Abstract

Prior research examining how macro-level factors contribute to aggregate rates of intimate partner violence (IPV) across neighborhoods has focused almost exclusively on economic disadvantage or residential instability. Fewer studies have assessed what structural factors might ameliorate rates of domestic violence, such as economic investment. Housing investment improves communities by increasing the number of homeowners, who tend to be more committed to the neighborhood and more likely to develop strong social ties with other residents. The benefits of strong socially connected communities should extend to IPV victims, as studies have shown that female IPV victims tend to be less connected with their social environment and live in less supportive communities. This study examines the influence of external economic investment through home mortgage loans on the number of IPV incidents in a neighborhood and whether an influx of investment mitigates the negative effects of structural conditions on IPV. We examine these issues using panel data on home loan investment among neighborhoods in Cleveland, Ohio, between 1995 and 2010 to predict female and male domestic assault victimization rates. We find that the number of home purchase loans in a neighborhood has no appreciable impact on the level of IPV incidents, but as the average dollar amount of investment increases, the number of IPV incidents significantly decreases. This relationship is moderated by the neighborhood level of disadvantage: in highly disadvantaged neighborhoods, even low average dollar amounts contribute to a reduction in the number of female victims of domestic assault, but the same relationship is not apparent for male victims or in low disadvantaged neighborhoods. Our findings suggest that investment is important for disrupting the relationship between neighborhood structure and IPV, and implementing place-based strategies to encourage homeownership, particularly in disadvantaged neighborhoods, will be especially impactful.

Keywords

Introduction

Research suggests that violent victimization can be explained by neighborhood characteristics (Browning et al., 2004; Powers et al., 2018). Certain neighborhood factors such as residential instability and poverty weaken residents’ social ties and the informal social control that regulates crime and victimization. An increasing body of research has also connected neighborhood context to intimate partner violence (IPV) specifically, finding that factors such as disadvantage (Benson et al., 2003, 2004; Van Wyk et al., 2003), resource deprivation, (Miles-Doan, 1998), and foreclosures (Wallace et al., 2018) are linked to increased IPV. Current neighborhood-level IPV research, however, has largely focused on aggravating factors associated with higher rates of IPV; less attention has been focused on mitigating factors that may ameliorate the influence of structure on victimization. One factor that is particularly advantageous for neighborhoods in terms of crime reduction is economic investment: an influx of residential mortgage loans diminishes the negative effects of neighborhood characteristics on crime (Saporu et al., 2011; Vélez et al., 2012; Vélez & Richardson, 2011). Yet, the relationship between housing investment and IPV is relatively unexplored.

Housing investment brings needed resources to neighborhoods that can combat crime and victimization. More loans mean more homeowners, who tend to be more committed to the neighborhood, participate more in community organizations, and are more likely to develop strong social ties with other residents. Homeowners are also more likely to reside in neighborhoods for longer periods of time (Dietz & Haurin, 2003; Rohe & Stegman, 1994), which can increase and strengthen residents’ social connections. The benefits of strong socially connected communities may be especially important for IPV (Burke et al., 2006); studies have shown that female IPV victims tend to be less connected with their social environment and live in less-supportive communities (Jasinski & Williams, 1998; Katerndahl et al., 2013). These effects may be compounded in disadvantaged neighborhoods (Van Wyk et al., 2003). The increased economic resources in a neighborhood associated with investment may also improve the accessibility of critical services, such as legal aid or shelters (Parker & Hefner, 2015) and may help residents leverage political capital for improved local services such as better police coverage (Logan & Molotch, 2007; Vélez & Richardson, 2011). This suggests that home loan investment may influence neighborhood connectedness and resources in ways that would protect victims from domestic violence.

This study builds on the growing body of work that assesses neighborhood factors and IPV (Pinchevsky & Wright, 2012; VanderEnde et al., 2012; Voith, 2019) by examining the role that economic investment vis-à-vis mortgage loans may play in reducing neighborhood rates of IPV. Given that prior research has shown that neighborhood structure may have differential effects on female versus male victims (Cunradi et al., 2000; McKinney et al., 2012), we disaggregate rates of IPV across female and male victims. To investigate these relationships, we draw upon a unique data set that combines annual information on neighborhood investment and domestic assault victimization by sex over a 15-year period (1995 to 2010) in Cleveland, Ohio. By incorporating time-varying neighborhood characteristics for both investment and victimization by sex, we account for the changing nature of investment over time and how these changes might influence IPV outcomes.

Literature Review

Neighborhood Disadvantage and IPV

A long-standing body of criminological research has shown that neighborhood conditions can facilitate or prevent crime (Bursik & Grasmick, 1993; Chamberlain & Hipp, 2015; Sampson et al., 1997). Within a social disorganization framework, neighborhoods characterized by greater levels of poverty, racial and ethnic heterogeneity, residential mobility, and female-headed families have higher crime rates because these factors inhibit resident interaction and the formation of social ties (Kornhauser, 1978). These social ties are the foundation for establishing neighborhood cultural norms and informal social control that are needed to regulate criminal behavior (Bursik & Grasmick, 1993). Neighborhoods without such strong social connections or those that lack collective efficacy—the willingness of residents to intervene on another’s behalf—are less capable of preventing crime (Rountree & Warner, 1999; Sampson et al., 1997).

Neighborhood factors are also related to IPV specifically, especially economic disadvantage (Benson et al., 2003, 2004; Browning, 2002; DeMaris et al., 2003; Miles-Doan, 1998; Pinchevsky & Wright, 2012; Wright & Benson, 2010, 2011). Disadvantage can create stress between couples or within families that can exacerbate IPV, and the distrust in police that is often associated with disadvantaged communities may decrease the likelihood of reporting (Pinchevsky & Wright, 2012; Sampson & Bartusch, 1998). Furthermore, weaker social connections in disadvantaged neighborhoods means that residents may be unaware of IPV occurring among their neighbors (Wright & Benson, 2011) and that they will be less likely to intervene in domestic incidents (Browning, 2002; Wright & Benson, 2011; Wright & Skubak Tillyer, 2017). Residents in disadvantaged neighborhoods also tend to be more socially isolated (DeMaris et al., 2003; Tigges et al., 1998), a common factor among those experiencing IPV (Jasinski & Williams, 1998). For residents undergoing IPV, accessing social support and resources to address and escape IPV is largely dependent on these networks (Van Wyk et al., 2003). These ties are especially important for women, particularly those in disadvantaged neighborhoods, who are more likely to rely on social support as a response to victimization (Baumgartner, 1993; Wright, 2012).

Investment and IPV

Investment through home mortgage lending can increase neighborhood factors associated with stronger social ties. Research has shown that investment into neighborhoods reduces crime, especially in disadvantaged (Ramey & Shrider, 2014; Vélez, 2001) or predominantly non-White neighborhoods (Saporu et al., 2011; Squires & Kubrin, 2006). More home loans in a neighborhood translate into more homeowners, who play a significant role in the formation of social ties. Homeowners are more committed to the neighborhood in ways that promote informal social control, such as increased social and political engagement (McCabe, 2013), and seeking out community groups that can aid in resolving neighborhood problems (Rohe & Stegman, 1994). This engagement among homeowners likely reduces social isolation that is associated with IPV and increases the likelihood that residents would be aware of and intervene in violent acts against intimates (Browning, 2002; Wright & Benson, 2011) despite the fact that IPV is considered a “non-intervention norm” (Browning, 2002, p. 848).

Homeowners also tend to live in the neighborhood longer than renters (Dietz & Haurin, 2003; Rohe & Stewart, 1996), which reduces residential turnover. This is important for the development of social ties, as the in-and-out movement of residents can sever social networks and weaken informal social control. While results of studies linking residential instability to IPV are mixed (Benson et al., 2003; Lauritsen & Schaum, 2004; Wright & Benson, 2010), research has shown that the longer the residents remain in a neighborhood, the stronger and denser the ties become (Mesch & Manor, 1998; Taylor et al., 1984). Strong ties can facilitate the transmission of social norms against IPV (Browning, 2002; Wright & Benson, 2011). Neighborhoods in which ties are weak or that are more accepting of family violence or violence against women tend to have higher rates of IPV (Browning, 2002; Koenig et al., 2006; Wright & Benson, 2010). For example, Browning (2002) showed that the relationship between disadvantage and IPV is conditioned on the neighborhood level of tolerance for violence against women, and Koenig and colleagues (2006) determined that community attitudes tolerant of violence against wives are the strongest predictors of IPV.

Importantly, economic investment in neighborhoods helps shape the trajectory of a neighborhood: more investment in a neighborhood signals an expectation that neighborhood conditions, including housing prices or levels of crime and disorder, are moving in a positive direction. Improvements such as a reduction in physical disorder and higher housing values have been linked to reduced crime (Boggess et al., 2013; Vélez, 2009). Physical disorder is also associated with IPV (Kirst et al., 2015). Abandoned or vacant housing and run-down buildings can increase the neighborhood-level risk for IPV (Gracia et al., 2015), and residents associate these factors with violence generally and IPV specifically (Yonas et al., 2011). However, homeowners’ concern for their property values may increase their involvement in the community, particularly with regard to reducing disorder and contacting local officials for code violations or crime concerns (O’Brien, 2016). As neighborhoods become more attractive, investment can impact the economic development of a neighborhood, including employment opportunities, business development, and the presence of local institutions (Peterson & Krivo, 2010; Squires & Kubrin, 2006; Vélez, 2001) all of which may improve the amount and quality of resources in a neighborhood. Importantly, this may also increase the resources available for domestic violence victims, such as shelters or legal aid, which are typically are less prevalent in socially disorganized neighborhoods (Bent-Goodley, 2005).

Sex-Specific IPV Victimizations

The benefits of strong social organization may have differential effects on male versus female victimization. Women may be particularly susceptible to intimate partner victimization in disadvantaged neighborhoods. For example, collective efficacy has been shown to protect male but not female victims (Jain et al., 2010). Women may be perceived as more attractive targets because their disadvantaged status limits access to economic, political, or occupational advantages that may reduce victimization (Fox et al., 2002). This may be especially true for women in traditional roles who have fewer resources and are more socially isolated than women who work outside of the home (Vieraitis & Williams, 2002). Studies show that as women are more economically dependent on men (Yount, 2005) or when men dominate family life (Kruttschnitt, 1993), IPV is more likely to occur. Through qualitative interviews, Yonas and colleagues (2011) found that residents associated male neighborhood unemployment with IPV against women: status differentials between partners (i.e., women with better jobs or higher salaries) are likely drivers of male-perpetrated IPV against women. Similarly, male victims of IPV may be more reluctant to report victimization to the police or seek help from social networks because victimization is seen as antithetical to norms of masculinity (Machado et al., 2016), especially in disadvantaged neighborhoods (Anderson, 1999).

Data

To investigate the relationship between economic investment and intimate partner victimization, we use panel data from Cleveland, Ohio, between 1995 and 2010. 1 The investment data come from the Federal Financial Institutions Examination Council (FFIEC) via the Home Mortgage Disclosure Act (HMDA) and were obtained from the Center on Urban Poverty and Community Development’s Northeast Ohio Community and Neighborhood Data for Organizing (Center on Urban Poverty and Community Development, n.d.). HMDA requires financial institutions to disclose applications and originations for home loans annually. These data include information on the dollar amount and number of loans applied for, denied, and originated by Census tract—our proxy for neighborhood. The victimization data include all incidents reported to the Cleveland Police Department (CPD) and was also obtained from the Center on Urban Poverty and Community Development. The victimization data were initially reported by block group, but were aggregated to Census tracts to match the HMDA data. Data on neighborhood characteristics are from the 1990 and 2000 U.S. Census Summary File 3, and data for 2010 is from the American Community Survey 5-year estimates. All data were combined using the unique Federal Information Processing Standards (FIPS) code designation provided by the U.S. Census. Given that tract boundaries can change at different Census years, data were harmonized to 2000 Census tract boundaries to facilitate analysis using population-weighted apportionment in ArcGIS 10.2. To obtain intercensal year estimates, a linear interpolation was conducted so that each tract has unique neighborhood values for each year of analysis. There were 225 Census tracts in Cleveland, Ohio, in 2000, but we excluded 12 tracts for incomplete victimization or housing data; 213 census tracts are included in the final models.

Dependent Variables

Our outcome variable is the number of domestic assault victimizations per tract. We focus on domestic assaults specifically because they are the most severe nonlethal form of interpersonal violence, and women may be particularly vulnerable to assault in intimate relationships (Yllo & Straus, 2017). 2 In Ohio, assaults are classified as domestic violence when an assault or attempted assault is directed toward a family or household member, including former family or household members (Cuyahoga Domestic Relations Court, 2019). In our data, the CPD identified crime events as a domestic assault (i.e., IPV) at the time the incident was recorded. 3 Although IPV incidents may be underreported, we rely on police data because it is the most readily accessible and reliable data on domestic incidents over time; focusing on a severe form of violence increases the likelihood that the incident will be reported to the police. Based on these data, we create three variables capturing the total number of domestic assault victimizations, as well the total numbers of male victimizations and female victimizations. On average, there were 29.2 domestic violence incidents reported to the police each year by census tract. Over the study period, the number of IPV incidents decreased: the average number of domestic assaults peaked in 1997 at 34.63 and then generally declined through the 2000s, with a low of 21.36 incidents in 2008. By sex, there averaged 4.39 domestic assaults against male victims, ranging from a high of 5.11 in 2001 to a low of 3.06 in 2008, and 24.64 domestic assaults against female victims, ranging from 29.20 in 1997 to 18.20 in 2008, a statistically significant difference between groups. 4

Investment Variables

Prior studies have shown that both the dollar amount and number of mortgage loans are associated with lower crime rates over time (Peterson & Krivo, 2010; Saporu et al., 2011; Squires & Kubrin, 2006; Vélez et al., 2012). Therefore, we include two indicators of external mortgage investment into neighborhoods: the rate of home purchase loans originated (i.e., approved by the bank/lender and accepted by the applicant) and the average dollar amount of originated loans. The rate of home purchase loans originated is calculated as the number of loans originated in a tract per 1,000 owner-occupied housing units. This measure captures how many home purchase loans are going into a neighborhood relative to how many housing units are in the neighborhood. Loans for refinancing, home improvement, and purchases of multifamily properties are excluded. The average home purchase loan dollar amount captures how much money, on average, is being invested in home purchases each year and is measured as the total dollar amount of home purchase loans that are originated divided by the total number of home purchase loans originated in a tract. 5 On average, a neighborhood had 24 home purchase loans originated per 1,000 housing units and an average loan amount of $70,262. Over the study period, Cleveland’s population decreased from approximately 500,000 residents in the 1990s to around 395,000 in 2010. This resulted in downward pressure on home values, directly impacting mortgage loan amounts: adjusting for inflation, the average home loan in Cleveland in 1995 was $68,642 in 2010 dollars, which increased to $79,364 in 2000 before declining to $57,475 in 2010. 6

Neighborhood Characteristics

We include a number of neighborhood-level variables to account for characteristics associated with crime and victimization (Powers et al., 2018; Wright & Benson, 2011). To account for disadvantage, we used principle components factor analysis of three measures: (a) the percent of residents below poverty, (b) percent unemployed residents, and (c) average income (reverse-coded). Higher values represent greater disadvantage. To account for residential stability, we factored (a) the average length of residence, (b) the percent of households that moved into their residence recently, and (c) the percent of homeowners in the neighborhood. Higher values indicate greater stability. We include the percent vacant housing units as a proxy for potentially available housing. In addition, prior research has shown that the impact of investment on crime can vary by neighborhood racial or ethnic composition (Saporu et al., 2011). Therefore, we control for the racial composition of the neighborhood by including the percent Black residents and the percent Latino residents. We also include a measure of the percent female-headed households with children because prior research has found this to be a consistent and strong predictor of violence (Lauritsen & Schaum, 2004; Lauritsen & White, 2001; Pinchevsky & Wright, 2012). Finally, because our panel data cover the years of the housing market crash in the mid-2000s, we include a binary variable indicating the crash years (2006–2008) (Wallace et al., 2018).

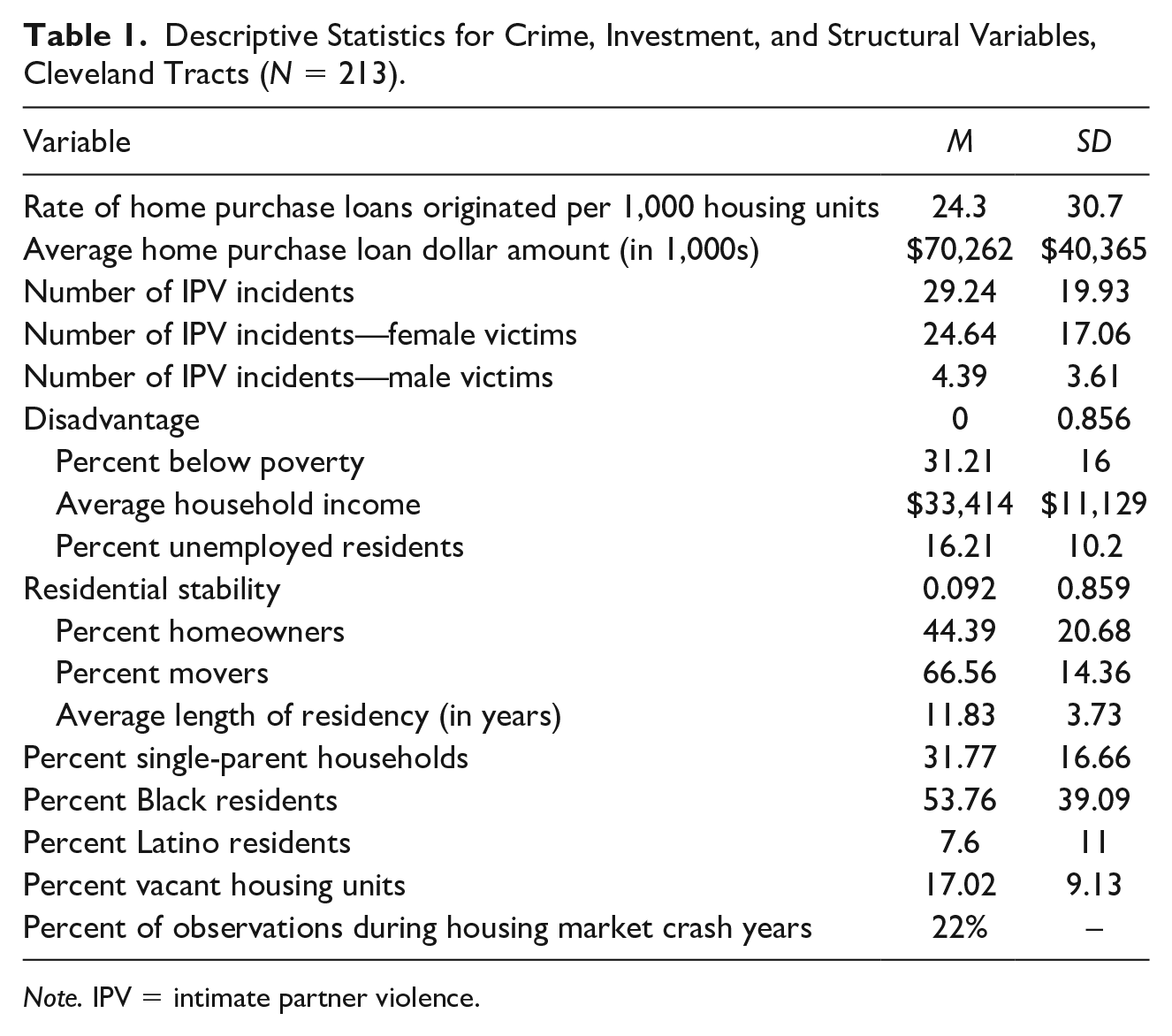

Summary statistics for all variables used in the models are shown in Table 1.

Descriptive Statistics for Crime, Investment, and Structural Variables, Cleveland Tracts (N = 213).

Note. IPV = intimate partner violence.

Methods

To assess the impact of home investment on IPV between 1995 and 2010, we use time-series Poisson models with fixed effects (conditional maximum likelihood) and robust standard errors (xtpoisson in Stata). Poisson regression models are used when the outcome variable is a count, and time-series models account for the dependence among the observations inherent in repeated variable measures over time. We use fixed effects to measure changes within a neighborhood over time but hold (unobserved) changes between neighborhoods constant (Allison, 2009). 7 To correct for potential overdispersion in the data, we use robust standard errors (Allison, 2009). 8 To ensure the proper temporal sequencing of these relationships, we use 1-year-lagged measures of all our independent variables and a count of the number of IPV incidents in the prior year. We include an exposure variable of the total neighborhood population with a coefficient constrained to 1 to account for variation in the population at risk of victimization. We did not identify any multicollinearity in the models; all variance inflation factor (VIF) scores are below 4. We first run the analyses for all IPV victims and then run separate models examining the differential effects on female versus male victims. We also test a series of multiplicative interactions. First, we test whether the effects of disadvantage on IPV are moderated by investment. Second, whether the combined effect of investment and stability is consequential for IPV.

Results

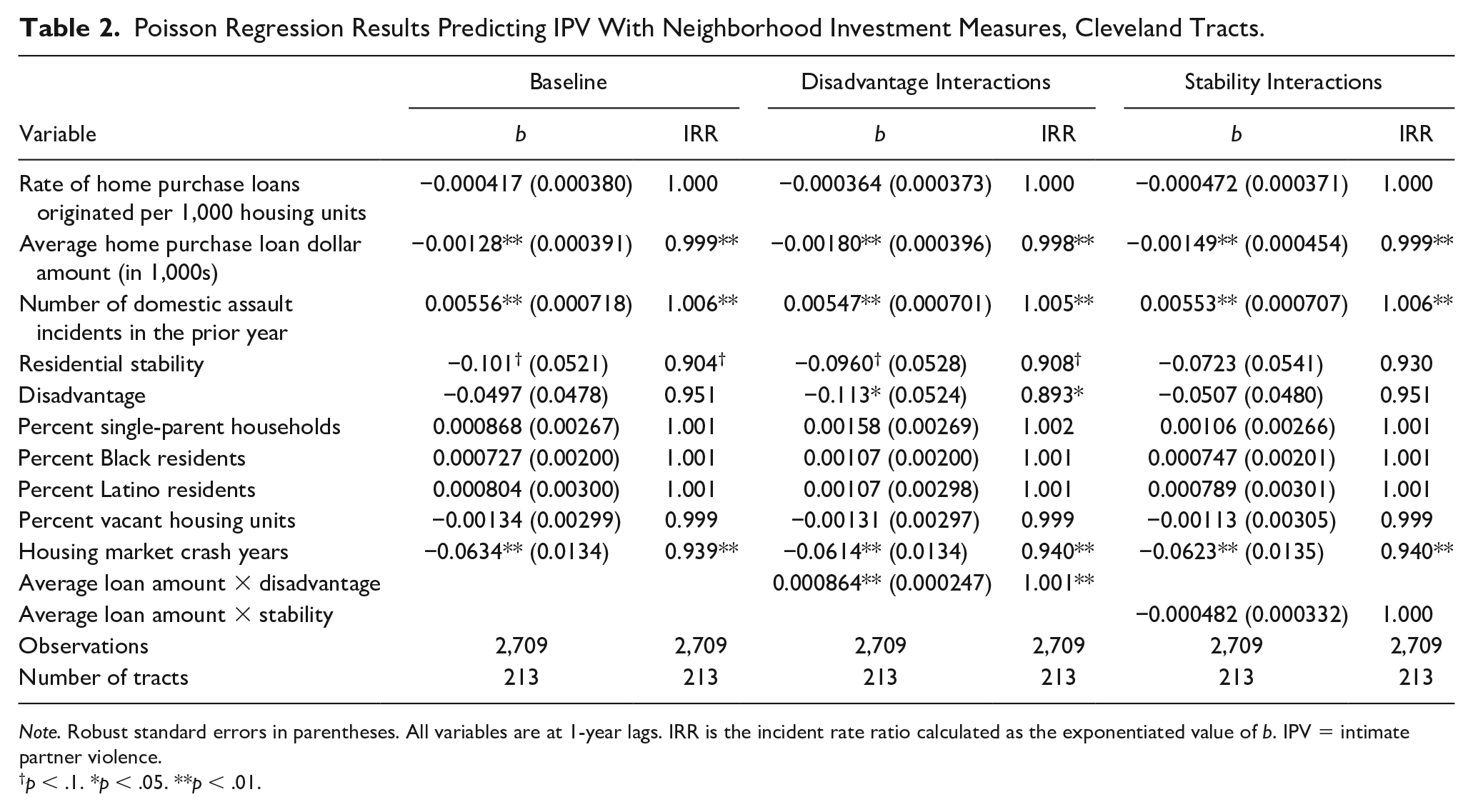

Table 2 shows the results examining the relationship between investment and neighborhood structure on rates of IPV without disaggregating victim sex. Model 1 presents the baseline models without the interaction terms. We find that the number of loans originated (per 1,000 housing units) in a neighborhood in the previous year has no appreciable effect on domestic assaults. However, the average dollar amount of loans originated in a neighborhood is a significant predictor of IPV (b = −0.00128, incident rate ratio (IRR) = 0.99, p < .01). For every additional $1,000, there is a 1.28 decrease in the number of IPV assaults. Few other structural variables are associated with IPV incidents. We find that residential stability is a negative predictor of IPV (b = −0.120, IRR = 0.904, p < .10), suggesting that more stable neighborhoods may have a greater capacity to exert informal social control. However, this finding is only marginally significant. The racial composition of a neighborhood, the percent of single-parent households, disadvantage, and the percent vacant homes are not significant predictors of IPV. Finally, IPV is significantly lower during the years of the housing market crash (b = −0.063, IRR = 0.939, p <.01) and neighborhoods with a greater number of IPV incidents in the prior year saw more incidents in the following year (b = 0.0056, IRR = 1.006, p < .01).

Poisson Regression Results Predicting IPV With Neighborhood Investment Measures, Cleveland Tracts.

Note. Robust standard errors in parentheses. All variables are at 1-year lags. IRR is the incident rate ratio calculated as the exponentiated value of b. IPV = intimate partner violence.

p < .1. *p < .05. **p < .01.

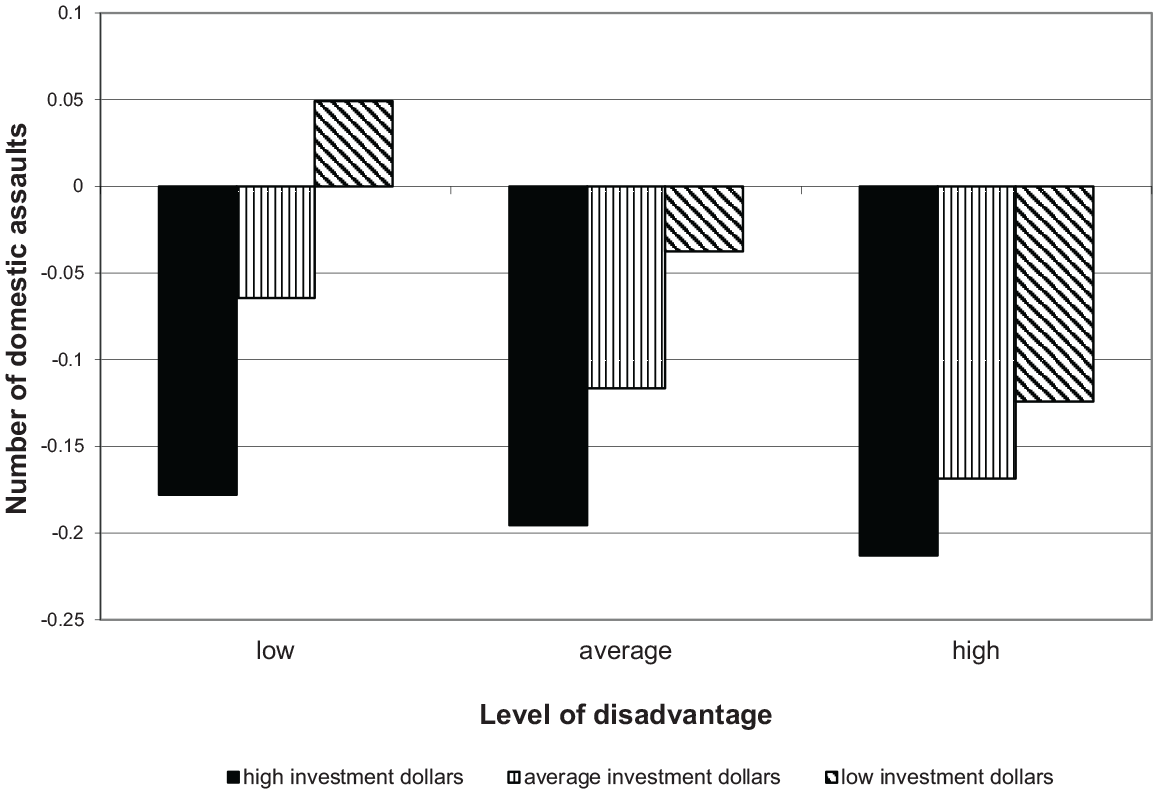

Next, we examine whether the effects of investment dollars on IPV are conditional on neighborhood structural characteristics by including our multiplicative interaction terms with disadvantage (Model 2) and residential stability (Model 3). In Model 2, we find a similar pattern in terms of investment and IPV: there is no significant relationship with the rate of home loans in a neighborhood, but a higher average loan dollar amount is related to fewer IPV incidents (b = −0.0018, IRR = 0.998, p < .01). This latter relationship, however, is moderated by the neighborhood level of disadvantage (b = 0.0009, IRR = 1.001, p < .01). Furthermore, the main effect for disadvantage becomes significant and negative in Model 2 when the interaction term is included. To more easily interpret this relationship, we graph the results in Figure 1. The x-axis represents neighborhood disadvantage at high (one standard deviation above the mean), average (mean), and low (one standard deviation below the mean) levels. Levels of average investment (in dollars) are categorized in a similar manner: The solid bars represent high investment (one standard deviation above the mean), the vertical striped bars represent average investment (mean), and the diagonal striped bars represent low investment (one standard deviation below the mean).

Effect of interaction of investment dollars and disadvantage on IPV.

Two primary conclusions can be made from Figure 1. First, high (solid bars) and average (vertical striped bars) investment dollars reduce IPV in all types of neighborhoods, with the greatest effects being in the most disadvantaged neighborhoods (far right). Second, even low or average investment dollars reduce IPV in neighborhoods with average or high levels of disadvantage, and again the greatest impact on IPV is in neighborhoods with the highest levels of disadvantage. This suggests that even modest amounts of economic investment are beneficial for IPV reduction in the most disadvantaged neighborhoods, a finding in line with research that shows investment has the most meaningful negative impact on crime in disadvantaged areas (Ramey & Shrider, 2014; Vélez, 2001). Notably, low average investment dollars into low disadvantage neighborhoods is actually associated with a slight increase in IPV incidents.

Model 3 presents the findings assessing whether the relationship between the amount of investment and domestic related assaults is conditional upon levels of residential stability. The main effect for investment dollars is still significant and negative (b = −0.0015, IRR = 0.999, p < .01), but the main effect of stability and the interaction term are not significant. Few other structural variables have significant effects on IPV in Models 2 and 3.

Investment and Sex-Specific IPV

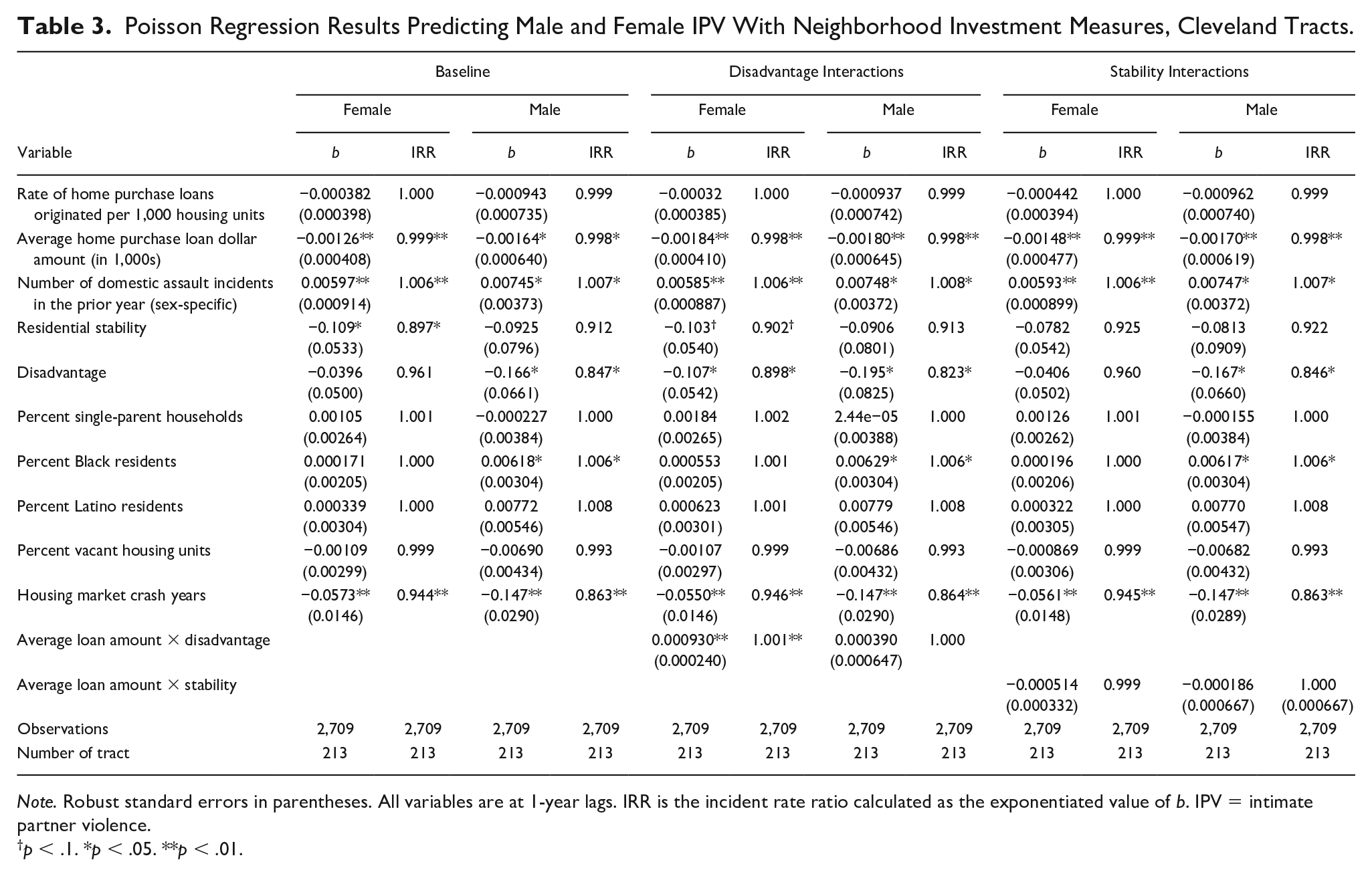

We next present the results examining investment and neighborhood structure on female and male IPV incidents. These results are presented in Table 3; Model 1 shows the results for our baseline models. Similar to the aggregated models in Table 2, we find that the rate of home purchase loans originated in a neighborhood has no appreciable effect on female or male domestic assaults. However, the average dollar amount of loans originated in a neighborhood is a significant predictor of IPV for both females and males, although the effect size is slightly larger for male victims. For every additional $1,000 dollar average investment, there is a 1.26 decrease in the number of female IPV assaults and a 1.64 decrease for male victims. Model 1 also reveals some differences in neighborhood effects across victim sex. For example, residential stability is associated with fewer female IPV victims (b = −0.109, IRR = .897, p < .05) but is not significantly related to the number of male victims. The racial composition of a neighborhood, however, only matters for male victims (b = .006, IRR = 1.006, p < .05). Similarly, disadvantage is also only significantly related to male victims of IPV, but the relationship is opposite of what would be expected (b = −0.166, IRR = .847, p < .05).

Poisson Regression Results Predicting Male and Female IPV With Neighborhood Investment Measures, Cleveland Tracts.

Note. Robust standard errors in parentheses. All variables are at 1-year lags. IRR is the incident rate ratio calculated as the exponentiated value of b. IPV = intimate partner violence.

p < .1. *p < .05. **p < .01.

Next, we examine whether the effects of average investment dollars on sex-specific IPV are conditional on neighborhood structural characteristics. These results are displayed in Table 3 Model 2 for the disadvantage interaction and Model 3 for the residential stability interaction. Interestingly, although disadvantage was not a significant predictor of female IPV in Model 1, it becomes significant and negative (b = −0.107, IRR = 0.898, p < .05) when the interaction term is included; and the interaction term is only significant for female victims of IPV (b = 0.0009, IRR = 1.001, p < .01). When this interaction is graphed (not shown), the pattern of results is similar to Figure 1. That is, (a) higher average investment dollars are associated with fewer female victims of IPV across all neighborhoods although the effect is largest in high disadvantage neighborhoods, and (b) even lower amounts of investment dollars significantly reduces female IPV incidents in high disadvantage neighborhoods. For males, the main effects of disadvantage and the average loan amount are significantly related to fewer male IPV victimizations, but the interaction is not significant. Finally, we examined the moderating effects of residential stability on investment, shown in Model 3. The interaction effects are not significant for both female and male victimizations, and the pattern of results is largely similar to those in Model 1.

Discussion

This study examines the impact of investment through home mortgage loans on the domestic assault victimization of men and women. We assess the extent to which investment might mitigate the deleterious effects of disadvantage and instability on IPV and whether the alleviating effects of investment on disadvantage vary across sex-specific victimization. We find that investment reduces domestic assault victimization generally and across sex, and higher levels of financial investment temper the aggravating factors associated with neighborhood disadvantage.

First, we find that neighborhood investment reduces levels of IPV generally, as well as rates of female and male IPV victimization specifically. However, the effect is contingent on the measure of investment: the number of loans in a neighborhood does not significantly influence IPV, rather, the average loan amount—or the financial extent of investment—does. Although the presence of homeowners in a neighborhood has been shown to significantly reduce crime rates (Boggess & Hipp, 2010), our findings suggest that the number of homeowners in a neighborhood may be secondary in reducing domestic assault victimization relative to the overall amount of money invested in a neighborhood. Our findings largely align with O’Campo and colleagues (1995), who found no association between owner-occupancy rates and IPV. Although homeownership rates are linked with reductions in crime generally, for victims of domestic assaults, owner-occupied housing may represent a private sphere where neighborhood factors do not pervade, especially in disadvantaged or nonsocially connected communities. Women may hide in their own homes becoming increasingly isolated, and the financial commitments associated with homeownership may make it more challenging to leave abusive situations. Indeed, Valentine et al. (2019) found an increased likelihood of repeat victimization in neighborhoods with high homeownership rates, suggesting women may be trapped with an abuser or an unwillingness of longer-term homeowners to get involved in domestic matters.

Investment dollars flowing into neighborhoods, however, is associated with fewer IPV incidents. This represents greater financial resources entering the neighborhood rather than an increase in homeowners. Neighborhoods where the average amount of investment is increasing over time likely represents improvements to the neighborhood and corresponding increases in property values. Greater investment improves the amount of economic capital in a neighborhood and may trigger future economic growth and the establishment of businesses. Neighborhoods with more robust housing markets are more attractive to investors and may incentivize businesses to relocate to these same neighborhoods. This type of investment contributes to the number of overall economic opportunities for neighborhood residents (Peterson & Krivo, 2010) and may specifically provide employment opportunities for residents. This may be particularly critical for female victims of IPV, since male unemployment may be an important trigger for male aggression toward female partners (Yonas et al., 2011). Additional economic capital in a neighborhood also improves the number and quality of community services, including shelters, legal aid (Parker & Hefner, 2015), and health centers utilized by IPV victims (Yonas et al., 2011). For female victims who are more likely to be relegated to traditional roles, this may result in increased access to resources to help leave abusive situations.

Second, we find evidence that the effects of investment on IPV are conditional on the level of disadvantage in a neighborhood. Higher average dollar amounts are associated with a reduction in IPV incidents across levels of disadvantage, but in neighborhoods with high disadvantage, even small loan amounts can reduce IPV. This suggests that minimal amounts of economic investment in neighborhoods provide benefits that are associated with fewer IPV incidents. This pattern mimics findings that show economic investment provides greater “bang for the buck” in terms of crime reduction in disadvantaged or minority neighborhoods (Saporu et al., 2011; Vélez, 2009). In these neighborhoods, an influx of money may have a more visible impact, given the generally lower property values in minority neighborhoods or higher numbers of abandoned properties in impoverished communities.

Notably, this relationship is driven by its impact on female victimization. For women, the structural factors associated with disadvantage might disapate the presence and effectiveness of social ties in a neighborhood (Rountree & Warner, 1999; Wright, 2012). Indeed, Wright (2012) found that the effectiveness of family support to reduce the frequency of IPV vicimization against women was tempered in disadvantaged neighborhoods and that some friends may actually be associated with more frequent victimization. Increased investment in a neighborhood may begin to address some of the conditions associated with disadvantage that impede the effectiveness of social ties (Rountree & Warner, 1999). This suggests the importance of investment by individuals who intend to reside in the neighborhood, as opposed to external investors, as residents will be more entrenched in the neighborhood and become part of social ties in the neighborhood.

For males, disadvantage reduced the likelihood of IPV victimization, and the amount of investment occurring in a neighborhood did not mitigate these effects (Table 3). While this finding is somewhat surprising, cultural norms regarding masculinity and violence may minimize reporting among male victims of IPV, as victimization may undermine respect or challenge the victim’s masculinity (Anderson, 1999; Huntley et al., 2019). Indeed, male victims of IPV reported fears of being shamed as one of the reasons for not reporting the abuse (Machado et al., 2016). This may be particularly true among Hispanics, who are less knowledgable about IPV resources in the community and are generally less likely to seek formal assistance than their non-Hispanic counterparts (West, 1998) in part out of fears or threats of deportation (Reina et al., 2014). Moreover, the impact of disadvantage on male social support is not as consequential as it is for females, which may explain why investment did not moderate the effects of disadvantage. Males do not rely on their social networks for support in the same manner that females do (Broidy & Agnew, 1997), and males are less likely to invest in their intimate networks. This suggests that levels of disadvantage may do little to disrupt male social supports, particularly when social support to address victimization might damage victims’ reputations (Anderson, 1999) or call attention to their statuses as victims (Corbally, 2015).

Third, residential stability was not associated with a decrease in IPV victimization generally, or across sex. Prior research has found mixed support for the role of residential stability on IPV: some studies have found that residential stability increases IPV (Li et al., 2010; Wright & Benson, 2010), some have failed to find significant effects (Browning, 2002; Lauritsen & White, 2001; Miles-Doan, 1998; O’Campo et al., 2005), and other research found that residential instability actually reduces IPV (Benson et al., 2003). One explanation for these mixed findings may be that both male and female victims of IPV are reluctant to leave their abusers (Huntley et al., 2019). In which case, the neighborhood may be experiencing changes in residents over time, but the level of IPV may remain fairly constant if victims are not the ones leaving.

While this study extends our understanding of how neighborhood investment might mitigate the effects of neighborhood conditions on IPV generally, as well as gender differences in IPV, we acknowedge some limitations. First, although social ties are a critical mechanism for reducing IPV, particularly for women, we are unable to directly measure social ties. Given the implications of social ties for both relieving strain and providing emotional support (Broidy & Agnew, 1997), and the potential for neighborhood investment to bolster social ties, future research examining these relationships should more directly assess neighborhood social networks to understand how they may evolve with increasing or decreasing investment. Second, we rely on official reports of victimization, the limitations of which are well documented. The results presented rely on the reporting officer’s designation of an incident as “domestic” in nature. Furthermore, victim reports to the police may be underreported in certain neighborhoods and by sex of the victims. Third, we have no information on the race/ethnicity of the victim (or offender). Given potential disparities in the frequency of IPV (Field & Caetano, 2005) and the likelihood of reporting, future studies should disaggregate the rates of victimization across racial or ethnic background while incorporating elements of the larger social context.

In sum, our study expands on prior work by considering the impact of neighborhood investment on IPV. We find that investment vis-à-vis loan amount is associated with decreases in IPV generally, and for both male and female victims. Investment potentially enhances neighborhood stablity and strenthens social ties, therein bolstering informal social control and underscoring normative expectations of behavior in neighborhoods. Importantly, investment—even in small amounts—can dramatically reduce IPV even in the most disadvantaged neighborhoods. This suggests that investment should be encouraged in communities that have historically experienced disinvestment or abandonment. Encouraging investment in these areas can be challenging; however, some states have taken a proactive approach to enhancing homeownership in disadvantaged neighborhoods. For instance, Texas’ Homeownership Program provides affordable loans and down payment assistance to low-to-moderate income residents purchasing and residing in homes in economically distressed areas (Texas Department of Housing and Community Affairs, n.d.). Directed policies such as these can have meaningful effects on IPV and crime in neighborhoods, disrupting the relationship between neighborhood disadvantage and IPV.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.