Abstract

There have been a number of class action lawsuits filed against Section 403(b) retirement plans sponsored by prominent private sector universities alleging breaches of fiduciary responsibility and other failures prompted by new Internal Revenue Service regulations issued in 2007 under the Employee Retirement Income Security Act of 1974. More recently, the California State University 403(b) plan has been targeted for a class action lawsuit under state law. This article examines Section 403(b) plans, Internal Revenue Service and Department of Labor regulations and employer responses to the new rules. The consequences of these lawsuits could be immense.

Keywords

There has been a rash of class action lawsuits filed against prominent private sector not-for-profit university Section 403(b) retirement plans. Plaintiffs claim that the universities have failed in their fiduciary duties under the Employee Retirement Income Security Act of 1974 (Pub. L. 93-406; ERISA). This article examines Section 403(b) plans, ERISA, recent Internal Revenue Service (IRS) and Department of Labor (DOL) regulations and guidance and employer response to the new rules. It also explores a more recent development of an impending class action lawsuit against the California State University’s (CSU) 403(b) plan under California state law.

The stakes are high. If plaintiffs prevail under ERISA, it will open the floodgates of litigation against hundreds of less prominent universities, private K-12 schools, not-for-profit hospitals and other 501(c)(3) charitable organizations. If they prevail in the CSU suit, it will spread to other public sector entities in California and to public employers in other states.

Section 403(b) Plans

Section 403(b) was added to the Internal Revenue Code (IRC or Code) by the Technical Amendments Act of 1958 (Pub. L. 85-866). The IRS published regulations in 1964. 1 However, the concept has been in the tax code since 1942 and its roots go back to the early 20th century. When Andrew Carnegie served as a trustee of Cornell University (1890-1905), he established a retirement program for university faculty members. In 1918, the Carnegie Foundation created the Teacher Insurance and Annuity Association, subsequently the first half of TIAA-CREF, now the largest provider of 403(b) plans. 2 In 2016, TIAA-CREF changed its name to “TIAA.”

Sections 401(k) and 457(b) were added to the Code 20 years later by the Revenue Act of 1978 (Pub. L. 96-600), though a number of similar plans already existed under private-letter rulings from the IRS.

The 1958 legislation allowed participants in 403(b) plans to invest only in tax-sheltered annuities (TSA) marketed by insurance companies. They are now referred to as 403(b)(1) accounts. In 1974, the ERISA added Section 403(b)(7) to the Code. It allows participants in 403(b) plans to establish custodial accounts and invest in registered mutual funds.

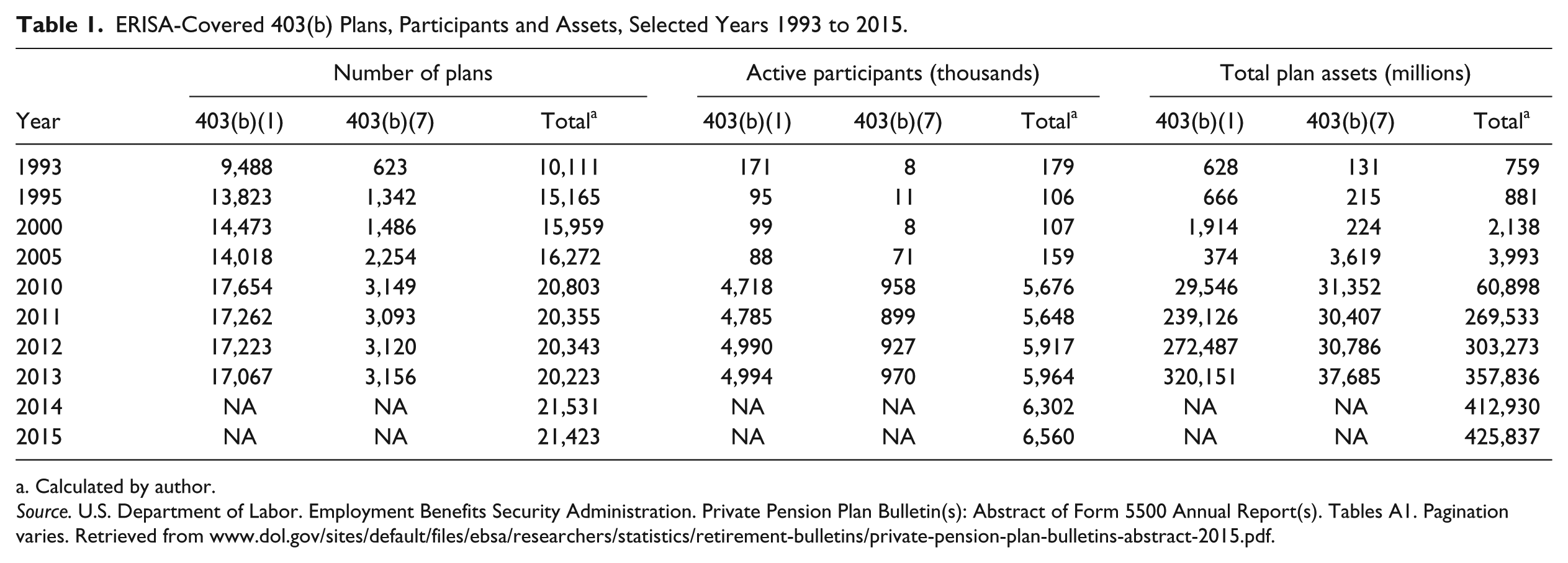

Table 1 reports the number of 403(b)(1) TSA, 403(b)(7) custodial accounts and their totals for selected years 1993 through 2013 (and totals only for 2014 and 2015). There have always been significantly more 403(b)(1) TSA accounts than 403(b)(7) custodial accounts. The same applies to active participants and total assets.

ERISA-Covered 403(b) Plans, Participants and Assets, Selected Years 1993 to 2015.

Calculated by author.

Source. U.S. Department of Labor. Employment Benefits Security Administration. Private Pension Plan Bulletin(s): Abstract of Form 5500 Annual Report(s). Tables A1. Pagination varies. Retrieved from www.dol.gov/sites/default/files/ebsa/researchers/statistics/retirement-bulletins/private-pension-plan-bulletins-abstract-2015.pdf.

In 1984, the Retirement Equity Act (Pub. L. 98-397) added Section 403(b)(9) to the Code. It allows qualified church organizations and affiliated church organizations to sponsor “retirement income accounts” in addition to 403(b)(1) and 403(b)(7) accounts. Section 403(b)(9) allows ministers, who typically reside in church-provided housing throughout their careers, to have a tax-free designated housing allowance when they retire. Self-employed “ministers” are also eligible to participate if their denomination sponsors such a plan. The term affiliated church organizations includes synagogues, mosques, temples, and related schools operated by them.

Section 403(b) plans are required to have “universal availability” for all common law employees. If the employer allows any employee to participate, it must allow all employees in the same class to participate. The only employees who may be excluded are those who work less than 20 hours per week (1,000 hours per year), students performing certain services, employees covered under another plan and nonresident aliens. The employer must notify employees of their eligibility to participate at least once per year. 3

Defined Contribution Plans: Who Can Do What

Section 403(b) plans may be sponsored by public sector education (K-12, colleges and universities), research institutions, not-for-profit hospitals and other health care providers; 501(c)(3) tax-exempt charitable organizations; church and church-related organizations and Indian Tribal Governments if the plan was established before 1995.

Section 401(k) plans may be sponsored by private sector employers. They may also be sponsored by state and local governments if the plan was established prior to May 6, 1986, and has continued since then. Since 1997, 401(k) plans may also be sponsored by certain not-for-profit organizations (NPO).

Section 457(b) plans have been available to state and local governments since 1978. In 1986, the deferred compensation plans of certain tax-exempt NPOs became covered by Section 457.

There are also a number of defined-contribution pension plans that are available to small employers. The specifics are complicated and lie beyond our immediate interest.

At one time, 403(b), 401(k) and 457(b) plans were quite different reflecting their different origins and separate developments. They are now almost identical.

Elective Deferrals Catch-Ups and Employer Matching Contributions

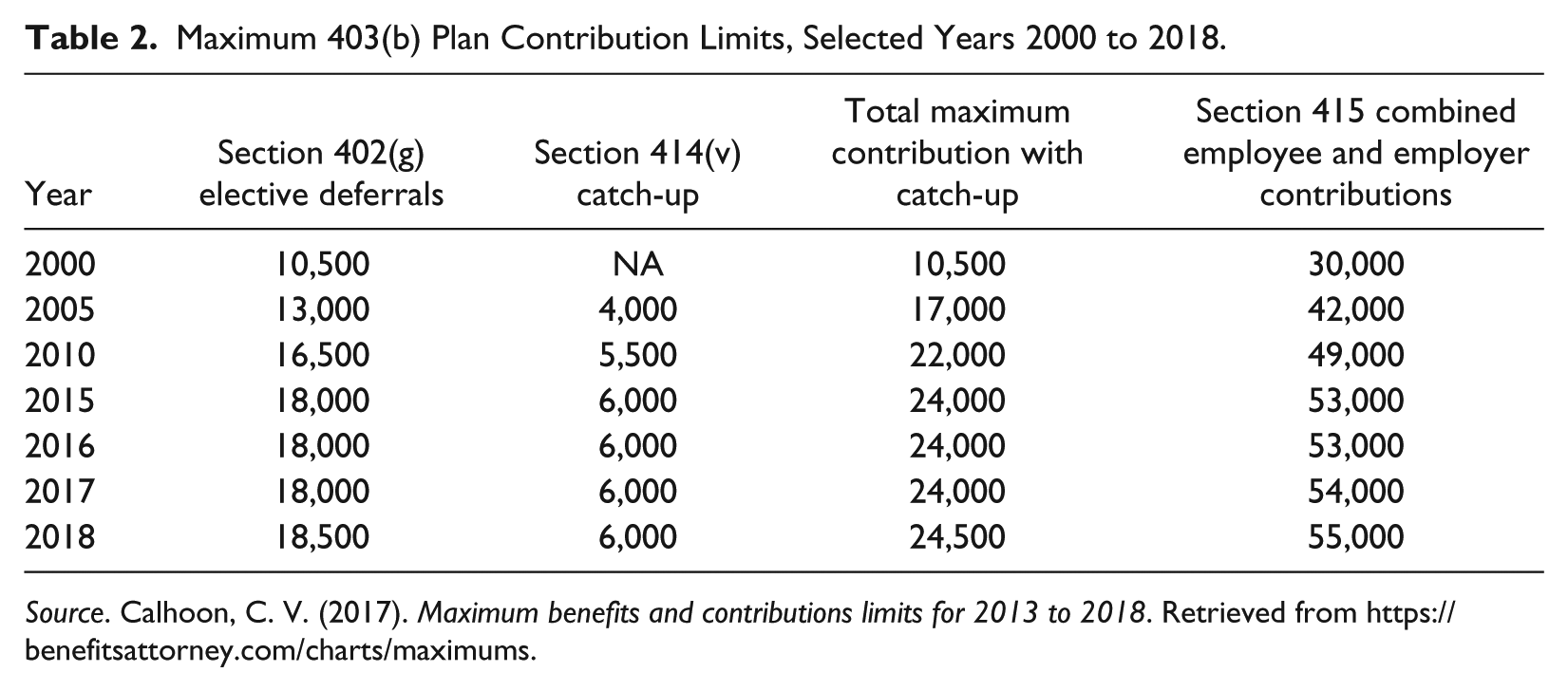

Section 402(g) of the IRC limits the maximum “elective deferral” (employee contribution) to a 403(b), 401(k) or 457(b) plan. For 2018, it is $18,500 (indexed). Section 415 limits the maximum combined participant and employer matching contribution to $55,000 (indexed).

Employees aged 50 years or older are allowed to make an additional $6,000 “catch-up” contribution under Section 414(v) of the Code. Table 2 displays the contribution limits for defined-contribution plans for selected years 2000 through 2018.

Maximum 403(b) Plan Contribution Limits, Selected Years 2000 to 2018.

Source. Calhoon, C. V. (2017). Maximum benefits and contributions limits for 2013 to 2018. Retrieved from https://benefitsattorney.com/charts/maximums.

One of the remaining distinctions of 403(b) plans is that participants who have been in the plan (with the same employer) for at least 15 years may contribute up to an additional $3,000 per year for a total of $15,000 (not indexed). If the employee is eligible for both catch-up provisions, the 15-year catch up must be used first.

Some public sector universities and not-for-profit hospitals may offer their employees a choice of 403(b), 401(k) and/or 457(b) plans. Contributions to 403(b) and 401(k) plans must be coordinated. Contributions to a 403(b) or 401(k) and a 457(b) plan do not. If an employee is enrolled in a 403(b) and a 401(k) plan, the combined contributions are subject to the 402(g) limit of $18,500 and the Section 415 limit of $55,000. If, however, he or she is enrolled in a 403(b) or 401(k) and a 457(b) plan, those limits apply to plan separately. That would allow a total elective deferral of $37,000 and a combined employee and employer contribution of $110,000 not counting catch-ups. The logic of this escapes me. Was it a congressional oversight?

How Many 403(b) Plans Are There?

Most of what we know about retirement and other benefit programs comes from the ERISA-required Form 5500s that plan sponsors file annually with the DOL (which shares them with the IRS). Thus, we know a lot about ERISA-covered 403(b) plans. However, we know relatively little about non-ERISA plans sponsored by state and local governments (exempted from ERISA) and those plans sponsored by charitable NPOs exempt from ERISA Title I requirements if they are compliant with the 1979 DOL safe harbor rules (discussed below).

As reported in Table 1, over the period 1993 through 2015, total ERISA-covered 403(b) plans more than doubled from 10,111 to 21,423. The number of active participants increased from 179,000 to 6.6 million. Total assets increased from $759 million to $426 billion. As impressive as these data are, they do not include the large number of non-ERISA 403(b) plans.

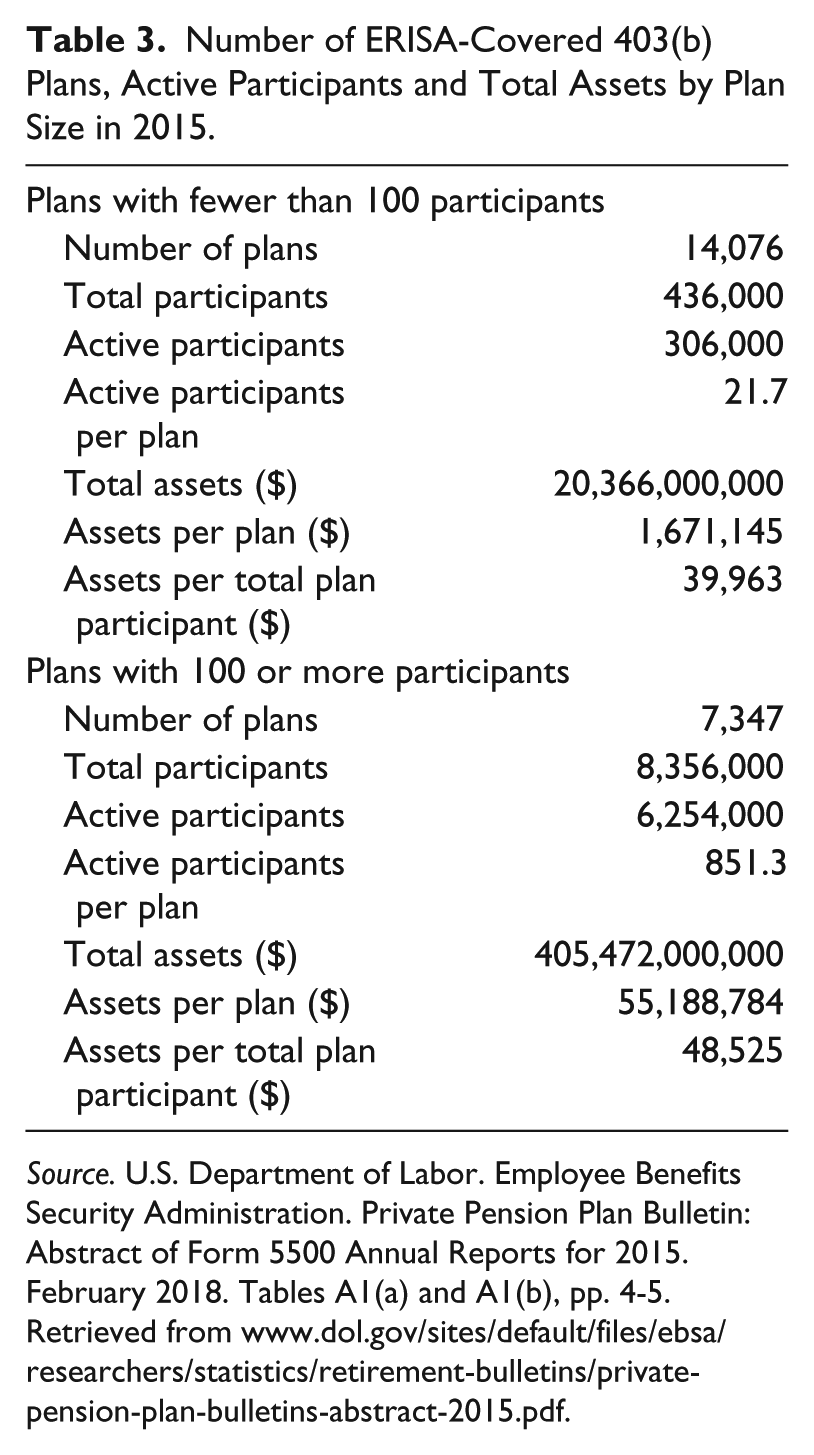

There are interesting differences between small (less than 100 participants) and large (100 or more participants) ERISA-covered 403(b) plans. Table 3 shows 403(b) plans by plan size for 2015. There are twice as many ERISA-covered small plans as there are large plans: 14,076 compared with 7,347. However, the total number of participants in small plans was only 436,000 compared with 8.4 million in large plans. The number of active participants in small plans was 306,000 compared with 6.3 million in large plans. The average number of active participants in small plans was 21.7 compared with 851.3 in large plans.

Number of ERISA-Covered 403(b) Plans, Active Participants and Total Assets by Plan Size in 2015.

Source. U.S. Department of Labor. Employee Benefits Security Administration. Private Pension Plan Bulletin: Abstract of Form 5500 Annual Reports for 2015. February 2018. Tables A1(a) and A1(b), pp. 4-5. Retrieved from www.dol.gov/sites/default/files/ebsa/researchers/statistics/retirement-bulletins/private-pension-plan-bulletins-abstract-2015.pdf.

There was also a huge difference in the assets held. Total assets held by small plans was $20.4 billion compared with $405.5 billion in large plans. The average small plan had $1,671,145 ($1.7 million) in assets in 2015 compared with $55,188,784 ($55.2 million) for large plans. The average size of participant accounts in small plans was $39,963 compared with $48,525 for large plans.

These larger plans would include the university 403(b) plans being sued under ERISA’s fiduciary provisions discussed below.

What we do not have aggregate data on are the large number of state and local government 403(b) plans and other non-ERISA plans sponsored by charitable NPOs under the DOL’s “safe harbor” regulations. However, the Investment Company Institute (ICI) reports that there is $0.9 trillion ($900 billion) in 403(b) plans, 43% in plans covered by ERISA and 57% are in non-ERISA plans. 4 This allows us to infer that ERISA-covered 403(b) plans have roughly $387 billion in assets and non-ERISA plans have $513 billion in assets ($900,000,000,000 × 0.57).

Regulations

If a 403(b) plan is covered by ERISA, it must meet minimum standards of Title I of the act. They include an annual filings of Form 5500, actuarial reviews and nondiscrimination testing. Discrimination in this context means favoring “highly compensated employees” defined as anyone earning $120,000 in 2018 (indexed) or a 5% or more owners on the firm.

ERISA-covered 403(b) plans are sponsored by private sector NPOs (including universities), the overwhelming majority of which involve an employer matching contribution. Non-ERISA 403(b) plans are sponsored by state and local governments (exempt from ERISA) and some NPOs that do not have employer matching contributions.

Until recently, non-ERISA 403(b) plans were a regulatory “backwater,” albeit a large backwater. As mentioned, Section 403(b) was added to the IRC in 1958. The IRS published regulations in 1964. 5 The DOL issues 403(b) “safe harbor” regulations in 1979. 6 They provided that if a 403(b) plan was funded entirely by elective deferrals; was completely voluntary to the employee; rights under the plan enforceable only by the participants, beneficiary or their representative; the employer received no consideration or compensation and that the employer exercised minimal administrative involvement, the plan would maintain its non-ERISA status.

The IRS issued proposed 403(b) plan regulations in 2004, 40 years after the 1964 regulations. New final regulations were issued in 2007, effective January 1, 2009. 7 They required that all 403(b) plans be in writing and established that plan sponsors (employers) were fiduciaries responsible for administering their plans, including the selection and monitoring investment choices and record keeping services.

This presented non-ERISA 403(b) plans, which had been operating under the “minimal involvement” principle of the DOL’s 1979 “safe harbor” regulations, with a problem. It was feared that if a sponsor took any of the actions required by the new IRS regulations, it could invalidate the plan’s safe harbor status and subject the plan to ERISA’s fiduciary reporting and testing requirements.

In conjunction with the new IRS regulations, the DOL issued Field Assistance Bulletin (FAB) 2007-02 addressing the impact of the IRS final regulations on the DOL’s safe harbor regulations. FAB 2007-02 provided that if a 403(b) plan was funded solely by elective deferrals, the following actions would not cause the plan to lose its safe harbor status due to (1) conducting administrative reviews of plan structure and operations for tax compliance purposes; (2) discrimination testing to determine maximum contributions; (3) fashioning and proposing corrections of operational failures; (4) developing improvements in administrative processes to avoid recurrence of tax defects; (5) obtaining the cooperation of entities to correct tax defects; (6) keeping records of its activities; (7) terminating the 403(b) plan in accordance with IRS regulations; (8) certifying to an annuity provider factual information such as participant addresses, service records and compensation and/or (9) limiting the funding methods and products available to employees to a reasonable number of investment choices. 8

Remedial Amendment Period

The 2007 IRS final regulations required profound changes in the sponsorship of non-ERISA 403(b) plans. Historically, plan sponsors were not even required to maintain written plan documents. The annuity contracts and custodial agreements were between the investment providers and the participants. The issuance of the 2007 final regulations and the related DOL safe harbor guidance required important amendments to non-ERISA 403(b) plans. However, since the IRS provided no guidance for 6 years, plan sponsors had to make revisions by interpreting the 2007 final IRS regulations and DOL’s FAB 2007-02 on a “best-guess” basis.

The IRS announced the beginning of the “remedial amendment period” (RAP) as January 1, 2010, and said that it would announce the end of the RAP at a future date. It was not until 2017 that it specified the end of the RAP as March 31, 2020, in Revenue Procedure 2017-18. 9

University Class Action Lawsuits

The new regulatory situations presented class action law firms with a huge opportunity. Beginning in 2006, Schlichter Bogard & Denton had made tens of millions of dollars in contingency fees and expenses suing private sector sponsors of 401(k) plans under ERISA beginning in 2006. 10 It now turned its attention to private sector universities.

In 2016, Schlichter Bogard & Denton filed class action lawsuits against 12 prominent universities that sponsored large 403(b) plans: Columbia, Cornell, Duke, Emory, Johns Hopkins, MIT, NYU, Northwestern, University of Pennsylvania, University of Southern California, Vanderbilt and Yale. Since then at least four additional suits have been brought against other universities by other law firms: Brown, Princeton, Chicago and Washington University.

All of the lawsuits are similar. They allege breaches of fiduciary duties by allowing excessive fees for administrative and investment services, imprudent selection and monitoring of investment options, allowing multiple record keepers and offering a confusing array of investment options.

As of this writing (May 2018), none of these cases has been settled or gone to trial. The University of Pennsylvania and the Northwestern University cases have been dismissed, the latter “with prejudice,” which means that it cannot be refiled at the district court level but may be appealed to a higher court. It is likely that both cases will be appealed. 11 Most of the others have been approved to go forward on some of the allegations, but not on others. It is expected that the litigation will continue for years. 12

The Public Sector

Private sector universities are covered by ERISA. Public sector universities are not. They are subject to the provisions of their respective state laws.

The most recent development in this area involves the CSU. The law firm of Keller Rohrback of Seattle, Washington (and Oakland, California), intends to file a class action lawsuit against CSU’s 403(b) plan and its fiduciaries. It is seeking plan participants to join the suit. 13

Unlike their private sector cousins, employees of public sector universities usually enjoy traditional defined benefit pension plans, such as CalPERS. Many university faculty and staff employees use 403(b) plans to augment their often generous public pensions. Such 403(b) plans typically do not have an employer matching contribution. In addition, under California state law, the statute of limitations for breach of a written contract is generally 4 years, not the 6 years allowed under ERISA. 14 Moreover, it is not clear (to me) that there was a written contract between the CSU’s 403(b) plan and the participants before 2016.

This suggests that even if the class action status is approved and the plaintiffs prevail, none of the participants or beneficiaries is going to get rich from this. The recoveries will be quite modest, probably a few hundred dollars. As in most class action lawsuits, the potential big winner will be the class action law firm.

Keller Rohrback seems to be basing its case largely on information provided by the CSU to active participants in the 403(b) plan about the changes it had made to the plan in response to the new regulations. They included naming Fidelity Investments as the sole TSA provider for all new elective deferrals after April 1, 2016. So-called “legacy assets” with other providers (MetLife, TIAA, VALIC and VOYA) will remain in those accounts. Participants may transfer such assets to the new Fidelity TSA program. However, there are anecdotal reports that when some participants did this, they were hit with exorbitant “rollover fees.” 15

The new Fidelity CSU 403(b) reforms also cut annual fees in half. The average investment fee for a $100,000 account went from $517 (0.52% of asset values) to $400 (0.40%) and the average administration fee from $290 (0.29%) to $46 (0.05%). Thus, total fees were reduced from $807 (0.81%) to $446 (0.45%). Annual average savings on a $100,000 account will be $446. 16 These savings were due to moving from fees based on asset values to a per-participant basis and from multiple record keepers to a single record keeper, Fidelity Investments.

The new arrangement also established a four-tiered approach to investing based on how active the participant wants to be. Tier 1 involves investing only in target date funds, Tier 2 in indexed funds, Tier 3 in active funds and Tier 4 in self-directed investments.

Clearly, the CSU has responded to the new regulatory requirements in a way that prospectively benefits its active (contributing) participants. That, of course, has not prevented a class action lawsuit over retrospective fiduciary duties and excessive fees. Interestingly, Keller Rohrback appears to be basing its position on information and data provided to participants in the CSU/Fidelity Investments transition material. 17

Conclusion

Class action lawsuits perform an important function in society. Typically, the potential recoveries of individual plaintiffs are too small to warrant a lawsuit. However, if a law firm can aggregate the claims of several thousand claimants in a class action suit, it can amount to millions of dollars in contingency fees and expenses for the firm. It may also result in the defendant mending its ways. Because of the lawsuits against private sector corporate sponsors of 401(k) plans under ERISA, administrative and investment fees were significantly reduced. It is doubtful that they would have been otherwise.

In the case of the private sector universities, most (all?) of them had already made changes in response to the 2007 IRS regulations. In the case of the CSU 403(b) plan, the university had already made changes in response to the new rules. Effective April 1, 2016, Fidelity Investments is the only TSA allowed in the CSU 403(b) plan and the fees have been roughly cut in half. Keller Rohrback is seemingly basing its lawsuit on information provided to the 403(b) plan participants announcing the improvements. No good deed goes unpunished.

The stakes are high. If the lawsuits against the 16 or so large prominent university 403(b) plans are successful, it will open the floodgates against numerous other colleges, universities’ not-for-profit hospitals and related organizations that sponsor 403(b) plans.

If the lawsuit against the California State University is successful, it will open the floodgates of litigation against other public sector universities and governmental entities in California and probably in other states as well.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.