Abstract

This article belongs to the special cluster, “Politics and Current Demographic Challenges in Central and Eastern Europe,” guest-edited by Tsveta Petrova and Tomasz Inglot.

We explore housing finance and policy in East Central Europe to understand the connection between housing, in particular independent household formation, and the demographic crisis. The combination of high debt-free homeownership rates with illiquid housing finance and limited rental markets produces conditions where housing restricts independent household formation and likely has a restrictive effect on fertility. We first assess the housing regime type in East Central Europe and demonstrate that it closely corresponds to the “difficult housing regime” in Southern Europe, which has well-established negative effects on independent household formation and fertility. Then we present a detailed case study of Hungary, which is a country with very low fertility rates and substantial changes in housing finance and policy over time. In particular, the issue was recently politicized through housing policies centered on household formation to counter the demographic crisis. We present a detailed analysis of policies related to access to housing for young adults through increased access to markets or state housing support schemes. These policies attempted to reduce dependence on families, but after the crisis, we find that these policies reinforce, rather than challenge, dependence on families for housing solutions, thereby limiting independent household formation. While these policies may serve a rhetorical role demonstrating a state response to the demographic crisis, we claim that their impact on fertility can be at most minimal because of stringent restrictions in access that concentrates on upper-middle-income households and limited financial commitment.

Introduction

According to recent United Nations Data, the “10 fastest shrinking countries on earth are in Eastern Europe,” 1 surpassing even Japan, the country that has been associated with the most severe demographic challenges in recent decades. It is therefore no wonder that a number of governments in the region have identified halting the demographic decline as a policy priority. Although the demographic decline has many causes, most importantly low birth rates, massive emigration, and limited immigration, policy makers in the region are reluctant to challenge the free movement of their citizens, and skeptical or even outright hostile to accepting immigration. As a result, they most often seek to address low birthrates through financial incentives and (traditional or pro-natalist) family policy measures. 2

What explains the low fertility in Eastern Europe, and how likely are these policy measures to redress the situation? Traditionally, explanations of low fertility focus on the uncertainty inflicted by the regime change, deteriorating labor market opportunities, and the collapse of socialist enterprises that were largely responsible for running child care facilities. Some of these major upheavals have led to postponement of childbearing and, concomitantly, a decrease in higher-order birth. 3 Our article, in contrast, focusses on a critical, but often neglected, factor. It seeks to shed light on how the housing regimes in Eastern Europe contribute to the difficulties of independent household formation and exacerbate the demographic crisis.

To this aim, we build on recent scholarship on how housing regimes affect household formation and fertility. 4 This literature argues that access to housing is crucial for independent household formation and analyses the mix of the role of markets, states, and the family that allow for or inhibit easy access to housing. Building on this literature, we will show that Eastern Europe’s post-socialist housing regimes share crucial features with the South European ones, where high homeownership, limited access to affordable mortgages, and limited rental markets makes access to housing exceedingly difficult for young people. Rather than being able to rely on market or state resources, they have to turn to their families for housing provision.

We also seek to understand how policy changes have affected East European housing regimes and what has been the impact on independent household formation. Policy makers in the region have pursued two prominent approaches to ease access to housing for young people: increasing the role of markets in providing mortgage finance and providing generous state subsidies for young families. Honing in on the Hungarian case, where governments have made ample use of both of these policy approaches, we evaluate the degree to which each approach has eased independent household formation.

The article is structured as follows. The following section provides a bird’s-eye view on Eastern Europe’s fertility crisis. In the third section, we introduce the concept of housing regimes and discuss the links between housing regimes and fertility. The fourth section focusses on the case of Hungary, which we select because of its potential for overcoming the challenges posed by its difficult housing regime through both major shifts in housing finance and substantial state policies supporting housing for young people. We evaluate the extent to which Hungary could overcome the limitations that its difficult housing regime poses on independent household formation through market mechanisms and state housing subsidies. The final section concludes and summarizes how the effects of the crisis and the subsequent policy changes have even reinforced challenges that young people face in independent household formation in East Central Europe (ECE).

A Bird’s-Eye View of Eastern Europe’s Demographic Crisis

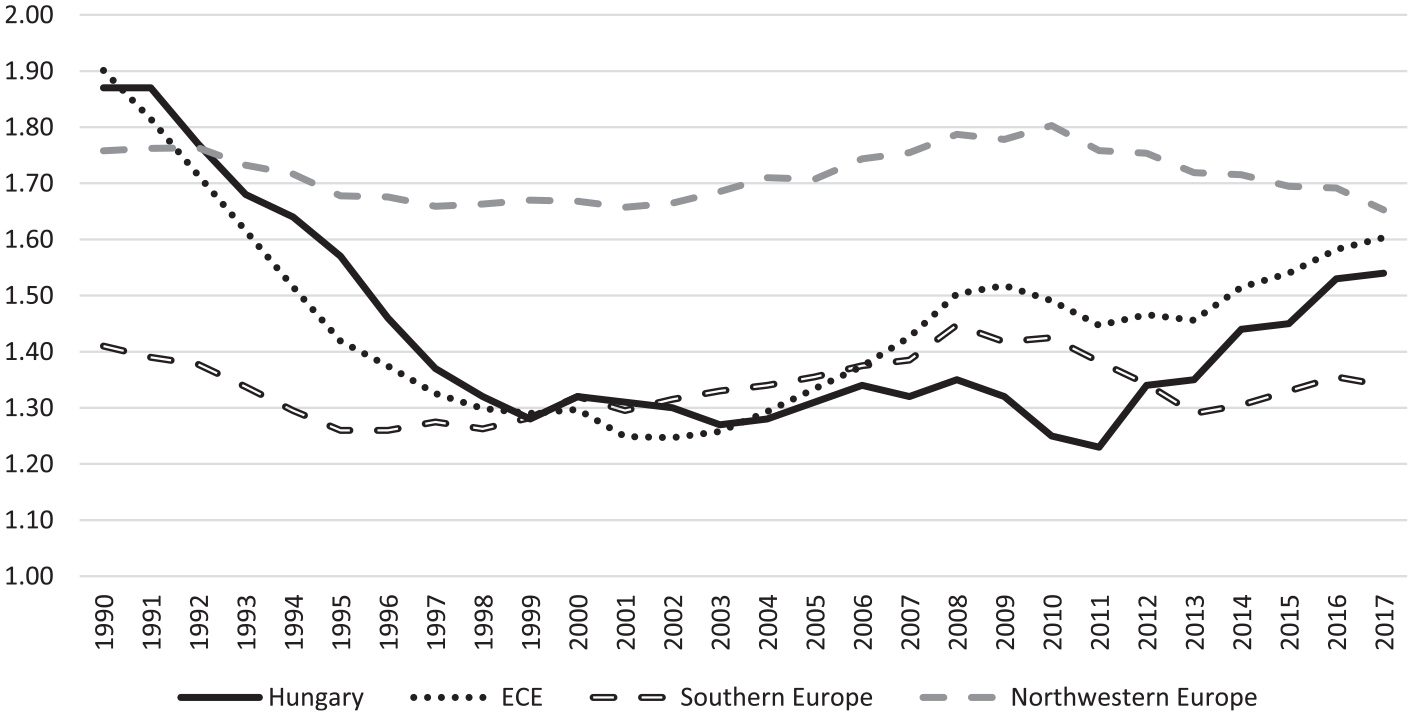

ECE countries exhibit some of the lowest fertility rates among the OECD countries. While fertility in Eastern Europe still hovered around the replacement rate in the early 1990s, the transition had a detrimental impact (see Figure 1 5 ). By the early 2000s, almost all ECE countries were characterized by very low fertility rates of fewer than 1.3 children per family. Fertility rates began to rebound around 2002–2004, but a second decline occurred in the wake of the financial crisis. Since 2011, we detect another rebound in fertility rates. The substantial increase since 2011 may also be driven by a reduction in the number of people of childbearing age due to population decline and outmigration. 6 Evidence suggests that young people migrating from ECE to Western Europe have higher fertility rates than those staying at home. 7

Total fertility rate, 1990–2016

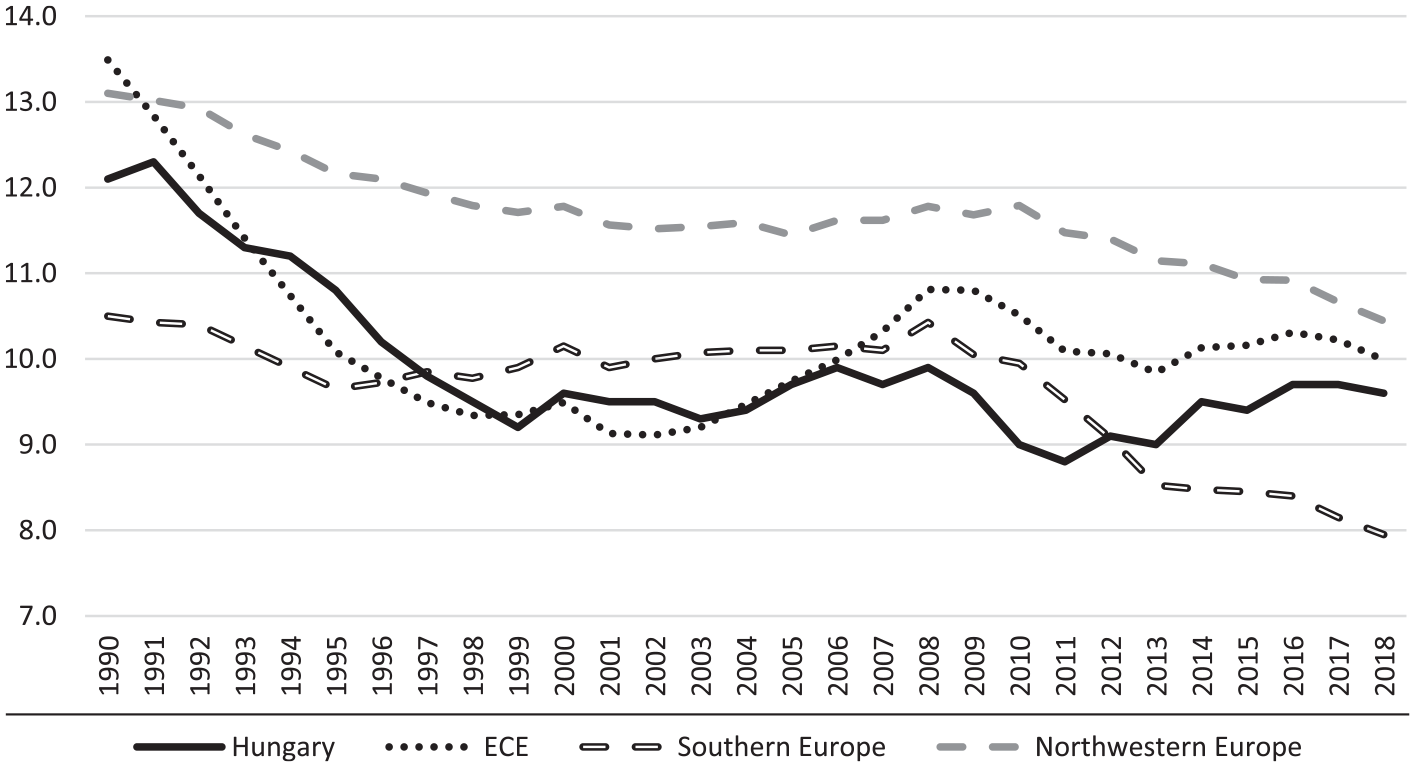

For this reason, together with fertility rates, it is important to consider the birth rates, which are shown in Figure 2. Here we detect a similar pattern, but the post-crisis recovery looks more meager in ECE overall and in Hungary in particular. Given that fertility rates remain well below replacement rates and the recovery of birth rates for ECE are much less promising, we detect an ongoing demographic crisis.

Crude birth rate (live births as a share of population, per 1000 people)

Fertility rates depend on a multiplicity of factors, and an extensive explanation of shifts in fertility is beyond the scope of this article. In a study of fertility in postcommunist countries, Billingsley considers three explanations for the decline: a second demographic transition, reaction to economic recession, and postponement of childbearing. 8 The variation in experiences across countries with similar demographic conditions refuted the second demographic transition argument. Billingsley finds mixed effects of the economic factors, with economic improvements leading families to postpone the first child, but expediting higher-order births. The main argument is that the decline in fertility in postcommunist countries results from “postponement of childbearing on the one hand and a decline in higher order births on the other.” 9 While economic factors have complex effects on childbearing, access to adequate housing is an oft-neglected factor with a clear effect on postponement of childbearing. The next section seeks to shed light on how Eastern Europe’s postsocialist housing regime might have contributed to the dismal demographic outcomes.

Difficult Housing Regimes in Eastern Central Europe and Demographic Outcomes

In a Green Paper on Europe’s difficult demographics, the European Commission singles out housing as one of the factors responsible for undesired low fertility. “Europeans would like to have more children. But they are discouraged from doing so by all kinds of problems that limit their freedom of choice, including difficulties in finding housing.” 10 But what explains housing provision and access to housing, and how does it impact independent household formation, and therefore, fertility? The literature on housing regimes has provided some answers to this.

Housing Regimes

There is a longstanding debate in the literature on the relationship between the welfare state and housing. Three closely related but distinct strands of discussion can be distinguished. First, some authors focus on the role of housing within the welfare state. Here, authors conceptualize housing as a public service and analyze how it “compares with other service areas in terms of scope, reach and condition of access.” 11 The focus of this research is on public social housing, and it is concerned with the question of why housing has never become as removed from the market (i.e., decommodified) as other welfare state services. 12

A second strand of research looks at the interaction of housing and welfare. Here, housing is understood as being separate from the welfare state proper. Most famously, Kemeny argued that there was a trade-off between homeownership and generous pensions. In societies where homeownership is prevalent, households who have to put up a lot of money upfront early in their life to purchase housing are reluctant to finance a generous welfare state. As homeownership however reduces housing costs later in life and as housing capital can be used to pay for health or care expenses, households are also not in need of generous public pensions. The opposite is the case in societies that have a large rental sector and where housing costs are distributed more equally over time. 13

The third strand of literature looks not so much at the relationships between welfare and housing, although this is an important aspect of this strand too. Its core however is elsewhere, in that it seeks to apply the insights generated from comparative welfare regime research for analyzing housing systems. Drawing on Esping-Andersen’s definition of welfare regimes as forming distinct clusters that differ in the quality of social rights and the relationship between state, market, and family, these authors differentiate housing regimes, which partly overlap with, and partly differ from welfare regimes. 14 Below, we present two such approaches, which will be the building blocks for our understanding of post-socialist housing regimes.

The first approach is the influential varieties of residential capitalism typology developed by Schwartz and Seabrooke. 15 These authors classify national housing systems according to two broad criteria: ownership (which might be private, public, communal, cooperative, or familial) and access and ease of mortgage credit. They distinguish between four varieties of residential capitalism. The first, liberal market type, is characterized by high levels of homeownership and mortgage debt, and liberal mortgage markets. In this model, markets play the major role in granting access to housing and housing provision. In contrast, in the statist-developmentalist model, homeownership is comparatively low, and mortgage finance highly repressed. Here, the state plays the major role. The corporatist-market capitalism has comparatively low levels of homeownership and a sizeable cooperative or social rental sector. While the levels of mortgage debt are high, mortgage markets are highly regulated. In this model, the cooperative sector interacts with markets. Finally, familial residential capitalism has very high homeownership levels but low mortgage debt. In this model, families pool resources to enable access to housing. These four models show partial, not full, overlap with the familiar welfare clusters.

The typology presented by Mulder and Billari 16 also draws on the welfare state typologies and the literature on housing systems, and as such shares some similarity with the Schwartz and Seabrooke typology. However, the authors were interested in the impact of housing regimes on fertility. Their typology, therefore, answers the question “how well . . . housing markets, and particularly the organization of homeownership, allows a smooth first entry of young people.” 17 Housing entry can be based on a large rental or a widely accessible owner-occupied housing. For the latter, access to mortgage finance is crucial. Based on these considerations, the authors define four homeownership regimes: the “career homeownership,” where homeownership is not universal, and typically not the first housing tenure, but mortgage finance is available. Households acquire their first homes only once they have stable income. However, given that alternatives to homeownership exist, housing is accessible also for young households. The “elite homeownership” regime is similar in that homeownership is far from universal, and that renting is widely accepted as an alternative to homeownership. In contrast to the career homeownership, however, mortgage finance is not broadly available. The third, “easy homeownership” regime, combines widespread homeownership with wide availability of mortgages. Thus, despite high homeownership, access is also easy for young households. Finally, the “difficult homeownership regime” equally has a high share of homeownership, but low access to mortgages. Housing can thus only be accessed via personal savings or family resources. At the same time, the rental sector is very small and does not provide an alternative.

As stated, the main aim of Mulder and Billari is to explore the links between housing regimes and fertility. They postulate that access to housing is the main variable that matters as access can constrain or enable independent household formation and thus, indirectly, fertility. They also show that there is indeed an association between homeownership regimes and fertility rates, albeit mostly in countries with the easy and the difficult regimes. Thus, in countries with the easy homeownership model, total fertility rates are substantially higher than in the other models. In contrast, the countries with difficult homeownership regime, where homeownership is “not only the norm, but also almost the only way of obtaining housing for a family,” 18 have the lowest fertility rates.

These authors identify most Southern European countries as having difficult homeownership regimes. While they also mention the Central Eastern European countries, they argue that housing regimes in these countries have not yet settled. Below, however, we build on existing literature on East European housing regimes to establish that they exhibit similar feature as the Southern European difficult (or familial) homeownership regimes.

Difficult Housing Regimes in East Central Europe “by Default”

This section will show that Eastern Central Europe has traditionally been caught in rather extreme vicious constellations of illiquid housing finance markets and an overreliance on family resources for access to housing, which parallels the more frequently studied Southern European model. 19 While the paths to becoming housing systems with low debt and high homeownership differed markedly between Southern Europe and ECE, 20 the resulting features of limited rental markets and limited access to private finance implies similar impacts on independent household formation. As argued by Stephens et al, the emergence of a difficult housing regime occurred “by default” 21 rather than as a set of deliberate policy decisions. Nevertheless, we claim that there is a notable resemblance between Southern Europe and ECE on the characteristics of the housing regime that have an impact on independent household formation, and therefore fertility. In this section, we highlight some common features of the ECE homeownership regime and compare them to Southern Europe. 22

Most ECE countries exhibit very high homeownership rates with a low share of the population holding mortgage debt, as shown in Figure 3. They thus exhibit a high degree of debt-free homeownership, clustering in the lower quadrant with Southern European countries, consistent with Schwartz and Seabrooke’s typology. 23

Share of population that owns their home and has a mortgage (of total population), 2005

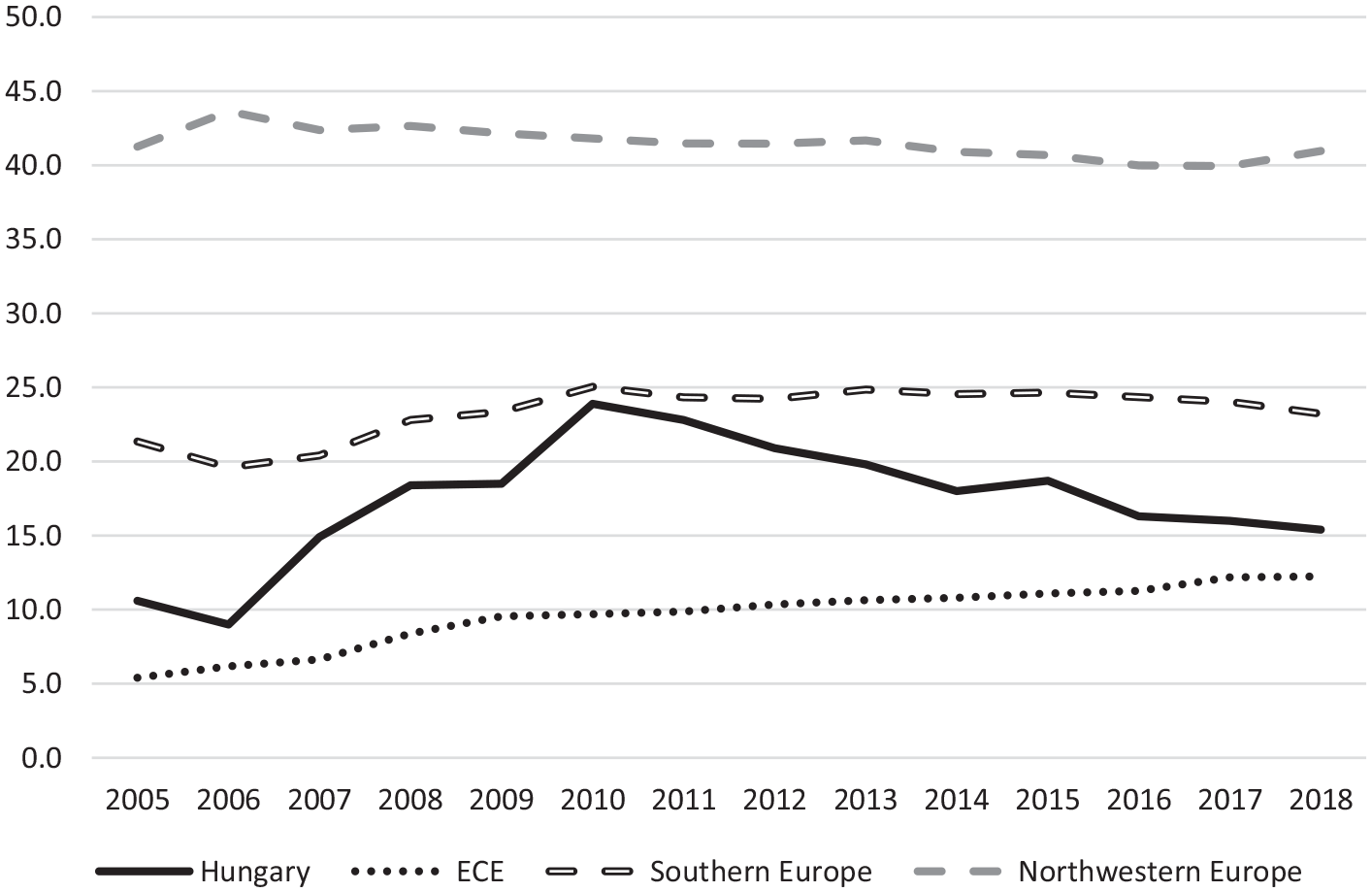

Taking a look at the share of the population with a mortgage over time reveals consistently lower levels in ECE (about an average of 10 percent) and Southern Europe (about 20–25 percent) compared with Northeastern Europe (about 40–45 percent) (Figure 4).

Share of the population with a mortgage over time.

This demonstrates that in ECE and Southern Europe, the share of households relying on mortgage finance remains significantly lower than Northwestern European countries. The alternative indicator of outstanding residential loans per capita shows similar patterns (see Figure A1 in the appendix), but is a less reliable indicator for comparison over time because of dramatic changes in the denominator around the financial crisis.

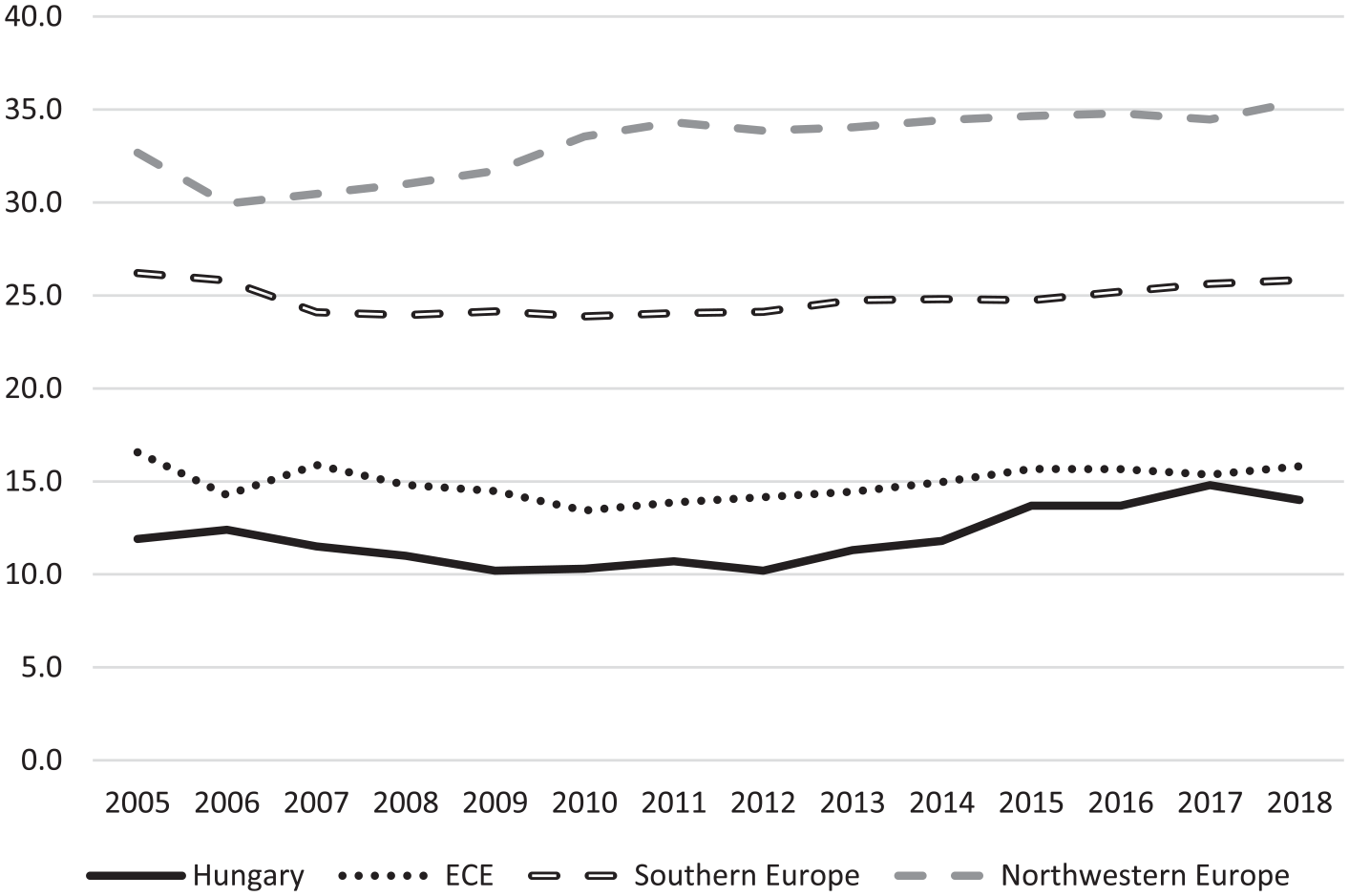

The limited scope of opportunities to live in public or private rental housing is another feature of the difficult housing regime in ECE. 24 As shown in Figure 5, the rental market is minuscule in ECE, compared with both of the other regions. 25

Share of population representing tenants in rental housing

Overall, we see that the housing regime in ECE faces similar challenges as the Southern housing regime. Where there are differences, the difficulties faced in ECE are more extreme, but point in the same direction as in Southern Europe. Specifically, debt-free homeownership, combined with limited access to housing finance, and a small-scale rental market, creates high dependence on families or state support to assist in financing homeownership.

Undoubtedly, the historical paths to difficult housing regimes in Southern Europe and ECE differ, and these legacies are vital for understanding the path to debt-free homeownership and the lack of urgency of the development of institutions for housing finance.

The Southern European paths to difficult housing regimes are closely linked to the region’s late industrialization. 26 While after the Second World War a process of rural depopulation began, cities only offered precarious jobs, forcing recent city dwellers to look for cheap accommodation, who found it in the form of “low standard, owner occupied dwellings, self-built or otherwise acquired. As a consequence, home ownership in Southern Europe is very high among low-income groups.” 27 Late and limited industrialization and the concomitant weakness of state capacity can also account for the fact that the Southern European states have not strongly engaged in the promotion—let alone development—of a social rented sector. Most Southern European countries launched major public housing programs after World War II. However, they were sooner or later sold to tenants, often at low prices. Promoting homeownership rather than social rentals was also a device to achieve social stability.

The specific Eastern European housing regime is of recent, post-communist origin. Under socialism, the state took a leading role in providing large-scale housing. In most cases, public housing development was “limited to small, standardized, low-quality, prefabricated apartments in pre-cast concrete high-rise buildings . . . in high density zones on the periphery of cities.” 28 There was also a shortage of housing, as the state was unable to meet the demand for housing associated with fast industrialization and urbanization. As a consequence, “cracks” appeared in the socialist housing system, which governments either tried to address with increasing control of access to housing, or the gradual implementation of quasi-market mechanisms, as in Hungary or Yugoslavia. 29 Thus, while public housing remained the main form of ownership, in some countries segments of private or quasi-private housing already existed under socialism. Both sectors were however heavily regulated.

The high homeownership rates in Eastern Europe are therefore a direct result of transition policies and the “emphatic retreat of the state.” 30 Indeed, transferring the predominantly public housing stock into private hands was among the first steps undertaken by post-communist governments. The most common method to transfer the housing stock was to sell it to current occupants at low prices. In addition, restitution of property also reinforced private homeownership. 31 Policy approaches to public housing in early transition resulted in high rates of debt-free homeownership and a severely underdeveloped social and private rental sector in most ECE countries.

There are many reasons for the fast and encompassing privatization of housing in Eastern Europe. Among politicians and the general public, private homeownership was considered the norm, and large-scale public housing stock a socialist aberration. At the same time, the neoliberal orientation of most early transition governments, and the involvement of the World Bank and IMF in early reforms, has further boosted the normative power of private homeownership. 32 A third reason for fast privatization is that private housing acted as a “shock absorber,” making it easier for the population to cope with the shocks of transformation. 33 Finally, fast privatization of the public stock also relieved the state (or local governments) from the burden of having to manage large housing stocks in the turbulent transition times under fiscal constraints. 34 All in all, “privatization could not have been avoided, because all social forces were in favor of it at the time; in fact it is in all actors’ short-term interests even today.” 35 The result was that most ECE countries ended up with extremely high homeownership rates.

Two by-products of the decisions related to housing privatization further enforced the emergence of a difficult housing regime. First, the “creation of a nation of largely debt-free home-owners meant that there was less urgency in the creation of housing finance systems.” 36 Second, the prevalence of debt-free homeownership limited the opportunity for developing a private rental sector. The state rental sector from the socialist period could have been transformed into a social rental sector, but any attempts to do so were limited and short-lived. 37 The social rental sector that existed was a financial burden on the states or local governments, and privatization of these units was a tempting source of revenue during the transitional recession. 38 Therefore, these homes were also privatized, reinforcing the model of debt-free homeownership and restricting the future availability of social rental homes. We link this difficult housing regime to independent household formation in the next section.

Linking Homeownership Regime to Demographic Outcomes

What are the links between homeownership regimes and demographic outcomes? As already discussed above, difficult housing regimes delay and limit independent household formation. This postpones the birth of the first child and thereby often decreases higher-order birth, which has a depressing effect on fertility. 39 In this section, we summarize the data on independent household formation to show that young people in difficult housing regimes indeed tend to delay or refrain from independent household formation. We consider three forms of support for young people aiming to form independent households: family-based, market-based, and state-based.

The factors that explain when individuals leave home include individual characteristics (education, employment status), parental characteristics (such as parental education level or role model), and macro-level contextual factors. 40 There are also multiple paths to depart from home, including with or without a partner. 41 Based on these studies, which included ECE countries, we observe that in ECE countries, leaving home is closely linked to formation of partnership and that, in these countries, the macro-level factors were more significant than individual or parental factors. 42 The dominance of macro-level contextual factors suggests that individual decisions are substantially curtailed by structural factors, and most importantly for this article, the structure of the housing (finance) system.

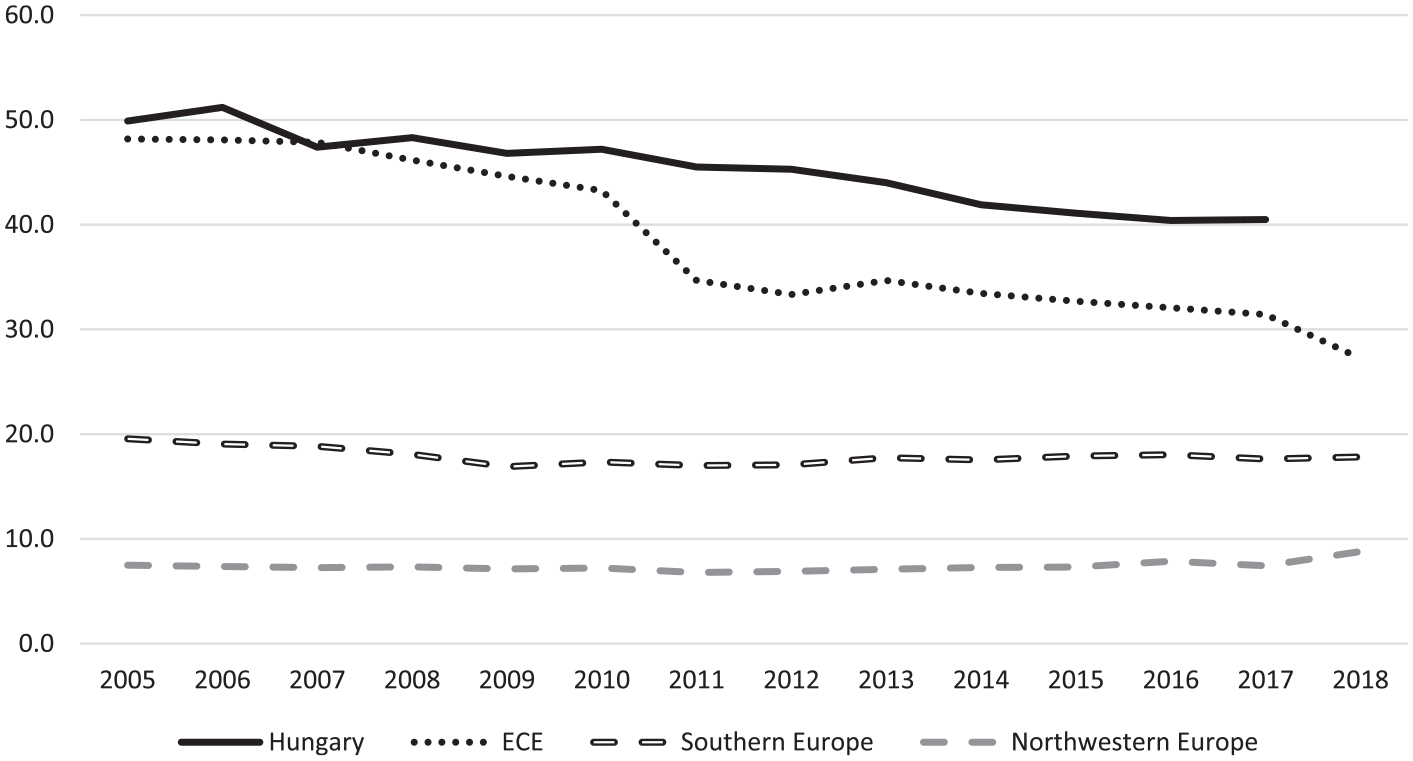

The difficult housing regime that emerged as a result of fast privatization of the housing stock in Eastern Europe is one of the driving forces behind the high share of young adults living with their parents in ECE (see Figure 6) and delayed household formation (see Figure A2 in the appendix). The levels of both indicators are very similar to Southern European countries. As houses cannot easily be bought and sold on the market, mortgage credit is not easy to come by, and affordable renting is not an alternative, buying a first home is likely to be considered an investment for a lifetime. 43 The legacy of housing shortages has made it additionally problematic for young people to leave their homes at an early age.

Share of young adults aged 18–34 years living with their parents, 2005–2016

In many ECE countries, including Hungary, the age of leaving home is close to the age of moving in with a partner, but then on average there is a delay before having children. 44 This suggests that many young adults are remaining in multigenerational households and postponing having the first child. The decision to postpone fertility could likely be a result of overcrowding of homes (see Figure 7), which also tends to result in lower fertility. 45 East European countries stand out in the share of the population living in overcrowded homes.

Overcrowding rate for all households, 2005–2016

Overall then, in ECE, “it is often through the [intergenerational] transfer of dwellings that members of the younger generation are enabled to start their own household.” 46 Household formation occurs at a very late age and depends heavily on intergenerational support. Young people’s high dependence on families includes provision of housing through multiple generations living together or to assist in financing the purchase of a first home. Mulder and Billari’s framework clearly demonstrates that family-based housing regimes bring about the lowest fertility.

How is it possible to overcome difficult housing regimes as a fertility trap? Market-based and state-based solutions remain. Writing about the problematic consequences for fertility that this model of family dependency has, Mulder and Billari 47 argue that two types of policies could be envisaged to enable younger cohorts to move out at an earlier age: the development of affordable rental housing or expansion of mortgage provision, such as mortgage guarantees and encouragement of bank lending. State programs promoting affordable rental housing have been in decline in many Western European countries, and such programs are largely absent from ECE as well. 48

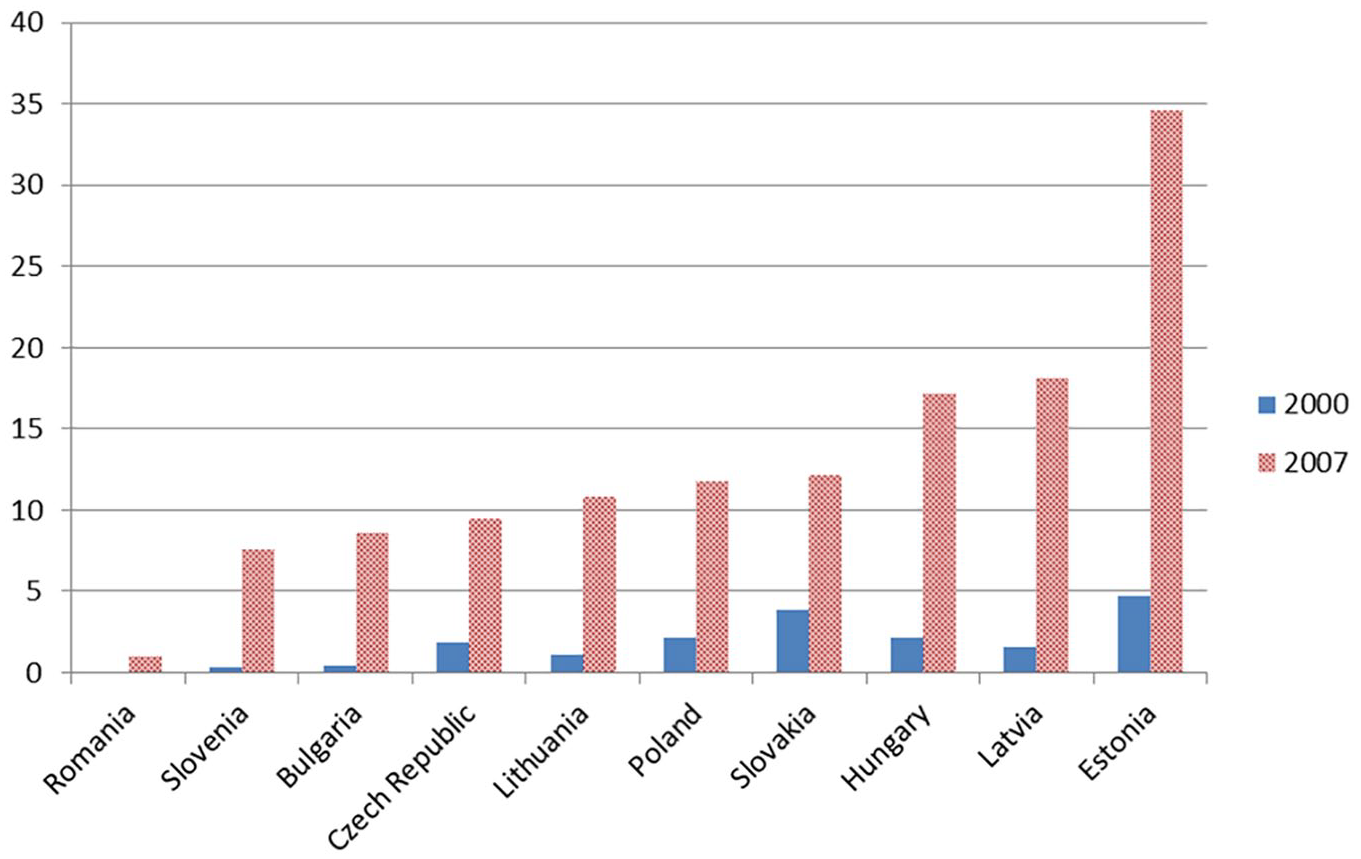

Stephens et al. however highlight important differences between the Southern European and ECE housing regime based on the importance of “state legacy welfare,” in addition to intergenerational support. 49 Various policy efforts did attempt to support access to homeownership through state programs and through the development of mortgage markets. In Eastern Europe, there is a notable emphasis on policies encouraging easier and more widespread mortgage provisions for some countries. Figure 8 shows the change in residential mortgage debt as a share of GDP from 2000 to 2007 for individual countries within ECE. It is noteworthy that over the 2000s, mortgage debt has risen significantly in Eastern Europe. Estonia has demonstrated the most remarkable increase in residential loans from around 5 percent in the early 2000s to above 40 percent in 2010, with Hungary and Latvia following suit.

Residential mortgage debt as a share of GDP, 2000 and 2007

The remainder of the article will explore whether market or state approaches to the expansion of access to housing finance and homeownership eased independent household formation through a case study of Hungary. The next section discusses the expansion of mortgages with the Hungarian example and investigates its effects on easing independent household formation. As we investigate the potential of markets or state to reduce the dependence on family for housing, we select the case of Hungary as a most likely case for policy effects on independent household formation given the strong political emphasis on both private and state-supported means of promoting homeownership.

Escaping the Difficult Homeownership Trap? A Case Study of Hungary

In this section, we review possibilities for overcoming the restraints of difficult homeownership through a case study of Hungary. The next two subsections focus on the Hungarian context to see the effects of markets and state housing policy, respectively.

Liberalizing Mortgage Markets in Hungary

As in other East European countries, it was only at the end of the 1990s that Hungarian public policies explicitly targeted the development of mortgage markets. This occurred in two phases. During the first phase, the state played a key role in subsidizing mortgages (see next subsection), while the second phase relied more on banks’ profit motives to supply mortgages. Most important for the first phase was the introduction of a generous housing loan subsidy program under the first Orbán government (1998–2002). This program allocated substantial resources for interest rate subsidies on long-term mortgage loans. The continuous expansion of the program, however, turned out to be financially unviable. 50 From 2003 onwards, the government cut the tax exemptions for mortgage repayment and reduced the scope of the housing loan subsidies.

It is at this moment that banks stepped in. The first movers were Austrian banks, which aggressively developed mortgage lending, engaging in ever more risky lending practices. Borrowing from their mother companies or wholesale money markets, these banks issued foreign currency loans, mostly in Swiss francs. These had the advantage of lower interest rates compared to loans in Hungarian forints. At the same time, however, homeowners shouldered the currency risk. 51 In terms of conditions, the average loan-to-value ratio was around 60 percent in 2007, and banks could grant mortgages with a maximum 75 percent loan-to-value ratio. As the mortgage market segment was very lucrative and competition between banks was intense, banks also started to become more relaxed with regard to their lending standards. A commercial for the Austrian Raiffeisen Bank showing the bank representatives covering her ears every time her customers mentioned the word down payment illustrates the lax attitude of banks. 52 The loan maturity was freely agreed on between lender and borrower, and typically amounted to fifteen to twenty years. For first-time home buyers, the mortgage lender FHB Bank calculated that they pay 6.3 times the average yearly income after taxes for their house. 53

Despite the take-off of mortgage lending, an improved macroeconomic environment and explicit pro-natalist policies, we see virtually no effect on the share of young adults living with their parents (Figure 6). What might explain this?

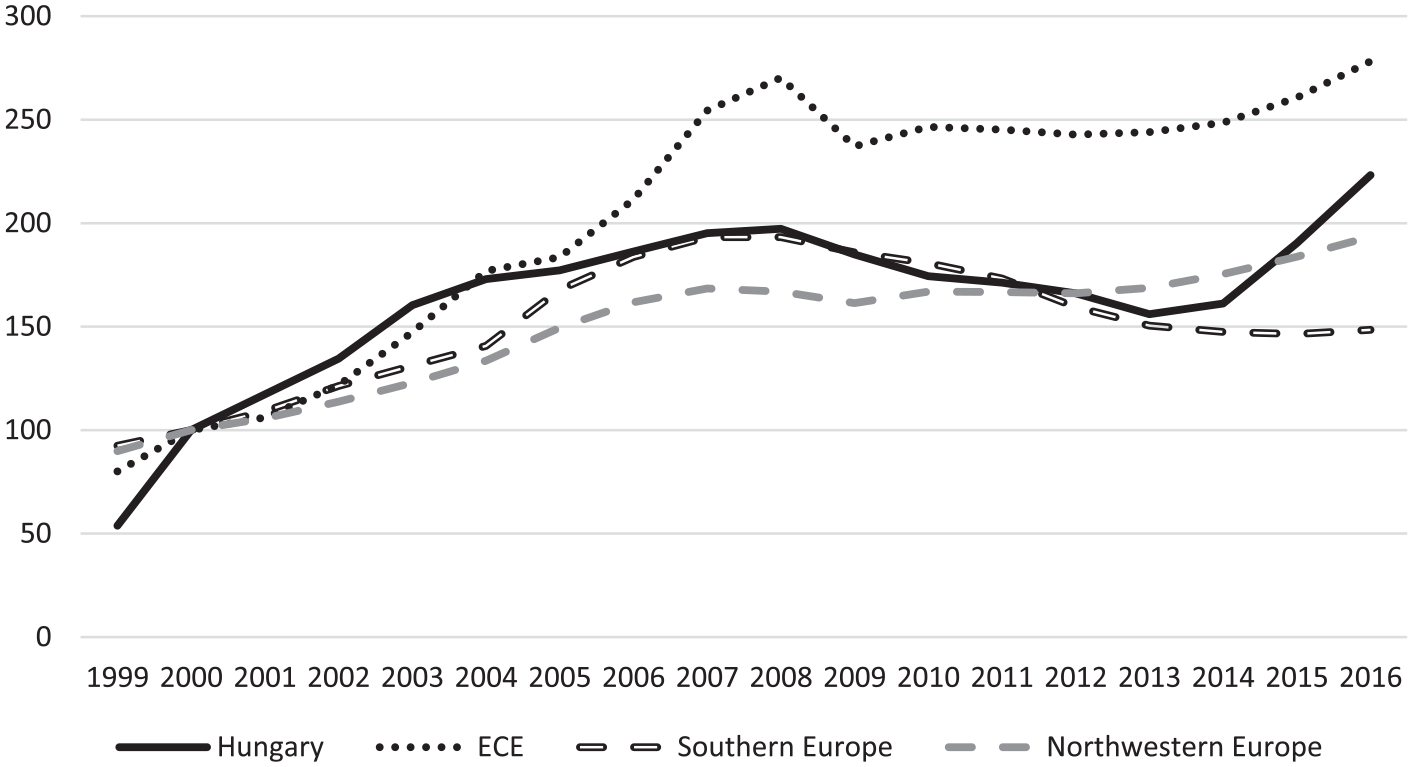

A first explanation might be that housing construction has not followed the rising demand. The building of new homes picked up significantly during the period of state-subsidization from 2000, but peaked already in 2004. 54 Given that Hungary had inherited a serious shortage of housing from socialism and the first decade of transformation, housing arguably was still in short supply. Another factor limiting housing supply was a massive increase in foreign demand. German, Austrian, Irish, Spanish, and Russian small investors started to move into the Hungarian housing market (mostly in the capital city and some tourist areas) to buy homes and rent them out (ibid.). Finally, house prices also increased significantly during the 2000s, making housing not easily affordable for first-time buyers (Figure 9).

Nominal house price (base year 2000 = 100)

All in all then, public policies and private market actor activities in the 2000s did allow more people to take out mortgages. However, this had no demonstrable effect on the age of emancipation. What is more, the financial crisis of 2008 onward put an end to banks’ mortgage lending.

In 2008, Hungary had to turn to the IMF when its banking sector faced a liquidity crisis resulting from the turmoil in the foreign currency swap market. 55 The recession and “unorthodox” economic policies under the second Orbán government (2010–2014) had detrimental consequences for housing affordability and mortgage lending. 56 In the wake of a severe recession and the rapid appreciation of the Swiss franc, an increasing number of households were unable to service their debt. Nonperforming household loans steadily increased, reaching 17 percent in 2015. 57 The government sought to alleviate the burdens for households with foreign currency loans. In 2011, it introduced the possibility to exchange foreign currency loans in forint at a preferential exchange rate for debtors who could repay their debt in one stroke and introduced an exchange rate protection mechanism where repayments were calculated at an advantageous fixed exchange rate. In late 2014, the government forced almost all debtors to swap their forex loans into local currency at the then current rate. 58

In addition to dealing with the forex loans, the government also imposed special taxes on banks, insurance companies, and other financial services. These taxes, levied from 2009 onward, were only lowered in 2015. In turn, credit institutions had to pledge to increase lending to the corporate sector, especially to SMEs, rather than to households. 59 Furthermore, in 2014, legislation also took on unfair banking practices, which forced banks to pay significant compensation to indebted households. 60 Given this, it is hardly surprising that banks have drastically reduced their lending activity. Lending to households in Hungary dropped by 14 percent between 2008 and 2013. 61 Market-based mechanisms to facilitate access to homeownership did not lead to any decrease in the share of adults living with their parents (Figure 6), and there has been a steady decline in the share of households with mortgages since 2010 (Figure 4).

Promoting Housing for Young Families through Policy Interventions

The difficulty of independent household formation has been recognized by policy makers in Hungary and has even been directly linked to demographic concerns. Multiple policy programs sought to ease access to mortgages for young people, which matches the needs within a “difficult housing regime,” characterized by high homeownership and difficult access to mortgages (combined with limited rental markets). However, the effects of these programs have been minimal for two reasons. First, before the crisis, the scope of the funding was so limited that it could not liberate young people from dependence on family for housing finance. Second, the benefit schemes often targeted higher-income groups and demonstrated a clear priority to encourage fertility among only specific sections of the population (identified by income, which is notably correlated to ethnicity).

Ever since 1971, Hungary has a policy tool in place that is intended to increase fertility through supporting homeownership among families with children (szociálpolitikai kedvezmény, “szocpol”). Indeed, this tool, which comprises a direct cash subsidy for home purchase, proportionate to the number of children and independent of family income, is the only socialist housing policy tool that was still around during the 2000s. Its structure reflects the housing regime in Hungary in that it emphasizes promoting homeownership among young people. The generosity of this benefit and its importance within the housing policy mix has fluctuated over time, reaching an apex in the 1990s, experiencing a scaling back between 2000 and 2002, a brief revival around 2005, gradual decline after 2006, an almost complete abolition in 2009, and a comeback in 2012. The introduction of mortgage subsidies by the first Orbán government from 1999 on brought a decline in the relative and also absolute importance of szocpol. However, it has to be noted that mortgage subsidies initially also had a “natalist” element—only young couples (under thirty-five) or couples with children could apply, but these conditions were softened later on. 62 Besides, the natalist stance of the Orbán government was intended to favor the middle class, and that was easier to achieve by family-friendly taxation and home-buying related tax breaks. 63 From the perspective of independent household formation, however, these programs were ineffective, as they alleviated a small fraction of the cost of housing. This meant that the dependence on family for housing remained.

The support for the policy programs assisting young families remained even after a change in government. The socialist-liberal government coalitions between 2002 and 2006, despite rolling back other mortgage subsidies, increased spending on szocpol and introduced a new program that supported the purchase of newly built flats. The related program (“Nesting” program, “Fészekrakó program”) also included some rental support for low-income families, but the impact of the program was limited by the fact that the rental market in Hungary is mostly informal, and landlords would be required to pay tax on the income generated by renting the apartment through a social rental program. However, this program was suspended as a part of a broad austerity reform in 2009.

After Orban returned to power, the szocpol program was reintroduced in 2012. While this could be framed as policy continuity, the new policy was sufficiently different to be considered as a “politically-driven legislative intervention” 64 to respond to insufficient demand for new housing units and the politicized demographic crisis. In 2015, the third Orbán government expanded this program that prioritized families with at least three children, also giving it a new name: the family home establishing allowance (CSOK 65 ). CSOK reflects many elements of the logic of the earlier mortgage support system but is much more generous and focuses support on newly built housing units for families with or planning to have three children. The program was clearly not designed to target the lowest-income households, which corresponds to the middle class–oriented welfare approach of the Hungarian conservative party. 66 One of the policy advisers active in designing the program claimed that trickle-down effects should benefit low-income families indirectly as they can move into the homes that the better-off families moved out of, thanks to government support. 67 This demonstrates the explicit neglect of housing concerns for low-income households. Furthermore, it shows that the state program targeted those families that already had established independent households and enabled them to improve the quality of the homes.

The program allocated substantial resources for interest rate subsidies on long-term mortgage loans at first only for new houses, but later for existing dwellings as well. In addition, people who take a housing loan also receive income tax exemption. 68 Combining all the mortgage supports and tax exemptions, the support covered 50–70 percent of the mortgage. 69 The government also waived VAT tax on building materials for families that qualified. These programs encourage the purchase or building of new housing units, this being aligned with the interests of the construction sector, which had experienced continuous decline since 2004. The number of homes completed in 2016 was just 25 percent of the level of 2005. 70 After much political debate and public backlash, some limited benefits were given to families with fewer than three children or for used apartments, but the scale of the benefits was a fraction of those offered to the primary beneficiaries of the program. However, the impact of rising home prices since 2015 (18.1 percent increase in 2015, 17.3 percent in 2016) has severely diluted the effects of subsidies and further reduced the affordability of homeownership for vulnerable populations. 71

Overall the beneficiaries of CSOK policy include (mostly middle- and upper-class) families, banks, and construction companies. Given the emphasis of the program on families with multiple children, CSOK does not address the significant difficulty that most young people face in independent household formation. It may have a positive impact on higher-order births in families that already have children. Unless these programs are expanded extensively and also inclusive of lower income strata and young people planning their first child, the majority of young people will remain dependent on families for independent household formation.

Where does the post-crisis environment then leave us with respect to independent household formation and social reproduction in Hungary? As indicated in Figure 6, a high proportion of young adults live with their parents and things have taken a turn to the worse since the crisis broke out. 72 At the same time, social inequalities have sharply increased. This is the result of financial repression and the stark upper-middle-class bias of the Orbán government’s social and housing policies. 73 Within the cohorts coming of age in post-crisis Hungary, only those who come from an affluent background will easily be able to afford climbing the property ladder. At the same time, access to rental or social housing remains very difficult. None of this bodes well for the crisis of fertility.

Conclusions

This article has shown East Central European countries belong to the difficult housing regime, 74 where high levels of debt-free homeownership make it difficult for young couples to form independent households. Young generations have to rely excessively on family resources to get launched, but family resources are few and far between. Housing regimes with high dependence on families also clearly have the lowest fertility outcomes. 75 To ease the dependency on the family, policy makers have two choices. They can either opt for market solutions in order to encourage easier and widespread mortgage provision, or they can find statist solutions by supporting attractive options for affordable renting or mortgage support.

With the example of Hungary, where a significant marketization of the housing finance system took place during the 2000s, we have sought to explore the advantages and limits of the first policy option. As we have shown, liberalization of housing finance has not made access to housing for young people easier. The liberalized mortgage finance has been associated with an increasing rather than decreasing age of emancipation. Furthermore, foreign currency loans and increasingly risky lending practices have contributed to their crisis vulnerability, resulting in “shattered housing dreams” 76 and major social problems.

Thus, as the Great Recession, in general, and the Hungarian case, in particular, have made amply clear, while the deregulation of mortgage finance can for some time lead to sustained growth and easing of housing access, it comes at a heavy cost. Namely it brings about major risks for households, leaving them worse off after the boom turned bust. The state’s attempts to intervene in the case of Hungary helped only those families who were the least vulnerable and still concentrated on improving access to mortgages rather than supporting affordable renting. More generally, the limited scope of housing expenditure in ECE is insufficient to overcome the substantial obstacles faced by young people in access to independent housing.

Families rather than markets or states then have to pick up the pieces. Families in Europe’s periphery, however, are now in a much worse shape to do so than before the crisis. Regardless of whether states tried to save the banks or seek a solution to the crisis in financial repression and in spite of social policy attempts, like in Hungary, few families in Europe’s periphery will be able to provide the upcoming generations with enough resources to get launched. Rather, in the luckiest of circumstances, young people will be able to eventually become economically independent enough to leave home. This has the effect of postponing childbearing and decreasing the likelihood of higher-order births. Most families will have to pool all available resources—increasingly meager pensions and insufficient incomes—to just sustain their existing homes. It is this particular housing challenge—that of being trapped in the overcrowded family home with nowhere to go—that probably distinguishes the post-crisis East European family model from that of its richer counterparts.

Footnotes

Appendix

Acknowledgements

The authors would like to thank Herman Mark Schwartz, Lindsay Flynn and Hubert Zimmermann as well as an anonymous reviewer and the editors of the special section for comments on the paper. All errors remain ours.