Abstract

The global financial crisis has put good corporate governance practices on the radar screen of investors, politicians, and the general public. To comply with corporate governance, executive compensation in general—and long-term incentives in particular—have become increasingly important for companies. Also, calls for more sustainable company performance have emerged all around the world, and politicians have put numerous reforms on the agenda. Some of these reforms especially emphasize the role of long-term incentives for sustainable business development. By doing so, an effective tool to foster a company’s long-term growth practices can be implemented. The article sheds light on global market practice of equity-based compensation, based on the GEO Global Equity Insights 2013 study—conducted by the Global Equity Organization, together with the global blue-chip company, Siemens, and Hostettler, Kramarsch & Partner, an international consulting firm with focus on performance management and compensation. The study identifies current market practice in 133 companies, including a number of the largest global corporations, across 13 countries and 10 industries.

Keywords

The idea that long-term incentive plans (LTIP), especially if they are equity based, support long-term company growth is not novel. This development is also supported by numerous academic studies confirming a positive impact of equity-based compensation on company performance and shareholder value.

For this reason, equity-based compensation has become a broadly used compensation instrument over the past two decades—both for executives as well as for all employees. In the pursuit of sustainable performance and driven by regulatory changes, companies around the world now consider equity-based compensation instruments to be an integral part of their remuneration programs. Thus, LTIP have become nearly universal for companies and the use of broad-based employee share purchase plans (ESPP) is on the rise.

Due to regional and country-specific parameters, there is little available information with regard to international market practice regarding design and implementation aspects of equity-based plans. To shed light on global market practice of equity-based compensation, the Global Equity Organization (GEO), together with the global blue-chip company, Siemens, and Hostettler, Kramarsch & Partner (hkp///), an international consulting firm with focus on performance management and compensation, have conducted the GEO Global Equity Insights 2013 study (GEI 2013) across the world’s most important economic regions, with a particular focus on Europe and North America.

GEI 2013 identifies current market practice and trends of equity-based compensation in 133 companies, including a number of the largest global corporations, across 13 countries and 10 industries. This groundbreaking study also reveals links between design practices, company performance, and satisfaction, from both employee and employer perspectives.

Implementing Equity-Based Compensation: Challenges to Consider

In compensation practice, there are many unresolved issues companies and compensation experts face. Practitioners must navigate through a complex landscape of regulatory and tax regimes, infinite design alternatives and very different experiences with equity-based compensation globally. The inherently complex nature of these plans challenge employers to make them attractive to their employees. In particular, plan communication and satisfaction with the plan are crucial determinants for successful implementation. Only when participants have a clear understanding of the plan can equity-based compensation foster company success.

The GEI 2013 study addresses these issues regarding company equity culture—both for LTIP and ESPP. There are significant differences in what successful companies and other companies do: design features, as well as how these features are perceived from an employee and employer perspective, vary considerably. Also, good plan communication is a crucial tool to develop and increase the equity culture within the company—and therefore ultimately drives a company’s success.

LTIP Lose Exclusivity and Now Affect Organizations More Broadly

Looking at company practices in general, LTIP have gained importance in the compensation of a broader employee group. They are no longer just an exclusive compensation instrument for the company’s top executives; rather, almost half of all companies surveyed offer LTIP down to Reporting Level 5 below the Board. This observation holds true for both European as well as North American companies.

Above all, 26% of the responding companies in North America grant LTIP to all employees. The prevalence of variable compensation linked to multi-year performance measures stems from, among other things, its impact on corporate policies. Compliance with corporate policies can be achieved by using LTIP to reward strategy-oriented performance. The fact that, according to the study’s findings, companies typically adjust their LTIP plan design with realignment or adjustment of the company strategy underpins this assumption.

LTIP Drive Company Value: but Participants’ Understanding Needs Improvement

In general, the analysis confirms the prevailing view that LTIP are related to company performance. 1 It shows that LTIP participation is compulsory in more successful companies. Moreover, the study shows that companies perform better if they require LTIP participants to make a self-financed investment of a certain percentage of their LTIP award level.

These factors suggest that company success is related to the extent to which employees hold a stake in the company. Thus, LTIP seem to represent an adequate instrument to pursue the objective of shareholder alignment. However, the extension of LTIP to a broader employee base comes at a cost. It is revealed that in companies with compulsory LTIP participation, employees tend to have more difficulties understanding the plan and are less satisfied with the plan communication. Said differently, although successful companies rely on LTIP on a broader scale, plan implementation and communication can and should be improved.

Besides examining LTIP on a general level, the study takes a closer look at current market practice of specific plan characteristics and analyzes how different plan design features affect both company success and employee satisfaction.

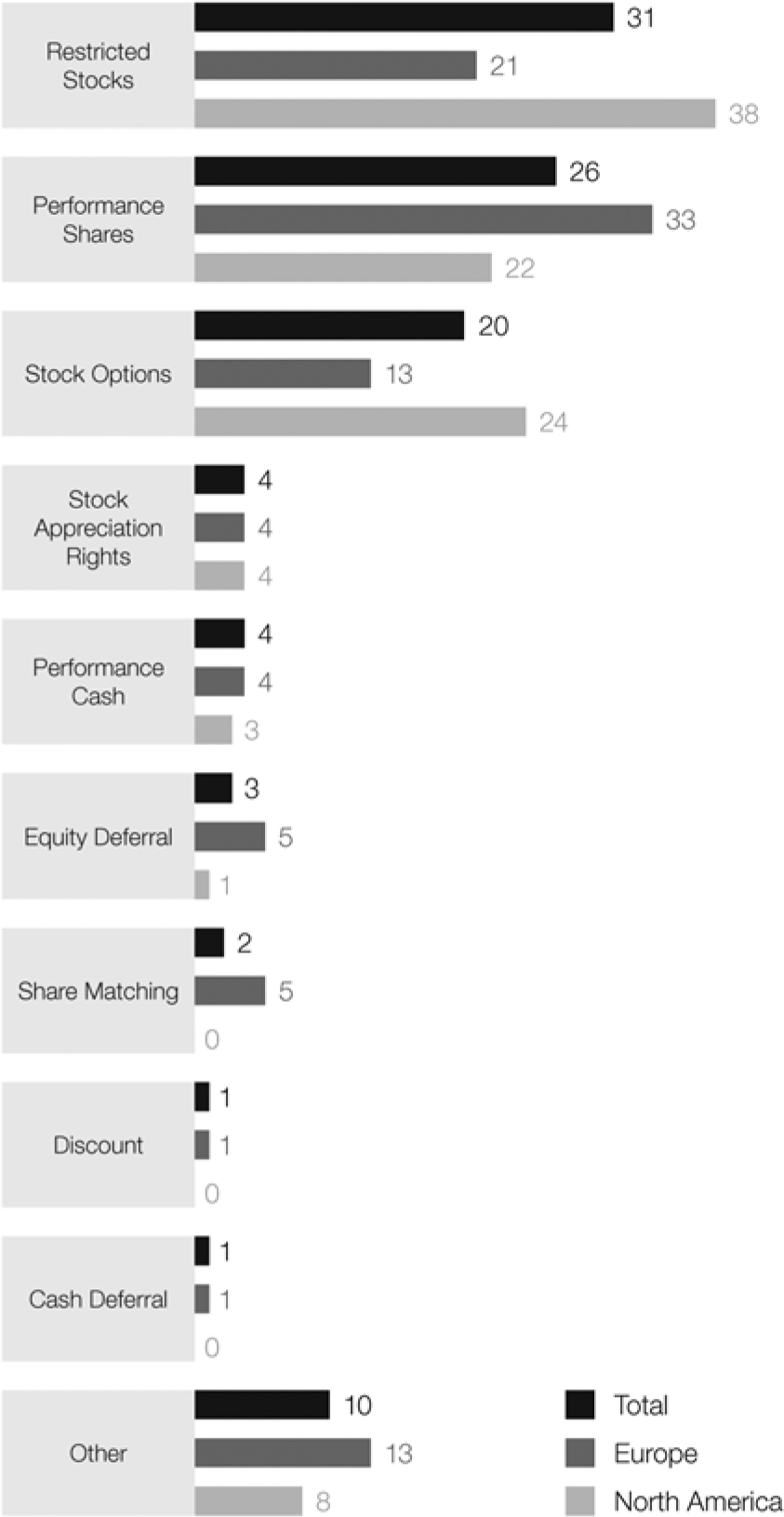

Use of Stock Options on a Steady Decline: Balanced Risk Profile Plans Gain Popularity

Looking closer at LTIP characteristics, market practice shows that LTIP grants in Europe are primarily Performance Shares, followed by Restricted Stocks and Stock Options. European regulatory regimes and investors have been clamoring for performance conditions for some time now. A slightly different picture emerges for companies across North America, where Restricted Stocks are the prevalent LTIP.

Whereas only a decade ago, Stock Options were the predominant plan type, they now rank only second in terms of prevalence, followed by Performance Shares. Regardless of region, other plan types like Performance Cash or Share Matching are of minor relevance.

The fact that Stock Options, “plain-vanilla U.S.-style,” are no longer the most common plan type does not come as a surprise: The public debate mainly focused on Stock Options when criticizing large pay-outs for executives and excessive risk-taking. Coupled with the change in accounting requirements for these instruments in the mid-1990s, the declining popularity of stock options as a compensation instrument is not unexpected.

Public and investors’ pressure, as well as changes in regulation, may have contributed to the use of plan types that are tied to additional performance conditions other than just share price. However, these forces alone can hardly explain the significant use of Performance Shares. Rather, the fact that LTIP have become a compensation cost makes companies choose incentive vehicles that feature a more balanced risk profile and thus arguably a higher perceived value.

When looking at plan types from an internal perspective, it appears that this development is in line with the perception of employees. Due to more predictable compensation outcomes, employees are most satisfied when the LTIP are designed as a Performance Share plan (Figure 1).

LTIP types (in percentage ranked by prevalence).

Beyond that, the study further shows that there is no clear link between plan type and company performance. That is, although the existence of LTIP increases company success in general, the specific choice (restricted stocks, performance shares, stock options, etc.) seems to be a matter of a company’s particular economic situation, strategy and objectives. Successful companies distinguish themselves from less successful companies in how their respective plans are implemented and, hence, how sophisticated the respective equity culture is.

Vesting Periods: Not a Crucial Factor for Success

The majority of firms surveyed (60%) apply vesting periods between 2 and 3 years, whereas in 25% of the companies surveyed vesting periods are slightly longer, ranging from 3 to 4 years. When looking at plan types, the vesting period applied for Stock Options is 4 years on average and therefore slightly longer than in the case of Performance Shares or Restricted Stocks. However, these differences are neither significantly related to company success nor to employee satisfaction.

Sophistication in Performance Promote Value Creation but is Negatively Related to Employee Satisfaction

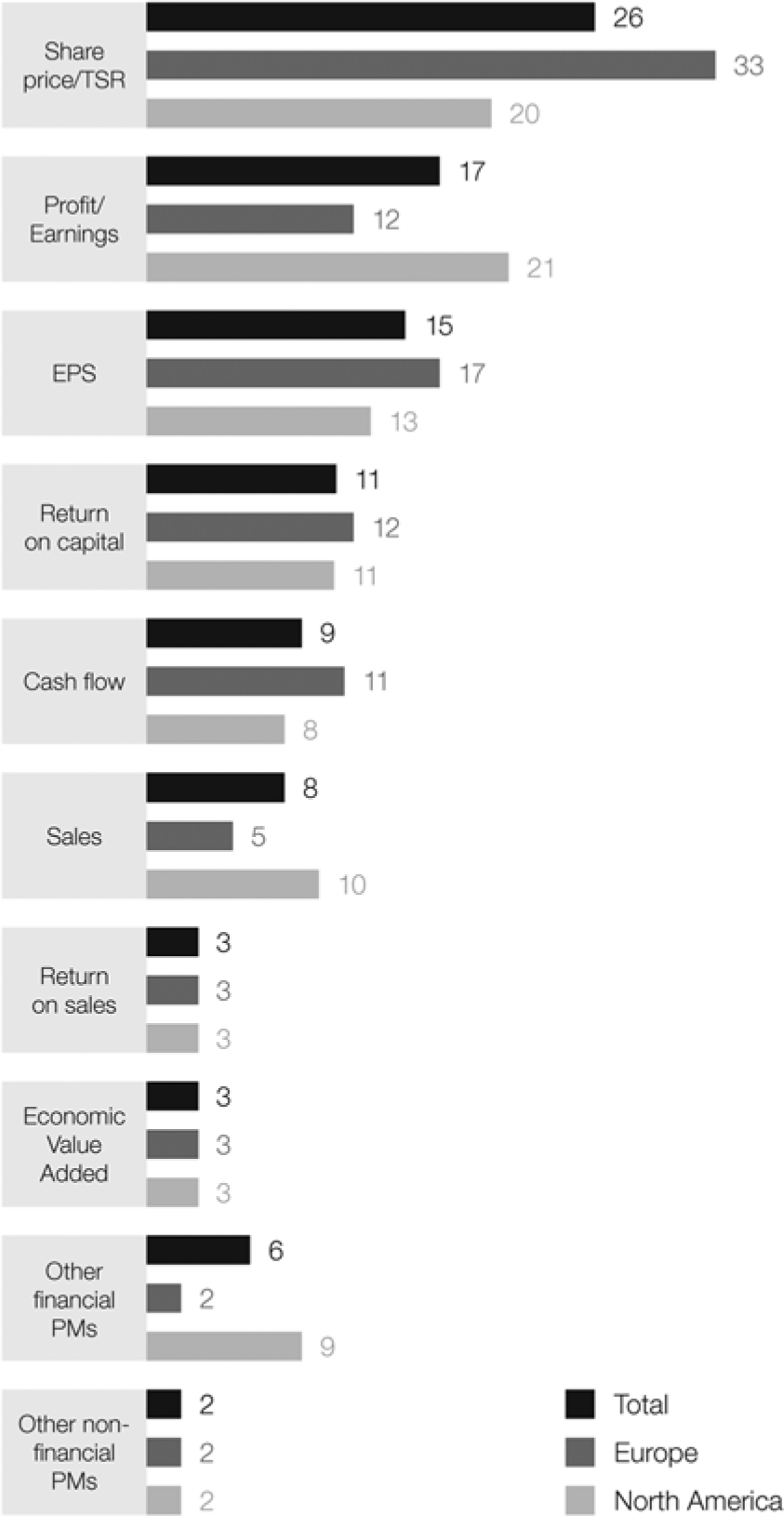

Another important LTIP feature is how companies set targets to be achieved under an LTIP performance grant. In addition to time restrictions, performance measures can be used to determine the final payout level of the LTIP.

In Europe as well as in North America, the most common performance measures are external ones such as share price and total shareholder return. Compared with other key performance indicator categories, profit- or earnings-oriented measures are also frequently used. The use of a certain key performance indicator category also differs according to the plan type applied: Whereas both Performance Shares and Stock Options are predominantly linked to external performance measures, Restricted Stocks are mainly tied to internal, profit-oriented measures.

Altogether, companies tend to use internal performance measures because they are easy to understand and provide LTIP participants with a direct line of sight from company objectives to individual performance.

Variety in Performance Measurement Drives Success: but Lowers Understanding

In successful companies, LTIP target achievement is subject to a higher number of performance measures. Moreover, the analysis reveals that companies that base LTIP awards on individual performance are more successful. At the same time, the increased complexity that comes with both decisions has a negative impact on employees’ understanding of plan design and their satisfaction with communication efforts (Figure 2).

LTIP performance measures (in percentage ranked by prevalence).

Thus, it can be argued that overall, a higher LTIP complexity, with regard to performance measures, allows a company to incorporate more performance measures in line with sustainable targets, which subsequently increases overall company value. At the same time, companies seem to fail to explain the increased plan complexity to the participants, which results in employee dissatisfaction.

Communication Connects Company Success and Employee Satisfaction 2

Limited understanding does not seem to be the only source of employee dissatisfaction. In general, the study shows the majority of employees are only moderately satisfied with their LTIP. This not only holds true for different aspects like risk profile and tax treatment but also for overall satisfaction. Nevertheless, for 31% of the employees the overall satisfaction is high.

Across various aspects of LTIPs—namely ease of participation, tax treatment, risk profile, communication and design—only plan design and communication significantly drive employee satisfaction with the LTIP, with communication having a bigger impact. Moreover, communication is the main driver of employees’ understanding of LTIP, and thus their satisfaction with them.

Although communication is crucial for plan understanding and thus employee satisfaction, the survey revealed companies spend the least portion of their overall budget for equity-based compensation on communication efforts. From the practical implications, we therefore suggest companies can improve their equity culture by focusing more on communication measures to facilitate participant understanding, and thus participant satisfaction.

When looking at current communication practices, evidence shows across all regions, traditional communication measures like letter or email are still predominant when informing employees about a company’s LTIP. More unconventional and innovative communication methods are rarely used, even though videos, social media, posters/roll-up banners, brochures/flyers and the like have an especially positive impact on employee satisfaction with communication.

Employee Participation: Equity is King, but Governments Need to Pave the Way

As the labor market has become more competitive, companies are enhancing their equity-based compensation vehicles through the implementation of broader ESPP in addition to LTIP. As LTIP typically aim to incentivize a certain employee behavior, they are still used, more often than not, on a selective basis. In contrast, ESPP are predominantly used to enhance employee identification with the company by creating a spirit of common responsibility and ownership—accordingly, they are offered to a broader employee base (see Figure 3).

ESPP types (in percentage ranked by prevalence).

Furthermore, ESPP can be a significant asset in attracting and retaining new talent and supporting an employee’s saving efforts. Hence, more than half of the companies surveyed (60%) have already implemented such plans. However, with regard to the regulatory environment, there is still much potential for providing initiatives, which promote wider employee share ownership. For example, in most of the companies surveyed, employees are only moderately satisfied with the tax regulations of ESPP. The same holds true for employers who might indicate that regulatory and tax requirements are hard to meet. This fact seems to prevent some companies from offering equity-based compensation vehicles to employees other than their top management. Implementing equity-based compensation plans in different countries requires companies to invest a lot of effort and expense because of the different regulatory and tax requirements. A standardization of legal requirements across countries would significantly ease implementation of LTIP and ESPP and, therefore, foster the positive effects of equity-based compensation.

Global Trend to Share Discount Plans

Share Discount plans are the most frequently used ESPP type in the sample. Share Matching plans rank second and represent a slightly higher portion in Europe than in North America. Regional differences regarding plan types are mainly because of country-specific tax regulations.

Nevertheless, across all regions, free shares are rarely used. In general, the finding that share discount plans are most commonly used is not surprising, considering the fact that they are less complex in terms of communication and administrative effort compared with share matching plans. Moreover, from a shareholder perspective, they support sustainable corporate development as they require each participant to make a personal investment in company shares.

Company Performance Driven by Broad-Based Equity Culture

ESPP has a positive impact on company performance. This is especially the case when firms offer both ESPP and LTIP to their employees. Also, successful companies tend to have a higher portion of employees that actually participate in the ESPP relative to total eligible participants. It appears that the more employees get “a hand at the wheel,” the stronger their sense of identification with the company, and the higher their motivation to strive toward the common goal of creating sustainable company value.

Drawing from this, it seems that establishing a broad equity culture drives company success. Thus, widespread equity ownership within a company is a powerful tool to align employees’ interests with shareholder interests.

Design parameters vary across companies and it appears that HR professionals know how to select the right design features that fit the company’s profile and objectives. However, it seems that plan design itself does not guarantee a successful ESPP implementation.

For ESPP Success, Communication is Key

Taking a closer look on potential factors that influence the extent to which an ESPP is implemented successfully, one crucial aspect stands out: Employees of successful companies exhibit a higher understanding of their plan, which helps them to make informed decisions about participation (see Figure 4). As in the case of a company’s LTIP, communication appears to be the crucial tool contributing to overall firm performance by increasing both the understanding of—and the participation rate in—ESPP.

Drivers of company success.

With this in mind, the fact that more than half of the employers surveyed are not very satisfied with their current communication efforts is rather surprising. As seen previously, when looking at the current portion of budget spent on plan communication, it becomes clear that companies do not put as much emphasis on communication when implementing ESPP as might be needed.

Summary

The GEI 2013 study sheds light on current market practice on equity-based compensation and reveals the links between plan design features, company success and both employee and employer satisfaction. Overall, although differences exist, most companies worldwide use sound equity-based compensation schemes. In particular, it appears that top performing companies incorporate plan features in line with sustainable performance. LTIP are used now more than ever and are increasingly anchored in a company’s reward culture. With regard to plan design, there is a global trend toward plan types with a more balanced risk profile, predominantly linked to performance measures within an employee’s line of sight.

However, successful companies, compared with others, seem to have established broad-based equity ownership among employees. That is, equity-based incentive schemes are not limited to a company’s leadership elite, but rather implemented across the organization, often in the form of ESPP.

Although effective communication of equity-based incentive schemes to employees appears to be the main source for employee satisfaction, and thus company value creation, companies do not yet devote enough attention to the subject. As plan design complexity increases, it makes it difficult to understand the underlying plan mechanisms, which in turn create discontent among employees.

Employee satisfaction can be significantly improved through increased communication efforts. This is especially true in the case of broader-based ESPP, where participants of varying levels of education are less familiar with equity-based instruments.

Thus, there are two main drivers companies should focus on in their pursuit of sustainable value creation. First, they need to allocate more time and budget on innovative communication measures such as image videos or social media. This is necessary in order for plan participants to understand their role in the company performance and what their reward will be in case of target achievement. Second, companies should actively promote equity culture across all employee levels by introducing broader-based equity plans such as ESPP or all-employee LTI plans, in addition to conventional LTIP. Finally, one can claim that governments need to encourage broad-based equity culture and entrepreneurship by strengthening the regulatory framework and therefore easing implementation of LTIP and ESPP on a global level.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.