Abstract

Unlike the popular market-value stock options, stock awards and stock appreciation plans, phantom stock plans do not involve ownership of publicly-traded stock, although market-based stock may be used as a measurement of the phantom stock plan. Another popular method for valuing phantom stock plans is book value (i.e. assets minus liabilities). It is important to note that phantom stock plans can incorporate any design features of a market-based plan. However, under FAS 123R, phantom plans will be treated as a liability award and subject to a variable accrual, unlike market based plans which are considered equity awards and fixed accounting using a pricing model. The company has a tax deduction at time of the recipient having taxable income in the same amount of such income.

Plans that compensate individuals based on a measure of stock appreciation and/or dividends but do not involve actual ownership of publicly traded or privately held stock are called phantom plans because the “stock” does not really exist. Such plans may also be called shadow or pretend stock plans. There are two types of phantom plans: market value–based and nonmarket-based plans. Both provide for cash payouts.

Market Value–Based Stock Plans

These plans are a form of incentive pay that uses company stock (typically publicly traded) as the basis for measurement. There are three types: dividend equivalents, appreciation rights and full-value units. Payments are in cash. These plans are typical of countries where individuals cannot own foreign company stock and/or the taxing of such stocks and options is prohibitive. They are also found in the United States for companies in the mature stage or later of the market cycle.

Dividend Equivalents

The recipient’s income is based on a dividend equivalent multiplied by a stated number of shares of company stock. The executive does not receive the stock but will receive each year an amount in cash equal to the dividend paid. Thus, an executive who received 10,000 shares/units with dividends equaling $1 each would receive $10,000 for the year. The following year, if the executive received an additional 10,000 units and the dividend was increased to $1.10, payment would total $22,000. Such grants may be in effect for long periods of time, for example, until death or age 85, whichever comes last. Since the employee has income, the company has a deduction and an ongoing charge to the income statement. The early death of an executive could cause considerable cash liquidity problems for the estate if payments continue, because estate taxation requires including in the estate payments to be received in the future.

Appreciation Rights

These operate like market value stock appreciation rights except that they are not attached to actual shares of company stock. A stated number of phantom stock units at a prescribed price are given to the executive with a specified date of valuation. Thus, at valuation date, the executive receives the difference between fair market value and price at the time of grant, in cash. The company has a tax deduction at time of payment, and the executive has a comparable amount of income. The company has to amortize the compensation liability.

Full-Value Units

This approach differs from appreciation rights only in that appreciation is from first dollar to fair market value at date of valuation. In other words, the price at time of grant is zero rather than current fair market value, and at the time of payout the award is based on the current market value.

Nonmarket-Based Stock Plans

In general, anything that market-based plans can do, nonmarket-based plans can also do. While most common in privately held companies, under certain circumstances, they are useful for publicly traded companies as well. In addition, nonmarket plans probably have the most attractive and certainly the simplest payout—cash.

The formula for these plans is not tied to company stock in any way. Instead, it specifies the amount of cash that will be paid with the achievement of defined objectives (note that with performance unit plans, paying in cash, not stock, would meet this description). The award can be paid immediately or deferred over a period of time. The company has a deduction at the time of payment equal to the amount the executive has earned in the way of income. The earnings statement is charged with accrued expense over the performance period.

However, the strength of these plans is their weakness. With cash payments, there are no opportunities for long-term capital gains tax treatment. Also, although they are not likely to go “underwater” or remain flat for prolonged periods like market-based stock plans, they are also not capable of rising dramatically in times of a bullish stock market. These characteristics make such plans almost a form of guaranteed-payout profit sharing. Of course, establishing a minimum growth target before payment thwarts this problem.

Nonmarket-based plans are sometimes called employer stock plans because they have no market value stock component. Sometimes, publicly traded companies use them instead of stock. When prices are languishing on the stock market, an internal valuation might be more beneficial because of languishing stock price. Publicly traded companies also use them for strategic business units that do not have their own stock. However, they are most common with privately held companies, where they are an attractive alternative to diluting ownership.

Measurements Used

Lacking a market measurement, nonmarket-based plans rely on internal financial measurements. Probably the most common is book value, or shareholder equity (i.e., assets minus liabilities) divided by shares outstanding. The phantom stock issued could be full-value units or appreciation only; other possibilities include budget attainment, cash flow, earnings, earnings per share (EPS), economic profit, equity growth, market share, net worth growth, return on assets, return on equity (ROE), return on invested capital, return on net assets, return on sales, revenue and total shareholder return. Variable accounting rules are in effect to determine charge to earnings, and the company will have a tax deduction when the individual receives the income.

Dividend Equivalents

A privately held company may also use phantom stock to compensate the executive based on dividends. This is advantageous in closely held organizations where the owners do not wish to dilute ownership. Alternatively, the dividends could be paid on stock actually awarded.

Appreciation Rights

An appreciation right on the phantom stock of privately held companies or strategic business units would use some measuring device other than market value. Many plans are constructed around book value. Unlike company stock, which can bounce up and down under the influence of macroeconomics issues rather than company performance, book value usually has a nice steady progress. (However, it is affected by acquisitions and divestitures.) Book value plans have been used primarily by privately held companies, although publicly held companies may also adopt them when stock performance is lackluster. Simply stated, such a plan allows executives an opportunity to benefit from appreciation in book rather than market value.

Another variation deals with EPS; such plans are likely to use a moving multiyear average (or total) to avoid small annual swings. Still another variation for those involved in mining or drilling might relate to established reserves; clearly, this would place a significant emphasis on new discoveries.

Full-Value Units

The 100% discount of full-value units may be accomplished by allowing the executive to purchase stock at its current book value, for example, repaying the loan with dividends received. (Remember that the Sarbanes–Oxley Act prohibits loans to insiders.) Alternatively, the stock might be awarded outright. Using the example shown in Table 1, assume an executive received 10,000 book value units at $25 a share. In the illustration, earnings per share increases at 10% per year. If the plan specified that payment could also include dividends, the executive would have received almost as much in dividends after 10 years (i.e., $23.90 a share) as the $25 initial stock price. The stock would now be worth $648,600 (i.e., 10,000 shares at $64.86 a share).

Example of Book Value Stock Purchase.

If the executive were simply given appreciation units, no investment would be required and the executive would have received $398,400. If dividend equivalents were also a feature, the executive would receive an additional $239,000 during the 10 years. Both would be ordinary income with the company receiving a like tax deduction when paid; however, expense would have been accrued over the 10-year period.

Typically, the executive must sell the stock back to the company when employment is terminated. In case of death, disability or retirement, the stock would be bought back at current book value. However, with voluntary terminations some form of penalty may exist (e.g., buyback at original book or forfeiture of all gains for the previous 5 years).

Rather than award the book value stock outright, the executive might be given the option to purchase. A variation to book value would be book-value-plus-dividends-paid. The advantage of this approach is that a change in the level of earnings retained has no impact on the valuation. Remember period-ending book value is by definition equal to book value at beginning of period plus EPS less dividends paid.

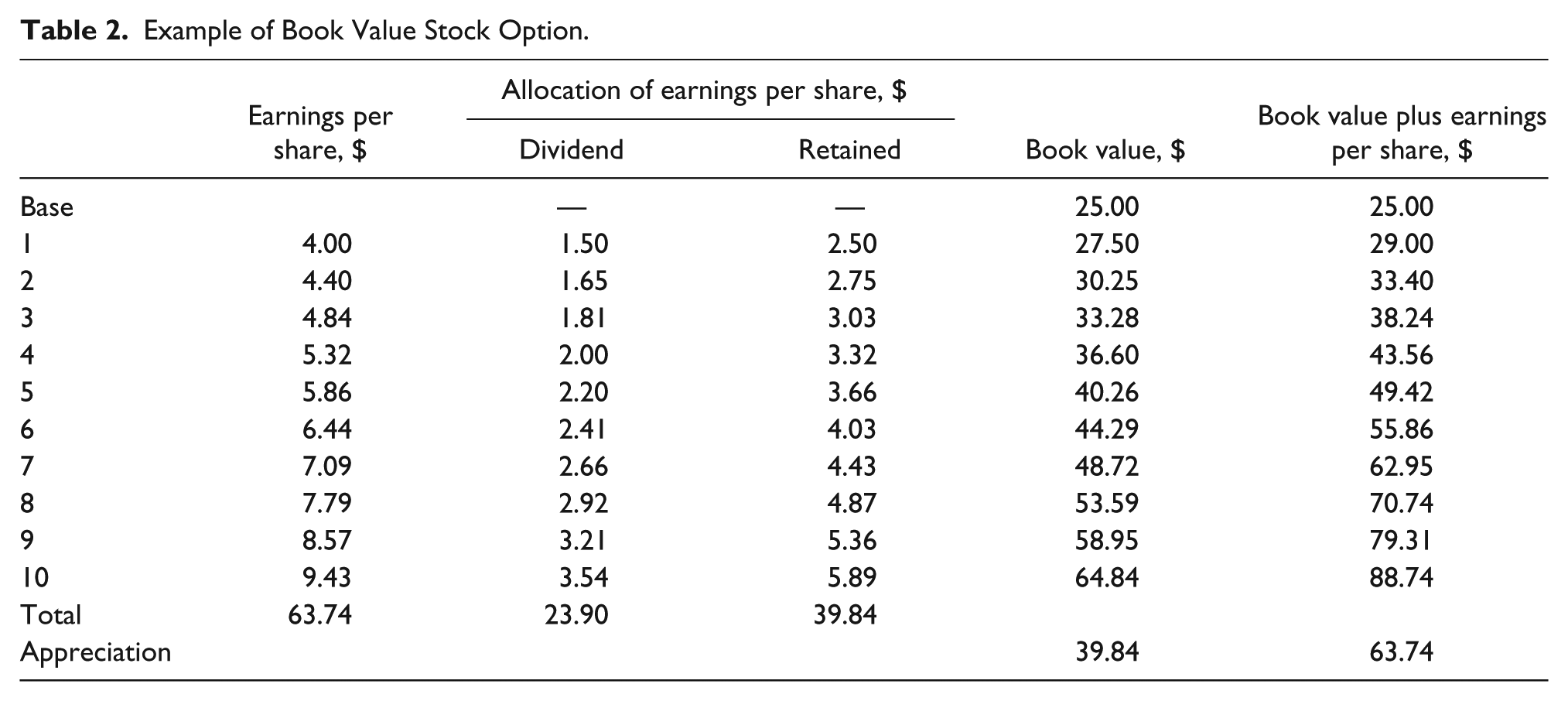

Following the same example, repeated in Table 2, the executive would be offered an option to buy at $25. If the executive exercises the option 5 years later, the gain would be either $15.26 (i.e., $40.26 − $25.00) or $24.42 (i.e., $49.42 − $25.00) per share, depending on which definition of book value was used for purposes of the option.

Example of Book Value Stock Option.

At time of exercise, the executive would have income in the amount of $152,600 or $244,200 (again depending on the definition), assuming 10,000 shares were purchased. There would be no tax event if constructive receipt were avoided. Assume the individual retires 5 years after when the book values are $64.84 and $88.74, or $648,400 and $887,400, respectively, for 10,000 shares. The difference of $495,800 and $643,200, respectively, could qualify for long-term capital gains taxation.

The company would have a tax deduction and charge to earnings equal to the amount the executive received as ordinary income, but not on any long-term capital gains. The total increase at retirement, either $495,800 or $643,200, would have been charged to earnings, and the company would have a like tax deduction assuming no long-term capital gains tax availability. The lack of long-term capital gains would greatly reduce the attractiveness to executives of this type of plan. One would have to wonder why anyone would purchase phantom stock unless it could qualify for long-term capital gains.

However, privately held companies must be very careful in setting up such plans if they may at some point go public through an initial public offering. Plan design should ensure that accounting and tax issues do not complicate such a transaction. Lacking an ownership interest, management cannot buy out owners because they have no real stock.

The appreciation with these plans is a direct function of corporate financial success and is not subject to external factors, except for acquisitions, spin-offs, changes in accounting procedure or other unusual events that could affect book value (all of which can be netted out), Thus, the executive with book value units in a publicly traded company is not concerned with the stock market assessment of corporate performance. As long as shareholder equity is increasing on a per-share basis, the potential value of the nonmarket incentive is also increasing. Not surprisingly, the executive’s degree of interest in book value options is almost directly inversely related to the direction of movement in common stock: great interest in times of bear markets, little interest during bull markets.

Similar Plan Models

While book value has been used here to illustrate nonmarket-type plans, a number of other measurements are available. Let’s take a look at several variations using EPS: performance cash plans, performance unit plans and performance percentage plans.

Performance-Cash Plans

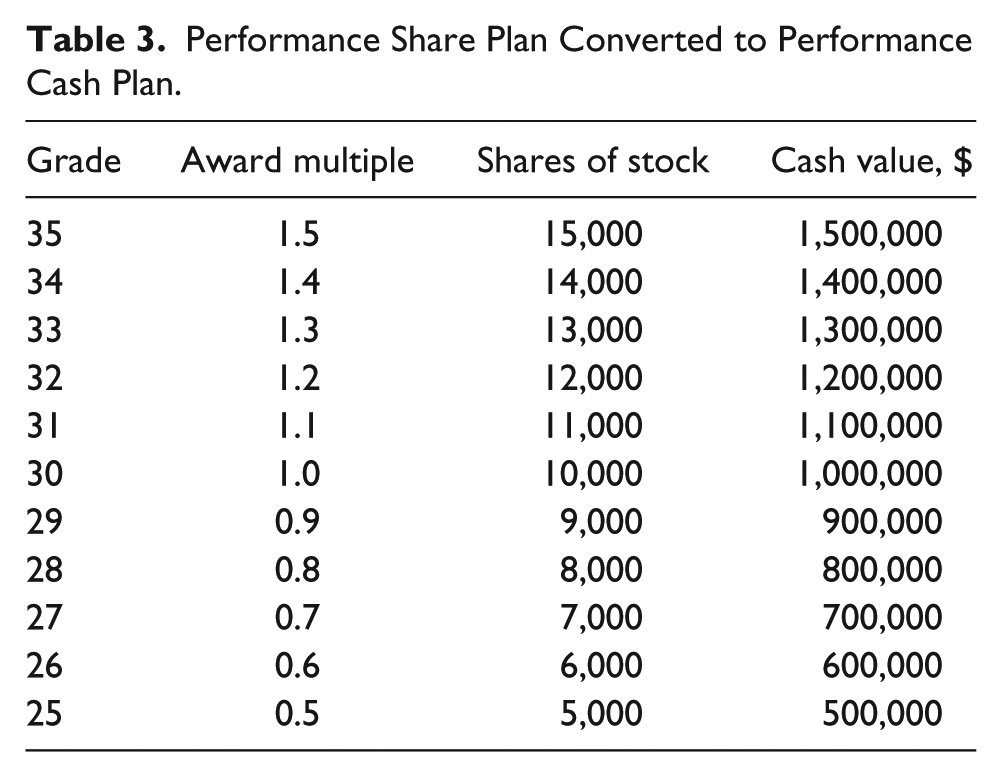

Rather than set the schedule in shares of stock, performance-cash plans use the current value of the stock to develop a dollar or cash figure. In Table 3, the performance shares have been converted using $100 a share.

Performance Share Plan Converted to Performance Cash Plan.

The dollar allocation is adjusted by company performance as shown in Table 4. Thus, if the corporate 3-year average EPS were 16%, the payment would be $3,000,000 (i.e., $1,500,000 × 200%). This amount would be paid in cash, stock or a combination. If paid in stock, the difference would inversely reflect the change in stock price. That is to say, if the price of the stock doubled, one would receive half the number of shares that would have been given if it were a performance share plan. In other words, had this been a performance share plan, the executive would have received 30,000 shares (i.e., 15,000 × 2) worth $600,000 (i.e., 30,000 shares × $200). With these same numbers, under the performance cash plan the individual would have received 15,000 shares (i.e., $3,000,000 ÷ $200).

Percentage Cash Award Based on Earnings per Share.

Since the plan is insulated from market factors, it will exactly equal the dollar value believed appropriate at a prescribed level of performance. While the expected dollar allocation must be amortized, there is no adjustment for movement in company stock since its market value has no impact on the dollar value of the award.

Performance Unit Plans

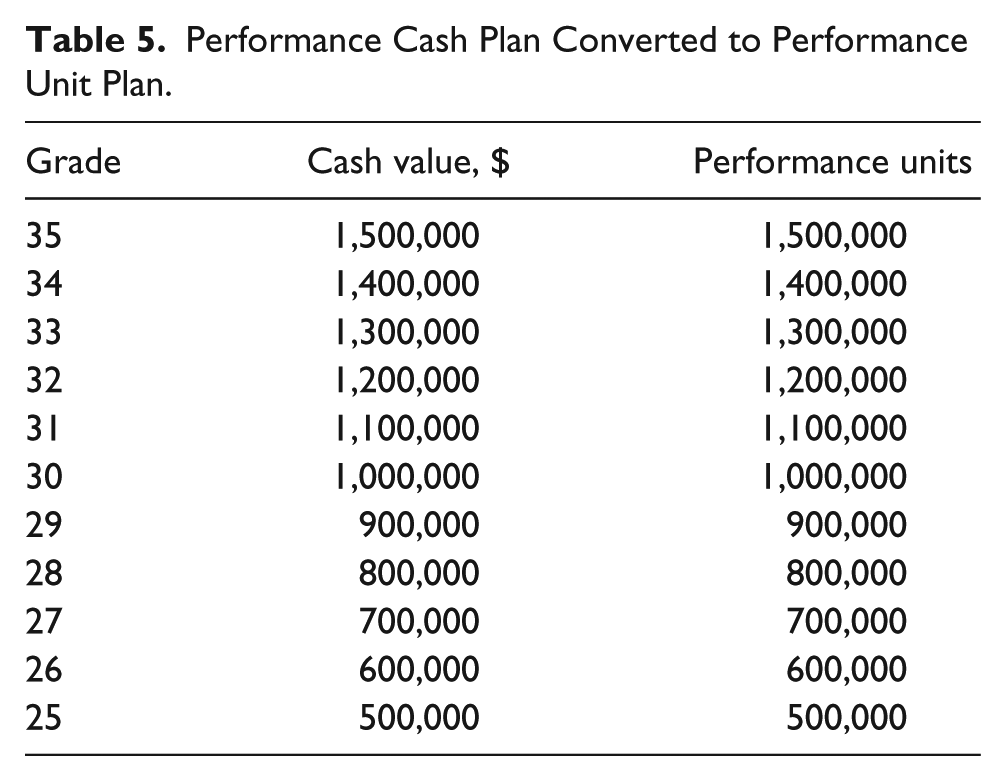

It is a simple step to convert from a performance cash to a performance unit plan—simply remove the dollar signs and the values become units. As illustrated in Table 5, each unit is worth a dollar.

Performance Cash Plan Converted to Performance Unit Plan.

Why make this conversion? Because it means never having to redo the plan if one decides at a future date to increase the payout. To increase payouts by 10%, one would have to restate the payments in Table 3. Namely, $1,500,000 would become $1,650,000; $1,400,000 would become $1,540,000; and so on. However, if the plan were in units, the number of units would not be changed, only the unit value, which would now become $1.10. It is easy to see that a performance unit plan can easily and quickly be adjusted on a frequent basis to maintain the desired relationship to salary and annual incentives. Again, the payout can be in cash, stock (valued at time of payout) or some combination. Accounting and tax treatment are the same as performance cash plans.

Fixed number of units and fixed price per unit: This was illustrated in Table 5, with the number of units fixed for each job grade and each unit worth $1. Alternatively, the price of each unit could be set equal to the current stock price. If payout is in cash, it is a cash-settled plan and subject to variable accounting. However, if settled in stock, it is probably eligible for grant date–fixed accounting using an appropriate option pricing model.

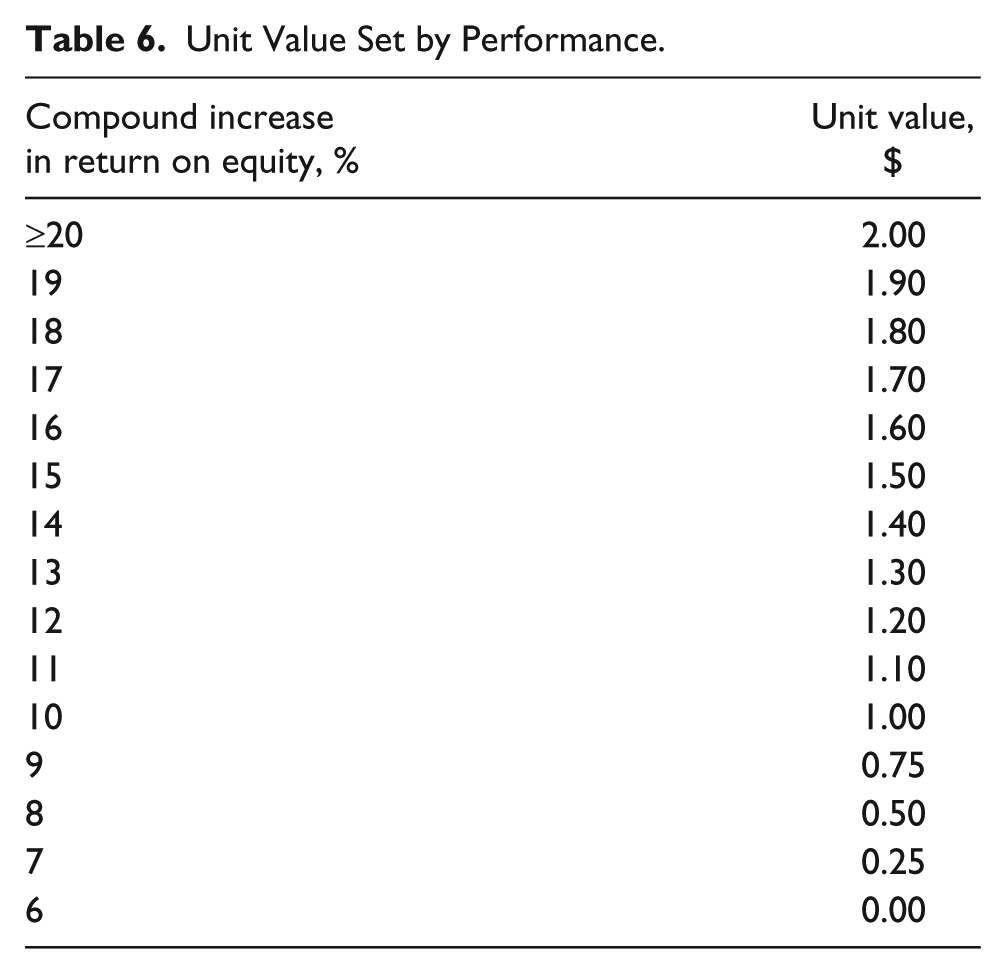

Fixed number of units and variable price per unit: This is often called a cash formula value plan. The units shown in Table 6 are worth a unit value based on performance achieved. If the person had 1 million units (Grade 30 in Table 3) and the compound ROE over the 3-year period was 15%, each unit would be worth $1.50. One million units would be worth $1.5 million.

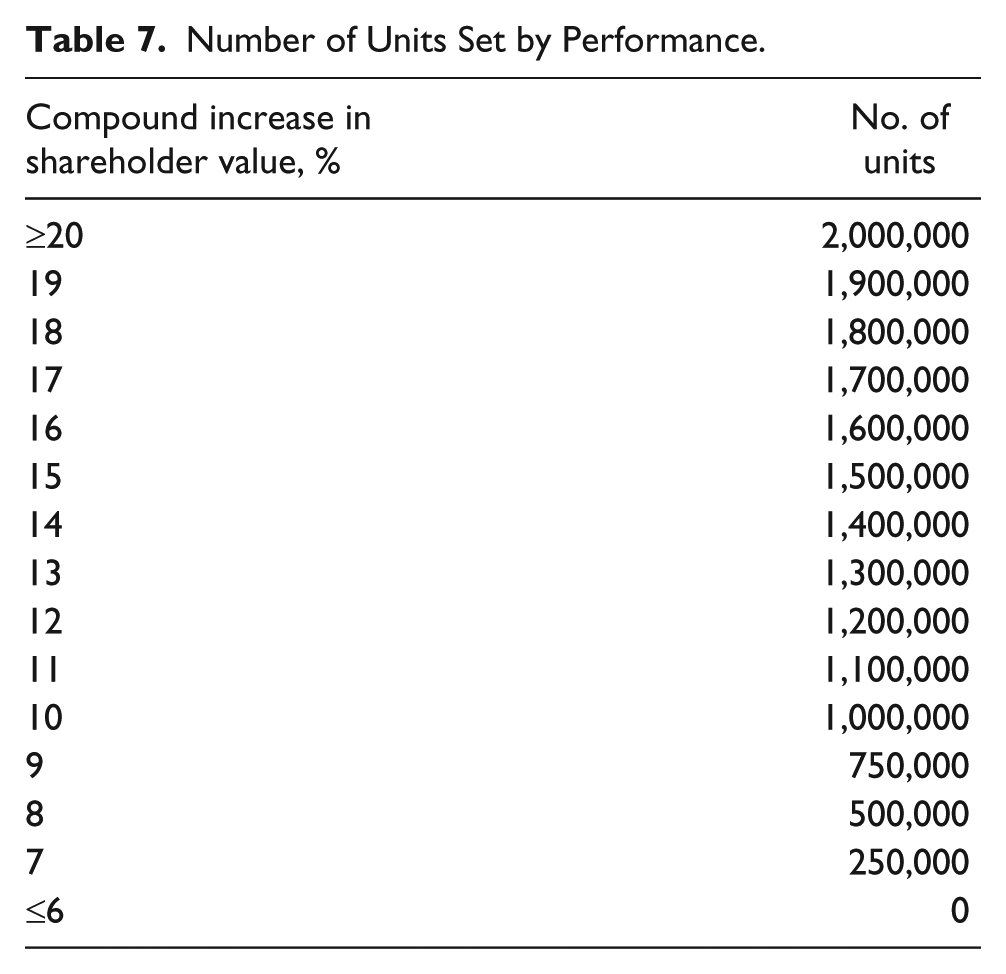

Variable number of units and fixed price per unit: The units shown in Table 7 are each worth $1. Again assuming a person in Grade 30, that would suggest that up to 2 million units (worth $2 million) could be earned. However, in this case it would probably be simpler to use the straight performance cash plan. Why go through the extra step of converting back to cash if the unit value does not vary? However, if the unit value was initially set equal to the company stock price and settlement is in shares of stock, then fixed-date grant accounting may be appropriate using one of the option pricing models. If settlement is in cash, then variable accounting will apply.

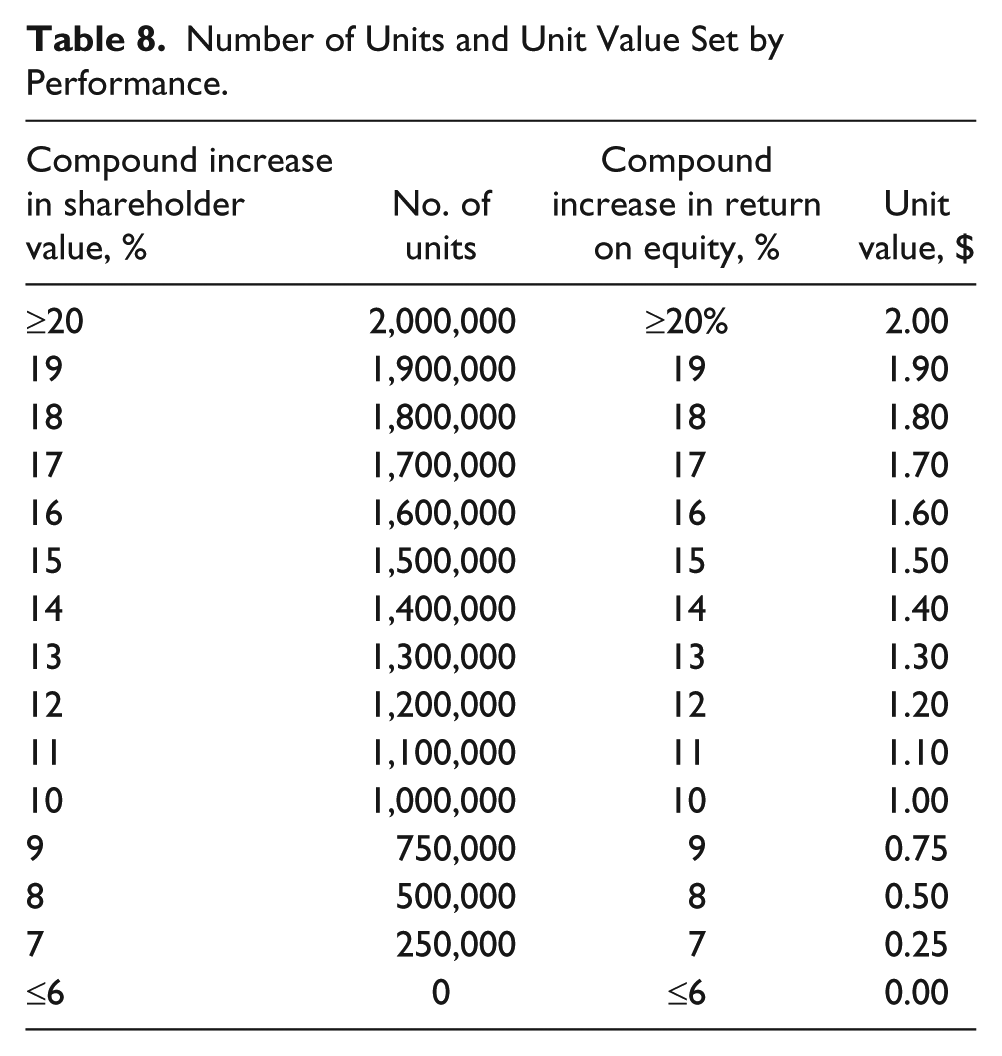

Variable number of units and variable price per unit: This variation is illustrated in Table 8.

Unit Value Set by Performance.

Number of Units Set by Performance.

Number of Units and Unit Value Set by Performance.

Thus, if the compound increase in shareholder value was 17% percent and the compound increase in ROE was 14%, the recipient would receive 1,700,000 units valued at $1.40 each, or $2,380,000.

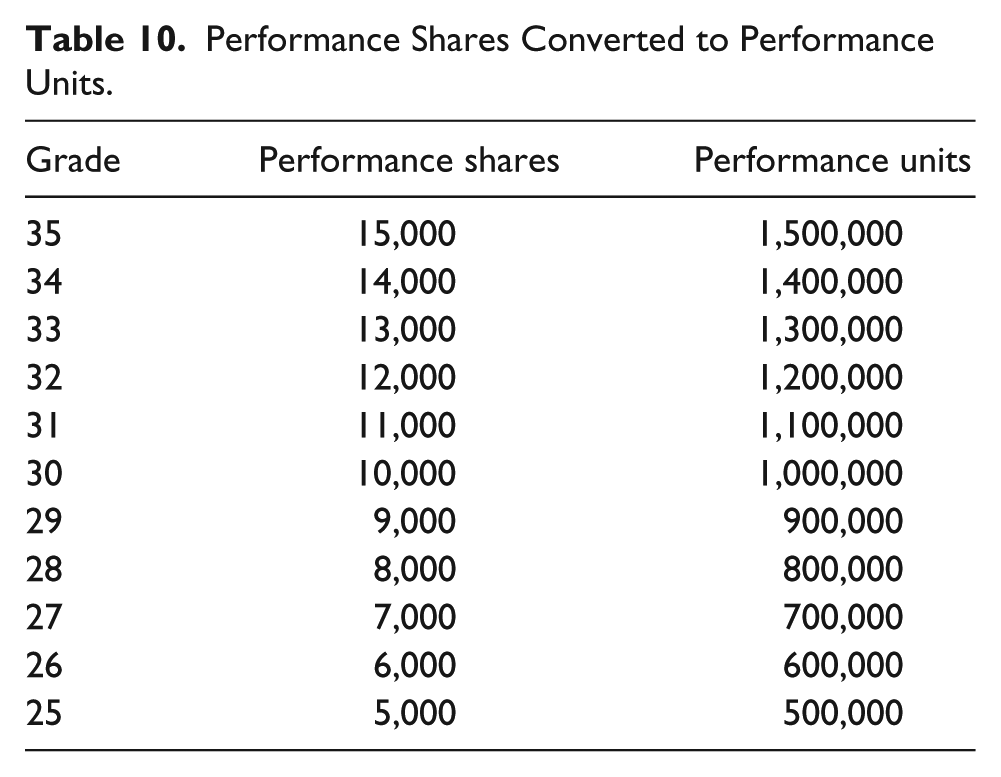

Conversely, a performance share plan could be converted into a performance unit plan, using the number of shares in Table 9 (valued at $100 a share). The result is seen in Table 10.

Stock Award Multiple by Grade Example.

Performance Shares Converted to Performance Units.

Because performance share plan costs have two variables (level of performance achieved and price of stock at time of payout), the performance unit plan quickly followed the performance share plan in the early 1970s, following the issuance of APB (Accounting Principles Board) Opinion 25. Performance unit plans only have one variable—performance. Price of company stock is not a factor. Under FAS (financial accounting standard) 123R this is a liability award with fair value accrued over the period of the plan and finalized on settlement date.

Performance Percentage Plans

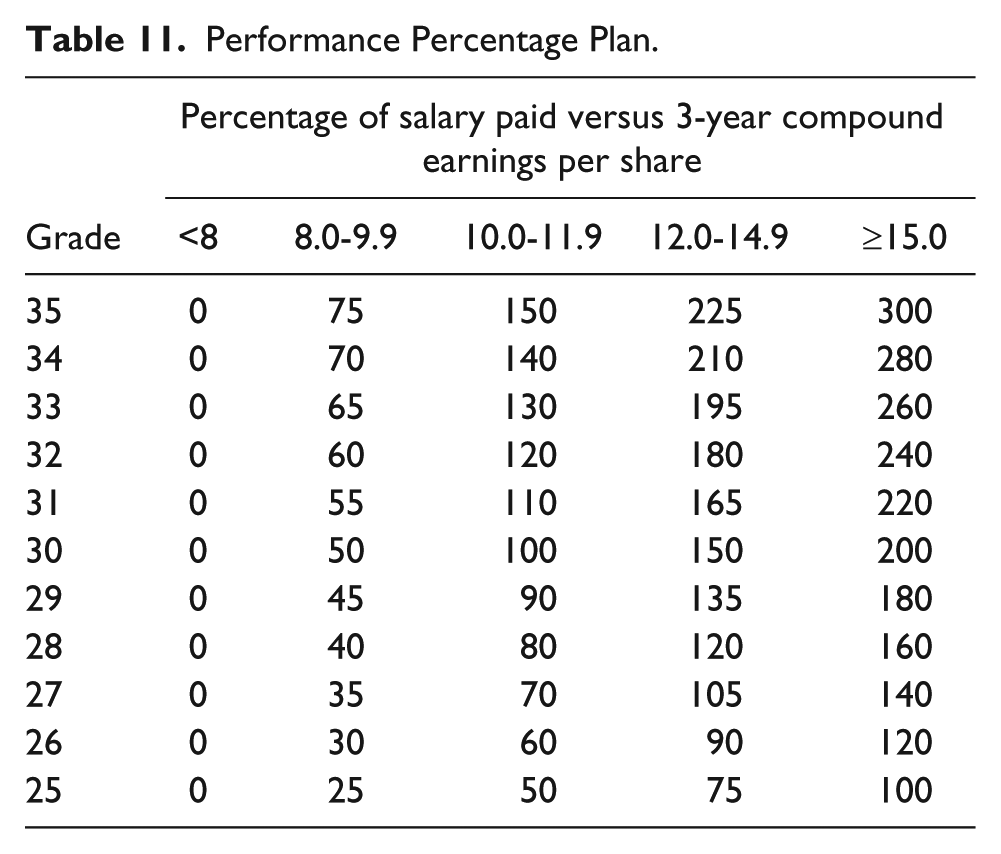

Another variation is the performance percentage plan. Here, rather than express the payout in cash or in units, the payout is typically expressed as a percentage of salary, although it could be of salary-plus-annual-incentive. An example is illustrated in Table 11.

Performance Percentage Plan.

Barring a desire to change the relationship of the long-term plan to salary (or salary-plusannual-incentives if included in the formula), there is no need to change the percentages annually. When salary is increased, the long-term payout will bear a constant relationship.

Accounting Treatment

It is important to remember that FAS 123R distinguished between equity awards and liability awards. Equity awards apply to awards settled in stock. The charge to earnings is calculated at grant date using a pricing model (e.g., Black–Scholes) and the fixed amount is accrued over the period of vesting.

Liability awards are paid in cash and the fair value is the actual value determined at settlement date. Until that date the charge is a variable accrual.

Tax Treatment

The company can take a tax deduction equal to the recipient’s income at time the income is received and the individual has taxable income in same amount of that date.

Advantages and Disadvantages of Cash Plans

The advantages of cash plans are as follows:

The executive has no financing issue, no money at risk and a tax liability only when the cash is received.

The company has a tax deduction, and the earnings charge is solely on performance; company stock value has no impact.

The disadvantages of cash plans are as follows:

The executive has neither an opportunity to share in the increase in stock price nor an opportunity for favorable long-term capital gains tax treatment.

The company has a variable charge to earnings and the tax deduction is deferred to a future date.

Summary

Phantom stock plans are typically used in private companies where market stock is unavailable; however, they can also be used in a division of a company with market stock.

While book value plans are the most common phantom stock plans for privately held companies, these can also include stock options, stock appreciation rights and stock awards. Any form of market-valued stock can be used in phantom stock plans. And if based on the private stock shares, it should be possible to achieve capital gains, otherwise all payments will be ordinary income.

Footnotes

Author’s Note

The material in this article is based on the author’s book The Complete Guide to Executive Compensation (3rd ed.) published by McGraw-Hill. The reader should not rely on accounting, tax, Securities and Exchange Commission or other professional service statements. One needs to seek appropriate professional counsel for such guidance.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Author Biography

![]() and elsewhere. Much of the material in this article has been taken from this book. Ellig served as worldwide head of human resources for Pfizer Inc. for the past 11 years of his 35 years with the company, where he also served as secretary to the board’s executive compensation committee. He is a member of the National Academy of Human Resources and the recipient of many lifetime achievement awards, including those from the Society for Human Resource Management and WorldatWork.

and elsewhere. Much of the material in this article has been taken from this book. Ellig served as worldwide head of human resources for Pfizer Inc. for the past 11 years of his 35 years with the company, where he also served as secretary to the board’s executive compensation committee. He is a member of the National Academy of Human Resources and the recipient of many lifetime achievement awards, including those from the Society for Human Resource Management and WorldatWork.