Abstract

In recent years, student loan repayment programs have emerged as the hot new employee benefit. However, their growth has been restricted by their lack of favored tax status. On August 17, 2018, the Internal Revenue Service issued a private letter ruling approving a proposal to create such a program within a 401(k) plan. In a deft piece of reasoning, the private letter ruling provides relief from the so-called “contingent benefit prohibition.” This article examines student loan borrowing, the private letter ruling and its likely consequences and limitations.

On August 17, 2018, the Internal Revenue Service (IRS) released a private letter ruling (PLR) in response to a request from an unnamed employer to amend its 401(k) plan to include a student loan repayment (SLR) program. Under the proposal, if the employee made a 2% or more of eligible compensation payment toward his or her student loan debt, the employer would make a nonelective contribution to the 401(k) plan of 5% of the employee’s compensation. The program would allow SLR benefits to be made on a tax-favored basis for the employer and employee.

This article examines the growth and extent of student loan debt, the existing efforts by some employers to help their employees repay their student loans and the recent IRS PLR. It then discusses the limits of the PLR and appraises its likely consequences.

Student Loan Borrowers

The student loan debt is often thought of as a problem of the Millennial Generation (also known as Generation Y) born between 1981 and 1996. Its leading edge began entering the post-college job market in 2003. The Millennial Generation will continue to grow until it makes up 25% of the U.S. labor force in 2025. 1

But the student loan debt problem is not limited to Millennials. About 6.8 million borrowers between the ages of 40 and 49 owe an average of $33,735. In addition, many older employees have taken out federal Parent PLUS loans to finance the education of their children or have cosigned for private student loans for their children from private sector lenders.

Student Loan Debt

According to Student Loan Hero, aggregate outstanding national student loan debt amounted to over $1.5 trillion as of 2018, and the number of student loan borrowers was 44.2 million. For the class of 2017, the average debt was $39,400, up from $37,172 in 2016 and $35,000 in 2015. By these numbers, the average student debt is growing at about 6% per year. 2 These often-quoted data are attributed to Mark Kantrowitz, an expert on student loans. 3

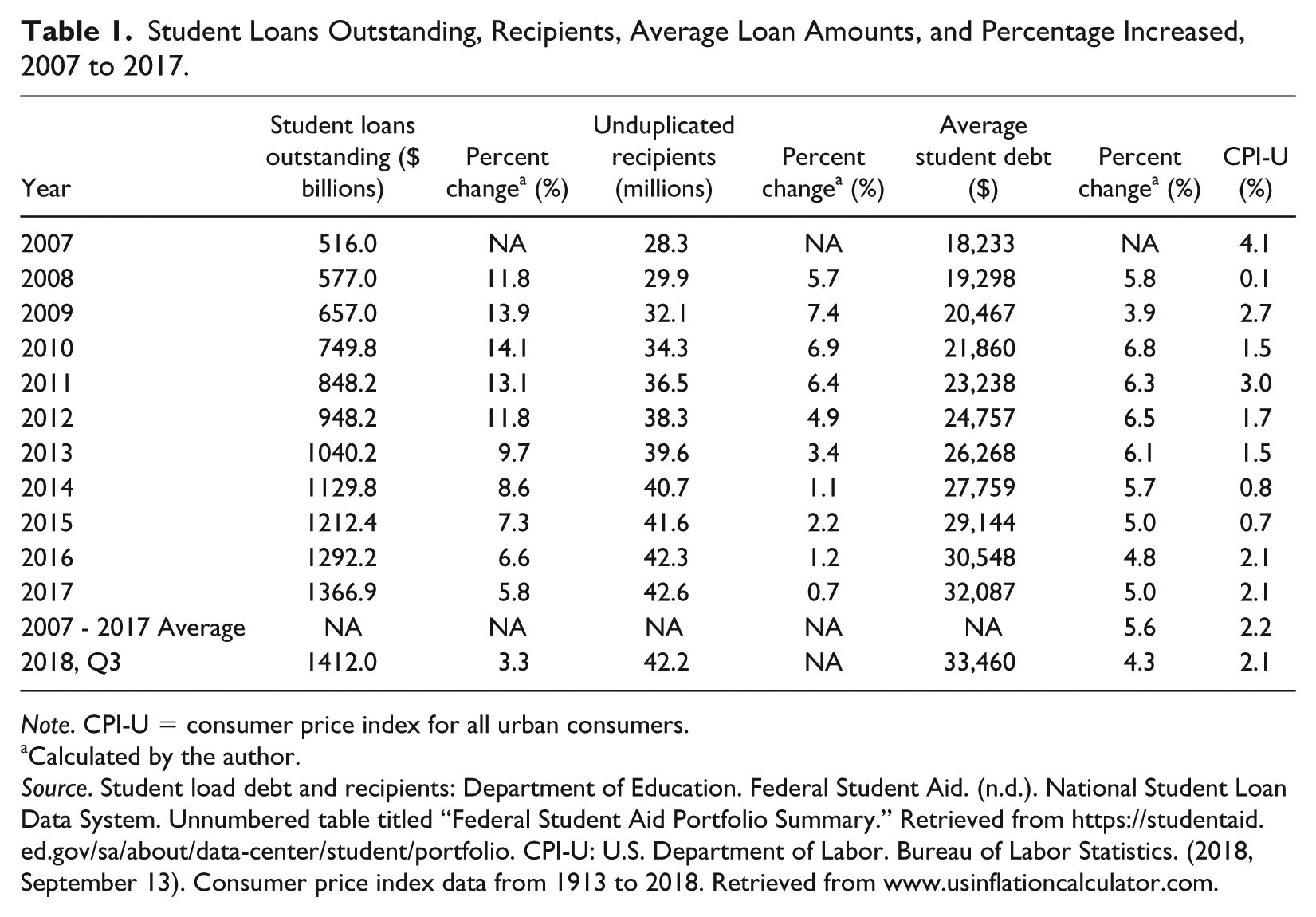

Table 1 reports somewhat different data developed by the author from the Federal Reserve Bank of St. Louis for the period 2007 through 2017 and for 2018 Q3. The amount of student debt owned or securitized by the federal government had grown substantially from $589.5 billion in 2007 to over $1.4 trillion in 2018 Q3. Over the 10-year period (2007-2017), the number of unduplicated loan recipients had grown from 28.3 million to 42.6 million while the average amount borrowed per recipient increased from $18,233 to $32,087. (Securitizing debt involves selling it to a third party (loan servicer) who then receives the loan repayments.)

Student Loans Outstanding, Recipients, Average Loan Amounts, and Percentage Increased, 2007 to 2017.

Note. CPI-U = consumer price index for all urban consumers.

Calculated by the author.

Source. Student load debt and recipients: Department of Education. Federal Student Aid. (n.d.). National Student Loan Data System. Unnumbered table titled “Federal Student Aid Portfolio Summary.” Retrieved from https://studentaid.ed.gov/sa/about/data-center/student/portfolio. CPI-U: U.S. Department of Labor. Bureau of Labor Statistics. (2018, September 13). Consumer price index data from 1913 to 2018. Retrieved from www.usinflationcalculator.com.

Table 1 also shows the annual increase in average student loan debt for per year. Over the decade, the average increase was 5.6%. That is 2½ times higher than the 2.2% average rate of inflation for the period measured by the Consumer Price Index for All Urban Consumers (CPI-U).

Note that the percent increase in student loans outstanding has decreased appreciably from 11.8% in 2008 to 5.8% in 2017. That is attributable to two developments. One is the 2013 adoption of a limit on the number for which undergraduates may receive federal subsidized student loans to 150% of the advertised length of the program. Thus, a student pursuing a 4-year bachelor’s degree was limited to a maximum of 6 years of subsidized loans.

The other is the federal government’s response to the Great Recession of 2008-2009. It included the Budget Control Act of 2011 (Pub. L. 112-25), which established automatic federal budget cuts called “sequestration” that decreased the amount of money available for student loans. Sequestration was scheduled to run through 2020. However, it was effectively ended for 2018 and 2019 by the Bipartisan Budget Act of 2018 (Pub. L. 115-123). 4 It is unlikely that it will be resurrected for 2020.

About 70% of recent college graduates owe student loans and 90% of that debt is owed to the federal government. The remainder is owed to private sector lenders and state programs. 5

Millions of employees begin their post-college careers seriously encumbered by student debt. In addition, many older employees also have outstanding student debt of their own or in the form of Parent PLUS loans or because they cosigned for their children’s loans from private lenders. Table 2 reports outstanding student debt, the number of borrowers and average amount owed by age for 2017 Q4 and 2018 Q3 (the most current data as of this writing). While it shows that the bulk of student debt is owed by relatively young people, significant amounts and surprising average debt amounts are owed by people in their 40s, 50s and 60s.

Student loan portfolio by borrower age, 2017 Q4 and 2018 Q3.

Calculated by the author.

Source. U.S. Department of Education. (2018). Enterprise Data Warehouse. Unnumbered table titled “Direct Loan Portfolio by Borrower, Age.” Retrieved from https://studentaid.ed.gov/sa/about/data-center/student/portfolio.

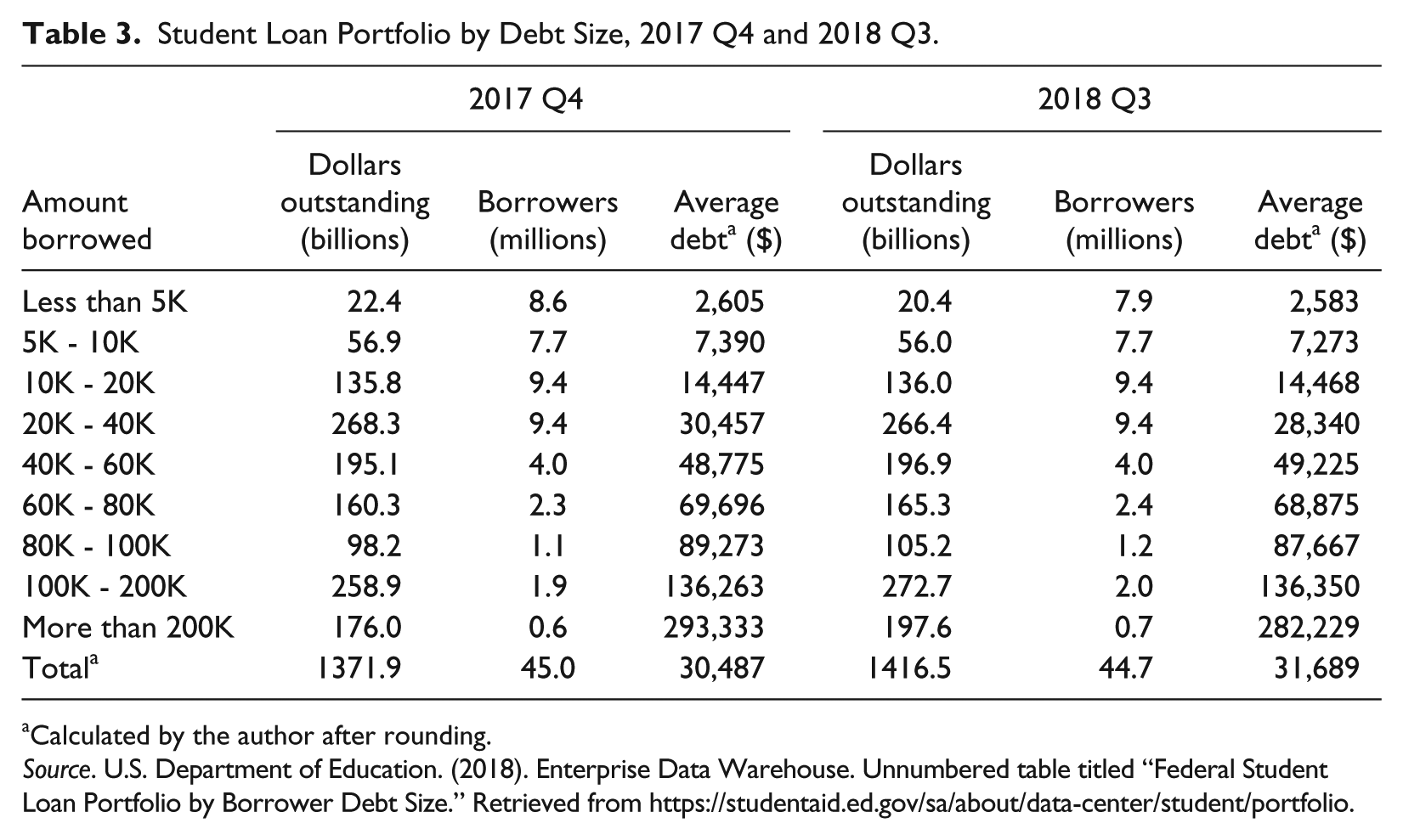

Averages often conceal more than they reveal. Table 3 reports the amounts borrowed by size of debt for 2017 Q4 and 2018 Q3. It shows that while aggregate average student debt was over $30,000 by these measures (roughly consistent with Table 1), the average amounts by bracket size ranged from $2,605 for those owing less than $5,000 to $293,333 in the highest bracket. It should be noted that many of those in the higher brackets are medical doctors and other high-income professionals who have access to loan forgiveness opportunities. But, many are not.

Student Loan Portfolio by Debt Size, 2017 Q4 and 2018 Q3.

Calculated by the author after rounding.

Source. U.S. Department of Education. (2018). Enterprise Data Warehouse. Unnumbered table titled “Federal Student Loan Portfolio by Borrower Debt Size.” Retrieved from https://studentaid.ed.gov/sa/about/data-center/student/portfolio.

All of this has generated considerable interest in employer-provided programs to help employees repay their student loans. It is widely held that such SLR plans give employers a competitive advantage in attracting and retaining employees. However, a major constraint has been the lack of favorable tax treatment for employers and employees.

The Current Situation

Many employers had already established SLR programs to help attract and retain employees. 6 The Society for Human Resources Management (SHRM) estimates that, as of 2017, 4% or employers, and 8% of large employers with 40,000 or more employees, had adopted some form of SLR benefit. SHRM expected that employer-provided SLR benefits will be adopted by 20% of employers in 2018. 7 These programs varied significantly from each other due in part to the lack of guidance from Congress or the IRS.

Before the 2018 PLR, none of these programs were tax favored. Unlike Internal Revenue Code (IRC) Section 127 educational benefits, employees have to pay income tax on SLR benefits (included in the W-2) and employers cannot deduct such benefits as a business expense. Moreover, employers have to pay the FICA (Federal Insurance Contributions Act; 7.65% including Medicare) and FUTA (Federal Unemployment Tax Act; a federal minimum of 5.4% on the first $7,000 of earnings amounting to $378), but more in most states. 8 The highest is the state of Washington with a wage base of $47,300 and a maximum unemployment tax rate of 7.73% ($3,656). However, the actual rate varies substantially among employers due to experience rating. 9

Under IRC Section 127 (Educational Assistance Programs), the employer may deduct up to $5,250 per year in educational benefits per employee. Such funds are not counted as taxable income to the employee and are deductible as a business expense by the employer.

The idea of extending Section 127 to cover SLR benefits has been around for years and has support on both sides of the isle in Congress. The Employer Participation in Student Loan Assistance Act (H.R. 795) was introduced in the House of Representatives by Rodney Davis (R-IL) on February 1, 2017, and was referred to the Ways and Means Committee. 10 No further action has been taken. Given the current divisiveness in the Congress, the chaos in the White House and the recent increase in the federal deficit and national debt, it may be a long time before anything in this area is approved.

The Contingent Benefit Prohibition

Section 401(k) cash or deferred arrangements (CODA) plans must satisfy the “contingent benefit prohibition” of IRC Section 401(k)(4)(A) and the related Treasury Regulation 1.401(k)-1(e)(6) to qualify for favorable tax treatment. The rule prohibits an employer from conditioning other benefits (such as vacation, health insurance or stock options) on employees making or not making 401(k) elective contributions (also called elective deferrals). The only exception to the rule is employer matching contributions subject to Section 401(m) of the IRC.

The contingent benefit rule has been in the IRC since the 1981 Section 401(k) regulations. However, it has received little attention until the SLR benefit issue arose.

The contingent benefit rule was a major constraint to the adoption of tax-favored SLR benefits. With a deft piece of reasoning, the IRS approved a way to accommodate employers seeking to offer tax-favored SLR benefits while preserving the contingent benefit prohibition.

The Private Letter Ruling

In its private letter ruling (PLR 201833012), the IRS approved a proposal from an unnamed “taxpayer” (employer) to amend its traditional 401(k) plan by adding a SLR program. Specifically, the PLR addressed the narrow issue of providing relief from the contingent benefit prohibition.

It was widely believed that the unnamed taxpayer in this case was Abbott Laboratories, 11 a major pharmaceutical and medical device manufacturer with 99,000 employees headquartered in Illinois. Abbott Labs had requested a PLR from the IRS on May 22, 2018, and the IRS released its determination on August 17, 2018. (The IRS releases PLRs to the public on Friday mornings at https://apps.irs.gov/app/picklist/list/writtenDeterminations.html.)

Abbott Labs subsequently confirmed that it was the employer that requested the PLR. It also reported that 200 employees had already signed up for its SLR program and that it expected several thousand more to eventually do so. 12

On August 30, 2018, the ERISA Industry Committee (ERIC), which represents large employers with benefit plans governed by Employee Retirement Income Security Act of 1974 (Pub. L. 93-406; ERISA), sent a letter to the IRS commending it on the PLR. ERIC also asked the IRS to issue a revenue ruling that would broaden the rule to allow all sponsors of all 401(k) plans with employer matching contributions to make similar SLR contributions for their employees. 13 This may be the first of several such requests.

The Proposal

Abbott Labs proposed to amend its very generous 401(k), available to all of its employees, by adding a student loan repayment program. If the employee made a student loan repayment of 2% of eligible compensation per pay period, the employer would make a nonelective contribution of 5% of compensation to the 401(k) plan. The SLR program would be entirely voluntary and the participant could withdraw at any time.

If the employee also made a 2% of compensation elective deferral to the 401(k) plan, he or she would not receive both the regular 401(k) match and the SLR nonelective contribution. If, however, the employee failed to make the minimum required 2% SLR payment for any pay period, but had made a 2% elective contribution to the 401(k) plan, he or she would be entitled to regular 5% matching contribution to the 401(k) plan for that pay period. This was to be handled by a “true-up” at the end of the plan year (providing that the participant was still employed by the company).

In the PLR the IRS held that the proposed arrangement did not violate the contingent benefit prohibition because the SLR is in response to an event “outside the plan” while the contingent benefit prohibition applies only to “inside the plan” benefits.

The IRS’s determination was based on three important conditions: (1) that the nonelective contribution under the SLR program is not itself conditioned on the employee making or not making an elective contribution to the 401(k) plan; (2) because the employee is entitled to make a 2% elective contribution to the 401(k) plan in addition to the SLR, the nonelective SLR employer contribution is not contingent on the employee making or not making an elective contribution in lieu of receiving cash and (3) that the plan sponsor (employer) will not extend any student loans for employees eligible for the SLR program. 14

Limitations of the PLR

A PLR applies only to the party that requested it and may not be used as precedent by anyone else. Furthermore, its approval is contingent on the accuracy of the facts provided by the requesting party and their faithful implementation. However, the PLR provides welcomed guidance to employers on how to craft a SLR program without running afoul of the contingent benefit rule. But, that is all that it does.

The PLR pertains only to a 401(k) plans with employer matching contributions. It does not apply to other forms of defined-contribution retirement arrangements. Section 401(k) plans are available to private sector for-profit employers and some public sector employers with “grandfathered” plans adopted before May 6, 1986, and in continued operation since then.

The SLR programs are subject to the same requirements as a qualified 401(k) CODA. They include the vesting schedule, distribution rules, contribution limits, coverage and nondiscrimination testing. 15 Nondiscrimination in this context means that the plan not unduly favors “highly compensated employees” (HCE) over “non-highly compensated employees” (NHCE) as measured by the “actual deferral percentage” (ADP) and the “actual contribution percentage” (ACP) tests. For 2018, an HCE is generally defined as employee earning a salary of $120,000 or more or a 5% or more owner of the company regardless of income.

The PLR would not apply to safe-harbor 401(k) plans in which the employer must provide a contribution to the plan that is fully vested when made. Similarly, it probably would not apply to SIMPLE 401(k) plans (available to employers with 100 or fewer employees) for the same reason. The PLR also may not work for 401(k) plans with an automatic-enrollment feature. 16

There are two disadvantages of the approved program to the employee. First, unlike elective contributions to a 401(k) plan, SLRs are made with after-tax dollars. A participating employee will have to pay more to make the 2% repayment. Second, if the employee makes a 2% loan repayment in lieu of elective deferrals to the 401(k) plan, it will result in the accumulation of less retirement dollars over time. 17 Given the time value of money, this could be quite serious.

Appraisal

The fact that the employer may make either a nonelective SLR contribution or a matching 401(k) plan matching contribution, but not both, makes the SLR program cost neutral to the employer (ignoring the expense of setting up and administering the program). 18 It may be even better than that for employers that have already adopted a SLR program.

There are also significant tax advantages. The employer can deduct the SLR contribution from its corporate income tax and it does not have to pay FICA and FUTA taxes on those funds. In addition, the employee benefits by not having to pay individual income or his or her share of the FICA tax on the amount of the contribution. 19

The PLR is a major step in the right direction. Indeed, it may be a “game changer.” Many employees are burdened by large student loan obligations. The Abbott Labs and the IRS has found a way to allow employers with 401(k) plans to help them while preserving the contingent benefit prohibition. That was a nice piece of work. It will be of significant benefit to millions of young—and some not-so-young—employees encumbered with student loan debt.

However, the PLR does not address all potential issues. Any SLR program attached to a 401(k) plan would still have to meet all of the eligibility, vesting and distribution rules, contribution limits, coverage and nondiscrimination testing requirements of the 401(k) CODA plan. It is likely that most SLR benefits will go to relatively young employees early in their careers. Such employees are likely to not contribute or will contribute less to the 401(k) plan. That could affect the chances of the plan passing the ADP and ACP nondiscrimination tests. 20 If this results in lower allowed elective deferrals and matching contribution for HCEs, there could be negative consequences.

Who the PLR Does Not Help

The recipients and potential recipients of the SLR program allowed under the PLR are the fortunate ones. They have chosen sensible majors at sound educational institutions, completed their degree requirements and found employment with an organization that sponsors a 401(k) plan with an employer matching contribution. There are many millions of other former students who have made less sensible decisions and now suffer under a mountain of student loan debt. There are also many debt-encumbered former students who work in the public sector, not-for-profit sector or for firms that do not sponsor a 401(k) plan. The PLR will do little, if anything, to help most of them.

Conclusion

Over the last few years, student loan debt repayment has emerged as the hot new benefit. However, the lack of favorable tax treatment has restricted their growth. Now that the IRS’s PLR to Abbott Labs has provided guidance on how to establish a tax-favored program, we can expect many more mainly private sector employers to adopt such programs.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.