Abstract

Tax increment financing (TIF) has become a mainstay of local economic development efforts. A significant body of research has investigated the effectiveness of TIF efforts as economic development tools. Such research has concentrated on measuring economic impact of TIF projects, with widely varied results. There has been little examination of the internal differences in TIF project planning and management that affect TIF district performance. This qualitative study builds a theory of TIF performance by examining differences in management practices across TIF districts in the Dallas/Fort Worth Metroplex. Archival analysis is used to determine what efforts cities take to assess risk (preimplementation) and to measure ongoing TIF project performance (postimplementation). Cities are then classified, and descriptive analysis documents the observed differences.

Keywords

Tax increment finance (TIF) is a popular local economic development tool, but state requirements for local administration differ. Some states offer localities-wide discretion in implementation of such projects, whereas others regulate them strictly. This has influenced the popularity of TIF use from state to state, and it affects the consistency of TIF administration both across and within states. TIF performance has been broadly assessed, but until we better understand the existing variation in local administration, we cannot definitively attribute causality in explaining project success. This essay considers the internal management practices that drive TIF performance to better conceptualize the existing variation in local TIF administration. The qualitative analysis moves us toward a theory of TIF performance based on the key dimensions of management practice prior to and during TIF project implementation.

Texas establishes minimum parameters for cities that lead to considerable variation in project administration from place to place. Our archival analysis examines TIF project administration in cities located in the core counties of the Dallas/Fort Worth (DFW), Texas metropolitan area. After a brief review of Texas TIF regulations, we examine the relevance of two key conceptual dimensions of agency practice—risk assessment and performance measurement—to establish an administrative theory of TIF performance. We then present our analytic approach, the findings, and the qualitative differences we observe across the population of cities studied.

Tax Increment Finance Requirements in Texas

Texas TIFs may be created by cities or counties. Texas TIFs differ from most other states in three ways. First, property owners may directly petition a city for designation as a TIF zone as long as the owner’s property constitutes at least 50% of the TIF’s appraised value. Second, each included taxing unit may negotiate with the city to establish the portion of value it will allocate to the TIF. Third, Texas law requires that the zone’s predevelopment condition “‘substantially impair the city’s growth, retard the provision of housing, or constitute an economic or social liability to the public health, safety, morals or welfare” and that “redevelopment will not be likely to occur solely through private investment in the reasonably foreseeable future” (Texas Tax Increment Financing Act, Title 3, Subtitle B, Chap. 311).

Whereas many states strictly regulate TIFs administered by their cities, Texas operates under a more flexible approach with significant local discretion. Texas establishes minimum threshold requirements that cities must fulfill to establish and operate a TIF. To establish a TIF District, Texas state law (Chap. 311) requires the following:

A detailed list of project costs and administrative expenses

A statement listing the kinds, number, and location of proposed public works

An economic feasibility study

An estimated amount of bond indebtedness to be incurred

A time frame when related costs and/or indebtedness will be incurred

A description of methods of financing of all project costs and expected sources of revenue, including the percentage of tax increment to be derived from the property taxes of each property unit

The total appraised value of the taxable real property in the TIF

The estimated captured appraised value of the TIF during each year of its existence

The total duration of the TIF

Texas cities have considerable latitude in establishing and operating their TIFs; their size and duration may be established by the city or may be delegated to the TIF board in its authorizing ordinance. TIF board composition is determined by the affected taxing entities (each appoints 1 member) and the entity that creates the TIF (appoints up to 10 members) with total size varying from 5 to 15 members in most cases; appointees must be eligible to vote and own property in the district (Texas Tax Increment Financing Act, Title 3, Subtitle B, Chap. 311).

In Texas, cities or counties can initiate TIF districts. This may occur via property owner petition of at least 50% of the affected property or by direct city council ordinance (Council of Development Finance Agencies, 2003). Laws vary between states, but in establishing a TIF district, in most cases, a local jurisdiction selects an area where development is needed and freezes the property value of the district for the duration of the TIF (Sullivan, Johnson, & Soden, 2002). This initial valuation is the TIF base value, and it provides a reference point against which to judge TIF performance in future years. The city, or its TIF authority, works with private developers to redevelop the target district, usually relying on construction of new structures. Redevelopment increases property values and consequently adds tax revenue from new construction in excess of the base value into the TIF fund. The revenue may pay for improvements up-front or repay local bonds (Council of Development Finance Agencies, 2003).

Texas’ TIF process requires the following 10 general steps for implementation:

The governing body must prepare a preliminary reinvestment zone financing plan.

The local government creating the zone must provide a 60-day written notice of its intent to designate a reinvestment zone and of the hearing on the proposed zone to the other taxing units that levy property taxes within the area.

Once the local government creating the zone has provided its 60-day notice of a proposed zone, the other affected taxing units within 15 days must designate a representative to meet with the local government creating the zone in order to discuss the project and financing plans.

In addition to meeting with the other taxing unit representatives, the local government creating the zone must provide a formal presentation to the governing body of each taxing unit that levies real property taxes within the proposed zone.

After the local government creating the zone has made its formal presentations to the other taxing units, it must hold a public hearing on the creation of the reinvestment zone.

After the public hearing, the governing body of the city or county may designate, by ordinance or order, a contiguous area as a reinvestment zone for tax increment financing (TIF) purposes.

After the city or county has adopted the ordinance or order creating the zone, the board of directors of the zone must prepare both a “project plan” and a reinvestment zone “financing plan” (Office of the Attorney General of Texas, 2008).

After the project plan and the reinvestment zone are approved by the board of directors and by the city or county’s governing body, the other taxing units with property within the zone contract with the city or county regarding the percentage of their increased tax revenues that will be dedicated to the tax increment fund.

Once the reinvestment zone is established, the board of directors must make recommendations to the governing body of the city or county on the implementation of TIF.

The city or county must submit an annual report to the chief executive officer of each taxing unit that levies taxes on property within the zone (Office of the Attorney General of Texas, 2008).

Texas’s TIF law is more flexible than most other states. These requirements provide the baseline for evaluating TIF management practices within the state; effort beyond the minimum reflects enhanced management effort.

Texas was chosen for analysis for several reasons. The Lone Star State uses TIFs extensively but has greater flexibility in its administration between the state and local levels than do most other states (Arvidson, Hissong, & Cole, 2001). The state provides a clear framework for TIF adoption and administration, but the discretion allowed in implementation results in considerable variation in local TIF administration. This range of variation provides the basis for the study. DFW was chosen as the region of analysis because of the high number of TIFs in close proximity to one another, experiencing similar economic and developmental change at roughly the same time. The DFW Metroplex is a large regional economy with 28 different administrations in the five core counties attempting to achieve economic development via TIF. We selected TIFs in a concentrated geographic area to minimize the effect of economic differences from place to place that might bear on the TIFs’ observed performance. If the economy is performing similarly well in all areas, then TIF performance might be attributed to the macroeconomy rather than local project attributes. If, however, performance variation is observed across places with similar economic conditions, that performance is more likely a result of project-specific attributes. Our objective is to explore the degree of variability in management practices and their relationship to performance while minimizing the effects of external economic conditions on the observed outcomes. Although counties are eligible to initiate TIFs, the TIFs in the study area are all municipally initiated, further reducing potential variance.

Risk Assessment and Performance Measurement Research

Both performance measurement and risk assessment are integral to successful design and execution of economic development projects. Projects are often politically driven (Wolman, 1996) and may not be planned and/or measured to the degree needed for optimal results. This section examines prior research in economic development literature as it relates to both risk assessment and performance measurement and provides an overview of the main areas of inquiry as they relate both to economic development generally and TIF in particular.

There have been repeated calls for stronger links between academic research and agency practices regarding public performance assessment (Coplin, Merget, & Bourdeaux, 2002). Behn (2003) believed that performance assessment is still in developmental stages, and Ammons (2002) called for a more comprehensive use of performance indicators at all agency levels. At the same time, researchers in economic development have also noted that “there is a marked paucity of systematic empirical research on the distributional outcomes of local economic development policy” (Wolman, 1996, p. 148). The disparity in local tax incentive effectiveness found among recent studies (Byrne, 2006; Carroll, 2008; Weber, Bhatta, & Merriman, 2003) suggests that we have much yet to learn about economic development performance and its causes. Oden and Mueller (1999) suggested a more systematic approach involving the public before any tax incentives are awarded to private companies. Bartik (1991) called for more study to determine the effectiveness of recent economic development programs.

TIF has been popular at the state and local level since the 1970s. Almost all states currently authorize some form of TIF program (Man, 1999). Even so, research to evaluate their performance has neglected the effects of management practices on TIF effectiveness. Two key practices of interest are formal risk assessment (preimplementation) and performance measurement (postimplementation). The challenge in exploring the impact of management practices on TIF performance is data availability. No standard variables exist to assess management practices that occur within an administration; hence, studies seeking to measure and explain TIF performance have failed to adequately incorporate these constructs.

Performance Measurement in Economic Development

Quality of economic development program evaluation varies widely and is often lacking. As Bartik and Bingham (1997, pp. 268-269) explain, comparison groups are hard to find, the cost of data collection is prohibitive, and evaluations are politically sensitive. Giloth (1997, pp. 280-282) believes the scope of economic development evaluation analysis to be too narrow. He calls for programs to be clearly designed and implemented at the outset, making it easier to evaluate program performance. Hissong (2003, pp. 131-132) suggests that the heterogeneity of different models and geographies leads to contradictory findings and calls for researchers to develop models with measurement units that could be cross-analyzed.

Rational Decision Making and Risk Assessment

Just as performance measurement tends to vary in quality, risk assessment also differs considerably from place to place. Developers and public officials may design and execute programs without full consideration of their potential negative consequences. More rigorous risk assessment, in conjunction with effective methods of performance measurement, may be a means of addressing criticisms of local economic development projects. Risk assessment refers to the formal process used to determine potential risks in financing and developing a project.

To date, few studies have considered the concepts of risk and risk assessment in reference to local economic development projects. Iraci and Bass (2008) called for a new model of risk assessment that would clearly define potential risks, assure appropriate review is in place, and clearly delineate roles and responsibilities. Němecěk and Kocmanová (2008) called for new risk-forecasting models that consider tax, investment and for environmental policy in decision making.

Sullivan et al. (2002) found that local governments that aggressively promote development tend to offer more incentives but couple them with more stringent performance agreements in order to prevent losses or failures. He also found that poorer cities tended to offer less stringent clauses in contract agreements, thereby subjecting their respective municipalities to greater risk of failure. Green and Fleischmann (1989) found poorer cities to be more active in promoting development. These findings imply that cities may vary in their risk-seeking behavior, and those preferences may manifest themselves in terms of management practices. This is important to the extent risk assessment affects TIF success. Leavitt, Morris, and Lombard (2008) present case study evidence documenting the value of reducing public risk to the success of a TIF in Virginia Beach, Virginia. City wealth most likely affects capacity to engage in such practices as well. As such, an administrative theory of performance would better characterize and measure the independent variables that lead to project success. This is not to suggest that wealth and risk aversion are not meaningful predictors but that omitted variable bias may have skewed past findings.

High costs, potential political repercussions, and the possibility that the benefits of analysis may not accrue directly to the agency paying for the assessment prevent design and implementation of more rigorous preliminary risk assessments. Economic development officials must make calculated risks in favoring any type of incentive. Absence of formal risk assessment procedures may jeopardize project success.

Defining risk as the potential for negative consequences, with uncertainty as to the likelihood of that harm (Hall & Jennings 2008), there are clearly many potential risks inherent in economic development. Scarce public resources can be squandered. Funds may be redirected to well-off private developers rather than the poor and unemployed. Growth in one region could be offset by a decline in another (Bartik, 1991). The projects may not be completed on time or in a cost-efficient manner. There may be better projects or better means of addressing development problems. Risk, and the process and practice of assessing risk, is a prominent characteristic of project design and development and should be incorporated in models of project performance.

In contrast to the relative paucity of detailed means of risk assessment, the study and practice of public performance measurement has had a much richer history. Considering postimplementation performance measurement in tandem with preimplementation risk assessment will yield a more thorough understanding of project administration. Effective management practice is expected to yield improved performance.

Toward an Administrative Theory of Tax Increment Finance Performance

A few studies have considered TIF performance specific to the Texas setting. Most have focused on external characteristics such as political support and the presence of partnerships prior to implementation. For example, Arvidson et al. (2001) surveyed cities to examine political support, citizen participation and performance. They found little political opposition to TIF creation but discovered that women and minorities are underrepresented on TIF Boards. The majority of the 14 cities in their sample were able to increase their tax base and attract new businesses. Ewoh (2007) examined the use of public–private partnerships and the use of TIFs (or TIRZs [tax increment reinvestment zones]) in Houston. He found programs to be successful in places where effective partnerships are in place prior to project implementation.

Yuasa and Thomas (2006) found varied equity across Houston, Texas, TIFs and found that project zones’ development focus (inner city vs. commercial development) affects performance, with more improvement in inner-city redevelopment zones. Sullivan et al. (2002) enumerated Texas TIF best practices based on projects in El Paso. Included was a list of financial considerations consisting of property assessment growth rates, net present value of the property, financial viability, financial efficiency, and likely spillover effects prior to district and project implementation. Their study considers risk indirectly in the form of potential hazards if TIFs are not carefully planned, but it does not offer a formal risk assessment or postimplementation performance measurement.

To date, no studies of TIF performance have considered the role of internal management characteristics, such as preimplementation risk assessment and postimplementation performance measurement, as meaningful explanatory constructs. Ewoh (2007) suggested that constant program monitoring can support local economic development; he does not consider risk assessment in his analysis. This study examines these key management constructs across TIFs in the DFW Metroplex to improve our understanding of the predictors of TIF effectiveness. This study departs from past efforts by selecting an environment within which state law permits variation in local processes and procedures and by then directly measuring local TIF management efforts and cataloging variation across cities within the selected local economic context. No studies have considered management practices to examine their role in program effectiveness. By so doing, this study makes a viable contribution to understanding risk assessment and performance measurement in relation to economic development projects more broadly.

Much of the criticism surrounding TIFs, as other economic development incentive programs, is that they serve political principals’ need to “do something” (Wolman, 1996) and that they support economic development that would have occurred absent government involvement. As Buss (2001) indicates, “economic growth and location decisions are separate fields;” he continues, “Consequently, correlations attributed to variables in models probably represent relationships outside the model” (pp. 94-95). In other words, growth is often attributed to government action, and policies are adopted with the belief that they matter, when it is actually quite difficult to attribute outcomes to specific policies and not external factors.

Another criticism that looms large for local officials is the potential information asymmetry inherent in the process; self interested firms or developers seeking to enhance the value of their investments seek public support. Government officials may lack knowledge about expected job creation (Nunn, 1994). Developers and property owners have information and expectations about the market to which government officials may not be privy, thereby shaping the decision process (Feiock, 2002). To the extent governments engage in rational decision making (e.g., risk assessment) prior to TIF adoption, they minimize the harmful effects of information asymmetry that may be at play. So our approach does not negate the potential for politically-motivated decisions, nor does it downplay the potential for information asymmetry in the process. However, movement toward rational decision processes should reveal the extent to which a project is feasible and likely to generate positive outcomes. In that such rationality can help compensate for information deficiencies and lead to improved decisions, it is important to ascertain the extent to which cities use such strategies in their TIF management processes.

This study examines TIF districts in DFW to determine the level of current city attention to risk assessment and performance measurement in the management process. In theory, cities’ rational analysis of the economic environment, district and project design, selection, and monitoring increases to the degree that the TIF management considers risk analysis and performance measurement. TIF revenue and property valuation projections should increase as the level of management scrutiny increases. Consequently, projects that undergo greater risk assessment and aggressive performance measurement should experience improved performance.

We select these two components because they reflect identifiable management practices that may or may not be part of the cities’ strategic approach to TIF-oriented development. A significant body of research has examined the effects of capacity on performance (Gargan, 1981; Hall, 2008; Honadle, 1981), revealing the importance of both administrative and financial capacity on performance outcomes. To this end, there are numerous city characteristics that may shape the use of the identified practices or their quality, such as budget size, number of staff, staff training and expertise, and so on. Our analysis does not discount the importance of these factors, but they are not directly considered here. From an evaluation standpoint, these are inputs affecting the quality of management practices; our interest is not on the cause of the observed practices but on their use and intensity. To clarify, a city with few staff resources may contract out the feasibility study, a city with little discretionary revenue may leave the task to internal staff, a large city may have capable professional analysts on hand, or a city may emphasize this aspect of planning and disregard other considerations. The strategies that are used and their quality may or may not be a proxy for city resources. Our concern is not with the process through which the strategies came to be but with their observed use in practice.

Causality is difficult to establish with most economic development programs; TIF is no different in this regard. Performance variation may result from utilization of these practices but may also result from external factors such as general economic climate, project type (e.g., industrial vs. central business district, etc.; Byrne, 2006), city desperation for growth, or selection of projects in areas destined for growth without government intervention. Although we are unable to control for all potential influences on performance, our design attempts to limit their effects. Selecting projects in a single metropolitan area limits the effects of economic fluctuation—all cities experience relatively similar economic trends. Inclusion of all active or completed projects in the area provides the full spectrum of available project types and locations.

Our study contributes to the growing TIF performance literature by exposing a key source of potential bias in existing studies. Even the best-modeled studies (e.g., Byrne, 2006) fail to account for management strategies in TIF governance. The general movement toward government performance management and accountability suggests these characteristics are important explanatory factors (Poister & Streib 1999). Byrne (2006) includes various independent variables that may influence growth in TIF districts. These include neighborhood characteristics (percentage White, median income, vacancy rate, median age of structures, population density), spatial characteristics (area, distance from downtown, proximity to city boundaries), and TIF age and classification (mall, mixed use, industrial, housing, other). Although well specified, management characteristics in this and other studies are assumed to be constant.

Texas requirements to establish TIF districts and to evaluate proposals for existing districts serve as a floor; many cities go well beyond the minimal requirements. We theorize that cities vary considerably in the use of two key management practices—risk assessment and performance measurement—and that greater use of these practices enhances their TIF projects’ performance. As our study later reveals, cities in the DFW area vary considerably in how much attention they give to risk assessment and performance measurement. Our purpose here is to establish and classify differences in the intensity with which cities administering TIFs approach risk assessment and performance measurement. Our qualitative archival analysis explores city records, including TIF reports and ordinances, to determine the extent of variation in program planning and administration within a single large metropolitan area.

Method of Analysis

A qualitative review of government documents from pre- and postimplementation practices was conducted to (a) determine if there is variance among local municipalities, (b) determine how they vary, and (c) analyze the influences of the local practices on performance. The primary method of data collection is archival public record analysis of TIF districts in cities located in Collin, Dallas, Ellis, Rockwall, and Tarrant counties. These are the five central counties in the DFW–Arlington, Texas Core–Based Statistical Area (No. 19100), as of November 2008. According to the North Central Texas Council of Governments (2009), there are 111 designated municipalities in these counties. Of these, 28 have active TIF districts, with a total of 70 active TIFs. Most cities have one or two districts, but large municipalities, including Fort Worth and Dallas, have 11 and 18, respectively.

Local ordinances vary considerably from city to city, and we reviewed them for content pertinent to performance management and risk assessment. Selected TIF managers (selected for convenience) were consulted informally as the conceptual design was being developed to better understand the process of TIF formation and the type of consistent archival documentation that would be available to inform the analysis. Annual reports are required by the state and provide the primary source for performance measurement information. These reports provide the original base property valuation, the annual updated valuations, and the amount of revenue in the tax increment for the latest fiscal year. The greatest variation in detail in the annual reports concerns the amount and depth of description for each individual project within each TIF district. TIF feasibility studies are required by the state and provide the richest source of data for district risk assessment practices. They provide initial property valuations, value projections over the TIF’s life span, and projected revenue amounts each fiscal year. Studies vary considerably in the amount of detail provided with respect to risk assessment and performance measurement.

Our choice of revenue and valuation as measures of TIF performance is consistent with existing studies and offers the most consistent information available for direct comparison of TIF performance. A number of studies use property valuation growth rates as the measure of TIF performance (Byrne, 2006; Carroll, 2008; Man & Rosentraub, 1998). Again considering an evaluation framework, TIF valuation and revenue are the two most direct measures of TIF performance, and both are mandatory in annual reports (Texas Tax Increment Financing Act, Title 3, Subtitle B, Chap. 311, § 311.016). Valuation is the most direct outcome, with revenue being derived from increased value but subject to tax rates in force. Indirect measures such as employment, business start-ups, personal income, and unemployment are meaningful long-term economic development goals but are subject to greater external influence and are more difficult to attribute to the project, much less its management practices.

TIF valuation and revenue performance are important to various stakeholders. Cities and private investors are partners in the project’s success. When valuation goals are not met, everyone loses. When valuation goals are met, the redevelopment has occurred and real investment is in place; the blight has been reduced or removed. However, when valuation goals are met but revenue goals are not, stakeholders may be affected differently. Insufficient revenue means debt service payments will be difficult to meet; the financing structure will determine whether that harms the government and its citizens or business investors. Insufficient revenue may indicate that the investment has failed to attract economic activity and growth.

Texas’s Tax Increment Zone Financing Registry summarizes each TIF every 4 years, so although it was helpful in building the data set, we relied on data provided directly from each city (voluntarily or through Freedom of Information Act requests) for this analysis. Although the primary unit of analysis is the TIF, management practices are measured at the city level. City data were compiled and categorized according to the level of detail in planning, execution, and monitoring of TIF districts and projects. The rubrics used to classify city management practices are displayed in Table 1 (risk assessment) and Table 2 (performance measurement). Management practices were benchmarked against minimum state requirements to classify variation in city management practices in TIF administration. Cities receiving a rating of state minimum for risk assessment met the basic state requirements identified above (Texas State Law Chap. 311). Cities were classified as advanced and intensive as risk assessment efforts increased.

Classification Rubric for Risk Management

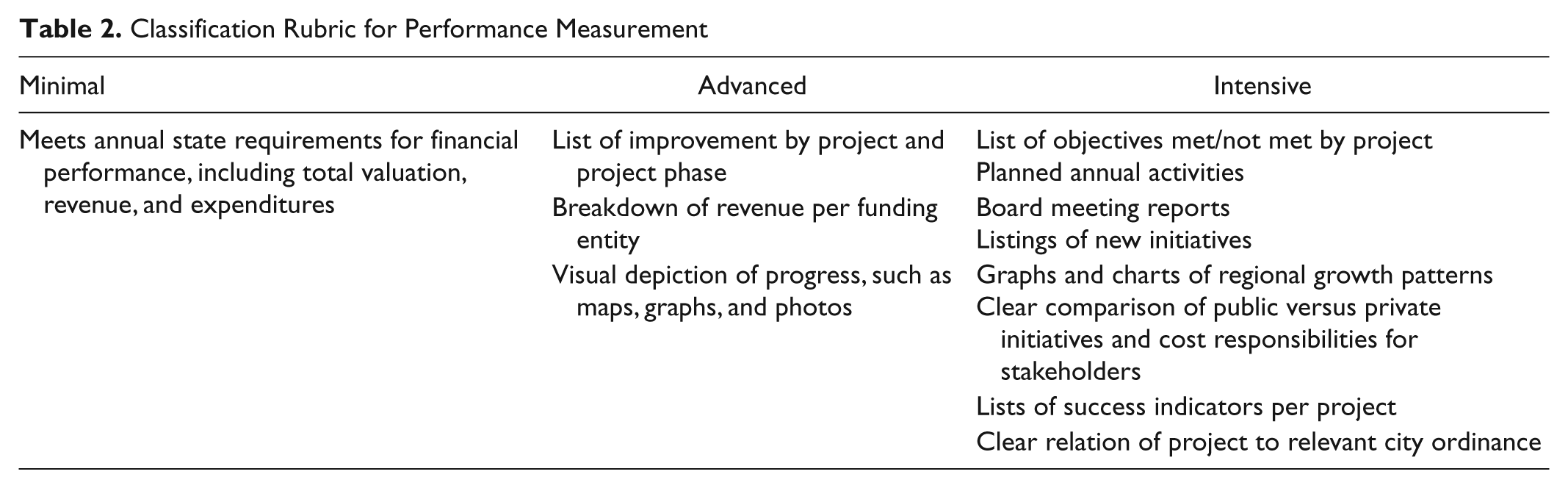

Classification Rubric for Performance Measurement

As with risk assessment, public records (primarily TIF annual reports) provided the information for rating performance assessment. Texas’ minimum annual reporting requirements are as follows:

The amount and source of revenue in the tax increment fund established for the zone

The amount and purpose of expenditures from the fund

The amount of principal and interest due on outstanding bonded indebtedness

The tax increment base and current captured appraised value retained by the zone

The captured appraised value shared by the city and other taxing units

The total amount of tax increments received

Any additional information necessary to demonstrate compliance with the TIF plan adopted by the city

The seventh requirement is the most subjective and provided the majority of the information that documents variation in city practice. Cities’ performance measurement was rated state minimum, advanced, or intensive. As before, cities rated minimum provide only the minimum effort required by law. Advanced cities provided more information than was required by the state and offered better visual depictions and clearer breakdowns of project costs and progress. Intensive cities provided systematic measures in their annual reports that provided an extensive explanation of project accomplishments and future plans.

To provide descriptive comparison, each project’s actual performance (for the most recent available year) was assessed categorically according to the initial estimated performance for that year at the TIF’s inception. Two dependent variables are used: tax revenues and property valuation. Performance was assessed as underperforming (>15% lower than estimate), meeting expectations (estimate ±15%), or exceeding expectations (>15% higher than estimate).

Findings

Content analysis revealed that cities vary considerably in the quality of their management practices. Table 3 provides each city’s risk assessment ranking, along with the specific details provided in their public records for TIF design and execution. These records include ordinances, financing plans, annual reports, and any general announcements that the city chose to include as part of the TIF’s documentation. The proportion of cities rated minimum, advanced, and intensive for risk assessment was 21%, 32%, and 46%, respectively. This indicates that approximately half of the cities in the DFW area do apply a systematic focus to risk assessment, and about four-fifths consider risk assessment beyond the minimal state requirements. A focused approach to risk assessment is already a managerial concern for most DFW TIF districts.

City Risk Assessment Detail

Note. TIF = tax increment financing; ED = economic development; COG = Council of Government; DART = Dallas Area Rapid Transit; ISD = independent school district; DFW = Dallas/Fort Worth.

Table 4 lists each city’s rating for performance measurement effort. As with Table 3, there is a wide range of local response in meeting the state’s legal requirements. Proportions for performance measurement ratings minimum, advanced, and intensive cities are 48%, 30%, and 22%, respectively. In contrast to consideration of risk assessment, only about one fifth of cities reveal significant effort in performance measurement, and approximately half meet only the minimal requirements. Many cities in DFW do not use performance measurement to the same degree as risk assessment, but cities vary considerably.

City Performance Measurement Detail

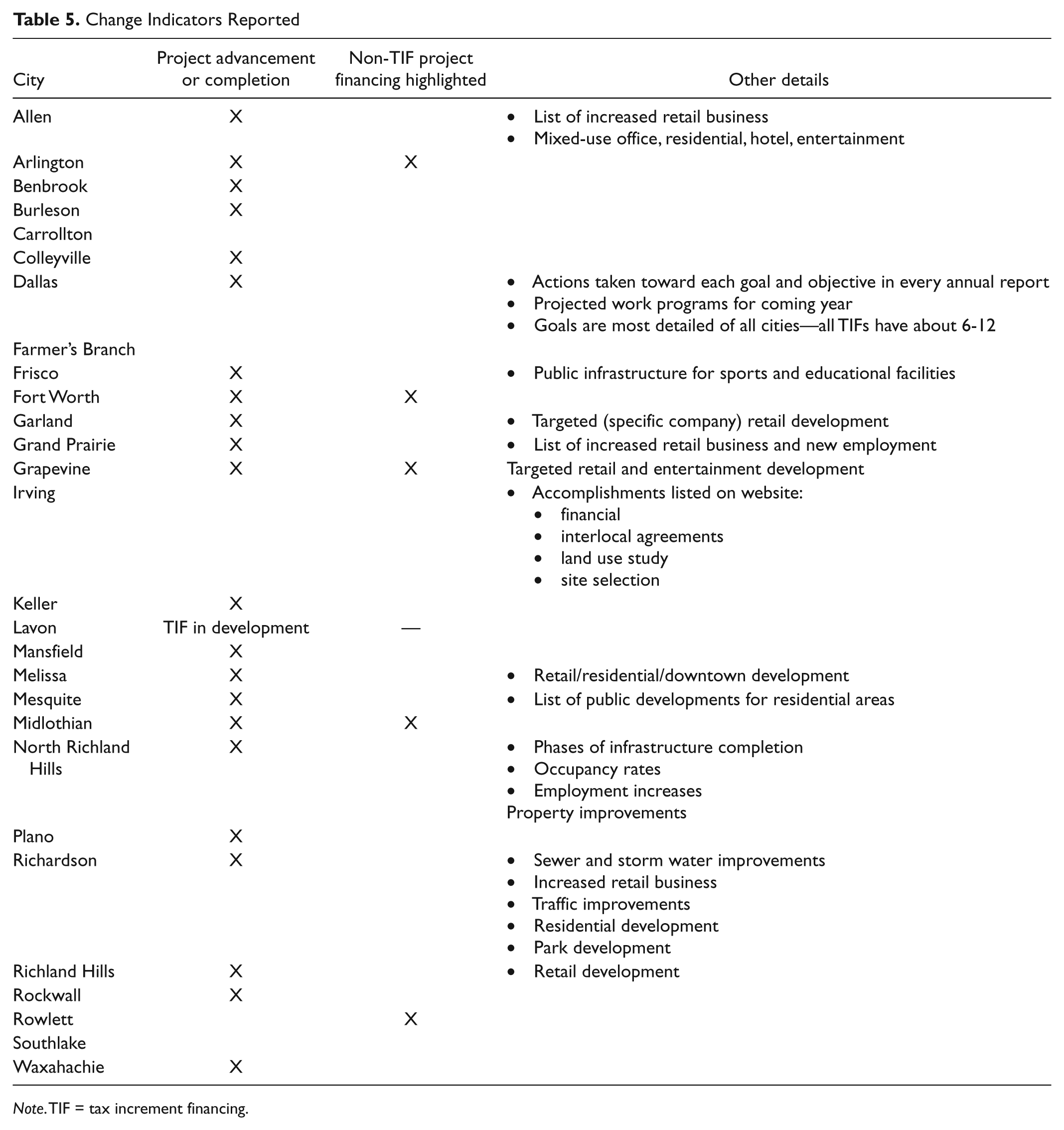

Table 5 provides detail on performance indicators for project advancement and project financing. Most cities used clear indicators during project execution and completion, but fewer provided clear details of non-TIF project financing. Table 5 provided a means to assist in determining the rating (advanced or intensive) for performance measurement. Table 5 shows cities that use performance indicators and benchmarks, indicating a stronger approach to performance measurement and also reveals which cities highlight means of financing TIF projects outside of the tax increment, indicating a stronger approach to risk assessment. Other details are included to demonstrate examples of specific approaches by the respective cities to plan and execute their projects. Cities that had clear performance indicators were given more detailed ratings in performance measurement, risk assessment, or both, according to their focus.

Change Indicators Reported

Note. TIF = tax increment financing.

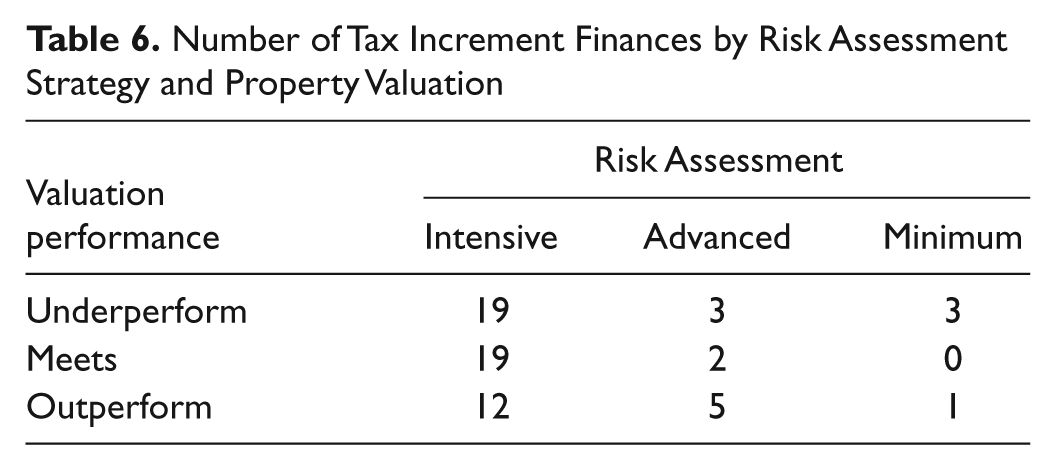

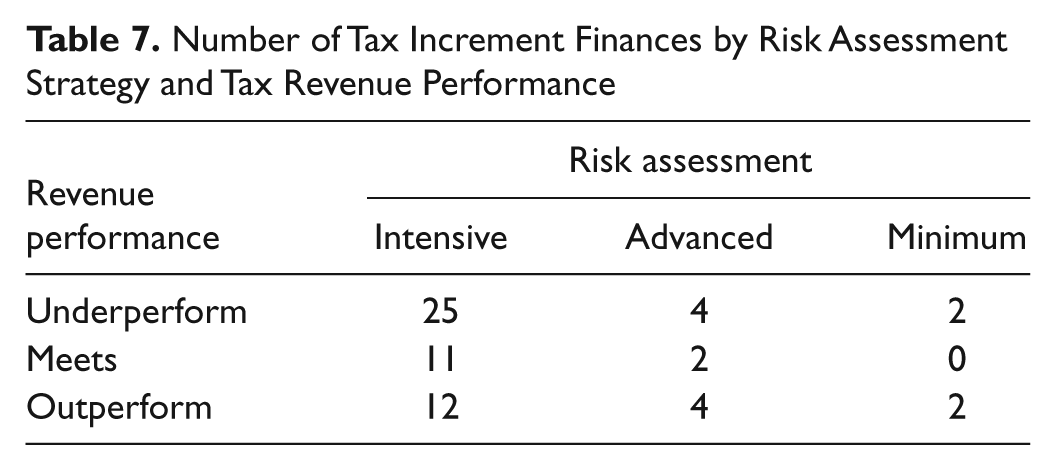

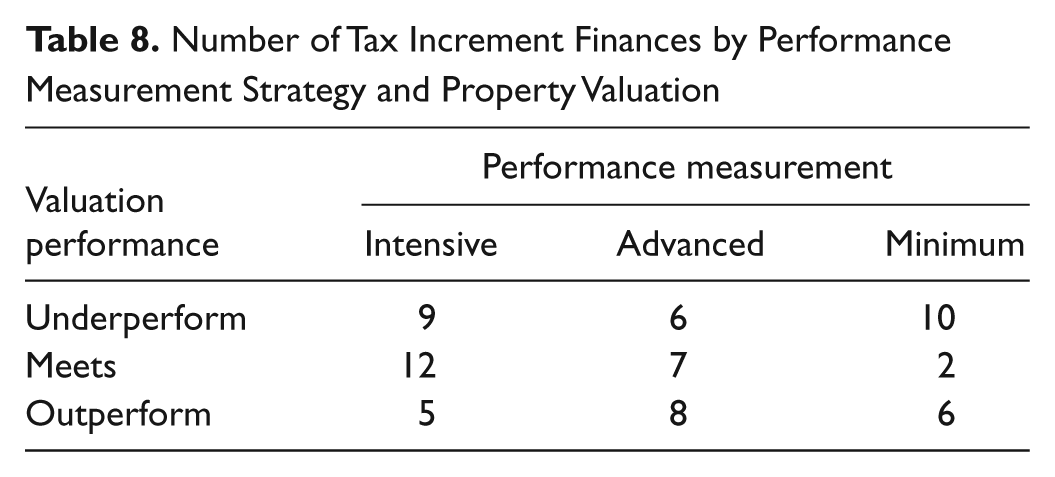

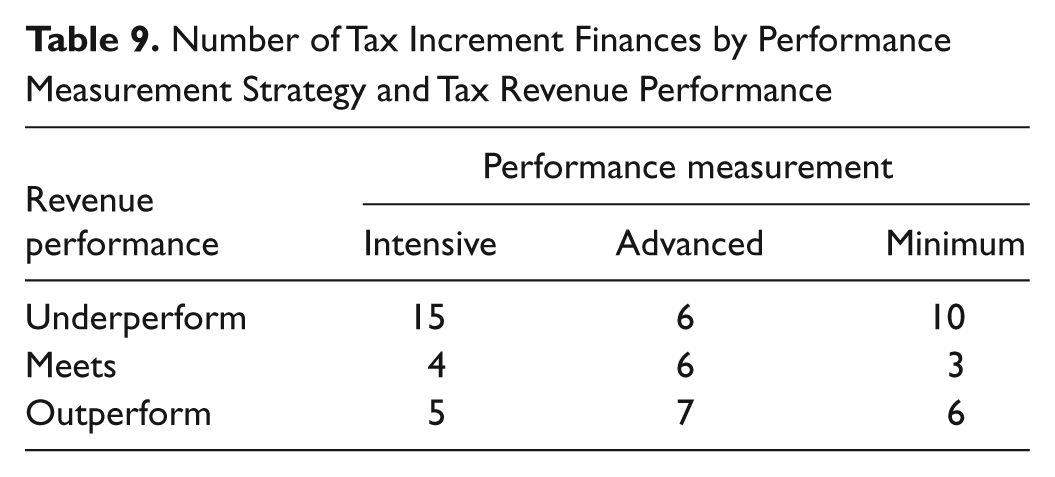

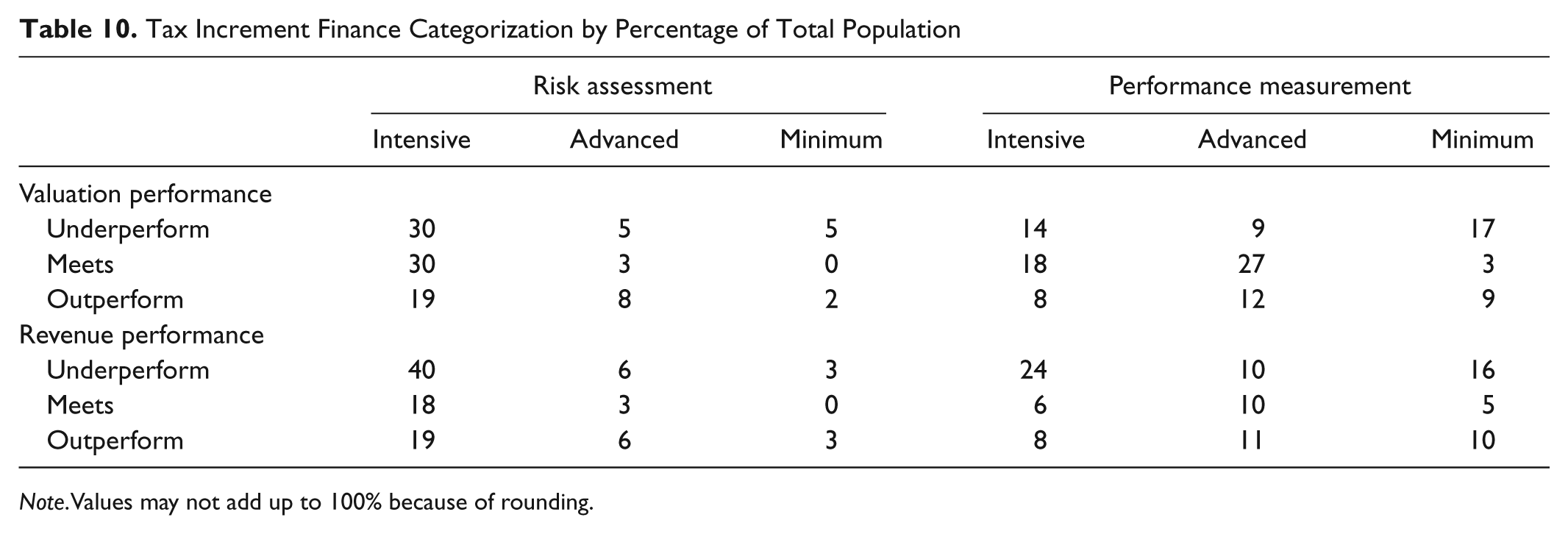

Tables 6 through 9 show the proportion of districts by category, according to valuation and revenue performance. Table 6 shows a relatively equal amount of intensive TIFs underperforming or meeting property valuation projections by risk assessment category. Table 7 shows that most intensive TIFs actually underperform in terms of tax revenue but are equally likely to meet or exceed standards. Table 8 shows the strongest correlation with stronger performance management measures leading to more successful outcomes, as most minimum-rated TIFs underperformed in terms of property valuation, but tended to improve with increased intensity. Table 9 shows underperformance by both intensive and minimal TIFs in terms of performance by tax revenue. Table 10 presents each TIF by classification and whether it met, outperformed, or underperformed original projections.

Number of Tax Increment Finances by Risk Assessment Strategy and Property Valuation

Number of Tax Increment Finances by Risk Assessment Strategy and Tax Revenue Performance

Number of Tax Increment Finances by Performance Measurement Strategy and Property Valuation

Number of Tax Increment Finances by Performance Measurement Strategy and Tax Revenue Performance

Tax Increment Finance Categorization by Percentage of Total Population

Note. Values may not add up to 100% because of rounding.

Descriptive Vignettes

Each city in the study (with the exception of those meeting only minimum requirements for both measures) is somewhat unique in its approach to TIF district development and project measurement. Each of the 28 cities is cross-categorized by its evaluation on both indicators. Described below are examples of cities in each risk assessment and performance measurement classification. Consistent with the purpose of our research, these vignettes reveal considerable variation in practice. As discussed above, this addresses management practices—a potentially key determinant of TIF performance not previously considered in TIF evaluations.

Dallas: Intensive Risk Assessment; Intensive Performance Measurement

The city of Dallas is the best example of a city rated intensive for both risk assessment and performance measurement. Dallas has a total of 18 TIFs, one of which, the State Thomas district, is the oldest TIF in the study. It is also the only fully retired TIF in the study, ending in 2009. The two newest TIFs, Maple/Mockingbird and the Transit-Oriented District, are still in the planning stages and not included in the analysis. Each of Dallas’ TIFs exists to develop a different neighborhood in the city. Unlike many other cities, Dallas tends to avoid using TIFs to support a single company or industry. This is partially because of the larger size of the city, 1.3 million, compared with an average population of 110,000 for the rest of the cities.

Dallas’ approach to risk assessment is unique in the study because of vigorous evaluation standards. The total values of financial benefits and policy benefits to the city are scored separately. Each indicator must score 70% or higher for a proposed TIF district to be created. Specific projects within TIFs must provide financing projections and match specific development objectives for the respective TIF. All Dallas TIFs clearly list development goals and objectives, and their progress is tracked in their annual reports.

For this reason, Dallas also rates intensive for performance measurement. Every district measures its accomplishments by project and includes activity for the next fiscal year. No other city in this study provides annual reports with as much detail as Dallas. All annual reports are standardized and vary only slightly according to the differences in the nature of the districts’ projects themselves (i.e., TIFs with smaller scale projects tend to be somewhat more numerous and have different benchmarks for progress than larger scale commercial developments). For this reason, Dallas’ evaluation procedures may be considered a best practice for other cities considering new TIFs and new projects within existing TIFs.

For property valuation projections, Dallas is one of the best performing cities in the study. Of 16 functional TIFs, 4 exceed valuation expectations, 9 meet expectations (within 15% of the original projection), and only 3 fell short, the largest gap being 34%. However, the same cannot be said for the performance of Dallas’ revenue projections. Only 4 TIFs met or exceeded revenue expectations, whereas 12 fell short, ranging from 26% less than expected to 100% (no revenue earned at all). Some of the initial revenue projections are overly optimistic, but since most of the property valuations are according to expectation, Dallas may experience administrative difficulties in revenue collection (see Data Sources, City of Dallas, 2010).

Allen: Intensive Risk Assessment, Advanced Performance Measurement

The city of Allen’s risk assessment rated intensive, and its performance measurement, advanced. The city has two TIFs, created in 2005 and 2006. The first, named the Garden District or Montgomery Farm, was designed to create a multiuse (retail, office, housing, hotel, and wellness) development along U.S. Highway 75. The second, the Central Business District TIF, includes areas further east and west of the highway. Allen received a rating of intensive for its risk assessment, as its TIF plans provide project reports, visual depictions, development projections, and economic impact analyses well exceeding state legal requirements. Both TIFs have several phases of development. The TIF projections include multiple schedules of property appraisals, projected increments, and estimated project costs.

For performance measurement, Allen rated advanced, as its annual reports slightly exceed state requirements, in contrast to the detail given in project development. The annual reports do include photographs and changes in commercial productivity for the year. Allen met its valuation projection, but fell short of its revenue projection (see Data Sources, City of Allen, Texas, 2008).

Melissa: Intensive Risk Assessment, State Minimum Performance Measurement

The City of Melissa provides an example of an intensive rating for risk assessment and a minimum rating for performance measurement. Its only TIF was created in 2006 to develop a core business area. The TIF was split into two phases, one in a relatively undeveloped area west of State Highway 5 and the other east of the highway to redevelop a deteriorated downtown.

Melissa provided detailed employment projections, nonproject development costs, cumulative economic impacts, and a project breakdown per neighborhood. Each phase of development was analyzed to a much greater level of detail than the state requires. However, Melissa provided only the minimum requirements in its annual report. Melissa fell short on both valuation and revenue projections (see Data Sources, City of Melissa, Texas, 2008).

Irving: Advanced Risk Assessment; Intensive Performance Measurement

The only city in the study rating advanced for risk assessment and intensive for performance measurement is Irving. Begun in 1999, the TIF includes mixed-use office and residential projects. Its categorization for risk assessment is because of its inclusion of local market analysis and historic property usage slightly beyond state requirements. Its performance measurement is intensive, as its annual reports provide a rich depth of current project valuations, photographs, and future estimates (see Data Sources, City of Irving, Texas, 2009).

Frisco: Advanced Risk Assessment; Advanced Performance Measurement

Frisco provides an interesting case study, despite its ratings of advanced for both performance measurement and risk assessment. The city’s TIF was created in 1997 and was enlarged in 2000 and 2003. The city partnered with private businesses to develop a multiuse sports and entertainment complex. Frisco does exceed the state minimum for risk assessment by providing a more detailed explanation of both public and private projects to be developed in the district. Its consideration of performance assessment is also at the advanced level, as its annual report lists project phases and improvement costs at a level of detail above state requirements. Frisco is one of the few cities in the study to exceed both its revenue and valuation projections (see Data Sources, City of Frisco, Texas, 2008).

Richardson: Advanced Risk Assessment, State Minimum Performance Measurement

An example of a city with an advanced risk assessment rating and a minimum performance measurement rating is Richardson. Richardson’s only TIF, Centennial Park, follows the U.S. Highway 75 corridor and concentrates investment into a 30-acre zone. Created in 2007, its purpose is to provide mixed-use retail and residential development. Project assessments consider the need for and projected use of the TIF at a level of detail above minimum requirements, including summary material on Centennial Park’s planning and development. The city does not surpass minimal requirements for its annual performance reports. Richardson’s projected property valuations fell short by 20%. Revenue projections were met, with zero revenue projected. Its performance to date is therefore mixed (see Data Sources, City of Richardson, Texas, 2008).

Rockwall: State Minimum Risk Assessment, Advanced Performance Measurement

Rockwall was rated minimum for risk assessment and advanced for performance measurement. Its only TIF, the Harbor Project, was created in 2004, designed to develop part of the eastern shore of Lake Ray Hubbard. Although its project descriptions meet the state requirements, there is virtually no added detail to describe the project to the public. Its performance measurement standards rate advanced as it exceeds the state minimum by providing descriptions of distinct phases of project funding. Rockwall exceeded its valuation expectations but fell short of revenue projections (see Data Sources, City of Rockwall, Texas, 2005).

Rowlett: State Minimum Risk Assessment, State Minimum Performance Measurement

Finally, the city of Rowlett was rated minimum on both measures. Its TIF began in 2002, and it is intended to develop three subregions around the city. Descriptions of these regions are sparse. Although valuation expectations were exceeded, the revenue data provided were incomplete (see Data Sources, City of Rowlett, Texas, 2008).

Very few cities rated minimal on both measures, and those that did provided inadequate data for analysis. No cities in the study rated minimum for risk assessment and intensive for performance measurement. External factors can influence even the most well-planned and well-executed TIF district or project. Frisco is a clear example of a city with strong economic growth during the period matching its TIF performance, whereas Dallas displays a range of performance that may reflect revenue expectations out of line with the growth of property values.

Conclusion

The summaries of TIF practices reveal that cities in DFW vary considerably in terms of risk assessment and performance measurement in their TIF districts. This analysis shows that cities that carefully consider risk assessment do not necessarily also consider performance measurement and vice versa; the two different management efforts appear to vary independently. Some cities provide extensive documentation prior to and during the execution of their TIFs, whereas others meet only the minimum state requirements.

Our descriptive statistics suggest that there may be associations between these management strategies and performance, but these effects may not be consistent across revenue and valuation performance measures. What is clear at this stage is that cities vary on both management strategies and performance, and from this study, city size does not appear to be a determining factor. The qualitative nature of this analysis is not equipped to control for various external characteristics that may contribute to TIF success or failure but does shed light on potential bias inherent in existing studies that fail to account for management capacity. These results are limited to the DFW Metroplex but may have conceptual application in other regions and states, depending on the influence of state laws and local economic conditions. Naturally, these findings characterize the development of an administrative theory of TIF performance; further research should seek to validate the findings through quantitative analysis.

General economic development practices can improve by filling gaps in program design, implementation, and project-monitoring procedures to enhance their effectiveness. Following state minimum requirements may not be the most effective long-term strategy. Given the current political and economic climate favoring more rigorous analysis of public sector activities, especially in relation to economic development, cities may be able to maximize the value of their investments by emphasizing risk assessment and performance measurement. Research is needed to determine how risk assessment and performance measurement may affect other geographic areas and other types of economic development programs. As analysis matures, greater conceptual specificity can be developed to generate best practices in TIF administration.

Footnotes

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The author(s) received no financial support for the research, authorship, and/or publication of this article.