Abstract

Budget silos innate to hospital global funding schemes tend to inhibit the adoption of innovative clinical practices. In contrast, budget fluidity can encourage initiatives that align with the Quadruple Aim. This article calculated the budget impact of Surgical Aortic Valve Replacement (SAVR) and Transcatheter Valve Implant (TAVI) in high-risk aortic stenosis to demonstrate the value of a full-cost accounting approach. The budget impact of TAVI was $4,000 more than SAVR ($52,576 vs $48,578). However, the cost of managing SAVR adverse events was higher than TAVI ($17,718 vs. $11,754) over 1 year. A scenario analysis demonstrated that the total cost of care for a cohort of 100 patients at baseline ratio of 30% TAVI versus 70% SAVR was similar to a future scenario, with reverse proportions. While TAVI may seem expensive upfront, when considered as a surgical department budget item, the overall cost to the hospital is comparable to the SAVR.

Introduction

Rapid and continuous advances in medicine and technology have transformed the primary focus of the healthcare system from acute care to complex chronic disease management. 1 As a result, patient care often requires a multidisciplinary and interdepartmental approach. 2 Concurrently, continuous fiscal pressures on the healthcare system, especially in hospitals, require innovative program planning and implementation. 3 In this regard, hospital programs should have the option to re-examine department funding based on patient preferences and providers’ professional judgment to achieve optimized outcomes as opposed to historical trends.

In a patient-centric healthcare model, department funding can be linked to outcomes eminent to the total care cycle cost, including adverse event management. 4 One example of such an approach is the management of potential adverse events following surgical procedures, which may require a multidisciplinary intervention. 5 Consequently, optimizing therapeutic choices may necessitate inter- and intradepartmental budget transferability and the elimination of budget silos.

This article proposes a pragmatic approach through a budget impact analysis of therapeutic alternatives for the treatment of high-risk severe symptomatic Aortic Stenosis (AS) patients with Transcatheter Aortic Valve Implant (TAVI) and Surgical Aortic Valve Replacement (SAVR) for optimized service delivery. The goal of this analysis is to quantify the budget impact of the total cost of care for each procedure from a hospital perspective within 1 fiscal year. The hypothesis is that there is no significant budget difference between TAVI and SAVR for the hospital.

Clinical context

Aortic stenosis is a serious condition wherein the narrowed calcified aortic valve obstructs the left ventricular blood flow to the aorta, resulting in chronic heart failure and reduced quality of life. 6,7 This condition predominately affects the elderly individual, with the prevalence of the condition for people above the age of 75 being 3.4%. 7 Surgical aortic valve replacement, the conventional treatment of high-risk AS, is an open-heart procedure in which the aortic valve is surgically replaced. This procedure has a significant mortality risk (75.1% within 4 years). 8,9

Transcatheter valve implant is a minimally invasive alternative to open-heart surgery wherein a bio-prosthetic valve is implanted via a catheter. 10 Transcatheter valve implant was initially proposed for extreme-risk patients with AS, but recent clinical trials have shown TAVI benefits in high- and medium-risk patients. 11,12 Importantly, studies have demonstrated that patients prefer minimally invasive procedures that require a shorter hospital stay. 13 Furthermore, TAVI is associated with fewer serious adverse events than SAVR. 3 These events include life-threatening bleeding, atrial fibrillation, kidney injury, stroke, and death.

Methods

The author developed a budget impact model in the EXCEL spreadsheet (Microsoft Corp) to quantify the total cost associated with healthcare resource utilization for the treatment of patients with AS, including the surgical procedure itself and the subsequent management of potential adverse events and follow-up visits. The resources used for each procedure were defined by expert consult at an Ontario teaching hospital cardiology department, and the cost of the resources used was determined from the hospital coding department and manufacturers’ list price. The average cost of managing major adverse events was calculated by applying the probability of each adverse event and the 1-year cost associated with the resources used. The probability of adverse events was derived from published literature, and the cost of managing the adverse events in the first year was acquired from published literature and the Ontario Ministry of Health data portal. 14 A teaching hospital cardiac department expert validated the study assumptions. The average total cost of managing high-risk patients with AS in the first year was estimated by adding the procedural costs and costs associated with adverse event management.

Using a separate model developed in EXCEL spreadsheet, a scenario analysis was conducted to estimate the total cost of treating a hypothetical cohort of 100 high-risk patients with AS, with varying proportion of procedures, changing from a baseline of 30% TAVI versus 70% SAVR to a future state of 70% TAVI versus 30% SAVR. A one-way sensitivity analysis was used to examine the study results’ robustness.

Results

Table 1 summarizes and compares the procedure cost of TAVI and SAVR. The cost of the procedure for TAVI and SAVR was $52,576 and $48,578 per case, respectively (Δ = $3,998 in favour of SAVR). The average cost of managing adverse events in the first year for TAVI and SAVR was $11,754.22 and $17,718.21, respectively (Δ = $5,963.99 in favour of TAVI; Table 2). The total cost of care in the first year for TAVI and SAVR was $64,330 and $66,296, respectively (Δ = $1,966 marginal cost saving in favour of TAVI).

Comparison of costs associated with healthcare resource utilization for high-risk aortic stenosis treatments

Abbreviations: ICU, intensive care units; LOS, length of stay; OR, operating room; SAVR, surgical aortic valve replacement; TAVI, transcatheter aortic valve implantation.

a The costs are derived from manufacturer list price, hospital sources, and Ontario Health Insurance Policy schedule of fees.

Comparison of annual adverse events cost management in high-risk aortic stenosis

Abbreviations: OCCI, Ontario Case Costing Initiative; SAVR, surgical aortic valve replacement; TAVI, transcatheter aortic valve implantation.

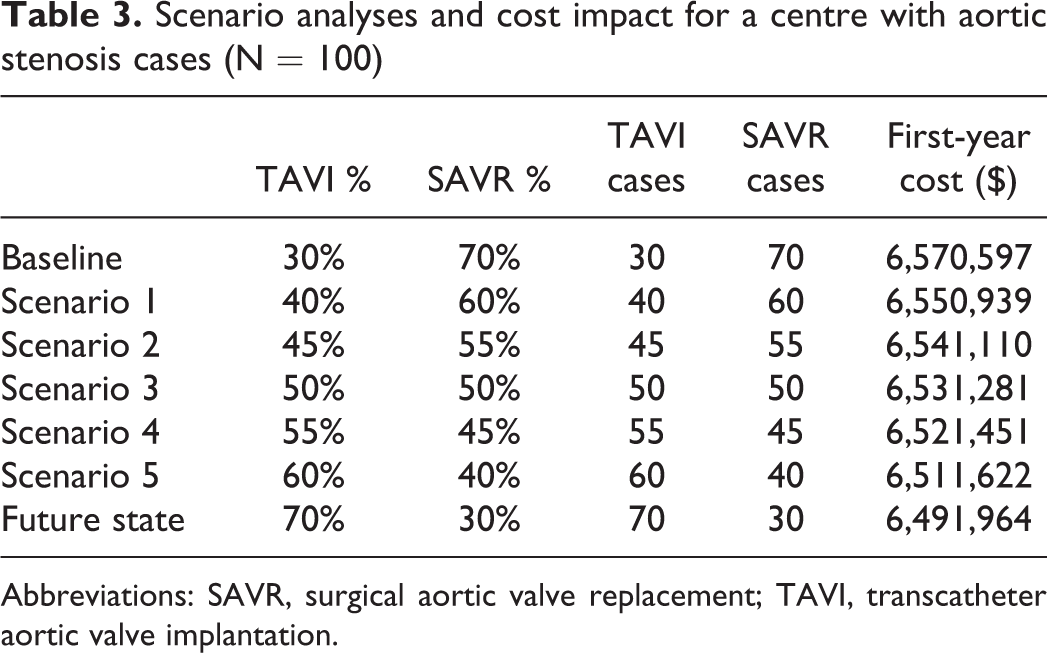

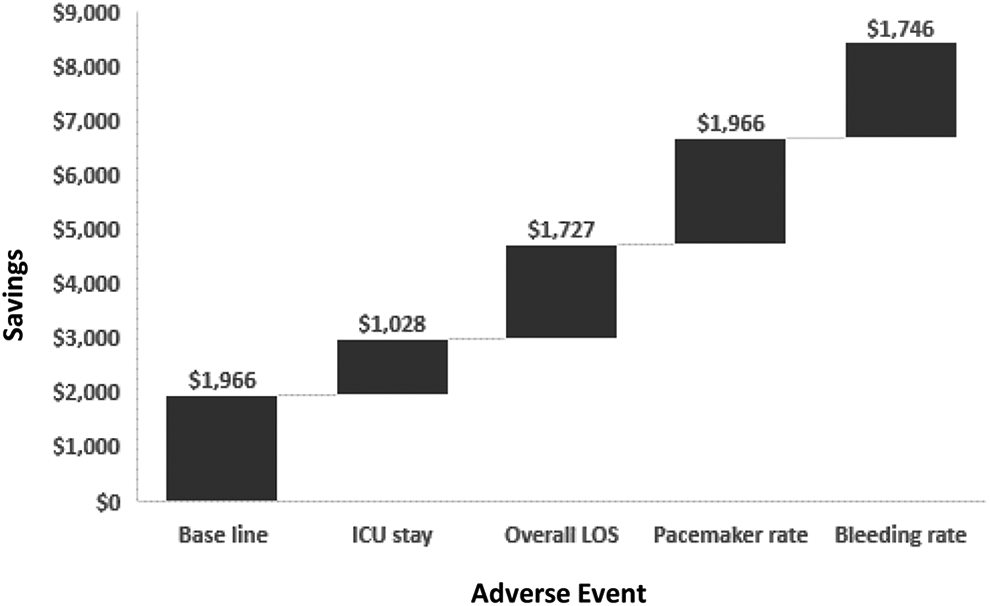

The scenario analysis demonstrated that increasing the proportion of TAVI to SAVR and reallocating the department budget from one procedure to others did not have a significant impact on overall hospital finances. The total first-year cost of TAVI versus SAVR at baseline scenario was $6,570,597, and the total cost of care for the future state scenario was $6,491,964, with a difference of 1.2% ($78,632) of baseline costs (Table 3). Figure 1 shows the result of the one-way sensitivity analysis (+20%) on major adverse event rates. The high-cost/high-rate adverse events had the most impact on the overall cost, including severe bleeding hospital length of stay, intensive care unit stays, and the pacemaker rate. However, in all instances, TAVI was cost saving.

Scenario analyses and cost impact for a centre with aortic stenosis cases (N = 100)

Abbreviations: SAVR, surgical aortic valve replacement; TAVI, transcatheter aortic valve implantation.

One way sensitivity analysis for main cost drivers.

Discussion

Canadian studies have established the cost-effectiveness of TAVI from a provincial healthcare system perspective, yet in many centres, TAVI is underused. 15 This analysis supports the hypothesis that increased use of TAVI versus SAVR does not have a significant impact on the hospital budget in Canada. Due to a lower valve cost, SAVR is deemed to be less expensive than TAVI. Nonetheless, the higher upfront cost of the transcatheter valve for TAVI is offset by the lower rate of major costly adverse events, with potentially marginal cost savings for the hospital. The results of this study are aligned with similar evaluations in the United States and New Zealand, where the cost of TAVI in high-risk patients with AS was comparable to SAVR. 16,17

Further, the ongoing discussions regarding the appropriation and optimization of healthcare resource utilization are often tackled by cutting services at a department or hospital level. This analysis illustrates the importance of breaking down the budget silos within the hospital, allowing for budget reallocation based on patient needs and professional judgment and considering the total cost of care. For example, budget and volume allocation for specific surgical processes (eg, TAVI versus SAVR) may create arbitrary wait times, sub-optimal clinical outcomes, and hinder delivering “value” to the patients and the healthcare system.

In a patient-centric healthcare system aligned with the Quadruple Aim model of care, funds should be allocated based on patient needs, considering the overall care pathways and evidence-based outcomes, as opposed to system needs and acute-phase considerations. Such budget reallocation alleviates the perpetual access constraints and improves the patient experience. Budget allocation is a delicate issue in hospitals. While managing hospital finances is critical in providing service, considerations should be made for optimal health outcomes and efficiencies in the system. Senior hospital management may consider co-designing programs to implement budget policies aligned with the Quadruple Aim. 8 The goal of achieving optimal care outcomes at reasonable and sustainable costs, with the flexibility for professional judgments, requires innovative thinking and change management. 18 This analysis demonstrates the advantage of using the total care cycle to determine the cost of care, which requires change management. Hospital leaders could adopt such an approach through interdepartmental consultation, stakeholder buy in, and increased patient engagement. It takes strong collaborative leadership to co-design a policy that permits the reallocation of resources and cross-department budgeting. Funding needs to balance patient preferences for best available care while considering the constraints in delivery.

This analysis is one example illustrating the benefits of adopting a new viewpoint on care delivery and budgets. At a broader system level, the sum of multiple opportunities can help optimize and prioritize care delivery based on outcomes and value to both patients and society as chronic illnesses have a more substantial impact beyond individual patients. This optimization cannot happen without buy in from all stakeholders in the system. Canadian hospitals and healthcare systems require team-building initiatives, a transparent co-design approach, and strong leadership and vision. Nonetheless, similar analysis and evidence may start a dialogue, especially where there is a worrying need within a fiscal discipline.

Limitations

This study used a hospital financial perspective, which is limited to 1 fiscal year, using Ontario information. This is an arbitrary but realistic viewpoint, as the out-of-date funding models used in the Canadian healthcare system are based on financial accountability and system-centric assessments. Using a broader healthcare system or social perspective further supports the findings. The use of this approach requires contextualization based on the healthcare system’s funding and fiscal accountability. Although the results of this study support the budget fluidity in one department, extending this concept to other departments requires further assessment. Budget allocations and service delivery would require a new level of collaboration among all healthcare system stakeholders from leadership down to frontline personnel.