Abstract

Research in supply chain management focused on the buyer-supplier relationship (BSR) indicates that costing practices can impact relationship quality and performance. Yet, few studies have examined how the supplier’s costing methods affect the BSR. To address this gap, this study investigates the role of open costing in the BSR within the apparel supply chain. Open costing is a popular costing practice in which a supplier compiles an itemized list of costs rather than a fixed price. To examine the extent to which open costing is practiced as part of BSRs, interviews were conducted with 30 professionals operating as suppliers in China and Bangladesh. A thematic analysis of the interview data identified several factors important to open costing and the BSR, including Mutual Trust, Fairness, Flexibility, Efficiency, and Sustainability. Findings shed light on the mechanism and practice of open costing within the BSR, and specifically from the perspective of suppliers.

Keywords

Supply chain management (SCM) research has been increasingly focused on how firms can improve their competitiveness through close collaboration with supply chain partners (Adams et al., 2014; Fawcett et al., 2012). Some studies suggest that supply chain competitiveness can be achieved by building long-term buyer-supplier relationships (BSRs) (Elfenbein & Zenger, 2014). Within the BSR, product costing is a key factor for both buyer- and supplier-side decisions, and particularly as to whether the two parties will engage in an extended contract and/or commit to a long-term relationship (de Almeida Fehr & Rocha, 2018; Norek & Pohlen, 2001). Indeed, Norek and Pohlen (2001) found that different costing practices have different kinds of impact on the overall level of collaboration within a BSR. For example, open costing is a method by which a supplier compiles the focal product’s itemized list of cost factors to the buyer, then collectively finalizes the costs of the product, rather than providing a fixed price (Miller & Hohenegger, 2018). Because it is an open process where information is shared with the buyer, it is considered a more collaborative costing practice than methods that have traditionally been employed in apparel SCM.

The extant literature on product costing and pricing is largely nested in the disciplines of accounting, economics, marketing, and SCM in general (Norek & Pohlen, 2001). However, thus far, few studies within this body of literature have examined the role of the supplier’s costing method relative to the BSR. In light of this gap in the existing literature, the two-fold purpose of this study was to investigate the current practice of open costing in apparel SCM and particularly to understand its role in BSRs. Two objectives were developed to address the purpose: (1) to explore the reasons why suppliers use open costing, and (2) to identify the extent to which the BSR may be impacted by the practice of open costing. The theoretical framework of social exchange theory (SET) (Homans, 1958) was employed to elucidate the findings for the BSR literature and managerial practice.

Background

According to the literature, BSRs in the apparel supply chain are inherently complex and differ from those of other industries (Singh & Hodges, 2011) for several reasons. First, the apparel supply chain is lengthy, as numerous suppliers, steps, and processes are involved (Su, 2013). Second, the industry is characterized by low barriers to entry, making the apparel supply chain extremely fragmented (Su, 2013). Third, the search for low cost suppliers among buyers has created different operational practices across the primary apparel producing countries (Bruce et al., 2004). Such factors can lead to opportunistic behaviors among both buyers and suppliers, thereby preventing them from developing long-term and collaborative BSRs (Brito & Miguel, 2017; Huo et al., 2017).

The complexity of the apparel supply chain presents both opportunities and challenges. For example, as Kannan and Tan (2002) pointed out, building long-term BSRs with a minimum number of suppliers can be as beneficial to buyers as it is to suppliers. To this end, costing is one way that both the buyer and supplier can work toward achieving a long-term relationship.

Costing Practices and the Apparel Industry

According to Adams et al. (2014), the particular costing practice adopted by the buyer and supplier has implications for the level of cooperation within the BSR and ultimately for supply chain performance. Indeed, product cost inquiries have moved away from traditional costing methods to those that are more cooperative in nature (de Almeida Fehr & Rocha, 2018), as the competitive environment of the apparel industry calls for more collaboration-oriented approaches to product costing. In order to investigate the role of open costing in apparel BSRs, a review of the more traditional costing practices is necessary.

Traditional costing methods

Traditional costing methods, such as full costing and target costing, have been used in the apparel industry for many years. With traditional costing methods, the supplier is not obligated to reveal his or her costing model to the buyer. Under such “secretive” costing processes, a supplier decides what the final product price will be without participation or input from the buyer. Non-cooperative costing and pricing decisions are common characteristics of all traditional costing practices in the apparel industry. However, researchers have pointed out that such unilateral approaches to costing can be detrimental to developing and maintaining BSRs in the modern supply chain environment (Norek & Pohlen, 2001).

The full costing method, as defined by Shim and Sudit (1995), is the sum of “variable costs plus allocated fixed costs” (p. 37). In the apparel industry, full costing starts when a supplier receives the product sample from the buyer. Based on the sample design, material, accessories, and other technical requirements, the supplier assesses direct production costs and assigns an overhead amount, which varies depending on overhead structure. Then, as in other industries, the supplier provides the price to the buyer. The buyer then negotiates the offer, usually based on his or her previous experiences with producing similar products (Masschelein et al., 2012). Masschelein et al. (2012) found that during the full costing negotiation process, suppliers view such bargaining on the part of the buyer as an imposition and therefore potentially damaging to the BSR.

While full costing is the traditional costing method used in supplier-driven mechanisms, target costing is a buyer-driven method. Hergeth (2002) defined target costing as “a process of first assessing a target price and then designing a product to meet this price” (p. 2). In an apparel industry scenario, the “target” of target costing is a specific price given by the buyer for a certain product. This target is based on the maximum price the buyer is willing to pay the supplier and still maintain the desired profit amount. The target costing method is a convenient way for buyers to achieve their desired price by setting the “target” and requiring suppliers to “hit” this target, especially in the buyer-dominated apparel industry (Hergeth, 2002).

However, target costing has two major negative effects, as noted by both Norek and Pohlen (2001) as well as de Almeida Fehr and Rocha (2018). First, target costing is buyer-driven, and could require that the supplier lower prices to levels that are unsustainable for their business operations. Second, when buyers require the supplier to hit the target price, they also expect the quality and desired characteristics of the product to be maintained, therefore, suppliers will have to “cut corners” that do not directly affect the product.

To achieve the cost target, the supplier might cut costs by doing what Hughes (2005) described as Activity Based Costing (ABC), which is to identify all activities that have costs in producing the product and then eliminate “non-essential” costs such as reducing worker benefits, enforcing longer working hours, or spending less on equipment maintenance. Although the ABC method is helpful in achieving a product’s target price, it does not necessarily help the supplier or the buyer to gain a competitive advantage in the industry.

In sum, the various traditional product costing methods discussed all involve unilateral decision-making. As Brito and Miguel (2017) pointed out, such decision-making does not facilitate the level of collaboration necessary to achieve competitive advantage through the BSR. Open costing, wherein each type of cost is based on a bilateral agreement, is more conducive to collaboration within the BSR.

Open costing

As previously mentioned, open costing is a mechanism wherein the supplier breaks down the costs of producing an apparel product into materials, wages, processes, overhead, and markups. In contrast to traditional costing methods, where the buyer will usually bargain down the cost provided by the supplier, in open costing, the two parties work collaboratively to optimize and validate each cost item, and therefore, the overall direct cost of producing the product (Miller & Hohenegger, 2018). That is, they total the itemized costs, add a mutually agreed upon markup, and arrive at the per unit cost of the apparel product. Once the supplier accepts the unit cost per the agreement, it becomes the supplier’s selling price for it. This collaboration in cost determination reduces the potential for conflict between the buyer and supplier because it is a transparent process and any indirect costs, such as those related to social or environmental compliance, are built in to the final price for producing the product (Miller & Hohenegger, 2018).

Norek and Pohlen (2001) pointed out that when product costs are jointly determined by the buyer and supplier, it can lead to a stronger and more competitive BSR. When compared to the traditional methods of full costing (Shim & Sudit, 1995) and target costing (Hergeth, 2002), open costing arrives at the final price not by negotiation, but by collaboration through information sharing. For this reason, the open costing model has great benefits. For example, a benefit of open costing is increased supply chain efficiency by reducing the potential for lengthy price haggling and production stalls caused by product price negotiation and re-negotiation (Miller & Hohenegger, 2018). However, it is not without risks and challenges for both parties in the BSR, the biggest one for the supplier being the possibility that the buyer may take advantage of the knowledge of the itemized costs and use this knowledge to seek out a lower cost supplier (de Almeida Fehr & Rocha, 2018).

As the number of apparel suppliers has increased globally, it has become both necessary and beneficial for buyers to understand the rationale behind apparel cost differences among suppliers and across source countries. For example, during the joint process of product development, issues of increased cost when adding certain design or product attributes often impact both parties. These issues are not easy to manage if the supplier presented the cost of the product as a lump-sum unit price. Doing so does not communicate how changes to product design can result in significant costs added to the finished product, which, in turn, increases the product cost at retail. As a result, the overall competitiveness of the product is reduced because of the higher cost. However, because the nature of open costing requires the supplier to share proprietary cost information with the buyer, it is important to understand why suppliers practice open costing with their buyers. Therefore, the first research question (RQ) guiding the study was: RQ1: What are the reasons why suppliers may or may not practice open costing?

Costing and the Buyer-Supplier Relationship

Any business entity engaged in supply chain activities will typically have multiple BSRs. Developing, maintaining, and terminating these BSRs involves expense, including overhead as well as opportunity costs (Cannon & Homburg, 2001). Cannon and Homburg (2001) tested two contrasting types of BSR approaches—adversarial and collaborative—and found that, overwhelmingly, a collaborative BSR leads to much greater cost reductions for the customer firm (i.e., the buyer). In fact, Han et al. (1993) found that when attitudes toward the BSR shifted from adversarial to collaborative, the result was lower relationship costs for both parties.

Naturally, a common goal for both parties in a BSR is overall cost reduction. Adoption of open costing can be a tactic to reduce the overall costs involved in the daily operation of the business, both inside and outside of the manufacturing plants. This is because the open cost mechanism details all costs of production, with no surprises or hidden costs. However, open costing does not come without risks to the supplier. Han et al. (1993) demonstrated that the exposure of the actual costs of a product can make the supplier vulnerable in the BSR, which may lead to a disadvantaged position in the market. This is because revealing the specifics of product cost information creates a situation of information asymmetry that positions the supplier as vulnerable to the buyer’s potential for opportunistic and exploitative behavior (de Almeida Fehr & Rocha, 2018). Thus, open costing largely indicates the suppliers’ willingness to build a long-term relationship. As Han et al. (1993) argued, the long-term BSR provides benefits (e.g., cost reduction, supply assurance, quality improvement) to both parties that often outweigh the risks.

Considering the above literature, collaboration is as much a requirement of the open costing process as it is an outcome. It is therefore possible that, as a practice, open costing facilitates a more collaborative BSR overall. Thus, the second research question guiding this study was: RQ2: What are the benefits and challenges of open costing for both parties in the BSR?

Conceptual Framework

Social exchange theory (SET) is a social behavioral theory that describes relational exchange behavior and concerns interpersonal relations and group functioning (Blau, 1964; Emerson, 1976; Homans, 1958). The application of SET in studying BSRs helps to explain the interactions between buyers and suppliers in a relationship-based exchange, which is different from a short-term, transaction-based exchange (Cho et al., 2015). Academic studies on BSRs therefore have tended to focus on the constructs of “exchange” and “relationship,” collectively termed “relational exchange” (Lambe et al., 2001).

In SET, a BSR can be viewed as the costs and rewards of the relational exchange between the two parties. Cho et al. (2015) pointed out that, with respect to the BSR, SET is able to explain not only the intentions for economic outcome but also the social outcome of collaboration. For example, Chaudhry and Hodge (2012) suggest that, in the case of demand-based deliveries (where suppliers carry the entire stock and ship loose quantities directly to buyers’ retail stores on demand), the BSR is highly dependent on collaboration between buyer and supplier. BSRs are social exchanges that must be able to respond quickly to demand in order to remain competitive.

SET allows for an examination of the BSR as “encompass[ing] reciprocal obligations stemming directly from the relational orientation between suppliers and distributors” (Kingshott, 2006, p. 724). In this light, factors stemming from working together on open costing may impact the apparel BSR, including increasing the level of collaboration between and long-term orientation views of the two parties. As Kingshott (2006) found, disclosing behaviors increases trust as well as other positive psychological outcomes between the two parties. In the present study, it is proposed that open costing is a disclosing behavior because it requires the supplier to be transparent about everything that is factored into the bottom line. As discussed earlier, open costing carries benefits as well as risks for suppliers. From the SET perspective, the benefit of having a more collaborative relationship with buyers is the reward for suppliers by adapting open costing. By sharing cost information, risking opportunistic behavior by the buyer is the potential cost to the supplier. Thus, the third research question guiding this study was: RQ3: What does open costing mean for the BSR as a relational exchange?

Method

Data Collection

Because there is little empirical research on open costing in apparel SCM, a qualitative approach was deemed suitable for the present study (Merriam, 1998). When applying an established theory such as SET to investigate a relatively unexplored phenomenon, Merriam (1998) suggests using semi-structured, in-depth interviews to collect data. Interview questions were therefore balanced between the theoretical assumptions of SET, and at the same time, were open-ended to explore the individual’s perspective (Mason, 1996). Moreover, questions were guided by the RQs, SET assumptions, and the BSR literature (Brito & Miguel, 2017; Bruce et al., 2004). Specific questions related to BSRs were adapted from the literature related to product cost determination (Cannon & Homburg, 2001).

Based on the review of literature, the interview instrument was developed. Designed to address the purpose of investigating the practice of open costing, it included questions specific to the practice as part of the BSR using SET as the theoretical lens. Interview questions were organized into three sections: the practice of open costing, implications of open costing for the BSR, and the role of open costing in SCM. In the first section, questions included: What is your preferred method of reporting a garment’s cost to buyers? Why? Questions in the second section included: Do you think that open costing is the fairest method in determining your costs? Why or why not? For the third section, exploring the role of open costing in SCM, questions included: Do you think that open costing impacts supply chain efficiency? If so, in what ways? Interview data provided the basis for developing an in-depth understanding of the role of open costing in the BSR.

Description of Participants

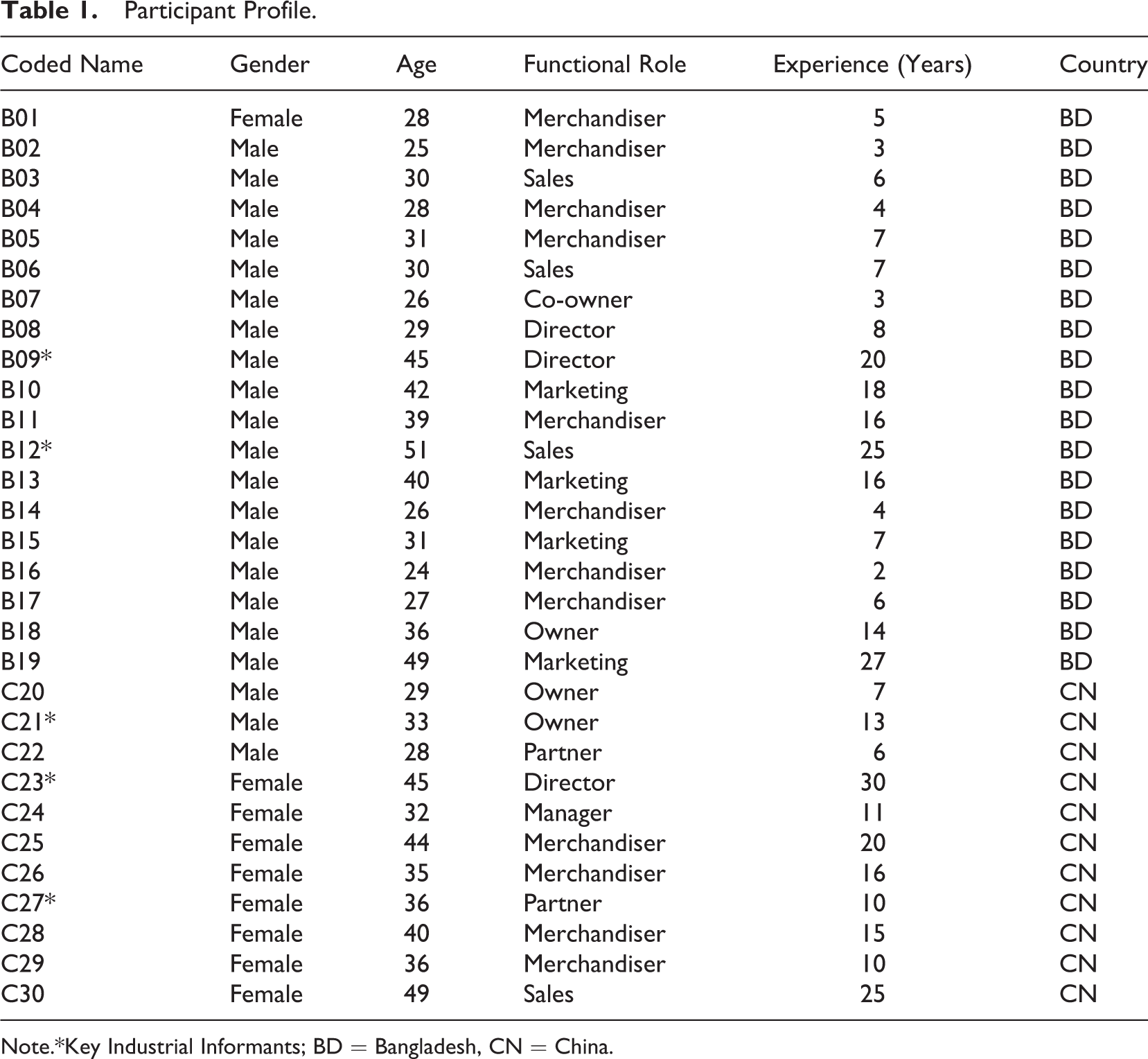

With IRB approval from the researchers’ university, a total of 30 apparel industry professionals employed with supplier firms were recruited through the authors’ professional networks in the apparel industry using the snowball method (Mason, 1996). Participants occupied operational and managerial roles, with job titles ranging from merchandiser to owner. A total of 11 participants were from China and 19 from Bangladesh. According to the World Trade Organization (2020), China and Bangladesh were the top two clothing exporting countries in 2017, accounting for close to 42% of the total global value. It is likely that apparel suppliers from these two countries therefore have the richest experiences in dealing with all kinds of buyers. To address the purpose and research questions guiding the study, participants had a combined average of 12.03 years of experience in interacting with buyers. Participants all indicated they have been practicing open costing for at least 12 months. The sample size was determined upon data saturation (Hodges, 2011). See Table 1 for participant information.

Participant Profile.

Note.*Key Industrial Informants; BD = Bangladesh, CN = China.

Interviews were conducted in either face-to-face or using WeChat’s “video chat” function depending on the participant’s preference and availability. With the participants’ consent, interviews were digitally recorded and were conducted in Mandarin for the Chinese participants and English for the Bangladesh participants. Five of the 30 participants were further classified as key industry informants (KIIs). Following Eisenhardt (1989), KIIs were selected using three criteria: (1) have worked in the apparel industry for at least 5 years; (2) job functions must include interacting with buyers and must be a key decision maker regarding buyer orders; and (3) mainly practice open costing with their buyers. Interviews with KIIs lasted 60–90 minutes each and involved more in-depth probing of the core issues. Interviews with the other 25 participants lasted 30–45 minutes each. As per the IRB requirements, any personal or identifying information was removed from the data and all data were kept in a secure location with access restricted to the authors.

Data Analysis

All interviews were transcribed verbatim and, when necessary, translated to English by two of the researchers who are native Chinese speakers. After the interviews were transcribed, the texts were read jointly across the interviews. All interview texts were analyzed collectively. Participants agreed to be contacted via telephone or email for additional information or clarification if needed. An iterative, hermeneutic approach to interpretation of the dataset was employed to analyze commonalities and differences across the interview texts (Kvale, 1996). The researchers performed both open and axial coding, comparing the data within each interview and across different interviews to identify reoccurring categories of meaning. An initial set of categories were generated by the first author using open and axial coding methods. These were then reviewed and discussed by the research team and differences between categories were resolved through consensus (Merriam, 1998). Themes that emerged from category consolidation were discussed and further integrated to form broader conceptual themes that best reflect the participants’ perspectives and experiences across the data (Strauss & Corbin, 1998). The interpretation of the data was guided by the tenets of SET while maintaining an inductive approach to allow the discovery of new data patterns for theoretical development (Strauss & Corbin, 1998). Once categories of meaning were identified and agreed upon by the authors, five key emergent themes were defined and used to structure the interpretation: Mutual Trust, Fairness, Flexibility, Efficiency, and Sustainability.

Findings and Discussion

Interpretation of the data indicates that participants must feel as though the BSR is characterized by mutual trust and fairness before they will consider adopting an open costing approach with a buyer. If they trust the buyer and the buyer is seen to be fair when it comes to the relationship, then the participants think that the use of open costing can help add flexibility and efficiency to the order and production processes. Moreover, they think there is a greater possibility of incorporating sustainable practices into the process because their costs will be covered. In the following sections, each theme is discussed separately and then examined as parts within the whole of the overall process of making the decision to use open costing.

Mutual trust

Although all of the participants have engaged in open costing, of the 30 participants, 26 indicated that they would be very reluctant to use this approach with buyers that they have not done business with before, or that are not well known in the industry. This cautiousness was particularly evident among participants that are senior managers, many of whom expressed concern about information confidentiality when giving open costing information to “unfamiliar” buyers. For example, as one participant, who is the director of an apparel factory explained, I have instructed my sales department not to give open costing information to non-regular buyers. Some of them are probing our open costing information, then use it as a counter-offer for other suppliers. We could be seriously compromising ourselves. (B09) Open costing means there is trust between us. Some buyers haggle over individual item costs. These buyers are trying to fish out a lower cost. So, if we don’t trust a buyer, we don’t do open costing with him. (C23)

Fairness

Much like trust, fairness is a requirement for participants before they decide to engage in open costing. This is evident in a study by Masschelein et al. (2012), which argued that cost information disclosure is based on the supplier’s perception of fairness. Of the 30 participants in the present study, 22 indicated that, as suppliers, they often feel tremendous pressure to agree to unfair terms during the product inquiry and negotiation process with a buyer, particularly when the buyer uses information available in the market to argue each of the itemized costs to achieve an impossibly low total cost. As one participant, (B12), who is a sales manager explained, “We may give the buyer our open costing information with an item’s reasonable unit price, but some buyers use this information to exploit us on individual item costs.”

According to participants, it is also common for buyers to abuse the open costing process by insisting that they are willing to place the order only when each item’s cost is the cheapest on the market. However, as Hughes (2005) and Norek and Pohlen (2001) pointed out, it is difficult for a supplier to make a profit and, at the same time, be the least expensive available source for all of an item’s cost elements. Yet one participant, who is a factory owner, pointed out that there are buyers, especially those they have worked with over a prolonged period of time, are less cost-sensitive and instead want an open costing approach so that they can intentionally look for reasonable item costs to make sure suppliers will not use low quality materials: Our long-term buyers are “quality” buyers. They don’t want the cheapest or lowest price. Their concern is the quality of the apparel. They understand if we use inferior quality materials which fail quickly with consumers, it costs their brand’s reputation. (B20)

Flexibility

According to 27 of the 30 participants, once the relationship with the buyer has reached a point where the supplier feels like there is mutual trust and fairness between the two parties, open costing becomes the preferred method. One reason for this preference is that when more traditional, lump-sum quotes for a product are used, any changes to or modifications of the production of that product that are required by the buyer means that the costing and negotiation process must begin all over again (Miller & Hohenegger, 2018). This is because, in most cases, any product- or production-related modification will change the overall costs, and particularly in terms of labor and materials (de Almeida Fehr & Rocha, 2018). As B05 explained, After a purchase order is placed, buyer-initiated changes increase our costs. Any change will render the respective prior investment obsolete. In traditional costing, the buyer never pays us back. In open costing, we show these costs and the buyer must compensate us.

The idea that open costing offers flexibility and therefore makes the process easier surfaced repeatedly across the interviews. Participants talked about the fact that open costing means greater flexibility in the process because costing becomes “less of a daily burden” and makes it “easier managing production.” In particular, the nine participants who are senior managers all talked about the fact that open costing makes their interaction with their counterparts in buying companies more straightforward. Likewise, as one business co-owner (C11) noted, “Without open costing, any change that costs extra in the course of production the buyer will force us to absorb it. With open costing, we have a solid framework to support our claim.” Open costing allows the supplier to be up front with the buyer about all of the costs involved, and, in turn, to be compensated for these costs rather than having to cover them at a loss. When the supplier’s costs are compensated fairly, the chances of building a more long-term BSR are enhanced. Moreover, according to participants, when the supplier is a partner in the process, the buyer can still modify some elements in response to changing fashion trends, and, in turn, maintain a supply chain that is responsive to changing market demands (Chaudhry & Hodge, 2012).

Efficiency

Twenty-five of the thirty participants indicated that, alongside flexibility, another outcome of open costing is efficiency. That is, the open costing mechanism saves pre-production lead time by reducing negotiation time and effort that results from a lot of back and forth between the parties. Open costing can also allow the lead time cycle to begin earlier in terms of product development, which the supplier can engage in as part of the process. As one participant, who is a managing director, remarked, “Product development is crucial and part of the lead time cycle. Based on trust and open costing, we invest resources in product development without buyers spending valuable lead time juggling among several suppliers to get the best price” (B08).

This lead time reduction reflects how integration between buyers and suppliers can enhance supply chain efficiency (Bruce et al., 2004) and illustrates some of the benefits of establishing strong BSRs. As a participant, who is a factory owner, said: Open costing assumes mutual trust and saves pre-production time. When buyers have “staple” items (repeat orders) with little changes, buyers estimate our costs. Open costing helps us save time and resources. This time-efficient practice is not possible without open costing. (C27)

Sustainability

Although supply chain flexibility and efficiency are critically important to the participants as suppliers, the fact that both are considered outcomes of open costing may not necessarily be surprising. However, the idea that open costing can lead to greater efforts toward integrating sustainability within the supply chain, something that 24 of the 30 participants mentioned frequently, was somewhat surprising, as this idea has not been widely discussed in the supply chain literature.

Sustainability costs usually include costs associated with environmental protection, employee well-being, and meeting statutory requirements (Sarkis et al., 2010). For participants as suppliers, costs related to sustainability included those designed to improve worker welfare, reduce waste, prevent environmental damage, and those that are designed to build safety and/or sustainability attributes into the product itself. Participants explained that open costing provides them with opportunities to include the costs of such considerations into the overall price that they provide the buyer to produce the item. Moreover, in open costing, these costs are clearly documented, which allows the supplier to be compensated specifically for them. For example, one participant, who is a factory owner explained, Buyers that have brand images will avoid working with bad social practice factories. Social sustainability costs like worker benefits, safety, environmental and other statutory requirements are high. Open costing supports us to demand higher compensation for these costs from buyers. (B18)

For 19 of the 30 participants, the use of the open costing approach means they can put more effort into sustainability in their production of a given product for a buyer. It appears that this is the case for at least two reasons. Number one, the open costing approach clearly highlights the extent to which efforts toward sustainable supply chain practices have costs associated with them. Number two, it indicates that these costs must be covered by someone, that is, the supplier. Open costing therefore justifies the idea that the total cost for producing the item should include compensation for the supplier who is building sustainable practices into the process. In other words, the buyer should not just assume that the supplier will “eat” the costs associated with sustainability. Working together with the supplier, the buyer can establish a fair price for a quality product to be made in a way that addresses sustainability expectations. As a result, the buyer is made aware of how much sustainable practices cost the supplier and the supplier does not have to “cut corners” to achieve a profit. As B10, a marketing manager pointed out, Socially sustainable brands hold suppliers to high sustainable standards. These sustainable practices are expensive to start and maintain. Because our long-term buyers allow us to put these costs in the open costing sheet, we can continue being socially and environmentally sustainable.

Antecedents and Consequences of Adopting Open Costing. Note. The smaller boxes within each of the five larger boxes represent the categories that define the respective emergent themes.

Applying the social exchange theory (set) framework

Participants’ use of open costing only with select buyers indicates that trust is a required BSR characteristic when using this costing method. According to the SET, if trust has not been established in a BSR, then there is likely an imbalance in the relationship’s exchange due to power differences between the two parties (Blau, 1964). Cook and Rice (2005) suggested that these differences can stem from resource imbalance and/or information asymmetry (such as cost information provided by other suppliers that the buyer has access to but the supplier does not). As Brito and Miguel (2017) argued, the buyer-supplier interaction will not be perceived to be fair by one party if a decision outcome is unilaterally in favor of the other, such as pricing a product so low that the buyer benefits but the supplier cannot make a profit. An imbalance in power was found to be a reason not to use open costing among participants in the present study, which, alongside their emphasis on trust and fairness, helps to address RQ1 (what are the reasons why suppliers may or may not practice open costing?). Participants were clearly very hesitant to practice open costing with buyers they do not trust or who behave in ways that reflect a power imbalance in the BSR favoring the buyer. Cook and Rice (2005) explained that this power imbalance in relationships typically discourages the less powerful actor from sharing more information. This is because the more powerful actor tends to exploit the shared information, using it to their advantage via their more powerful position (Brito & Miguel, 2017). As a result, the information sharing required of open costing puts the participants, as suppliers, in a vulnerable position relative to their buyers.

A supplier is one of two parties in a BSR, both of which operate on an exchange basis (Lambe et al., 2001), and expect costs as well as rewards from the relationship. The more a party is rewarded, the more likely they are to continue to participate in the exchange (Homan, 1958). In the case of the present study, the practice of open costing brings benefits to both parties and thus facilitates a long lasting BSR. Open costing allows for all of the costs that go into producing an apparel item to be made transparent and accessible to both parties, which reflects a focus on fairness in the exchange. Further, this fairness helps to ensure the supplier is both capable and willing to be flexible to accommodate production changes requested by the buyer, which are common in the apparel the supply chain, per Chaudhry and Hodge (2012). As the data revealed, flexibility and efficiency, as outcomes of the open costing approach, are rewards for both parties, which in part addresses RQ2 (what are the benefits and challenges of open costing for both parties in the BSR?). Further, the benefits of implementing open costing therefore fit the fundamental premise of participating in a BSR, which is to maximize rewards at minimal costs (Cook & Rice, 2005; Lambe et al., 2001). As an exchange relationship, flexibility as a characteristic of the BSR and one that findings suggest can be achieved through open costing, served as a stimulus for both parties to achieve the reward, which is to continue the exchange relationship. When SET (Homan, 1958) is applied to understanding the BSR, a focus on the rewards that stem from the equality in the exchange relationship can help to overcome challenges involved in open costing, such as risk and vulnerability on the part of the supplier and increased overall costs on the part of the buyer.

To further address RQ2, the interpretation of the data indicates that, along with flexibility, efficiency and sustainability are benefits that participants think can come from open costing. As the data indicate, open costing results in greater flexibility in terms of production, increased efficiency through information sharing and streamlined operations, and ultimately creates a framework in which suppliers are compensated for employing more socially and environmentally sustainable practices. Participants were motivated to use the open costing approach in the hopes that it would help them secure future business with buyers and ultimately strengthen the BSR. That is, as the extant literature has pointed out (Canon & Homburg, 2001; Chaudhry & Hodge, 2012; Cho et al., 2015), long-term oriented BSRs are more conducive to becoming competitive BSRs. As was found in the present study, open costing is a joint effort between buyers and suppliers that ultimately improves the competitiveness of both parties, in that open costing can strengthen both parties’ commitment to working together to ensure the long-term success of the BSR.

It should be noted that, as seen in the data, the use of open costing in the apparel industry is not without challenges. From the perspective of SET, the main challenge of a non-contractual practice like open costing comes from instabilities in a BSR (Lambe et al., 2001). As participants have pointed out, when engaged in open costing with their buyers, the exposure of their costing details makes them vulnerable to buyer exploitation. Moreover, from an operations perspective, while participants considered the open costing practice to be beneficial to the long-term competitiveness of their BSRs, the increased vulnerability of a supplier in sharing cost information with buyers may put the supplier at risk of supply chain disruption (Masschelein et al., 2012). Therefore, avoiding operational disruptions is a practical challenge brought about by the practice of open costing.

To address RQ3 (what does open costing mean for the BSR as a relational exchange?), based on the data, it is clear that the adoption of open costing can improve a BSR through flexibility and efficiency. Indeed, in a BSR, operations are smoother and more efficient when the behaviors of both parties are predictable. Likewise, repeated back and forth price negotiations are not necessary and therefore time and effort costs are reduced for both parties. Per Cho et al. (2015), the predictable social exchange behavior of open costing practitioners could have facilitated the cost reductions in the BSR. Open costing requires the honest exchange of information between the two parties, which, as found in this study, can help the parties avoid BSR conflicts stemming from hidden expectations, such as social and environmental compliance. It is evident that, as a BSR interaction mechanism, the practice of open costing can actually lead to increased sustainability-related outcomes.

Conclusions and Implications

Several key findings shed light on the extent to which open costing plays a role in developing a long-term BSR, as well as the relevance of SET for understanding the supplier’s perspective on the BSR. As the themes highlighted, suppliers are generally in favor of using open costing to better manage their BSRs and particularly the factors of relationship trust, perceptions of fairness, supply chain flexibility, operational efficiency and corporate sustainability. As previous SCM studies have pointed out, a well-managed BSR is an important part of SCM and one that can significantly improve a company’s performance (Huo et al., 2017). Therefore, when incorporated into a supplier’s SCM strategy, open costing has the potential to benefit both parties in the BSR, as the popularity of the open costing approach found in this study indicates that there are benefits to both parties.

Findings of this study make several contributions to the academic literature, apparel industry SCM practice, and society. From a theoretical perspective, SET helps to explain why the BSR is important to open costing, and vice versa. According to SET, all types of social interaction between people are exchanges of resources (Homans, 1958). The motivation for parties in a relationship to engage in an exchange is driven by their particular exchange needs (Emerson, 1976). In the context of the present study, a higher level of collaboration (i.e., the use of open costing) with the buyer is the reward the supplier gains from the exchange. In this case, and according to SET, the risk of the buyer’s abuse of open cost information is the cost of the exchange. Per the tenets of SET (Homans, 1958), the desire to exchange could be tangible (money, materials, etc.) or intangible (partnership, collaboration, etc.). The intangible needs of the two relationship parties are met through sharing open costing knowledge, which as Lambe et al. (2001) pointed out, enhances the quality of the BSR. Therefore, through the exchange of open costing knowledge in BSR interactions, both parties believe open costing results in a reward that is greater than the cost for them individually or collectively. The open costing practice improves their overall efficiency and thereby reduces costs internally as well as externally.

Given the hyper-competitiveness of the global apparel industry, the idea of open costing may seem risky at first glance. However, the supplier’s net gain from the adoption of open costing in the BSR leads to its repeated use, which is a clear indication that the open costing practice has a positive influence on the BSR (Cook & Rice, 2005). The idea that BSR collaboration leads to a competitive advantage for both parties is a motivation for them to continue practicing open costing. Thus, open costing can result in better relationship outcomes, both financially and non-financially, and, in turn, encourage both parties to develop the BSR over time. In SET, Homans (1958) and Blau (1964) argued that for a social exchange relationship to last, the relationship parties should be equal and the exchange outcomes should be as expected. The results of the present study indicate that perceived fairness (or equality) in a BSR makes suppliers more willing to invest in long-term relationships that achieve expected outcomes (Elfenbein & Zenger, 2014). Consequently, both the buyer and the supplier engage in opportunistic kinds of behaviors less frequently (Whipple et al., 2010). As the findings of the present study suggest, the fairness that allows for the use of open costing is essential to building a long-term BSR.

Participants strongly emphasized that trust is the foundation for the open costing mechanism, both in terms of their trust of the buyer as an antecedent of the decision to use open costing, and as a characteristic of the BSR exchange. Results of this study indicate that the practice of open costing helps build mutual trust between a buyer and a supplier because the supplier must be convinced of the buyer’s credibility before and during the implementation of open costing. Findings revealed that fairness is vital in a BSR, in that suppliers view fairness as a prerequisite for the open costing practice to be successful. Findings also indicate that open costing increases flexibility in the supplier’s order handling and production cycle. That is, once trust and fairness have been established, and operational procedures have been standardized, open costing can lead to increased efficiency in the BSR exchange, primarily because improved buyer-supplier interactions can reduce overall production lead times. Finally, from participants’ perspectives, open costing increases the sustainability performance of the supplier’s SCM by properly compensating the supplier’s sustainability costs. As a result, open costing can help avoid the typical conflict that arises when buyers expect social and environmental compliance but are reluctant to pay the costs suppliers must incur to be compliant. Overall, the results indicate that open costing is important to building a strong BSR and one in which the two parties collaborate rather than compete with one another.

Limitations and Future Research

Findings of this study contribute to the existing apparel SCM literature in terms of understanding the mechanism and practice of open costing and specifically from the perspective of suppliers operating in China and Bangladesh. Because this study was exploratory in nature, and among the first to examine the practice of open costing in the apparel industry, any generalization of the results should be made with caution. Likewise, although findings suggest that the implementation of open costing will enhance the BSR, given the specific focus on the apparel industry, results may not apply to other industries. Due to the limited current research available on open costing, further empirical study of the causal effects of open costing on the BSR is needed, and particularly studies that examine its impact on BSR collaboration and overall supply chain performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.