Abstract

After many years of declining fortunes, the Detroit Three carmakers were at risk of closure and liquidation during the severe recession of 2008-2009. Efforts by the Bush and Obama administrations to support the carmakers culminated in a government-managed reorganization of Chrysler and General Motors during 2009. As a result of the restructuring, the two carmakers emerged from bankruptcy protection with lower labor costs, higher capacity utilization, and a more concentrated geographic distribution of assembly plants.

The severe recession of 2008-2009 created a near-death experience for the three U.S.-headquartered carmakers—Chrysler Corporation, 1 the Ford Motor Company, and General Motors Corporation (GM)—known as the Detroit Three. The purpose of this article is to review the restructuring of the North American auto industry during that severe recession and to evaluate the principal changes in the North American auto industry as a result of the restructuring.

The first section of this article describes the events leading up to a government-managed reorganization of the U.S. carmakers. The second section identifies the principal strategies by which the U.S. government, with the assistance of the governments of Canada and Ontario, reorganized the carmakers in 2009. The third section assesses the extent to which competitive conditions in the auto industry changed as a result of the reorganization. The fourth section discusses the extent to which the spatial distribution of the North American auto industry was altered by the reorganization. 2

Prelude to Bankruptcy

This section reviews the principal events leading up to the filing by Chrysler and GM for reorganization under bankruptcy protection in 2009. The first part of this section discusses some of the elements that produced a deteriorating business climate for the Detroit Three. The second part describes key actions taken by the U.S. government during the final days of the Bush administration in late 2008. The third part summarizes the principal steps taken by the newly inaugurated Obama administration during the first half of 2009.

Deteriorating Business Climate

The severe recession of 2008-2009 took a heavy toll on the auto industry. In addition to rising unemployment, tightening credit markets contributed significantly to the drop in vehicle sales (Jackson, 2009). Declines in U.S. sales, production, and employment between 2007 and 2009 were the sharpest since World War II:

Sales of light vehicles dropped 38%, from 16.2 million in 2007 to 10.1 million in 2009.

Production of light vehicles dropped 46%, from 10.4 million in 2007 to 5.6 million in 2009.

Employment dropped between 2007 and 2009 from 185,800 to 123,400 in assembly plants and from 607,700 to 413,500 in parts plants—declines of 34% and 32%, respectively.

Activity in the motor vehicle sector also declined in Canada and Mexico between 2007 and 2009. During the 2-year period, production declined 42% in Canada and 26% in Mexico, and sales declined 13% in Canada and 31% in Mexico.

The steep decline between 2007 and 2009 was disruptive for carmakers because it ended an unusually long period in which the companies had enjoyed record high sales of 16 to 17 million per year. During the second half of the 20th century, sales had soared from 6 million in 1950 to 17 million in 2000. Until the early 1990s, short-term cyclical changes were typical, with double-digit annual percentage changes, usually in a see-saw pattern. In contrast, between 1992 and 2007, annual sales were much less volatile, rarely fluctuating by more than 3% and never by more than 9%. 3 After nearly two decades of remarkable stability, carmakers had come to rely on high volumes of vehicle sales.

The decline was especially severe for the Detroit Three carmakers. Combined U.S. sales for Chrysler, Ford, and GM declined from 8.4 million in 2007 to 6.4 million in 2008 and 4.6 million in 2009, and their combined market share fell from 52% in 2007 to 48% and 44% in the next 2 years. The Detroit Three carmakers were vulnerable during the severe recession in part because their viability critically depended on selling large volumes of light trucks, a segment of the market that declined relatively rapidly during the recession.

Foreign carmakers had entered the U.S. market during the 1970s with fuel-efficient vehicles and began producing cars here in 1978. The Detroit Three reacted to the loss of much of their share of the passenger car market by focusing on light trucks. In 2007, the last year before the recession, the Detroit Three accounted for 65% of light truck sales but only 39% of car sales in the United States. Between 2007 and 2009, U.S. sales declined by 43% for light trucks and by 28% for cars. A sharp spike in gas prices during the first half of 2008 played a major role in the relatively rapid drop in light truck sales (Klier, 2009).

The long-standing lack of competitiveness of the Detroit Three carmakers, especially in labor costs (Klier, 2009; McAlinden, 2007, 2008), left them in a poor position to survive in the harsh environment of the 2008-2009 recession (Nardelli, 2008; Zandi, 2008). As the condition of the Detroit Three became dire in 2008, a number of analysts concluded that the national economy would be adversely affected should one or more of the Detroit Three were to go out of business (see, e.g., Cole, McAlinden, Dziczek, & Monk, 2008; McAlinden, Dziczek, & Menk, 2008; Scott, 2008).

As the recession deepened, the financial condition of Chrysler and GM grew more perilous. “By the beginning of December 2008, GM and Chrysler could no longer secure the credit they needed to conduct their day-to-day operations,” according to Chrysler CEO Robert Nardelli (Congressional Oversight Panel, 2011a, p. 9). GM was set to post a near-record loss of $30 billion, holding a cash supply of only $14 billion. Privately held Chrysler, acquired by Cerberus Capital Management from DaimlerChrysler only a year before the recession in 2007, also had a dangerously low supply of cash to meet day-to-day obligations. Ford, although it had posted a record $14.6 billion loss in 2008, did not face the immediate cash shortage of the other two Detroit-based carmakers, because it had borrowed $23.5 billion in 2006, secured by virtually all of the company’s assets (Cooney et al., 2009, p. 6).

Bush Administration’s Short-Term Rescue

In the waning days of his administration, President George W. Bush provided Chrysler and GM with enough capital to keep them afloat for a few months (U.S. Government Accountability Office, 2009; White House, 2008). President Bush acted after the administration and the carmakers failed to secure the support of Congress.

The Detroit Three had turned first to Congress for financial assistance. Chrysler CEO Robert Nardelli, Ford CEO Alan Mulally, GM CEO Rick Wagoner, and United Auto Workers’ (UAW) President Ron Gettelfinger pleaded their case for emergency aid before the Senate Committee on Banking, Housing, and Urban Affairs on November 18, 2008, and before the House Committee on Financial Services the next day (Cooney et al., 2009, p. 3). The timing was especially awkward: A new Congress had been elected 2 weeks earlier but was not yet in office, so the men presented their testimony before committees of the outgoing lame-duck Congress.

The appeal was not sympathetically received on Capitol Hill, especially after news organizations reported that the three CEOs had flown from Detroit to Washington on three private jets. The reaction of Rep. Gary Ackerman (D-NY) was typical: “There is a delicious irony in seeing private luxury jets flying into Washington, D.C., and people coming off of them with tin cups in their hand, saying that they’re going to be trimming down and streamlining their businesses” (Levs, 2008).

The following month, on December 4 and 5, 2008, the three CEOs returned to Washington, appearing before the same two congressional committees, this time with an even more urgent message: that aid was required immediately. Ford’s CEO accompanied his colleagues from GM and Chrysler, even though Ford did not request a government loan. Ford’s leadership recognized that a default by one of the other Detroit carmakers could adversely affect all carmakers, because they shared parts suppliers, which were at risk.

On December 10, 2008, legislation authorizing loans to the carmakers was introduced in the House and passed by a 237–170 vote (Cooney et al., 2009). Supporters included 205 Democrats and 32 Republicans; opponents included 20 Democrats and 150 Republicans (Nunnari 2011). At the suggestion of the Bush administration, the legislation facilitated the use of a direct loan program that had previously been authorized by the Energy Independence and Security Act of 2008, and was already appropriated to the U.S. Department of Energy to support alternative fuel and low emissions technologies.

In the Senate, a move on December 11 to close debate for the purpose of achieving a final vote on the House-passed bill failed, having garnered an insufficient majority of 52–35, well short of the 60 votes needed. Supporters included 41 Democrats, 9 Republicans, and 2 Independents; opponents included 4 Democrats and 31 Republicans (Nunnari, 2011). After considering other funding mechanisms, the Senate abandoned further action on the issue, and the bill died (Cooney et al., 2009). Congress kept watch over the subsequent restructuring initiatives by the executive branch, primarily through reviews by a bipartisan Congressional Oversight Panel 4 (see, e.g., Congressional Oversight Panel, 2009), testimony at committee hearings (see, e.g., Troubled Asset Relief Program [TARP], 2009), and reports by the Congressional Research Service (see, e.g., Cooney et al., 2009).

Faced with the imminent collapse of Chrysler and GM 1 month before he was to leave office, and with the lame-duck Senate unwilling to support rescue measures, President Bush issued an executive order on December 19, 2008 providing emergency aid to the two desperate carmakers. President Bush stated that

government has a responsibility not to undermine the private enterprise system . . . [but if] we were to allow the free market to take its course now, it would almost certainly lead to disorderly bankruptcy and liquidation for the automakers. (Cooney et al., 2009, p. 8)

The executive order directed the U.S. Department of the Treasury to provide support to Chrysler and GM through the Emergency Economic Stabilization Act, enacted by Congress in October 2008. The EESA had established the TARP, which authorized the secretary of the Treasury to purchase troubled assets from financial firms. Guiding principles for the Treasury’s management of TARP were as follows:

To protect taxpayer investments and maximize overall investment returns within competing constraints

To promote stability for and prevent disruption of financial markets and the economy

To bolster market confidence and thus increase private capital investment, and

To dispose of investments as soon as practicable, in a timely and orderly manner that minimizes any negative impact on the financial markets and the economy. (U.S. Department of the Treasury, 2010, p. 10, as cited in Webel & Canis, 2011, p. 3)

Though the EESA did not authorize support for manufacturing firms, the White House argued that using TARP money was appropriate:

The direct costs of American automakers failing and laying off their workers in the near term would result in a more than one percent reduction in real GDP growth and about 1.1 million workers losing their jobs, including workers for automotive suppliers and dealers. (White House, 2008)

To provide funds to carmakers, the Treasury Department established the Automotive Industry Financing Program under TARP on December 19, 2008.

The term sheets accompanying the loans to Chrysler and GM imposed a number of conditions on executives, unions, investors, dealers, and suppliers. They were derived from the legislation passed by the House (Cooney et al., 2009, pp. 41-43): “The overriding condition is that each firm must become ‘financially viable’; that is, it must have a ‘positive net value, taking into account all current and future costs, and can fully repay the government loan’” (Cooney et al., 2009, p. 9; White House, 2008). The two carmakers were required to demonstrate financial viability through submission of restructuring plans by February 17, 2009.

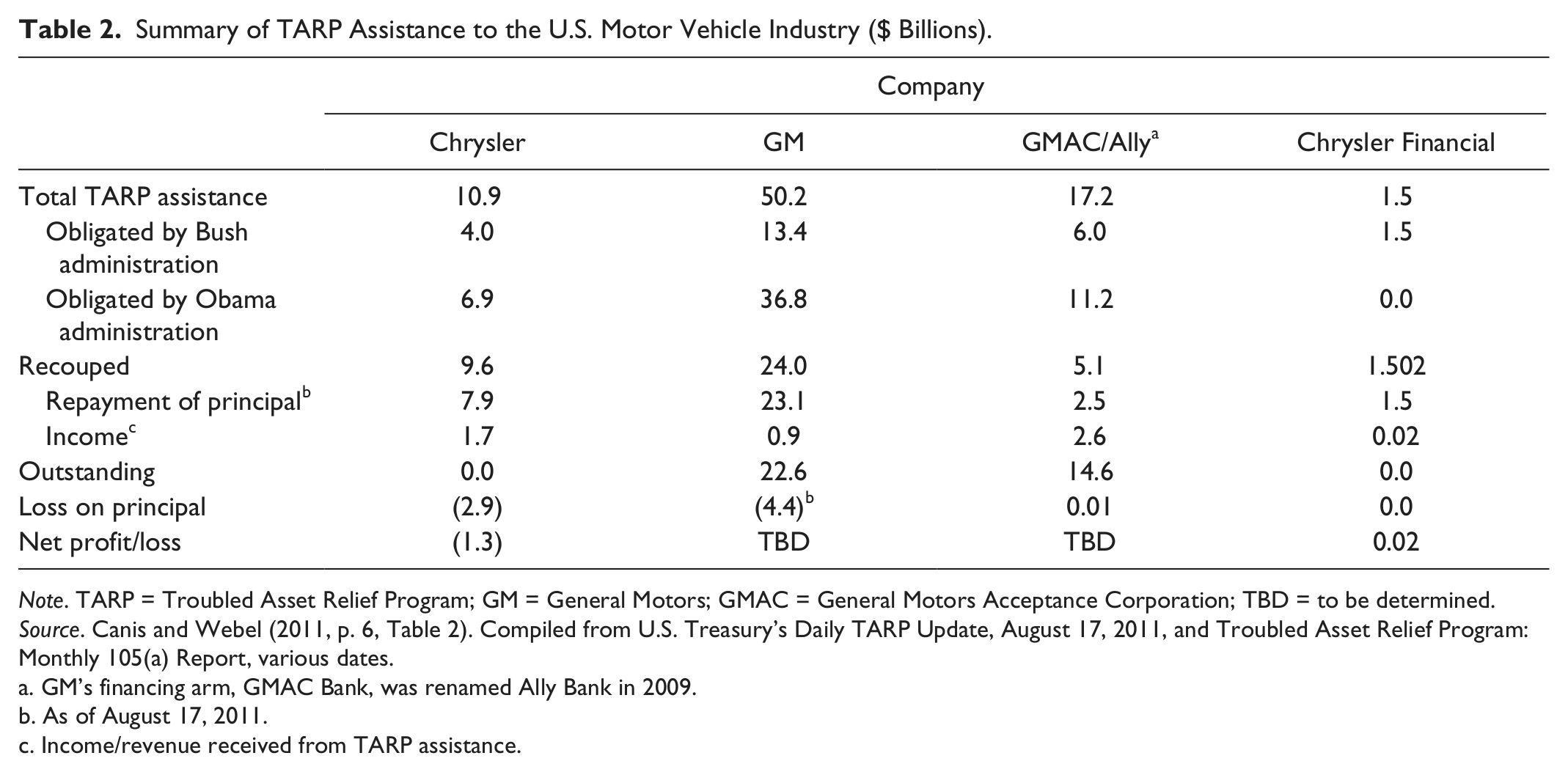

Through the Bush administration’s TARP commitments, Chrysler and GM each received $4 billion on December 29, 2008. The initial TARP loans made it possible for Chrysler and GM to stay afloat during the transition from the Bush administration to the Obama administration (Cooney et al., 2009). Including the Obama administration’s assistance, GM ultimately received $50.2 billion through TARP, Chrysler $10.9 billion, General Motors Acceptance Corporation (GM’s credit affiliate, now known as Ally Financial) $17.2 billion, and Chrysler Financial $1.5 billion.

In addition to U.S. support, GM received $10.6 billion and Chrysler $3.8 billion from Canada. The funding was shared, two thirds by the federal government and one third by the province of Ontario (Shiell & Somerville, 2012). It was provided to keep the industry viable and maintain Canada’s share of vehicle production going forward (Industry Canada, 2009). In January 2009, the Mexican government established the Programme for the Preservation of Employment. It committed 2 billion pesos ($147 million) to subsidize workers in the automotive, electronic, electrical, and capital goods industries for reduced working hours (Messenger & Rodríguez, 2010; Pope, 2010). It also introduced a limited vehicle scrappage program, at a cost of 500 million pesos. In 2010, the Mexican government added two additional measures: a phaseout of the vehicle ownership tax and a program that offered 2.5 billion pesos in loan guarantees to auto-financing institutions and banks (Economist Intelligence Unit, 2010).

Obama Administration’s Task Force

To devise a strategy for dealing with Chrysler and GM, President Barack Obama appointed a Presidential Task Force on the Auto Industry on February 16, 2009. The task force was cochaired by Treasury Secretary Timothy Geithner and National Economic Council Director Larry Summers. A 14-person staff was headed by Steven Rattner, cofounder of the hedge fund Quadrangle Group. Replacing Rattner later in 2009 was another adviser to the task force, former investment banker and United Steelworkers union negotiator Ron Bloom, who at that time was also named senior adviser for manufacturing policy. Task force leaders have explained their policy decisions through books, interviews, and speeches (Auto Industry Financing Program, 2009, Lassa, 2010; Ramifications of auto industry bankruptcies, 2009; Rattner, 2010a, 2010b).

The composition of the task force was notable for not including individuals with close ties to the auto industry. Instead, membership was drawn primarily from financial investors and legal experts with experience in restructuring troubled companies. The task force adopted metrics for evaluation and processes for decision making from other industries, rather than relying on those long in use in Detroit Three accounting offices.

The first program established by the task force propped up the parts suppliers. Typically, suppliers are paid by the carmakers 45 to 60 days after parts are shipped. Under normal market conditions, suppliers raise capital by borrowing against receivables (the carmakers’ commitments to pay for the parts). However, in the depth of the recession, banks were not providing credit to suppliers against receivables, given the uncertain future of Chrysler and GM (Congressional Oversight Panel, 2011a). The Auto Supplier Support Program, announced on March 19, 2009, was designed to ensure that Chrysler and GM suppliers would have access to capital during a period of uncertainty and tight credit. The Treasury committed $3.5 billion to a company called GM Supplier Receivables LLC, and $1.5 billion to a second company called Chrysler Receivables SPV LLC. Ultimately, only $290 million was loaned to GM suppliers and $123 million to Chrysler suppliers, and the program was terminated in April 2010 (Congressional Oversight Panel, 2011a).

Regarding the future of Chrysler and GM, the task force considered three policy options, according to Bloom:

No further government assistance beyond the already committed TARP loans,

Additional loans with no strings attached, and

Additional financial resources tied to restructuring. (Lassa, 2010)

Had Option 1 been selected, Chrysler and GM “would have unquestionably run out of cash quickly, slid into [Chapter 7] bankruptcy, closed their doors and liquidated” (Rattner, 2010a, p. 2). The task force rejected Option 1 for GM: “We soon could not imagine this country without an automaker of the scale and scope of General Motors. The task became not whether to save GM, but how to save GM” (Rattner, 2010a, p. 3). “The consequences of allowing General Motors to go into an uncontrolled Chapter 7 liquidation would’ve been devastating,” Bloom said. He repeated the word for emphasis: “The ‘D’ word I’d use would be ‘devastating’” (Lassa, 2010).

Chrysler was another matter. “From a highly theoretical point of view, the correct decision could be to let Chrysler go,” said Rattner (2010a, p. 4). If Chrysler were liquidated, buyers of its most attractive vehicles—jeeps, minivans, and trucks—were likely to turn to Ford and GM: “Thus, the substitution effect [of Chrysler customers switching to Ford and GM products] would eventually reduce the net job losses substantially. . . . We intuited that the substitution analysis was more right than wrong . . .,” Rattner added (pp. 3-4). Rattner considered the probability of successfully restructuring Chrysler at less than 50-50.

The task force was evenly divided on whether to rescue or liquidate Chrysler, so President Obama had to cast the deciding vote, and he chose to continue a government-managed restructuring. Continuing support for Chrysler was necessary because liquidation would have increased the already unacceptably high unemployment rate (Rattner, 2010a). Estimates of job losses varied considerably. The Council of Economic Advisers expected losses of more than 1% in real GDP growth and about 1.1 million jobs, including parts production and dealers (White House, 2008). Moody’s Analytics chief economist Mark Zandi estimated the total job losses to come to 2.5 million (Zandi, 2008), the Center for Automotive Research expected 2.5 to 3 million (Cole et al., 2008; McAlinden et al., 2008), and the Economic Policy Institute placed the figure at 3.3 million (Scott, 2008).

Option 2 was also rejected. Bloom argued that “the costs of that would have been in the many multiples of what we spent.” That left Option 3 as the task force’s ultimate choice for both Chrysler and GM (Lassa, 2010).

As a condition for receiving TARP loans in December 2008, Chrysler and GM had been required to submit restructuring plans to the Treasury Department by February 17, 2009, to qualify for further federal assistance. The task force took on the responsibility of reviewing the plans. On March 30, President Obama announced the result of the task force’s review: Neither GM’s nor Chrysler’s plan had established a credible path to viability.

The task force concluded that Chrysler’s viability plan to close plants and dealerships, reduce labor costs, and change operations did not go far enough. Chrysler was offered working capital through TARP for 30 more days to devise a more thorough restructuring plan that had the support of major stakeholders, including labor unions, dealers, creditors, suppliers, and bondholders (Webel & Canis, 2011).

GM’s plan was judged not viable primarily because of “overly optimistic assumptions about prospects for the macroeconomy and GM’s ability to generate sales” (Congressional Oversight Panel, 2011b, p. 97; White House, 2009). The task force decided that GM could survive only after a change of leadership (Rattner, 2010a). The task force replaced GM CEO Rick Wagoner on March 30. At the time it was announced that GM’s board would be overhauled: Six of the existing board members would resign by the time the new GM emerged from bankruptcy. GM was provided 60 days of working capital to submit a substantially more aggressive plan (Congressional Oversight Panel, 2011b; White House, 2009).

To assuage consumers’ concerns about buying Chrysler and GM vehicles during the period of uncertainty, the Treasury also announced on March 30 that it would honor warranties on all new Chrysler and GM vehicles purchased during the restructuring period (Congressional Oversight Panel, 2009). Nevertheless, though Chrysler and GM were both given time to submit acceptable viability plans, the task force’s assessment, as announced by President Obama on March 30, 2009, set the two companies on a course that led to the first bankruptcy filings by U.S. carmakers since Studebaker in 1933.

Restructuring Through Bankruptcy 5

“Bankruptcy is not our goal,” Rattner insisted in public statements, speaking for the task force. “It is never a good outcome for any company, and it’s never a first choice” (Rattner, 2010a, p. 101). Bankruptcy would be “scary,” according to Rattner (2010a, p. 2), because customers might be unwilling to buy from bankrupt carmakers, especially if the proceedings dragged on for a long time. “Yet all the while,” he revealed a year later, “we were preparing for it” (Rattner, 2010a, p. 101).

Bankruptcy, asserted the Detroit Three CEOs in November 2009, “would shatter consumer confidence and cost the government more than $25 billion in lost taxes, while triggering a domino effect throughout the auto industry.” In their failed appeal to Congress in November 2009, the Detroit Three CEOs had warned of “grave damage to the entire U.S. economy should one or more of them be thrown into bankruptcy.” UAW President Ron Gettelfinger agreed: “If any of these [Detroit Three] companies would go into bankruptcy, I would bet it would take another one with them or possibly all three” (Hyde & Spangler, 2008).

Bankruptcy made sense to some: “We’ve gone [from 17 million] to 10 million sales a year in this country. We may not need three automakers,” argued Sen. Bob Corker (R-TN), after leading an effort that failed in the Senate in December 2008 to require substantial restructuring of the Detroit Three as a condition of support (Hyde & Spangler, 2008).

Even “the industry’s closest observers did not know what had, for all practical purposes, already been decided” in March, namely restructuring through bankruptcy (Rattner, 2010a, p. 126). The task force had in fact concluded, and President Obama had accepted, that the best chance of success for Chrysler and GM lay in bankruptcy, although “in a quick and surgical way” (White House, 2009). Restructuring “would not entail liquidation or a traditional, long, drawn-out bankruptcy, but rather a structured bankruptcy as a tool to make it easier for Chrysler [and GM] to clear away old liabilities” (Congressional Oversight Panel, 2009, p. 13; White House, 2009).

To accomplish “a quick and surgical” bankruptcy, the task force resorted to a rarely used section of the U.S. Bankruptcy Code known as Section 363(b) of Chapter 11 (Fishman & Gouveia, 2010), writes Rattner:

Section 363 allows a bankrupt company to act quickly to transfer intact, valuable business units to a new owner. (The conventional bankruptcy process restructures the corporation as a whole.) Once exotic and obscure, 363 had provided the only bright spot in the cataclysmic implosion of Lehman Brothers. It was used to salvage Lehman’s money-management and Asian businesses. . . . [However,] 363 had never been applied to industrial companies on the scale of Chrysler and GM . . . (Rattner, 2010a, p. 60)

Through Section 363, the viable assets—properties, contracts, personnel, and other assets necessary to move forward as a viable operation—were allocated to a “new” carmaker. The “old” carmaker kept the “toxic” assets destined for liquidation or write-off, as permitted under bankruptcy laws.

Chrysler filed for bankruptcy on April 30, 2009, and was cleared to sell all viable assets to the “new” Chrysler May 31, 2009. GM filed for bankruptcy on June 1, 2009, and a “new” GM emerged from protection on July 10, 2009. These remarkably quick trips through bankruptcy contrast with the more typical experience of the then-largest parts supplier in the United States—Delphi Automotive, which filed for Chapter 11 bankruptcy protection on October 8, 2005, and did not emerge until 4 years later, on October 6, 2009.

Given 30 days to create a viable restructuring plan outside bankruptcy, Chrysler worked with its stakeholders during April 2009 and reached tentative agreements with most of them. The larger banks agreed to write down their debt by more than two thirds. However, some mutual funds and hedge funds holding about 30% of the debt did not agree. Chrysler could avoid bankruptcy only if all its creditors approved the settlement (Webel & Canis, 2011), so the lack of unanimity prompted the filing in bankruptcy court and permitted the task force to cite “greedy” stakeholders as the reason for the bankruptcy filing.

Three Indiana state pension plan bondholders appealed bankruptcy Judge Arthur J. Gonzalez’s approval of Chrysler’s restructuring plan to the U.S. Court of Appeals for the Second Circuit, located in New York. Holders of 92% of Chrysler’s secured debt had agreed to an exchange of debt at a value of 29 cents on the dollar. The Indiana funds argued that they should have been repaid at 43 cents on the dollar, because that was the value at which they had obtained their bonds a year before the bankruptcy filing. However, the court of appeals affirmed the bankruptcy judge’s ruling on June 5, 2009, and 4 days later the U.S. Supreme Court allowed the sale of Chrysler to proceed, ending the legal proceedings. The government provided the “new” Chrysler with a final TARP installment of $4.6 billion in working capital and exit financing to assist in the transformation to a new, smaller automaker (Webel & Canis, 2011, p. 7).

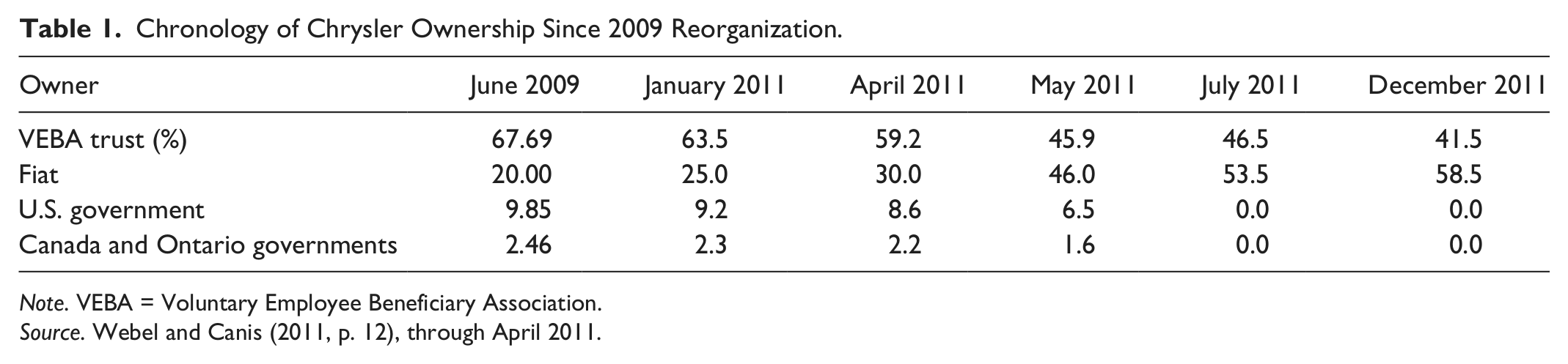

The task force had concluded that Chrysler was not viable outside a partnership with another automotive company. That partner turned out to be the Italian carmaker Fiat. Fiat initially held 20% of new Chrysler equity, without making a direct financial contribution (Table 1). The justification was that Fiat would manage Chrysler and develop competitive products, especially small, fuel-efficient vehicles (Webel & Canis, 2011).

Chronology of Chrysler Ownership Since 2009 Reorganization.

Note. VEBA = Voluntary Employee Beneficiary Association.

The bankruptcy court decision set three performance benchmarks that would enable Fiat to raise its equity stake in Chrysler (Klier & Rubenstein, 2012):

A technology event: Fiat could increase its stake in Chrysler by 5% by manufacturing in the United States a fuel-efficient engine based on a Fiat design. Fiat met this benchmark in January 2011 by starting to make its MultiAir engine at a Chrysler plant in Dundee, Michigan.

A distribution event: Fiat could increase its stake by a further 5% by exporting vehicles from North America. Fiat met this benchmark in April 2011 when it exported $1.5 billion worth of Chrysler vehicles, primarily jeeps to Europe and Latin America.

An ecological event: Fiat could increase its stake by yet another 5% by assembling a vehicle in the United States that achieved at least 40 miles-per-gallon (mpg) fuel efficiency. Fiat met this benchmark in December 2011 when it committed to build the Fiat-based Dodge Dart at Chrysler’s Belvidere, Illinois, assembly plant (Webel & Canis, 2011).

Initially, the largest equity owner in “new” Chrysler, with 67.69%, was the United Auto Workers’ Voluntary Employee Beneficiary Association (UAW VEBA) health care retirement trust. “Fiat’s share could rise to more than 70 percent if it exercises the rights it holds to purchase some of the UAW VEBA Trust stake,” Webel and Canis (2011, p. 8) write, “Fiat purchased these rights from the U.S. Treasury for $60 million.”

The UAW VEBA trust was allocated a substantial interest in “new” Chrysler because “old” Chrysler owed the trust $8 billion. Converting the liability to an ownership stake closely intertwined the solvency of the hourly workforce’s generous retirement benefits with Chrysler’s survival. The UAW VEBA also received a $4.6 billion unsecured note from “new” Chrysler (Webel & Canis, 2011, p. 7).

The “new” GM that emerged from bankruptcy proceedings placed majority ownership with the U.S. government through conversion of “old” GM’s TARP loans into an ownership stake of 60.8%. 6 In addition, the government of Canada held 7.8%, the government of Ontario 3.9%, the UAW VEBA 17.5%, and unsecured bondholders and creditors of the “old” GM 10% (Canis & Webel, 2011, p. 9; Shiell & Somerville, 2012, p. 12). If the “new” GM proved viable, the governments intended to sell their stakes to the public. In fact, an initial public offering (IPO) was launched on November 18, 2010, and the result exceeded expectations. The government sold $23.1 billion worth of shares, the largest IPO in U.S. history. Because of strong investor demand, more shares than anticipated were sold, and they were sold for $33 per share, higher than the anticipated $25-$26. After the IPO, the U.S. government’s stake dropped to around 32%. 7

Once the task force had successfully guided Chrysler and GM into and out of bankruptcy, it was disbanded. Assuming some of the task force’s oversight functions was the White House Council for Automotive Communities, created by executive order on June 23, 2009. The council was transferred to the Department of Labor and renamed the Office of Recovery for Auto Communities and Workers in August 2010. The principal function of the Auto Communities Office has been to identify appropriate sources of federal funds for assistance to communities negatively affected by the auto industry restructuring, especially in the Great Lakes states. Examples include funds to clean up sites of closed plants from the U.S. Departments of the Treasury and Justice and the Environmental Protection Agency, as well as a $2.4 billion initiative from the U.S. Department of Energy to accelerate the manufacture and deployment of the next generation of batteries and electric vehicles (see, Klier & Rubenstein, 2011).

After completing the reorganization of Chrysler and GM, the principal government initiative to revive the auto industry was the Car Allowance Rebate System during the summer of 2009. The program, more commonly known as Cash for Clunkers, provided any interested consumer with a credit of $3,500 to $4,500 toward the purchase of a new vehicle, provided an older vehicle was traded in. To qualify, the scrapped vehicle had to be currently registered, less than 25 years old, and rated by the EPA at 18 mpg or less.

The initial plan was for the program to disperse $1 billion over 3 months, but when demand proved much higher than expected, Congress appropriated an additional $2 billion and ended the program after 1 month. Cash for Clunkers provided a sales spike of roughly one-half million vehicles during the summer of 2009 (Li, Linn, & Spiller, 2011; Mian & Sufi, 2010). In addition, the Department of Energy offered low-interest loans to improve energy efficiency in the motor vehicle industry through a $25 billion facility that was approved as part of the 2007 energy bill. It also provided funding designated for the electrification of the transportation sector under the American Recovery and Reinvestment Act of 2009 (see Klier & Rubenstein, 2011).

Thus, only a year of failing to convince Congress to rescue them, Chrysler and GM had both entered government-managed bankruptcy protection and exited with new management and fresh infusions of capital. The next sections of this article evaluate the most important changes to occur in the North American auto industry as a result of the restructuring.

Impact of Restructuring on Competitiveness of U.S. Carmakers

The second half of this article discusses the two most significant changes in the North American auto industry resulting from the government-managed reorganization of Chrysler and GM: changes in the competitive position of the Detroit Three (discussed in this section of the article) as well as the spatial distribution of production within North America (discussed in the next section).

A fundamental goal of the restructuring was to place the Detroit Three carmakers in position to achieve profitability in a highly competitive market. This section focuses on two key strategies—used in addition to the debt reduction—by which the government-managed restructuring improved the competitiveness of the Detroit Three:

Reduce labor costs

Reduce production capacity

Reduced Labor Costs

GM’s North American bill for hourly labor declined from $16 billion in 2005 to $5 billion in 2010 (Congressional Oversight Panel, 2011a). Three strategies resulted in lower labor costs:

Employ Fewer Workers

Employment at the Detroit Three carmakers declined during the restructuring period, from 250,639 in 2007 to 169,966 in 2009. Detroit Three employment had been declining for a long time before bankruptcy, from just more than 600,000 in 1990 to just less than 300,000 in 2006. The decline was more rapid during the restructuring period—15% per year, compared with 5% per year during the previous 15 years. A significant part of the Detroit Three employment decline earlier in the decade had resulted from Ford and GM turning their parts-making divisions into the independent companies of Visteon and Delphi, respectively, as well as several employee buyout programs (McAlinden, Dziczek, & Schwartz, 2011).

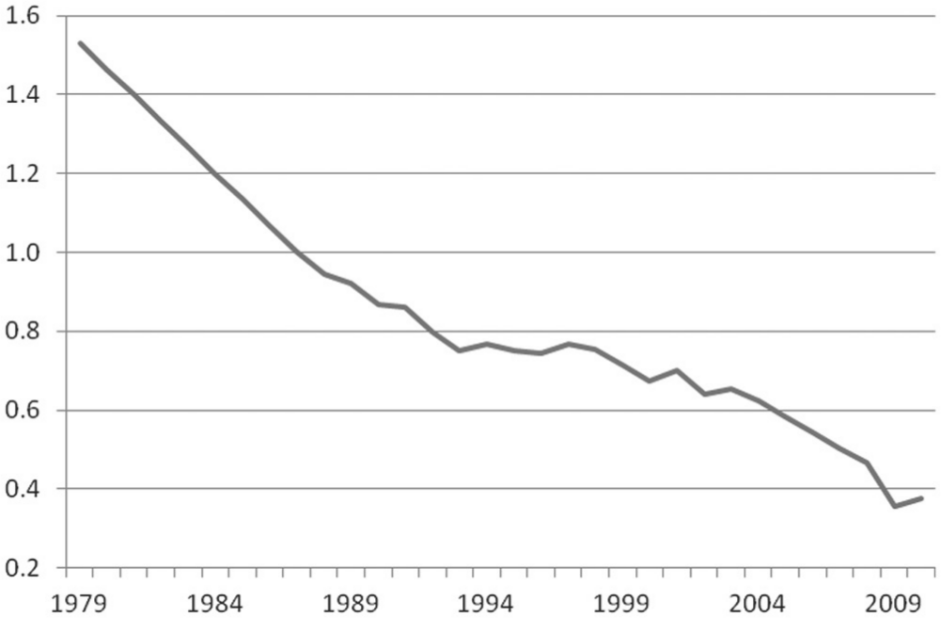

Cuts at the Detroit Three were more severe for hourly workers than for salaried workers during restructuring. Between 2007 and 2009, the Detroit Three hourly workforce declined by 34%, from 175,000 to 115,000, whereas the salaried workforce declined by 27%, from 75,000 to 55,000. The relatively sharp decline in the hourly workforce is reflected in declining union membership (Figure 1). The actively working UAW membership dropped by 30%, from 500,000 in 2007 to 350,000 in 2009 (McAlinden et al., 2011).

United Auto Workers’ actively working membership (in millions).

Reduce the Wage Premium

Another significant change was a reduction of the wage premium paid to the Detroit Three hourly workforce. The Detroit Three workforce was paid more than that of other U.S. manufacturers. Between 1960 and 2005, hourly wages at the Detroit Three rose from $2.63 to $27.42 in nominal terms, compared with an increase among the entire U.S. manufacturing workforce from $2.26 to $16.56. By 2005, Detroit Three hourly wages were 66% higher than the average for all manufacturing workers (McAlinden, 2007).

The gap between Detroit Three workers and others was even higher when benefits were included. Total labor costs including health care and pensions for the Detroit Three increased (in nominal dollars) from around $15 per hour in 1977 to $25 in 1987, $45 in 1997, and $78 in 2007 (McAlinden et al., 2011).

The 2007 labor contracts between the UAW and the Detroit Three made great strides in reducing the average hourly labor costs from $72-$78 per hour to $50-$58 per hour. Key elements were the transfer of retiree health care liabilities from the carmakers to the VEBA, and the introduction of a much lower Tier 2 wage rate for new hires. As a result, by 2011, average hourly labor costs for Ford ($58), GM ($56), and Chrysler ($52) 8 were much more competitive with those of foreign producers operating in the United States, such as Toyota ($55) and Honda ($50). The 2011 labor contracts continued to hold the line on fixed labor costs while increasing variable pay. Labor costs for the Detroit Three were expected to grow by less than 1% annually through 2015 (McAlinden et al., 2011). 9

Transfer the Health care Costs of Retired U.S. Union Workers

The largest component of closing the labor cost gap between the Detroit Three and international carmakers came from changes in the provision of retiree health care benefits. Health care costs for retired Detroit Three employees had skyrocketed in the decade before bankruptcy. By 2006, retiree health care costs added $950 to the cost of each vehicle assembled by GM and $635 to each vehicle assembled by Ford (McAlinden, 2008).

The Detroit Three had reached agreement with the UAW in 2007 to transfer the financial responsibility for retired U.S. hourly workers’ health care to the union’s VEBA. The Detroit Three had then agreed to fund VEBA with cash. 10 During the restructuring, a large portion of the cash claims were turned into equity stakes in Chrysler and GM, as the companies lacked the financial resources to provide cash. 11

Higher Capacity Utilization

Capacity utilization is a key driver of profitability for carmakers. Auto assembly is a capital-intensive undertaking. An assembly plant costs hundreds of millions of dollars to build, employs several thousand when operated at capacity, and produces more than 200,000 units per year under standard operating conditions. If an assembly plant is run below capacity, a carmaker still incurs significant fixed costs (Klier & Rubenstein, 2012).

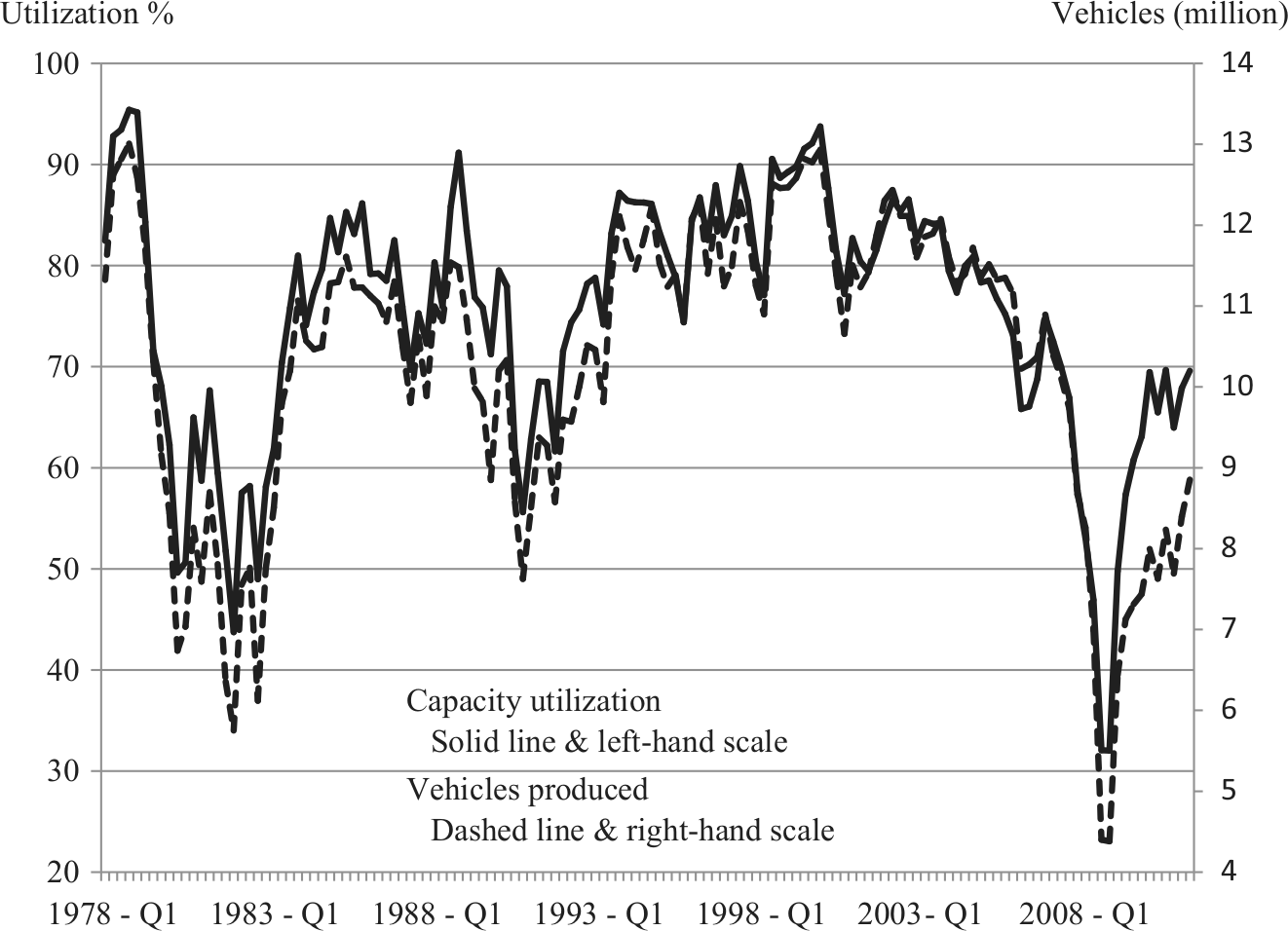

In January 2009, at the depth of the 2008-2009 recession, capacity utilization in the production of light vehicles in the United States hit a record-low 25.9%. By comparison, capacity utilization averaged 77.6% between 1972 and 2007 (Figure 2). During peak sales years, capacity utilization reached approximately 90%, and during recessions it averaged approximately 50%. Historically, changes in capacity utilization were closely associated with changes in production. As production decreased, so did capacity utilization. This relationship continued through the severe recession of 2008-2009.

U.S. assembly plant capacity utilization and vehicle production, 1978-2011.

Capacity utilization in the U.S. auto industry during 2010 and 2011, the first 2 years after restructuring, was approximately 70%, much higher than in the past at similar output levels. For example, in 2010, U.S. production was about 8 million vehicles and U.S. assembly plants were used at a rate of about 70% of capacity. On the previous occasions that U.S. production sank to the level of 8 million vehicles—during the recessions of the 1980s and the early 1990s—capacity utilization one year out was noticeably lower, at approximately 60%.

This is a reflection of the large number of plants that the Detroit Three closed during the bankruptcy proceedings. Between the end of 2007 and the start of 2010, the Detroit Three closed or announced for closure 16 assembly plants, including 14 in the United States and one each in Canada and Mexico. By comparison, only six assembly plants were closed between 1979 and 1983, around the time of the recession of the early 1980s.

The result of this sharp and rapid reduction in capacity has been a decoupling of the traditional relationship between the level of capacity utilization and the level of production, as approximately 2.6 million units have been removed from production capacity in the United States. That enabled carmakers to become profitable at relatively low output levels.

Impact of Restructuring on the Geography of Auto Production

The restructuring of the Detroit Three carmakers during the recent severe recession has altered the distribution of assembly plants within North America. We find three distinct aspects to the changing geography of North American automotive production:

The clustering of production along “Auto Alley,” with a northward extension into southwestern Ontario

The clustering of production that occurs outside Auto Alley in Mexico, instead of in the United States

The separation of Auto Alley into distinct northern and southern segments

The geography of North American production had been changing since the 1980s, but the severe recession accelerated the changes.

Clustering in Auto Alley

The U.S. motor vehicle industry is highly concentrated in a region known as Auto Alley (Figure 3). Auto Alley is a narrow corridor, roughly 700 miles long and often less than 100 miles wide, in the interior of the United States, stretching between the Great Lakes and the Gulf of Mexico. Two parallel north–south interstate highways, I-65 and I-75, form the backbone of Auto Alley. Several east–west highways, including I-40, I-64, and I-70, connect the two north–south routes like rungs on a ladder. A Canadian extension of Auto Alley follows Highway 401 in southwestern Ontario between Windsor and Toronto.

Auto Alley, 2010.

Motor vehicle production involves two types of activities: the assembly of the finished vehicle and the production of parts. The roughly 15,000 parts that go into vehicles are produced at several thousand parts plants. In 2010, light vehicles were assembled at 42 final assembly plants in the United States owned by 13 carmakers. In 2010, Auto Alley was home to 34 of the 42 assembly plants. During the recession and restructuring period, 12 assembly plants were closed in the United States, including 4 in Auto Alley and 8 elsewhere.

Auto Alley began to form in the 1980s, well before the 2008-2009 recession. Prior to the 1980s, branch assembly plants were distributed around the country near major population centers (see Rubenstein, 1992). The rationale for branch assembly plants near major population centers unraveled once product variety grew much faster than the size of the overall vehicle market. Auto Alley developed during the 1980s through the construction of assembly plants in new locations, primarily by foreign-owned carmakers (see Klier & McMillen, 2006, 2008; Klier & Rubenstein, 2008, 2010). Honda was the first Japanese-owned carmaker to establish an assembly plant in the United States, in Marysville, Ohio, in 1982. During the next 7 years, another six Japanese-owned assembly plants opened in the United States and three in Canada; all six U.S. plants were located in Auto Alley. A second wave of construction began in 1995 and continued through the first decade of the 21st century. Between 1995 and 2008, carmakers opened or announced their intention to build 10 final assembly plants in the United States and three in Ontario. Foreign-owned carmakers were responsible for all 14, and 9 of the 10 U.S. plants were located in Auto Alley.

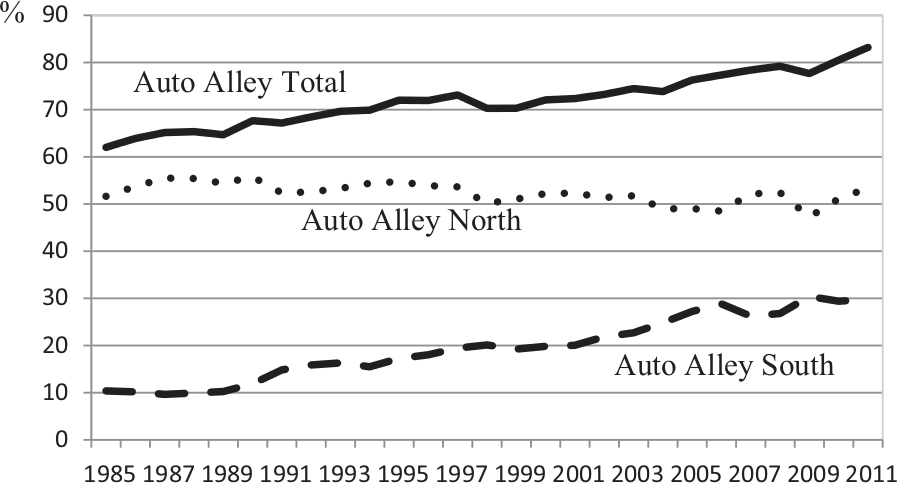

In 1980, the United States had 32 assembly plants in Auto Alley and 25 elsewhere. The impact of the recession was to accelerate the clustering of nearly all U.S. auto production in Auto Alley. Thus, Auto Alley’s share of U.S. assembly, which had increased from 62% in 1985 to 78% in 2007, increased at a more rapid rate, to 83% in 2010 (Figure 4).

Auto Alley share of U.S. light vehicle production.

Canada and Mexico

Within North America, the assembly plant closures during the 2008-2009 recession were focused almost exclusively on the United States. The number of assembly plants in Canada remained unchanged between 2007 and 2010, at 11; one plant was opened and one was closed. The number in Mexico remained at 10. Meanwhile, the number in the United States declined from 52 to 42.

The increasing importance of Canada and especially Mexico in North American vehicle assembly is also reflected in production figures. Between 2007 and 2010, production increased in Mexican assembly plants from 2.1 million to 2.3 million, whereas production during the 3-year period declined in U.S. assembly plants from 10.8 million to 7.8 million and in Canadian assembly plants from 2.6 million to 2.1 million. As a result, between 2007 and 2010 the share of North American vehicle production increased in Mexico from 13.5% to 18.9% and decreased in the United States from 69.7% to 63.7%; Canada’s share increased from 16.8% to 17.2% during the period.

North–South Split

Restructuring also accelerated a spatial division within the United States in Auto Alley, with the northern half dominated by the Detroit Three carmakers and the southern half dominated by international carmakers (Figure 5). U.S. Highway 30, which runs east–west through northern Ohio, Indiana, and Illinois, serves as the dividing line between the northern and southern portions of Auto Alley. In 2011, the Detroit Three operated 17 of their 18 U.S. assembly plants north of U.S. 30, and the international carmakers operated 16 of their 18 plants south of U.S. 30. In 2007, the Detroit Three had 21 northern plants and 7 southern ones, whereas the international carmakers had 1 northern one and 11 southern ones.

Auto Alley subregions.

Thus, in 4 years the Detroit Three withdrew nearly all their production from the southern portion of Auto Alley. The two surviving southern assembly plants were both operated by Ford in Louisville, Kentucky, relatively close to the north–south divider. 12 Meanwhile, the only assembly plant north of U.S. 30 that assembled international brands, at Flat Rock, Michigan, was slated to end production for Mazda in 2012, and the plant was to be transferred back to Ford.

Labor considerations helped form the north–south division within Auto Alley. Spreading out within Auto Alley would reduce competition among assembly plants for a relatively skilled high-wage workforce. The Deep South was also attractive to foreign-owned carmakers in part because of the prevalence of right-to-work laws, which prohibit making membership in a union a condition or requirement of employment. To work at a Detroit Three plant, union membership is required; union dues are withheld from employee pay and turned over directly to the union.

Research has shown that manufacturers are attracted to the 23 U.S. states with right-to-work laws (Burlett, 2006). For example, since the enactment of right-to-work laws beginning in 1947, 8 of the 10 states with the most rapid growth in manufacturing have been right-to-work states, and all 10 states with the lowest growth rates are not right-to-work states (Holmes, 1998). Of the 10 assembly plants opened or announced between 1997 and 2012, 8 were in right-to-work states. The two exceptions were located in Indiana, which enacted legislation in 2012 to become a right-to-work state.

The changing distribution of auto plants during the restructuring is significant for two reasons. First, the very high concentration of investment in Michigan and nearby areas in the northern portion of Auto Alley has helped the severely downsized Detroit Three to reduce production costs. The concentration of Detroit Three assembly plants in the northern portion of Auto Alley reduces transportation costs for both receiving parts from suppliers and shipping assembled vehicles to consumers.

Second, as a result of a more concentrated footprint, the Detroit Three operate major manufacturing facilities in a noticeably smaller number of states. The number of states with a Detroit Three assembly plant declined from 19 in 1980 to 8 in 2011. Between 1980 and 2011, the Detroit Three closed assembly plants in California, Delaware, Georgia, Louisiana, Maryland, Minnesota, New Jersey, New York, Tennessee, Virginia, and Wisconsin, leaving them with plants only in Illinois, Indiana, Kansas, Kentucky, Michigan, Missouri, Ohio, and Texas. The sharply reduced footprint may have also contributed to widespread opposition for the rescue of the Detroit Three in Congress and in public opinion.

On the other hand, the 11 international carmakers that had set up plants in the United States by the end of 2011 opened their first U.S. assembly plants in nine different states: Alabama (Daimler-Benz and Hyundai), Georgia (Kia), Illinois (Mitsubishi), Indiana (Subaru), Kentucky (Toyota), Michigan (Mazda), Ohio (Honda), South Carolina (BMW), and Tennessee (Nissan and VW). This pattern reflected the escalating competition among states to attract new assembly plants through generous financial incentives. States typically offered three types of financial incentives: 13

Site improvements, such as land acquisition and construction of new roads and sewers

Recruitment and training of new employees

Tax relief, such as lower property taxes and foreign trade subzone status (Molot, 2005)

Altogether, the foreign-headquartered carmakers had assembly plants in 11 states in 2012 (Alabama, Georgia, Illinois, Indiana, Kentucky, Michigan, Mississippi, Ohio, South Carolina, Tennessee, and Texas), compared with only one in 1980 (Pennsylvania). The spread of international carmakers was also politically astute: Each time a new state received a foreign-owned assembly plant, the number of public officials sympathetic to the distinctive needs and priorities of international carmakers increased.

Summary

The government-managed reorganization of Chrysler and GM in mid-2009 spawned numerous evaluations. The White House has made it clear that it considers the restructuring of Chrysler and GM to be a success (see, e.g., Executive Office of the President, 2010; White House, 2009; White House Blog, 2010; White House Council on Automotive Communities and Workers, 2010). “There is no doubt that over the course of the past year they have moved back from the brink to a position of contributing to the economic recovery of the nation and auto communities,” the administration said (White House Council on Automotive Communities and Workers, 2010, p. 16). Task force head Rattner called the rescue “one of the clearest successes of tough presidential decision making” (Rattner, 2010a, p. 299).

Congressional evaluations have been mixed (Canis & Webel, 2011; Congressional Oversight Panel, 2009, 2011a, 2011b; Webel & Canis, 2011). The Congressional Oversight Panel finds that

GM and Chrysler are both more viable firms than they were in December 2008. . . . The industry’s improved efficiency has allowed automakers to become more flexible and better able to meet changing consumer demands, while still remaining profitable. (Congressional Oversight Panel, 2011a, pp. 7, 20)

On the other hand, the panel pointed out that the use of TARP money was “controversial,” because it was enacted to rescue financial firms, not manufacturing ones (Congressional Oversight Panel, 2011a, pp. 8, 107; Webel & Canis, 2011, p. 2). The Congressional Oversight Panel (2011a) also decried what it called the “moral hazard” of rescuing Chrysler and GM, because it “sent a powerful message to the marketplace—some institutions will be protected at all cost, while others must prosper or fail based upon their own business judgment and acumen” (p. 8).

From a narrow accounting perspective, the governments of the United States, Canada, and Ontario appear destined to lose money. In the case of Chrysler, the Congressional Research Service estimated that there was a $1.3 billion gap between the funds that were loaned to Chrysler and the funds that were eventually recouped (Table 2). Regarding GM, accounts were not finalized at the time of this writing, although a loss was likely. In May 2012, the government held approximately 500 million shares, or 32% of GM’s common equity. In order for the government’s 32% of the company to be worth $26.2 billion—representing all of the remaining unrecovered government investment—GM’s market capitalization would have to be approximately $81.9 billion. To achieve this market capitalization, the price of GM stock would have to exceed $52 per share, whereas the company’s actual share price remained throughout 2012 in a narrow range between 23 and 29.

Summary of TARP Assistance to the U.S. Motor Vehicle Industry ($ Billions).

Note. TARP = Troubled Asset Relief Program; GM = General Motors; GMAC = General Motors Acceptance Corporation; TBD = to be determined.

Source. Canis and Webel (2011, p. 6, Table 2). Compiled from U.S. Treasury’s Daily TARP Update, August 17, 2011, and Troubled Asset Relief Program: Monthly 105(a) Report, various dates.

GM’s financing arm, GMAC Bank, was renamed Ally Bank in 2009.

As of August 17, 2011.

Income/revenue received from TARP assistance.

On the other hand, in 2010, the first full year after restructuring, GM earned $2.89 per share. GM’s credit rating was upgraded to within a shade of investment grade. 14 In comparison, GM had lost money for four consecutive years before restructuring, including record losses of $68.45 per share in 2007 and $53.32 in 2008. The financial turnaround was especially significant because GM sold fewer vehicles in the United States in 2010 than it had in 2007, yet the company was profitable: “In sum, GM is now able to break even with a smaller share of a smaller market,” the congressional panel reports (Congressional Oversight Panel, 2011a, p. 41).

Regardless of the financial accounting, the government-managed restructuring altered the structure of the North American auto industry in two fundamental ways. First, the labor cost structure of the Detroit Three carmakers is no longer uncompetitive with that of their international competitors, thanks to the multitier union contract and the transfer of retiree pension and health care obligations to VEBA. Second, the restructuring substantially lowered the break-even point for the Detroit carmakers.

The first 2 years after restructuring brought cautious optimism concerning the prospects of the Detroit Three carmakers. Detroit Three sales increased from 4.68 million in 2009 to 6.02 million in 2011, whereas foreign-headquartered carmakers’ sales increased more modestly, from 5.75 in 2009 to 6.76 million in 2011. The market share of the Detroit Three increased for the first time in decades, from a historic low of 44.9% in 2009 and 45.4% in 2010 to 47.1% in 2011. All Detroit carmakers were profitable in 2011, operated with much reduced debt levels, and both GM’s and Ford’s credit ratings were rising again.

Ultimately the market share gain for the Detroit Three in 2011 may prove to be an anomaly attributable to severe disruptions in production faced by its Japanese competitors as a result of the March 2011 earthquake and tsunami in Japan and the October 2011 floods in Thailand, where Japanese carmakers have a large number of suppliers. Yet the improved performance of the Detroit Three in 2011 could also represent a genuine shift in momentum. It is too early to tell which of these competing explanations will hold.

Footnotes

Authors’ Note

The views expressed in this article are those of the authors and do not represent the official policy of the Federal Reserve Bank of Chicago.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.