chinese textile firms that technological innovation efficiency enhances profitability, particularly when standardized processes and economies of scale are adopted. Similarly, studies of Vietnamese textile enterprises confirm that efficiency gains translate into financial outcomes when production aligns with global demand. 68

Profitability differentials between indigo and lac enterprises persist even after controlling for scale and cost intensity, suggesting intrinsic technological and market advantages for indigo. Rani 69 found that standardized dyeing processes yield better fastness properties and consumer acceptance, enhancing market viability. Indigo’s relatively standardized extraction and application methods confer a competitive edge over lac, which remains more artisanal and fragmented. 70

Sales volume also emerges as a strong determinant of profitability, underscoring the role of scale economies. Larger enterprises spread fixed costs and achieve better resource utilization, consistent with Wang et al., 71 who found that scale expansion improves efficiency and profitability in textile and garment enterprises. DEA clarifies that inefficiency under constant returns to scale is partly attributable to scale rather than technical shortcomings. Lac enterprises, in particular, exhibit lower scale efficiency, consistent with their tendency to operate below optimal size. This echoes studies emphasizing clustering and collective production as strategies to overcome diseconomies of small scale and enhance competitiveness.72,73

Labour cost intensity exerts a negative effect on profitability, reflecting the artisan-based production structure. This aligns with broader evidence where labour inefficiencies undermine profitability. Saravanan and Chandrasekar 74 highlighted that skill development and process standardization are essential for improving labour productivity. DEA results similarly imply that input optimization is critical for lac units, while indigo enterprises must manage labour cost sensitivity to sustain profitability. Contribution margin emerges as the most influential determinant, underscoring the central role of variable cost efficiency. Garrido Moreno et al. 75 likewise emphasized that enterprises optimizing variable costs through innovation are more resilient to market fluctuations.

Taken together, regression and DEA results confirm that efficiency improvements translate into tangible profitability gains. International evidence reinforces this: Chen and Chen 67 showed efficiency improvements enhance financial sustainability, while Wang et al. 71 linked DEA efficiency scores to profitability outcomes. The emphasis on scale, labour optimization, and cost efficiency resonates with sustainability discourses in textiles, where circular economy practices and resource efficiency are pathways to competitiveness. 74 In Assam, indigo units are better positioned to leverage technological and market advantages, while lac enterprises require targeted interventions to overcome scale inefficiencies and labour cost challenges. Policy support for clustering, collective production, and skill development could help lac units achieve greater efficiency, while managing labour costs and sustaining demand will be critical for indigo enterprises.

Economic viability in the context of Assam

The economic viability of natural dyeing enterprises examined in this study is intricately linked to the specific socio-economic and production structure of Assam. In contrast to industrial textile systems, these enterprises operate within a localized resource base, where essential inputs such as lac and indigo are either readily available locally or procured at relatively low cost. This substantially reduces variable cost components, as evidenced by the high contribution margin ratios reported in the empirical findings.

Another important aspect is the labour organization of these enterprises. Production primarily takes place within households, with a heavy dependence on family labour. Because family labour is often unpaid or valued at rates lower than the market, effective labour cost intensity remains low. This situation directly leads to higher gross profit ratios and stronger contribution margins, as confirmed by the regression results showing that labour cost intensity has a negatively effect on profitability, also consistent with findings that labour cost intensity significantly affects SME profitability. 58

In Assam, on the revenue side, natural dye-based textiles occupy niche market segments that value cultural authenticity and growing demand for environmentally sustainable products. These products often fetch higher price premiums compared to conventionally dyed textiles, enabling enterprises to sustain substantial mark-ups over their costs.33,34 This combination of low variable costs and favourable pricing conditions accounts for the consistently high gross profit ratios seen in both lac and indigo dyeing businesses.

The low break-even levels highlighted in the CVP analysis are largely due to the enterprises’ minimal fixed cost structure. These businesses typically require limited capital investment for production, relying on simple tools, traditional techniques, and household infrastructure. Consequently, fixed costs such as equipment and rent remain low, reducing the sales threshold required to cover total costs. This structural feature also explains the relatively high margins of safety, reflecting their ability to withstand changes in demand.

Moreover, the flexibility inherent in small-scale, household-based production systems enables enterprises to adjust their output and input usage according to market, thereby mitigating operational risk. Nonetheless, while these factors collectively explain the observed profitability and viability, it is crucial to recognize that such performance is contingent on the continued availability of low-cost inputs, stable niche demand, and the continuation of traditional labour arrangements. Consequently, the economic viability of natural dyeing enterprises in Assam is not solely determined by efficiency but is intricately linked to the region’s resource endowments, cultural economy, and production structure.

Thus, the observed profitability and resilience of natural dyeing enterprises are not generic outcomes but are rooted in Assam’s unique socio-economic and production structures, reinforcing the place-based relevance of our findings.

Conclusion

This study provides evidence that natural dye-based textile enterprises can be economically viable under favourable conditions, while also aligning with environmental sustainability goals. Profitability is driven by contribution margin, scale of operation, and technology type, while labour cost intensity exerts a negative influence. Indigo dyeing enterprises consistently outperform lac units in profitability and technical efficiency, reflecting technology-specific advantages such as lower raw material costs, standardized processes, and stronger market demand. Lac enterprises, however, display greater financial resilience due to higher margins of safety, highlighting a trade-off between efficiency and risk cushioning.

The integration of regression analysis, cost–volume–profit tools, and data envelopment analysis provides methodological strength. By jointly examining profitability, efficiency, and resilience, the research advances literature on traditional and sustainable textile enterprises. DEA results confirm that higher technical efficiency translates into superior profitability, while scale efficiency patterns explain why lac enterprises often operate below optimal size. This methodological contribution underscores the value of combining econometric and frontier approaches to capture both determinants and efficiency dimensions of enterprise performance.

Managerial implications are clear. Contribution margin emerges as the most influential determinant of profitability, emphasizing the need to prioritize variable cost control. Improved procurement, reduced material wastage, and adoption of standardized dye extraction and reuse practices can enhance profitability and resilience. Labour productivity is equally critical. Since profitability depends on efficient utilization rather than increased labour input, managers should invest in skill development, task specialization, and labour-saving but skill-intensive techniques. This is particularly important for indigo enterprises, which are more sensitive to labour cost escalation despite higher average profitability.

From a theoretical standpoint, the findings both align with and extend existing perspectives on the sustainability of small enterprises. The results provide credence to the sustainable livelihoods view that locally embedded, resource-based enterprises can generate viable and resilient income in rural contexts. At the same time, the study extends firm-level performance theory by showing that cost structure and contribution margins, rather than scale expansion, drive profitability in micro and artisanal settings. This suggests that conventional scale-centric interpretations of firm performance may be insufficient for explaining outcomes in household-based enterprises. Instead, a more context-sensitive framework that incorporates cost dynamics, efficiency considerations, and place-based production structures is required to better understand enterprise sustainability in such settings.

Policy implications follow directly. For lac enterprises, interventions should focus on scale expansion through cooperative production models, clustering, and shared infrastructure for dye extraction and processing. For indigo enterprises, sustaining efficiency while managing labour costs is essential. Governments and development agencies can support the sector by establishing common facility centres, promoting cluster-based marketing systems, and providing shared infrastructure for storage, quality control, and waste management. Skill development programs should emphasize advanced dyeing techniques, quality consistency, and process optimization, while financial support through subsidized credit, start-up grants, and working capital assistance can mitigate risk and facilitate growth. Overall, technological advantages, scale efficiency, and cost management practices shape profitability in natural dyeing enterprises. Evidence-based interventions that strengthen efficiency, optimize scale, and enhance cost structures can significantly improve sustainability within the studied context, contributing to environmental protection, rural employment, and inclusive development.

The findings provide evidence of economic viability among the sampled natural dye-based textile enterprises. However, this conclusion should be interpreted with appropriate caution, as the observed performance reflects conditions specific to the study context. In particular, factors such as market access, demand uncertainty, input availability, and scale constraints may influence enterprise performance and its sustainability over time.

Limitations and scope for future studies

While the results indicate favourable profitability, cost structures, and efficiency patterns, these outcomes are not necessarily uniform across all enterprises or stable under changing market conditions. Accordingly, the economic viability of natural dyeing enterprises should be understood as context-dependent rather than universal, and contingent on the continued alignment of production practices with market opportunities and resource availability. In addition to this, the study has identified a few limitations. First, the analysis is based on cross-sectional data, which limits the ability to draw causal inferences between key variables. In particular, the observed relationships between efficiency, cost structure, and profitability should be interpreted as associative rather than strictly causal. While the findings provide useful insights into enterprise performance, longitudinal data would be required to capture dynamic adjustments and establish causal relationships more rigorously. Second, DEA efficiency estimates are relative to the sample and may be influenced by extreme observations, affecting robustness. Third, although environmental sustainability motivates the study, the ecological benefits of natural dyeing are not explicitly quantified or monetized, leaving an important dimension unaddressed.

These limitations open avenues for future research. Longitudinal studies could examine how productivity and efficiency evolve, capturing resilience under changing market conditions. Integrating environmental cost–benefit analysis or life-cycle assessment with financial evaluation would allow for a more comprehensive appraisal of the dual economic and ecological contributions of natural dyeing enterprises. Comparative studies across regions or countries could further enrich understanding by highlighting contextual differences in technology adoption, market structures, and policy environments. Such extensions would strengthen the evidence base and enhance relevance for scaling natural dye-based enterprises in diverse settings.

Footnotes

Ethical considerations

The research follows the ethical guidelines of Sibsagar University.

Consent to participate

Informed consent was obtained.

Consent for publication

Informed consent was obtained.

Author contribution

The concept was developed by Morami Dutta. Analysis was carried out by Bidyutt Bikash Hazarika. Formatting and review were carried out by Mrinal Saikia. The results and discussion were contributed by all the authors. The final version was reviewed and approved by all the authors.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The authors decided not to share data publicly.