Abstract

There are hundreds of church-affiliated hospitals and other not-for-profit organizations that are exempt from ERISA’s funding and other requirements because they have IRS private letter rulings granting them church plan status. Many of them are seriously underfunded. Over the past few years, a number of class action lawsuits have been brought on behalf of participants challenging the validity of these exemptions and dismissing the authority of the private letter rulings. While the district courts have split on the issue, two appellate courts have ruled in favor of the participants and against the hospitals. The matter will ultimately be decided by the U.S. Supreme Court. This article is an analysis of this complex and important development.

Keywords

When the Employee Retirement Income Security Act of 1974 (ERISA) became law, it exempted from its coverage pension (and welfare) plans established and maintained by churches. In this context, “church” includes synagogues, mosques, and other houses of worship.

Church plans that covered employees of church-affiliated not-for-profit organizations were allowed to continue to do so through the end of 1982. After that, those employees were to have been shifted to plans covered by ERISA.

In 1980, Congress amended the law to allow church plans to continue to include employees of affiliated agencies. The General Counsel of the Internal Revenue Service (IRS) interpreted the 1980 amendments as allowing church-affiliated organizations to establish and maintain their own pension plans if sanctioned by an IRS private letter ruling (PLR). Over the years, the IRS issued hundreds of PLRs to hospitals, schools, colleges, universities and other not-for-profit organizations that claimed a church affiliation.

Beginning in 2013, a number of class action lawsuits were filed against hospitals that challenged the validity of the IRS’s interpretation of 1980 amendment and the PLRs. The district courts have split on the issue, some holding for the plaintiffs (participants) and some for the defendants (hospitals). Thus far, the Third, Seventh and Ninth Circuit Courts of Appeal have held for the plaintiffs. The issue will eventually be decided by the U.S. Supreme Court (or possibly the Congress).

This article examines the origins of the church plan exemption and its widespread extension to hospitals that have gained church-exempt status from the IRS and the current campaign to nullify this development. Our main focus will be pension plans sponsored by hospitals that, rightly or wrongly, have been exempted from ERISA. However, the resolution of this dispute will also apply to other employee benefits and other church-affiliated institutions.

ERISA

The Employee Retirement Income Security Act of 1974 (P.L. 93-406) governs pension and welfare plans in the private sector. It does not cover public sector (governmental) plans or church plans. ERISA established minimum standards for participation, vesting, funding, fiduciary responsibility and reporting and disclosure. The law was aimed most directly at traditional defined-benefit (DB) pension plans. It requires that they be operated solely in the interest of participants and beneficiaries.

ERISA established the Pension Benefit Guaranty Corporation (PBGC) to ensure the vested benefits of DB pension plan participants and beneficiaries. The PBGC is funded by insurance premiums paid by covered DB pension plan sponsors (employers).

ERISA, as amended, provides important protections to the participants and beneficiaries (surviving spouses) of covered pension plans. In particular, it requires that DB pension plans be prefunded. Originally, existing plans were allowed to amortize “unfunded actuarial accrued liability” (UAAL) for 40 years. New plans and improvements to existing plans had 30 years. Funding requirements have been strengthened several times over the years. Most recently, the Pension Protection Act of 2006 (P.L. 109-280) set the amortization period as 7 years. A finite amortization period for UAAL and a full funding requirement are the same thing.

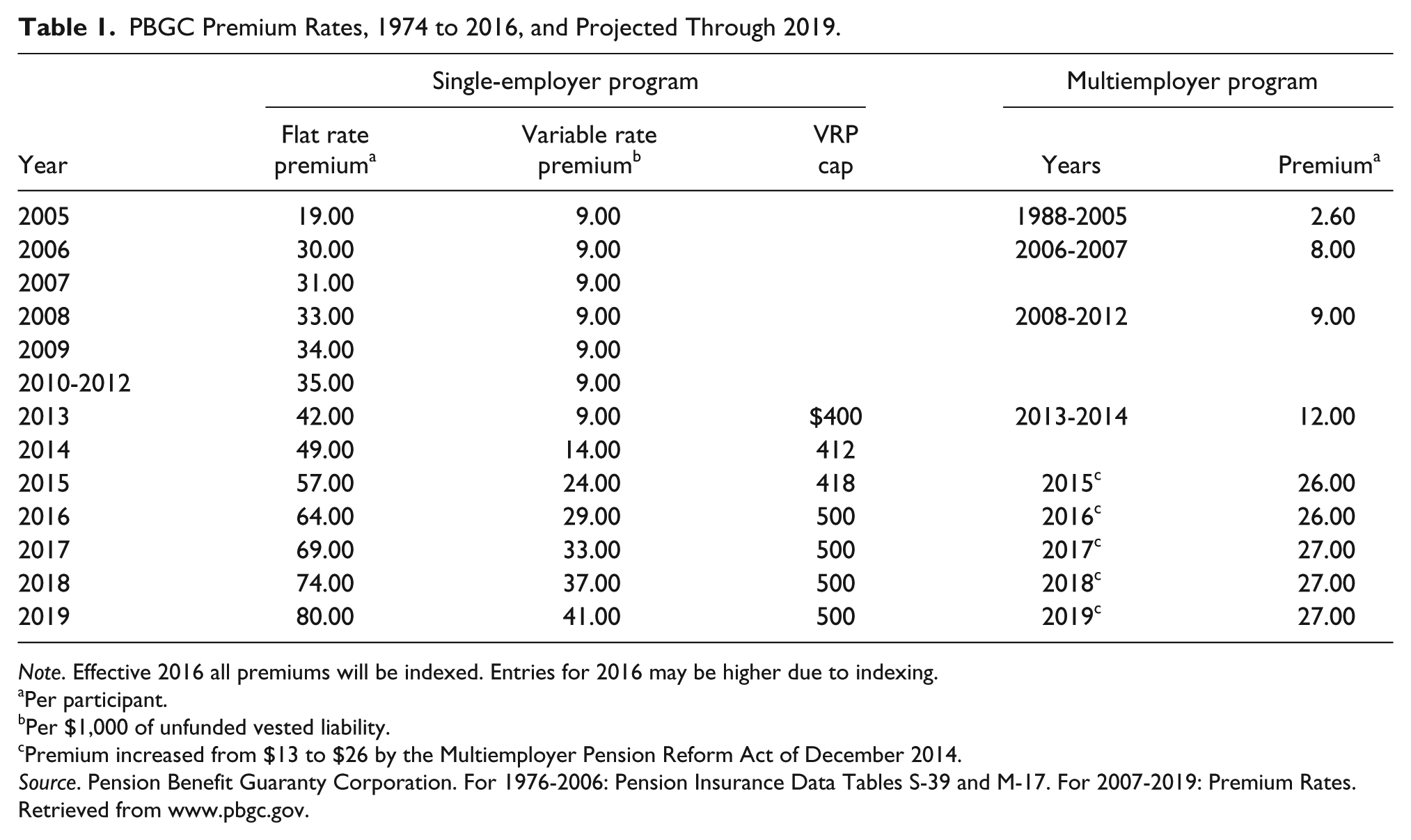

If a pension plan is exempted from ERISA, it is relieved from this full-funding obligation. It also does not have to pay PBGC insurance premiums, which, as indicated in Table 1, have increased considerably in recent years. As recently as 2012, the single-employer plan Flat Rate Premium was $35 per participant per year plus a Variable Rate Premium (VRP) of $9.00 per $1,000 of UAAL. As of 2016 the Flat Rate was $64 per participant and the VRP is $29 per $1,000 of UAAL to a maximum of $500 per participant. These rates were indexed and are projected to be $80 and $41, respectively, by 2019. The increasing costs of PBGC premiums have made church plan status more valuable to sponsors.

PBGC Premium Rates, 1974 to 2016, and Projected Through 2019.

Note. Effective 2016 all premiums will be indexed. Entries for 2016 may be higher due to indexing.

Per participant.

Per $1,000 of unfunded vested liability.

Premium increased from $13 to $26 by the Multiemployer Pension Reform Act of December 2014.

Source. Pension Benefit Guaranty Corporation. For 1976-2006: Pension Insurance Data Tables S-39 and M-17. For 2007-2019: Premium Rates. Retrieved from www.pbgc.gov.

ERISA also requires that pension plans provide significant information to participants through Supplementary Plan Descriptions, Supplementary Actuarial Reports and notifications whenever a substantive change is made. It also requires that they submit Form 5500s (Schedule R) to the Department of Labor, which shares them with the IRS and PBGC. Much of what we know about private sector benefit plans comes from Form 5500s. Since church-exempt plans are not required to report, we know very little about them. Perhaps for that reason, they are paid scant attention in the academic and professional journals.

Church and church-affiliated plans have been exempted from these and many other ERISA requirements and their companion provisions in the Internal Revenue Code (IRC). They are often seriously underfunded, which places their participants and beneficiaries at risk of losing their retirement benefits. Since their sponsors do not pay PBGC insurance premiums, the participants and beneficiaries do not have benefit protection when a plan fails or is terminated.

A church plan sponsor may make an irrevocable decision to be covered by ERISA. Some churches with 403(b) or other defined-contribution (DC) plans have done that to avoid state regulation. The “ERISA preemption” precludes states from enforcing state laws in such cases. That can be important for employers with multistate benefit programs. Few, if any, churches with defined-benefit pension plans have elected ERISA coverage. The IRS refers to church plans exempt from ERISA as “non-electing church plans.”

The 1980 Amendments

When ERISA was passed, many church pension plans covered the employees of affiliated not-for-profit organizations. The law allowed this practice to continue through December 31, 1982, for plans that were in existence on January 1, 1974. It was expected that church-affiliated entities would have established separate pension plans for their employees in compliance with the provisions of ERISA. That did not happen.

Churches were not happy with the “sunset provision.” Almost immediately after the passage of ERISA, 25 churches formed the Church Alliance for the Clarification of ERISA (now called the Church Alliance) and began to lobby Congress.

Congress responded with a provision in the Multiemployer Pension Plan Amendments Act of 1980 (P.L. 96-364; MPPAA). As its name implies, almost all of the MPPAA address problems with collectively bargained multiemployer pension plans. However, Section 407 (Church Plans) made permanent the temporary exception that was to have expired after 1982. It also eliminated the requirement that church-affiliated organization had to have been in existence on January 1, 1974.

The MPPAA amended ERISA’s Section 3(33) in two ways. One, plans that were established and maintained by a church could continue to cover employees of affiliated agencies. Two, plans that were maintained by a church-affiliated or -controlled organization whose principle purpose was the administration and funding of the pension plan could continue. 1

IRS General Counsel’s Memorandum

In 1983, the General Counsel of the IRS issued a memorandum interpreting the church plan provisions of the MPPAA (IRS General Counsel Memorandum 39007). The General Counsel’s analysis was based on the filings of two health care systems founded and operated by nuns. The memo’s conclusion was that a retirement plan covering the lay employees of a religious order whose main activity is the operation of nursing homes or hospitals, exempt from taxation under IRC Section 501, may be a church plan if the requirements of Section 414(e) are met.

Section 414(e) defines a church plan as one that has been established and maintained by a church or convention or association of churches that is exempt from taxation under IRC Section 501.

Memorandum 39007 paid little attention to legislative history or congressional intent other than to a reference by Senator Jacob Javits that he was very unhappy that the MPPAA would exempt “employees of schools and similar institutions which are church-related.” The General Counsel’s memorandum of 1983 was the authority upon which the IRS issued hundreds of private letter rulings to hospitals and other institutions that claimed a church affiliation.

Private Letter Rulings

A taxpayer can petition the IRS for a private letter ruling by filing Form 5300. Question 6C(1) of the form asks, “Is this a church plan under Section 414(e)?” A PLR is a written statement that interprets and applies federal tax laws to a specific fact situation before a transaction consummated. The ruling is binding on the IRS if the taxpayer fully and accurately described the transaction in the request and carries it out as described. The decision as to whether a plan is a church plan is made on a case-by-case basis by the IRS’s Employee Plan Technical Office.

PLRs are non-precedential and they may not be relied on by other taxpayers or IRS personnel in other situations. They are usually made available to the public after any information that could identify the recipient of the ruling is deleted.

Hundreds of PLRs have been issued mainly to hospitals that had previously operated as ERISA plans. Prior to 2012, the sponsors of pension plans that “churched up” were not required to inform the participants and beneficiaries that they were filing for the church plan exemption.

How Big Is the Problem?

We do not really know how many PLRs have been issued to church-affiliated not-for-profit organizations. However, when sponsors of formerly ERISA-covered pension plans receive a PLR affirming that they are “church plans,” they almost always request a rebate of the PBGC premiums paid by the plan over the last 6 years. That is the number of years that a sponsor must retain its records and may amend its insurance premium filings. 2 The 6-year reference for amending premium filings disappeared from the Premium Payment Instructions after 2013. The Pension Rights Center, a small not-for-profit organization in Washington, D.C. (that does wonderful work), gained access to PBGC premium rebates to formerly ERISA-covered pension plans that had gained church plan status from 1992 through 2007 and for 2013 under the Freedom of Information Act. 3

Due to mounting criticism, and especially that associated with the case of the Hospital Center at Orange, NJ (discussed below), the IRS placed a moratorium on church-affiliated conversion PLRs from 2007 through 2011. It resumed issuing PLRs in 2012 but now required sponsors to inform the participants that they were applying for an exemption from ERISA, what the possible consequences of that might be and that the participants and beneficiaries had a right to provided written testimony or appear at a hearing before the decision was made (IRS Rev. Proc. 2011-44).

As reported in Table 2, from 1992 through 2007 the PBGC paid premium rebates to 174 former ERISA-covered pension plans totaling $36,071,342. The average rebate was $207,307. The number of refunds, amounts refunded and the average refund varied widely from year to year.

PBGC Rebates of Insurance Premiums Paid by Pension Plans That Became Church Plans, 1992 to 2007 and 2013.

Source. Pension Benefit Guaranty Corporation. 1992-1998 and 2013: Table titled Church Plan Listing. 1999-2007: Table titled Church Plan Refunds Paid. Both obtained by the Pension Rights Center under Freedom of Information Act procedures. Retrieved from www.pensionrights.org/publications/fact-sheet/legislative-history-church-pension-plans.

Class Action Lawsuits

About 30 class action lawsuits have been brought over the last few years against hospitals exempted from ERISA by participants represented by two law firms: Cohen, Milstein, Sellers & Toll, PLLC of Washington, D.C., and Keller Rohrback, LLP of Seattle. The suits in several District Courts are at different stages of resolution. Several are stayed awaiting a decision from an Appellate Court. Until about 2011, the courts had never closely examined the church-affiliated exemption. 4

As of August 2016, the Third Circuit (New Jersey and Pennsylvania), the Seventh Circuit (Illinois, Indiana and Wisconsin) and the Ninth Circuit (seven western states plus Alaska and Hawaii) have ruled in favor of the plaintiffs (participants). They held that the hospitals involved were not entitled to a church plan exemption. All of the important cases have involved large hospital systems.

Hospital Consolidation

The challenge to the church-exempt status of church-affiliated hospitals is not taking place against a stable backdrop. There is an interesting coincidence in the timing of class action law suits and the consolidation of hospital systems in the United States due in large part to the Patient Protection and Affordable Care Act in 2010 (P. L. 111-148; ACA).

The ACA contains a number of cost-reduction provisions, including the Accountable Care Organizations that tie payments to hospitals to quality of care rather than the quantity. The economies of scale and increased specialization allowed by such consolidation are supposed to result in better service at reduced costs. However, the increased volume of mergers and acquisitions (M&A) in the hospital industry has reduced competition in many markets and seems to be having the opposite effect.

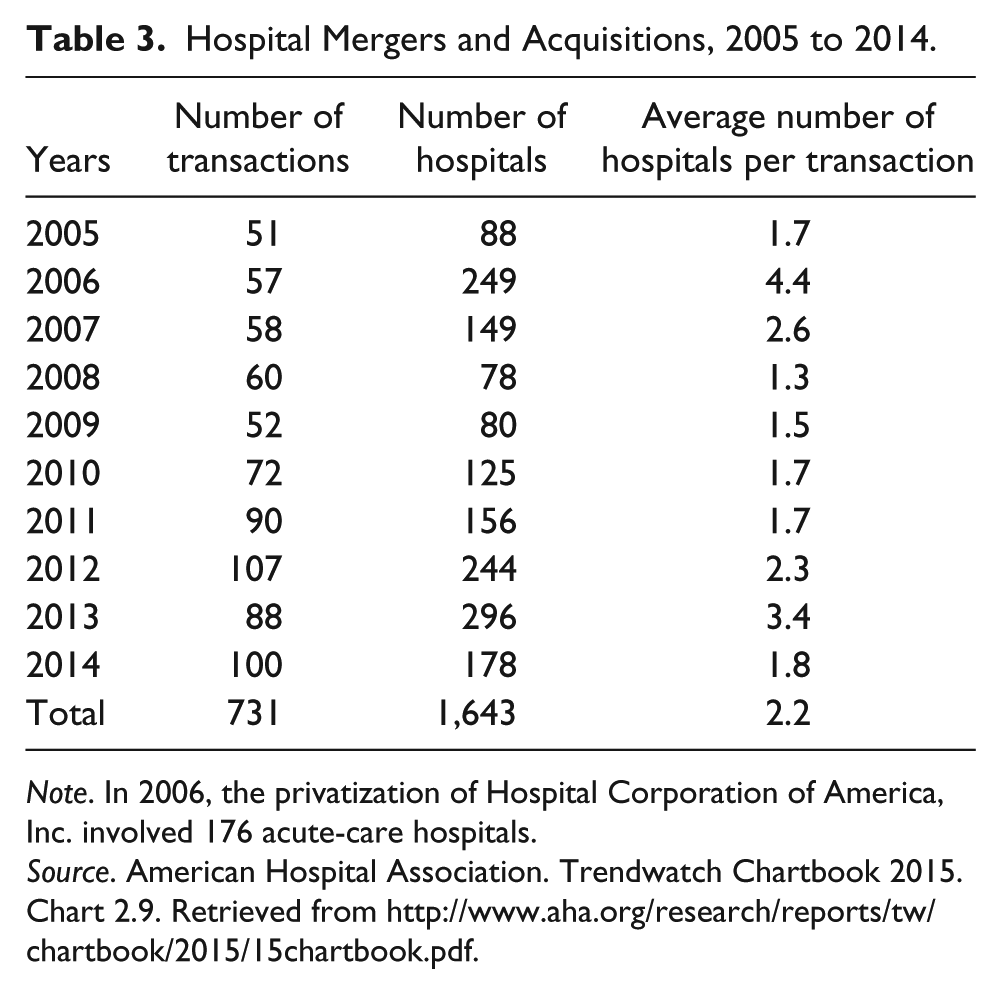

Table 3 reports the number of hospital M&A transactions from 2005 through 2014. Over the 10-year period, there were 731 transactions involving 1,643 hospitals. Note how the volume of M&A activity increased beginning in 2010, the year the ACA was passed.

Hospital Mergers and Acquisitions, 2005 to 2014.

Note. In 2006, the privatization of Hospital Corporation of America, Inc. involved 176 acute-care hospitals.

Source. American Hospital Association. Trendwatch Chartbook 2015. Chart 2.9. Retrieved from http://www.aha.org/research/reports/tw/chartbook/2015/15chartbook.pdf.

The consolidations include mergers and acquisitions of hospitals and groups of hospitals and other health care providers such as physician practices. The movement includes the renaming and restructuring of formerly church-affiliated hospital groups into large church and secular hospitals conglomerates. This has changed the hospital landscape throughout the United States.

The Hospital Center at Orange

A particularly egregious example of a church-affiliated organization abusing the ERISA church exemption involved the Hospital Center at Orange, New Jersey. The Hospital Center at Orange had been a secular hospital for over 100 years and its pension plan had been covered by ERISA since 1974. In 1998, Cathedral Health Systems, a corporation owned by the Archdiocese of Newark, acquired the Health Center at Orange. Four years later it filed for a church exemption from ERISA, which was approved by the IRS in 2003. In 2004, the Hospital Center at Orange shut down. Its pension plan had 800 participants and beneficiaries, an unfunded liability of $30 million and enough assets to continue to pay benefits for only 9 months.

The pension benefits were eventually rescued when a smart and determined nurse, with a background in financial advising, got the story to some high-ranking federal officials. The IRS was persuaded to withdraw its PLR approval and the PBGC agreed to guarantee the pension benefits. 5 Based on a review of the source documents to Table 2, Cathedral Health Systems did not request a refund of the PBGC premiums paid by Health Center at Orange (or if it did, the request was not approved).

While this story had somewhat of a happy ending, it may be unique. The PBGC does not have the funds to bail out other troubled church-affiliated plans. It has its own financial problems. Moreover, to use funds that are the result of premiums paid by other pension plan sponsors to pay the benefits of plans that have “churched up”—especially if they have received a rebate of 6 years of PBGC premiums—would be patently unfair and probably illegal.

Saint Peters’ Healthcare System

The first case to be decided by an Appellate Court was Kaplan v. Saint Peters’ Healthcare System (SPHS). The main component of SPHS is Saint Peter’s University Hospital founded in New Brunswick, NJ, in 1907 and was sponsored by the Roman Catholic Diocese of Metuchen, NJ. It now has 2,800 employees and 1,900 retirees.

The District Court of New Jersey held that the SPHS pension plan was not a church plan because it had not been established by a church. The Third Circuit Court of Appeals agreed and went on to say that the legislative history clearly showed that Congress intended that the church exemption should be narrowly applied. It also said that the IRS’s private letter ruling could not be given deference because it conflicts with the clear wording of the statute and was unreasonable, conclusionary, lacking in statutory analysis and issued in a non-adversarial setting based on information provided solely by SPHS. 6

Effective January 1, 2013, SPHS replaced its DB pension plan with a TIAA-CREF defined contribution plan (probably a 403(b) plan). The defined benefit plan was “frozen.” Participants with vested benefits would be allowed to retain them (as required by ERISA). However, unless the participant was close to retirement age, those benefits would be eroded by inflation and wage growth. This may herald what other hospitals will do if they lose their church-exemption status.

Advocate Health Care Network

Advocate Health Care Network (Advocate) is the result of a complex series of mergers and acquisitions going back to 1897. They involved the Norwegian Lutherans, the German Lutherans, Church of Christ and a Masonic hospital. Advocate is now the largest hospital system in Illinois with 12 acute care hospitals and 250 “cites of care.” It has 28,700 employees.

Stapleton v. Advocate Health Care Network presented a similar fact situation to SPHS. Advocate was first reviewed by the U.S. District Court for Northern Illinois, which ruled that the pension plan at issue was not a church plan because it was not established by a church. It had been established by a predecessor of Advocate that was not a church. On an interlocutory appeal, the Seventh Circuit Court of Appeals agreed with the lower court. It, too, was dismissive of the IRS private letter ruling.

Dignity Health

In January 2012, Catholic Health West (formed in 1986) changed its name to Dignity Health and restructured itself into a conglomerate of Catholic and secular hospitals. It is now the fifth largest health care system in the United States and the largest in California. Dignity Health operates 40 hospitals (24 Catholic and 16 non-Catholic) in three states (Arizona, California and Nevada) plus 150 continuing-care locations. It has 60,000 employees (and 10,000 doctors).

In 2013, in Rollins v. Dignity Health, the District Court for Northern California held that Dignity Health’s pension plan was not a church plan because it was not established by a church. The judge excoriated the IRS General Council for the three additional PLRs given to Dignity Health’s predecessor, Catholic Health West, in 1995, 1997 and 2000. 7 The decision was appealed to the Ninth Circuit Court of Appeals in November 2014. In July 2016, the Ninth Circuit joined the Third and Seventh Circuit Courts in holding that Dignity Health’s pension plan was not a church plan.

Trinity Health

In a parallel development with a different outcome, Catholic Health East (organized in 1998) joined Trinity Health (a larger Catholic church-related group) in 2013. The expanded Trinity Health now operates 90 hospitals and 126 continuing-care locations in 21states. It has 95,000 employees. 8 The hospital conglomerate has a UAAL of $600 million.

In a lawsuit, Lann v. Trinity Health Corporation, filed in the District Court of Maryland in 2014 Greenbelt Division, plaintiffs (participants) claimed that none of Trinity Health’s pension plans were established by a church and were therefore in violation of ERISA on several counts. Defendants (Trinity Health) argued that it was an organization “controlled by or associated with a church or convention of churches” and was therefore permitted to establish a church plan under ERISA Section 3(33). The District Court ruled partially in favor of Trinity Health’s motion to dismiss in 2015. Trinity filed a second motion to (fully) dismiss. Oral argument was heard October 19, 2015. No final decision has been handed down yet. 9

Consequences of Losing Church-Exemption Status

Having a church plan exemption from ERISA provides a hospital or hospital system with a competitive advantage over those without an exemption. ERISA’s participation, vesting, funding and reporting and disclosure requirements significantly increase the cost of sponsoring a DB pension plan. In addition, sponsors have to pay the substantial and ever-increasing PBGC insurance premiums depicted in Table 1.

If the Supreme Court eventually agrees with the Third, Seventh and Ninth Circuits and holds that church-affiliated not-for-profit organizations cannot establish and maintain a church pension plan, the consequences will be dire for the sponsors of many such plans nationwide. Many of the plans are underfunded to the extent of tens of millions or hundreds of million dollars (by ERISA standards). If special arrangements are not made, the hospitals will have to pump huge sums of money into the trust funds over the subsequent few years.

PBGC insurance premiums are another matter. Newly ERISA covered or re-covered DB pension plans will have to start or resume paying PBGC premiums. However, there are two related questions that (to my knowledge) have not been addressed. One is that, if a plan has applied for and received a rebate of 6 years of its premiums, will it have to repay that amount to the PBGC? The other is that, if a plan stopped paying PBGC premiums, say, 20 years ago, will it have to make up those payments retroactively?

In addition to the funding and contribution and the PBGC premium payments, there are other potential costs to plans that lose their church exemption. They include having to offer a joint survivor option, nondiscrimination testing, reporting and disclosure costs, and ERISA’s participation and vesting requirements. However, they need not detain us. Suffice it to say that when they are added to the ERISA funding requirements and the PBGC premium reconciliation, many church-affiliated DB pension plans will have a mess on their hands. What will they do?

Many small and rural hospitals have already closed as a result of the Affordable Care Act. Others will follow. For those that remain, the additional burden of increased required contributions to the pension plan will exacerbate the problem.

Large urban hospitals and hospital systems will have more options. One of them is to pay the cost associated with the ERISA funding requirements and the PBGC premiums. The sponsors’ ability to do that will vary depending on its market position (ability to pass costs on to its customers), how underfunded the plan is and how long they have enjoyed a church exemption. Many will follow the Saint Peters Healthcare Systems example mentioned above and “freeze” their DB plan and adopt a defined-contribution 401(k), 403(b) or 457(b) plan to the detriment of existing long service employees. That would be consistent with the recent corporate development known as “de-risking.”

Conclusion

Given the large number of participants and beneficiaries involved in the several class action lawsuits, the disagreements among the District Courts and the decisions handed down by the Third, Seventh and Ninth Circuit Courts of Appeal, it is all but certain that the matter will be determined by the U.S. Supreme Court.

It is likely that the Supreme Court will rule in favor of the participants and beneficiaries and that church-affiliated not-for-profit hospitals are not entitled to establish and maintain ERISA exempt pension plans. If so, many of the hospitals affected will have a real mess on their hands. Many of them are woefully underfunded and will have to greatly increase their contributions. They will also have to begin making PBGC premium payments and possibly repay premium rebates received and make up past unpaid premiums. That may result in some bankruptcies or the freezing of traditional defined-benefit pension plans and their replacement with some form of defined-contribution plan, as was done by Saint Peter’s Healthcare System.

While this will operate to the disadvantage of many long-service hospital workers, it will also provide them with the protections of ERISA, including safer and better funded pension plans. It will also provide them with PBGC insurance for their DB vested benefits, but not for those in the replacement DC plans.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.