Abstract

Pharmaceutical companies claim that they need high drug prices to generate sufficient profits to invest in innovation. While this claim can be valid in principle, it is contradicted by the extent to which “Big Pharma” companies in the United States (US) distribute profits to shareholders in the form of cash dividends and stock buybacks. For 2013-2022, the 14 US-based pharmaceutical companies in the S&P 500 Index paid out 54% of net income as dividends and another 51% as buybacks. Incentivizing senior corporate executives to allocate resources in this financialized manner is, as we document, their stock-based compensation. In effect, these companies use high stock prices to boost stock yields at the expense of investing in innovation and compensating workers and taxpayers who make value-creating contributions to the corporation. Given the prominence of US-based pharmaceutical corporations in Canada, we explain how their financialization results in high Canadian drug prices and underinvestment in pharmaceutical research and development in Canada.

The problematic argument for high drug prices

In 2019, patients in the United States (US) paid $1,126 USD per capita for prescription medicines. The average for 10 comparable high-income nations was $552 USD, with Germany second at $805 USD and Canada third at $737 USD. 1 Unlike other nations, drug prices in the United States are largely unregulated. While Canada regulates drug prices, they are still high relative to those of most other high-income companies, and the consequent profits largely benefit the foreign-based companies that dominate the Canadian pharmaceutical industry.

With a view to saving on Medicare costs, 13 states have established programs to import drugs from nations that regulate prices. 2 In early January 2024, for the first time, the US Food and Drug Administration (FDA) approved an application from a state’s Medicare program—in this case, Florida—to purchase its drug supply from Canada. The Canadian authorities have opposed the drug exports, arguing that they could create shortages in Canada.3,4

While Florida and several other states are looking to Canada for cost savings, the US Inflation Reduction Act (IRA) of 2022 permits, for the first time, Medicare (at the federal level) to negotiate the prices of 10 high-cost drugs with the pharmaceutical companies that produce them.5,6 In persistent and vigorous opposition to drug-price regulation has been the US industry lobby association, Pharmaceutical Research and Manufacturers of America (PhRMA), contending that government-imposed price caps will deprive member companies of the profits needed to augment and accelerate investment in drug innovation. 7

Underpinning the PhRMA argument is the assumption that the pharmaceutical companies systematically reinvest profits in productive capabilities that improve the development, manufacture, and delivery of drugs. This assumption is consistent with the “theory of innovative enterprise” which we use to analyze corporate resource allocation. 8 Negating this assumption in practice, however, is the fact that many US pharmaceutical executives allocate all or more of their corporate profits to massive distributions to shareholders in the form of cash dividends and stock buybacks.9,10 Instead of committing high profits from high drug prices to augment investment in drug innovation, many US-based pharmaceutical companies burden patients and taxpayers with costly medicines for the sake of distributions to shareholders to boost the yields on the companies’ publicly traded shares.

This “financialized” behaviour of US-based pharmaceutical companies has deleterious impacts on drug innovation and the cost of medicines not only in the United States but also in Canada. In 2022, 9 of the top 10 pharmaceutical companies by revenues in Canada were foreign-based (the one exception was Canada-based Apotex, a generic drug producer that is privately held). 11 Among the top 10 were 4 US-based companies: Johnson & Johnson (#1), Merck (#2), AbbVie (#4), and Pfizer (#7). These companies, on which Canada is dependent for business-sector investment in pharmaceutical Research and Development (R&D), have been in the forefront of distributing corporate cash to shareholders. In effect, the higher drug prices that Canadians pay compared with most other high-income nations enable foreign-based companies that operate in Canada to distribute more profits to shareholders as dividends and buybacks.

Massive distributions to shareholders by US-based pharmaceutical companies

The 478 corporations in the S&P 500 Index in September 2023 that were publicly traded from 2013 through 2022 distributed $6.4 trillion as stock buybacks during their 2013-2022 fiscal years, representing 57% of net income, and $4.5 trillion as cash dividends, an additional 40% of net income. Dividends are the traditional way of providing an income stream to shareholders for (as the name says) holding shares in a company. Most buybacks, however, reward sharesellers such as senior corporate executives and hedge-fund managers who are positioned to reap gains by timing the buying and selling of shares when a company repurchases shares on the open market. Indeed, the purpose of these buybacks is to give manipulative boosts to the company’s stock price. 12

Financial data, 2013-2022, and 2022 employment, for the 14 pharmaceutical companies in the S&P 500 Index, publicly listed for fiscal years 2013-2022.

Notes: IPO = initial public offering, REV = revenues, NI = net income, BB = stock buybacks, DV = dividends, R&D = research & development expenditures, EE = end-of-fiscal-year employment (in thousands); J&J is Johnson & Johnson; BMS is Bristol Myers Squibb; Baxter is Baxter International. The founding and IPO years listed for AbbVie are those of its predecessor company Abbott Laboratories; for BMS, the founding of Squibb and the IPO of Bristol Myers; and for Viatris, its predecessor company Mylan.

Sources: Calculations from data in company 10-K flings with the US Securities and Exchange Commission.

Executive stock-based pay incentivizes distributions to shareholders

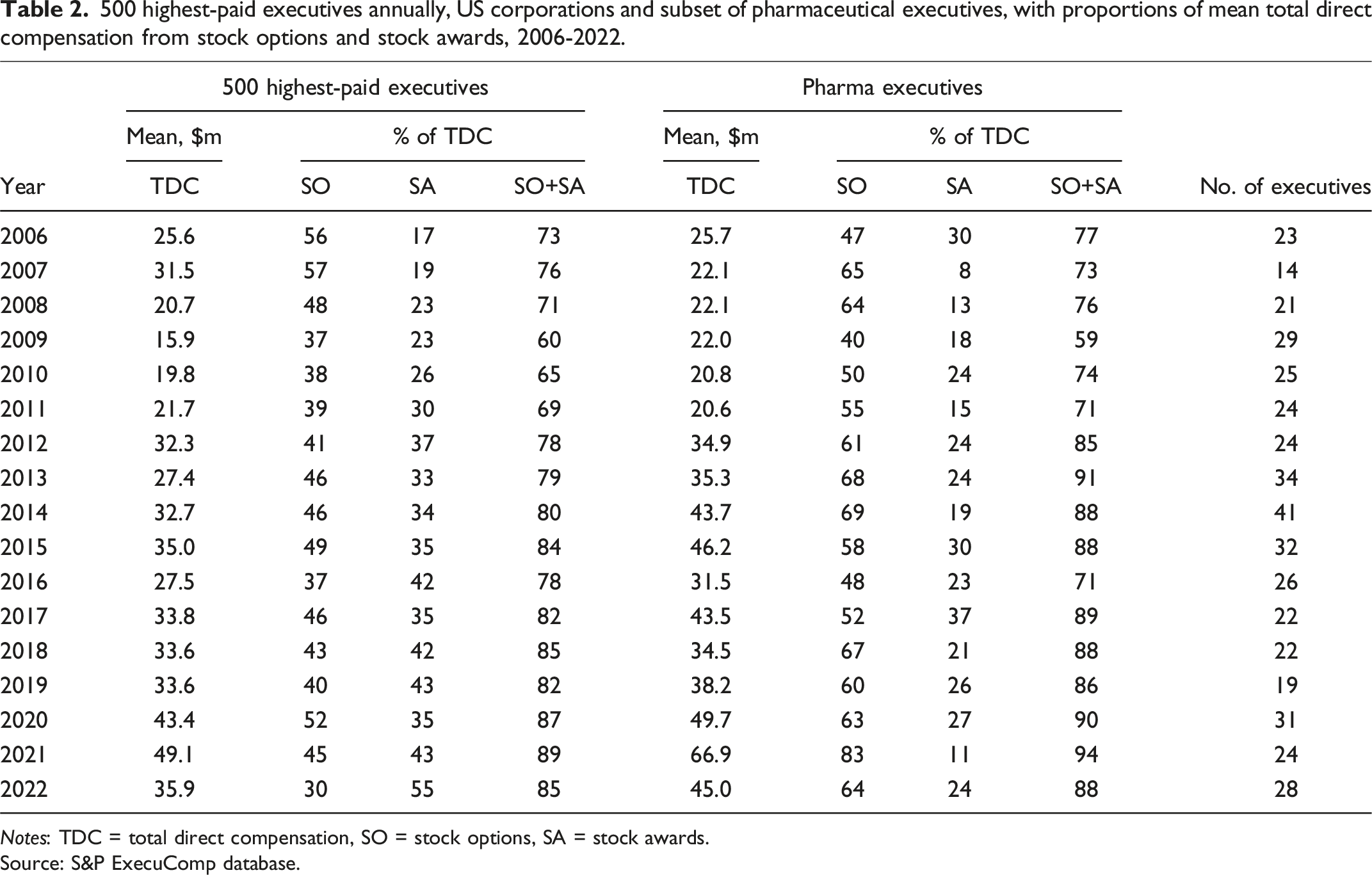

500 highest-paid executives annually, US corporations and subset of pharmaceutical executives, with proportions of mean total direct compensation from stock options and stock awards, 2006-2022.

Notes: TDC = total direct compensation, SO = stock options, SA = stock awards.

Source: S&P ExecuComp database.

From 2006 through 2022, the mean Total Direct Compensation (TDC) of the 500 highest-paid executives ranged from, with the stock market depressed, a low of $15.9 million in 2009, of which 60% were realized gains from stock-based pay, to, with the stock market booming during the SARS-CoV-2 pandemic, a high of $49.1 million in 2021, of which 89% were realized gains from stock-based pay. In 2021, when the mean TDC of the two comparison groups peaked, pharmaceutical executives’ mean TDC of $66.9 million (94% stock-based) was significantly higher than for all 500 highest-paid executives.

Distributions to shareholders in the form of dividends and buybacks inflate executives’ realized gains on stock-based pay. In the case of stock buybacks, not even the US Securities and Exchange Commission (SEC) knows the precise days on which buybacks as open-market repurchases are executed. 13 But the Chief Executive Officer (CEO) and Chief Financial Officer (CFO) of the repurchasing corporation possess this material insider information, and, moreover, they decide when to execute buybacks. The timing of buybacks can contribute to the gains that these executives realize in exercising stock options and the vesting of stock awards.14,15

Who invests in drug innovation?

Notwithstanding the fact that many long-established Big Pharma companies spend all or more of their profits on distributions to shareholders, and it could be argued that the promise of future dividends and buybacks has been needed to induce investment in the hundreds of start-up companies that since the late 1970s have become a characteristic feature of the US pharmaceutical industry. 16

There are problems with this argument. Younger companies such as Regeneron, Vertex, and Incyte, which appear in Table 1, have become large enough to be listed as constituent companies in the S&P 500 Index without doing large-scale distributions to shareholders. These “new economy” companies raise funds from the stock market when they do their Initial Public Offerings (IPOs), listing on the highly speculative NASDAQ exchange, as well as through subsequent secondary stock issues. These funds are forthcoming, however, even when the companies are productless, let alone profitless—as is typically the case with these IPOs—and do no distributions to shareholders. 16

Rather, the purchasers of shares in an IPO or secondary issue of a young pharmaceutical company seek to realize gains by selling their shares on the speculative market, while the issuer companies can use the funds raised on the stock market to finance development of revenue-generating products. Meanwhile, as data that we have collected shows, even in cases in which no revenue-generating drug is ever forthcoming, the founders and CEOs of these young companies typically become super-rich from their founder shares and stock-based pay just by getting the company to an IPO. 10

More generally, the prevailing notion that only shareholders invest in a company’s productive capabilities is a fiction propagated by “shareholder value” ideology. 17 Beyond the speculative primary and secondary stock issues by young companies, discussed above, common shareholders in publicly listed companies simply invest in shares outstanding on the market; they do not as a rule invest in the productive capabilities of the companies in which they hold shares. The actual investments in productive capabilities are made by taxpayers through government agencies—most notably in US pharmaceuticals by the National Institutes of Health (NIH)—and by employees through the application of their skills and efforts to the value-creating processes of developing, manufacturing, and delivering safe, effective, accessible, and affordable medicines.

The NIH’s 27 specialized institutes and centres had a 2023 budget of $48.4 billion. 18 From 1938 through 2023, the NIH spent about $1.6 trillion in 2023 dollars in support of life-sciences research. A study of 356 drugs approved by the FDA from 2010 to 2019 documents that “the NIH spent $1.44 billion per approval on basic or applied research for products with novel targets or $599 million per approval considering applications of basic research to multiple products.” 19 Besides its own internal research, NIH funding supports labs in universities and hospitals and makes it possible to attract to the United States talented people from around the world to engage in medical studies and scientific research.

The pharmaceutical industry has benefited from general patent laws, with an increase in 1995 to 20 years of protection against competition from the time of filing a successful patent from the 17 years that had prevailed from 1861 through 1994. The US Orphan Drug Act (ODA) of 1983 provides financial subsidies and market protection for pharmaceutical companies to develop drugs for rare and genetic diseases. From January 1, 1983 through May 28, 2024, there are 6,889 ODA designations and 1,235 ODA approvals. 20 ODA also offers R&D tax credits and FDA assistance in ensuring the rapid transformation of a promising compound into an approved marketable drug. Of great importance, ODA approvals provide 7-year marketing exclusivity for a specific indication from the date that it receives FDA approval for commercial use.16,21

Employees invest in a company’s innovative capabilities. An innovative company wants workers who apply their skills and efforts to organizational learning so that they can make enduring productive contributions—including those that will enable the development of the firm’s next generation of high-quality, low-cost products. In making these productive contributions, employees expect that they will be able to build their careers within the company, putting themselves in positions to reap future benefits at work and in retirement. Rather than distributing profits to shareholders—who in established publicly listed companies make no productive contribution at all—a pharmaceutical company that seeks to innovate must retain corporate profits, reinvest in the productive capabilities of its labour force, and reward its employees equitably.

When, under the IRA, Medicare negotiators confront the pharmaceutical companies, they will be told that ground zero is “value pricing”—the notion that the price of a medicine should be set so that the pharmaceutical company, by which they mean its shareholders, can capture the cost saving of the medicine to the US healthcare system; that is, the saving achieved by obviating the use of alternative high-cost therapies and procedures whose prices are also inflated by healthcare companies in the name of “maximizing shareholder value.” The fact that public shareholders make no contribution to value creation only accentuates the moral bankruptcy of the “value pricing” position. It is taxpayers and workers, not public shareholders, who invest in the productive capabilities that can provide society with safe, effective, accessible, and affordable medicines. Drug-price regulation should reward progressive value creation—and forbid predatory value extraction. 22

How stock buybacks by US-based pharmaceutical companies adversely affect Canadians

In certain industries, stock buybacks are a problem in Canada. For example, in 2022, among grocery chains, Loblaw did $1.2 billion CDN in buybacks, Metro $470 million CDN and Empire $248 million CDN—money that could have been used to continue the “hero pay” that the chains’ workers had received during the pandemic. 23 As a policy response, as of January 1, 2024, publicly listed corporations based in Canada must pay a 2% tax on their share repurchases. 24 This new law one-ups a 1% buybacks tax in the United States as part of the Inflation Reduction Act of 2022. 25 Neither levy will have a significant impact on reducing the allocation of corporate resources to manipulate stock prices.

We have already noted that Canadians, like Americans, could be paying less for prescription drugs if the pharmaceutical companies that dominate the Canadian market were placing less priority on reaping profits for the sake of distributions to shareholders. At the same time, as foreign-based corporations, these pharmaceutical companies tend to locate a disproportionate amount of their R&D spending in their home-base nations, which means that they place more pressure on their home-base governments to fund life-sciences research. This combination of greater business and government research means a nation such as the United States is far more successful than Canada in educating and attracting the global talent pool, including a brain drain from Canada to the United States, to engage in life-sciences research. 26

According to Research Canada’s web page, “Get the facts: Research in Canada is in trouble,” 27 the nation spends only 1.5% of its public health budget on research, compared with 5.9% in the United States. Whereas the US NIH spends $196.23 CDN per capita of the US population on research, the spending by the Canadian Institutes of Health Research (CIHR) was only $31.80 CDN per capita of the Canadian population. The underfunding of Canadian life-sciences research translates into a dearth of Canadian research personnel. The Research Canada web page cites a BioTalent Canada estimate that by 2029 the Canadian biotech industry will be short 65,000 workers.

These problems in pharmaceuticals echo a decades-long critique of the Canada’s innovation deficit inherent in its “branch plant” industrial economy. 28 Lee et al. recount how in 1987, the Canadian government granted Big Pharma companies operating in Canada extra patent protection against generics in exchange for a promise from the Pharmaceutical Manufacturers Association of Canada, later renamed Innovative Medicines Canada (IMC), that its member companies would spend at least 10% of their Canadian drug revenues on R&D in Canada 29 —a reasonable proportion given that, for example, the 14 US-based companies in Table 1 spent 19% of their global revenues on R&D in 2013-2022.

IMC lived up to this accord until 2002, but subsequently fell short. In 2019, member companies spent only 3.9% of their revenues on Canadian R&D, a deteriorating situation. 29 Lee et al. propose that the shortfall from the 10% target—which amounted to $7 billion CDN from 2010 to 2020—should be paid into an independent biomedical research trust fund in Canada. In response to IMC’s inevitable complaint that, to increase R&D spending, its members will need higher drug prices, the Canadian authorities should demand that these corporations generate the requisite cash flow by reducing their distributions to shareholders in the form of dividends and buybacks.12,17,30

Canadian regulators can figure out precisely how to implement policies that require foreign-based pharmaceutical corporations to make broader and deeper R&D investments in Canada. In pursuit of this objective, however, Canada’s hand would be significantly strengthened by explicitly confronting the highly damaging ideology that, for the sake of economic efficiency, a company should be run to “maximize shareholder value.” 17 The body of research that underpins the facts and logic summarized in this article supports our contention that the health of Canada’s life-science knowledge base requires eradication of the American corporate-governance disease.9,10,21,22,25,31

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge funding from the Institute for New Economic Thinking (INET) and the Canadian Institute for Advanced Research Program on Innovation, Equity & the Future of Prosperity (CIFAR IEP). This draft reflects comments from the CIFAR IEP working group at its meetings on November 4, 2023 and May 18, 2024 as well as detailed comments from IEP program leader Dan Breznitz.

Ethical approval

Institutional Review Board approval was not required.

Authors' note

All the information, with notes and sources, is in Table 1.